Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

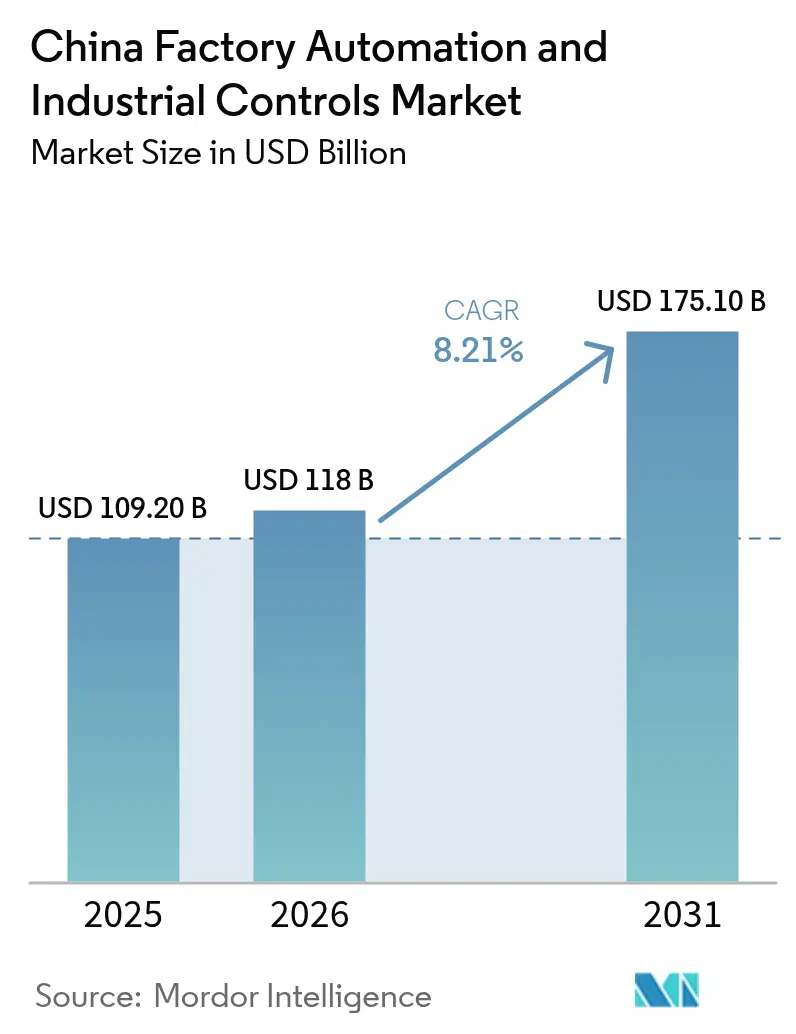

| Base Year Market Size (2025) | USD 109.20 Billion |

| Market Size (2026) | USD 118 Billion |

| Market Size (2031) | USD 175.10 Billion |

| Growth Rate (2026 - 2031) | 8.21% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Factory Automation And Industrial Controls Market Analysis by Mordor Intelligence

The China Factory Automation And Industrial Controls Market size is projected to be USD 109.20 billion in 2025, USD 118 billion in 2026, and reach USD 175.10 billion by 2031, growing at a CAGR of 8.21% from 2026 to 2031.

Unprecedented venture-capital funding, Made-in-China 2025 mandates, and the accelerated roll-out of smart-factory projects in Guangdong, Jiangsu, and Zhejiang anchor demand for industrial robots, PLCs, and next-generation control software. The policy framework compels manufacturers to raise local content across core automation components, fueling scale advantages for domestic suppliers and encouraging faster technology diffusion into small and midsize enterprises. Meanwhile, electrification of transport and battery gigafactory build-outs spur investments in flexible, AI-enabled production lines that can switch among multiple vehicle models without disruptive re-tooling. At the same time, legacy OT cybersecurity gaps and a digital-talent shortfall of more than 4 million workers pose structural risks, yet the upward trajectory remains intact as discrete manufacturing continues to absorb advanced robotics to offset rising labor costs and quality-control pressures.

Key Report Takeaways

- By component, hardware led with 59.98% revenue share in 2025 in the China factory automation and industrial controls market, while software is projected to post the fastest 12.54% CAGR to 2031.

- By control system type, PLCs accounted for 32.24% of China factory automation and industrial controls market share in 2025 and are advancing at an 11.62% CAGR through 2031.

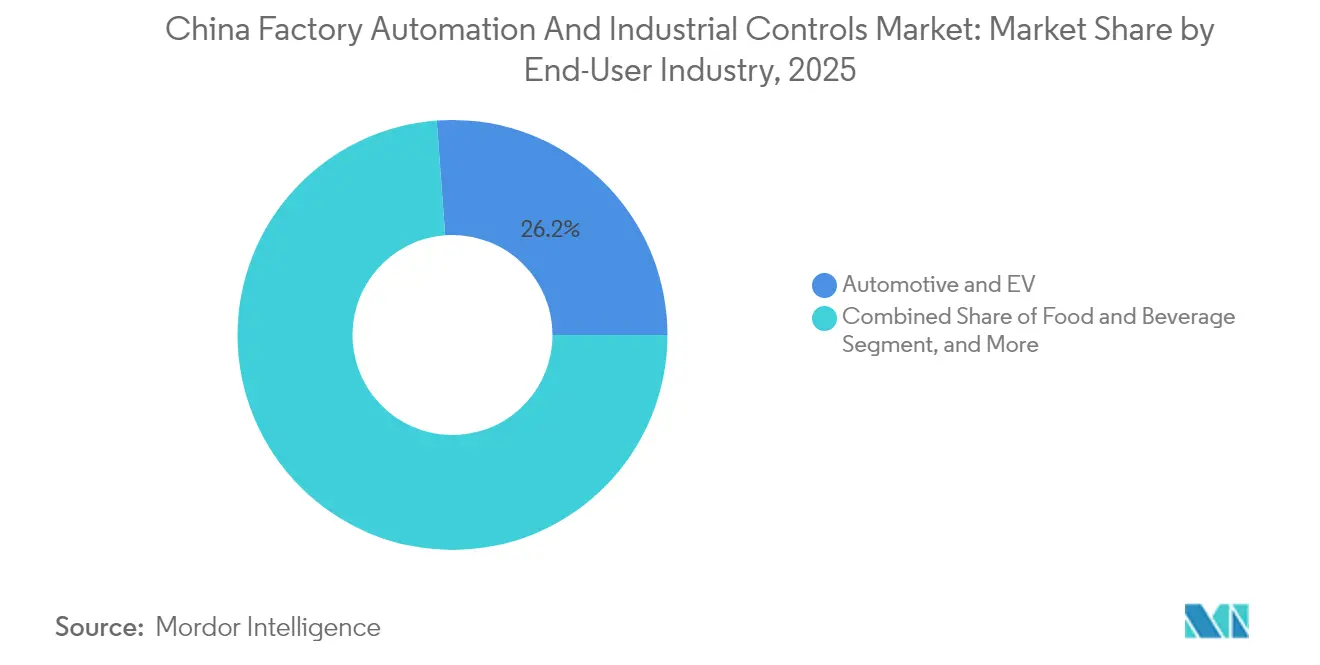

- By end-user industry, the automotive and EV segment held 26.17% share of the China factory automation and industrial controls market automation market size in 2025 and is expanding at an 11.33% CAGR through 2031.

- By automation solution, discrete automation commanded 45.05% share in 2025 in the China factory automation and industrial controls market, whereas hybrid automation is set to register a 12.12% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Factory Automation And Industrial Controls Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid adoption of Industrial Internet-of-Things (IIoT) platforms | +2.1% | Global, with concentration in Guangdong, Jiangsu, Zhejiang | Medium term (2-4 years) |

| Government incentives for "Made-in-China 2025" smart-manufacturing upgrades | +2.8% | National, with early gains in tier-1 manufacturing cities | Long term (≥ 4 years) |

| Accelerated demand for flexible manufacturing from EV and battery gigafactories | +1.9% | Asia Pacific core, spill-over to global EV supply chains | Short term (≤ 2 years) |

| Edge-AI based predictive-maintenance reducing unplanned downtime | +1.4% | Global, with pilot deployments in Chinese smart factories | Medium term (2-4 years) |

| On-premise 5G private networks enabling ultra-reliable low-latency control | +1.6% | National, concentrated in industrial parks and manufacturing clusters | Medium term (2-4 years) |

| Rising labor-cost inflation driving robotic substitution in SMEs | +1.4% | National, particularly affecting labor-intensive manufacturing regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Incentives for Made-in-China 2025 Smart Manufacturing Upgrades

Beijing orchestrates one of the world’s largest industrial-policy programs, coupling a CNY 1 trillion state-backed venture fund with MIIT guidelines that require 70% domestic content in core automation parts by 2025.[1]RoboticsTomorrow Staff, “China to Invest 1 Trillion Yuan in Robotics and High-Tech Industries – IFR Reports,” RoboticsTomorrow, roboticstomorrow.com Provincial subsidies worth USD 9.7 billion are earmarked for SME automation retrofits, allowing even resource-constrained factories to deploy collaborative robots and edge-computing hubs. Together, procurement preferences, tax rebates, and fast-track approvals create a self-reinforcing cycle of localized supply chains, more competitive pricing, and quick technology adoption. Automation vendors benefit from guaranteed demand, while manufacturers gain faster ROI from interconnected production lines that deliver higher throughput, consistent quality, and lower energy consumption. The policy suite also embeds data-sovereignty requirements, driving uptake of domestic IIoT platforms that keep sensitive shop-floor data within China’s borders.

Accelerated Demand for Flexible Manufacturing from EV and Battery Gigafactories

Electric-vehicle OEMs and cell makers are scaling production at unprecedented speed, driving a surge in demand for modular, AI-driven automation. CATL, BYD, and Gotion deployed more than 20,000 robots in 2024 to support 24/7 lithium-ion cell output while achieving 99.5% quality-inspection accuracy. XPeng’s USD 13.8 billion humanoid-robotics initiative underscores the need for agile lines capable of multivehicle production in a single facility. Tesla’s Shanghai Gigafactory has set a 750,000-unit annual benchmark that Chinese rivals aim to replicate through digital twins and synchronized PLC-robot architectures. These programs anchor long-term orders for motion controllers, drives, and machine-vision systems made by domestic suppliers, further lifting the China Factory Automation and Industrial Controls Market.

Rapid Adoption of Industrial Internet-of-Things (IIoT) Platforms

Manufacturers are integrating thousands of sensors, cameras, and controllers into unified IIoT fabrics to boost OEE and trim energy use. Midea Group connected 10,000 devices and recorded a 27% uptick in OEE alongside a 20% cut in power consumption.[2]Schneider Electric, “Shanghai Baosteel Group Corporation,” Schneider Electric, schneider-electric.com Shanghai Electric’s humanoid-robot plant pairs IIoT connectivity with AI-enabled cranes that handle 98% of material movements autonomously, lowering mechanical wear and labor inputs. The regulatory tilt toward local platforms such as Kaos Industrial Internet, engineered to meet China’s Cybersecurity Law, accelerates deployment among OEMs wary of cross-border data risks. As multi-tier suppliers hook into OEM digital ecosystems, network effects magnify benefits, spreading best practices across the entire China Factory Automation and Industrial Controls Market.

Edge-AI-Based Predictive Maintenance Reducing Unplanned Downtime

Latency-sensitive production lines turn to edge AI to interpret vibration, temperature, and current signatures in milliseconds, predicting anomalies before breakdowns occur. Advantech’s iFactory PHM deployment on robot arms in panel manufacturing lifted output and curtailed scrap through unsupervised fault detection.[3]Advantech Case Study Team, “Increase Production Efficiency and Product Yield for Robot Arms,” Advantech, advantech.com Jiangsu Yinbao Salt’s smart factory secured 18.3% productivity gains after embedding vision algorithms that flag micro-defects in real time. Domestic chipmaker Rockchip now supplies RK3588S processors for Unitree humanoid robots, indicating a deepening localized AI hardware stack that lessens exposure to foreign export controls. The resulting hike in equipment availability feeds directly into higher plant throughput and margin resilience for China Factory Automation and Industrial Controls Market participants.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-security vulnerabilities in legacy OT systems | -1.8% | Global, with particular exposure in manufacturing regions with older infrastructure | Short term (≤ 2 years) |

| Fragmented industrial communication standards hindering interoperability | -1.2% | National, affecting cross-vendor system integration | Medium term (2-4 years) |

| Shortage of domain-skilled automation engineers | -1.5% | National, with acute shortages in tier-2 and tier-3 cities | Long term (≥ 4 years) |

| Capital-expenditure freezes in export-oriented factories amid geo-economic risk | -1.3% | Global, with concentration in export-heavy coastal manufacturing regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cyber-Security Vulnerabilities in Legacy OT Systems

The INCONTROLLER malware episode exposed gaping holes in decades-old PLCs and SCADA nodes that were never designed for Internet connectivity. As factories connect to IIoT clouds for analytics, these soft spots invite ransomware, intellectual-property theft, and potential safety incidents. Operators must now layer zero-trust architectures, local data centers, and continuous patching routines onto production networks, inflating capex and project timelines. Heightened geopolitical tensions intensify scrutiny of foreign firmware and chipsets, nudging buyers toward trusted domestic vendors even when performance is on par. The immediate capex burden slightly tempers the otherwise robust CAGR of the China Factory Automation and Industrial Controls Market.

Fragmented Industrial Communication Standards Hindering Interoperability

Manufacturers juggle EtherCAT, PROFINET, and emerging Chinese protocols, often within the same facility, complicating line expansions and boosting integration costs. SMEs, representing 90% of factories, feel the pinch most acutely as they lack in-house OT engineers to navigate overlapping standards. Gateways and protocol converters offer temporary relief, but they add latency and maintenance overhead, sometimes discouraging smaller projects. Policymakers encourage convergence toward localized standards, yet the installed base of foreign equipment means multi-protocol environments will persist for years, dampening the pace at which the China Factory Automation and Industrial Controls Market can standardize.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Growth Outpaces Hardware Dominance

Hardware contributed 59.98% of 2025 revenue, anchored by record robot and servo-drive installations, yet software is poised to grow at a 12.54% CAGR as factories chase AI-enabled optimization. Domestic robot vendors lifted their local share from 17.5% in 2015 to 32% in 2024, signaling rapid catch-up on payload, repeatability, and mean-time-between-failure metrics.

Services, though currently the smallest slice, secure consistent demand for systems integration, operator upskilling, and lifecycle support, forming annuity-style cash flows. As adoption deepens, manufacturers shift focus from mechanical installation to data-driven performance gains, rerouting budgets toward MES, APS, and digital twins that amplify return on fixed assets. The result is a virtuous cycle: advanced software squeezes extra throughput from existing machines, encouraging further investment and sustaining momentum in the China Factory Automation and Industrial Controls Market.

By Control System Type: PLCs Dominate Across All Segments

Programmable Logic Controllers held a commanding 32.24% share in 2025 and are on track to log an 11.62% CAGR to 2031, affirming their centrality in both discrete and process plants. Domestic firms such as Inovance Technology and STEP Electric steadily erode Western incumbents’ leads by bundling local support with competitive pricing and firmware tuned for Chinese standards.

Small PLCs post 5.6% growth as SMEs automate single-purpose stations, while mid-to-large models still favor multinationals for mission-critical applications in petrochemicals and power. Complementary SCADA and DCS layers flourish in continuous industries, whereas HMI panels expand with each new robot cell. Motion-controller demand mirrors the robotics surge, underpinning growth across all nodes of the china factory automation industry.

By End-User Industry: Automotive and EV Sector Leads Adoption

Automotive and EV lines absorbed 26.17% of automation spend in 2025 and should compound at 11.33% through 2031 as OEMs race to diversify model portfolios and battery chemistries. Seres Group’s Chongqing plant showcases 100% automated welding and a 30-second takt time, setting a new domestic benchmark.

Electronics and semiconductors remain a close second, leveraging clean-room robots and high-precision pick-and-place systems to maintain sub-10-micron tolerances. Food-and-beverage processors automate palletizing and traceability to comply with stringent safety codes, while chemicals and metals exploit remote-operation capabilities to protect workers from hazardous processes. The breadth of applications underscores the resilience of demand across the China Factory Automation and Industrial Controls Market.

By Automation Solution: Discrete Automation Leads with Hybrid Growth

Discrete automation secured 45.05% revenue share in 2025 due to high robot density in welding, painting, and electronics assembly. Process automation thrives in chemical, oil-and-gas, and bulk-material handling, but hybrid systems are climbing fastest at a 12.12% CAGR as factories blend batch and continuous workflows under unified control.

Shangmei Technology Park’s cosmetics plant integrates 12 lights-out lines, 30 AGVs, and 42 articulated robots, cutting labor needs by 75% and illustrating how hybrid layouts improve both flexibility and cost structure. Hybrid adoption widens the addressable base, enabling the China Factory Automation and Industrial Controls Market to penetrate industries where production modes once limited automation ROI.

Geography Analysis

The China factory automation and industrial controls market clusters along the coast, with Guangdong, Jiangsu, and Zhejiang housing more than 30,000 smart factories that anchor demand for sensors, drives, and AI-enabled analytics. Guangdong’s Pearl River Delta leverages dense electronics and auto supply chains to pilot cobots and vision-guided inspection stations that slash takt times for smartphones and EVs alike. Shenzhen’s concentration of component suppliers fosters a rapid prototype-to-production loop that keeps deployment costs low and learning cycles short. Jiangsu showcases balanced sector exposure, ranging from chemicals to machinery, while Suzhou’s rise as an automation hub was cemented when Mitsubishi Electric designated the city its local FA headquarters, signaling confidence in the region’s technical talent and logistics infrastructure.

Zhejiang’s specialization in precision machinery and textiles drives niche applications such as AI-driven loom monitoring and automated packaging lines for small appliances. Access to Shanghai’s ports and finance accelerates global partnerships, enabling faster import of high-spec servo drives yet also empowering local firms to compete abroad. Inland, Chongqing and Sichuan leverage lower operating costs and central-government incentives to attract automotive and aerospace production. Changan Automobile’s multi-model line in Chongqing, capable of assembling four vehicles concurrently within 15 hours, exemplifies inland capabilities catching up with coastal peers. Shaanxi, benefiting from aerospace spillovers, deploys collaborative robots for composite-material layup, underscoring the diffusion of high-end automation beyond legacy manufacturing corridors. The geographic spread mitigates regional demand shocks and broadens the China Factory Automation and Industrial Controls Market.

Competitive Landscape

Global majors-ABB, Siemens, Schneider Electric, and Rockwell Automation, retain technological edges in high-precision and safety-critical domains but face swift domestic encroachment. Local champions such as Inovance Technology, STEP Electric, and Hollysys expand through tailored firmware, rapid on-site support, and government-linked purchasing frameworks. Domestic servo suppliers seized a 37% share in 2024, up five points year-over-year, illustrating accelerated catch-up in performance and reliability. Foreign firms respond by localizing R&D, entering joint ventures, and focusing on advanced motion control, functional safety, and green-factory solutions where their IP advantage remains material.

The next competitive frontier stretches into humanoid robotics and edge-AI ecosystems, with firms vying to set de facto standards that lock in customers for multi-decade maintenance and upgrade cycles. As software share rises, platform stickiness and third-party developer networks become decisive, tilting value capture toward companies that can fuse hardware, analytics, and cybersecurity into a single offering adaptable to China’s evolving regulatory environment. This evolving rivalry keeps pricing keen and drives relentless innovation across the China Factory Automation and Industrial Controls Market.

China Factory Automation And Industrial Controls Industry Leaders

Schneider Electric SE

Honeywell International Inc.

ABB Ltd.

Rockwell Automation, Inc.

Emerson Electric Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: China’s NDRC opened a 1 trillion-yuan venture fund to propel robotics and AI, marking the largest industrial-automation investment globally.

- March 2025: Mitsubishi Electric set up an FA business headquarters in Suzhou to sharpen local product planning and shorten delivery cycles.

- March 2025: Pacific Precision Forging invested CNY 100 million in a humanoid-robot joint venture to manufacture precision reducers and drives.

- March 2025: Guilin Fuda purchased a 35% stake in Changban Yangzhou Robot Technology to mass-produce 10,000 precision screw units annually for humanoid and industrial robots.

China Factory Automation And Industrial Controls Market Report Scope

The China Factory Automation and Industrial Controls Market Report is Segmented by Component (Hardware, Software, Services), Control System Type (Distributed Control Systems (DCS), Programmable Logic Controllers (PLC), Supervisory Control and Data Acquisition (SCADA), Human-Machine Interface (HMI), Motion Controllers and Drives), End-User Industry (Automotive and EV, Electronics and Semiconductor, Food and Beverage, Chemicals and Petrochemicals, Metals and Mining, Other End-User Industries), and Automation Solution (Discrete Automation, Process Automation, Hybrid Automation). The Market Forecasts are Provided in Terms of Value (USD).

By Component

| Hardware |

| Software |

| Services |

By Control System Type

| Distributed Control Systems (DCS) |

| Programmable Logic Controllers (PLC) |

| Supervisory Control and Data Acquisition (SCADA) |

| Human-Machine Interface (HMI) |

| Motion Controllers and Drives |

By End-User Industry

| Automotive and EV |

| Electronics and Semiconductor |

| Food and Beverage |

| Chemicals and Petrochemicals |

| Metals and Mining |

| Other End-User Industries |

By Automation Solution

| Discrete Automation |

| Process Automation |

| Hybrid Automation |

| By Component | Hardware |

| Software | |

| Services | |

| By Control System Type | Distributed Control Systems (DCS) |

| Programmable Logic Controllers (PLC) | |

| Supervisory Control and Data Acquisition (SCADA) | |

| Human-Machine Interface (HMI) | |

| Motion Controllers and Drives | |

| By End-User Industry | Automotive and EV |

| Electronics and Semiconductor | |

| Food and Beverage | |

| Chemicals and Petrochemicals | |

| Metals and Mining | |

| Other End-User Industries | |

| By Automation Solution | Discrete Automation |

| Process Automation | |

| Hybrid Automation |

Key Questions Answered in the Report

What is the projected value of China factory automation market in 2031?

It is forecast to reach USD 175.1 billion by 2031, rising at an 8.21% CAGR.

Which component segment is growing fastest?

Software is expanding at a 12.54% CAGR as factories prioritize AI and analytics.

Why do automotive and EV plants dominate adoption?

They require flexible, high-throughput lines to meet soaring EV demand and quality goals, accounting for 26.17% of 2025 spend.

How is government policy influencing supplier choice?

Made-in-China 2025 mandates 70% local content, steering purchases toward domestic PLC, servo, and IIoT vendors.

What is the main cybersecurity risk in smart factories?

Legacy PLCs and SCADA nodes lack modern protections, exposing production lines to malware and disruptive attacks.

Which region is emerging as a hub for localized automation R&D?

Suzhou in Jiangsu Province, where Mitsubishi Electric set its China FA headquarters in 2025.

Page last updated on: