South Korea Data Center Server Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

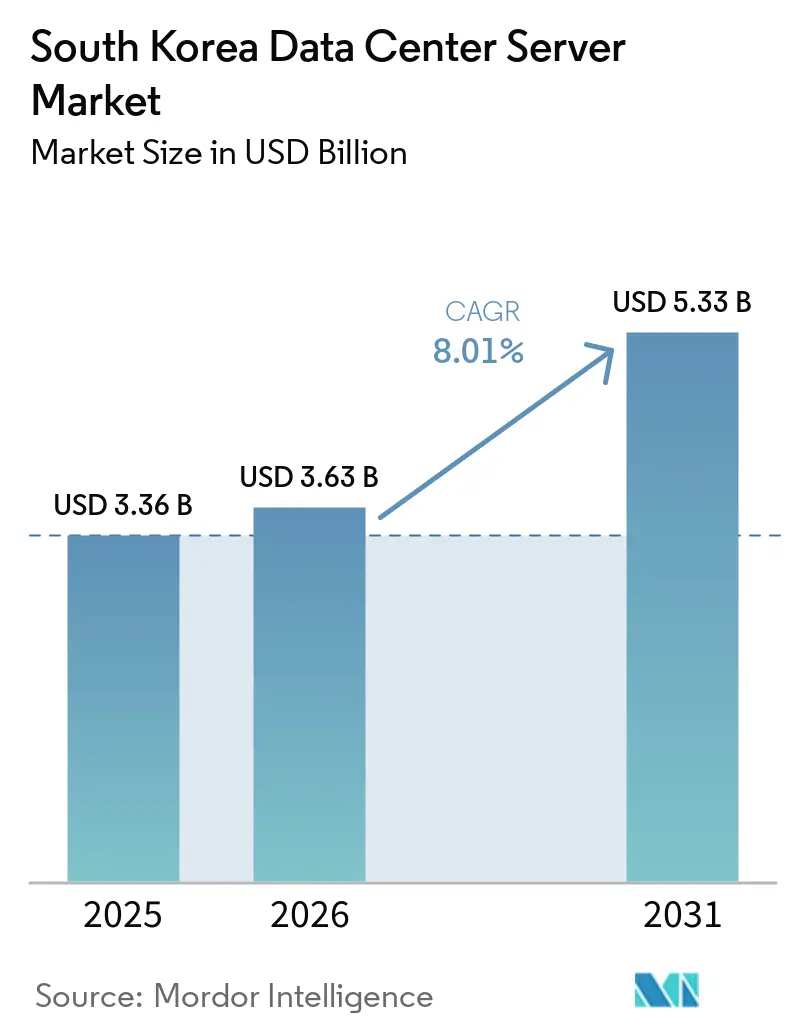

| Base Year Market Size (2025) | USD 3.36 Billion |

| Market Size (2026) | USD 3.63 Billion |

| Market Size (2031) | USD 5.33 Billion |

| Growth Rate (2026 - 2031) | 8.01% CAGR |

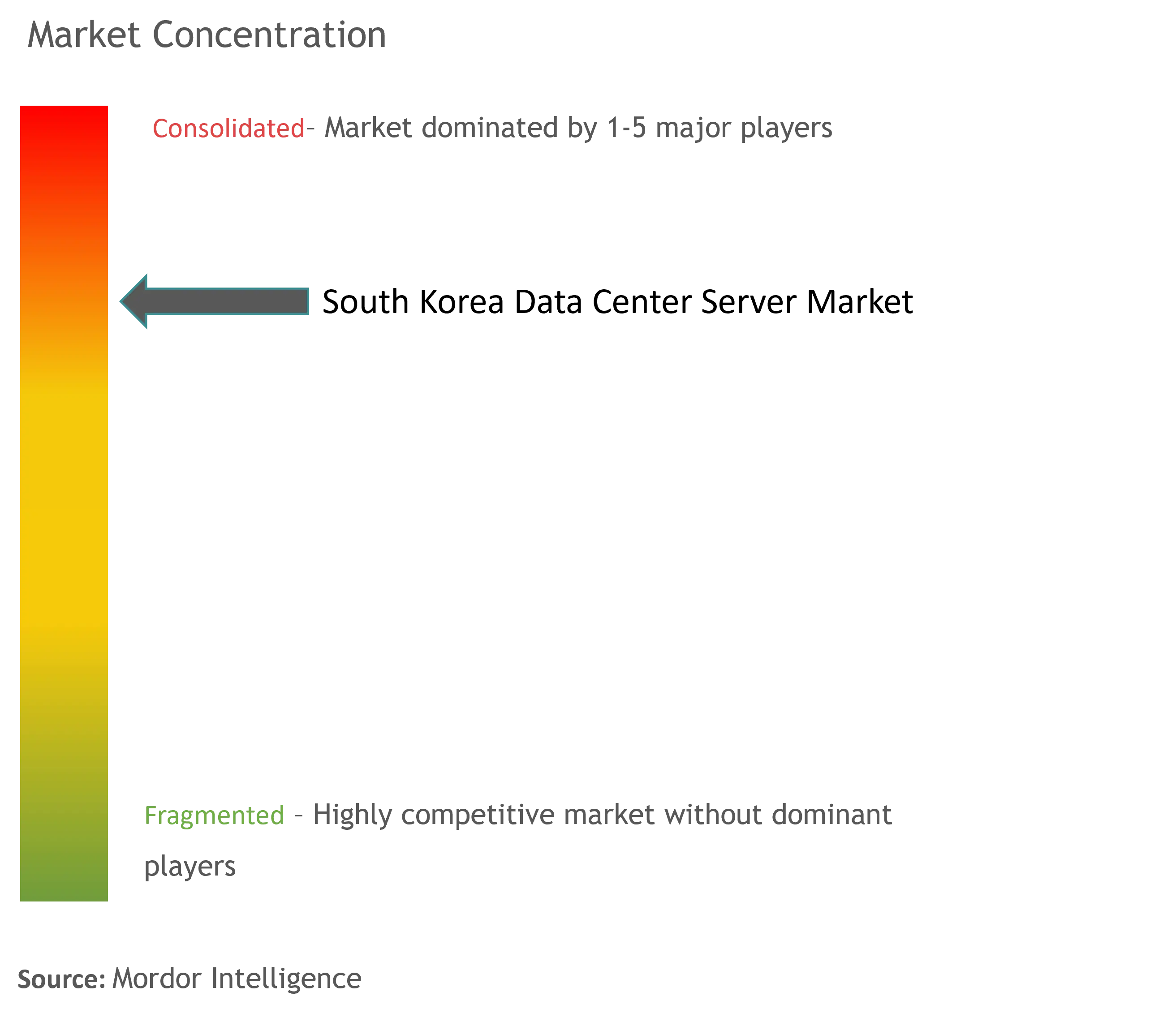

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Data Center Server Market Analysis by Mordor Intelligence

The South Korea data center server market size was valued at USD 3.36 billion in 2025 and estimated to grow from USD 3.63 billion in 2026 to reach USD 5.33 billion by 2031, at a CAGR of 8.01% during the forecast period (2026-2031). Robust government funding of KRW 1.46 trillion for data centers, hyperscale cloud expansion, and a national goal to deploy 30,000 AI servers by 2027 are anchoring revenue visibility. Demand accelerated sharply after 2024 as AI-optimized GPU systems lifted server shipments by 72.7%, underscoring the market’s sensitivity to next-generation workloads. Intensifying competition among global cloud providers, a proliferating edge-computing ecosystem, and tax incentives for local server manufacturing are further amplifying hardware refresh cycles. At the same time, power-grid congestion in the Seoul metropolitan area and compliance costs tied to strict data-sovereignty laws weigh on near-term profitability, steering new builds toward secondary cities and renewable-powered campuses.

Key Report Takeaways

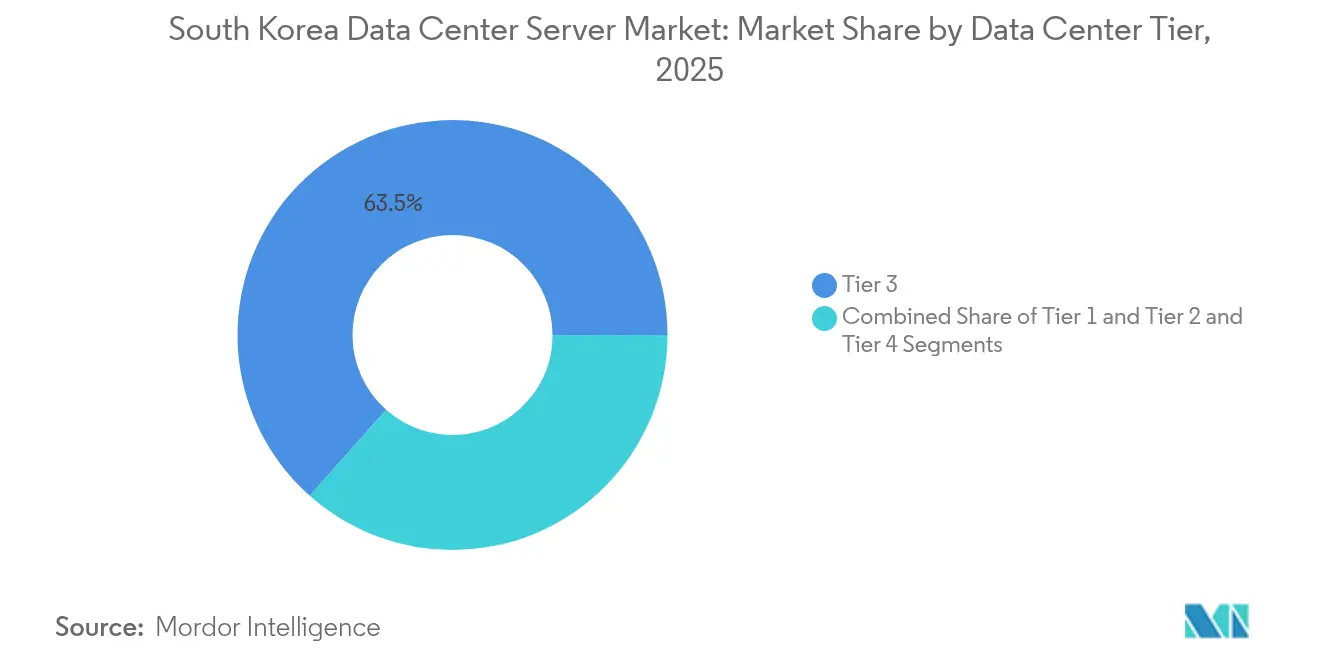

- By data-center tier, Tier 3 facilities led with 63.45% of South Korea data center server market share in 2025; Tier 4 sites are projected to grow at a 13.55% CAGR through 2031.

- By form factor, half-height servers accounted for 54.60% of the South Korea data center server market size in 2025, while quarter-height and micro-blade systems are expanding at 15.12% CAGR.

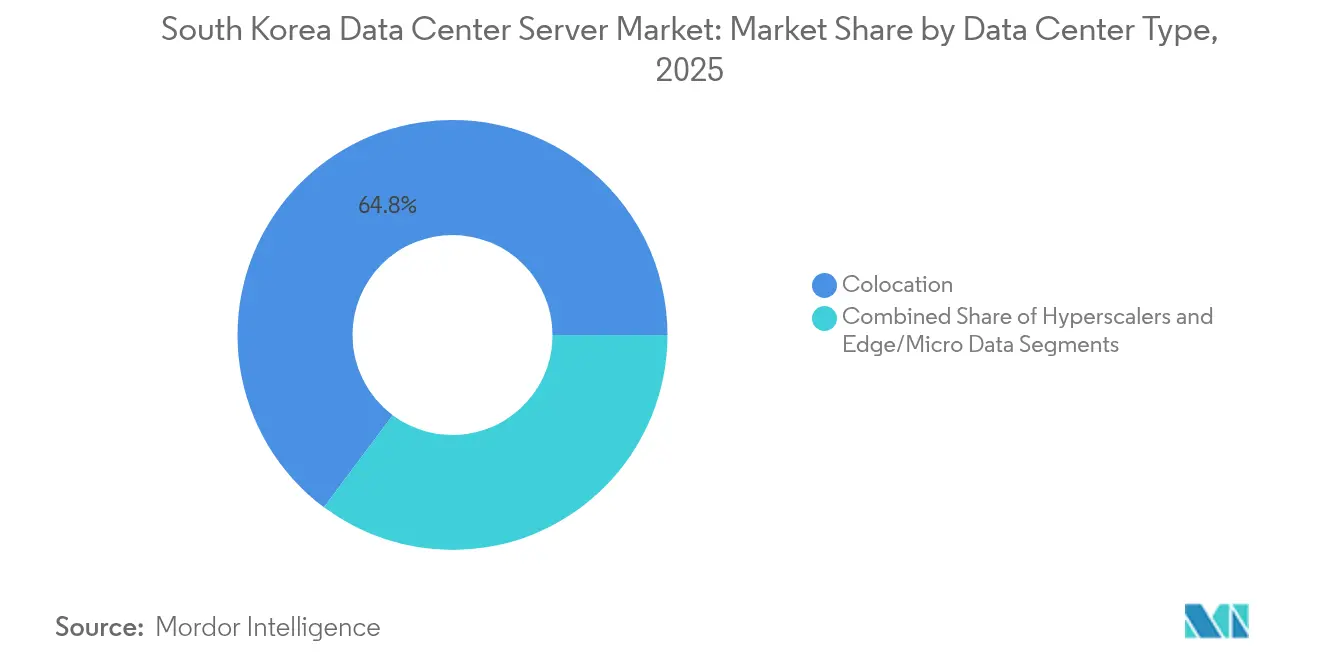

- By deployment type, colocation captured 64.80% of South Korea data center server market share in 2025; hyperscale cloud build-outs are advancing at 13.69% CAGR to 2031.

- By end-user industry, IT and telecommunications commanded 27.95% revenue share in 2025; government workloads are forecast to expand at 14.88% CAGR through 2031.

- Samsung Electronics, SK Telecom, Dell Technologies, Hewlett Packard Enterprise, and Lenovo collectively held an estimated 70.25% share of the South Korea data center server market size in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Dynamics observed within South korea present a country level view when set against the broader international context. The data center server market analysis by Mordor Intelligence provides that expanded global perspective.

South Korea Data Center Server Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government rollout of nationwide fiber and 5G networks | +1.2% | National, concentrated in Seoul-Busan corridor | Medium term (2-4 years) |

| Hyperscale cloud region build-outs (AWS, Google, MS Azure) | +2.1% | Seoul metropolitan area, expanding to Busan | Short term (≤ 2 years) |

| AI/GPU-optimised server demand surge | +2.8% | Global, with early adoption in Seoul tech clusters | Short term (≤ 2 years) |

| Edge computing needs for smart factories and cities | +1.5% | National, pilot programs in Sejong and Busan | Medium term (2-4 years) |

| Server-manufacturing tax incentives and ODM support | +0.9% | National, focused on industrial complexes | Long term (≥ 4 years) |

| Data-center heat-reuse projects lowering OPEX | +0.5% | Urban areas, pilot in metropolitan regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government rollout of nationwide fiber and 5G networks

Rapid 5G densification and continuous fiber upgrades are enabling low-latency connectivity that pushes compute closer to users. The Ministry of Science and ICT reported more than 13 million 5G subscribers by 2021 and targets ubiquitous 5 G-Advanced coverage by 2026.[1]Samsung Electronics, “Q3 2024 Earnings Press Release,” news.samsung.com Telecommunications carriers now integrate edge nodes at base-station hubs, triggering procurement of compact servers designed for constrained spaces. These installations often rely on ruggedized half-height chassis with high core-count CPUs and modest GPU accelerators, balancing power draw against real-time processing needs. As smart-factory and autonomous-mobility pilots scale, localized server clusters are expected to proliferate beyond Seoul, lifting total installed base and broadening vendor addressable opportunities within the South Korea data center server market.

Hyperscale cloud region build-outs

Global cloud leaders are racing to enlarge their Korean footprints to meet enterprise cloud-migration demand. AWS already operates multiple availability zones in Seoul and has announced three additional data centers that will create an estimated 10,000 jobs by 2025. Microsoft and Google are following suit with new zones in metropolitan and coastal areas. Hyperscalers deploy standardized 1U GPU nodes and 2U storage sleds in racks optimized for liquid cooling, thereby amplifying orders for ODM servers with strict cost-to-performance thresholds. Their procurement scale influences component pricing, accelerating the adoption of DDR5 and PCIe 5.0 technologies across the South Korean data center server market.

AI/GPU-optimised server demand surge

AI institutes, cloud gaming firms, and fintech providers are consuming high-end GPU clusters at unprecedented speed. Samsung Electronics generated KRW 29.27 trillion in Device Solutions revenue in Q3 2024, citing robust demand for HBM3 memory used in AI servers Samsung.[2]SK Telecom, “SKT Launches GPU-as-a-Service Platform,” sktelecom.com NHN Cloud and other providers are fielding Dell PowerEdge XE9680 nodes with NVIDIA H100 GPUs, each system drawing nearly 10 kW and requiring liquid cooling. The government has brought forward its schedule to deploy 30,000 AI servers by 2027 as part of the Digital New Deal, accelerating the expansion of the South Korea's artificial intelligence optimised data center ecosystem while driving near-term capacity constraints and intensified competition for cutting-edge accelerators. This GPU wave reshapes rack-level power budgets and propels the South Korea data center server market toward higher-density architectures.

Edge computing needs for smart factories and cities

The Manufacturing Innovation 3.0 road map aims to convert 20,000 plants into smart factories supported by local compute resources. In parallel, the National Smart City Program has established data hubs in Sejong and Busan to coordinate traffic control, energy management, and public safety applications.[3]MDPI, “Smart Cities in South Korea: Policy and Implementation,” mdpi.com Edge sites favor micro-blade designs and tower variants that can withstand industrial temperatures and vibration. Vendors are tailoring servers with ingress protection and extended temperature components to satisfy these environmental constraints. As sensor counts multiply, decentralized analytics engines will account for a rising share of shipments within the South Korea data center server market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex, land and power constraints around Seoul | -1.8% | Seoul metropolitan area | Short term (≤ 2 years) |

| Strict data-sovereignty and security compliance costs | -1.1% | National, affecting all sectors | Medium term (2-4 years) |

| Renewable-power procurement bottlenecks | -0.7% | National, acute in metropolitan areas | Medium term (2-4 years) |

| Scarcity of server-hardware engineering talent | -0.6% | National, concentrated in tech hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High capex, land and power constraints around Seoul

Seventy percent of Korean data centers reside in the capital region, creating grid bottlenecks. The state-owned utility requires lengthy impact assessments for facilities exceeding 10 MW, delaying new builds. Land scarcity has pushed average site acquisition costs above USD 4,000 per square meter, increasing payback periods. Enterprises are shifting capacity to coastal provinces where renewable-energy projects offer lower tariffs and faster approvals, diversifying demand patterns but lengthening supply chains for server vendors.

Strict data-sovereignty and security compliance costs

Amendments to the Personal Information Protection Act and the Cloud Security Assurance Program impose tight residency and encryption rules on public-sector workloads. The 2025 AI Basic Act adds mandatory risk controls for high-impact algorithms. Compliance drives preference for on-premise or colocation deployments equipped with tamper-resistant modules, secure boot, and segregated networks. Foreign vendors must certify firmware and comply with local cryptographic suites, raising engineering overhead and potentially slowing product launches in the South Korea data center server market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data-Center Tier: Infrastructure resilience drives premium adoption

Tier 3 facilities dominated revenue, reflecting balanced uptime and cost profiles that resonate with telecom operators and banks. This segment commanded 63.45% of South Korea data center server market share in 2025, equal to an installed base supporting roughly two-thirds of national cloud and colocation workloads. Tier 4 complexes are expanding at a 13.55% CAGR as hyperscale clouds and AI research centers insist on 2N power, waterless cooling, and dedicated substations. The approved 3-gigawatt campus in Jeollanam-do will embed Tier 4 specifications, opening a multi-year pipeline for ultra-dense GPU racks with direct-to-chip liquid loops. Tier 1 and Tier 2 sites remain viable for edge nodes, smart-factory kiosks, and regional disaster-recovery suites that prioritize proximity over full redundancy.

Tier 3 operators are upgrading legacy halls with busway power distribution, hot-aisle containment, and AI-optimized rack layouts. These retrofits sustain refresh demand for half-height and quarter-height servers able to exploit improved power envelopes. Meanwhile, Tier 4 newcomers negotiate long-term green-power purchase agreements and integrate AI-aware orchestration platforms that automate GPU cluster scheduling. Such investments elevate average selling prices and heighten the strategic relevance of Tier conversions within the South Korea data center server market.

By Form Factor: Density optimization reshapes hardware architectures

Half-height 1U and 2U chassis provided 54.60% of shipments in 2025, favoring balanced compute and storage expansion. These enclosures align with rack design standards across most enterprise and colocation facilities, delivering appropriate airflow within existing raised-floor layouts. Quarter-height blades and micro-nodes are growing at 15.12% CAGR as hyperscalers and edge operators seek maximal cores per square foot. Their success stems from integrated mid-plane networking, shared power, and backplane-level liquid cooling that reduces per-system capital charges.

Blade revenue gains are reinforced by AI training clusters that concentrate eight GPUs and dual Xeon processors in high-density trays. Vendors respond with silicon photonics interconnects and high-efficiency power supplies hitting 97% conversion. Although tower formats survive in small offices and edge locations lacking racks, the migration toward cloud and AI is skewing demand toward sled-based and blade-based designs, reinforcing density-led culture in the South Korea data center server market.

By Processor Architecture: x86 dominance faces emerging alternatives

x86 CPUs from Intel and AMD powered more than 84.65% of installed capacity in 2025, owing to rich software ecosystems and familiar management stacks. Generational advances such as Advanced Matrix Extensions and CXL 3.0 have improved inference throughput while preserving backward compatibility, securing continued preference among banks and public agencies. ARM-based servers, however, now penetrate web-scale caching, video transcoding, and cold-storage workloads that reward high core counts and low watt per thread.

Samsung’s foundry progress toward 2 nm gate-all-around transistors supports potential domestic ARM designs optimized for sovereign AI clusters. Proprietary architectures, including IBM Power and NVIDIA Grace, carve out workloads where memory bandwidth and deterministic latency outrank general-purpose metrics. Although x86 leadership is intact, total cost-of-ownership assessments and sovereign-tech incentives are likely to accelerate heterogeneous compute adoption inside the South Korea data center server industry.

By Data Center Type: Colocation leadership amid hyperscale expansion

Colocation maintained 64.80% of 2025 shipments as enterprises outsourced facility management and capital overhead. Telecom carriers KT, SK Telecom, and LG Uplus operate roughly thirty carrier-neutral halls, bundling network transit and managed security to shorten migration cycles. Hyperscale clouds are adding double-digit megawatt halls at a 13.69% CAGR, tilting the power mix toward 30 kW-plus racks populated with GPU blades and NVMe over-Fabric arrays.

Enterprise-owned data rooms persist for workloads bound by residency or latency covenants. Edge and micro data centers are emerging in smart-factory parks and highway rest areas, hosting ARM-based single-socket servers optimized for real-time analytics. This multicloud deployment mosaic complicates lifecycle planning but multiplies node counts, sustaining shipment velocity inside the South Korea data center server market.

By End-User Industry: Telecommunications leadership drives digital infrastructure

Telecom and IT services led with 27.95% revenue share, acting as infrastructure landlords and major server consumers for 5G core, CDN, and AI inference stacks. Their demand patterns favor horizontally scalable nodes with DPU acceleration for network offload. Government demand is growing fastest at 14.88% CAGR under the Korea Digital New Deal, which funds AI supercomputers, cybersecurity fabrics, and e-government modernization programs.

BFSI institutions invest heavily in low-latency trading and fraud analytics clusters that require FIPS-validated hardware security modules. Manufacturing firms equip predictive-maintenance platforms in smart factories, choosing ruggedized edge servers with accelerometers and GPU inference modules. Healthcare providers adopt cloud-hosted diagnostics engines that halve image-processing turnaround, reinforcing steady node refresh rates within the South Korea data center server market.

Geography Analysis

The Seoul metropolitan area hosts roughly 70% of installed capacity, leveraging dense fiber rings, IX hubs, and proximity to the largest corporate headquarters. Such concentration boosts operational efficiency but strains a grid already delivering 14 GW to ICT facilities, compelling curtailment requests during summer peaks . Municipal opposition to further substations and high-voltage lines elevates project risk, encouraging operators to scout coastal or inland provinces.

Busan, home to submarine cable landing stations, is emerging as a secondary cloud locale. Lower land prices, port-adjacent logistics, and municipal tax holidays have attracted Equinix and local telcos to build xScale campuses. The National Smart City pilot in Busan generates consistent edge-server demand for traffic monitoring, e-health, and disaster response analytics, embedding localized compute as a civic utility.

Jeollanam-do’s 3-GW AI campus marks the first megaproject outside the capital corridor, underpinned by long-term offshore-wind power purchase agreements and direct seawater cooling. Regional governments in Gwangju, Daegu, and Chungnam follow with zoning reforms, purpose-built industrial parks, and renewable-energy credits aimed at decentralizing growth. This redistributes purchase orders for racks, PDUs, and switching gear, broadening territorial exposure for vendors active in the South Korea data center server market.

Coverage of the data center server market by Mordor Intelligence spans a wide geographic footprint, with regional analysis available for North America, Americas, and Europe, alongside detailed country-level intelligence for Philippines, Singapore, United States, Brazil, Germany, and Israel, each shaped by local operating conditions.

Competitive Landscape

Global OEMs Dell Technologies, Hewlett-Packard Enterprise, and Lenovo leverage end-to-end portfolios and established service networks to anchor enterprise accounts. Dell’s PowerEdge XE series pairs NVIDIA H100 GPUs with direct-liquid cooling, while HPE integrates Cray interconnects for HPC-as-a-Service offerings. Lenovo maximizes supply-chain efficiency through ODM partnerships and localized final assembly, reducing lead times for Korean buyers.

Samsung Electronics exploits vertical integration by bundling servers with HBM3 memory, DDR5 modules, and CXL-attached SSDs, capturing scale economies and aligning with technology-sovereignty objectives. SK Telecom’s GPUaaS platform combines H100 clusters, telco edge PoPs, and proprietary AI orchestration, creating a hybrid model that blurs the lines between hardware vendor and cloud provider.

Domestic ODMs gain traction through government grants that support indigenous server boards, immersion-ready chassis, and ORAN-compliant edge appliances. The National IT Industry Promotion Agency’s KRW 4.5 billion equipment localization fund enables small manufacturers to certify boards for public procurement, diluting import dependence and intensifying competition in the South Korea data center server market.

South Korea Data Center Server Industry Leaders

Dell Technologies Inc.

Hewlett Packard Enterprise Co.

Lenovo Group Ltd.

Super Micro Computer Inc.

Inspur Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Stock Farm Road received approval for the world’s largest AI data center in Jeollanam-do with 3 GW capacity and an initial USD 10 billion investment, expandable to USD 35 billion. Construction begins in 2025 and completes in 2028

- January 2025: SK Telecom launched GPU-as-a-Service at its Gasan AI Data Center using NVIDIA H100 GPUs, with H200 upgrades slated for early 2025.

- January 2025: South Korea enacted the AI Basic Act, mandating risk controls and human oversight for high-impact AI workloads.

- April 2025: Dell Technologies introduced PowerEdge and PowerStore updates optimized for AI-ready data centers

- May 2025: The National IT Industry Promotion Agency unveiled a KRW 4.5 billion program for localized data-center equipment and a KRW 4 billion program for sustainable technologies.

- November 2024: SK Telecom acquired an additional 24.76% stake in SK Broadband to reinforce data-center and subsea-cable assets.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the South Korea data center server market as revenue generated from brand-new rack, blade, and micro-blade servers installed in Tier 1-4 facilities and owned by cloud service providers, colocation operators, and large enterprises.

Scope exclusion: edge boxes deployed in smart factories or retail micro-sites fall outside this baseline.

Segmentation Overview

- By Data-Center Tier

- Tier 1 and 2

- Tier 3

- Tier 4

- By Form Factor

- Half-height Blades

- Full-height Blades

- Quarter-height / Micro-blades

- By Application / Workload

- Virtualisation and Private Cloud

- High-Performance Computing (HPC)

- Artificial Intelligence/Machine Learning and Data Analytics

- Storage-centric

- Edge / IoT Gateways

- By Data Center Type

- Hyperscalers/Cloud Service Provider

- Colocation Facilities

- Enterprise and Edge

- By End-use Industry

- BFSI

- IT and Telecom

- Healthcare and Life-Sciences

- Manufacturing and Industry 4.0

- Energy and Utilities

- Government and Defence

Detailed Research Methodology and Data Validation

Primary Research

Discussions with facility operators in Seoul, Busan, and Gwangju, regional server ODMs, and local channel partners allowed us to validate shipment volumes, GPU share swings, and average contract prices. Structured surveys with BFSI and gaming workload owners tested our penetration assumptions.

Desk Research

We first mapped supply by mining Statistics Korea trade codes for HS 847141 and HS 847150, monthly shipment logs from Korea Customs Service, and rack-density disclosures lodged with the Ministry of Science & ICT. Industry guidance from the Korea Data Center Council, energy-use dashboards of Korea Electric Power Corporation, and listed-company filings enriched utilization, ASP, and power-cost benchmarks. Paywalled snapshots from D&B Hoovers and Dow Jones Factiva helped verify vendor splits and currency conversions. This list is illustrative; many additional public datasets supported fact-checking and clarification.

Market-Sizing & Forecasting

We start with a top-down reconstruction of server demand. National IT load (MW), average rack density (kW), and servers-per-rack ratios yield installed units, which are then multiplied by blended ASPs to arrive at value. Select bottom-up cross-checks, supplier roll-ups, and sampled hyperscale procurement prices flag gaps for adjustment. Key variables include: 1) GPU server share, 2) rack density trend, 3) cloud tenant growth, 4) KRW-USD exchange, 5) data-center power tariffs, and 6) renewal cycle length. A multivariate regression, back-tested since 2018, projects each driver through 2030 and feeds scenario analysis around energy pricing shocks.

Data Validation & Update Cycle

Outputs pass variance screens against IDC tracker exports, KEPCO energy usage, and Customs data. Anomalies trigger re-checks before analyst sign-off. Reports refresh every twelve months, with mid-cycle updates if policy shifts or large hyperscale expansions materially alter demand.

Why Mordor's South Korea Data Center Server Baseline Proves Dependable

Published values often diverge because firms pick different components, facility tiers, and currency bases.

By anchoring on installed IT load and tying it to verified shipment and price evidence, Mordor Intelligence gives decision-makers a figure that travels well across budgeting and capacity-planning discussions.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.03 Bn (2024) | Mordor Intelligence | - |

| USD 2.70 Bn (2024) | Regional Consultancy A | Omits micro-blade shipments and Tier 4 builds, leading to an undercount. |

| USD 3.80 Bn (2024) | Industry Tracker B | Includes on-prem enterprise servers outside dedicated data centers, inflating totals. |

| USD 13.30 Bn (2024) | Global Consultancy C | Measures full data-center hardware stack, servers, storage, and network, so scope is far broader. |

These contrasts show that once differences in server type coverage, facility inclusion, and component breadth are stripped away, our carefully bounded approach offers the most transparent, repeatable baseline for planners and investors.

Key Questions Answered in the Report

How big is the South Korea Data Center Server Market?

The South Korea Data Center Server Market size is expected to reach USD 3.63 billion in 2026 and grow at a CAGR of 8.01% to reach USD 5.33 billion by 2031.

What is the current South Korea Data Center Server Market size?

In 2026, the South Korea Data Center Server Market size is expected to reach USD 3.63 billion.

Who are the key players in South Korea Data Center Server Market?

HP Enterprise, Dell Inc., IBM Korea Inc., Fujitsu Limited and Super Micro Computer, Inc. are the major companies operating in the South Korea Data Center Server Market.

What years does this South Korea Data Center Server Market cover, and what was the market size in 2025?

In 2025, the South Korea Data Center Server Market size was estimated at USD 3.63 billion. The report covers the South Korea Data Center Server Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the South Korea Data Center Server Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: