Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

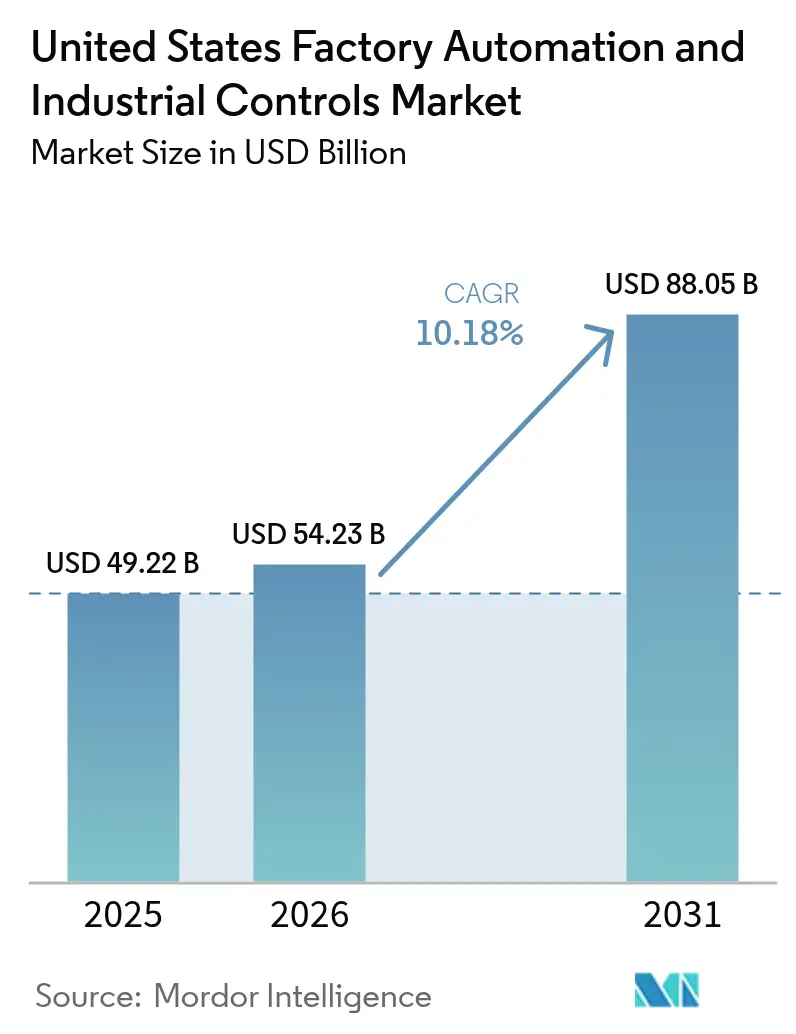

| Base Year Market Size (2025) | USD 49.22 Billion |

| Market Size (2026) | USD 54.23 Billion |

| Market Size (2031) | USD 88.05 Billion |

| Growth Rate (2026 - 2031) | 10.18% CAGR |

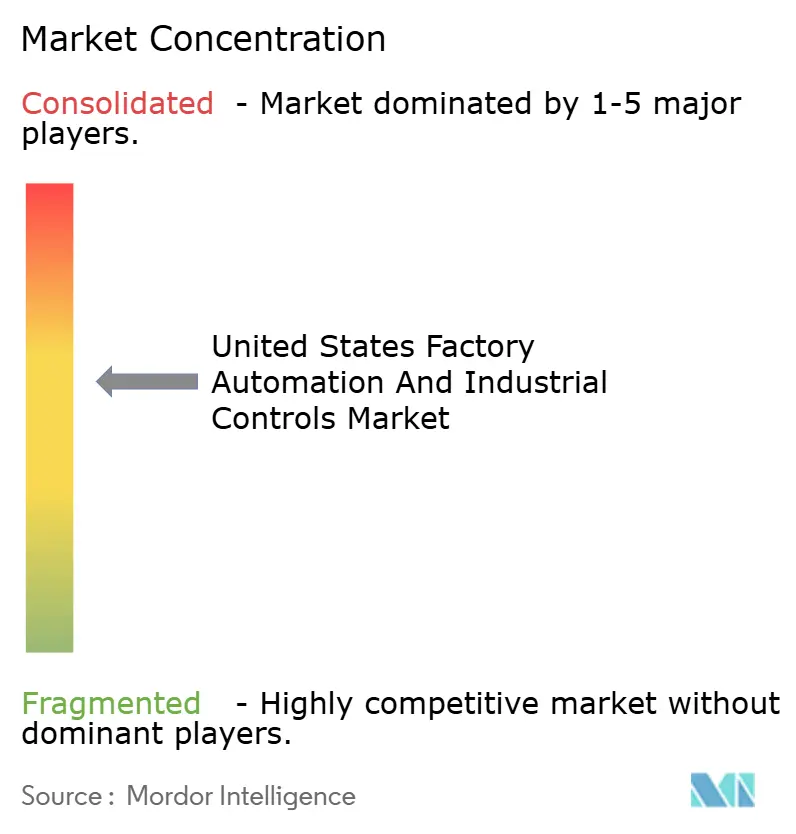

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United States Factory Automation And Industrial Controls Market Analysis by Mordor Intelligence

The United States factory automation and industrial controls market size is expected to grow from USD 49.22 billion in 2025 to USD 54.23 billion in 2026 and is forecast to reach USD 88.05 billion by 2031 at 10.18% CAGR over 2026-2031. The projected growth reflects a manufacturing pivot toward smart production lines that offset labor shortages, comply with stricter safety rules, and capture reshoring incentives delivered through the CHIPS Act and Inflation Reduction Act. Semiconductor fabs, battery plants, and clean-energy component makers lead new capital expenditure, while brownfield sites race to retrofit programmable logic controllers (PLCs), machine-vision systems, and industrial IoT sensors for real-time optimization. Hardware continues to dominate spending, yet service-led contracts that bundle cybersecurity, predictive maintenance, and performance guarantees are gaining momentum as manufacturers pursue outcome-based agreements. Heightened cyber-risk and tariff uncertainty remain hurdles, but the overall investment thesis is reinforced by state and federal policy alignment that rewards domestic, digitally enabled production.

Key Report Takeaways

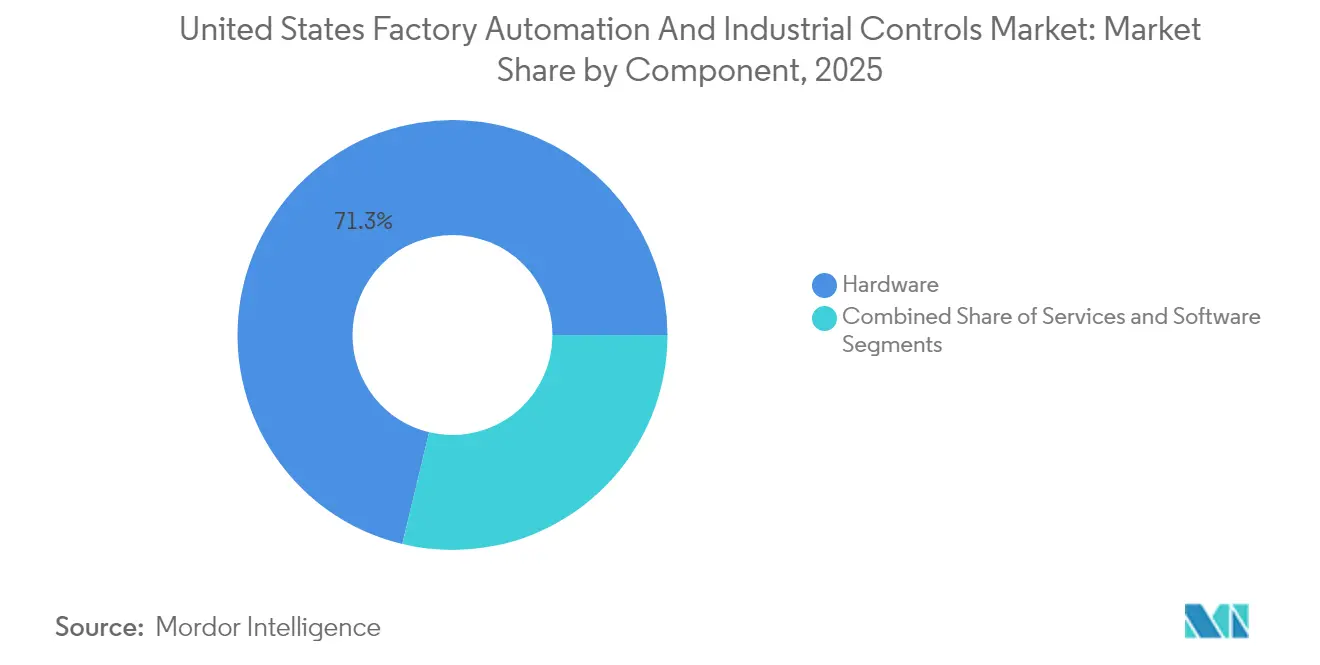

- By component, hardware captured 71.25% of United States factory automation and industrial controls market share in 2025, while services are expanding at a 12.42% CAGR to 2031.

- By type, industrial control systems accounted for 54.30% of the United States factory automation and industrial controls market size in 2025; field devices are projected to grow 11.30% annually through 2031.

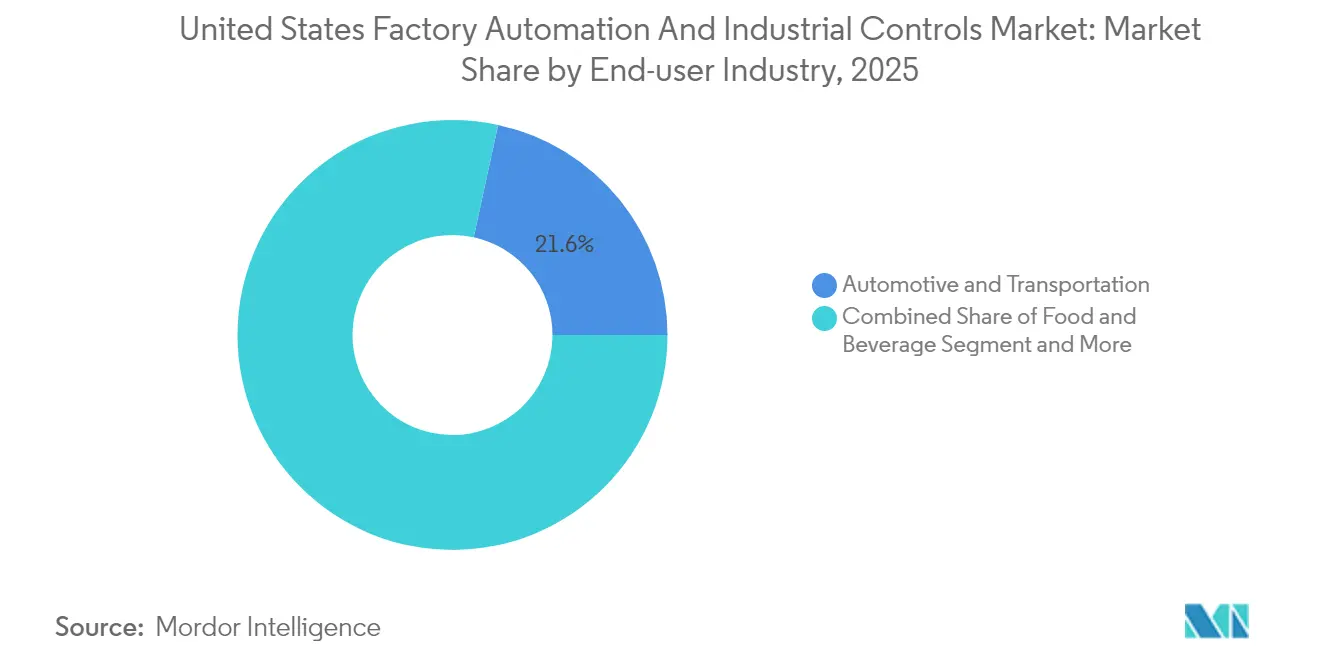

- By end-user industry, automotive & transportation held 21.60% revenue share in 2025, but food & beverage is advancing at a 12.75% CAGR and is the fastest-growing segment.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Factory Automation And Industrial Controls Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Reshoring incentives & CHIPS Act accelerate semiconductor factory automation | + 2.10% | National; Arizona, Texas, Ohio focal points | Medium term (2-4 years) |

| Labor shortage drives collaborative robotics adoption | +1.80% | Nationwide; strongest in Midwest | Short term (≤ 2 years) |

| Clean-energy manufacturing boost from Inflation Reduction Act | +1.50% | Nationwide; former coal regions prioritized | Medium term (2-4 years) |

| OSHA-enforced machine-safety compliance raises demand for safety-integrated control systems | +0.90% | Nationwide; high-risk industries | Short term (≤ 2 years) |

| Brownfield IIoT retrofits for real-time OEE optimization | +1.20% | Legacy manufacturing corridors | Medium term (2-4 years) |

| EV production expansion needs flexible high-speed assembly lines | +1.70% | South and Midwest EV clusters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Reshoring incentives & CHIPS Act accelerate semiconductor factory automation

The CHIPS and Science Act has triggered the largest wave of domestic semiconductor investment on record, with multibillion-dollar fabs in Arizona, Texas, and Ohio specifying ultra-clean robotics, nanometer-precision motion systems, and automated material handling that minimize particle contamination. Every USD 1 billion allocated to chip fabrication typically pulls USD 200–300 million of automation spend, magnifying demand for high-speed wafer transfer robots, machine-learning-driven process control, and safety-integrated PLC platforms. State-level abatements further shift large projects toward the South and Mountain West, where purpose-built greenfield sites can adopt fully digital, lights-out manufacturing cells from day one. Suppliers that bundle hardware, MES software, and lifecycle services gain a competitive edge as fab owners seek turnkey solutions that shorten qualification cycles and protect sensitive.

Labor shortage drives collaborative robotics adoption

Manufacturing payrolls face a 750,000-person gap today and risk 2.1 million unfilled roles by 2030, pressing management teams to deploy collaborative robots (cobots) that assume monotonous, high-repetition tasks while up-skilling employees into quality, maintenance, and data-analytics positions. Surveys show 57% of plants report that robots augment rather than eliminate human jobs, reinforcing adoption even in unionized facilities. Automotive assemblers are first movers, but small and midsize job shops follow suit as plug-and-play cobots drop in price and gain no-code programming interfaces. Federal and state training grants amplify the trend by covering tuition for certificate programs in robot operation and safety, accelerating labor-technology convergence.

Clean-energy manufacturing boost from Inflation Reduction Act

The IRA’s USD 10 billion Qualifying Advanced Energy Project Credit has already directed USD 6 billion into battery cells, solar-grade polysilicon, and grid components. Battery plants in particular demand automated slurry mixing, electrode stacking, and in-line X-ray inspection to hold micron-level tolerances that determine cell longevity and safety. Nearly three-quarters of new factories are sited in economically disadvantaged counties, intensifying the need for automation that compensates for limited local technical expertise. Vendors that combine remote monitoring, AI-powered fault prediction, and 24/7 virtual commissioning gain traction because they reduce ramp-up risk for first-time operators. [3]Source: U.S. Department of the Treasury, “Treasury and IRS Announce $6 Billion in § 48C Tax Credit Allocations,” home.treasury.gov

OSHA-enforced machine-safety compliance raises demand for safety-integrated control systems

OSHA’s stepped-up audits highlight machine-guarding violations, prompting factories to integrate safety PLCs, light curtains, and torque-limited servo drives that meet SIL 2 and SIL 3 standards. Modern safety-integrated systems arrest motion in milliseconds without shutting down entire lines, preserving throughput while protecting personnel. Vendors offering unified platforms that merge standard control and safety logic help manufacturers reduce wiring, spare-parts inventory, and validation time. Insurance carriers reinforce adoption by linking premium discounts to documented safety-system performance

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy OT interoperability challenges in diverse U.S. brownfield facilities | −1.4% | Rust Belt & other legacy sites | Medium term (2-4 years) |

| High initial CapEx limiting adoption by mid-sized manufacturers despite tax credits | −0.8% | Firms with <500 employees nationwide | Short term (≤ 2 years) |

| Cyber-security risks in connected control systems hindering deployment | −1.1% | Critical-infrastructure sectors nationwide | Short term (≤ 2 years) |

| Trade policy volatility and tariff uncertainties affecting automation component imports | −0.6% | Nationwide; higher exposure for mid-sized manufacturers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Legacy OT interoperability challenges in diverse U.S. brownfield facilities

Plants built across several industrial revolutions run a patchwork of proprietary protocols, making seamless data flow difficult. Integrators often confront PLCs installed before Y2K with no native Ethernet interface, forcing custom drivers that inflate project cost and risk. Open-architecture movements such as OPC UA over TSN aim to standardize connectivity, but progress is slower than software vendors predict because downtime windows remain narrow and capital budgets are stretched. Collaborative initiatives involving automation majors and component suppliers have begun to release pre-certified interoperability bundles, yet many small firms still delay projects until clearer return on investment emerges

Cyber-security risks in connected control systems hinder deployment

Manufacturing registered 68 publicly disclosed cyber incidents in 2023, a 19% jump, and ransomware accounted for over half. The discovery of CVE-2024-5659 in a leading PLC family underscored that even safety-critical devices carry exploitable flaws. Average breach cost reached USD 4.45 million, with extended downtime often dwarfing ransom payments. Boards now mandate zero-trust architectures, network segmentation, and asset-inventory audits before authorizing large-scale connectivity projects. Vendors able to demonstrate secure-by-design hardware, signed firmware, and continuous vulnerability disclosure programs gain preferential status in bid evaluations

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Hardware Dominance Amid Services Acceleration

Hardware accounted for 71.25% spending in 2025 as manufacturers purchased robots, drives, sensors, and HMIs to digitalize production lines. The United States factory automation and industrial controls market size for hardware is projected to post mid-single-digit growth while services expand faster, signaling a transition toward subscription-based support, remote condition monitoring, and performance guarantees. Leading suppliers bundle software licenses, cybersecurity management, and workforce training into multi-year agreements that stabilize revenue and align incentives with customer output. Software platforms bridge field data to MES and cloud analytics, enabling closed-loop optimization that lowers scrap and energy intensity. The hardware layer thus remains indispensable, yet value capture is migrating to integrators and OEMs that orchestrate devices, data, and domain expertise into measurable outcomes.

The services segment’s 12.42% CAGR reflects manufacturer preference for predictable operating expenditure over upfront capital outlay. As-a-service robotic welding cells, vision-as-a-service inspection, and security-as-a-service packages resonate with tier-one automotive and consumer packaged goods firms seeking to hedge technology obsolescence. Vendors that co-locate remote operations centers provide 24/7 support and real-time insight, shortening mean time to repair and driving continuous improvement cycles without inflating headcount. Such models unlock new margin pools and differentiate suppliers in a crowded hardware market.

By Type: Industrial Control Systems Lead Amid Field-Device Innovation

Industrial control systems (ICS) held 54.30% share in 2025, underpinned by distributed control systems, safety PLCs, and SCADA suites that coordinate complex multi-line operations. The United States factory automation and industrial controls market size for ICS is expanding steadily as food processors, chemical plants, and pharmaceuticals adopt redundant architectures to satisfy FDA, EPA, and OSHA requirements. Real-time deterministic performance, high availability, and integrated safety functions make modern ICS the backbone of digital factories.

Field devices—sensors, actuators, and machine-vision cameras—are growing faster at 11.30% CAGR as manufacturers push intelligence to the edge. High-resolution optical sensors verify EV battery welds in milliseconds, while vibration nodes stream data to AI models that predict bearing failure days in advance. Edge computing modules process inference locally, reducing bandwidth and latency while supporting closed-loop control. The convergence of 5G, Time Sensitive Networking, and advanced semiconductor supply is lowering cost per sensor and broadening deployment into mid-tier plants previously priced out of widespread IIoT adoption

By End-User Industry: Automotive Leadership Challenged by Food & Beverage Surge

Automotive & transportation producers captured 21.60% revenue in 2025, leveraging decades of automation know-how to reach near-zero defect rates and sub-60-second takt times. They continue to demand high-payload robots, advanced conveyance, and digital twin simulation to support simultaneous EV and internal-combustion vehicle production. However, labor scarcity and evolving food safety regulations are driving the food & beverage segment to invest aggressively, posting a 12.75% CAGR that could narrow the historical gap. High-mix, low-volume SKUs require agile robot-based packaging, hygienic design, and in-line X-ray inspection to meet retailer mandates for traceability. Vendors that package robotic case packing, CIP-qualified sensors, and batch-analytics software into turnkey solutions are winning bids in this expanding vertical.

Process industries such as oil & gas and chemicals exhibit steady demand for intrinsically safe instrumentation and redundant control architectures, while the pharmaceutical sector accelerates adoption of GxP-compliant automation for continuous bioprocessing. Semiconductor fabrication, though a smaller slice of the overall base, is on a high-growth trajectory thanks to federal incentives, amplifying opportunities for suppliers capable of sub-micron motion control and class 10 clean-room compatible robots. Mining and metals plants adopt autonomous haulage and AI-driven ore-sorting to cut emissions and lower energy per ton, rounding out a diversified end-user landscape

Geography Analysis

The Midwest remains the nucleus of the United States factory automation and industrial controls market, anchored by its deep automotive footprint and dense supplier ecosystem. Michigan alone added more than 400 robotics jobs after a USD 110 million facility opening in 2024, reinforcing its role as a robotics hub. Five Midwestern states collectively took 77% of U.S. robot sales, helping local manufacturers raise productivity and defend share against offshore rivals. Yet this regional concentration risks widening a digital divide as firms outside the cluster face longer lead times for integrator support and higher labor costs. State-funded training centers and university partnerships in Iowa and Wisconsin aim to spread expertise, but talent scarcity persists.

The South is the fastest-growing territory as greenfield EV, battery, and semiconductor plants flock to business-friendly incentives, affordable land, and port access. Tennessee, Georgia, and South Carolina attract both foreign and domestic investment, with Schneider Electric’s USD 23.8 million expansion illustrating supplier commitment to serve this corridor. Greenfield projects enable holistic digital-first designs: converged IT/OT networks, AI-driven quality analytics, and modular robot workcells that adapt as program volumes shift. Workforce development grants and community-college curricula tailored to mechatronics foster a steady talent pipeline, further reinforcing the region’s momentum.

The Northeast and West coasts contribute specialized demand. The Northeast’s concentration in aerospace, defense, and medical devices requires high-precision automation and validated data integrity. Collaborative R&D between OEMs and research universities accelerates adoption of machine vision and additive manufacturing solutions. On the West Coast, proximity to tech giants and venture capital fuels pilots in AI-driven robotics, though high real-estate and labor costs temper full-scale deployment. Semiconductor expansions in Arizona and California elevate demand for class 1 clean-room robots and advanced process control, while regional cybersecurity mandates push plants to adopt zero-trust architectures ahead of other states

Competitive Landscape

The United States factory automation and industrial controls market is moderately concentrated, with Rockwell Automation controlling about 42% share across North America. Siemens, ABB, and Schneider Electric leverage global scale, open-architecture portfolios, and aggressive M&A to chip away at this lead. Domestic incumbents counter by pairing specialized domain knowledge with deep installed bases and tight channel partnerships. The competitive arena now hinges less on component features and more on integrated software, digital services, and AI-enabled value propositions .

Strategic alliances with technology firms are reshaping market share trajectories. Rockwell’s tie-up with NVIDIA embeds GPU-accelerated AI into PLC programming and virtual commissioning, slashing simulation time and improving first-pass yield. Siemens’ acquisition of ebm-papst’s drive business broadens its mechatronics range and positions the company for autonomous mobile robot growth. Emerson’s Project Beyond introduces software-defined control platforms that abstract hardware layers, enabling flexible upgrades on existing assets and protecting stranded investments—a compelling pitch for brownfield operators .

Acquisition activity intensifies as vendors pursue niche capabilities: Lear bought WIP Industrial Automation to gain computer vision IP, while AMETEK snapped up Virtek Vision to strengthen laser-guided inspection in aerospace composites. Start-ups pioneering low-cost AI vision, autonomous intralogistics, and cybersecurity orchestration represent future targets as majors race to assemble end-to-end digital manufacturing stacks. The winners will be those balancing open ecosystems, rigorous security, and clear ROI for customers navigating workforce shortages and fast-moving regulatory demands

United States Factory Automation And Industrial Controls Industry Leaders

-

Rockwell Automation Inc.

-

Honeywell International Inc.

-

ABB Ltd

-

Schneider Electric SE

-

Emerson Electric Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Rockwell Automation partnered with NEO Battery Materials to automate a 240-ton silicon anode facility in Ontario, with future U.S. plants planned.

- May 2025: Emerson launched Project Beyond, a software-defined operations platform integrating control, data, and AI for brownfield modernization.

- April 2025: Schneider Electric announced USD 700 million U.S. manufacturing investment through 2027, creating 1,000 jobs focused on digitalization and energy infrastructure.

- March 2025: Rockwell Automation showcased Emulate3D Factory Test, powered by NVIDIA Omniverse, enabling virtual controls testing before deployment.

United States Factory Automation And Industrial Controls Market Report Scope

Factory automation refers to the use of control systems, machinery, and computer systems to automate industrial processes and tasks, reducing the need for human intervention. This includes processes like manufacturing, material handling, and quality control. The study tracks the revenue accrued through the sale of factory automation and industrial control systems through various end-user industries across United States. The study also tracks key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports market estimations and growth rates over the forecast period.

The United States factory automation and industrial controls market is segmented by type (industrial control systems and field devices) and end-user industry (oil and gas, chemical and petrochemical, power and utilities, food and beverage, automotive and transportation, and pharmaceutical). The market size and forecasts are provided in terms of value in USD for all the above segments.

By Component

| Hardware |

| Software |

| Services |

By Type

| Industrial Control Systems | Distributed Control System (DCS) |

| Programmable Logic Controller (PLC) | |

| Supervisory Control and Data Acquisition (SCADA) | |

| Product Lifecycle Management (PLM) | |

| Manufacturing Execution System (MES) | |

| Human Machine Interface (HMI) | |

| Other Industrial Control Systems | |

| Field Devices | Machine Vision |

| Industrial Robotics | |

| Motors and Drives | |

| Safety Systems | |

| Sensors and Transmitters | |

| Other Field Devices |

By End-user Industry

| Oil and Gas |

| Chemical and Petrochemical |

| Power and Utilities |

| Food and Beverage |

| Automotive and Transportation |

| Pharmaceutical |

| Semiconductor and Electronics |

| Metals and Mining |

| Pulp and Paper |

| Other End-user Industries |

By Region (United States)

| Northeast U.S. |

| Midwest U.S. |

| South U.S. |

| West U.S. |

| By Component | Hardware | |

| Software | ||

| Services | ||

| By Type | Industrial Control Systems | Distributed Control System (DCS) |

| Programmable Logic Controller (PLC) | ||

| Supervisory Control and Data Acquisition (SCADA) | ||

| Product Lifecycle Management (PLM) | ||

| Manufacturing Execution System (MES) | ||

| Human Machine Interface (HMI) | ||

| Other Industrial Control Systems | ||

| Field Devices | Machine Vision | |

| Industrial Robotics | ||

| Motors and Drives | ||

| Safety Systems | ||

| Sensors and Transmitters | ||

| Other Field Devices | ||

| By End-user Industry | Oil and Gas | |

| Chemical and Petrochemical | ||

| Power and Utilities | ||

| Food and Beverage | ||

| Automotive and Transportation | ||

| Pharmaceutical | ||

| Semiconductor and Electronics | ||

| Metals and Mining | ||

| Pulp and Paper | ||

| Other End-user Industries | ||

| By Region (United States) | Northeast U.S. | |

| Midwest U.S. | ||

| South U.S. | ||

| West U.S. | ||

Key Questions Answered in the Report

How big is the United States Factory Automation And Industrial Controls Market?

The United States Factory Automation And Industrial Controls Market size is expected to reach USD 54.23 billion in 2026 and grow at a CAGR of 10.18% to reach USD 88.05 billion by 2031.

What is the current United States Factory Automation And Industrial Controls Market size?

In 2026, the United States Factory Automation And Industrial Controls Market size is expected to reach USD 54.23 billion.

Who are the key players in United States Factory Automation And Industrial Controls Market?

Rockwell Automation Inc., Honeywell International Inc., ABB Ltd, Schneider Electric SE and Emerson Electric Company are the major companies operating in the United States Factory Automation And Industrial Controls Market.

What years does this United States Factory Automation And Industrial Controls Market cover, and what was the market size in 2025?

In 2025, the United States Factory Automation And Industrial Controls Market size was estimated at USD 54.23 billion. The report covers the United States Factory Automation And Industrial Controls Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the United States Factory Automation And Industrial Controls Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: