Mexico Chemical Warehousing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

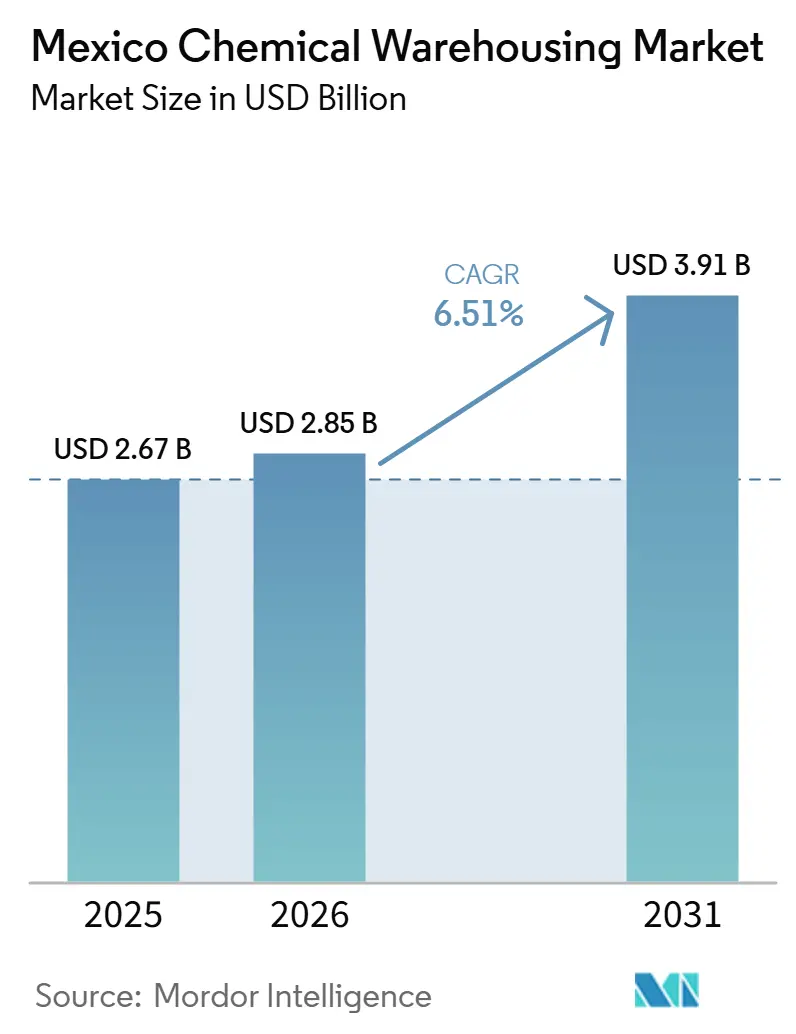

| Base Year Market Size (2025) | USD 2.67 Billion |

| Market Size (2026) | USD 2.85 Billion |

| Market Size (2031) | USD 3.91 Billion |

| Growth Rate (2026 - 2031) | 6.51% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Chemical Warehousing Market Analysis by Mordor Intelligence

The Mexico Chemical Warehousing Market size is expected to grow from USD 2.67 billion in 2025 to USD 2.85 billion in 2026 and is forecast to reach USD 3.91 billion by 2031 at 6.51% CAGR over 2026-2031.

The trajectory reflects stronger integration with North American manufacturing under USMCA, faster nearshoring decisions, and investment in compliant facilities for hazardous and temperature-sensitive chemicals. Warehousing operators benefit from stable trade flows and the repositioning of Mexico as a strategic node for chemical-intensive value chains that serve automotive, electronics, agrochemicals, and pharmaceuticals. Compliance-driven upgrades, including GHS labeling and dangerous goods packaging, are shaping facility design and standard operating procedures in ways that raise barriers to entry. Security and water stress remain operational risks, yet ongoing port, rail, and cross-border improvements reinforce the long-run potential of the Mexico chemical warehousing market. Near-term capital allocation prioritizes temperature-controlled capacity and co-located warehouses near key clusters that support short lead times and audit-ready documentation for regulated flows.

Key Report Takeaways

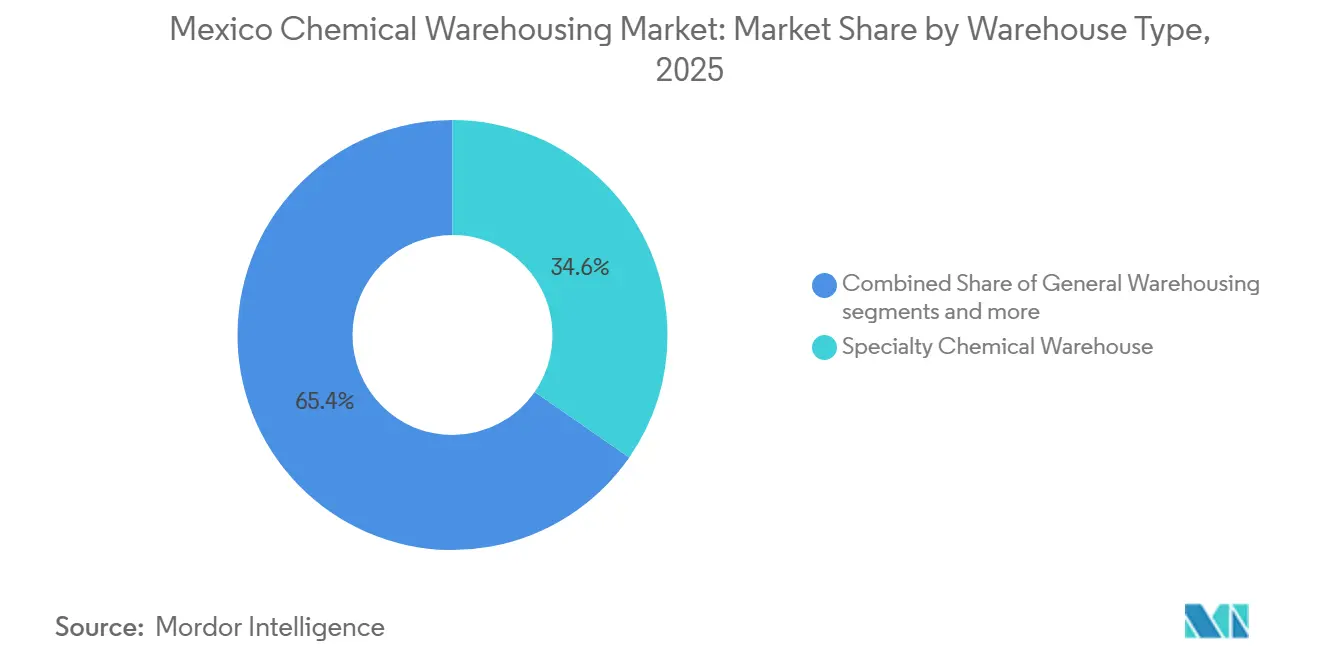

- By warehouse type, specialty chemical warehouses led with 34.64% of Mexico chemical warehousing market share in 2025 revenue, while temperature-controlled facilities are projected to expand at a 6.71% CAGR through 2026-2031.

- By chemical type, flammable liquids accounted for 42.61% of the Mexico chemical warehousing market size in 2025 storage volumes, and toxic substances are forecast to grow at a 7.42% CAGR through 2031.

- By end-user industry, basic chemicals manufacturing held 32.70% in 2025, while pharmaceuticals and life sciences are the fastest-growing end user at a 6.92% CAGR through 2031.

- By geography, the Bajío corridor and northern border states concentrated 68% of capacity in 2025, while Central Mexico is projected to post the fastest 2026-2031 CAGR at 7.1%.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Mexico operates as part of an interconnected international environment rather than as a self-contained country level unit. The chemical warehousing market research by Mordor Intelligence places together all major developments across the globe within that wider frame.

Mexico Chemical Warehousing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| USMCA Manufacturing Integration | +1.8% | National, with concentrated gains in the Bajío corridor, Nuevo León, and Chihuahua | Medium term (2-4 years) |

| Nearshoring and Reshoring Acceleration | +1.5% | Global, with primary impact on northern border states and the central Mexico industrial parks | Medium term (2-4 years) |

| Oil and Gas Sector Liberalization | +0.9% | Gulf Coast, with spillover to Monterrey distribution hub | Long term (≥ 4 years) |

| Maquiladora and IMMEX Program Growth | +0.8% | Northern border states, with expansion into Bajío and Jalisco | Short term (≤ 2 years) |

| Strategic Geographic Position | +0.7% | National, with early gains at border crossings and Pacific, Gulf ports | Short term (≤ 2 years) |

| Agrochemical Market Expansion | +0.6% | National, with emphasis on Sinaloa, Jalisco, Guanajuato, and Michoacán | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

USMCA Manufacturing Integration

Mexico’s role in integrated North American production networks is strengthening, which is increasing pre-positioning of compliant intermediates and compounds across warehouse networks. Non-petroleum manufacturing exports rose in October 2025, including a sharp jump in machinery and special equipment, which signals deeper use of specialty chemical inputs that must meet regional value thresholds. Operators prioritize audit trails for Certificates of Origin and co-locate near automotive and electronics hubs to control dwell time and maintain compliance. Policy stability and reduced trade uncertainty are supporting capital plans that add compliant space near major corridors in the Mexico chemical warehousing market. Combined effects of traceability, proximity, and documentation rigor are improving service reliability and cycle times. These conditions favor operators that can balance cost and compliance within USMCA rules. [1]Instituto Nacional de Estadística y Geografía, “Balanza Comercial de Mercancías de México (BCMM),” INEGI, inegi.org.mx

Nearshoring and Reshoring Acceleration

Manufacturers are redistributing production closer to end markets, and Mexico is a key base for regulated chemical flows that require reliable storage and handling. Global 3PLs have added large sites near airports and cross-border gateways to support high-tech, automotive, and healthcare shipments. Expansion moves include added cross-dock and warehouse space in El Paso that links Juárez with U.S. distribution, while new mega-campuses near Felipe Ángeles International Airport are built for temperature-controlled and compliant operations. Standardized dangerous goods packaging and labeling aligned to UN model regulations are embedded into contracts and site design to de-risk transitions. This proximity, standardization, and service mix underpin the growth profile for the Mexico chemical warehousing market.

Oil and Gas Sector Liberalization

Mexico’s oil and gas liberalization has unlocked private investment in midstream and petrochemical infrastructure, which secures feedstock and stabilizes chemical flows into storage and distribution. The USD 500 million Terminal Química Puerto México, inaugurated in May 2025, added 54,000 tons of ethane storage with two 50,000 m³ cryogenic tanks, a dedicated jetty, and pipeline links that feed Braskem Idesa’s polyethylene complex at full capacity. The project, the first private industrial investment tied to the Interoceanic Corridor of the Isthmus of Tehuantepec, signals how corridor and port upgrades can catalyze new chemical storage and handling capacity. Gulf Coast throughput is also rising, with the Port of Altamira moving 14 million tons through August 2025, including 570,902 TEUs and year-on-year gains in petrochemical fluids, which lifts nearby warehousing needs. As feedstock reliability improves, producers and traders sign longer contracts and hold higher safety stocks, driving co-located storage for ethane, methanol, propylene, and related corrosives near Veracruz, Coatzacoalcos, and Altamira. Facilities handling these products must meet NOM-005-STPS-1998 requirements for explosion-proof systems, flame arresters, and continuous ventilation, which raises design standards and favors certified HAZMAT operators while expanding regulated volumes and supporting premium pricing for compliant capacity across Gulf nodes and their inland lanes.

Maquiladora and IMMEX Program Growth

Streamlined procedures under the National Digital Investment Window and enhancements to IMMEX have shortened time to launch and increased flexibility for export-linked manufacturers. Temporary import deferrals tied to export commitments reduce working capital tied up in duties and support just-in-time storage of resins, adhesives, and solvents. The framework’s sectoral coverage now extends to pharmaceutical API synthesis and polymer compounding that need temperature and humidity controls aligned with quality standards. Duty suspension and efficient rotation improve alignment with regional content rules under USMCA for customers using compliant intermediates. These conditions support durable demand for certified capacity and predictable inspections across the Mexico chemical warehousing market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Security and Organized Crime Risks | -0.9% | National, with acute exposure in Veracruz, Tamaulipas, Guanajuato, Jalisco | Short term (≤ 2 years) |

| Regulatory Complexity and Enforcement Inconsistency | -0.7% | National, with variability across federal and municipal jurisdictions | Medium term (2-4 years) |

| Water Scarcity in Northern Industrial Zones | -0.5% | Northern states, including Nuevo León, Chihuahua, Coahuila, Sonora | Long term (≥ 4 years) |

| Skills Shortage in Hazardous Materials Management | -0.4% | National, with gaps in pharmaceutical-grade cold-chain and HAZMAT certification | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Security and Organized Crime Risks

Illicit groups have infiltrated logistics corridors, which exposes chemical storage and transit to theft, fraud, and inspection delays. U.S. Treasury actions in May 2025 targeted companies tied to fuel theft and mislabeling schemes that used legitimate networks and facilities. Enhanced inspections after such events can add 6 to 12 hours at crossings, and insurance and security measures raise operating costs for affected sites. Operators deploy GPS tracking, escorts, and hardened access, and some shift high-value inventory to lower risk jurisdictions to preserve service levels. These responses help maintain continuity yet add cost and complexity for the Mexico chemical warehousing market.[2]Financial Crimes Enforcement Network, “Oil Smuggling Schemes Alert,” U.S. Department of the Treasury, fincen.gov

Regulatory Complexity and Enforcement Inconsistency

Warehouses operate under multiple standards that require harmonized labeling, documentation, and worker training while enforcement varies by location. GHS labeling and Spanish-language safety data sheets are core to compliant intake, storage, and training. Hazardous waste classification uses detailed lists and test protocols, yet inspection timelines differ across regions, which influences expansion pacing. Dangerous goods packaging requirements aligned to UN model regulations are in effect after a transition period, and some locations are still ramping up inspection capacity. These variations add uncertainty to project timelines and budgets for operators in the Mexico chemical warehousing market.[3]Secretaría del Trabajo y Previsión Social, “NOM-018-STPS-2015,” Gobierno de México, economia.gob.mx ,

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Warehouse Type: Specialty Dominance Meets Temperature-Controlled Momentum

Specialty chemical warehouses led with 34.64% in 2025, supported by export-facing coatings, adhesives, and electronic-grade solvents that align with regional content rules under USMCA. Temperature-controlled warehouses post the fastest projected growth at a 6.71% CAGR to 2031 as pharmaceutical and biotech customers expand regulated storage needs in proximity to major airports and urban hubs. The Mexico chemical warehousing market responds by standardizing audit-ready processes, traceability, and controlled environments that meet regulated stability profiles for sensitive inputs. General warehouses maintain a share for bulk commodities that require less specialization and are distributed across major cross-border and in-country corridors. HAZMAT facilities focus on ports and petrochemical clusters where dangerous goods packaging, labeling, and equipment standards converge with tenant requirements. The Mexico chemical warehousing market benefits when operators integrate sensor networks that monitor temperature, humidity, and shock for regulated drugs and specialty intermediates.

Regulatory streamlining reduces onboarding time for compliant sites that serve export-oriented manufacturers. Investments in temperature control and serialization increase the ability to win multi-year contracts in pharmaceuticals and high-purity chemicals. Dangerous goods standards, including packaging and labeling aligned to UN model regulations, are embedded into site planning and operating procedures. GHS labeling and safety data sheet management remain core for worker protection and inspections. These capabilities strengthen customer confidence and drive recurring demand within the Mexico chemical warehousing market.

By Chemical Type: Flammable Liquids Lead, Toxic Substances Surge

Flammable liquids represent the largest category at 42.61% of 2025 volumes, reflecting steady movement of ethane, methanol, and related feedstocks through Gulf Coast platforms that support polyethylene and other downstream chains. Toxic substances show the fastest growth with a 7.42% projected CAGR, lifted by upgraded agrochemical storage as programs expand fertilizer access and guide a shift away from highly dangerous molecules. Corrosives and oxidizers track demand from mining, water treatment, and pharmaceutical processes, with throughput influenced by infrastructure spend and export activity. The Mexico chemical warehousing market prioritizes segregation and compatibility to manage these categories safely and efficiently. Dedicated storage and labeling practices limit cross-contact and align with regulatory requirements for hazardous materials. The integration of port and inland distribution supports reliable flows in the Mexico chemical warehousing market.

Operators align with labeling and documentation standards that help reduce risk in handling and transit. Hazardous waste classification protocols help define intake processes and disposal coordination when necessary. National dangerous goods packaging rules, adopted in 2024 and effective after their transition period, are incorporated into equipment procurement and training. Clear pictograms and instruction sets support audits and promote consistent practices across sites and subcontractors. These measures support quality, safety, and throughput in the Mexico chemical warehousing industry.

By End-User Industry: Mexico's Pharma Warehousing Opportunity

Basic chemicals manufacturing accounted for 32.70% of 2025 warehousing demand, sustained by broad consumption across mining, pulp and paper, and water treatment. Pharmaceuticals and life sciences are the fastest-growing end users, posting a 6.92% projected CAGR as regulatory recognition of foreign GMP certificates improves time-to-market for temperature-sensitive APIs and biologics. Specialty chemicals growth tracks automotive and electronics clusters, where regional content rules drive nearer suppliers and compact storage cycles. Agrochemicals maintain momentum as policy extends fertilizer access and moves suppliers toward safer formulations. These combined needs support reliable base demand in the Mexico chemical warehousing market.

Pharmaceutical-grade facilities invest in controlled environments, serialization, and process validation support to meet customer audits. Fourth-party logistics models coordinate multi-tenant capacity and tap specialized subcontractors to serve high-compliance verticals. Energy and water constraints in northern states influence location decisions and backup capability planning. Port-linked warehousing on the Gulf Coast complements inland hubs for petrochemicals and finished goods. Consistent documentation and labeling practices reduce inspection delays and reinforce reliability in the Mexico chemical warehousing industry.

Geography Analysis

The Bajío industrial corridor and northern border states held 68% of chemical warehousing capacity in 2025, supported by robust cross-border freight through Laredo, El Paso, and Tijuana. Chihuahua recorded USD 47.551 billion in exports in Q2 2025, reflecting the pull from electronics and automotive segments that consume regulated chemical inputs. Recent expansions in cross-dock and bonded facilities around El Paso and Juárez indicate continued throughput gains for specialized freight. The Mexico chemical warehousing market in these regions benefits from dense supplier networks and fast-cycle logistics between production and U.S. distribution. Water stress and power planning remain critical considerations for larger sites in northern states. Policy measures and digital permitting are improving setup timelines for new facilities that serve export-oriented clusters.

The Gulf Coast commanded 18% of national capacity in 2025, anchored by Veracruz and Altamira, where petrochemical flows support large storage requirements for flammables and corrosives. Terminal Química Puerto México, inaugurated in May 2025, secured ethane supply and enhanced system reliability for downstream polyethylene production. Altamira’s cargo performance shows the range of commodities served, including resins and auto parts, which connect marine, rail, and trucking modes. The Mexico chemical warehousing market in Gulf states integrates port operations with inland petrochemical distribution. Security risk management, including route planning and hardening of assets, remains essential for operators in select corridors. These controls help contain operating cost pressures that rise when threats intensify.

Central Mexico, including the State of Mexico, Querétaro, Guanajuato, and Jalisco, accounted for 14% of demand in 2025 and is projected to deliver the fastest growth through 2031. Large greenfield campuses near Felipe Ángeles International Airport are designed for pharmaceutical and specialty chemical customers that need sub-25°C integrity. Regulatory recognition of foreign GMP certificates supports time-to-market and expands inbound flows for temperature-sensitive APIs and biologics. Contract logistics providers deepen their service mix in this region to support inventory visibility and controlled storage for audits. The Mexico chemical warehousing market in Central Mexico captures growth from both domestic consumption and re-exports under USMCA. Inspection cycles are generally faster here than at select coastal locations, which helps compress certification timelines.

The chemical warehousing market is assessed by Mordor Intelligence through a multi-layered geographic lens, covering other regions such as Middle East, Africa, and North America, along with detailed country-level analysis for Canada, Italy, Japan, China, India, and South Korea.

Competitive Landscape

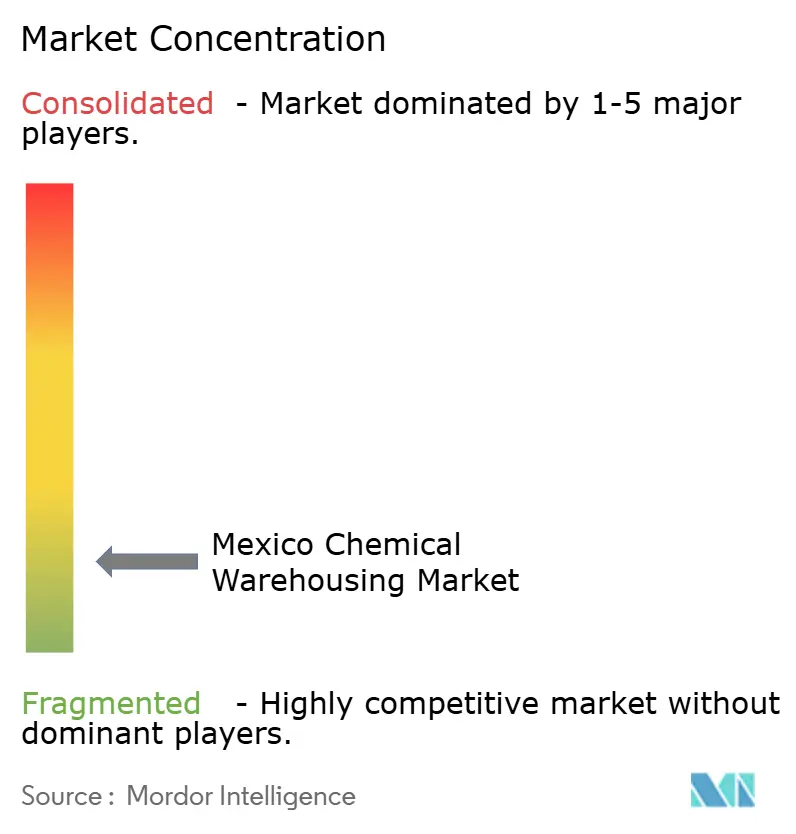

Competitive intensity remains fragmented, with no single operator controlling more than 12% of national capacity. Global 3PLs such as DHL Supply Chain, DSV, Kuehne+Nagel, and C.H. Robinson compete with domestic specialists that manage compliance and local relationships. Asset-heavy players invest in build-to-suit sites with integrated dangerous goods and GHS capabilities baked into leases and site designs. Asset-light orchestrators coordinate multi-tenant networks and provide 4PL services for pharmaceuticals and medical devices. Recent expansions added millions of square feet along the U.S.-Mexico border, while large Central Mexico campuses serve regulated life sciences flows. This mix supports a diverse customer base across the Mexico chemical warehousing market.

White-space opportunities arise in secondary cities that want to attract API and specialty producers without long build times. Agrochemical transitions to safer profiles increase needs for compatibility checks and segregated environments. Reverse logistics for chemical packaging and material recovery grow with supportive state policies on solid waste and circularity. Digital routing and consolidation tools enhance cross-border efficiency and visibility for regulated loads. Adoption of sensor networks and tighter access controls reduces tampering risk and improves compliance outcomes in the Mexico chemical warehousing market.

Operators are also testing alternative fuels for select transport needs and evaluating decarbonization pathways. At the same time, they are strengthening governance and training regimes that align with hazard identification and documentation norms. End-to-end visibility supports better risk control and customer assurance during audits. Combining physical site hardening with data controls helps deter infiltration risks identified by authorities. These approaches enhance resilience and service quality for customers across the Mexico chemical warehousing market.

Mexico Chemical Warehousing Industry Leaders

Traxion

DHL Group

Rhenus Logistics

Den Hartogh Logistics

Innovacion Logika

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: The U.S. Treasury’s FinCEN issued an alert sanctioning two Mexico-based hazardous materials transportation companies linked to fuel theft schemes, emphasizing security risks in logistics corridors.

- May 2025: PSA BDP acquired a majority stake in ED Forwarding in Mexico City, strengthening cross-border logistics and customs brokerage for nearshoring manufacturers.

- March 2025: COFEPRIS published guidelines recognizing GMP certificates for medicines from ANVISA, supporting Mexican storage and distribution of temperature-sensitive APIs and biologics under foreign approvals.

Mexico Chemical Warehousing Market Report Scope

The Mexico Chemical Warehousing Market Report is Segmented by Warehouse Type (General Warehousing, Specialty Chemical Warehouse, Hazardous Materials (HAZMAT) Warehouses, and Temperature-Controlled Chemical Warehouses), by Chemical Type (Flammable Liquids, Corrosives, Toxic Substances, Oxidizers, and Others), by End-user Industry (Basic Chemicals Manufacturing, Specialty Chemicals Manufacturing, Pharmaceuticals & Life Sciences, Agrochemicals, Paints Coatings & Adhesives, Food & Feed Additives, Oil & Gas/Petrochemicals, and Others), and Geography. The Market Forecasts are Provided in Terms of Value (USD)

| General Warehousing |

| Speciality Chemical Warehouse |

| Hazardous Materials (HAZMAT) Warehouses |

| Temperature-Controlled Chemical Warehouses |

| Flammable Liquids |

| Corrosives |

| Toxic Substances |

| Oxidizers |

| Others |

| Basic Chemicals Manufacturing |

| Specialty Chemicals Manufacturing |

| Pharmaceuticals & Life Sciences |

| Agrochemicals |

| Paints, Coatings & Adhesives |

| Food & Feed Additives |

| Oil & Gas / Petrochemicals |

| Others |

| By Warehouse Type | General Warehousing |

| Speciality Chemical Warehouse | |

| Hazardous Materials (HAZMAT) Warehouses | |

| Temperature-Controlled Chemical Warehouses | |

| By Chemical Type | Flammable Liquids |

| Corrosives | |

| Toxic Substances | |

| Oxidizers | |

| Others | |

| By End-user Industry | Basic Chemicals Manufacturing |

| Specialty Chemicals Manufacturing | |

| Pharmaceuticals & Life Sciences | |

| Agrochemicals | |

| Paints, Coatings & Adhesives | |

| Food & Feed Additives | |

| Oil & Gas / Petrochemicals | |

| Others |

Key Questions Answered in the Report

What is the Mexico chemical warehousing market size and growth outlook to 2031?

The Mexico chemical warehousing market size is projected to expand from USD 2.67 billion in 2025 and USD 2.85 billion in 2026 to USD 3.91 billion by 2031, at a 6.51% CAGR between 2026 and 2031.

Which warehouse type leads and which is growing fastest in Mexico?

Specialty chemical warehouses led in 2025 with 34.64%, while temperature-controlled facilities are projected to grow the fastest at a 6.71% CAGR to 2031.

Which chemical categories are most important for storage in Mexico?

Flammable liquids held 42.61% of 2025 volumes, while toxic substances are the fastest-growing category with a projected 7.42% CAGR.

Which end-user segments drive warehousing demand in Mexico?

Basic chemicals held 32.70% of 2025 demand, and pharmaceuticals and life sciences are the fastest-growing end user with a 6.92% projected CAGR through 2031.

Which regions concentrate capacity and where is growth fastest?

The Bajío corridor and northern border states held 68% of 2025 capacity, and Central Mexico is projected to record the fastest growth through 2031.

What are the top operational risks to chemical warehousing in Mexico?

Key risks include security challenges on select corridors, complex and variably enforced regulations, and water scarcity in several northern states.

Page last updated on: