Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

South Korea Data Center Processor Market Report Segments the Industry Into Processor Type (GPU, CPU, FPGA, AI Accelerator), Application (Advanced Data Analytics, AI/ML Training and Inferences, and More), Architecture (x86, Non-X86 (ARM, Power and Other Processors)), Data Center Type (Enterprise, Colocation, Cloud Service Providers). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

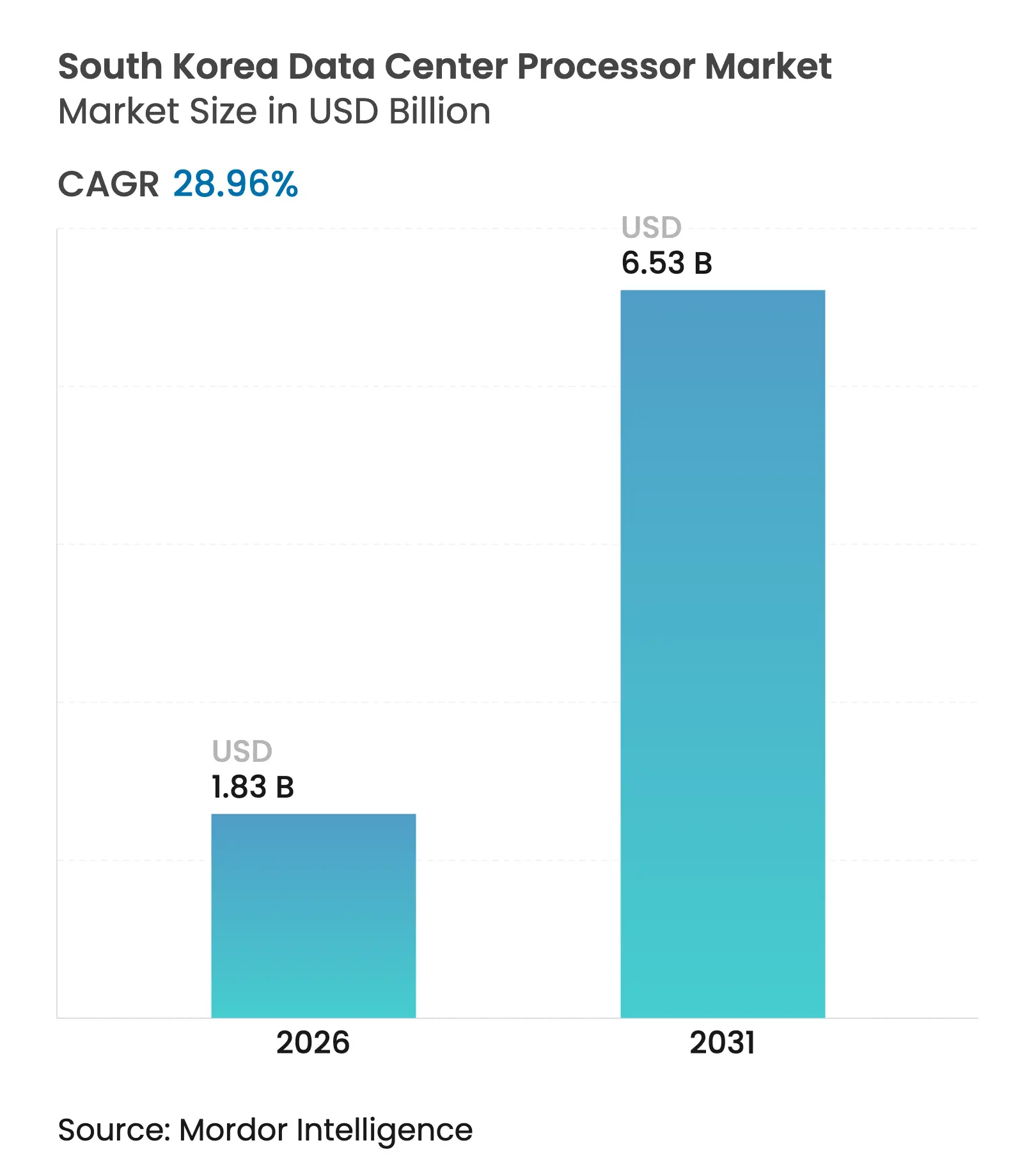

| Market Size (2026) | USD 1.83 Billion |

| Market Size (2031) | USD 6.53 Billion |

| Growth Rate (2026 - 2031) | 28.96 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The South Korea data center processor market size was valued at USD 1.42 billion in 2025 and estimated to grow from USD 1.83 billion in 2026 to reach USD 6.53 billion by 2031, at a CAGR of 28.96% during the forecast period (2026-2031). This growth reflects the nation’s ambition to become a global AI compute hub, underpinned by a USD 471 billion semiconductor investment pipeline and the national 10,000-GPU program. Hyperscaler demand, a rapid shift toward GPU-rich server architectures, and government incentives for advanced packaging have widened the total addressable market for processors. CPUs still anchor most server deployments, but AI accelerators and ARM-based alternatives are reshaping procurement priorities as operators seek lower total cost of ownership and higher energy efficiency. Rising electricity prices, RE100 compliance pressures, and ongoing HBM shortages temper short-term momentum, yet local champions—buoyed by supportive policy—continue to close technology gaps with multinational rivals.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Soaring AI/ML compute demand from hyperscalers and

national 10,000-GPU programme

Soaring AI/ML compute demand from hyperscalers and

national 10,000-GPU programme

| +8.5% | National (Seoul–Gyeonggi corridor) | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

+8.5%

|

Geographic Relevance

:

National (Seoul–Gyeonggi corridor)

|

Impact Timeline

:

Medium term (2-4 years)

|

USD 471 billion national semiconductor and AI-DC

investment pipeline

USD 471 billion national semiconductor and AI-DC

investment pipeline

| +7.2% | National (Gyeonggi Province mega cluster) | Long term (≥ 4 years) | |||

Rapid GPU server mix-shift expands processor TAM

Rapid GPU server mix-shift expands processor TAM

| +6.8% | National (cloud providers) | Short term (≤ 2 years) | |||

Arm/ASIC total-cost-of-ownership advantage accelerates

server refresh

Arm/ASIC total-cost-of-ownership advantage accelerates

server refresh

| +3.1% | Global hyperscalers in Korea | Medium term (2-4 years) | |||

Emergency power-tariff discounts for high-density DC

clusters

Emergency power-tariff discounts for high-density DC

clusters

| +2.4% | Jeollanam-do and industrial zones | Short term (≤ 2 years) | |||

Local glass-substrate supply chain boosts advanced

packaging yields

Local glass-substrate supply chain boosts advanced

packaging yields

| +1.8% | National | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Soaring AI/ML Compute Demand from Hyperscalers and the 10,000-GPU Programme

Processor demand is accelerating as the government’s 10,000-GPU program stockpiles compute capacity while hyperscalers such as SK Telecom build gigawatt-scale AI data centers in Seoul and Gumi. Public procurement validates domestic AI chips and crowds in private investment, enabling startups like Rebellions to target one-third of local large-language-model inference workloads within 30 months. Naver’s 65-exabyte Sejong campus illustrates how national AI ambitions translate into record processor orders.

USD 471 Billion National Semiconductor and AI-DC Investment Pipeline

Sixteen new fabs and seven million wafers per month of output are slated by 2030, reducing reliance on foreign architectures and lowering production cost curves.[1]TrendForce Analysts, “Korea Mega-Cluster Fabs on Track,” trendforce.com Samsung’s KRW 360 trillion commitment to advanced packaging and SK Hynix’s KRW 122 trillion HBM build-out reinforce long-run supply security. State-backed loans and tax relief trim capital costs, incentivizing local design houses to tape-out processors domestically.

Rapid GPU Server Mix-Shift Expands Processor TAM

GPU-equipped servers captured 45% of shipments in 2023, up from 26.2% a year earlier, reflecting the pivot to generative AI workloads.[2]Jon Brodkin, “GPU Servers Overtake CPU-Only Boxes in 2023,” cio.com The premium attached to HBM-driven GPU nodes inflates average server prices and stimulates auxiliary demand for cooling and power delivery upgrades. LG AI Research’s adoption of FuriosaAI chips underscores how local enterprises seek NVIDIA alternatives.

Arm/ASIC Total-Cost-of-Ownership Advantage Accelerates Server Refresh

ARM designs already command 13.2% of server revenue, and ASICs like Rebellions’ ATOM deliver 5× energy savings relative to legacy GPUs,[3]Claire Kim, “Korea Aims for 10% of Global System-Chip Market,” koreatimes.co.kr shortening payback periods as tariffs and carbon fees rise. Korean cloud operators are therefore retiring x86 racks ahead of schedule to curb operational costs.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

US export controls and China tensions squeeze supply

chains

US export controls and China tensions squeeze supply

chains

| -4.2% | National (China-linked chains) | Short term (≤ 2 years) |

(~) % Impact on CAGR Forecast

:

-4.2%

|

Geographic Relevance

:

National (China-linked chains)

|

Impact Timeline

:

Short term (≤ 2 years)

|

Chronic GPU/HBM shortages raise lead-times

Chronic GPU/HBM shortages raise lead-times

| -3.8% | Global (Korean hyperscalers) | Medium term (2-4 years) | |||

High electricity cost and RE100 compliance risk

High electricity cost and RE100 compliance risk

| -2.1% | National (metro areas) | Long term (≥ 4 years) | |||

Under-utilised provincial AI DCs dampen investor

confidence

Under-utilised provincial AI DCs dampen investor

confidence

| -1.6% | Secondary cities | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

US Export Controls and China Tensions Squeeze Supply Chains

Washington’s tightening of semiconductor tool exports heightens uncertainty for Samsung and SK Hynix facilities in China, threatening advanced node availability for Korean data centers. February 2025 exports to China fell 31.8%, prompting operators to delay processor orders amid policy flux.

Chronic GPU/HBM Shortages Raise Lead-Times

HBM capacity is booked solid through 2025, with SK Hynix and Samsung pushing high-volume runs into 2026. Lead times extending beyond a year complicate capex planning, while smaller buyers struggle to secure allocation behind hyperscaler queues. Alternative CXL-based memory expansion from Panmnesia offers partial relief

By Processor Type: AI Accelerators Shape Heterogeneous Servers

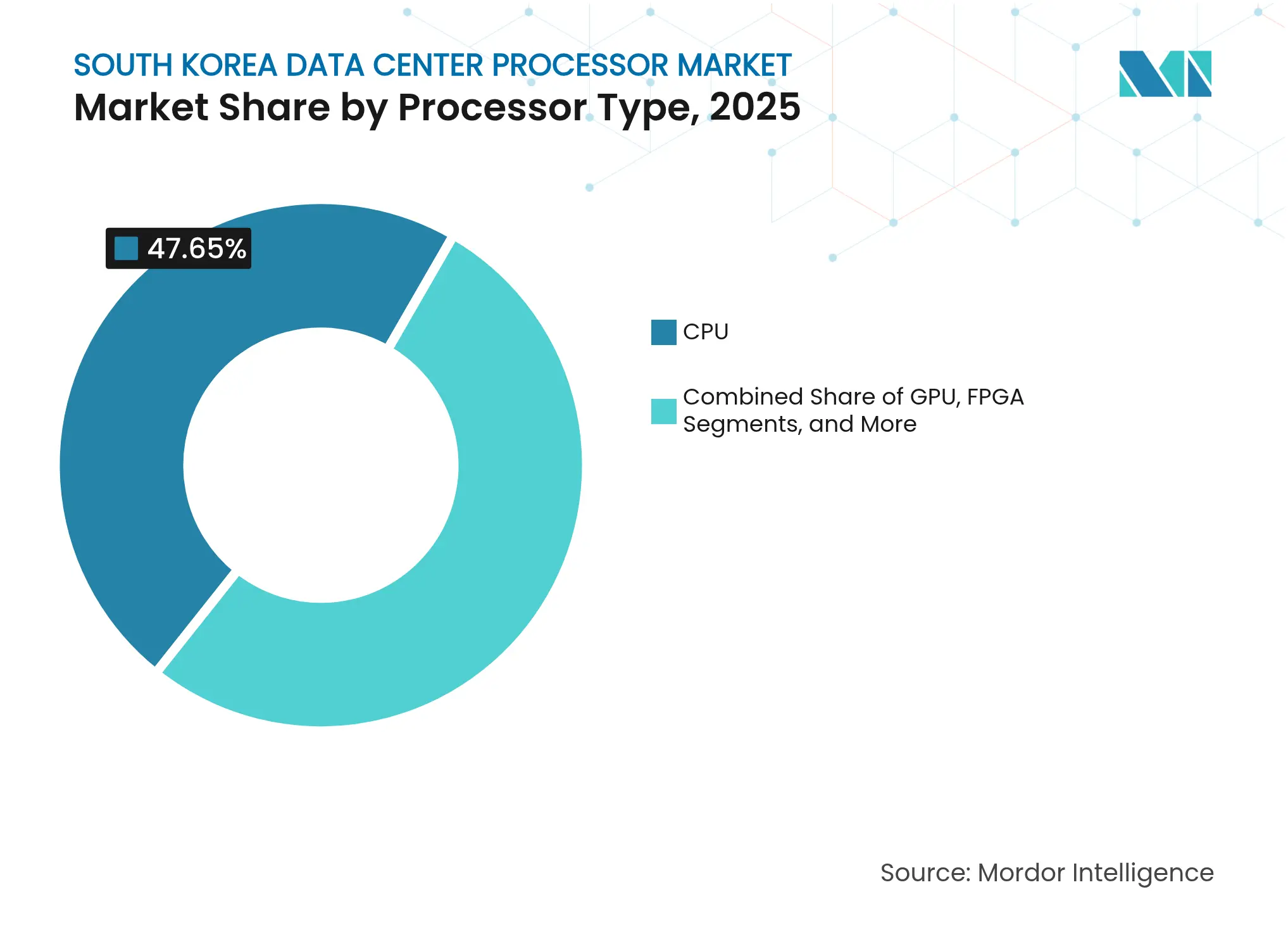

AI accelerators are forecast to post a 25.55% CAGR through 2031 even as CPUs retained 47.65% South Korea data center processor market share in 2025. The energy-efficiency gains of neural processing units such as Rebellions’ ATOM are key purchase triggers, while GPUs continue to dominate large-scale model training.

Hybrid configurations now blend CPUs, GPUs and AI ASICs on unified fabrics, reducing bottlenecks and maximizing HBM utilization. Samsung’s CXL 2.0 DRAM enables such interconnects, fostering demand for accelerators in workloads ranging from vision inference to autonomous robotics.

Note: Segment shares of all individual segments available upon report purchase

By Application: Analytics Outpaces Core AI Training

AI/ML training and inference controlled 30.05% of the South Korea data center processor market size in 2025, yet advanced analytics is growing faster at 24.6% CAGR as enterprises pivot to real-time insights. Financial services leverage processors for millisecond fraud detection, while manufacturers deploy edge inference for predictive maintenance.

Government investment in a KRW 94.6 billion national AI hub broadens adoption beyond big tech, driving fresh demand in healthcare diagnostics and public-sector services that value low-latency analytics.

By Architecture: Non-x86 Chips Gain Traction

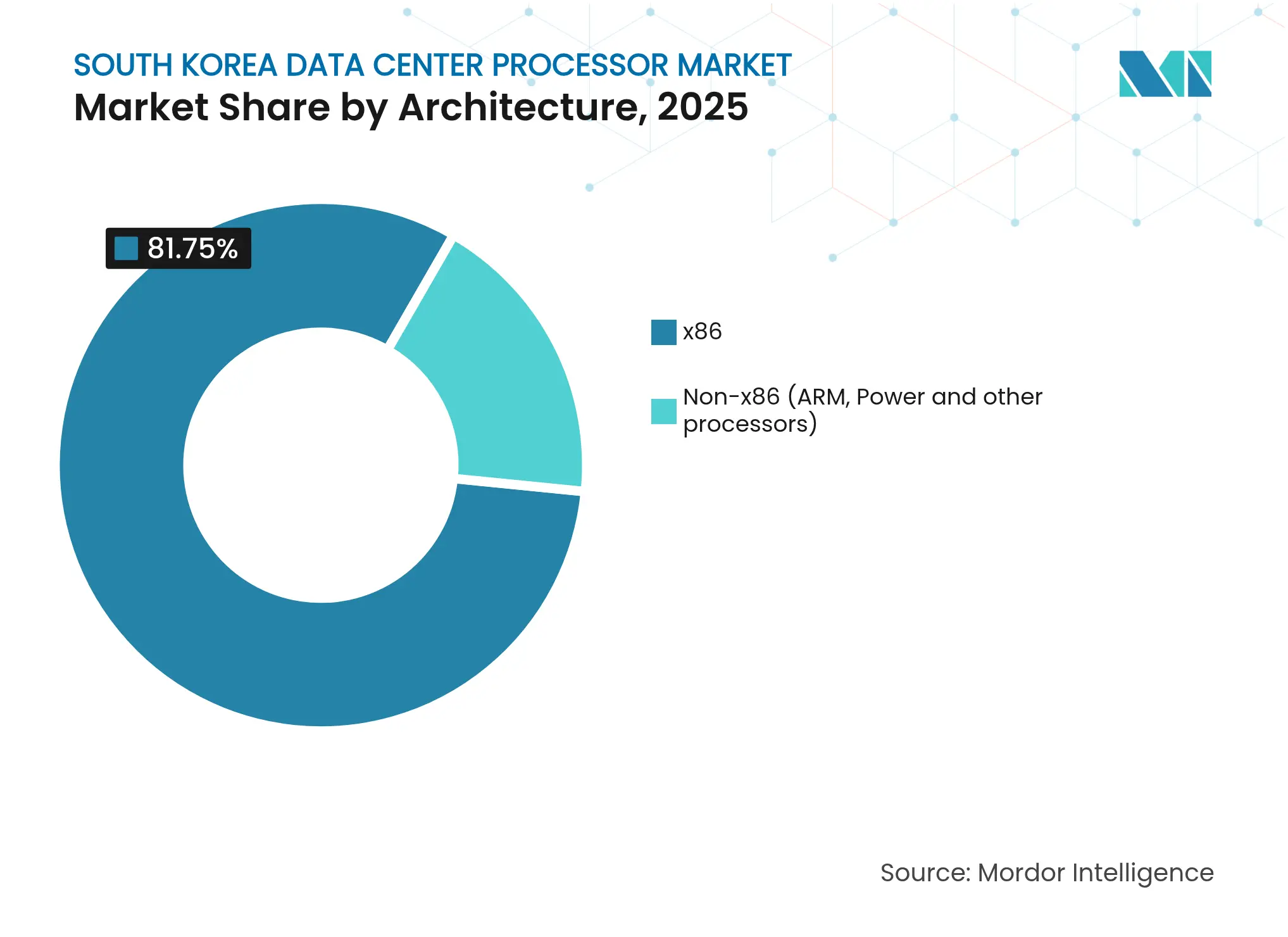

Although x86 processors still deliver 81.75% revenue share, non-x86 alternatives will expand at 23.9% CAGR to 2031. ARM’s power-per-watt advantage resonates with hyperscalers chasing PUE reductions, and SEMIFIVE’s Neoverse-based HPC platform signals local momentum.

AMD’s server share climb to 27.2% also re-energizes competition within x86, spurring price-performance gains that benefit Korean operators. Neuromorphic designs from KAIST highlight longer-term pathways for ultra-low-power inferencing at the edge.

Note: Segment shares of all individual segments available upon report purchase

By Data Center Type: Cloud Providers Extend Lead

Cloud service providers captured 45.75% South Korea data center processor market share in 2025 and will grow at 26.6% CAGR. Hyperscalers exploit scale to lock in scarce GPUs and negotiate bespoke silicon roadmaps. Enterprise on-premises facilities persist for regulatory workloads, yet colocation and managed service providers bridge hybrid demand.

MegazoneCloud’s USD 7 billion IPO plan underlines sector capital intensity, while SK Telecom’s USD 200 million stake in SMART Global Holdings secures procurement leverage for future AI nodes.

Processor deployments cluster along the Seoul–Gyeonggi technology corridor, leveraging proximity to fabs, universities, and cloud regions anchored by Naver and Kakao. The proposed 3-gigawatt Jeollanam-do campus will shift demand southward, with USD 35 billion earmarked for construction. Busan’s Eco Delta City project and Gwangju’s AI cluster diversify capacity away from the capital, yet utilization lags in some provincial builds due to limited local budgets.

Regional power-tariff incentives offset higher grid costs, encouraging operators to pre-locate compute near renewable sources. Internationally, Korean developers are exporting know-how to Southeast Asia, evidenced by the USD 300 million Jakarta facility joint venture with Sinar Mas. Geographic spread reduces single-point risks and supports balanced national digital growth.

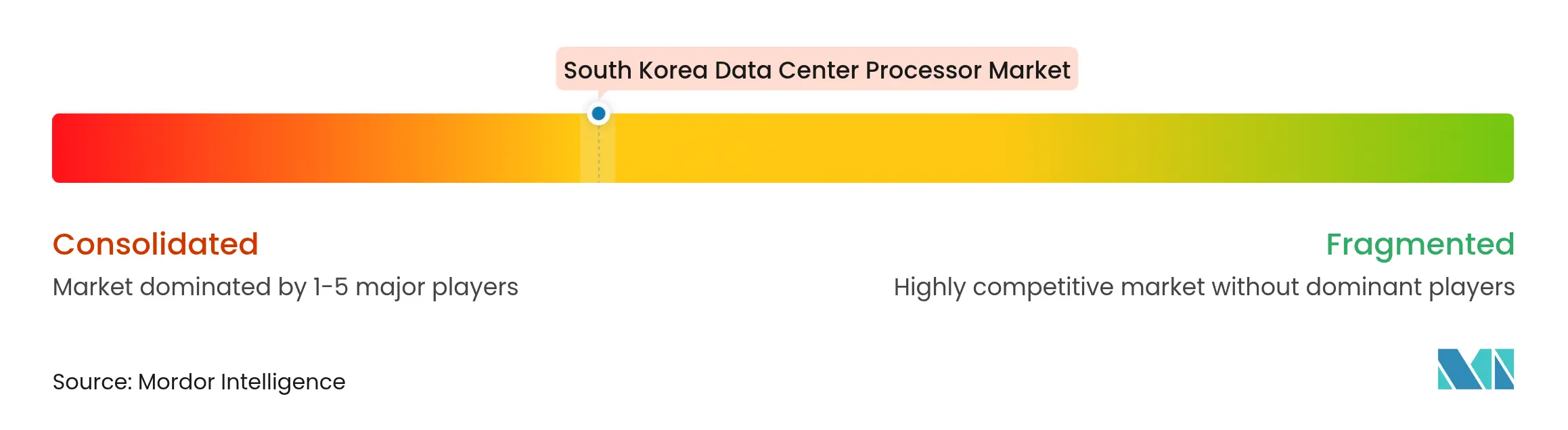

Market Concentration

The market is moderately concentrated, with global giants NVIDIA, Intel and AMD sharing space with domestic innovators Rebellions, SAPEON and FuriosaAI. Product roadmaps increasingly hinge on ecosystem partnerships: Rebellions collaborates with ARM and Samsung Foundry on chiplets, while Samsung leverages CXL leadership for memory-centric differentiation.

The December 2024 merger between Rebellions and SAPEON formed Korea’s first AI chip unicorn valued near KRW 2 trillion, signaling a consolidation wave aimed at challenging foreign dominance. Access to HBM, advanced packaging, and export-license-free IP positions local vendors to secure domestic inferencing contracts, especially in public AI clouds, complying with data-residency rules.

Strategic moves include FuriosaAI’s rejection of an USD 800 million takeover by Meta to preserve sovereignty and Samsung’s adoption of a 64-hour R&D workweek to accelerate tape-outs. SK Hynix, meanwhile, fast-tracked HBM4 pilot lines to lock in NVIDIA design wins and sustain high margins on premium memory.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SEGMENTATION

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES and FUTURE OUTLOOK

Data centers house and manage critical applications and data, using computing and storage networks for efficient delivery. Processors—GPUs, CPUs, and TPUs—are central to their operation. GPUs handle multitasking, excelling in graphics rendering and AI tasks. CPUs, with multi-core architecture, support parallel processing. TPUs, designed for machine learning, stand out from GPUs, which have transitioned from graphics to AI applications.

The South Korea Data Center Processor Market is Segmented by Processor Type (CPU, GPU, FPGA, AI Accelerators), by Application (Advanced Data Analytics, AI/ML Training and Inferences, High Performance Computing, Security and Encryption, Network Functions, and Others), by Architecture (x86 and Non-x86 (ARM, Power and other processors), and by Data Center Type (Enterprise, Colocation and Cloud Service Providers). The Report Offers the Market Size and Forecasts for all the Above Segments in Terms of Value (USD).

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.