Japan Chemical Warehousing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

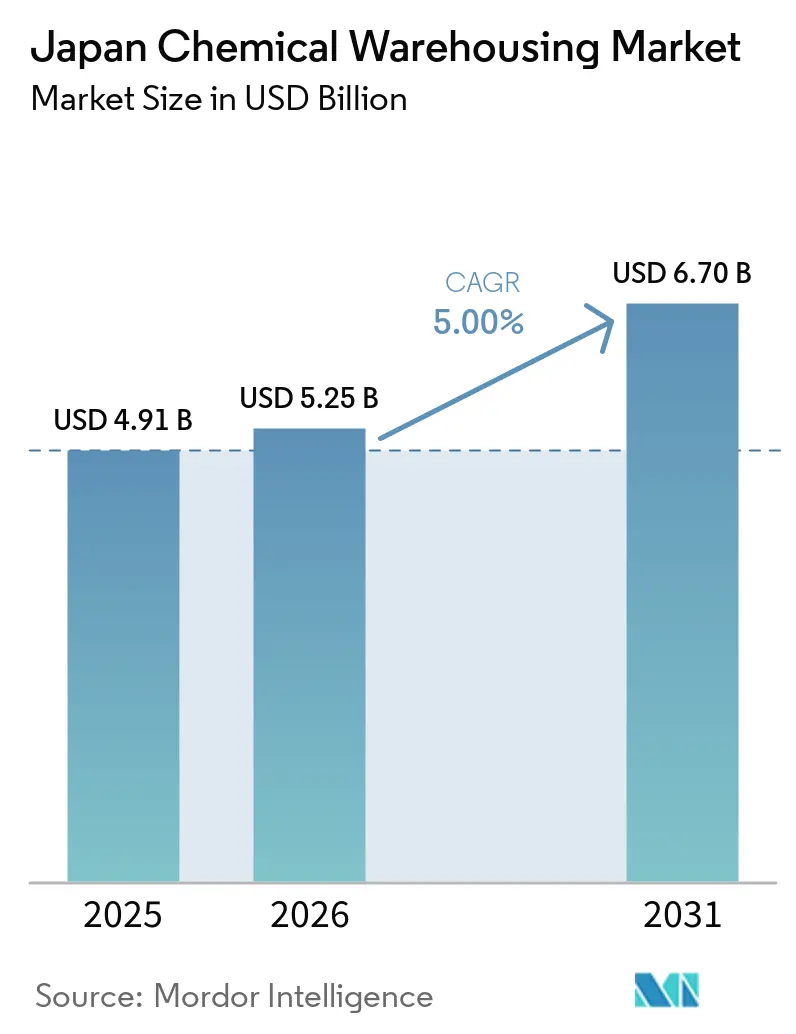

| Base Year Market Size (2025) | USD 4.91 Billion |

| Market Size (2026) | USD 5.25 Billion |

| Market Size (2031) | USD 6.70 Billion |

| Growth Rate (2026 - 2031) | 5.00% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Chemical Warehousing Market Analysis by Mordor Intelligence

The Japan Chemical Warehousing Market size is projected to expand from USD 4.91 billion in 2025 and USD 5.25 billion in 2026 to USD 6.70 billion by 2031, registering a CAGR of 5% between 2026 to 2031.

Demand is being shaped by stricter safety rules for hazardous materials, growth in advanced materials and pharmaceutical manufacturing, and fast adoption of automation to counter labor scarcity in logistics operations. HAZMAT-certified and temperature-controlled capacity are central to supporting GMP-compliant pharma and life sciences production as companies add new lines domestically. Consolidation in chemicals and the 2024 driver overtime cap are also driving a modal shift to rail and joint freight schemes, which are raising the role of intermodal hubs and standardized safety infrastructure. Operators are investing in robotics, AI-enabled WMS, and validated climate control as labor markets tighten and compliance costs rise across designated hazardous-material categories.

Key Report Takeaways

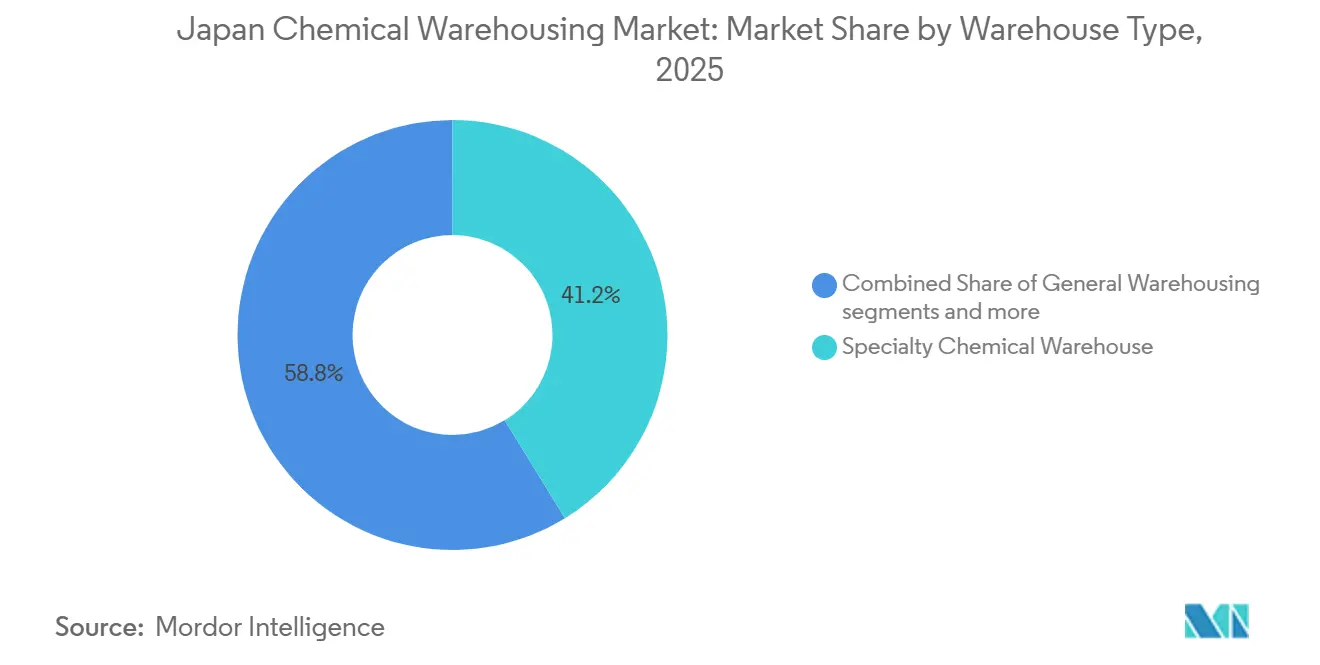

- By warehouse type, specialty chemical warehouses led with 41.24% of the Japan chemical warehousing market share in 2025. Temperature-controlled chemical warehouses are projected to expand at a 5.78% CAGR through 2031, outpacing all other warehouse categories.

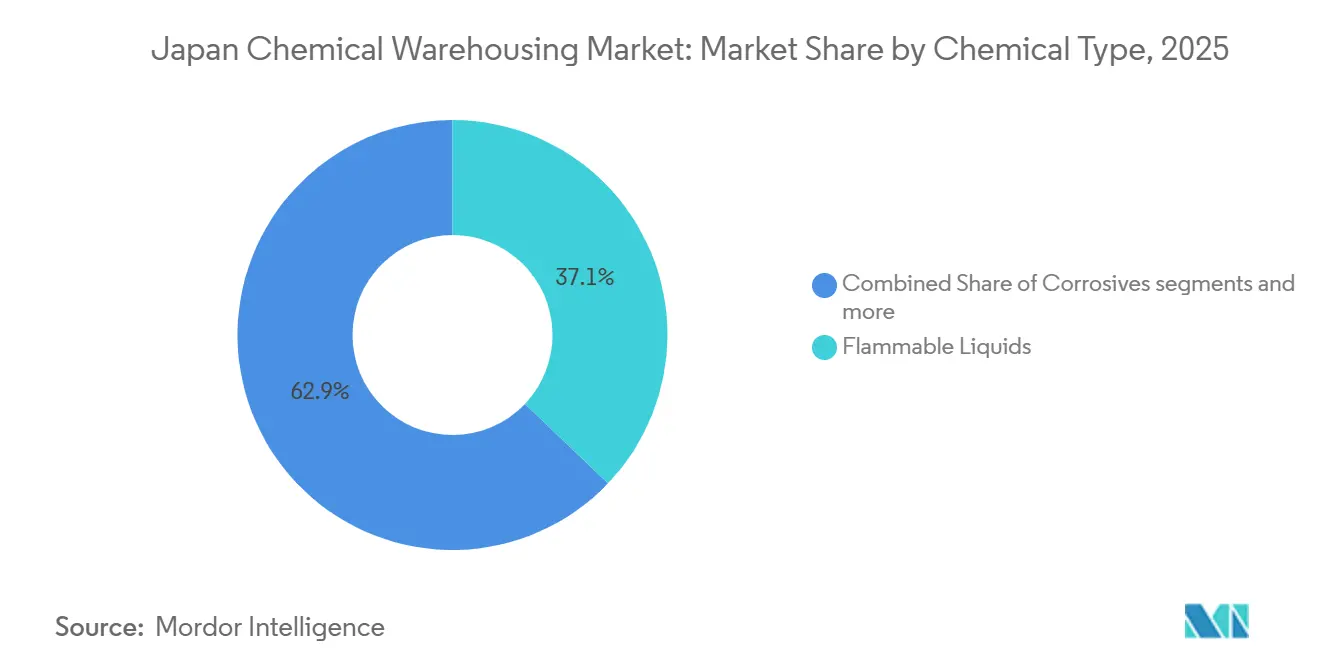

- By chemical type, flammable liquids captured 37.12% of the Japan chemical warehousing market size in 2025. Toxic substances are forecast to post the fastest growth at a 6.21% CAGR through 2031.

- By end-user, specialty chemicals manufacturing accounted for 34.21% share of the Japan chemical warehousing market size in 2025. Pharmaceuticals & life sciences are advancing at a 6.67% CAGR through 2031, the quickest among all end-user groups.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Projections can easily extend beyond country and regional trends as they are defined by movement across the full international system. Mordor Intelligence's worldwide chemical warehousing market outlook captures this forward trajectory.

Japan Chemical Warehousing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Advanced Materials Manufacturing Leadership | +1.2% | Osaka bio-cluster, Hokkaido semiconductor adjacency, broader national impacts | Medium term (2-4 years) |

| Pharmaceutical and Life Sciences Expansion | +1.5% | Osaka, Aichi, Kanagawa, with spillover to Ibaraki contract manufacturing | Medium term (2-4 years) |

| Logistics Automation and Robotics Adoption | +0.8% | National with concentration in Kanto and Kansai logistics hubs | Short term (≤ 2 years) |

| Fine Chemicals and Intermediates Growth | +0.7% | Keiyo and Osaka Bay complexes, Tokai-Chugoku corridor | Long term (≥ 4 years) |

| Regulatory Push for Safety Infrastructure | +0.9% | National, priority in FDMA-designated Special Disaster Prevention Areas | Medium term (2-4 years) |

| Chemical Industry Consolidation | +0.6% | Western Japan ethylene clusters, Keiyo polyolefin bases | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Advanced Materials Manufacturing Leadership

Japan’s tilt toward high-value specialty chemicals and pharma intermediates is changing warehouse design and procedures, with validated environments and robust traceability becoming the constraint rather than bulk capacity. Nippon Shokubai plans to expand nucleic acid API capacity tenfold at its Suita site by 2027, which requires GMP-grade storage close to production and rigorous handling rules that extend into the warehouse. FUJIFILM Wako tripled its output capacity for GMP-compliant raw materials in 2024, strengthening local needs for temperature control, process segregation, and electronic documentation of environmental conditions. Towa Pharmaceutical targets 17.5 billion tablets annually by fiscal 2026, which will increase demand for cleanroom-adjacent warehousing and accurate lot-level custody logs to protect quality and meet release schedules. As production shifts to medium- and high-potency products, storage value density rises, increasing the financial stakes of temperature deviations and handling errors and pushing digital tracking into everyday warehousing practices.[1]Towa Pharmaceutical Co., Ltd., “TOWA PHARMACEUTICAL 2025 Integrated Report,” Towa Pharmaceutical, towayakuhin.co.jp

Pharmaceutical and Life Sciences Expansion

An aging population and steady progress in biologics and nucleic acid therapies keep pharma warehousing demand resilient, requiring climate assurance, validated processes, and redundant systems to cut spoilage risk. Nippon Shokubai’s program to install a large GMP production line for nucleic acid APIs by 2027 shows how manufacturing scales translate into heightened needs for compliant storage, data integrity, and clean logistics interfaces. Dedicated HAZMAT zones and enhanced ventilation are also relevant, as facilities handle higher-potency compounds alongside solvents and reagents common to pharma manufacturing. Warehouse operating models evolve to include validated temperature monitoring, real-time alerts, and audit-ready electronic records to satisfy documentation and release processes. Regional clusters in Osaka and Ibaraki are adding capacity near plants, supporting just-in-time flows for clinical and commercial timelines without compromising compliance.

Logistics Automation and Robotics Adoption

A tight labor market and the 2024 overtime cap on drivers are making automation a frontline solution for warehouse throughput and dock productivity. Kao implemented Japan’s first automated truck-loading solution with autonomous lift trucks at its Toyohashi Plant, demonstrating how loading precision and cycle times can improve while reducing dependence on scarce, certified operators. Intermodal tests in the Tokai and Chugoku regions by Mitsui Chemicals and peers complement warehouse automation, as smoother rail interfaces reduce time pressure at docks and stabilize shift planning. The push for robotics is also financially motivated, as wage growth has outpaced productivity for many smaller operators, making capital investment in automation a practical hedge against rising operating costs. As automated systems spread from interior handling to truck interfaces, warehouses improve safety, material traceability, and 24-hour utilization while aligning with stricter handling rules for flammables and corrosives.

Regulatory Push for Safety Infrastructure

The FDMA recorded 711 hazardous-material facility accidents in 2023, including 243 fires and 468 spillage incidents, which intensified oversight of warehouse layouts, equipment, and operator training. New guidance released in March 2025 set expectations for large warehouses regarding information sharing with fire brigades, early detection in unmanned spaces, and system integration to ensure autonomous equipment does not impair fire compartmentalization. Warehouses handling dangerous goods must comply with the Fire Service Act and the Building Standards Act rules on construction, segregation, discharge containment, and fire resistance, which increase capital intensity for compliant builds. Operators in Special Disaster Prevention Areas maintain self-defense disaster teams, specialized equipment, and association participation, which reinforces coordinated emergency readiness across clusters. This framework raises barriers to entry and advantages incumbents with established permits, certified personnel, and relationships with municipal authorities for pre-consultation and ongoing audits.[2]Fire and Disaster Management Agency, “Guidelines for Effective Fire Safety Management in Large-Scale Warehouses,” Fire and Disaster Management Agency, fdma.go.jp

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Severe Land Scarcity and High Costs | -1.3% | Tokyo Bay and Osaka Bay coastal belts, Keiyo complex | Short term (≤ 2 years) |

| Aging Workforce and Labor Shortage | -1.0% | National, more acute outside megacity cores | Medium term (2-4 years) |

| Stringent Regulatory Compliance Burden | -0.6% | National with focus in Special Disaster Prevention Areas | Long term (≥ 4 years) |

| High Energy and Operating Costs | -0.7% | National, especially in temperature-controlled facilities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Severe Land Scarcity and High Costs

Scarcity of suitable plots near petrochemical clusters and deep-water terminals constrains new warehouse construction and prompts developers to consider inland locations that trade proximity for lower costs. City planning and building rules in industrial belts keep pressure on design choices and timelines, especially for single-story fire-resistant HAZMAT facilities that require impermeable floors and spill containment. Operators respond with vertical storage systems and higher automation density to increase throughput within constrained footprints, improving economics but increasing capital requirements and complexity for future tenant changes. Circular-economy hubs are emerging at industrial ports that host chemical-recycling assets, thereby increasing the value of nearby bonded warehousing and pre-sorting capacity for inbound feedstock. These dynamics lift the strategic value of intermodal nodes and brownfield upgrades that can be brought up to code with validated fire protection and segregation.

Aging Workforce and Labor Shortage

Labor markets remain tight as job openings remain elevated and wage growth runs ahead of productivity in many logistics operations, making automation a practical response for warehouse operators. Smaller logistics firms report significant wage increases without a corresponding gain in business performance, compressing margins and reducing flexibility to absorb new compliance investments. Chemical warehousing faces an additional constraint because certified hazardous-materials engineers must complete training and recertification, limiting the available pool for HAZMAT sites. The 2024 driver overtime limits compound warehouse pressures by reshaping inbound and outbound windows, which intensifies the need for precise dock scheduling and intermodal alternatives. As operators expand robotics, dock automation, and digital visibility tools, they mitigate labor risk and maintain resilient service levels for pharma and specialty chemicals.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Warehouse Type: Specialization Drives Differentiation

Specialty chemical warehouses held 41.24% of the Japan chemical warehousing market share in 2025, underscoring the country’s shift toward high-value formulations and strict safety protocols. Specialty chemical storage near production lines supports fast cycle times and strict segregation between lots and product families, both of which are essential for GMP-compliant inputs and advanced materials. General warehousing still supports bulk polymers and commodity inputs, though operators are adding WMS and sensors to align with lean replenishment cycles for automotive and construction customers.[3]Public Interest Incorporated Association Japan Logistics Systems Association, “2024 Logistics Cost Report, Summary,” Japan Logistics Systems Association, logistics.or.jpHAZMAT sites follow Fire Service Act thresholds for designated quantities and adopt impermeable floors, foam suppression, and lightning protection, as relevant, which push construction costs beyond general warehouse norms. This mix increases switching costs for customers that require validated storage, a documented chain of custody, and audit-ready records covering the warehouse segment of the flow.

In the Japan chemical warehousing market, temperature-controlled chemical warehouses are leading the charge, boasting a robust 5.78% CAGR projected through 2031. These facilities, alongside HAZMAT-certified counterparts, stand out for their unique capabilities. Notably, they emphasize fire-resistant construction, climate redundancy, and meticulous traceability. The operational stack now spans backup generation with automatic failover, continuous temperature and humidity monitoring, alerting protocols, and electronic records that meet audit needs. Multi-tenant campuses add automated fire shutters and segregated bays because mixed stored goods bring overlapping hazard classifications that must be isolated. The Japan chemical warehousing industry is also lifting robotics adoption at docks and high-density aisles, which offsets margin pressure from rising wages and helps recover capacity lost to the 2024 driver overtime rules. Together, these investments are reshaping competitive positioning across warehouse types because validated capabilities command premium rates that support reinvestment and compliance upkeep.

By Chemical Type: Hazard Profiles, Shape Infrastructure

Flammable liquids accounted for 37.12% of Japan's chemical warehousing market in 2025. The Japan chemical warehousing market, particularly around petrochemical clusters with access to pipelines, jetties, and shared emergency responses, predominantly stores flammable liquids. Storing these liquids requires bonded-area segregation, explosion-proof electrical equipment, and Class B foam suppression, which drive up capital costs per square meter compared to general storage. Corrosives, on the other hand, demand acid-resistant flooring, scrubbing ventilation, and clear incompatibility matrices to avert reactive incidents during routine operations. Toxic substances, including oncology APIs and specific agrochemical actives, are the fastest-growing segment, boasting a 6.21% CAGR through 2031. Their stringent requirements for containment, low-volume handling, and layered traceability elevate storage premiums above standard pallet rates. These stringent requirements bolster the role of certified operators and complicate the implementation of mixed storage programs across expansive campuses.

Oxidizers and special categories, including water-reactive and self-reactive substances, require niche infrastructure and disciplined process control, which favors operators with deep safety records. Maintenance and inspection regimes are important because FDMA reports showed hundreds of spill incidents in 2023, which focus on equipment integrity and operator training. Chemical recycling is also creating reverse logistics flows that require pre-sorting and risk controls before materials enter decomposition or refining processes, as shown by the ENEOS and Mitsubishi Chemical facility in Ibaraki, which began commercial operations in 2025. These streams introduce new handling protocols and quality checks into warehouses that feed circular operations, thereby increasing the value of bonded and intermodal nodes in the cluster. As programs scale, operators refine segregation maps and firefighting strategies to match changing mixes of incoming materials and hazard profiles.

By End-user Industry: Vertical Integration Versus Third-Party Logistics

Specialty Chemicals Manufacturing accounted for 34.21% of Japan's chemical warehousing market in 2025. Specialty chemicals use a blend of captive and outsourced warehousing, tailoring their approach to value density and regulatory mandates. They ensure validated storage and strict segregation for high-value intermediates, while lower-risk products can share facilities. The pharmaceuticals & life sciences sector emerged as the fastest-growing segment, boasting a 6.67% CAGR projected through 2031. This growth is driven by the sector's stringent standards for cold-chain and GMP-grade processes, as well as an increasing demand for audit-ready electronic records and climate logs. Such requirements bolster premium service tiers and elevate the strategic significance of warehouses near labs and plants, enabling synchronized production cycles with compliant logistics. As outsourcing trends rise, suppliers, like Towa Pharmaceutical Co., Ltd., are stepping up, offering value-added services that seamlessly integrate inventory control, release workflows, and real-time visibility for both inbound and outbound logistics.

Lead Logistics Partner models are expanding as chemical producers convert fixed logistics assets into variable spending while retaining governance over service levels and capacity. DHL’s five-year agreement with Sanyo Chemical covers five in-plant sites and leverages MySupplyChain digital visibility, demonstrating how integrated control towers can standardize operations and address driver shortages through a single program. Pharma and fine-chemical clients also maintain strategic stockpiles in captive facilities for launch protection and business continuity, while using third parties for routine flows. The Japanese chemical warehousing industry is aligning end-user models with modal shifts, including rail-linked sites that consolidate pallets and standardize handoffs to maintain throughput within driver-hour limits. This blend of captive control and outsourced execution supports resilience as compliance requirements continue to tighten.

Geography Analysis

Japan’s coastal clusters along Tokyo Bay’s Keiyo belt and the Osaka Bay complex anchor HAZMAT storage, which aligns warehouses with ethylene derivatives, solvents, and bulk inputs connected to pipelines and marine terminals. These regions host a dense network of hazardous facilities under the Fire Service Act, which enhances joint emergency preparedness and supports inter-facility coordination for fire prevention and response. Keiyo’s access to container ports and refined-product jetties reduces drayage, while Osaka’s blend of marine and air access suits time-sensitive pharma and specialty inputs. The Japan chemical warehousing market benefits from these agglomeration effects because compliance investments and emergency assets can be shared or coordinated across multiple sites. As logistics networks adapt to driver-hour limits, intermodal nodes gain visibility in both corridors for rail consolidation and consistent service windows.

The FDMA lists 77 Special Disaster Prevention Areas across 33 prefectures and 97 municipalities, encompassing 642 specified business establishments that cluster specialized response capabilities and share training programs across industrial zones. These areas deploy 75 large chemical fire trucks and 117 large elevated chemical water trucks and support 70 joint disaster-prevention associations that coordinate mutual aid and evacuation. The Japan chemical warehousing market uses this framework to align equipment standards, update multilingual evacuation protocols, and conduct joint exercises to improve incident readiness across large campuses. Inland capacity is adding value in pharma clusters like Suita and in Ibaraki’s chemical corridor, where GMP-compliant warehousing links directly to plants or intermodal yards with lower land intensity. The result is a layered network that balances coastal economies of scale with inland compliance and specialty handling.

Business continuity priorities are shaping cross-border flows, with Nippon Express launching a Busan-based BCP service in 2025 that provides bonded storage, inventory management, and a single insurance policy to secure supply chains during large-scale disasters. This model provides Japan chemical warehousing market users with an offshore buffer against seismic risk while maintaining access to major shipping routes and customs processes. The intermodal rail demonstration between Nagoya and Otake by Mitsui Chemicals and partners adds a domestic layer to this resilience, reducing reliance on constrained trucking capacity and supporting standardized loading practices for hazardous materials. Circular-economy sites like the plastic-to-oil facility in Ibaraki are also producing steady reverse flows, which raises the profile of bonded and intermodal warehouses near reprocessing terminals. Over time, these geography choices will influence how much of the Japan chemical warehousing market remains in coastal clusters versus moves to inland campuses that specialize in validated storage and value-added services.

The chemical warehousing market is analyzed by Mordor Intelligence across multiple other geographies, with in-depth regional assessments available for Africa, North America, and Europe. This is complemented by country-specific insights for India, South Korea, Canada, Germany, Italy, and China, reflecting various localized market behavior and policy environments' coverage.

Competitive Landscape

The Japan chemical warehousing market is moderately fragmented, with integrated logistics groups, captive facilities owned by chemical producers, and specialized HAZMAT providers serving different needs. General warehousing faces price pressure, while validated pharma storage commands premiums based on compliance and process integrity. Players differentiate through automation, intermodal readiness, and quality systems that integrate climate logs and audit trails into daily operations. Warehouse operators that align closely with the Fire Service Act requirements and FDMA guidance for large facilities strengthen their position during customer audits and municipal permitting workflows.

Strategic moves include expanding LLP models and conducting intermodal pilots to reduce exposure to driver-hour constraints and stabilize linehaul options for hazardous cargo. DHL’s LLP agreement with Sanyo Chemical spans five plant sites and incorporates digital visibility to coordinate in-plant logistics and outbound flows. Mitsui Chemicals and partners are advancing a standard rail scheme for hazardous goods using 31-foot containers, which seeks to scale nationwide if trial results remain favorable. Business continuity solutions are also gaining traction, with Nippon Express offering a Busan-based BCP warehousing and transport model that bundles bonded storage and comprehensive insurance for disaster readiness. Together these steps help the Japan chemical warehousing market balance safety, reliability, and cost under tightening labor and regulatory conditions.

Technology is a growing wedge in competition, particularly where autonomous lift trucks streamline truck loading, and AI tools improve slotting and cycle control. Circular-economy assets like the Ibaraki plastic-to-oil plant are adding new reverse flows and expanding the role of bonded and safety-compliant warehouses near reprocessing hubs. In pharma and fine chemicals, validated storage with real-time monitoring and documented segregation supports premium pricing and longer contract durations. Intermodal readiness and incident preparedness aligned with FDMA expectations remain selection factors for risk-sensitive shippers.

Japan Chemical Warehousing Industry Leaders

Mitsubishi Logistics Corporation

Mitsui-Soko Holdings Co., Ltd.

Nippon Express Holdings

Yusen Logistics Co., Ltd. (NYK Line)

Mitsubishi Chemical Logistics Corp. (Subsidiary of Mitsubishi Chemical Corporation)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: NX Europe, part of Nippon Express, confirmed participation in LogiPharma 2026, highlighting its focus on GDP-aligned pharma logistics and visibility solutions in Europe, which complements Japan-origin pharma flows and compliance needs.

- July 2025: ENEOS and Mitsubishi Chemical completed construction of a 20,000-ton-per-year plastic-to-oil facility at the Ibaraki Plant in Kamisu, using hydrothermal technology, with commercial operations scheduled for the end of fiscal 2025.

- June 2025: Nippon Shokubai announced plans to expand its GMP-compliant nucleic acid API manufacturing capacity by 10 times at its Suita site, with commissioning slated for 2027.

Japan Chemical Warehousing Market Report Scope

The Japan Chemical Warehousing Market Report is Segmented by Warehouse Type (General Warehousing, Specialty Chemical Warehouse, Hazardous Materials (HAZMAT) Warehouses, Temperature-Controlled Chemical Warehouses), by Chemical Type (Flammable Liquids, Corrosives, Toxic Substances, Oxidizers, Others), and by End-user Industry (Basic Chemicals Manufacturing, Specialty Chemicals Manufacturing, Pharmaceuticals & Life Sciences, Agrochemicals, Paints, Coatings & Adhesives, Food & Feed Additives, Oil & Gas / Petrochemicals, Others). The Market Forecasts are Provided in Terms of Value (USD Billion).

| General Warehousing |

| Specialty Chemical Warehouse |

| Hazardous Materials (HAZMAT) Warehouses |

| Temperature-Controlled Chemical Warehouses |

| Flammable Liquids |

| Corrosives |

| Toxic Substances |

| Oxidizers |

| Others |

| Basic Chemicals Manufacturing |

| Specialty Chemicals Manufacturing |

| Pharmaceuticals & Life Sciences |

| Agrochemicals |

| Paints, Coatings & Adhesives |

| Food & Feed Additives |

| Oil & Gas / Petrochemicals |

| Others |

| By Warehouse Type | General Warehousing |

| Specialty Chemical Warehouse | |

| Hazardous Materials (HAZMAT) Warehouses | |

| Temperature-Controlled Chemical Warehouses | |

| By Chemical Type | Flammable Liquids |

| Corrosives | |

| Toxic Substances | |

| Oxidizers | |

| Others | |

| By End-user Industry | Basic Chemicals Manufacturing |

| Specialty Chemicals Manufacturing | |

| Pharmaceuticals & Life Sciences | |

| Agrochemicals | |

| Paints, Coatings & Adhesives | |

| Food & Feed Additives | |

| Oil & Gas / Petrochemicals | |

| Others |

Key Questions Answered in the Report

What is the current size and growth outlook for the Japan chemical warehousing market?

The Japan chemical warehousing market size was USD 4.91 billion in 2025 and is projected to reach USD 6.70 billion by 2031 at a 5.0% CAGR over 2026-2031.

Which capabilities are driving premium pricing in Japan’s chemical warehousing?

Validated, temperature-controlled storage near production, rigorous segregation, and audit-ready electronic records are commanding premiums, especially for pharma and high-value intermediates.

How are regulations shaping warehouse investments in Japan?

Fire Service Act compliance and FDMA guidance for large warehouses raise standards for construction, detection, data sharing, and incident readiness, which increases capital intensity and creates barriers to entry.

How is labor scarcity influencing operations in Japan’s chemical warehouses?

Tight labor markets and driver-hour limits are accelerating automation at docks and inside warehouses, improving throughput and safety while stabilizing service windows.

Where are intermodal solutions gaining traction for chemical logistics in Japan?

The Tokai and Chugoku regions are piloting standard rail schemes for hazardous goods using 31-foot containers to address trucking constraints and improve loading efficiency.

What resilience strategies are shippers using for disaster risk in Japan?

Business continuity models include bonded storage in Busan with single-policy insurance coverage and domestic intermodal options, which diversify exposure while keeping access to Japan trade lanes.

Page last updated on: