Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

The Middle East and Africa (MEA) Industrial Automation Market Report is Segmented by Solution Type (Automated Material-Handling Solutions, and Factory-Automation Solutions), Component (Hardware, Software, and More), End-User Industry (Discrete Manufacturing, and More), Technology (IIoT, Edge Computing, Cloud MES, AI Analytics, and AR/VR), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

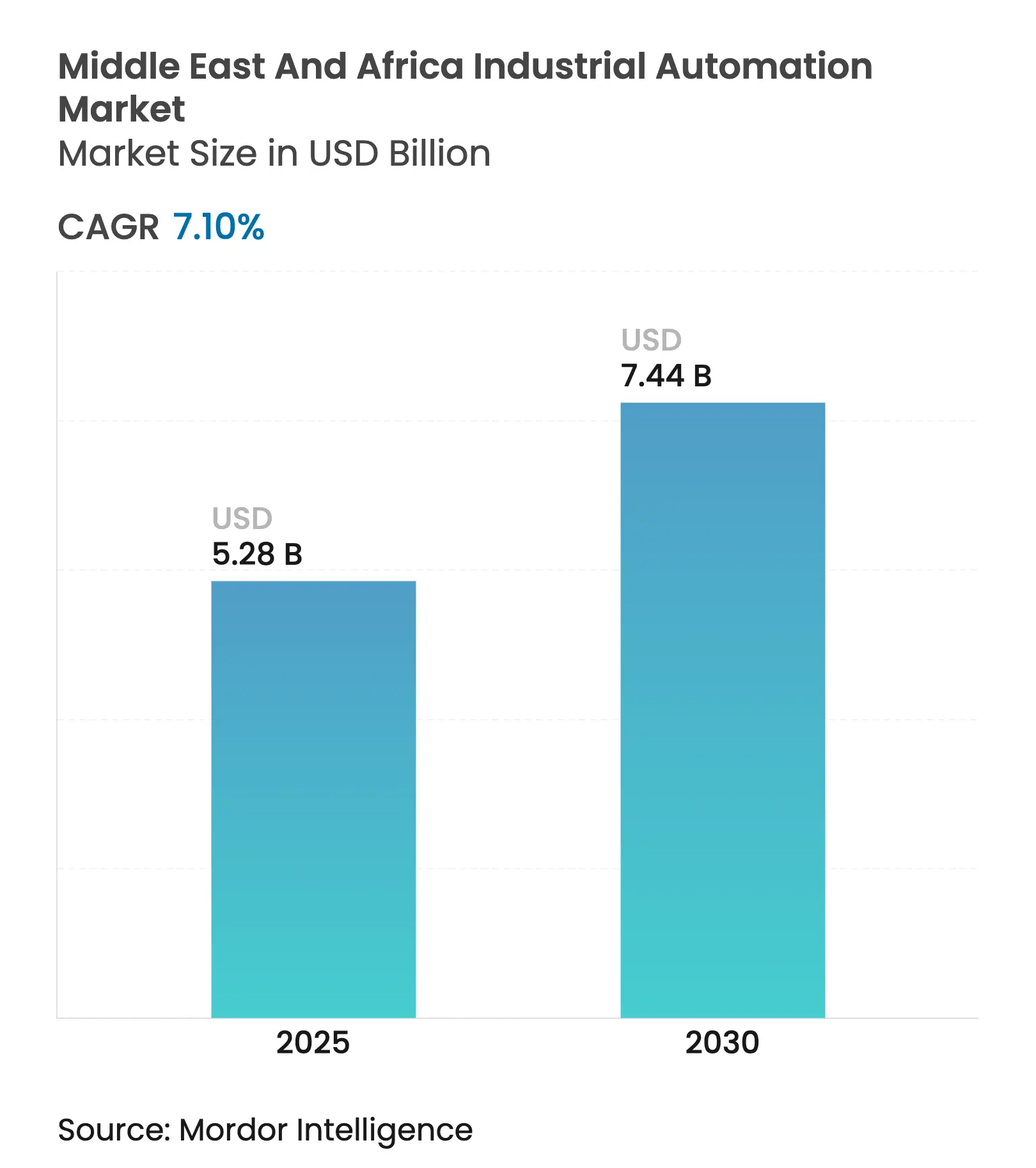

| Market Size (2025) | USD 5.28 Billion |

| Market Size (2030) | USD 7.44 Billion |

| Growth Rate (2025 - 2030) | 7.10 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The Middle East and Africa industrial automation market size stands at USD 5.28 billion in 2025 and is on course to reach USD 7.44 billion by 2030, expanding at a 7.10% CAGR over the period. A surge in sovereign-wealth-fund spending, localization mandates such as Saudi Vision 2030, and the build-out of green-hydrogen and e-commerce logistics assets anchor growth momentum. Regional customers are pivoting from isolated control upgrades toward plant-wide digital transformation projects that combine sensors, industrial IoT, AI analytics, and cybersecurity. Multinational vendors have responded with joint ventures and local assembly plants that shorten lead times, meet content rules, and transfer skills. At the same time, financing innovations, equipment-as-a-service and vendor-backed credit-are accelerating deployments among mid-sized manufacturers that previously lacked capital access.

Key Report Takeaways

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Government-backed localization programs (Saudi Vision 2030) Government-backed localization programs (Saudi Vision 2030) | +1.8% | Middle East, primarily Saudi Arabia and UAE | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+1.8% | Geographic Relevance :Middle East, primarily Saudi Arabia and UAE | Impact Timeline :Medium term (2-4 years) |

Rapid e-commerce warehousing growth Rapid e-commerce warehousing growth | +1.2% | Global, with concentration in GCC and South Africa | Short term (≤ 2 years) | |||

Energy-sector digital-oil-field roll-outs Energy-sector digital-oil-field roll-outs | +1.5% | Middle East and North Africa oil-producing regions | Medium term (2-4 years) | |||

Declining robot prices and financing models Declining robot prices and financing models | +0.9% | Global, with faster adoption in Middle East | Short term (≤ 2 years) | |||

Green hydrogen giga-projects automation demand Green hydrogen giga-projects automation demand | +1.1% | Middle East, Morocco, Egypt | Long term (≥ 4 years) | |||

Rise of sovereign wealth-fund tech investments Rise of sovereign wealth-fund tech investments | +0.8% | Middle East, primarily GCC countries | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Government-backed Localization Programs Drive Transformation

Mandatory local-content thresholds under Saudi Vision 2030 and the UAE’s similar policies are forcing global suppliers to manufacture or assemble inside the GCC. The Public Investment Fund’s Accelerated Manufacturing Program has already seeded robot factories via the ALAT-SoftBank joint venture. NEOM’s USD 8.4 billion green-hydrogen complex embeds automation contracts that stipulate local engineering participation. Emerson’s 13,000 m² Dammam hub shows how suppliers establish regional lines for control valves, PLC panels, and instrumentation. These moves shorten delivery cycles, lower import costs, and upskill local workforces, creating a virtuous circle of demand for the Middle East and Africa industrial automation market. Over the medium term, localization is expected to add 1.8% points to the overall forecast CAGR by anchoring manufacturing ecosystems that absorb successive waves of digital technology.

E-commerce Warehousing Expansion Accelerates Adoption

Sky-high online-order volumes are driving 24-hour fulfillment centers that depend on goods-to-person robotics and AI-enabled slotting algorithms. Kuwait’s first AutoStore facility for Raha E-Grocery demonstrated 30% space savings and three-fold picking speed increases.[1]Swisslog, “Swisslog Builds Kuwait’s First Automated Grocery Fulfilment Centre,” swisslog.com Saudi supermarket group BinDawood earmarked USD 390 million for dark-store and micro-fulfillment automation. In Egypt, Roboost’s AI dispatch engine reached 99.8% task automation, cutting delivery times by 35%. Strategic partnerships like Apex-Dematic extend advanced intralogistics from the GCC to Southern Africa. Collectively, these projects raise short-term demand for conveyor/sortation, AMR fleets, WMS, and computer-vision QA, lifting the Middle East and Africa industrial automation market.

Energy-Sector Digital-Oil-Field Roll-outs Transform Operations

National oil companies are digitizing seismic, drilling, and production workflows to extract marginal barrels at lower cost. ADNOC’s ENERGYai improved seismic interpretation accuracy by 70% and now oversees thousands of wells via AI agents. Saudi Aramco’s Marjan megaproject uses virtual commissioning to synchronize yards on three continents, eliminating costly re-work. Halliburton and Nabors completed the first fully automated drilling sequence in Oman, slashing non-productive time by double digits. As energy firms chase barrel-of-oil equivalency gains, orders for edge compute nodes, wired/wireless condition sensors, and AI model-hosting platforms continue to swell.

Declining Robot Prices and Financing Models Open the Mid-tier

Component commoditization and global overcapacity have trimmed average selling prices for six-axis arms by roughly 18% since 2020. Vendors now bundle robots with subscription software, maintenance, and embedded finance, cutting upfront cash outlays by up to 60%. The International Federation of Robotics recorded a 31% compound rise in autonomous mobile robot shipments between 2020 and 2023.[2]International Federation of Robotics, “Mobile Robots Revolutionize Industry,” ifr.org Lower cost barriers entice mid-sized food processors and metal-fabrication shops across the GCC and North Africa into first-time automation projects, expanding the addressable base for the Middle East and Africa industrial automation market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Prolonged political instability in parts of Africa Prolonged political instability in parts of Africa | -1.3% | Sub-Saharan Africa, excluding South Africa | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:-1.3% | Geographic Relevance :Sub-Saharan Africa, excluding South Africa | Impact Timeline :Long term (≥ 4 years) |

Fragmented standards and skills mismatch Fragmented standards and skills mismatch | -0.8% | Regional, with higher impact in Africa | Medium term (2-4 years) | |||

Under-developed OT-cyber-insurance market Under-developed OT-cyber-insurance market | -0.4% | Global, with concentration in emerging markets | Short term (≤ 2 years) | |||

Persistent power-quality issues outside GCC Persistent power-quality issues outside GCC | -0.6% | Africa and parts of Middle East excluding GCC | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Political Instability Constrains African Market Development

Coups in the Sahel and election-related unrest have frozen capital budgets for industrial parks and mines. Research from the Foundation for Strategic Research cites climate-linked resource pressure as a “threat multiplier” that fuels social unrest. Zambia’s copper sector, for instance, battles grid disruptions and policy uncertainty that delay process-control retrofits. While South Africa, Morocco, and Egypt remain comparatively stable, investors often demand higher hurdle rates for cross-border installations, reducing project counts and shaving 1.3 percentage points off the regional CAGR.

Skills Mismatch and Standards Fragmentation Limit Adoption

A World Economic Forum survey found 87% of African CEOs worried about technical skill gaps. Even in the GCC, only 26.4% of companies that claim ISA-95 alignment actually exchange live data between ERP and shop-floor assets. Multiple industrial-Ethernet protocols and nascent TSN adoption complicate integration and raise commissioning costs. Saudi programs such as Doroob target 20,000 AI specialists by 2030, but smaller economies lack equivalent pipelines. Until training catches up, skills scarcity is likely to subtract 0.8% points from the Middle East and Africa industrial automation market CAGR.

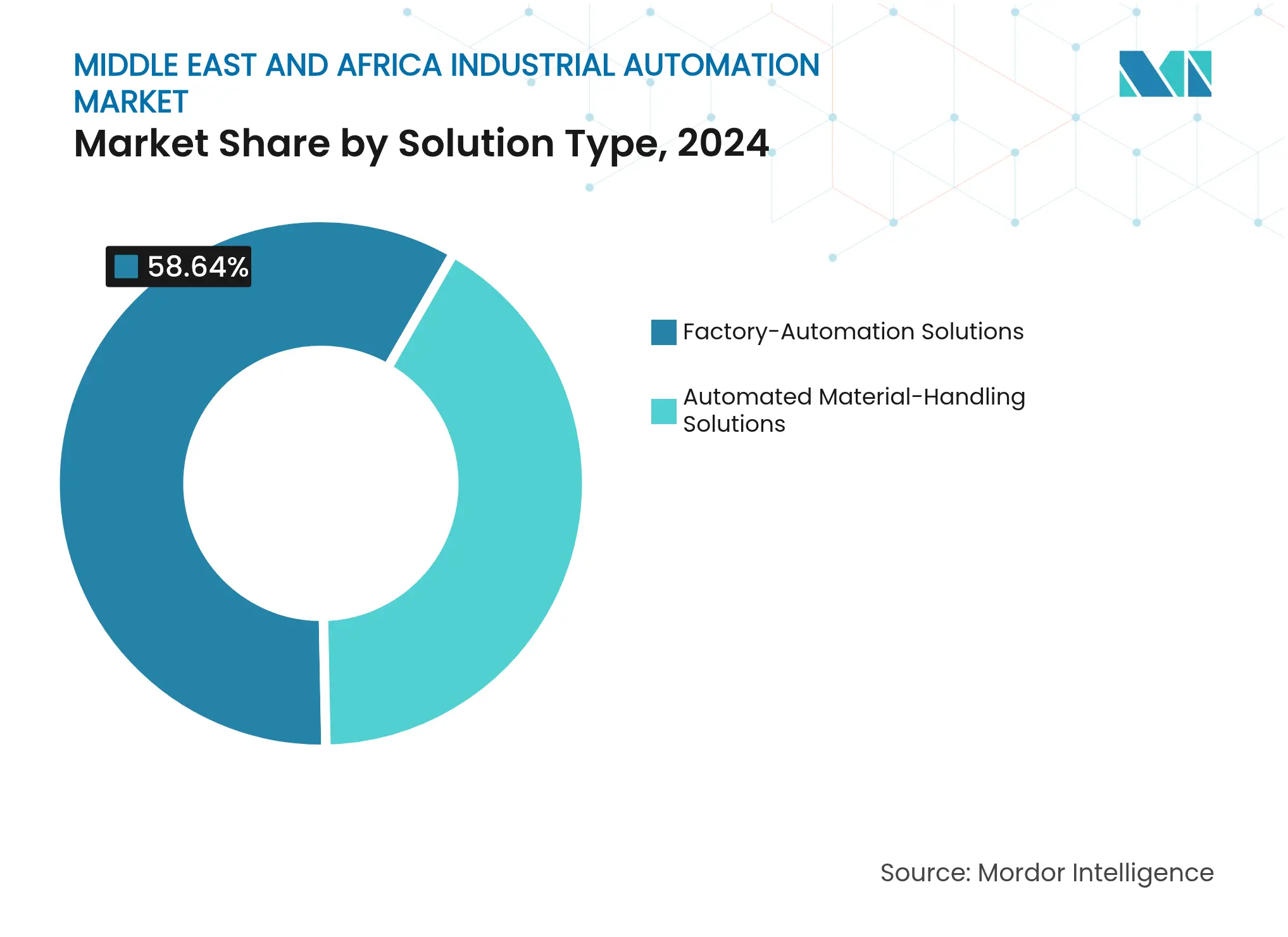

By Solution Type: Factory Automation Dominates Amid Mobile-Robot Surge

Factory-Automation Solutions accounted for 58.64% of 2024 revenue in the Middle East and Africa industrial automation market. Industrial control systems (DCS, PLC, SCADA) underpin the throughput of oil, gas, and petrochemical operations, while motion drives and HMIs enable high-speed packaging lines. Distributed architectures are migrating to Industrial Ethernet, boosting bandwidth for analytics. Within the same umbrella, mobile robots are projected to post the highest 8.29% CAGR through 2030, as e-commerce hubs in Riyadh, Jeddah, and Johannesburg shift to goods-to-person workflows. The Middle East and Africa industrial automation market size for mobile robots could reach a peak by the end of the forecast window if current adoption trends continue. Vendors are bundling fleet-management AI with laser-safe navigation to comply with ISO 3691-4, thereby shrinking deployment times from months to weeks.

Second-tier solutions, such as conveyor/sortation and AS/RS, receive steady orders tied to regional mega-warehouses that supply grocery and pharmaceutical chains. Automatic identification and data capture (AIDC) devices gain traction as logistics operators install RFID portals to comply with customs traceability rules. Meanwhile, the Middle East and Africa industrial automation market experiences a nascent push toward collaborative robots for low-volume, high-mix tasks in apparel and electronics clustering around Casablanca and Port. However, cobot adoption remains limited by end-of-arm tooling costs and safety-certification lead times.

By Component: Hardware Leadership Faces Software Disruption

Hardware still comprised 64.30% of the 2024 spending in the Middle East and Africa industrial automation market, reflecting the need for green-field plants for drives, sensors, and switchgear. Yet software is the fastest-growing line item at 8.84% CAGR, encompassing MES, historians, and AI analytics. Honeywell’s Experion PKS R530 demonstrates how HMI/SCADA packages now incorporate remote gateways and OPC UA over TSN, reducing controller counts by 15% and downtime by 25%.[3]Honeywell, “Experion PKS R530 Release,” automation.honeywell.com Subscription pricing reduces capex, appealing to CFOs in Egypt and Kenya who must balance currency volatility. Cybersecurity services register higher attachment rates as Saudi OTCC regulations mandate IEC 62443 compliance.

Services, ranging from system integration to predictive-maintenance outsourcing, are also scaling. Brown-field retrofits utilize digital twins to map legacy wiring, while multi-year service agreements guarantee uptime in critical desalination and LNG terminals. Edge hardware with containerized runtimes is cannibalizing traditional rack servers, pushing software deeper into the field. As a result, the Middle East and Africa industrial automation market size attributed to recurring revenue is set to double by 2030.

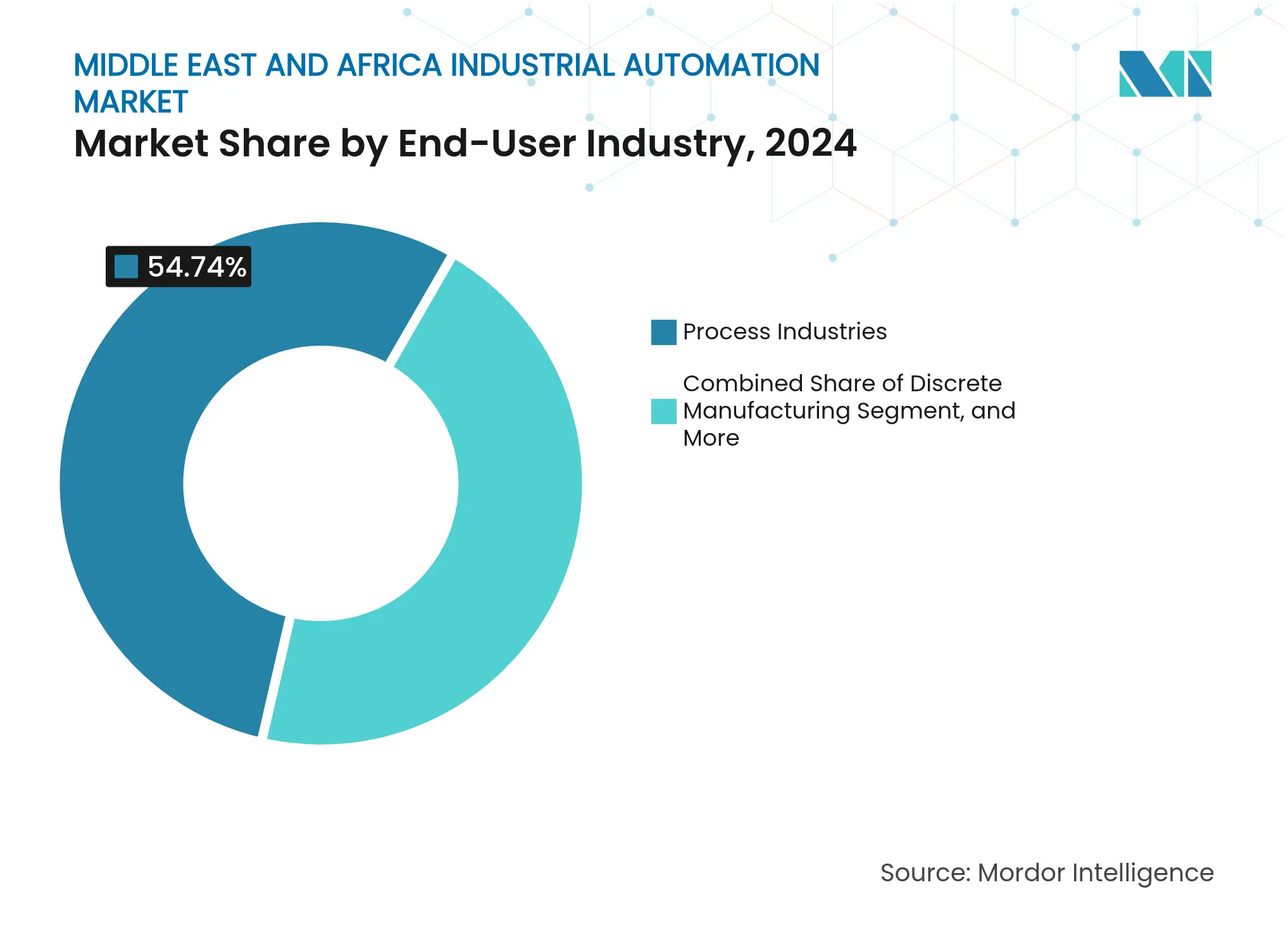

By End-User Industry: Process Industries Segment Leads, Driven by Oil and Gas

The process industries sector captured 54.74% of the 2024 turnover, thanks to megaprojects from ADNOC, Saudi Aramco, and QatarEnergy. Real-time production optimization, flare-reduction mandates, and carbon-intensity reporting drive control-system upgrades, fueling steady orders for wellhead RTUs and vibration analytics. Moreover, the process industries segment shows the quickest 9.02% CAGR, underpinned by same-day delivery promises in Dubai and Riyadh. Automated sorters, AMRs, and AI-driven WMS form the backbone of dark stores operated by retailers of grocery, fashion, and electronics.

Discrete manufacturing, automotive, electronics, and textiles benefit from localization policies. Morocco produced a significant number of vehicles in 2024 and has EV export targets for 2030. Battery gigafactories, such as Gotion’s USD 6.5 billion site, will heavily rely on gigapress robots, AGVs, and MES, thereby expanding the Middle East and Africa industrial automation market. Food and beverage plants install automated inspection to meet halal and export-quality standards, while pharmaceuticals implement track-and-trace lines ahead of regional serialization rules.

Note: Segment shares of all individual segments available upon report purchase

By Technology: Industrial IoT Dominance Challenged by AI Analytics

Industrial IoT accounted for 46.32% of 2024 revenue, as sensors and gateways proliferate across production units. However, AI and analytics are projected to claim the fastest growth at 9.26% CAGR. Qualcomm’s tie-up with Aramco Digital marries 5G private networks to edge AI inference engines, reducing latency in gas-plant safety loops.

As cloud connections remain sporadic in hazardous areas, there's a notable uptick in the adoption of edge computing. Augmented reality is carving a niche, especially in maintenance and operator training. The merging of cyber and physical realms is paving the way for autonomous operations. Honeywell's evolving AI suite is transitioning from advisory roles to achieving closed-loop autonomy, with 91% of enterprises acknowledging enhanced energy security as a key benefit.

The Middle East generated 65.64% of the 2024 revenue for the Middle East and Africa industrial automation market and is expected to retain 8.92% CAGR through 2030. Saudi Arabia’s Public Investment Fund allocated USD 106.6 billion for industrial infrastructure, covering the Oxagon floating hub and King Salman Energy Park.[4]Iconcox, “UAE and KSA: Rising Global Logistics Powerhouses,” iconcox.com The UAE logistics sector benefits from Jebel Ali Port’s automated terminals and the Al Maktoum air-sea corridor. Qatar’s technology blueprint further solidifies the GCC as a global hub for automation.

North Africa records solid pockets of demand. Morocco’s automotive corridor, located along the Tangier-Med Port, integrates robotic welding, AGV body shops, and AI QC cameras. Egypt’s Suez Canal Economic Zone hosts green-hydrogen and petrochemical projects that rely on advanced process control. Nigeria and Algeria present LNG and gas-based fertilizer potential, yet execution risk remains tied to political and currency stability.

Sub-Saharan Africa shows uneven progress. South Africa leads in mining automation, deploying collision-avoidance systems and remote-control loaders. Kenya and Ghana nurture new industrial parks for agro-processing, but power-quality problems hinder high-speed drives. The African Continental Free-Trade Area seeks to raise intra-African trade above 15%, which could unlock scale benefits and stimulate broader automation uptake if implemented smoothly.

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

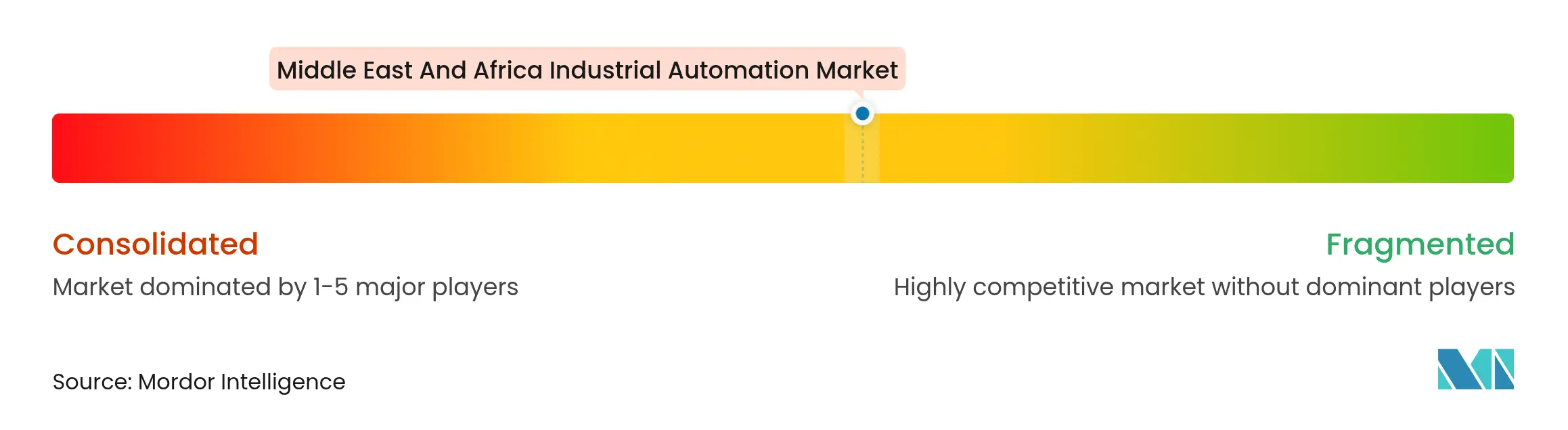

Market Concentration

The Middle East and Africa industrial automation market exhibits moderate fragmentation. Multinationals, ABB, Siemens, Schneider Electric, and Honeywell command premium shares through end-to-end portfolios and regional manufacturing. ABB’s Q2 2025 orders reached USD 9.8 billion, buoyed by process automation wins. Schneider delivered double-digit regional growth by pairing EcoStruxure software with LV switchgear made in Dubai. Honeywell’s pending spin-off will create a pure-play automation firm empowered to chase brown-field autonomy upgrades.

Festo in pneumatics, Yokogawa in DCS, Fortinet in OT security. Local champions such as Saudi Controls and Tectra Automation leverage content rules to secure refinery and water-utility tenders. Start-ups supply AI vision, QA, and AMR fleet software but face scale hurdles. Joint ventures like FFT-KJC-Easun in Saudi Arabia bring German automotive-line know-how under local ownership terms.

Strategic themes include AI/edge convergence, cyber-secure architectures, and lifecycle services. Vendors bundle digital twins with predictive-maintenance SLAs, embedding themselves in customer OPEX budgets. Green-hydrogen complexes represent the next battleground; players able to integrate electrolyzer control, renewable balancing, and ammonia synthesis will gain early mover advantage.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Industrial automation refers to utilizing control systems, including computers or robots, and information technologies to handle different industrial processes and machinery replacing human beings. Industrial automation marks the second step after mechanization in the direction of industrialization.

The Middle East and Africa industrial automation market is segmented by solution type (automated material handling solutions (conveyor/sortation systems, automated storage and retrieval systems (AS/RS), mobile robots (automated guided vehicles and autonomous mobile robots), automatic identification and data capture (AIDC), warehouse management systems (WMS)/warehouse control systems (WCS)), factory automation solutions (industrial control Systems (DCS, PLC, SCADA, HMI, etc.), field devices, industrial robotics, sensors, and transmitters, Motors, and drives) and end-user (automated material handling market (manufacturing, non-manufacturing (warehouses/distribution centers/logistics centers), general merchandise, healthcare, FMCG/non-durable goods), factory automation market, food and beverage, pharmaceuticals, durable manufacturing, textiles).

The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

Unlocking Saudi Arabia’s Regional Tourism Growth Potential

5 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.