India Lathe Machines Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

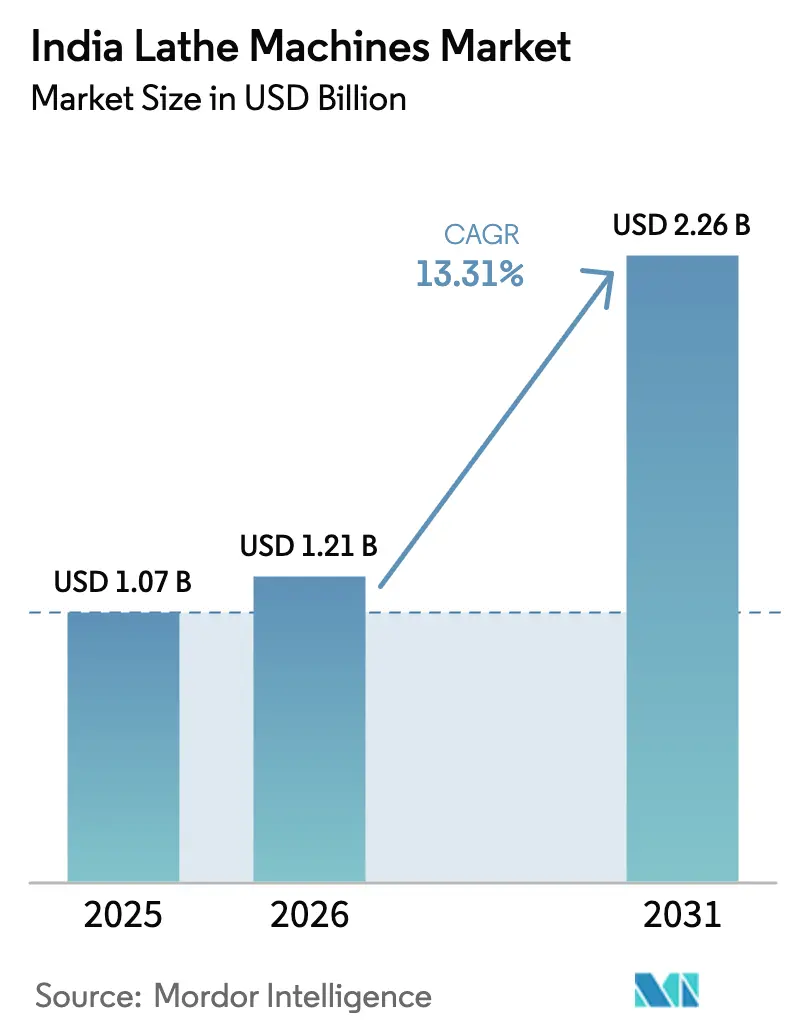

| Base Year Market Size (2025) | USD 1.07 Billion |

| Market Size (2026) | USD 1.21 Billion |

| Market Size (2031) | USD 2.26 Billion |

| Growth Rate (2026 - 2031) | 13.31% CAGR |

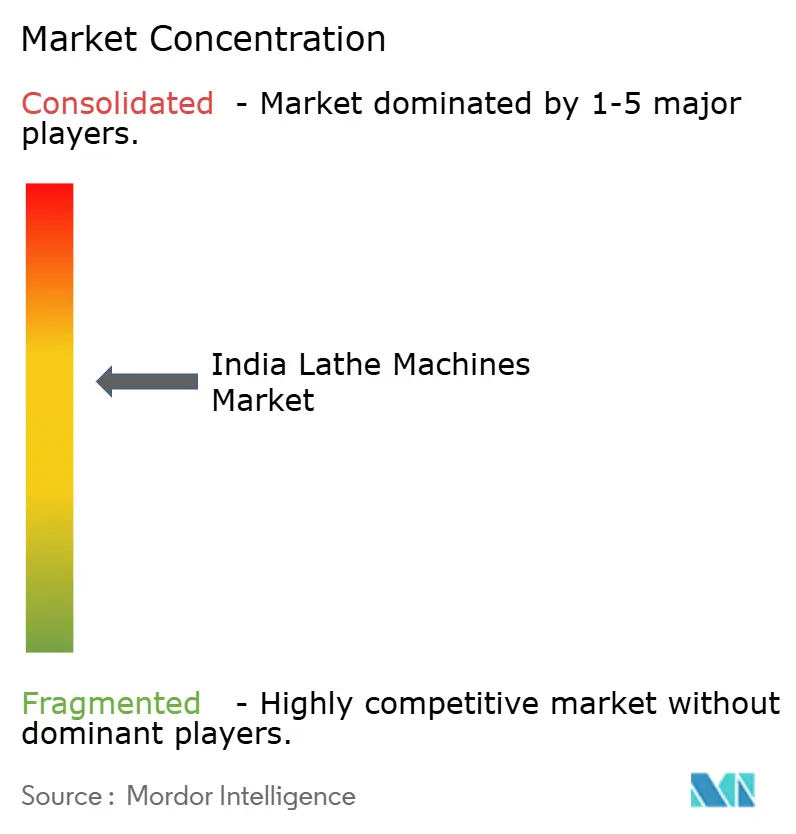

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Lathe Machines Market Analysis by Mordor Intelligence

The India lathe machines market size is expected to increase from USD 1.07 billion in 2025 to USD 1.21 billion in 2026 and reach USD 2.26 billion by 2031, growing at a CAGR of 13.31% over 2026-2031. Robust policy support, rising electric-vehicle power-train demand and rapid growth of medical-device clusters are steering capital spending toward multi-axis and Swiss-type CNC platforms. Tier-1 automotive and aerospace suppliers are consolidating machining steps into single-setup operations, while micro-, small- and medium-size enterprises (MSMEs) use retrofit kits to convert legacy manual equipment at one-fifth of the cost of a new CNC lathe. Domestic builders benefit from Production Linked Incentive (PLI) subsidies that lower price gaps with imports, yet persistent power-quality issues in tier-2 hubs inflate maintenance costs. Skill shortages and high ticket sizes for six-axis systems temper upgrade velocity, but expanding credit-guarantee coverage and local assembly plants are shortening delivery cycles and reducing landed prices.

Key Report Takeaways

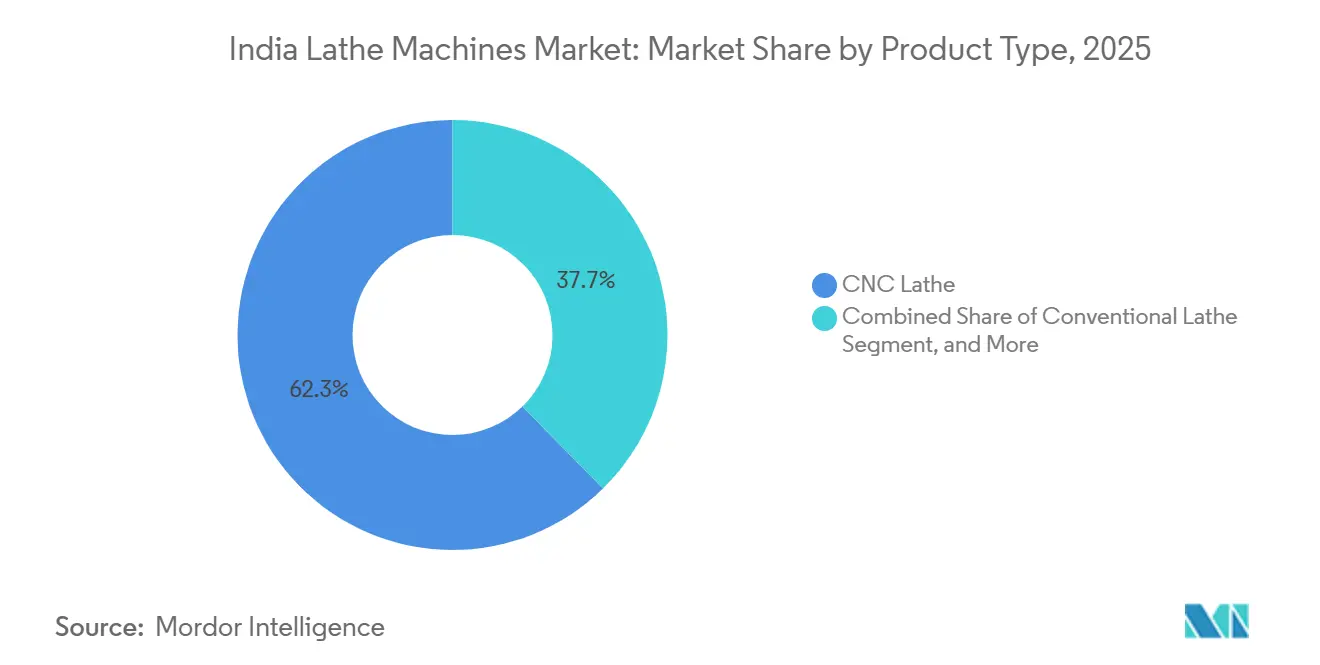

- By product type, CNC lathes led with 62.34% of India lathe machines market share in 2025, while Swiss-type automatics are forecast to expand at a 13.86% CAGR to 2031.

- By control type, automatic systems commanded 58.78% share of the India lathe machines market size in 2025, and are projected to register a 13.98% CAGR through 2031.

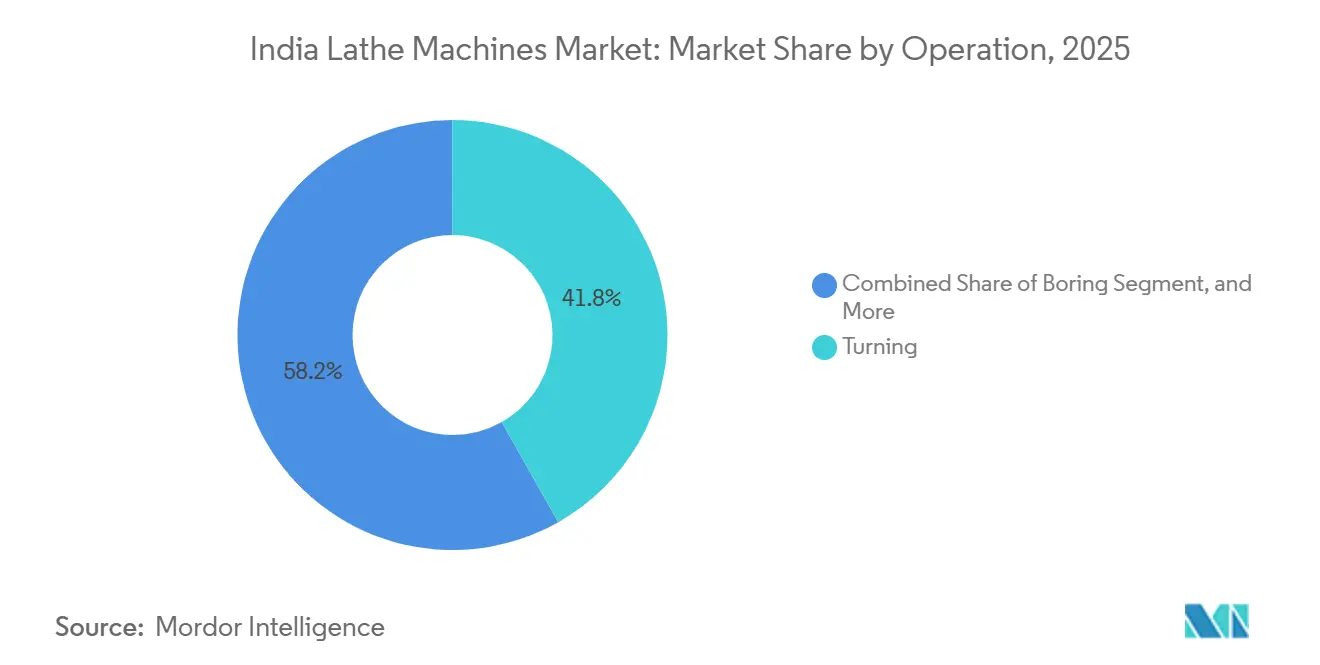

- By operation, turning was the largest category at 41.82% share in 2025, whereas cutting and parting processes are advancing at a 14.14% CAGR to 2031.

- By end-user industry, automotive accounted for 43.56% revenue in 2025, yet medical-device manufacturing is poised to grow fastest at a 14.28% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide, activity is shaped by contributions from multiple countries and regions, with India representing one among them. The global report on lathe machines market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

India Lathe Machines Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Automation Adoption in Indian MSME Manufacturing | +2.8% | National, with concentration in Gujarat, Maharashtra, Tamil Nadu | Short term (≤ 2 years) |

| Government PLI Incentives for Domestic Capital-Goods Production | +2.4% | National, early gains in Karnataka, Tamil Nadu, Haryana | Medium term (2-4 years) |

| Surge in EV Power-Train Machining Demand | +2.2% | West India (Pune, Aurangabad), South India (Chennai, Bangalore) | Medium term (2-4 years) |

| Rapid Rise of Medical-Device Clusters in Tamil Nadu and Telangana | +1.9% | South India, with spillover to Maharashtra | Long term (≥ 4 years) |

| Industry 4.0 Retrofit Kits Lowering Upgrade Costs | +1.6% | National, pilot deployments in Gujarat, Haryana | Short term (≤ 2 years) |

| Local Sourcing Mandates in Defence Offset Contracts | +1.4% | National, concentrated in Bangalore, Hyderabad, Pune aerospace corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated Automation Adoption In Indian MSME Manufacturing

India hosts about 72 million registered MSMEs, many of which are upgrading from conventional to CNC lathes to meet domestic supply-chain and export quality norms. A 2024 Gujarat pilot covering 750 factories showed scrap rates falling from 8-12% to 2-3% after CNC conversion, prompting wider replication programs. CNC installations at MSMEs grew 18% year-over-year in 2025 as the Credit Guarantee Fund Trust covered up to 85% of equipment value on loans below INR 50 lakh (USD 60,000). Yet penetration remains uneven because tier-2 cities such as Rajkot and Ludhiana still run 60-65% conventional lathes. The National Capital Goods Policy, which targets domestic machine-tool output of USD 4 billion, is cutting lead times to as little as four months, so the influence of this driver peaks by 2027.

Government PLI Incentives For Domestic Capital-Goods Production

The 2024 PLI scheme earmarked INR 1,207 crore (USD 14.5 million) for 33 CNC-oriented projects, reimbursing 4-6% of incremental sales for five years. India imported machine tools worth INR 15,352 crore (USD 1.85 billion) in 2023-24, of which turning centers formed roughly one-third.[1]Ministry of Commerce and Industry, “Foreign Trade Statistics 2023-24,” commerce.gov.in New greenfield facilities in Karnataka and Tamil Nadu promise 4- and 5-axis lathes with home-grown Fanuc-compatible controllers, while the 530-acre Tumakuru Machine Tools Park integrates foundry, fabrication and assembly services to slash component lead times by up to 40% . Because capacity commissioning spans two to three years, the bulk of output and export push arrives between 2027 and 2029.

Surge In EV Power-Train Machining Demand

Electric-vehicle production hit 1.7 million units in 2024, and traction-motor value could crest INR 96,000 crore (USD 1.156 billion) by 2030. Multi-axis CNC and Swiss-type automatics are essential to hold sub-5-micron tolerances on rotor shafts and stator housings, parts whose count rises to as many as 12 per motor compared with 3-5 in internal-combustion engines. Bureau of Energy Efficiency guidelines for 2025 encourage 15-20% drivetrain weight cutting, which in turn drives thin-wall machining on high-speed lathes equipped with through-coolant and vibration-damping tool holders.[2]Bureau of Energy Efficiency, “Energy Conservation Building Code 2025,” beeindia.gov.in Commercial-vehicle electrification, tipped to reach 25-30% of new truck sales by 2030, further widens the market for lathes with swing diameters above 500 mm.

Rapid Rise Of Medical-Device Clusters In Tamil Nadu And Telangana

PLI disbursements of INR 1,205.52 crore (USD 14.5 million) underpin parks near Chennai and Hyderabad that cater to implants and diagnostic gear. Global majors such as Stryker and Boston Scientific demand Swiss-type machines capable of machining titanium hip stems and stainless-steel catheter hubs to Ra 0.8 micron finishes. Central Drugs Standard Control Organisation rules require ISO 13485 certification, spurring investment in temperature-controlled shops with traceability software directly linked to CNC controllers.[3]Central Drugs Standard Control Organisation, “Medical Device Regulations,” cdsco.gov.in Cluster synergies, abundant skilled labor and export-market orientation mean impact will keep rising into the next decade.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Capex for Multi-Axis CNC Systems | -2.1% | National, acute in tier-2 and tier-3 cities | Short term (≤ 2 years) |

| Inadequate Nationwide Machine-Tool Financing Instruments | -1.8% | National, concentrated in MSME-heavy states (Uttar Pradesh, Bihar, Rajasthan) | Medium term (2-4 years) |

| Shortage of Trained CNC Programmers and Operators | -1.5% | National, severe in North and East India | Medium term (2-4 years) |

| Persistent Power-Quality Issues in Tier-2 Industrial Hubs | -1.2% | Gujarat, Rajasthan, Punjab, Uttar Pradesh tier-2 cities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Capex For Multi-Axis CNC Systems

Four- to six-axis lathes cost USD 80,000-250,000, roughly double or triple the annual turnover of a typical Indian job shop. A 2024 survey showed 62% of MSMEs quoting purchase price as the main block to CNC migration. Leasing penetration is barely 18%, far below the 50% norm in Germany, while the CGTMSE ceiling of INR 50 lakh falls short of premium machine prices. Advance payments of up to 40% strain liquidity for manufacturers in Rajkot, Coimbatore and Faridabad, so many defer purchases despite 18-24 month payback periods. The restraint bites hardest in the next two years as interest-rate volatility keeps risk premiums high.

Shortage Of Trained CNC Programmers And Operators

India’s 18 Tool Rooms graduated only 12,000 CNC-certified operators in 2024 versus a need of 35,000-40,000, forcing factories to run at 55-65% utilization and accept 10-15% scrap from programming errors. Industrial Training Institute syllabi remain locked on G-code for two-axis machines, lagging the multi-axis CAM skills demanded by Swiss-type automatics. Private OEM academies have trained 3,000-4,000 operators since 2023 but mostly serve large corporations. Planned Centers of Excellence will not add significant headcount until 2027-2028, keeping this drag relevant for the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Swiss Automatics Gain On Medical Precision

CNC lathes captured 62.34% of 2025 India lathe machines market share, reflecting their broad use across automotive, general engineering and metal fabrication. Swiss-type automatics, however, are forecast to outpace the India lathe machines market size with a 13.86% CAGR through 2031, fueled by implant and aerospace components that demand bar-fed machining and tolerances below 5 microns. Conventional lathes remain entrenched in roughly one-third of workshops that produce pump shafts and textile rolls, yet ISO 9001- and AS9100-driven audits increasingly disqualify non-CNC equipment.

Imports still dominate the Swiss segment, with Citizen Machinery, Tsugami and Star Micronics holding nearly three-quarters of sales. Domestic builders such as Jyoti CNC Automation and Ace Micromatic target MSMEs with entry-level models priced USD 25,000-40,000, integrating Fanuc or Siemens controls to bridge cost and capability gaps. Licensing moves, including Lakshmi Machine Works’ 2024 guide-bushing collaboration, aim to localize critical components and chip away at foreign dominance. Miniaturization trends in wearables and catheter fittings ensure a durable growth premium for Swiss automatics.

By Control Type: Automation Drives Lights-Out Machining

Automatic systems commanded 58.78% of 2025 India lathe machines market share and are set for a 13.98% CAGR through 2031 as factories push unmanned night shifts to offset labor cost inflation. Semi-automatic units linger in prototype and short-run roles but lose share as robotic loaders and pallet changers drop below USD 20,000 per cell. Manual machines still serve 25-30% of small repair shops yet face a generational skills void, with younger machinists gravitating toward CNC touchscreens.

Retrofit kits costing USD 8,000-15,000 allow MSMEs to reach 70-80% of new-machine precision, extending the useful life of cast-iron beds by a decade. Gujarat’s upgrade pilot showed cycle-time cuts of 25-35% after retrofit adoption. Still, limited spindle speeds and absence of live tooling restrict kits from high-spec EV and orthopedic work. Tier-1 suppliers increasingly treat Industry 4.0 predictive-maintenance readiness as table stakes, accelerating the pull toward fully automatic platforms.

By Operation: Parting Operations Surge With Medical Demand

Turning remained the workhorse at 41.82% share in 2025, yet cutting and parting operations are forecast to grow fastest at 14.14% CAGR as catheter, needle and screw makers insist on burr-free shearing. Swiss-type automatics excel here thanks to guide-bushing rigidity on slender bars with length-to-diameter ratios above 10:1. Facing and boring stay pivotal for flange and hydraulic-cylinder work, but multi-tasking turn-mill centers increasingly consolidate these steps, nudging standalone demand lower.

Advances in TiAlN- and AlCrN-coated carbide parting inserts lift permissible cutting speeds by up to 40%, slashing per-unit cost in titanium and stainless orthopedic runs. The shift toward lights-out production also benefits parting because broken-tool detection can halt machines before scrap accumulates. Over the forecast horizon, parting’s share gain will come mainly at the expense of basic turning tasks displaced by integrated machining cells.

By End-User Industry: Medical Devices Outpace Automotive Growth

Automotive applications held 43.56% of India lathe machines market in 2025, anchored by 26 million vehicle outputs and dense tier-1 corridors around Pune and Chennai. Medical-device manufacturers, however, are projected to grow at 14.28% CAGR through 2031, beating automotive as implant makers chase double-digit export margins and tap PLI subsidies. Aerospace and defense machining tracks a 13-14% CAGR as offset rules localize turbine shafts and missile housings.

Higher gross margins often 35-45% on implants versus 15-20% on engine parts compress CNC payback to under two years for medical subcontractors, spurring Swiss-type purchases in Chennai’s and Hyderabad’s device parks. Automotive demand remains solid for EV rotor shafts and aluminum motor housings but loses incremental share as electric drivetrains contain 30-40% fewer precision-turned parts than combustion engines. Defense push toward USD 25 billion output by 2025 keeps specialty alloy machining relevant, sustaining a broad customer base across verticals.

Geography Analysis

West India, led by Maharashtra and Gujarat, dominated 2025 shipments thanks to Pune’s vehicle ecosystem and Rajkot’s MSME clusters. Proximity to Jawaharlal Nehru Port streamlines import of high-end machines and export of precision components, yet voltage swings of ±10% in Rajkot and Aurangabad cause servo and encoder failures that drive 15-20% of downtime. EV investments by Tata Motors in Pune and Mahindra in Chakan will push the region toward larger swing-capacity CNC lathes for aluminum and copper components.

South India is the fastest-growing territory through 2031. Bangalore hosts aerospace primes such as Hindustan Aeronautics Limited, while Chennai anchors both automotive and the country’s largest medical-device park, which already houses a dozen Swiss-lathe lines turning orthopedic screws for the United States and Europe. Tumakuru’s 530-acre machine-tool park offers foundry-to-assembly integration that trims part lead times by up to 40%, a major lure for domestic builders. Tamil Nadu and Karnataka graduate around 5,000 CNC-certified operators each year, easing the skill bottleneck that plagues northern peers.

North India centers on Gurgaon, Ludhiana and Noida, where tractors, two-wheelers and household appliances sustain steady lathe demand. Growth is muted by a deficit of skilled programmers, forcing firms to import labor from the south at wage premiums of around 25%. East India remains smallest but gains momentum as Odisha’s steel expansions feed downstream hydraulic and mining component machining. Investments in power stabilization and tool-room institutes could unlock latent demand across Kolkata and Jamshedpur.

Competitive Landscape

Japanese and European builders Yamazaki Mazak, DMG MORI, Okuma and Citizen Machinery collectively hold about 55-60% share through leadership in multi-axis, Swiss-type and turn-mill platforms. They deepen moats by assembling locally to bypass 7.5-10% customs duties and by embedding Siemens Sinumerik ONE controllers that add real-time tool-wear analytics. Domestic firms Lakshmi Machine Works, Bharat Fritz Werner, Jyoti CNC Automation and Ace Micromatic secure 25-30% share by underpricing imports 30-40% and offering Hindi-language support plus 48-hour service coverage across 200 dealers.

Lakshmi Machine Works’ 2025 Coimbatore plant boosts annual capacity by 1,200 units and debuts an indigenous guide-bushing system, trimming import content by 25%. DMG MORI’s Bangalore line now hits 45% local sourcing in coolant and electrical subsystems, qualifying for PLI rebates. Chinese entrants such as Doosan Machine Tools sell at 20-25% discounts but face skepticism over after-sales reach, limiting share gains to cost-sensitive tier-2 workshops.

Retrofit and entry-level CNC niches offer white-space for Indian brands, while high-end multi-axis remains contested turf where technology partnerships become decisive. Certification requirements—ISO 9001, ISO 13485 and AS9100—split the user base into premium, compliance-driven buyers and cost-focused general manufacturers, reinforcing a two-tier competitive structure likely to persist beyond 2031.

India Lathe Machines Industry Leaders

Yamazaki Mazak Corporation

DMG MORI Aktiengesellschaft

Doosan Machine Tools Co. Ltd. (DN Solutions)

Citizen Machinery Co. Ltd.

Star Micronics Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Müller Hydraulik launched combiloop high-pressure systems at IMTEX 2025, marking its India debut and showcasing coolant integration for CNC turning centers.

- March 2025: Okuma’s Bangalore service center earned ISO 13485 certification, widening its medical-device clientele.

- February 2025: Citizen Machinery launched the Cincom L20-XII Swiss-type lathe in India, priced at USD 180,000 for titanium implant machining.

- January 2025: Lakshmi Machine Works commissioned a greenfield CNC-lathe plant in Coimbatore, capacity 1,200 units per year, featuring 4- and 5-axis models that integrate home-grown guide-bushing systems and target EV power-train work.

India Lathe Machines Market Report Scope

A lathe machine is a machine tool used to shape materials (usually metal or wood) by rotating the workpiece while a cutting tool removes material to create the desired shape.The material is clamped in a rotating chuck or between centers. As it spins, a stationary cutting tool is moved against it to cut, shape, drill, or finish the surface.

The India Lathe Machines Market Report is Segmented by Product Type (CNC Lathe, Conventional Lathe, Swiss-Type Automatic Lathe), Control Type (Manual, Semi-automatic, Automatic), Operation (Turning, Facing, Boring, Cutting/Parting), End-user Industry (Automotive, Aerospace and Defence, General Manufacturing, Metal Industry, Other End-user Industries). The Market Forecasts are Provided in Terms of Value (USD).

| CNC Lathe |

| Conventional Lathe |

| Swiss-Type Automatic Lathe |

| Manual |

| Semi-automatic |

| Automatic |

| Turning |

| Facing |

| Boring |

| Cutting / Parting |

| Automotive |

| Aerospace and Defence |

| General Manufacturing |

| Metal Industry |

| Other End-user Industries |

| By Product Type | CNC Lathe |

| Conventional Lathe | |

| Swiss-Type Automatic Lathe | |

| By Control Type | Manual |

| Semi-automatic | |

| Automatic | |

| By Operation | Turning |

| Facing | |

| Boring | |

| Cutting / Parting | |

| By End-user Industry | Automotive |

| Aerospace and Defence | |

| General Manufacturing | |

| Metal Industry | |

| Other End-user Industries |

Key Questions Answered in the Report

How quickly is the India lathe machines market expected to grow through 2031?

The market is projected to expand from USD 1.21 billion in 2026 to USD 2.26 billion by 2031, reflecting a 13.31% CAGR over the forecast period.

Which product category is expanding faster than the overall market?

Swiss-type automatic lathes are forecast to grow at 13.86% CAGR, slightly ahead of the total market pace.

Why are medical-device manufacturers investing heavily in CNC lathes?

Implant and surgical-instrument makers require sub-5-micron tolerances and ISO 13485 compliance, both of which favor Swiss-type and multi-axis CNC platforms that shorten payback to under two years.

What is the main barrier for MSMEs upgrading to multi-axis CNC systems?

Upfront prices of USD 80,000-250,000 exceed typical MSME annual revenue, and leasing penetration remains below 20%, limiting financing options.

Which region of India shows the fastest growth for lathe machines?

South India, especially Tamil Nadu and Karnataka, is the fastest-growing region due to aerospace, automotive and medical-device investments coupled with the nation’s highest output of CNC-trained labor.

How is government policy supporting domestic lathe production?

The PLI scheme reimburses 4-6% of incremental sales on approved CNC projects, while machine-tool parks like Tumakuru integrate casting, fabrication and assembly to cut lead times by up to 40%.

Page last updated on: