United Kingdom Factory Automation And Industrial Control Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

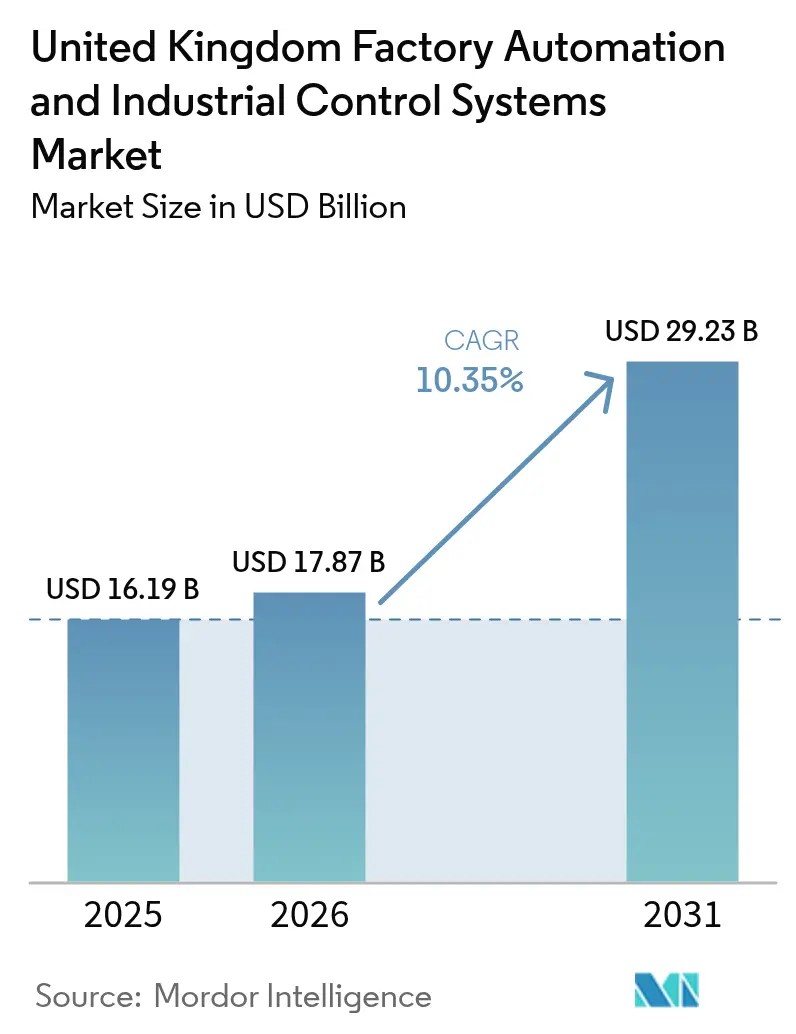

| Base Year Market Size (2025) | USD 16.19 Billion |

| Market Size (2026) | USD 17.87 Billion |

| Market Size (2031) | USD 29.23 Billion |

| Growth Rate (2026 - 2031) | 10.35% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Factory Automation And Industrial Control Systems Market Analysis by Mordor Intelligence

The United Kingdom factory automation and industrial control systems market size is expected to grow from USD 16.19 billion in 2025 to USD 17.87 billion in 2026 and is forecast to reach USD 29.23 billion by 2031 at 10.35% CAGR over 2026-2031. The outlook reflects a convergence of labor shortages, government-backed digitalization programs, rising energy prices, and the push for low-carbon production, all of which sharpen the economic rationale for end-to-end automation. Strong fiscal signals, such as the Modern Industrial Strategy’s USD 4.3 billion commitment to advanced manufacturing grants and R&D, reinforce private-sector momentum, while the scheduled 25% reduction in industrial electricity costs from 2027 materially improves the payback profile for capital-intensive automation projects.[1]Department for Science, Innovation & Technology, “AI Opportunities Action Plan,” GOV.UK, gov.ukFactory owners also attribute Brexit-related supply chain volatility to the acceleration of investment in autonomous systems that buffer against cross-border staffing and logistics risks, as evidenced by a 72% increase in imported industrial robots over the past two years. Concurrently, the Product Security and Telecommunications Infrastructure Act raises the compliance bar for connectable devices, catalyzing demand for secure-by-design control platforms and opening service opportunities for cybersecurity-focused integrators. Against this backdrop, the United Kingdom factory automation and industrial control systems market is transitioning from isolated hardware upgrades toward holistic, software-defined architectures that fuse operational technology (OT) with information technology (IT).

Key Report Takeaways

- By type, industrial control systems led with 58.15% revenue share in 2025 in the United Kingdom factory automation and industrial control systems market, while field devices are projected to expand at a 11.87% CAGR through 2031.

- By end-user, the automotive and transportation sector commanded 28.33% of the United Kingdom's factory automation and industrial control systems market share in 2025; the pharmaceutical and life sciences sector is advancing at a 13.77% CAGR through 2031.

- By component, automation hardware accounted for 46.85% of the United Kingdom factory automation and industrial control systems market size in 2025, and automation software is growing at an 12.7% CAGR over the forecast horizon.

- By industrial communication network, industrial Ethernet held a 43.25% share in the United Kingdom factory automation and industrial control systems market in 2025, while private 5G/LTE is poised for an 12.73% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Factory Automation And Industrial Control Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government incentives via United Kingdom "Made Smarter" programme | +1.8% | National, with early gains in North West, West Midlands, Yorkshire | Medium term (2-4 years) |

| Labour-shortage-led automation demand | +2.1% | National, concentrated in manufacturing regions | Short term (≤ 2 years) |

| Industrial IoT and Industry 4.0 uptake | +1.6% | England core, spill-over to Scotland and Wales | Medium term (2-4 years) |

| Energy-efficiency and decarbonisation goals | +1.4% | National, with emphasis on electricity-intensive sectors | Long term (≥ 4 years) |

| Private 5G campus networks for real-time control | +1.2% | England manufacturing corridors, selective Scotland deployment | Medium term (2-4 years) |

| Surge in pharma and battery gigafactory CAPEX | +0.9% | England South West, West Midlands, selective Northern Ireland | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government incentives via United Kingdom “Made Smarter” programme

Made Smarter has evolved from a regional pilot into a national policy instrument that lowers adoption risk for small and mid-sized manufacturers. The program delivered USD 242 million in net economic value in the North West alone and now supports more than 5,500 SMEs under the widened Industrial Strategy framework. Regional “technology translation” hubs diffuse best practices, helping firms trial digital twins, collaborative robots, and advanced analytics before committing significant capital. Peer-to-peer case studies published by hub leads shorten due-diligence cycles, while new procurement rules favor suppliers that demonstrate verifiable productivity or decarbonization gains. Together, these mechanisms compress payback periods and extend automation beyond large OEMs into the broader supply chain.

Labor-shortage-led automation demand

A persistent vacancy rate across British manufacturing has shifted board-level priorities toward immediate throughput improvements. Employers faced 55,000 unfilled shop-floor roles in 2025, prompting many to substitute hard-to-source labor with robotic welding, smart conveyors, and automated storage systems. Robot imports rose 72% post-Brexit as firms hedged against restricted EU labor flows. Apprenticeship starts in advanced manufacturing climbed 41% at Make United Kingdom member companies, signaling parallel investment in human capital. Yet the scarcity of certified automation engineers prolongs deployment cycles, driving demand for turnkey systems-integration services.

Industrial IoT and Industry 4.0 uptake

Maturing edge-compute platforms, coupled with local 5G networks, allow sub-10 millisecond response times essential for closed-loop motion control at flagship sites such as Jaguar Land Rover’s Solihull plant and Worcester Bosch’s boiler facility.[2]Manufacturing Technology Centre, “Private 5G Testbed Capabilities,” THE-MTC.ORG, the-mtc.org The AI Opportunities Action Plan allocates USD 2 billion for compute infrastructure and testbeds dedicated to industrial digital twins, reinforcing a pipeline of AI-driven manufacturing solutions. Open-source frameworks like Factory+ from the University of Sheffield’s AMRC standardize an enterprise-grade “unified namespace,” which reduces vendor lock-in and offers SMEs big-company data transparency at minimal cost.[3]University of Sheffield Advanced Manufacturing Research Centre, “AMRC Journal, Issue 18,” AMRC.CO.UK, amrc.co.uk As a result, factory operators gain plant-wide visibility, predictive maintenance insights, and rapid recipe changeovers.

Energy-efficiency and decarbonization goals

The Industrial Energy Transformation Fund injected USD 51.9 million into 25 projects that deploy variable-speed drives, heat recovery loops, and hydrogen-ready combustion systems. Eligible electricity-intensive manufacturers will see network charge discounts climb to 90% under the British Industrial Competitiveness Scheme from 2027, strengthening the business case for electrified robotics and regenerative braking. Procurement criteria are shifting: buyers now specify kWh per unit of output as tightly as cycle time, pushing vendors to integrate energy dashboards and AI-based load balancing into every proposal. Renewable intermittency further underscores the value of smart micro-grids and adaptive scheduling software that can align production with surplus green power.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX and ROI uncertainty for SMEs | -1.5% | National, concentrated in traditional manufacturing regions | Short term (≤ 2 years) |

| Automation-skills gap | -1.2% | National, acute in Scotland and Northern England | Medium term (2-4 years) |

| Legacy brown-field infrastructure fragmentation | -0.8% | England manufacturing corridors, selective Wales coverage | Medium term (2-4 years) |

| Cyber-security liability under PSTI Act | -0.6% | National, with emphasis on connectable device manufacturers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High CAPEX and ROI uncertainty for SMEs

Many small manufacturers still hesitate to finance multi-year automation programs, especially amid elevated interest rates that tighten working-capital buffers. Although the British Business Bank has expanded lending facilities for Industrial Strategy sectors, risk-averse owner-managers remain wary of staking limited collateral on technologies with unfamiliar payback metrics. Fragmented supplier ecosystems and inconsistent performance benchmarks complicate procurement, leaving some firms locked in prolonged pilot phases. Made Smarter’s “test before invest” offering alleviates part of this friction, yet the reluctance persists until stronger evidence links automation to order-book growth rather than incremental cost savings.

Automation-skills gap

Universities and technical colleges currently graduate fewer automation engineers than demand requires, despite an additional USD 1.2 billion per year earmarked for digital and engineering courses by 2028-29. Existing curricula seldom integrate mechanical design, controls programming, and OT cybersecurity, forcing industry to assemble interdisciplinary teams through on-the-job cross-training. Brexit-related visa hurdles further constrain talent inflows from continental Europe. In response, OEMs and integrators offer remote commissioning services and low-code configuration tools that lower the competency threshold for plant personnel, but the systemic skills shortfall continues to elongate project lead times.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Control systems anchor modernization

Industrial control systems accounted for 58.15% of total revenue in 2025, underscoring their centrality in orchestrating, ensuring safety, and facilitating regulatory traceability across both discrete and process plants. Replacement cycles are accelerating as operators retire legacy programmable logic controllers (PLCs), vulnerable to cyber intrusion and incompatible with unified namespace architectures. Manufacturers that replace aging supervisory control and data acquisition (SCADA) servers with modern, edge-ready units report double-digit reductions in scrap rates and shorter downtime. Field devices, namely articulated robots, machine-vision stations, and smart sensors, deliver the fastest momentum at an 11.87% CAGR, driven by demand for autonomous bin-picking, inline defect detection, and flexible packaging.

The United Kingdom factory automation and industrial control systems market benefits from hybrid control designs in which PLCs execute deterministic logic locally while cloud analytics tune parameters for energy or quality optimization. Augmented-reality human-machine interfaces now project live KPIs onto safety goggles, enabling line operators to diagnose variances without losing focus on their production tasks. Manufacturing execution systems (MES)aree heavilyutilized in highly regulated domain,s such asthe pharmaceutical industrys, where serialized batch records and electronic signatures are mandatory. The University of Sheffield’s AMRC recently demonstrated vision-guided robotic disassembly cells co-developed with Siemens that recognize product geometry and dynamically sequence toolpaths. These successes validate the swing toward perception-driven robotics that minimizes fixture complexity and adapts to variant-rich product families.

By End-User Industry: Pharma propels next-wave adoption

Automotive and transportation retained 28.33% revenue share in 2025 on the strength of long-running robotic welding, paint, and drivetrain assembly lines. Yet pharmaceutical and life sciences now set the growth pace at a 13.77% CAGR to 2031, buoyed by post-pandemic investments in sterile fill-finish, vaccine, and cell-therapy facilities. Clean-room automation demands closed-environment robots, automated guided vehicles (AGVs) for materials transfer, and granular MES capable of regulatory batch release. The forthcoming Somerset battery gigafactory, budgeted at USD 4 billion, demonstrates how adjacent sectors, such as electric mobility, feed into life-sciences-grade quality protocols.

Food and beverage processors are expanding the use of robotic palletizing and hygienic conveyance to offset high turnover in manual roles, while chemical and petrochemical sites are targeting advanced process control to reduce energy intensity. Oil and gas producers leverage remote supervisory systems for hazardous offshore platforms, integrating real-time vibration analytics to avert unplanned downtime. Power utilities deploy distributed control systems to stabilize grids saturated with renewable inputs, further bolstering software-defined automation. Electronics, metals, and aerospace producers round out the demand profile, each seeking flexible manufacturing systems that permit high-mix, low-volume production with minimal retooling.

By Component: Software shapes competitive edge

Automation hardware still contributes 46.85% of sector turnover, reflecting persistent demand for robots, drives, and sensors. However, software leads strategy deliberations as manufacturers acknowledge that differentiated value now lies in data orchestration and AI-driven decision loops. Cloud-native MES and edge-analytic platforms are projected to capture a 12.7% CAGR as plants adopt predictive quality, energy dispatch optimization, and digital twin simulations. The AI Opportunities Action Plan allocates funding to industrial inference chips and regulatory sandboxes, thereby lowering the entry hurdles for algorithm-centric vendors.

Services, including project integration, lifecycle maintenance, and cybersecurity hardening, have become indispensable, particularly for SMEs without in-house controls teams. Outcome-based service contracts, where providers guarantee throughput or energy savings, gain favor and shift capital outlays to operating budgets. Hardware suppliers respond with modular servo packs, reconfigurable gripper kits, and standard OPC UA interfaces that curtail commissioning time. The United Kingdom factory automation and industrial control systems market size related to software is projected to climb sharply as license subscriptions and analytics dashboards replace one-off hardware margins.

By Industrial Communication Network: Private 5G redefines latency

Industrial Ethernet maintained 43.25% market share in 2025, its determinism and broad vendor support securing first-choice status for backbone connectivity. Private 5G/LTE is expected to register the fastest expansion at a 12.73% CAGR to 2031, driven by sub-10 millisecond latency and network-slicing features that are pivotal for autonomous mobile robots and AR service routines. Jaguar Land Rover’s Solihull plant and the Manufacturing Technology Centre’s Coventry facility both utilize campus-scale 5G, which orchestrates guided vehicles, high-definition inspection cameras, and edge servers in real-time.

Legacy fieldbus systems persist in deep brownfield zones where deterministic cycles outweigh bandwidth needs. Wi-Fi 6, ISA100, and WirelessHART serve sensor swarms and handheld devices, provided traffic is segmented behind zero-trust gateways mandated by forthcoming PSTI enforcement. Edge nodes now host time-sensitive networking (TSN) features that merge IT and OT realms without sacrificing jitter control, solidifying the route toward converged but secure plant networks.

Geography Analysis

England underpins nearly three-quarters of the United Kingdom's factory automation and industrial control systems market, owing to the concentration of automotive clusters in the West Midlands, pharmaceutical production in the South East, and a dense ecosystem of integrators spanning from Cambridge to Manchester. The Halewood electric-vehicle project, budgeted at USD 500 million, alone deploys 750 industrial robots and next-generation paint lines that slash volatile organic compound emissions by 30%. Research corridors, such as the Catapult High-Value Manufacturing network and the West Midlands 5G testbed, accelerate the time-to-deployment for pilot projects. Foreign direct investors, such as Schneider Electric, have recently committed USD 42 million to scale smart-factory output in Scarborough, signaling confidence in England’s automation infrastructure.

Scotland commands specialized capabilities in offshore energy, food processing, and precision medicine. Make United Kingdom confirms Scottish output has rebounded above pre-pandemic peaks, supported by condition-monitoring systems for North Sea platforms and robotics for salmon processing. Renewables integration drives demand for sophisticated supervisory control that manages wind-farm intermittency alongside conventional grids. Enterprise agencies channel grants toward industrial digital tech adoption, while academic centers in Glasgow and Aberdeen nurture control engineering talent.

Wales exhibits resilience through high-mix aerospace and automotive sub-assemblies in South Wales corridors, where AGVs and collaborative robots lift line ergonomics and throughput. Energy-efficiency mandates spur upgrades to variable-speed drives and smart metering across metal fabrication sites. Northern Ireland leverages cross-border supply chains, investing in AI-oriented R&D labs in Belfast and Derry that co-develop vision systems and digital twins for local dairy, composites, and pharmaceutical exporters. Collectively, these regional initiatives ensure that growth in the United Kingdom factory automation and industrial control systems market is not confined to England but radiates across the devolved administrations.

Competitive Landscape

The market remains moderately fragmented, with tier-one multinationals, Siemens, ABB, Schneider Electric, Rockwell Automation, still controlling broad hardware portfolios and entrenched service networks. Their leadership is challenged by software-native entrants specializing in AI-enabled quality control, cybersecurity orchestration, and private 5G network management. Strategic acquisitions illustrate convergence: traditional PLC makers are snapping up edge-analytics startups, while industrial cloud providers are buying robotics middleware firms to deliver vertically integrated stacks.

Vendors increasingly package sector-specific solutions. Pharmaceutical suites now ship with GMP-compliant e-batch records and automated cleaning-in-place sequencing, while automotive bundles embed welding-path optimization and energy recovery modules tailored to body-in-white lines. Cybersecurity compliance under the PSTI Act has created a whitespace for “secure-by-default” device firms that pre-install zero-trust firmware and provide lifetime patch services. Partnerships between OEMs and academia, such as Siemens’ joint work with the AMRC on automated disassembly cells, speed commercial rollout of circular-economy applications.

Service models also evolve. Integrators increasingly guarantee KPIs, uptime, energy usage, and OEE in lieu of fixed-fee builds, monetizing AI algorithms via monthly subscriptions rather than capex. As cloud support becomes mission-critical, hyperscalers are courting OT specialists to host real-time manufacturing workloads in sovereign data centers, addressing concerns about latency and data residency. Competitive intensity thus pivots from hardware differentiation to holistic digital-service ecosystems underpinning the United Kingdom factory automation and industrial control systems market.

United Kingdom Factory Automation And Industrial Control Systems Industry Leaders

Schneider Electric SE

Emerson Electric Company

Mitsubishi Electric Corporation

ABB Ltd.

Rockwell Automation, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: The Advanced Manufacturing and Digital Technologies Sector Plans have pledged USD 4.3 billion to scale automation across an additional 5,500 SMEs under the expanded Made Smarter program.

- June 2025: The British Industrial Competitiveness Scheme confirmed electricity cost cuts up to USD 40 per MWh for 7,000 energy-intensive manufacturers beginning 2027.

- April 2025: The Office for National Statistics disclosed that 14% of manufacturing firms employed robotics versus 4% economy-wide, highlighting cross-technology complementarities among AI, cloud, and specialized machinery.

- March 2025: A Rapid Technology Assessment outlined advances in multi-agent robot coordination and identified supply-chain dependencies as obstacles to scale.

United Kingdom Factory Automation And Industrial Control Systems Market Report Scope

The United Kingdom's market for Factory Automation and Industrial Control Systems is segmented by Type. This includes Industrial Control Systems such as Distributed Control System (DCS), Programmable Logic Controller (PLC), Supervisory Control and Data Acquisition (SCADA), Manufacturing Execution System (MES), Product Lifecycle Management (PLM), and Human–Machine Interfaces (HMI). Additionally, it encompasses Field Devices like Industrial Robotics, Machine Vision, Motors and Drives, Safety Systems, and Sensors and Transmitters. The market is further categorized by End-User Industry, covering sectors such as Automotive and Transportation, Food and Beverage, Pharmaceutical and Life Sciences, Oil and Gas, Chemical and Petrochemical, Power and Utilities, among others. Component-wise, the market divides into Automation Hardware, Automation Software, and Services, which include Integration, Maintenance, and Consulting. Furthermore, under Industrial Communication Network, categories span Industrial Ethernet, Fieldbus, Wireless options (Wi-Fi, ISA100, WirelessHART), and Private 5G/LTE. All market forecasts are expressed in terms of value (USD).

| Industrial Control Systems | Distributed Control System (DCS) |

| Programmable Logic Controller (PLC) | |

| Supervisory Control and Data Acquisition (SCADA) | |

| Manufacturing Execution System (MES) | |

| Product Lifecycle Management (PLM) | |

| Human–Machine Interface (HMI) | |

| Field Devices | Industrial Robotics |

| Machine Vision | |

| Motors and Drives | |

| Safety Systems | |

| Sensors and Transmitters |

| Automotive and Transportation |

| Food and Beverage |

| Pharmaceutical and Life-Sciences |

| Oil and Gas |

| Chemical and Petro-chemical |

| Power and Utilities |

| Other End-user Industries |

| Automation Hardware |

| Automation Software |

| Services (Integration, Maintenance, Consulting) |

| Industrial Ethernet |

| Fieldbus |

| Wireless (Wi-Fi, ISA100, WirelessHART) |

| Private 5G / LTE |

| By Type | Industrial Control Systems | Distributed Control System (DCS) |

| Programmable Logic Controller (PLC) | ||

| Supervisory Control and Data Acquisition (SCADA) | ||

| Manufacturing Execution System (MES) | ||

| Product Lifecycle Management (PLM) | ||

| Human–Machine Interface (HMI) | ||

| Field Devices | Industrial Robotics | |

| Machine Vision | ||

| Motors and Drives | ||

| Safety Systems | ||

| Sensors and Transmitters | ||

| By End-user Industry | Automotive and Transportation | |

| Food and Beverage | ||

| Pharmaceutical and Life-Sciences | ||

| Oil and Gas | ||

| Chemical and Petro-chemical | ||

| Power and Utilities | ||

| Other End-user Industries | ||

| By Component | Automation Hardware | |

| Automation Software | ||

| Services (Integration, Maintenance, Consulting) | ||

| By Industrial Communication Network | Industrial Ethernet | |

| Fieldbus | ||

| Wireless (Wi-Fi, ISA100, WirelessHART) | ||

| Private 5G / LTE | ||

Key Questions Answered in the Report

What is the forecast value of the UK factory automation market by 2031?

The sector is projected to be worth USD 29.23 billion by 2031, expanding at a 10.35% CAGR.

Which segment holds the largest share in UK factory automation today?

Industrial control systems lead with 58.15% revenue share in 2025.

Which end-user industry is growing fastest in UK factory automation?

Pharmaceutical and life sciences are advancing at a 13.77% CAGR through 2031.

How will electricity-cost reductions influence automation adoption?

The British Industrial Competitiveness Scheme’s discounts from 2027 shorten payback periods, encouraging energy-intensive firms to accelerate projects.

Why are private 5G networks important for UK factories?

Campus-scale 5G provides the ultra-low latency needed for autonomous robots, augmented-reality maintenance, and real-time quality inspection.

Page last updated on: