Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

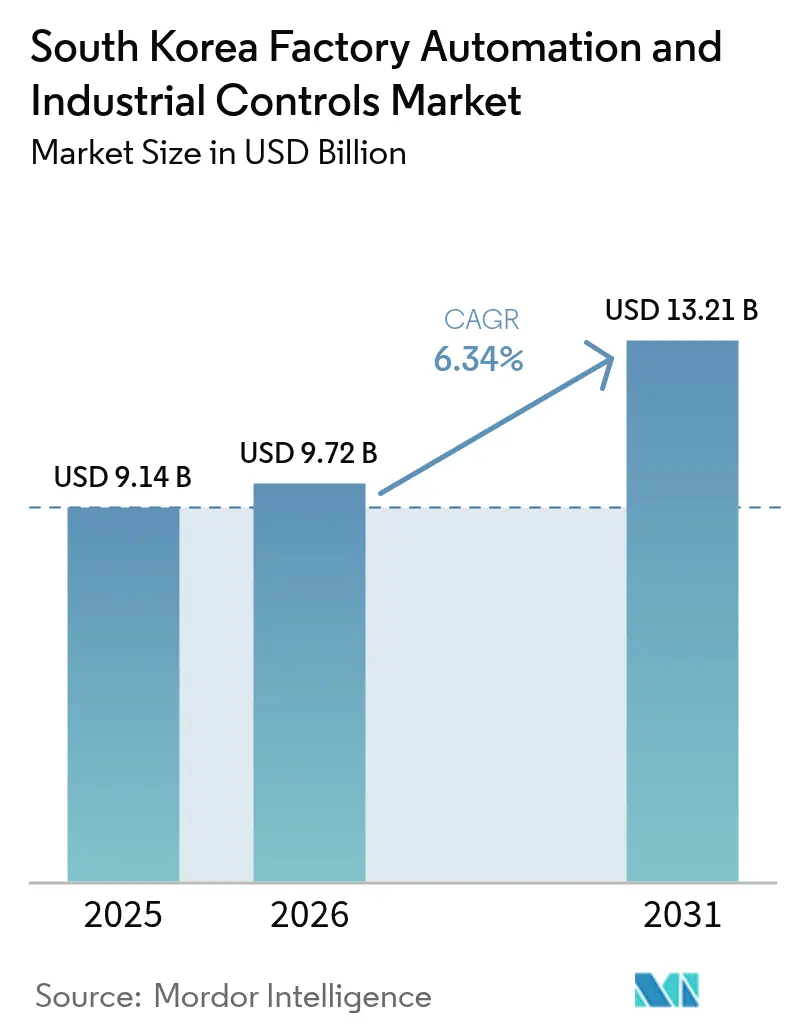

| Base Year Market Size (2025) | USD 9.14 Billion |

| Market Size (2026) | USD 9.72 Billion |

| Market Size (2031) | USD 13.21 Billion |

| Growth Rate (2026 - 2031) | 6.34% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Factory Automation And Industrial Controls Market Analysis by Mordor Intelligence

The South Korea Factory Automation and Industrial Controls market size was valued at USD 9.14 billion in 2025 and estimated to grow from USD 9.72 billion in 2026 to reach USD 13.21 billion by 2031, at a CAGR of 6.34% during the forecast period (2026-2031). Automation demand is intensifying because manufacturing employment declined by 8.2% between 2020 and 2024, even as factory output climbed by 12.4%, forcing producers to offset labor shortages with productivity-boosting equipment. Programmable Logic Controllers (PLCs) remain foundational, capturing a 25.7% share in 2024, while industrial robots lead new investment at a 9.2% CAGR as electric-vehicle (EV) and chip fabs overhaul their production lines. Hardware continues to dominate revenue with a 56.8% share, but software is scaling faster, with a 7.8% CAGR, as digital-twin projects and predictive analytics shift value toward data-driven performance. Regionally, the Seoul Capital Area holds a 48.4% share, while the Chungcheong Region is the growth hotspot, with an 8.0% CAGR, thanks to multibillion-dollar semiconductor and battery projects.

Key Report Takeaways

- By product type, PLCs led the South Korean factory automation and industrial controls market with a 25.42% market share in 2025; industrial robotics is projected to record a 8.84% CAGR through 2031.

- By component, hardware accounted for a 56.32% share of the South Korea factory automation and industrial controls market size in 2025, while software is poised to expand at a 7.46% CAGR to 2031.

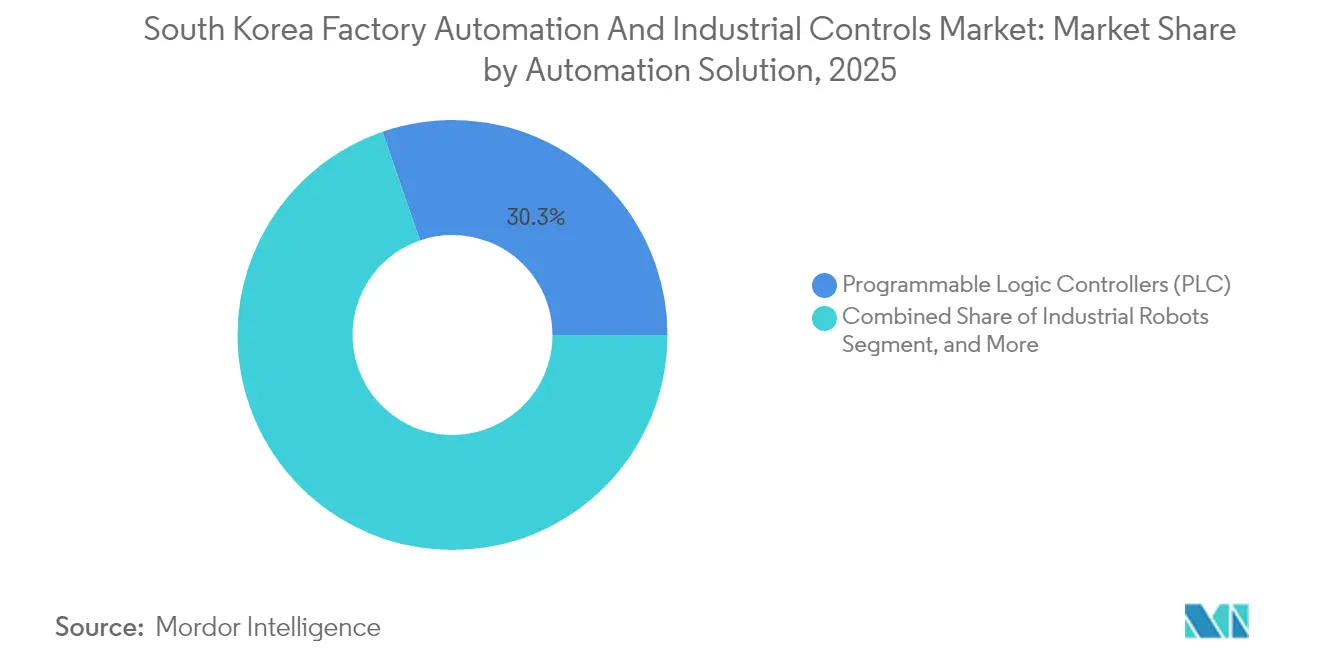

- By automation solution, PLCs maintained a 30.28% share of the South Korea factory automation and industrial controls market in 2025; industrial robots are forecast to advance at an 7.92% CAGR between 2026-2031.

- By end-user industry, general manufacturing held a 29.05% share of the South Korea factory automation and industrial controls market in 2025, and automotive is advancing at an 8.29% CAGR as EV programs scale.

- By region, the Seoul Capital Area contributed 47.86% of the 2025 revenue of the South Korean factory automation and industrial controls market; however, Chungcheong is on track for an 7.72% CAGR through 2031 as semiconductor megaprojects proceed.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Korea Factory Automation And Industrial Controls Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Smart Factory Plus incentives | +1.2% | National; strongest in Seoul and Chungcheong | Medium term (2-4 years) |

| 5G-enabled Industrial IoT roll-outs | +0.9% | Seoul, Chungcheong, Yeongnam | Short term (≤ 2 years) |

| Rising labor costs and aging workforce | +1.4% | Nationwide; acute in general manufacturing and automotive | Long term (≥ 4 years) |

| Carbon-neutrality and energy-savings mandates | +0.8% | National; early in semiconductor and chemical plants | Medium term (2-4 years) |

| Semiconductor supply-chain localization | +1.1% | Chungcheong and Yeongnam | Medium term (2-4 years) |

| Collaborative-robot tax credits for SMEs | +0.6% | National; clusters of SME workshops | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Government-backed Smart Factory Initiative 4.0 Incentives Drive Systematic Digitization

The Smart Factory Plus program provides up to 75% grants and tax credits on qualified automation purchases, lowering payback periods for SMEs to below 18 months and accelerating adoption beyond organic budgets. System integrators reported a 340% revenue spike in 2024 as firms rushed to meet subsidy deadlines before tapering off in 2026. Preferential financing terms for collaborative robots enabled Hanwha Robotics to surpass 1,200 domestic installations within a year. The policy also mandates standardized communication protocols, cutting integration times by 30% compared with pre-program projects. Early adopters now boast higher OEE (overall equipment effectiveness) scores, thereby strengthening the export competitiveness of Korean-made goods.

Accelerating 5G-enabled Industrial IoT Deployment Transforms Real-time Operations

Nationwide 5G ensures sub-10 ms latency, letting fabs stream thousands of sensor signals to edge-AI engines for instant defect detection and energy optimization.[1]Samsung Electronics, “Semiconductor Manufacturing Expansion Announcements,” samsung.com Samsung’s Pyeongtaek line trimmed defect rates by 23% and electricity use by 18% after wiring 15,000 nodes through 5G gateways. Hyundai Motor synchronizes schedules with 47 tier-1 suppliers in real-time, reducing inventory buffers by 12 days at the Ulsan complex. LG Energy Solution boosted equipment uptime by 31% and saved USD 12.4 million annually via 5G-enabled predictive maintenance at its Ochang battery facility.[2]LG Energy Solution, “Ochang Battery Plant Automation Implementation,” lgensol.com The connectivity layer positions South Korean factory automation and Industrial Controls market participants to deliver premium, ultra-reliable systems for export contracts that demand deterministic networking.

Rising Labor Costs and Aging Workforce Create Automation Imperative

Workers aged 50 and above now represent 41% of the manufacturing labor pool, up from 28% in 2019, while average shop-floor wages have climbed 34% over the same period, eroding cost advantages. Shipbuilders such as Daewoo Shipbuilding faced 15% annual wage inflation despite staff reductions, prompting rapid adoption of lift-assist and welding cobots. Hyundai Heavy Industries installed 340 collaborative robots, which reduced injury cases by 17% and enabled older artisans to remain productive. SMEs feel the pinch most acutely; 68% postponed automation in 2024 due to cash-flow strain, even with low-interest loans. Consequently, demand is shifting toward modular, human-centric solutions that augment rather than replace experienced operators.

Corporate Carbon-neutrality Targets Drive Energy-efficient Automation

Mandatory carbon-intensity ceilings introduced in 2024 are expected to propel investment in AI-based energy management systems that dynamically adjust set-points to minimize kilowatt consumption. POSCO invested USD 2.1 billion in automated controls, reducing emissions by 12% while maintaining tonnage levels. SK Hynix reduced power consumption by 25% at its Icheon fab by utilizing algorithms that schedule high-load steps during grid off-peak windows. Vendors now command 15-20% price premiums for controllers that are bundled with verified energy-saving functions. These gains enhance the export appeal of Korean-developed green automation technologies as global OEMs pursue sustainability targets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront CAPEX and integration complexity | -0.7% | Nationwide; especially SME job shops | Short term (≤ 2 years) |

| Scarcity of OT-IT integration talent | -0.9% | Seoul and Chungcheong hubs | Medium term (2-4 years) |

| Legacy-equipment compatibility hurdles | -0.5% | Traditional clusters nationwide | Medium term (2-4 years) |

| Export-control limits on motion-control parts | -0.4% | Precision manufacturers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Capital Expenditure and Integration Complexity Constrain SME Adoption

Even after subsidies, many SMEs still face out-of-pocket costs equivalent to 1.5-2.2 times their annual EBITDA, causing 68% to defer projects in 2024. Hidden engineering and commissioning fees can inflate budgets 40-60%, while typical roll-outs halt production for up to 12 weeks, jeopardizing cash cycles for thin-margin suppliers.[3]Korea Industrial Technology Association, “OT-IT Integration Specialist Certification Report,” koita.or.kr Some integrators now market modular plug-and-play cells; however, these packages often deliver only incremental efficiency gains compared to fully unified lines. Banks hesitate to extend unsecured credit to firms without a long audit history, thereby prolonging funding lead times despite government loan guarantees. Collectively, these hurdles dampen short-term growth in the South Korean Factory Automation and Industrial Controls market.

Scarcity of OT-IT Integration Talent Creates Implementation Bottlenecks

South Korea has only 2,400 certified OT-IT specialists to support more than 45,000 factories, resulting in consulting fees of USD 1,200-1,800 per day and extending project timelines by months. Universities often lag behind industry needs because curricula seldom integrate control engineering with cybersecurity, creating a pipeline mismatch. Large conglomerates launched in-house academies, but training cycles stretch 18-24 months, leaving near-term capacity gaps. International advisors could help, yet language barriers and data-sovereignty rules restrict their participation in high-security plants. Until the talent deficit narrows, integration delays will temper the otherwise robust CAGR outlook.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Industrial Robotics Leads Innovation Wave

Industrial robotics captured the spotlight, registering a 8.84% CAGR forecast through 2031, as demand for EV batteries and advanced semiconductor lines requires micron-level precision beyond conventional automation. PLCs secured a 25.42% share of the South Korean Factory Automation and Industrial Controls market in 2025, underscoring their indispensable role as real-time logic engines across both legacy and digital factories. Safety controllers and emergency-stop devices benefited from stricter 2024 workplace mandates, resulting in a 14% year-over-year increase in shipments. Machine-vision systems have grown in tandem with robotics, as higher-resolution inspection stations now detect defects 50% smaller than prior benchmarks. At the opposite end of the curve, power supplies faced margin squeeze as commoditization invited lower-cost entrants.

The trajectory reveals a transition from labor-replacing arms to collaborative, AI-enabled teammates; cobots already command 23.00% of 2025 robot revenues, up from 8.00% two years earlier. That acceleration signals a structural shift toward flexible, low-barrier deployments suited to mixed-model production runs. Vendors pairing vision with robotics inside turnkey cells have cut programming time by 35%, appealing to SMEs that lack in-house engineers. The interplay of safety regulation, demographic strain, and product customization pressure thus cements robotics as the pace-setter for future spending within the South Korean Factory Automation and Industrial Controls market.

By Component: Software Gains Strategic Importance

Hardware still generated 56.32% of 2025 revenue, yet software expanded at a 7.46% CAGR, as digital-twin models, AI analytics, and cloud SCADA unlock productivity that pure hardware cannot replicate. The adoption of subscription-based MES platforms increased from 18% in 2022 to 34% in 2024, as CFOs favored operating expenditures over large license payments. Hyundai Motor invested USD 180 million in virtual plants that test process tweaks in silico, reducing line-change downtime by 42%. Services installation, remote monitoring, and predictive-maintenance outsourcing round out the stack, capturing steady growth by offloading complexity from resource-strapped factories.

The shift mirrors global best practices: hardware establishes data points, software orchestrates insights, and services sustain uptime. As vendors embed edge-AI into PLC firmware and expose open APIs, buyers increasingly select ecosystems, not standalone boxes. Consequently, software’s share of the South Korea Factory Automation and Industrial Controls market size is expected to edge above 50% beyond 2031, fundamentally rewiring competitive moats around code, not capital goods.

By Automation Solution: Industrial Robots Transform Manufacturing Paradigms

PLC architectures retained a commanding 30.28% of 2025 revenues, yet robot systems are on track for an 7.92% CAGR as discrete industries shift to high-mix, low-volume portfolios that require agile cells. SCADA and DCS remained staples in the chemicals and power industries, where centralized safety and redundancy still trump agility. MES adoption reached 67% of large plants in 2024, anchoring data continuity between ERP suites and shop-floor controllers. Machine-vision modules surged in assembly lines manufacturing 2-nanometer chips and 800-V EV drivetrains, enabling defect capture at sub-micron thresholds and feeding AI models that refine upstream process set-points.

Hybridization is blurring classic taxonomy: PLC vendors bundle AI inference engines, while robot OEMs integrate native vision and MES connectors. Customers reward turnkey performance; procurement teams are increasingly issuing single contracts that cover motion, sensing, analytics, and service. That convergence elevates entry barriers for niche suppliers while amplifying the upside for integrators who master hardware-software fusion within the South Korean Factory Automation and Industrial Controls market.

By End-user Industry: Automotive Electrification Drives Automation Demand

General manufacturing remained the largest vertical, with a 29.05% revenue share in 2025, reflecting its broad base across consumer goods, machinery, and packaging industries. Automotive automation spend, however, is scaling at an 8.29% CAGR as Korea’s OEMs retool for high-volume battery packs, e-axles, and hairpin winding motors that necessitate micron-accurate robots and laser welders. Semiconductor fabs invested USD 2.3 billion in tools during 2024, prioritizing clean-room grippers and autonomous material-handling vehicles that reduce particle contamination. Chemicals and petrochemicals are channeling funding toward safety-instrumented systems following stricter 2024 hazard-prevention rules.

Power utilities invest heavily in grid automation and HVDC converter stations to support the integration of renewable energy, while food and beverage processors automate inspection, filling, and palletizing to combat chronic labor shortages. Oil and gas, though a shrinking slice, still upgrades legacy refineries with digital safety and emission-monitoring layers under the nation’s decarbonization roadmap. The vertical mosaic highlights why diversified vendors with cross-sector playbooks exhibit resilience in the South Korean Factory Automation and Industrial Controls market.

Geography Analysis

Seoul Capital Area’s 47.86% grip in 2025 reflects its cluster of headquarters, labs, and universities that cross-pollinate talent and innovation. Global suppliers co-locate R&D hubs near domestic champions, accelerating the co-development of Korea-specific modules, such as high-humidity redundant sensors for cleanrooms. Despite its maturity, the region continues to post steady upgrades as manufacturers integrate AI dashboards on top of legacy PLC networks.

The Chungcheong Region’s 7.72% CAGR to 2031 is anchored in the “K-Semiconductor Belt” policy, which funnels tax holidays and infrastructure subsidies into fabs that must meet sub-3-nm process tolerances. Automation intensity per square meter here surpasses any Korean zone, with fabs averaging 1.6 robots per employee and 100% AGV coverage. Suppliers that secure reference projects in Chungcheong typically springboard to global chip-plant deals, magnifying strategic value.

Yeongnam’s shipyards and EV plants upgrade heavy-payload robotics and machine-vision welding cells to retain export competitiveness against Chinese yards. Honam modernizes its steel and petrochemical complexes with AI-powered energy platforms that reduce both kWh consumption and carbon fees. Gangwon and Jeju contribute modestly but illustrate scope for niche applications such as quarry automation and food-safety inspection lines. The cumulative tapestry ensures the South Korea Factory Automation and Industrial Controls market remains geographically diversified, buffering cyclical shocks in any single province.

Regulatory Landscape

South Korea's factory automation and industrial controls market follows policy direction from the Ministry of Trade, Industry and Energy (MOTIE). Standards and conformity infrastructure are anchored by the Korean Agency for Technology and Standards (KATS), with sector execution support from the Korea Institute for Robot Industry Advancement (KIRIA). Robot deployment is framed by the Act on the Development and Supply of Intelligent Robots, which supports national diffusion planning and designation of safety testing and conformity assessment bodies, strengthening formal pathways for robot and automation safety compliance.

On the technical side, Korean Industrial Standards (KS) align closely with IEC and ISO norms used in industrial control systems. This includes KS X IEC 62443-4-2 for industrial cybersecurity requirements and KS C IEC 60204-1 for electrical equipment of machinery. In 2026, governance expanded to cover AI use in industrial settings through the AI Basic Act (effective January 2026). Separately, KATS began its secretariat responsibilities for the IEC Smart Manufacturing Standardization Committee (SC65F) on July 12, 2026, further tightening the link between domestic compliance expectations and global smart manufacturing standards.

Value Chain Analysis

The South Korean factory automation and industrial controls value chain begins with component and platform suppliers (controllers, drives, sensors, vision, safety, industrial networks, and software stacks such as SCADA, DCS, and MES). It then moves through equipment OEMs and local manufacturing, followed by system integrators and engineering services that design, install, and commission solutions at factories. Large end users across semiconductors, automotive, batteries, shipbuilding, steel, and chemicals increasingly pull cloud and AI infrastructure into the chain, shifting value toward OT-IT integration, digital twins, and AI-enabled production applications delivered by conglomerate IT arms and specialist integrators.

Ecosystem coupling between automation vendors and AI compute providers is also becoming a clearer bridge from upstream to midstream. For example, Samsung Electronics and NVIDIA disclosed an AI-megafactory collaboration in October 2025 centered on large-scale GPU deployment to accelerate manufacturing AI across semiconductor and robotics-related production. SK Group and NVIDIA also outlined a manufacturing AI cloud and AI factory cluster in Ulsan tied to a large data center project. On the services and deployment side, partnerships such as LG CNS and Honeywell (July 2025) show MES, analytics, and factory IT services being bundled with traditional controls, while policy-driven supply chain resilience measures, including the Framework Act on Supporting Supply Chain Stabilization for Economic Security (effective June 2024), reinforce localization and continuity planning across critical industrial inputs and software dependencies.

Competitive Landscape

International leaders such as ABB, Siemens, and Mitsubishi Electric are localizing R&D and production to comply with the K-Chips Act’s 70% domestic-content rule by 2027, channeling millions of dollars into Changwon and Incheon plants. Partnerships bloom: Rockwell Automation codesigned AI MES stacks with Samsung Heavy, and Schneider Electric teams with LG to embed edge analytics into low-voltage switchgear. These alliances blend global IP with Korean execution speed, deepening moats against pure import rivals.

Domestic champions LS Electric, Hanwha Robotics, and Hyundai Robotics leverage proximity to customers and preferential government procurement to expand their share. LS Electric’s USD 340 million smart-factory investment elevates its PLC and drives its portfolio into premium tiers, particularly after the 2025 takeover of Germany’s Lenze SE.[4]LS Electric, “Smart Factory Solutions Investment Announcement,” lselectric.co.kr Hanwha Robotics’ record order for 340 cobots at Samsung Display’s OLED expansion underscores buyer confidence in local service responsiveness.

Competitive intensity is rising as mid-tier specialists target white spaces, such as AI vision and edge cybersecurity. Start-ups born in chip-sector spin-offs introduce laser-guided micro-robots, while established giants cross-bundle hardware and SaaS to lock customers into multi-year service contracts. Certification of ABB’s cyber-secure controllers by the Korea Internet and Security Agency raises the security bar for all vendors. The resulting market is moderately consolidated yet dynamic, rewarding firms that align portfolios with Korea’s twin imperatives of localization and carbon reduction.

South Korea Factory Automation And Industrial Controls Industry Leaders

ABB Ltd. (ABB Korea Co. Ltd.)

Mitsubishi Electric Corporation (Mitsubishi Electric Automation Korea Co. Ltd.)

Siemens AG (Siemens Korea)

Rockwell Automation Inc.

Omron Corporation (Omron Electronics Korea Co. Ltd.)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

One clear opportunity is the upgrade path from controller-led automation to manufacturing AI and virtualized engineering. Buyers are shifting budgets toward digital twins, AI-based quality, and integrated OT-IT stacks that shorten commissioning and stabilize yields. This direction is reinforced by multi-ministry programs such as the Manufacturing AI 2030 Strategy announced in June 2026, which formalizes the build-out of AI factories, and by industrial AI standardization efforts that support interoperable data and security practices across plants. For vendors and integrators, this opens whitespace in factory AI enablement layers that sit above PLC and robot installations, including model lifecycle operations, edge orchestration, and cyber-secure connectivity aligned with KS X IEC 62443-4-2.

A second opportunity area is regional and cluster-based expansion tied to large announced investment hubs that draw in robotics, machine vision, and high-mix automation cells. Hyundai Motor Group announced an AI, robotics, and hydrogen-focused innovation hub in Saemangeum in February 2026, and in July 2026 unveiled a large-scale plan around physical AI and mobility hubs in the Yeongnam region. Samsung Group also disclosed a major investment program in July 2026 that included humanoid robot mass-production systems and AI-centered manufacturing processes. In parallel, the Ministry of SMEs and Startups actions in March 2026 (identifying strategic smart manufacturing technology items) and June 2026 (launching work on a 2026 smart manufacturing strategic technology roadmap using patent big data) point to near-term procurement and capability-building lanes for SMEs in areas such as CPS/digital twin, big data/AI, and machine vision, which aligns with the market's ongoing need to reduce integration lead times amid OT-IT talent constraints.

Recent Industry Developments

- June 2026: Siemens Korea signed an MOU with NAVER Cloud on June 23, 2026, to collaborate on AI conversion for domestic manufacturing, combining Siemens factory automation and digital twin capabilities with NAVER Cloud infrastructure. The partnership elevates cloud-delivered industrial AI and OT-IT convergence as a mainstream buying path, influencing how Korean plants package automation upgrades with data and compute services.

- November 2025: ABB Korea signed an MOU with Korea District Heating Corp (KDHC) on November 4, 2025, to develop AI-based intelligent plant technology and optimize AI solutions for energy facilities. The agreement broadens ABB's footprint in process and utility automation, where AI-driven optimization and controls modernization are tied to efficiency and operational reliability targets.

- June 2024: ABB Korea signed an agreement with Samsung E&A to apply robot automation to construction and industrial module assembly projects. This collaboration extends industrial robotics and automation know-how into adjacent industrial production workflows, supporting repeatable, higher-throughput fabrication approaches that can feed back into factory-side automation demand for heavy industries.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as revenues generated in South Korea from factory automation and industrial controls used to monitor, control, and automate production and industrial operations, including the related hardware, software, and services that make these systems work in real plants.

Scope exclusions: It excludes general office IT, consumer electronics, and non-industrial automation tools that are not deployed for industrial control or factory-floor automation use cases.

Segmentation Overview

- By Product Type

- Presence Sensing Safety Sensors

- Emergency Stop Devices

- Safety Controllers / Modules

- Safety Mats

- Programmable Logic Controllers (PLC)

- Human Machine Interface (HMI)

- Machine Vision Systems

- Industrial Robotics

- Sensors and Transmitters

- Switches

- Safety Switches

- Limit Switches

- Pushbutton Switches

- DIP Switches

- Relays

- Industrial Power Supplies

- By Component

- Hardware

- Software

- Services

- By Automation Solution

- SCADA

- Distributed Control System (DCS)

- Manufacturing Execution Systems (MES)

- Programmable Logic Controllers (PLC)

- Industrial Robots

- Machine Vision

- By End-user Industry

- Automotive

- Semiconductor and Electronics

- General Manufacturing

- Oil and Gas

- Chemical and Petrochemical

- Food and Beverage

- Power and Utilities

- Other End-user Industries

- By Region

- Seoul Capital Area

- Chungcheong Region

- Honam Region

- Yeongnam Region

- Gangwon Region

- Jeju Province

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the boundaries of what qualifies as factory automation and industrial controls in South Korea, and to anchor macro indicators that move demand. We referred to public sources such as Statistics Korea (KOSTAT), Bank of Korea releases, the Korea Customs Service trade statistics, and industry and safety publications from bodies such as ISO and IEC, which helps clarify standards and typical product definitions.

To make the dataset practical for sizing, we reviewed company annual reports and investor presentations for Korea-relevant revenue discussion, product mix cues, and manufacturing exposure across key end users such as automotive and electronics. In parallel, we used select paid subscriptions for company financial intelligence, news and financials, patent databases, and shipment-level import and export views, where product classification could support sanity checks on directionality. These desk inputs were also used to flag gaps that needed confirmation during interviews, and the source list is illustrative since we used many additional public materials for cross-checking and clarification.

Primary Interviews and Surveys

Primary work focused on interviews and structured surveys with stakeholders across the factory floor and control stack, including manufacturers, system integrators, distributors, and end users in major industrial hubs within South Korea. We used these discussions to confirm adoption rates for automation solutions, typical replacement cycles, pricing direction for key control and sensing equipment, and how buyers separate services versus embedded software.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 18% | |

| Mid tier: 57% | Functional/Unit leaders: 35% | |

| Smaller Players: 18% | Managers: 47% |

Market-Sizing & Forecasting

Sizing starts from a top-down reconstruction where manufacturing output and investment signals are translated into an addressable automation spend pool, and then split into factory automation and industrial controls based on observed penetration by end user. Once that structure is built, the totals are checked using selective bottom-up approximations, such as sampled price times shipments for commonly purchased items, and supplier and channel checks to adjust any overstatement.

Inputs that most often move the model include manufacturing production and export momentum in electronics and automotive, new plant and line expansion activity, installed base replacement cycles for control equipment, automation solution penetration (PLC, SCADA, DCS, MES), and price movement for sensing and control devices (including safety and switching products). For forecasting, scenario analysis was used, where a base case is guided by expected capex and output trends discussed by interviewees, and then a conservative and an expansion case are run to test sensitivity. Where bottom-up inputs are incomplete, missing parts are bridged using ranges validated with integrators and buyers, and then averaged only after the variance narrows to a defensible band.

Data Validation & Update Cycle

Outputs are validated through triangulation across independent signals, and we run variance checks year by year to catch jumps that do not match known investment cycles or end-user demand shifts. When an outlier appears, the assumptions are reviewed, the input series is rechecked, and follow-up calls are triggered with relevant respondents until the driver is clearly explained.

Before sign-off, a second analyst reviews the calculation logic, scope fit, and conversion assumptions, and then the narrative is aligned to the final numbers so there are no hidden step changes. The report is refreshed annually, and interim updates are made when material events occur that can shift production, investment, or pricing. Right before delivery, a final pass is done to ensure the latest available public indicators and interview feedback are reflected.

Mordor Intelligence's South Korea Factory Automation and Industrial Controls Market Size Versus Other Published Estimates

Published market sizes for this space often differ, even when the titles look similar, because the included product basket and the year used as the starting point are not always the same. Differences also come from how services are counted, how pricing is treated over time, and whether the estimate is tied back to plant-level investment signals.

The table shows a noticeable spread that is largely explained by scope and timing, and in Mordor Intelligence's model the South Korea total is built from a defined set of factory automation and industrial controls products and solutions (such as PLC, HMI, SCADA, DCS, MES, machine vision, industrial robotics, and safety and switching devices) and is reported with a 2025 base that rolls into 2026 sizing with current-year validation checks.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 9.72 B (2026) | |

| Industry Publisher A | USD 8.02 B (2023) | Uses an earlier base year, which can understate current pricing and adoption for automation solutions, and the published summary does not clearly spell out which product families and services are included in the value. |

| Industry Publisher B | USD 9.62 B (2024) | Covers a broader industrial automation label, which can pull in adjacent automation categories beyond factory automation and industrial controls, and it applies a higher growth curve that can amplify totals if penetration and ASP changes are not validated against current investment cycles. |

Taken together, the comparison points to two practical drivers of variance, which are scope boundaries and the choice of base year used for normalization. By anchoring the estimate to observable demand signals and then stress-testing it with interview-led checks on penetration, replacement, and pricing, the final number stays traceable to repeatable steps rather than to one single assumption.

Key Questions Answered in the Report

What is the 2026 value of South Korea’s factory-automation sector?

The South Korea Factory Automation and Industrial Controls market size stands at USD 9.72 billion in 2026.

How fast is automation spending expected to grow in South Korea?

Market revenue is projected to rise at a 6.34% CAGR, reaching USD 13.21 billion by 2031.

Which product category is expanding the quickest?

Industrial robotics posts the fastest growth at a 8.84% CAGR through 2031 because EV and chip plants need high-precision assembly.

Why is Chungcheong Region attracting significant investment?

Chungcheong hosts multibillion-dollar semiconductor expansions by Samsung and SK Hynix, driving an 7.72% regional CAGR.

How is the talent shortage affecting project timelines?

A deficit of OT-IT specialists is extending integration schedules by 3-6 months and inflating consulting fees to USD 1,800 per day.

What government incentives are spurring small-business adoption?

The Smart Factory Plus program covers up to 75% of eligible automation costs and offers tax credits for collaborative-robot purchases.

Page last updated on: