Africa Chemical Warehousing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

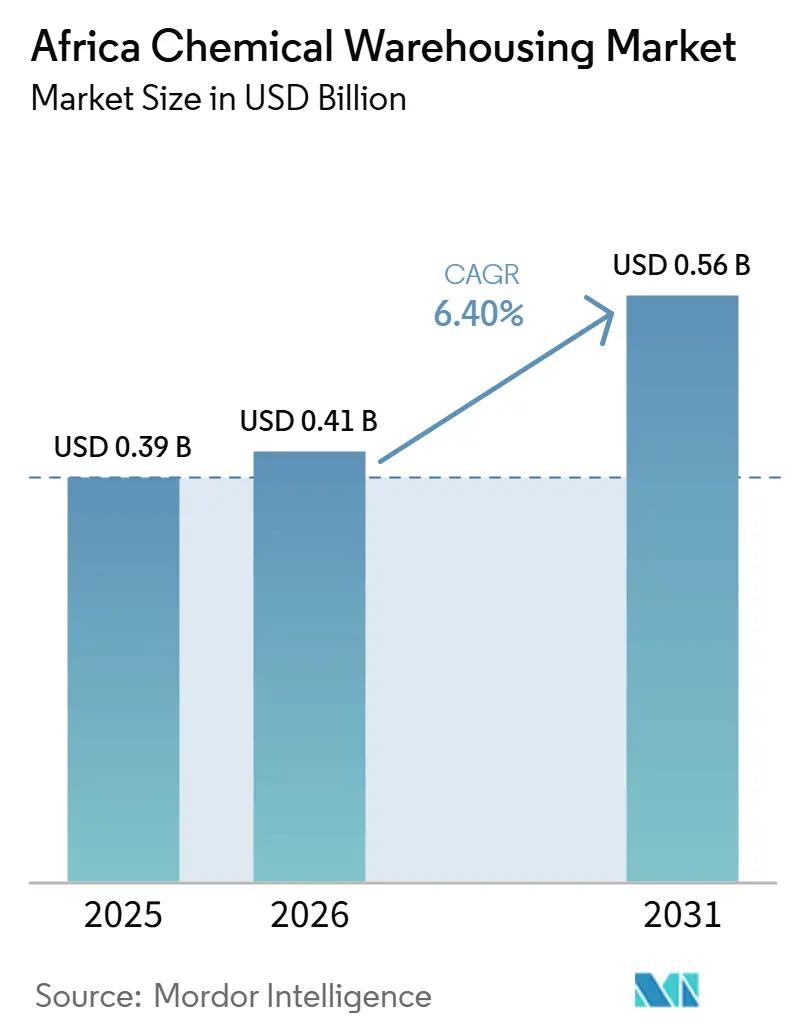

| Base Year Market Size (2025) | USD 0.39 Billion |

| Market Size (2026) | USD 0.41 Billion |

| Market Size (2031) | USD 0.56 Billion |

| Growth Rate (2026 - 2031) | 6.40% CAGR |

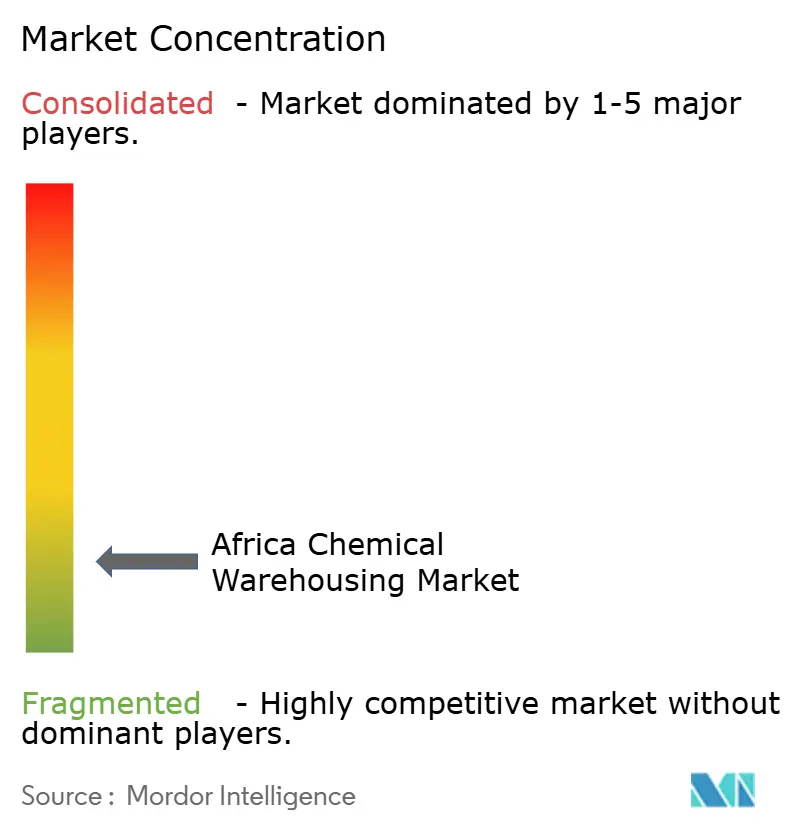

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Africa Chemical Warehousing Market Analysis by Mordor Intelligence

The Africa Chemical Warehousing Market size was valued at USD 0.39 billion in 2025 and is estimated to grow from USD 0.41 billion in 2026 to reach USD 0.56 billion by 2031, at a CAGR of 6.40% during the forecast period (2026-2031).

The Africa chemical warehousing market is benefiting from industrial policy momentum, including active port-led investments and logistics upgrades that raise standards for hazardous materials handling and temperature-controlled storage for active pharmaceutical ingredients and agrochemicals. Harmonized safety frameworks for labeling, monitoring, and transport compliance are setting new baselines in South Africa’s hubs, and they are influencing procurement criteria across neighboring markets. As AfCFTA implementation removes most tariff barriers across 54 countries, demand increases for certified storage nodes tied into regional corridors that can manage cross-border flows of reagents, solvents, and intermediates to manufacturing and mining clusters. The Africa chemical warehousing market is also lifted by upstream refinery and petrochemical expansions that require compliant tank farms and bonded storage at or near high-capacity gateways. Investments in deep-water and logistics platforms are enabling operators to bundle value-added services with visibility tools, which improve resilience for temperature-sensitive and hazardous inventories.

Key Report Takeaways

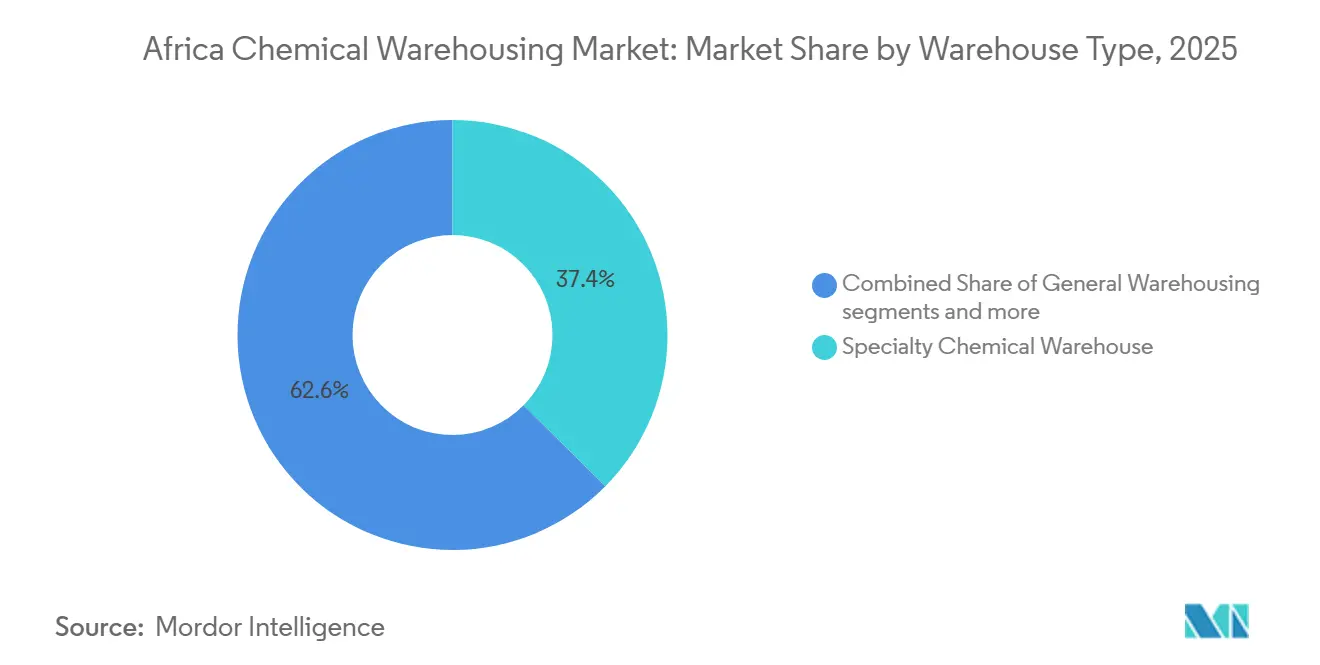

- By warehouse type, specialty chemical warehouses led with 37.41% share in the Africa chemical warehousing market size in 2025, while temperature-controlled chemical warehouses are forecast to expand at a 6.74% CAGR through 2031.

- By chemical type, flammable liquids accounted for 40.14% of Africa chemical warehousing market share in 2025, while toxic substances recorded the highest projected CAGR at 7.21% through 2031.

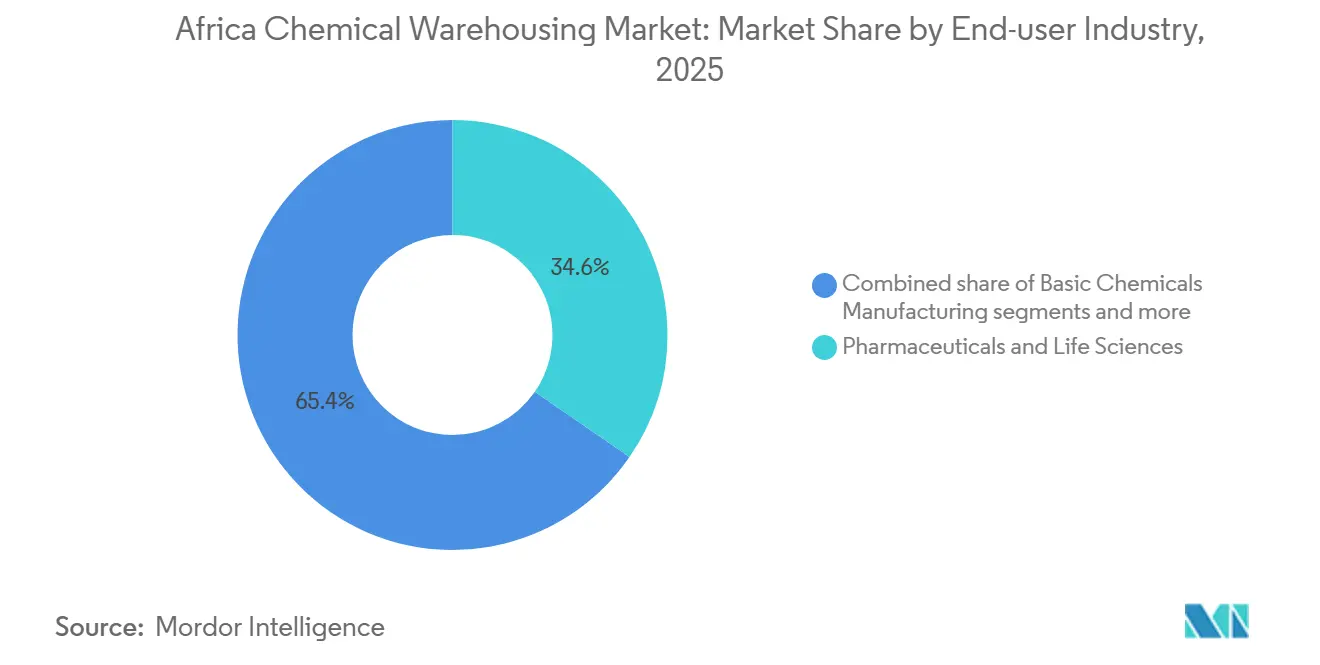

- By end-user industry, pharmaceuticals & life sciences captured 34.61% share in 2025 and is advancing at a 7.42% CAGR through 2031.

- By geography, South Africa commanded 38.14% share in 2025, while Kenya is projected to grow at a 7.54% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Figures recorded within Africa feed into a worldwide estimate while studying the global industry. Mordor Intelligence's chemical warehousing market size captures this aggregation.

Africa Chemical Warehousing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mining sector chemical demand growth | +1.2% | South Africa, DRC, Zambia, Ghana | Medium term (2-4 years) |

| Agricultural input market expansion | +1.5% | Morocco, Nigeria, Ethiopia, Kenya | Long term (≥ 4 years) |

| Oil and gas sector development | +1.3% | Nigeria, Algeria, Angola | Long term (≥ 4 years) |

| Manufacturing sector diversification | +1.0% | South Africa, Egypt, Morocco, Kenya, Ethiopia | Medium term (2-4 years) |

| Port infrastructure modernization | +0.9% | Durban, Mombasa, Lagos, Dakar, Dar es Salaam | Long term (≥ 4 years) |

| Pharmaceutical manufacturing localization | +0.5% | ECOWAS, East Africa, South Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mining Sector Chemical Demand Growth

The African Union’s Green Minerals Strategy shows that mines consume significant quantities of explosives, reagents, cyanide, and related chemical inputs after fuel, lubricants, and power, reinforcing the need for specialized storage at mine-adjacent and port-proximate depots. In South Africa, basic chemical input costs rose in 2025 alongside double-digit increases in electricity and water tariffs, which encouraged mining operators to maintain buffer stocks of sulfuric acid, hydrochloric acid, sodium hydroxide, and chlorine to avoid disruptions. These cost and reliability dynamics increase the role of compliant warehouses capable of segregating corrosives and toxics while supporting steady outbound flows to concentrators and smelters. South Africa’s heavy-haul rail supports long-distance movement of bulk liquids and hazardous cargoes tied to mining value chains, aligning with storage networks around Gauteng and KwaZulu-Natal.[1]Minerals Council South Africa, “Mining Input Cost Inflation December Full Year 2025,” mineralscouncil.org.za As mines process lower-grade ores, their reagent intensity increases, which sustains demand for capacity with robust ventilation, secondary containment, and incident response standards in the Africa chemical warehousing market. This supports a steady pipeline of upgrades to warehousing layouts and monitoring systems to manage higher turnover and maintain SHEQ compliance across corridors.

Agricultural Input Market Expansion

Large-scale investments in nitrogen and ammonia-urea capacity in West Africa are expanding the regional supply base for fertilizer inputs and driving demand for compliant storage of urea, ammonia, and methanol, including segregation and inventory controls suited to oxidizers and toxics. As AfCFTA eliminates tariffs on most goods, cross-border flows of agrochemicals are expected to rise, which shifts warehousing footprints toward integrated, corridor-based nodes linked to major ports and inland gateways.[2]Investment and Financial Authority of Ethiopia, “AfCFTA: Unlocking Africa’s Trade Potential,” ifa.gov.et Port-side liquid bulk capacity that can flex between edible oils and chemical cargoes supports agribusinesses that need both ambient and hazardous storage with strict hygiene and spill-control protocols. In Kenya, new special economic zones near Mombasa and in geothermal-powered Olkaria are designed to attract agro-processing, which raises the requirement for temperature-controlled and humidity-managed facilities for crop protection products. These trends favor operators that can pair cold-chain capabilities with regulatory documentation for dangerous goods to serve seasonal surges and port-to-inland distribution in the Africa chemical warehousing market. Compliance architectures that integrate labeling, monitoring, and emergency response help align agricultural chemical storage with evolving standards in key markets.[3]Department of Employment and Labour, “Regulations for Hazardous Chemical Agents,” gov.za

Oil and Gas Sector Development

The expansion of refinery and petrochemical output in Nigeria is set to increase feedstocks and intermediates that require hazardous storage, with plans to raise refining capacity to 1.4 million barrels per day and add 750,000 tonnes per year of propylene for polymer production using Oleflex technology. Nigeria’s domestic refineries have remained offline, which has sustained import reliance and increased the need for tank farms and certified warehousing at Lagos, Port Harcourt, and Warri to manage product flows and inventory resilience. South Africa’s regulatory updates, including the adoption of GHS Revision 10 and mandates for air and biological monitoring at hazardous sites, are strengthening compliance and documentation around chemical storage and handling. Port operators are investing in assets across Dakar, Dar es Salaam, and Banana to support the throughput of flammable and corrosive cargoes, complementing logistics platforms that stitch storage with inland transport. Multimodal pilots modeled on secure rail corridors with enhanced container locks illustrate how operators can reduce risk exposure for hazardous cargo within the Africa chemical warehousing market.

Manufacturing Sector Diversification

Kenya’s Olkaria Special Economic Zone, announced in 2025, is leveraging geothermal power and rail connectivity to attract green manufacturing and agro-processing, which requires specialized storage for solvents, catalysts, and additives used in local production. Multinational producers are localizing formulations and intermediates, as seen in the 2026 expansion of a dispersions facility in Durban that serves coatings, construction materials, and paper across East, West, and Southern Africa, which lifts demand for compliant storage near port and urban hubs. Rail-linked bulk liquids services are bolstering long-haul movements for caustic soda, methanol, ethanol, and acids to large plants and downstream converters, and that aligns with the need for flexible warehousing footprints near sidings and terminals. Safety frameworks and certification schemes, including SQAS-AFRICA audits of warehousing and spill response, are being used by multinational clients as qualifying criteria for long-term contracts. These mechanisms encourage investments in fire suppression, controlled access, and digital traceability that support consistent quality and performance for the Africa chemical warehousing market. Industrial policies and zone-level incentives are reinforcing these dynamics across focal markets that pair reliable power with port proximity and rail access.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inadequate infrastructure and logistics networks | -1.1% | Sub-Saharan Africa, landlocked corridors | Long term (≥ 4 years) |

| Regulatory fragmentation and weak enforcement | -0.7% | West, Central, and parts of East Africa | Medium term (2-4 years) |

| Shortage of specialized warehousing facilities | -0.6% | Secondary cities and interior markets | Short term (≤ 2 years) |

| High import dependency and forex volatility | -0.5% | Broadly across markets with import reliance | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Inadequate Infrastructure and Logistics Networks

Infrastructure gaps and climate exposure generate sustained costs and delays, with average annual losses linked to climate-related events that weigh on the financial performance of transport and storage operations. These conditions magnify risks for hazardous cargo, where delays increase safety and compliance burdens in port yards and inland depots that are not designed for prolonged dwell. Multimodal pilots that shift volume toward rail with enhanced container security can reduce exposure on long-haul routes, but these networks remain nascent outside select corridors. High import reliance on fuel and feedstocks in major hubs sustains the need for tank farms and specialized storage capacity, while also increasing sensitivity to exchange rate swings that affect inventory financing. These systemic hurdles slow the diffusion of advanced warehousing technologies and limit redundancy in secondary cities that the Africa chemical warehousing market will need as regional trade grows.

Regulatory Fragmentation and Weak Enforcement

South Africa’s adoption of GHS Revision 10 and detailed mandates for labeling, monitoring, and transport demonstrate how coherent frameworks raise the baseline for hazardous materials, while many neighboring markets still operate under patchwork standards. The SQAS-AFRICA audit system sets unified expectations for warehousing, tank cleaning, transport, and emergency response, and signals quality to multinational buyers seeking consistent standards. However, variation across jurisdictions in documentation, inspections, and fees requires operators to tailor compliance and invest in training and systems, which raises the cost to scale networks across borders in the Africa chemical warehousing market. Global carriers maintain conformity with IMDG, IATA, ADR, and other codes, yet note that adapting to local frameworks is necessary where national rules diverge from international practice. This mismatch increases administrative workload and can complicate service design for dangerous goods and cold-chain distribution across fragmented regulatory environments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Warehouse Type: Specialization Drives Differentiation

Specialty Chemical Warehouses accounted for 37.41% in 2025, reflecting a clear shift toward compliance-intensive storage that supports higher value products across formulations, additives, and polymers in the Africa chemical warehousing market. Temperature-Controlled Chemical Warehouses are projected to grow at 6.74% during 2026-2031 as pharma localization and agrochemical handling standards push demand for validated cold rooms and humidity control, and the Africa chemical warehousing market size for this segment is expected to expand at a 6.74% CAGR through 2031. Hazardous Materials facilities remain essential for flammables, oxidizers, and toxics, particularly where national standards reference classification, packaging, and emergency response codes aligned with international benchmarks. SQAS-AFRICA certification is being used by leading shippers to screen providers that can maintain safe operations for dangerous goods across handling, storage, and incident response. In parallel, general warehousing continues to serve ambient commodities, though margins face pressure as clients require segregation, fire suppression, and access control that exceed legacy footprints in secondary cities. The Africa chemical warehousing industry is therefore favoring facilities that combine automation with audit-ready processes to win long-term contracts from multinationals.

Over 2026-2031, the mix is expected to tilt toward specialty and temperature-controlled sites as AfCFTA supports intra-regional distribution of APIs, excipients, and high-spec agrochemicals that rely on certified chains of custody. New SEZs in Kenya, alongside rail-linked terminals in South Africa, illustrate how policy and infrastructure combine to attract chemical-intensive manufacturing that requires compliant storage models near ports and rail. Port-adjacent liquid bulk terminals, such as Durban’s 100,000 cubic meters of capacity, also reinforce a broader hub-and-spoke approach to inventory positioning for both edible oils and chemical cargoes. Operators that standardize labeling, monitoring, and air sampling per hazard-class rules are better positioned to meet audit requirements of global buyers in the Africa chemical warehousing market. This structure narrows the compliance gap and shifts procurement toward certified providers that integrate safety with visibility and data capture for sensitive cargo.

By Chemical Type: Flammable Liquids Dominate, Toxics Accelerate

Flammable Liquids held 40.14% in 2025, anchored by rising refinery and petrochemical activity and the transport intensity of solvents, fuels, and feedstocks in the Africa chemical warehousing market. Toxic Substances are projected to record a 7.21% CAGR through 2026-2031, reflecting rising reagent use in mining and more complex pharmaceutical and specialty chemical inventories that rely on segregated and monitored storage. Petrochemical expansions in Nigeria add to volumes of propylene and downstream polymers, which pull in associated feedstocks and drive tank farm and HAZMAT warehouse utilization near major ports. Regulatory standards in South Africa formalize classification and handling rules, including documentation and biennial monitoring requirements, which support investment in compliant facilities. Rail-suitable solutions with enhanced container security are expanding options for hazardous cargo transport across select corridors, complementing storage networks and improving chain-of-custody integrity. These use cases expand the scope of warehousing technologies, including controlled ventilation and floor coatings for corrosives, and increase digital monitoring for the Africa chemical warehousing market.

The forecast mix suggests that flammables will sustain leadership given feedstock and product flows tied to downstream projects, while toxics gain share as localization in pharma and specialized mining chemicals increases. Oxidizers and corrosives require strict segregation and secondary containment, which influences layout design and sprinkler choices in new-builds and retrofits in the Africa chemical warehousing market. South Africa’s enforcement posture, including labeling, SDS, and monitoring mandates, supports tighter operational discipline and strengthens the documentation trail for regulated cargo. With multinational manufacturers adding capacity in regional hubs like Durban, storage class diversification is rising, and operators are aligning with customer audits that emphasize traceability and incident preparedness. The Africa chemical warehousing industry will continue to reward providers that maintain disciplined separation by hazard class and offer visibility tools as standard features for compliance-driven clients.

By End-user Industry: Pharma Leads Growth Trajectory

Pharmaceuticals & Life Sciences represented 34.61% in 2025 and is expected to expand at a 7.42% CAGR through 2026-2031 as local production objectives and procurement policies emphasize compliant storage and distribution in the Africa chemical warehousing market. DHL’s expansion of GDP-certified facilities in Johannesburg and Nairobi connects temperature-controlled warehousing with compliant transport, and that reduces handoff risks in vaccine and antibiotic supply chains. Agrochemicals remain a major demand source with new urea and ammonia-methanol complexes under development in West Africa, which require storage configured for oxidizers and regulated products. Basic chemicals activity in Nigeria and South Africa frames demand for ambient and hazardous storage near port and refinery clusters as downstream producers expand. Specialty chemicals and dispersions support coatings, construction, and paper, with multinational capacity expansions signaling long-term throughput for audited providers. The Africa chemical warehousing market size for Pharmaceuticals & Life Sciences is projected to expand at 7.42% over 2026-2031 as localization and regulatory alignment deepen.

Across end uses, audited storage is becoming a procurement prerequisite, and operators that demonstrate robust quality systems and SQAS-AFRICA credentials gain an advantage in multi-year awards. Oil and gas, petrochemicals, and fuels will sustain flammable liquid demand for tank farms and HAZMAT-certified facilities, particularly near major ports, with continued import reliance maintaining throughput needs in Nigeria. Agrochemicals and basic chemicals continue to require mixed portfolios of ambient and hazardous capacity matched to corrosion protection and spill response, which intensifies focus on equipment and staff training investments in the Africa chemical warehousing market. Food-grade additives and related inputs require documented quality systems and hygiene protocols that align with customer audits in export-facing facilities. The Africa chemical warehousing industry will reward operators that pair regulatory compliance with dependable multimodal links that shorten lead times and improve predictability for downstream users.

Geography Analysis

South Africa held 38.14% in 2025, supported by new liquid bulk capacity in Durban of 100,000 cubic meters dedicated to chemicals and edible oils, which achieved high pre-lease levels before commissioning and signaled stable demand for port-proximate storage. The country continues to attract multinational investments in chemicals manufacturing, including a 2026 dispersions expansion in Durban that serves multiple subregions, which sustains demand for certified storage close to production and export nodes. South Africa’s regulatory framework for hazardous chemical agents, aligned with GHS Revision 10 and reinforced by monitoring obligations, sets a strong baseline for compliance at scale in the Africa chemical warehousing market. Kenya is projected to grow at 7.54% over 2026-2031, anchored by its new SEZs in Vipingo and Olkaria that connect manufacturing to Mombasa by rail and highway, a structure that favors audited storage providers with cold-chain and hazardous capabilities. DHL’s GDP-certified hub in Nairobi complements this structure with compliant storage and temperature-controlled distribution, reinforcing Kenya’s role as a pharma logistics center for East Africa. Nigeria’s upstream activity expansion and polymer output growth create a need for flexible tank farms and hazardous storage near Lagos and Port Harcourt, while offline state refineries sustain import reliance and associated storage utilization.

In Morocco, phosphate-linked chemical value chains drive storage for acids, fertilizers, and related intermediates, supported by integrated port platforms at industrial sites, which channel throughput to audited facilities in the Africa chemical warehousing market. Ethiopia’s manufacturing policy priorities continue to expand demand for chemical inputs across cement and processing lines, reinforcing needs for compliant storage and rail-connected hubs, supported by national industrial platforms and state holdings. Algeria’s petrochemical ambitions require secure inventories of flammable and corrosive intermediates across refineries and crackers coming online in the medium term, which elevates the importance of port-adjacent storage nodes to support commissioning and steady-state operations. The rest of Africa includes new and expanding assets across East and West Coast gateways, as port and corridor upgrades aim to reduce dwell times and synchronize storage with inland distribution in the Africa chemical warehousing market. Together, these geographies reflect a concentration of certified capacity in South Africa and an acceleration path in Kenya and Nigeria, where policy, investment, and demand intersect to shape warehousing footprints.

Comparing market dynamics, South Africa leverages a dense base of audited logistics providers and rail-linked bulk movement, which underpins resilient service levels at ports and metropolitan hubs. Kenya’s zones policy, geothermal power, and corridor connectivity position it to scale pharma and agro-processing storage that aligns with GDP and hazardous materials standards in the Africa chemical warehousing market. Nigeria’s focus on downstream value capture intensifies throughput for flammable and corrosive cargo near Lagos, which raises the premium on audited facilities with robust fire protection, access control, and monitoring. In the rest of the region, operators that can link compliant storage to emerging rail corridors and secure port platforms can differentiate on reliability and safety performance for cross-border trade in chemicals. These conditions favor providers that can document compliance and integrate digital visibility to win long-term contracts in the Africa chemical warehousing market.

Mordor Intelligence evaluates the chemical warehousing market across all key regional markets, including North America, Europe, and Middle East, with deeper country-level insights covering Germany, Canada, France, United Kingdom, Italy, and China.

Competitive Landscape

The market remains fragmented overall, although high-compliance and port-centric warehousing segments are increasingly consolidating among global and certified operators. While currently fragmented, high-compliance and port-centric segments are gradually consolidating. DHL is investing in GDP-certified Life Sciences and Healthcare facilities in Johannesburg and Nairobi and expanding specialized warehousing in South Africa, a strategy designed to lead in high-compliance verticals with premium service levels. CEVA Logistics has built a multicountry platform that integrates hazardous, temperature-controlled, and multimodal solutions, illustrated by the secure rail block train between Mozambique and Zimbabwe with enhanced container locks and documented chain-of-custody. DP World continues to invest in African gateways and logistics platforms that pair warehousing with inland access, reinforcing hub models connected to deep-water assets. These moves expand the pool of certified storage and raise the operational bar for providers across the Africa chemical warehousing market.

Niche operators are differentiating with cloud-based warehouse management systems, automated inventory controls, and upgraded fire protection, which strengthen audit readiness for multinational clients. In South Africa, SQAS-AFRICA audits extend across warehousing, transport, and spill response and are treated as a credential for supplier qualification by global buyers. Rail-linked bulk liquid services move acids, alcohols, and caustics at scale, lowering per-tonne costs and enabling higher consistency for industrial clients, particularly where road congestion and route security are constraints. In the Africa chemical warehousing market, partnerships with refiners, agrochemical producers, and pharmaceutical manufacturers are used to secure throughput for dedicated bays and to co-design storage solutions that match hazard profiles. Operators that integrate labeling, monitoring, and documentation to meet GHS requirements and client audit protocols remain best positioned to capture long-term, high-margin contracts.

Global carriers and logistics platforms note that while they comply with international dangerous goods codes, they must tailor service models to account for local rules and inspection practices. This fosters a premium tier of providers that invest in training, safety stock planning, and redundancy for critical equipment, which reduces incident risk and improves reliability. As deep-water expansions and logistics parks come online, the African chemical warehousing market will likely consolidate around audited hubs with multimodal access, validated cold rooms, and robust HAZMAT protocols. Port-centric expansions are also drawing value chains into integrated zones where warehousing connects directly to customs and inland distribution, compressing lead times for regulated cargo. Together, these moves indicate a maturing competitive field that values traceability, safety, and documented compliance.

Africa Chemical Warehousing Industry Leaders

DHL Group

BDP International

CEVA Logistics

Aramex

Rhenus Logistics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: NEXTCHEM secured a €485 (USD 570.51 million) million contract to supply licensing, process design, and critical equipment for three world-scale complexes in West Africa, covering hydrogen, ammonia, urea, and a combined ammonia-methanol unit.

- March 2026: DHL Supply Chain and Saudi Aramco launched ASMO, a joint venture that will roll out automated, AI-enabled procurement and logistics hubs for energy and chemical customers across MENA, with phased expansion into Sub-Saharan Africa.

- November 2025: Honeywell announced technology and catalysts to help expand Nigeria’s refinery capacity to 1.4 million barrels per day by 2028 and to add 750,000 tonnes per year of propylene via Oleflex, lifting total polypropylene output to 2.4 million tonnes per year.

- November 2025: DHL committed over €300 (USD 352.9 million) million to strengthen logistics in Sub-Saharan Africa, including GDP-certified Life Sciences facilities in Johannesburg and Nairobi, and expanded specialized warehousing and gateways.

Africa Chemical Warehousing Market Report Scope

The Africa Chemical Warehousing Market Report is Segmented by Warehouse Type (General Warehousing, Specialty Chemical Warehouse, Hazardous Materials (HAZMAT) Warehouses, and Temperature-Controlled Chemical Warehouses), by Chemical Type (Flammable Liquids, Corrosives, Toxic Substances, Oxidizers, and Others), by End-user Industry (Basic Chemicals Manufacturing, Specialty Chemicals Manufacturing, Pharmaceuticals & Life Sciences, Agrochemicals, Paints, Coatings & Adhesives, Food & Feed Additives, Oil & Gas / Petrochemicals, and Others), and by Geography (Nigeria, Morocco, Kenya, South Africa, Ethiopia, Algeria, and Rest of Africa). The Market Forecasts are Provided in Terms of Value (USD).

| General Warehousing |

| Specialty Chemical Warehouse |

| Hazardous Materials (HAZMAT) Warehouses |

| Temperature-Controlled Chemical Warehouses |

| Flammable Liquids |

| Corrosives |

| Toxic Substances |

| Oxidizers |

| Others |

| Basic Chemicals Manufacturing |

| Specialty Chemicals Manufacturing |

| Pharmaceuticals & Life Sciences |

| Agrochemicals |

| Paints, Coatings & Adhesives |

| Food & Feed Additives |

| Oil & Gas / Petrochemicals |

| Others |

| Nigeria |

| Morocco |

| Kenya |

| South Africa |

| Ethiopia |

| Algeria |

| Rest of Africa |

| By Warehouse Type | General Warehousing |

| Specialty Chemical Warehouse | |

| Hazardous Materials (HAZMAT) Warehouses | |

| Temperature-Controlled Chemical Warehouses | |

| By Chemical Type | Flammable Liquids |

| Corrosives | |

| Toxic Substances | |

| Oxidizers | |

| Others | |

| By End-user Industry | Basic Chemicals Manufacturing |

| Specialty Chemicals Manufacturing | |

| Pharmaceuticals & Life Sciences | |

| Agrochemicals | |

| Paints, Coatings & Adhesives | |

| Food & Feed Additives | |

| Oil & Gas / Petrochemicals | |

| Others | |

| By Country | Nigeria |

| Morocco | |

| Kenya | |

| South Africa | |

| Ethiopia | |

| Algeria | |

| Rest of Africa |

Key Questions Answered in the Report

What is the Africa chemical warehousing market growth outlook through 2031?

The Africa chemical warehousing market size is projected to reach USD 0.56 billion by 2031, expanding at a 6.4% CAGR over 2026-2031.

Which segments lead demand within the Africa chemical warehousing market?

Specialty Chemical Warehouses led in 2025 with 37.41%, and Pharmaceuticals & Life Sciences was the largest end user with 34.61%, supported by GDP-compliant cold-chain storage.

Which geographies are most important for the Africa chemical warehousing market?

South Africa led with 38.14% in 2025, while Kenya is projected as the fastest-growing at 7.54% over 2026-2031 on the back of new SEZs and corridor connectivity.

How are ports and logistics investments shaping the Africa chemical warehousing market?

New capacity in Durban, along with DP World’s investments in Dakar, Dar es Salaam, and Banana, is enabling integrated warehousing with inland access and better cargo visibility.

What regulatory updates matter most to the Africa chemical warehousing market?

South Africa’s GHS Revision 10 adoption and related monitoring mandates are raising safety and documentation standards that influence cross-border procurement and audits.

Which end-user vertical is set to grow fastest in the Africa chemical warehousing market?

Pharmaceuticals & Life Sciences is expected to grow at 7.42% during 2026-2031, driven by localization and compliant cold-chain distribution.

Page last updated on: