South Korea Automation And Industrial Control Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

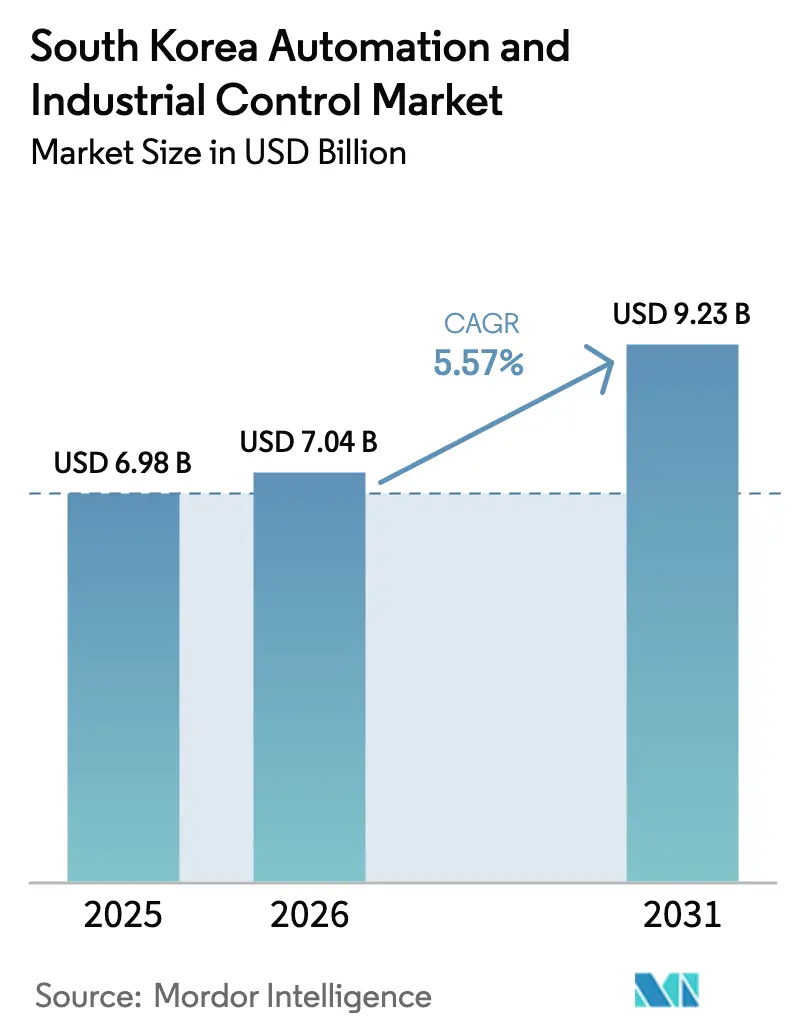

| Base Year Market Size (2025) | USD 6.98 Billion |

| Market Size (2026) | USD 7.04 Billion |

| Market Size (2031) | USD 9.23 Billion |

| Growth Rate (2026 - 2031) | 5.57% CAGR |

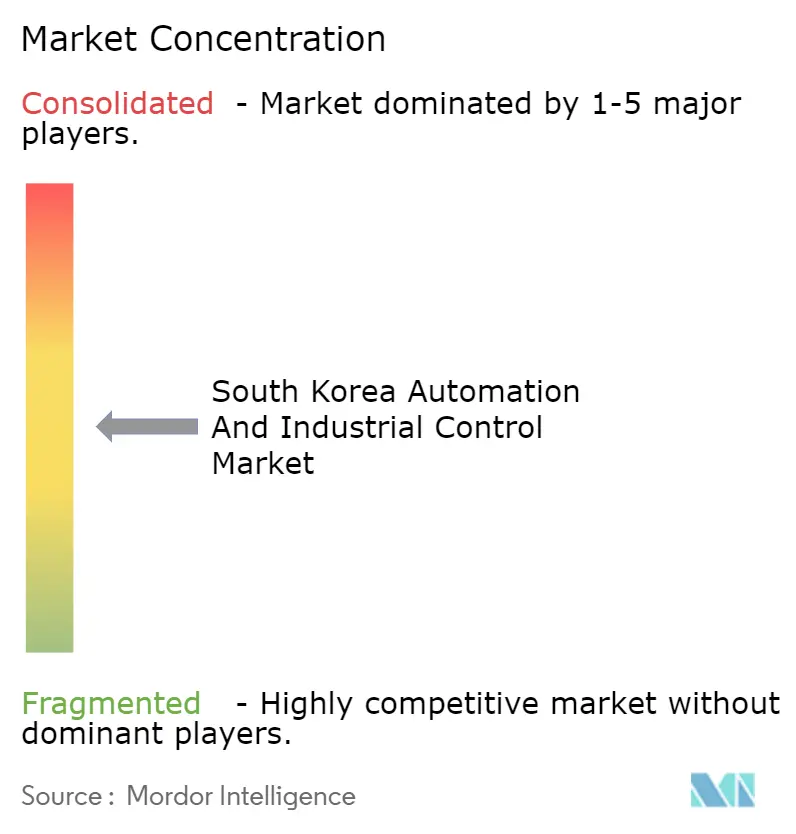

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Automation And Industrial Control Market Analysis by Mordor Intelligence

The South Korea Automation And Industrial Control Market size is projected to be USD 6.98 billion in 2025, USD 7.04 billion in 2026, and reach USD 9.23 billion by 2031, growing at a CAGR of 5.57% from 2026 to 2031.

Rising labor costs, semiconductor mega-investments and government smart-factory incentives continue to steer capital toward programmable logic controllers, distributed control systems and collaborative robots. Lights-out manufacturing strategies have become mainstream as the working-age population fell by 1.2 million between 2020 and 2025, prompting both chaebols and small manufacturers to accelerate plant automation. Semiconductor fabs are the single largest demand anchor: SK hynix’s KRW 122 trillion (USD 93.8 billion) Yongin project and Samsung’s Pyeongtaek P5 restart require process-safety systems, SCADA platforms and sub-nanometer electric motors. Budget support also matters, MOTIE earmarked KRW 436.56 billion (USD 336 million) in 2026 for smart-factory subsidies, while the 4th Intelligent Robot Basic Plan targets 1 million industrial robots by 2030. Low-latency 5G private networks, tax credits linked to locally sourced robot parts and cloud-hosted AI quality analytics together expand the addressable base of software and services.

Key Report Takeaways

- By product category, industrial robotics led with 49.83% revenue share in 2025, while collaborative robots amongst the other products are forecast to expand at a 7.31% CAGR through 2031.

- By component, hardware accounted for 60.59% of 2025 revenue; software is projected to grow at 6.02% CAGR to 2031.

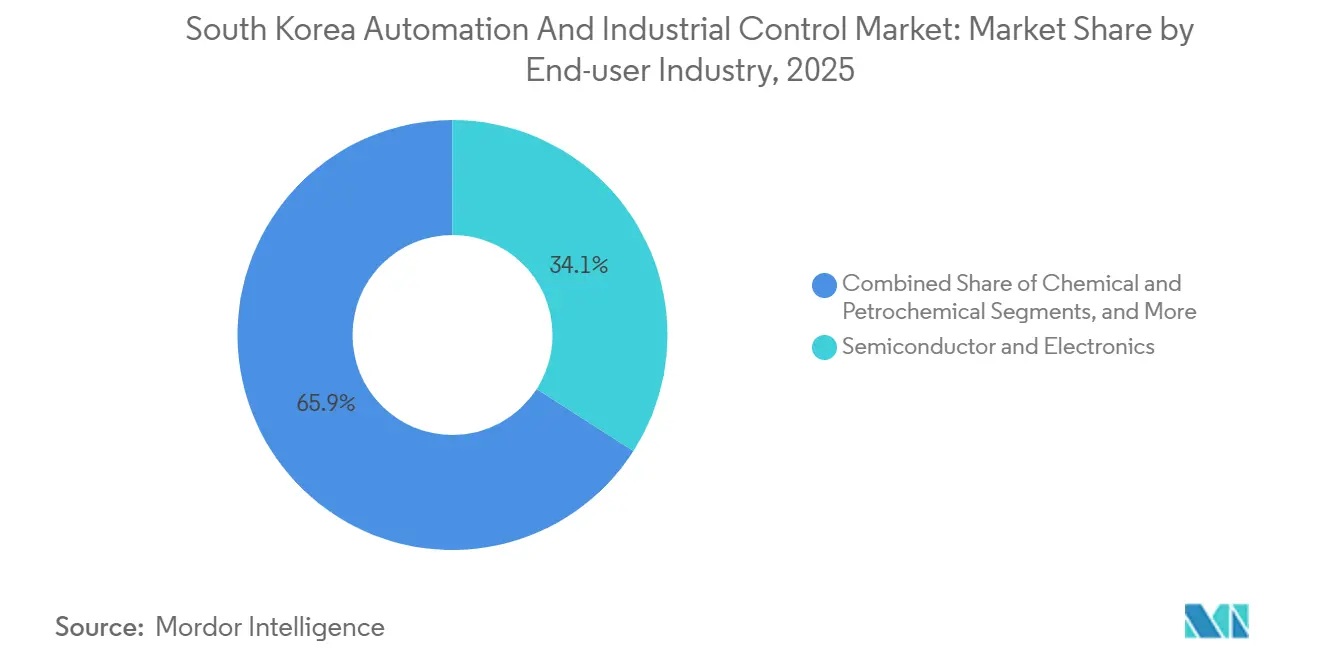

- By end-user industry, semiconductor and electronics held 34.07% of the automation and industrial control market share in 2025, whereas pharmaceutical and biotech facilities amongst the other end-user industries are advancing at a 6.52% CAGR through 2031.

- By control hierarchy, control devices captured 41.71% of 2025 spending, yet manufacturing execution and analytics layers are set to expand at 6.27% CAGR through 2031.

- By geography, Gyeonggi-do province commanded 26.93% revenue share in 2025; Jeolla Region registers the fastest CAGR at 6.87% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South Korea Automation And Industrial Control Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Smart Factory Subsidies and Tax Incentives | +0.8% | National focus on Gyeonggi-do, Jeolla and Gyeongsang | Medium term (2-4 years) |

| Surge in Semiconductor Fab Capacity Investments | +1.2% | Gyeonggi-do and Chungcheong | Long term (≥ 4 years) |

| Rising Labor Costs and Shrinking Workforce | +1.0% | Nationwide, acute in Seoul, Gyeonggi-do and Incheon | Long term (≥ 4 years) |

| 5G Private Networks Unlock Low-Latency Industrial IoT | +0.7% | Gyeonggi-do, Jeolla Region, Ulsan | Medium term (2-4 years) |

| Localization of Robot Core Components Under K-Robot Plan | +0.6% | National, manufacturing hubs in Changwon and Gwangju | Long term (≥ 4 years) |

| Cloud-Based AI Quality Analytics Adoption by SMEs | +0.5% | Nationwide, early uptake in Gyeonggi-do and Seoul | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Government Smart Factory Subsidies and Tax Incentives

The 2026 budget boosts smart-factory grants to KRW 436.56 billion (USD 336 million), covering up to 50% of PLC, HMI and MES costs for small companies. Tax credits rise to 20% of capex, climbing to 30% when 60% of the bill is sourced from domestic suppliers, thereby favoring LS Electric, CIMON and Doosan Robotics. A government-funded testbed in Daegu let 320 firms pilot DCS and SCADA setups in 2025, yielding an 18% throughput bump before investment commitments. ISO 9001 and ISO 14001 compliance now pre-qualifies applicants, encouraging widespread sensor upgrades to support real-time emissions monitoring.[1]Korea Agency for Technology and Standards, “ISO Certification Standards,” KATS.GO.KR

Surge in Semiconductor Fab Capacity Investments

SK hynix’s four-fab Yongin cluster broke ground in 2025, each facility demanding 12,000 motors, 45,000 sensors and 2,800 VFDs for cleanroom operations.[2]SK hynix, “SK hynix Breaks Ground on New Fab Cluster in Yongin,” SKHYNIX.COM Samsung’s contiguous six-fab expansion will lift combined capacity to 1.5 million wafers per month. Tool vendors such as ASML embedded redundant PLC architectures inside EUV units to ensure uptime, while provincial funding created an advanced-packaging hub that trains fabless firms on DCS platforms. Water-supply SCADA systems supervise 330,000 tons of daily flow from Hwacheon Dam to prevent contamination.

Rising Labor Costs and Shrinking Workforce

Manufacturing wages climbed 6.8% annually during 2020-2025 as Korea’s fertility rate fell to 0.72, fueling adoption of collaborative robots for battery-module assembly and pharmaceutical cleanrooms. The 4th Intelligent Robot Basic Plan allocates KRW 3 trillion (USD 2.3 billion) to deploy 1 million robots by 2030, including 400,000 in small factories. Hyundai Motor Group’s KRW 125.2 trillion (USD 96.3 billion) 2030 roadmap includes robotic production lines that hedge against workforce shortages.[3]Hyundai Motor Group, “Investment Plan 2026-2030,” HYUNDAIMOTORGROUP.COM

5G Private Networks Unlock Low-Latency Industrial IoT

A Samsung-Hyundai RedCap trial achieved 8 millisecond latency at Ulsan, enabling real-time AI visual inspection and mobile robot orchestration. LS Electric and Hyundai AutoEver deployed 4.7 GHz private 5G at Gwangju Global Motors, synchronizing 240 cobots and trimming battery line cycle time by 23%. LG CNS’s e-Um service now blankets steel mills and power plants, bringing predictive maintenance analytics to 18,000 motors without Wi-Fi handoff delays.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Initial Installation and Re-Engineering Costs | -0.6% | Nationwide, severe for SMEs in Gyeongsang, Chungcheong and Gangwon-do | Short term (≤ 2 years) |

| Cybersecurity and Data-Sovereignty Concerns in Connected Factories | -0.4% | National, critical sites in Gyeonggi-do and Seoul | Medium term (2-4 years) |

| Shortage of OHT-Certified and PLC Programming Talent | -0.3% | Nationwide, most acute in Jeolla Region and Jeju-do | Long term (≥ 4 years) |

| Supply Chain Volatility for Precision Motion Components | -0.3% | Nationwide, impacts robot and motor manufacturers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Initial Installation and Re-Engineering Costs

Retrofitting an automotive line can exceed KRW 1.17 billion (USD 900,000) once process-mapping, downtime and HMI upgrades are included. SMEs operate with debt-to-equity ratios near 180% and find payback horizons beyond three years tough to finance. Integration headaches rise when multivendor DCS assets require middleware that absorbs up to 20% of budgets. Cleanroom builds for pharma sites add KRW 2.8 billion (USD 2.15 million) per 500 square-meters, while rising power tariffs stretch ROI calculations for energy-intensive fabs.[4]Korea Electric Power Corporation, “Industrial Electricity Tariffs,” KEPCO.CO.KR

Cybersecurity and Data-Sovereignty Concerns in Connected Factories

KISA logged 47 ransomware attacks on OT networks in 2024, exposing gaps in network segmentation. The K-ICS framework now mandates air-gapped architectures at critical infrastructure, yet 5G private networks dissolve clear IT-OT boundaries. Data sovereignty rules keep MES logs on local soil, increasing cloud costs by 40%. SMEs rarely budget KRW 180 million (USD 138,000) for annual security assessments, leaving roughly 38,000 plants open to supply-chain malware propagation.[5]Korea Internet and Security Agency, “K-ICS Security Framework,” KISA.OR.KR

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Collaborative Robots Reshape Assembly Economics

Industrial robotics generated 49.83% of overall 2025 revenue, reflecting large-scale welding and wafer-handling deployments. The automation and industrial control market size for collaborative robots amongst the other products, however, is projected to grow at a 7.31% CAGR through 2031 as ISO 10218 compliance removes fencing and frees floor space in electronics and biotech cleanrooms. Doosan’s P3020 cobot, supporting a 30 kg payload, demonstrates the new economics by cutting system-integration costs by 35% in battery-module assembly cells.[6]Doosan Robotics, “P3020 Collaborative Robot Export,” DOOSANROBOTICS.COM PLCs and DCSs remain critical for deterministic 5-millisecond control loops in semiconductor wet benches, with LS Electric’s XGT series matching tier-one performance at lower price points. SCADA upgrades in water treatment underline the trend toward remote environmental compliance, while high-resolution HMIs such as Schneider’s Harmony iPC extend display life under aggressive wash-down regimes.

Step-change product innovation is visible in edge-AI vision sensors that sample at 10 Hz and push predictive quality analytics straight to cloud historians, compressing fault-detection latency. ABB’s System 800xA deployments at petrochemical sites integrate SIL 3 safety logic, underlining how process-risk regulation supports advanced control spend. The product mix therefore tilts toward smarter, safer and more people-friendly form factors even as classic six-axis frames dominate installed bases.

By Component: Software Monetization Gains Traction

Hardware captured 60.59% of 2025 revenue, yet software is tracking a 6.02% CAGR to 2031 as subscription models proliferate. The automation and industrial control market now rewards vendors that wrap PLC firmware in AI-driven predictive-maintenance dashboards. LG Electronics’ MAVIN-Cloud reduced false defect alerts by 95% after ingesting 18 months of image data, proving the value of cloud-native analytics. CIMON’s SCADA X 3.0 eliminates dedicated HMI panels, saving KRW 85 million per line and validating software’s deflationary role.[7]CIMON, “SCADA X 3.0,” CIMON.CO.KR Five-year service bundles already deliver 28% of LS Electric’s automation turnover, confirming that outcome-based support is a durable revenue hedge as hardware ASPs fall.

Market-wide, SaaS MES and digital-twin simulators gain favor among cash-constrained SMEs reluctant to fund perpetual licenses. Edge gateways now embed inference engines and OPC UA stacks, further blurring hardware-software lines. As private 5G extends to plant perimeters, usage-based software pricing looks set to accelerate, aligning costs with value captured.

By End-User Industry: Pharmaceutical Automation Accelerates

Semiconductor and electronics sites held 34.07% of 2025 revenue, yet pharma and biotech facilities amongst the other end-user industries will outpace with a 6.52% CAGR to 2031. Samsung Biologics’ Plant 5 alone added 28,000 sensors and 1,200 safety interlocks in 2025, testifying to biologics’ automation intensity. Cytiva’s Songdo hub supplies shared GMP-compliant equipment, enabling startups to sidestep high capex barriers. Automotive electrification also sustains collaborative-robot demand; Hyundai deployed 8,400 units in 2025 for battery packs and thermal-management sub-assemblies. Oil, gas and petrochemical complexes extend compressor overhaul intervals via vibration analytics, squeezing additional value from established control layers.

Food and beverage, pulp and paper and water-treatment plants round out the adopter pool. HACCP and phosphorus removal mandates respectively drive traceability and chemical-dosing upgrades. Cross-sector synergies appear as time-sensitive networking lets field devices feed cloud AI models without hierarchical detours, though cybersecurity policies could slow full adoption.

By Control Hierarchy Level: Edge Intelligence Reshapes Architectures

Control devices, PLCs and DCSs, captured 41.71% of spend in 2025, yet MES and analytics layers are projected to grow at a 6.27% CAGR through 2031 as plants flatten architectures. POSCO DX’s TensorFlow-enabled PLC dropped alert latency from 120 ms to 8 ms, demonstrating why inference is migrating toward field gear. Field devices, packed with sensors and actuators, remain the data spine for AI models: SICK’s time-of-flight sensors maintained ±1 mm accuracy across 1,800 cobot stations last year.

Supervisory systems now orchestrate multi-site optimization; Yokogawa’s controllers knit 18 water-treatment plants into one dashboard, cutting energy 14%. Meanwhile, Renesas dual-Ethernet processors reinforce redundant networking in high-purity fabs. The trade-off is cyber risk, prompting KISA guidance on segmentation and OT IDS deployment.

Geography Analysis

Gyeonggi-do province generated 26.93% of 2025 revenue thanks to the Yongin and Pyeongtaek fab clusters, each fab requiring tens of thousands of motion devices and sensors. The automation and industrial control market size attributable to these mega projects will expand steadily as six additional lines reach first-wafer output by 2030. Provincial grants worth KRW 41.3 billion (USD 31.8 million) opened an advanced-packaging center that trains fabless firms on DCS use, lowering entry hurdles and extending local value chains. Supplier colocation by ASML, Lam Research and Tokyo Electron creates pull-through for PLCs and HMIs capable of proprietary protocol interfacing. Infrastructure SCADA solutions regulate 330,000 tons per day of ultrapure water, highlighting how utilities spending complements direct equipment orders.

Jeolla Region, hosting the National AI Data Center and Bitgreen vehicle complex, is forecast to record a 6.87% CAGR to 2031. The Future Vehicle Triangle Belt attracted 90 tenant companies by 2025, each installing 5G-linked cobots and variable-frequency drives. VENA Energy’s KRW 20 trillion renewable and data-center commitment adds fresh demand for UPSs and grid DCSs. Regional R&D capacity, exemplified by the AI CNC Center in Changwon, shortens the time between prototype and production, accelerating adoption among machinery makers.

Seoul and Incheon exploit airport proximity to ensure 12-hour customs clearance for EUV spares, anchoring time-sensitive equipment flows. Gyeongsang’s Changwon Smart Green Industrial Complex deployed 3,200 industrial robots in 2025, revealing strong appetite among machinery exporters. Chungcheong leverages links to Sejong research institutes for pilot smart-factory schemes. Gangwon-do and Jeju-do remain light-industry zones, yet food processors there upgraded HMIs for export-grade traceability in 2025, signaling that even peripheral regions participate in the automation wave.

Competitive Landscape

Market concentration sits at a moderate level: the top five suppliers hold roughly 48% of 2025 revenue. Siemens, ABB, Schneider Electric, Yokogawa and LS Electric dominate DCS and PLC layers, yet white-space persists in collaborative robots and sensor niches where 17 Korean startups launched products during 2024-2025. Localization agendas matter; tax bonuses tied to domestic content drive LS Electric and Doosan Robotics to scale local servo-motor output, while LG Innotek started robot-parts production targeting 20% domestic share by 2028. Technology differentiation hinges on edge AI and 5G integration. Samsung’s 8 millisecond latency demo at Hyundai Ulsan underscores an advantage that legacy SCADA cannot match without heavy retrofit.

LS Electric aligns its XGT PLCs with Rockwell’s FactoryTalk to satisfy data-sovereignty rules while tapping global analytics that indicate partnerships are becoming a strategic, win-win growth lever. Vendor compliance with K-ICS cybersecurity mandates became a key selection criterion after 47 ransomware incidents in 2024. Patent intensity also rises; predictive-maintenance filings jumped 68% in 2024, led by Hyundai Motor, Samsung and LG. Against that backdrop, Rainbow Robotics’ USD 80,000 dual-arm mobile manipulator and POSCO DX’s AI-infused PLC exemplify challenger plays that could compress incumbent margins.

South Korea Automation And Industrial Control Industry Leaders

Yokogawa Electric Corporation

ABB Limited

Schneider Electric SE

Doosan Robotics Inc.

LS Electric Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: The ROK Navy finished the Busan Smart Naval Port with Samsung and KT, installing 5G-linked sensors and SCADA to cut vessel turnaround 14%.

- October 2025: VENA Group signed a KRW 20 trillion Jeolla investment LOI covering renewables and AI data centers.

- April 2025: Samsung Biologics activated Plant 5, adding 784,000 liters of capacity and 28,000 sensors.

- April 2025: Doosan Robotics exported 300 P3020 cobots to Southeast Asia.

South Korea Automation And Industrial Control Market Report Scope

Factory automation refers to the use of control systems, machinery, and computer systems to automate industrial processes and tasks, reducing the need for human intervention. This includes processes like manufacturing, material handling, and quality control. The industrial controls market encompasses the products and systems used to monitor and control various industrial processes. This includes components like programmable logic controllers (PLCs), human-machine interfaces (HMIs), sensors, and software that manage and optimize the operation of machinery and equipment in industrial settings.

The South Korea Automation and Industrial Control Market Report is Segmented by Product (Programmable Logic Controllers, Distributed Control Systems, Supervisory Control and Data Acquisition Systems, Human Machine Interface, Process Safety Systems, Sensors and Transmitters, Electric Motors, Variable Frequency Drives, Industrial Robotics, Other Product Technologies), Component (Hardware, Software, Services), End-user Industry (Automotive, Chemical and Petrochemical, Semiconductor and Electronics, Oil and Gas, Power Generation, Water and Wastewater, Other End-user Industries), Control Hierarchy Level (Field Devices, Control Devices, Supervisory and SCADA Systems, Manufacturing Execution and Analytics), and Geography (Seoul, Gyeonggi-do, Incheon, Gangwon-do, Chungcheong Region, Jeolla Region, Gyeongsang Region, Jeju-do). The Market Forecasts are Provided in Terms of Value (USD).

| Programmable Logic Controllers (PLC) |

| Distributed Control Systems (DCS) |

| Supervisory Control and Data Acquisition Systems (SCADA) |

| Human Machine Interface (HMI) |

| Process Safety Systems |

| Sensors and Transmitters |

| Electric Motors |

| Variable Frequency Drives |

| Industrial Robotics |

| Other Product Technologies |

| Hardware |

| Software |

| Services |

| Automotive |

| Chemical and Petrochemical |

| Semiconductor and Electronics |

| Oil and Gas |

| Power Generation |

| Water and Wastewater |

| Other End-user Industries |

| Field Devices (Sensors, Actuators) |

| Control Devices (PLC, DCS) |

| Supervisory and SCADA Systems |

| Manufacturing Execution, Analytics and Other Control Hierarchy Levels |

| By Product | Programmable Logic Controllers (PLC) |

| Distributed Control Systems (DCS) | |

| Supervisory Control and Data Acquisition Systems (SCADA) | |

| Human Machine Interface (HMI) | |

| Process Safety Systems | |

| Sensors and Transmitters | |

| Electric Motors | |

| Variable Frequency Drives | |

| Industrial Robotics | |

| Other Product Technologies | |

| By Component | Hardware |

| Software | |

| Services | |

| By End-user Industry | Automotive |

| Chemical and Petrochemical | |

| Semiconductor and Electronics | |

| Oil and Gas | |

| Power Generation | |

| Water and Wastewater | |

| Other End-user Industries | |

| By Control Hierarchy Level | Field Devices (Sensors, Actuators) |

| Control Devices (PLC, DCS) | |

| Supervisory and SCADA Systems | |

| Manufacturing Execution, Analytics and Other Control Hierarchy Levels |

Key Questions Answered in the Report

What is the current value of the South Korea automation and industrial control market?

The market is valued at USD 7.04 billion in 2026 and is forecast to reach USD 9.23 billion by 2031.

Which product segment is expanding the fastest?

Collaborative robots are projected to grow at a 7.31% CAGR through 2031 as cleanrooms and electronics lines adopt ISO 10218-compliant systems.

Why are semiconductor fabs so important for automation demand?

Projects from SK hynix and Samsung require tens of thousands of motors, sensors and safety systems, anchoring long-term equipment orders.

How do government incentives influence adoption among small firms?

Grants cover up to 50% of smart-factory capex and tax credits reach 30% when locally made hardware is used, halving payback periods to roughly two years.

What cybersecurity challenges do connected factories face?

Ransomware incidents surged, prompting K-ICS rules that require air-gapped or segmented OT networks and local data storage to meet sovereignty laws.

Which region is growing fastest?

Jeolla Region leads with a 6.87% CAGR, fueled by the National AI Data Center and electric-vehicle industrial complexes.

Page last updated on: