South Korea Chemical Warehousing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

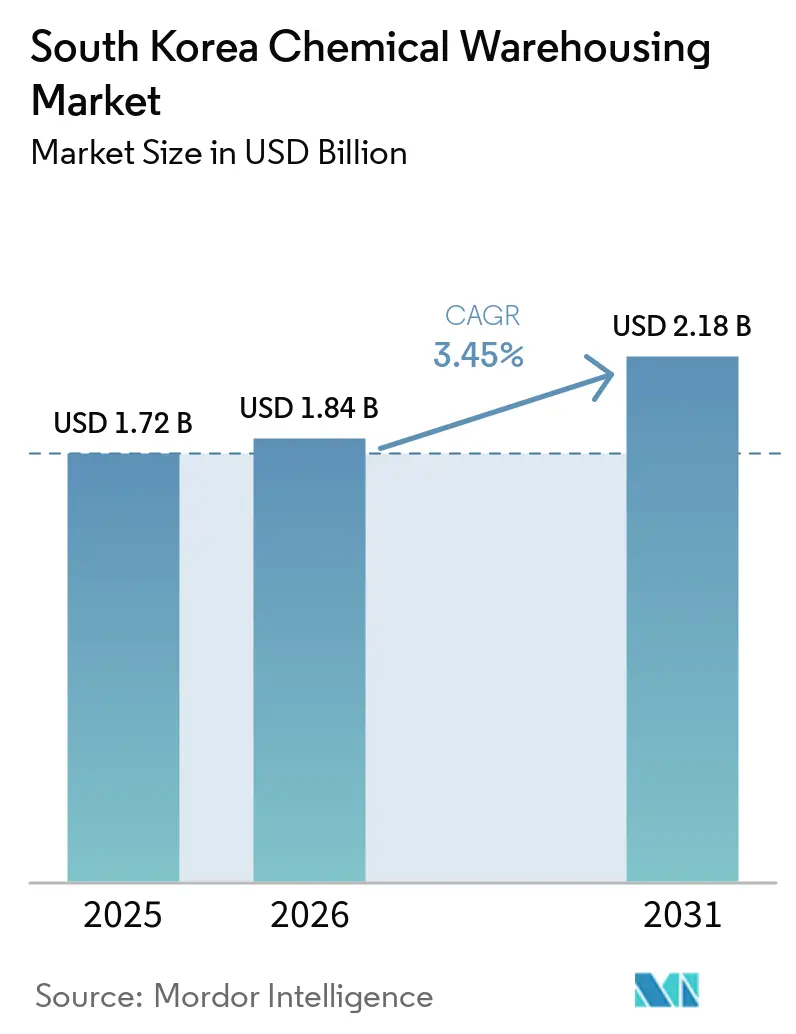

| Base Year Market Size (2025) | USD 1.72 Billion |

| Market Size (2026) | USD 1.84 Billion |

| Market Size (2031) | USD 2.18 Billion |

| Growth Rate (2026 - 2031) | 3.45% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Chemical Warehousing Market Analysis by Mordor Intelligence

The South Korea chemical warehousing market size is expected to increase from USD 1.72 billion in 2025 to USD 1.84 billion in 2026 and reach USD 2.18 billion by 2031, growing at a CAGR of 3.45% over 2026-2031. Demand is shifting toward high-specification storage as maritime fuel decarbonization, battery-material self-sufficiency, and government-backed digital safety mandates change the economics of facility design and location. Coastal hubs are racing to add ammonia-ready bunkering infrastructure, while inland clusters near battery-component plants require ultra-dry rooms that hold relative humidity below 1%. Artificial-intelligence (AI) safety systems are moving from pilot projects to mainstream practice because state subsidies offset roughly half of the upfront costs of sensors and software. Consolidation is likely as revised Chemical Control Act (CCA) rules add capital requirements that small operators struggle to meet.[1] Korea Energy Economics Institute, “Energy Transition and Logistics Safety Requirements,” keei.re.kr

Key Report Takeaways

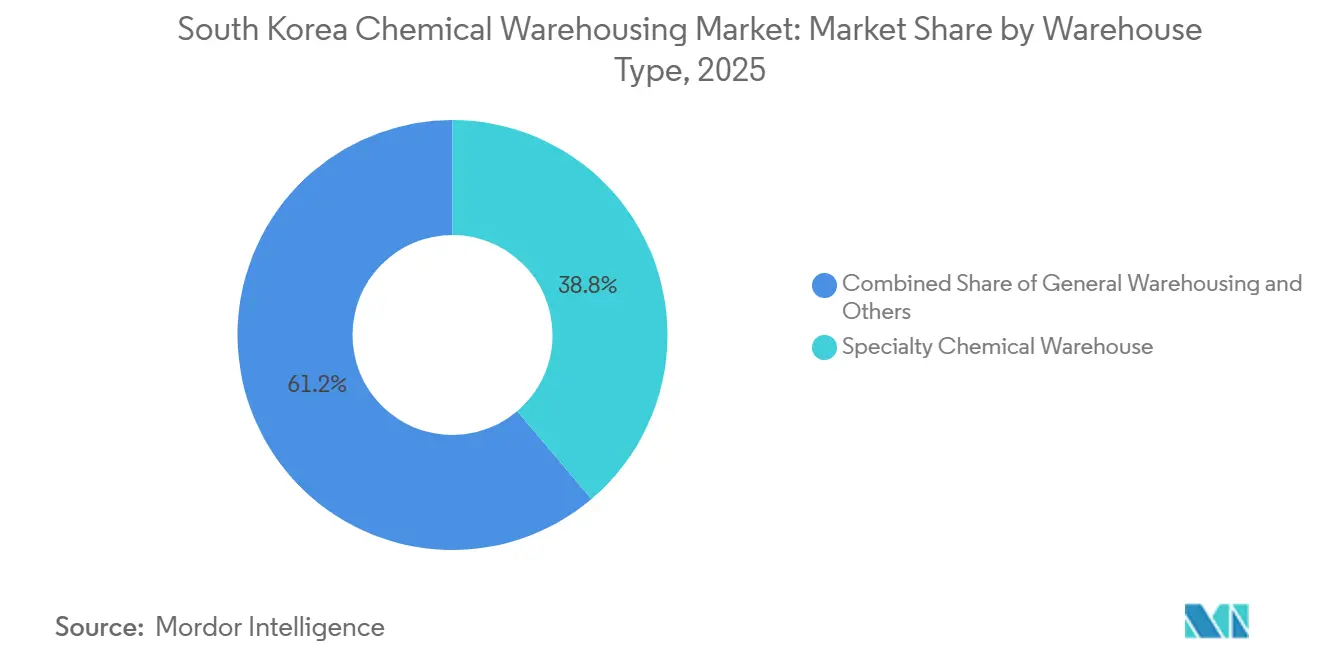

- By warehouse type, Specialty Chemical Warehouses led with 38.80% of the South Korea chemical warehousing market share in 2025. Temperature-Controlled Chemical Warehouses are forecast to expand at a 5.58% CAGR through 2031.

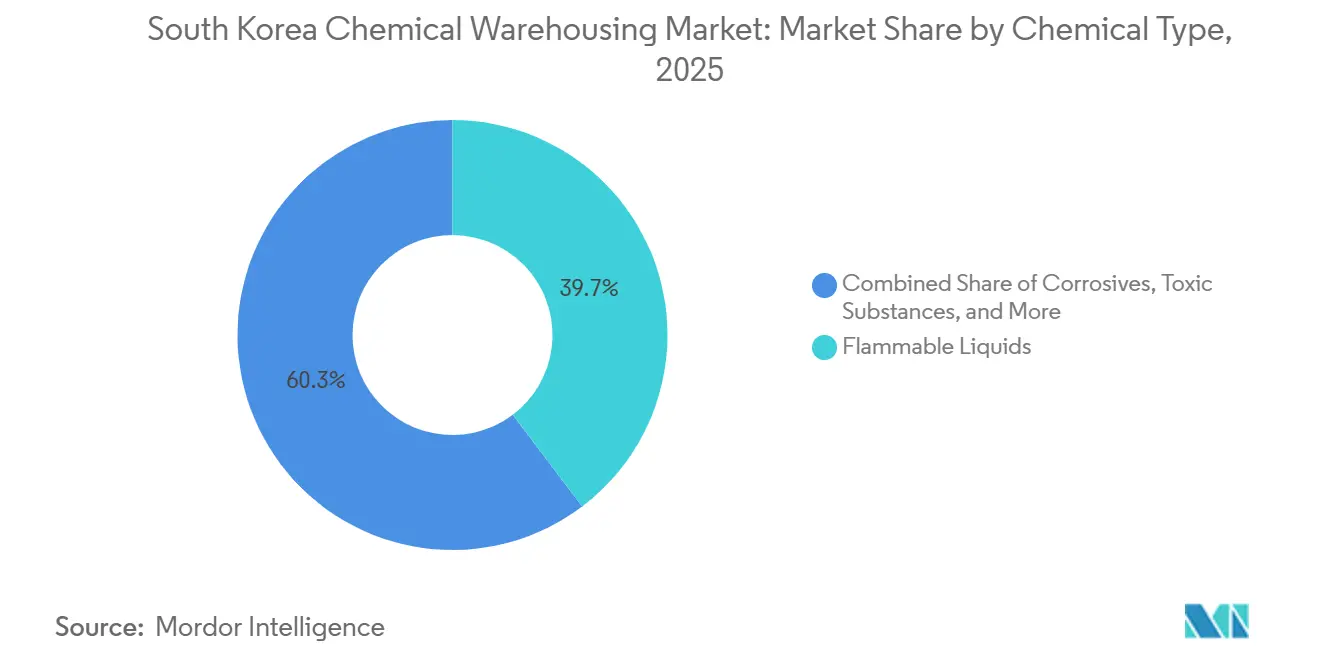

- By chemical type, Flammable Liquids accounted for 39.52% share of the South Korea chemical warehousing market size in 2025, Toxic Substances are projected to grow at a 4.70% CAGR between 2026-2031.

- By end user, Specialty Chemicals Manufacturing held 31.77% share of the South Korea chemical warehousing market size in 2025, while Pharmaceuticals & Life Sciences is advancing at a 5.35% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South korea contributes to a system defined not by any single country or region but by the interaction of many. The global chemical warehousing market data by Mordor Intelligence represents that combined structure.

South Korea Chemical Warehousing Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV battery-precursor boom needing ultra-dry storage | +0.9% | Chungcheong, Gyeonggi | Medium term (2-4 years) |

| Hydrogen-ammonia bunkering build-out at coastal eco-fuel hubs | +0.7% | Busan, Ulsan, and Incheon port zones | Long term (≥ 4 years) |

| Reshoring tax incentives driving SME fine-chemical clusters | +0.6% | Ochang, Sejong, Gwangju | Medium term (2-4 years) |

| Government AI-Smart Logistics subsidy program for hazmat DCs | +0.5% | National, Seoul Capital Area | Short term (≤ 2 years) |

| Sea-rail intermodal corridor expansion lowering coastal warehouse costs | +0.5% | Busan-Seoul, Gwangyang-Daejeon | Long term (≥ 4 years) |

| Mandatory IoT-based digital safety logbooks under the 2025 CCA revision | +0.4% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

EV Battery-Precursor Boom Needing Ultra-Dry Storage

Domestic electrolyte-salt production requires warehouses with relative humidity below 1%, pushing facility costs to USD 800-1,200 per square meter. Utilization in Chungcheong and Gyeonggi ultra-dry buildings already exceeds 95% because LG Energy Solution, SK On, and Samsung SDI have locked in long-term contracts for precursor inputs. Operators who finance high-grade desiccant, nitrogen-blanket, and dew-point monitoring systems command rental premiums near 80% over conventional space.

Hydrogen-Ammonia Bunkering Build-Out at Coastal Eco-Fuel Hubs

South Korea’s maritime-fuel roadmap requires ammonia-capable bunkering infrastructure at five major ports by 2030. Ports in Busan and Ulsan are already approving terminals that store cryogenic ammonia at -33 °C, a specification that raises demand for purpose-built chemical warehouses within two kilometers of berths to control pipeline length and safety risk. Operators must satisfy both the Chemical Control Act and Korea Coast Guard rules, which increases compliance complexity but limits new entrants. Early movers such as the joint venture between MOL Chemical Tankers and SK Gas have secured long-term leases near bunkering jetties, positioning for a projected USD 2 billion ammonia-fuel logistics market by 2035.

Reshoring Tax Incentives Driving SME Fine-Chemical Clusters

Expanded 2024 tax credits now cover fine chemicals, offering up to a 10-year corporate tax holiday for firms relocating production from China. Seventeen manufacturers have announced moves that together require 85,000 m² of certified storage, much of it within the Ochang and Sejong industrial zones. Shared third-party logistics (3PL) warehouses appeal to small and midsize enterprises (SMEs) lacking capital for stand-alone facilities, especially where semiconductor precursor storage demands Class 10 000 cleanroom specifications priced 60-80% above standard space. Clustering raises utilization rates and allows warehouse providers to amortize contamination-control systems across multiple tenants.

Government AI-Smart Logistics Subsidy Program for Hazmat DCs

The Ministry of Trade, Industry & Energy subsidizes up to 50% of spending on AI-powered safety, including computer-vision leak detection and digital-twin emergency modeling. Mid-tier operators have adopted systems that cut incident rates by roughly 25% and lift pallet density by roughly 15% through algorithmic stacking that considers chemical-compatibility tables. Interoperability requirements ensure that new platforms can link with legacy warehouse-management systems, reducing vendor lock-in risk and speeding scale-up.[2]Ministry of Trade, Industry & Energy, “Smart Logistics Subsidy Guidelines,” motie.go.kr

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Peak-hour electricity tariff volatility hitting cold & controlled warehouses | –0.7% | National, Seoul Capital Area | Short term (≤ 2 years) |

| Spiking marine-cargo insurance premiums post-2025 Busan spill | –0.6% | Coastal zones, export facilities | Short term (≤ 2 years) |

| Approval bottlenecks for new Seveso-tier chemical safety zones | –0.5% | Metropolitan areas | Medium term (2-4 years) |

| Price-war fragmentation among uncertified niche 3PL providers | –0.4% | National, secondary markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Peak-Hour Electricity Tariff Volatility Hitting Cold & Controlled Warehouses

Dynamic time-of-use pricing can push peak tariffs to 3.5 times off-peak rates, pushing energy costs to 30% of operating costs in cold, ultra-dry facilities. Operators install battery energy storage and high-efficiency refrigeration to shave peak-hour demand, but the capital intensity raises payback risk. Some pass charges to customers through variable storage fees, while others absorb costs to protect market share.

Spiking Marine-Cargo Insurance Premiums Post-2025 Busan Spill

Heightened regulatory scrutiny and global risk reassessments by marine underwriters are driving up hazmat premiums, with many insurers now demanding strict third-party safety audits before renewal. For small operators, these rising insurance costs, now reaching roughly 5% of revenue, are tightening margins and prompting some to exit high-risk chemical categories. Concurrently, environmental regulators are intensifying safety protocols and inspection frequencies for warehouses near sensitive waterways, adding significant compliance burdens for coastal operators.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Warehouse Type: Premium Ultra-Dry Facilities Redefine Value Proposition

Specialty Chemical Warehouses captured 38.80% of South Korea chemical warehousing market share in 2025 on the strength of electronics, semiconductor, and advanced-material clients. The sub-segment houses cleanrooms, contamination-control zones, and integrated quality labs that meet ISO 14644 standards. Operators such as CJ Logistics and Rinchem have invested in class-based zoning and AI temperature alarms, supporting just-in-time (JIT) delivery for photolithography chemicals used in 5-nm chip production. Although general chemical warehouses still command volume, their share is slipping as customers shift toward higher-specification space that includes IoT safety dashboards and value-added packaging lines.

Temperature-Controlled Chemical Warehouses are projected to post a 5.58% CAGR, the fastest within this segmentation. Growth stems from lithium salt, electrolyte, and biologics logistics, each demanding either ultra-dry atmospheres or deep-frozen bays down to -80 °C. The South Korea chemical warehousing market size for temperature-controlled sites is forecast to reach USD 710 million by 2031 as energy-storage retrofits make peak-hour power more manageable. Samsung SDI’s Cheonan battery plant requires dew points below -40 °C, showcasing how technical specs drive premium lease rates.

By Chemical Type: Flammable Liquids Dominate but Toxic Substances Grow Faster

Flammable Liquids held a 39.52% share of the South Korea chemical warehousing market size in 2025, reflecting the country’s petrochemical complex and new hydrogen-ammonia blends that need pressurized or cryogenic tanks. Commodity naphtha and xylene face price pressure, however, so average storage yields are flattening. Warehouse operators respond by bundling services such as tank-to-drum decanting and customs brokerage to preserve margin.

Toxic Substances are forecast to expand at 4.70% CAGR as pharmaceutical active-ingredient (API) and battery electrolyte production relocate from China. Facilities storing lithium hexafluorophosphate (LiPF6) require inert-gas blanketing and corrosion-resistant flooring, adding USD 200-400 per square meter to build cost. The South Korea chemical warehousing market share for toxic substances is set to climb because GMP-compliant APIs and high-value cathode powders carry higher storage fees. LG Energy Solution’s new LiPF6 line illustrates the upswing, having contracted a purpose-built, moisture-free warehouse near Ochang.

By End-User Industry: Specialty Chemicals Lead, Pharma Surges

Specialty Chemicals Manufacturing accounted for 31.77% of South Korea chemical warehousing market share in 2025, underpinned by semiconductor photoresists, display panel materials, and UV-curable resins. These clients require ISO-class zones, static-free flooring, and chemical-compatibility segregation, allowing operators to charge premiums of 25-40% over bulk petrochemical rates. Integrated vendor-managed inventory (VMI) programs further tether customers to value-added 3PLs.

Pharmaceuticals & Life Sciences are projected to grow at a 5.35% CAGR, fastest among end users, as biopharmaceutical contract development and manufacturing organizations (CDMOs) expand. New cell-therapy projects need cold-chain warehouses with power redundancy, alarmed dual compressors, and full audit trails for regulators. The South Korea chemical warehousing market size linked to pharma is lifting because companies such as Samsung Biologics depend on validated −80 °C storage for plasmid DNA and viral vectors, creating sticky, long-term contracts.[3]Ministry of Trade, Industry & Energy, “Smart Logistics Subsidy Guidelines,” motie.go.kr

Geography Analysis

Greater Seoul anchors roughly 40% of national demand despite high land prices, because electronics, biotech, and fine-chemical clusters prize proximity to R&D centers and export airports. Gyeonggi Province stands out as the fastest-growing geography with battery-related projects alone requiring more than 100,000 m² of ultra-dry space; utilization already approaches saturation in Anseong and Pyeongtaek corridors.

Chungcheong’s industrial belt ranks second in share and benefits from government incentives that offset relocation costs for reshorers; Ochang and Sejong complexes attract SMEs looking for shared warehousing that meets both CCA and GMP rules. Rail upgrades shorten transit to Busan Port, letting operators base inventory inland without sacrificing export turn-times.

The southeast coastal strip, home to Ulsan and Busan petrochemical plants, supports bulk flammable-liquid storage and is gradually adding ammonia-fuel infrastructure. Permitting delays stemming from tightened coastal environmental regulations have slowed new builds, yet comprehensive safety retrofits and containment upgrades are steadily underway across major port sites like Ulsan and Busan. Secondary regions such as Daegu and Gwangju offer favorable land costs but struggle to attract hazmat-certified technicians, keeping growth moderate.[4]Korea Trade-Investment Promotion Agency (KOTRA), “Invest Korea: Industrial Clusters & Logistics,” kotra.or.kr

The chemical warehousing market is analyzed by Mordor Intelligence across multiple other geographies, with in-depth regional assessments available for Europe, Middle East, and Africa. This is complemented by country-specific insights for China, India, France, Canada, Mexico, and United Kingdom, reflecting various localized market behavior and policy environments' coverage.

Competitive Landscape

Competition remains fragmented. Global firms like DHL Supply Chain, DSV, and CEVA import standardized quality protocols and global multi-client contracts, appealing to multinational manufacturers. Domestic champions such as CJ Logistics and Dongryun leverage local knowledge to navigate permitting and labor rules, giving them speed advantages in expansion.

Strategic bets now center on automation and specialization. Major domestic 3PLs like CJ Logistics are actively exploring investments in AI-equipped distribution centers and expanding their footprint in regions like Gyeonggi and Chungcheong to anticipate rising battery-precursor flows. Meanwhile, global forwarders are deepening their coastal liquids networks to capture export-linked petrochemicals, and expanding their pharma-cold-chain footprint in biopharma hubs like Songdo to lock in long-term capacity and diversify revenue.

Midsize players hedge against energy and compliance costs via strategic partnerships, particularly in high-barrier segments like ultra-dry battery storage. Technology adoption is also rising across the board, with operators deploying blockchain traceability for hazmat freight and securing ISO 14001 certifications to woo customers with sustainability mandates. Consolidation pressure will persist as IoT, insurance, and energy costs reward operators that can spread fixed charges across multi-site portfolios.

South Korea Chemical Warehousing Industry Leaders

CJ Logistics

LX Pantos

Rinchem Company, Inc.

Kukbo Express

Dongryun Logistics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Lotte Global Logistics collaborated with robotics firm Robros and multiple South Korean academic institutions (Kyunghee, Kwangwoon, and Sogang Universities). The partnership focuses on the field demonstration and deployment of bipedal AI Humanoid Robots at the company's Jincheon fulfillment center. The initiative aims to accumulate operational data and train the robots for complex outbound and packaging tasks, signaling a major push toward automating highly regulated domestic warehouse environments.

- March 2026: Lotte Global Logistics officially initiated field demonstrations of bipedal AI Humanoid Robots specifically designed for complex logistics environments. Partnering with the robotics firm Robros, alongside research teams from Kyunghee University, Kwangwoon University, and Sogang University, the company announced plans to deploy these autonomous units at its Jincheon fulfillment center. The initiative focuses on training the robots to execute outbound processing and specialized packaging tasks, allowing Lotte to accumulate critical operational data to accelerate the automation of its domestic warehousing and supply chain infrastructure.

- February 2026: Rinchem launched its 50th-anniversary initiative. The corporate update highlighted its ongoing strategic focus on operational discipline in regulated chemical and gas logistics. The company emphasized its continued commitment to zero-compromise safety standards across its hazardous materials warehousing, specialized transportation, and ISO tank handling networks, which directly support the world's most demanding semiconductor manufacturing environments.

- November 2025: LX International, the parent conglomerate of top-tier domestic 3PL LX Pantos, finalized the acquisition of IT service company BSG Partners. This strategic acquisition was executed to directly enhance the digital supply chain and operational capabilities of its logistics network. By integrating BSG Partners' specialized SAP and AWS-based solutions, LX Pantos aims to drive digital transformation, improve system implementation, and increase tracking efficiency across its extensive industrial and petrochemical logistics operations.

South Korea Chemical Warehousing Market Report Scope

| General Warehousing |

| Specialty Chemical Warehouse |

| Hazardous Materials (HAZMAT) Warehouses |

| Temperature-Controlled Chemical Warehouses |

| Flammable Liquids |

| Corrosives |

| Toxic Substances |

| Oxidizers |

| Others |

| Basic Chemicals Manufacturing |

| Specialty Chemicals Manufacturing |

| Pharmaceuticals & Life Sciences |

| Agrochemicals |

| Paints, Coatings & Adhesives |

| Food & Feed Additives |

| Oil & Gas / Petrochemicals |

| Others |

| By Warehouse Type | General Warehousing |

| Specialty Chemical Warehouse | |

| Hazardous Materials (HAZMAT) Warehouses | |

| Temperature-Controlled Chemical Warehouses | |

| By Chemical Type | Flammable Liquids |

| Corrosives | |

| Toxic Substances | |

| Oxidizers | |

| Others | |

| By End-user Industry | Basic Chemicals Manufacturing |

| Specialty Chemicals Manufacturing | |

| Pharmaceuticals & Life Sciences | |

| Agrochemicals | |

| Paints, Coatings & Adhesives | |

| Food & Feed Additives | |

| Oil & Gas / Petrochemicals | |

| Others |

Key Questions Answered in the Report

How large will South Korea’s chemical warehousing market be by 2031?

The sector is forecast to reach USD 2.18 billion by 2031, expanding at a 3.45% CAGR from 2026.

Which warehouse type is growing the fastest?

Temperature-Controlled Chemical Warehouses, driven by battery-material and pharma cold-chain demand, are set for a 5.58% CAGR through 2031.

What is the main driver behind ultra-dry storage demand?

Domestic production of battery precursors and electrolyte salts needs facilities held below 1% relative humidity to prevent material degradation.

How are new CCA rules affecting operators?

The 2025 revision mandates IoT safety logbooks, increasing capital spending but enabling data-driven insurance discounts for compliant firms.

Why are insurance costs rising for coastal warehouses?

The 2025 Busan chemical spill led insurers to tighten risk criteria and lift hazmat premiums by up to 40%, particularly for export-linked facilities.

Which regions are attracting the newest capacity?

Gyeonggi and Chungcheong provinces lead in new builds due to battery and fine-chemical investments, while coastal hubs focus on ammonia bunkering upgrades.

Page last updated on: