Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

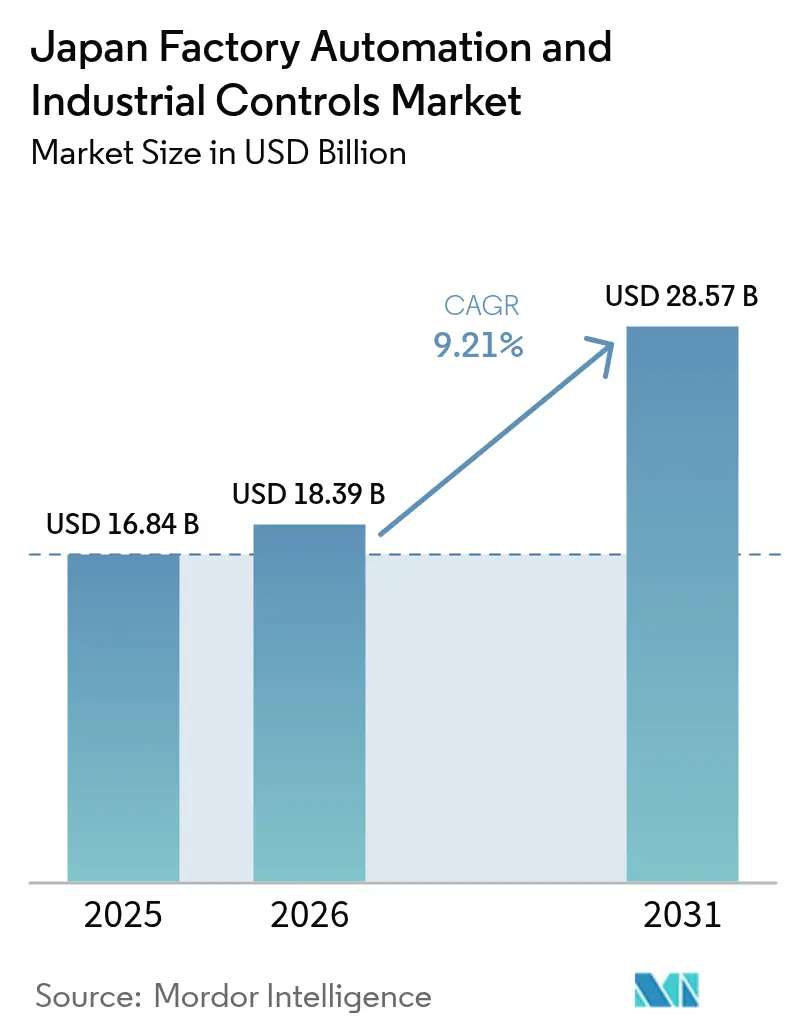

| Base Year Market Size (2025) | USD 16.84 Billion |

| Market Size (2026) | USD 18.39 Billion |

| Market Size (2031) | USD 28.57 Billion |

| Growth Rate (2026 - 2031) | 9.21% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Factory Automation And Industrial Controls Market Analysis by Mordor Intelligence

The Japan factory automation and industrial controls market size was valued at USD 16.84 billion in 2025 and estimated to grow from USD 18.39 billion in 2026 to reach USD 28.57 billion by 2031, at a CAGR of 9.21% during the forecast period (2026-2031). Momentum stems from a shrinking labor pool, aggressive decarbonization rules, and unprecedented fiscal incentives that are compressing payback cycles for next-generation robotics, distributed control systems, and edge-computing platforms. Energy-efficiency benchmarks introduced under the amended Energy Conservation Act, combined with the JPY 150 trillion Green Transformation Fund, are steering budgets toward integrated hardware-plus-software packages that guarantee measurable CO₂ cuts. Manufacturers also face rising wage inflation, cybersecurity requirements tied to OPC UA over TSN deployments, and a renewed urgency to localize semiconductor supply, all of which heighten demand for turnkey consulting and predictive-maintenance services. Competitive intensity is rising as domestic incumbents open their ecosystems while European suppliers differentiate through subscription analytics, tilting revenue models away from transactional hardware toward annuity-based service contracts

Key Report Takeaways

- By component, hardware captured 58.12% of the 2025 revenue in the Japan factory automation and industrial controls market, whereas services are advancing at a 10.41% CAGR through 2031.

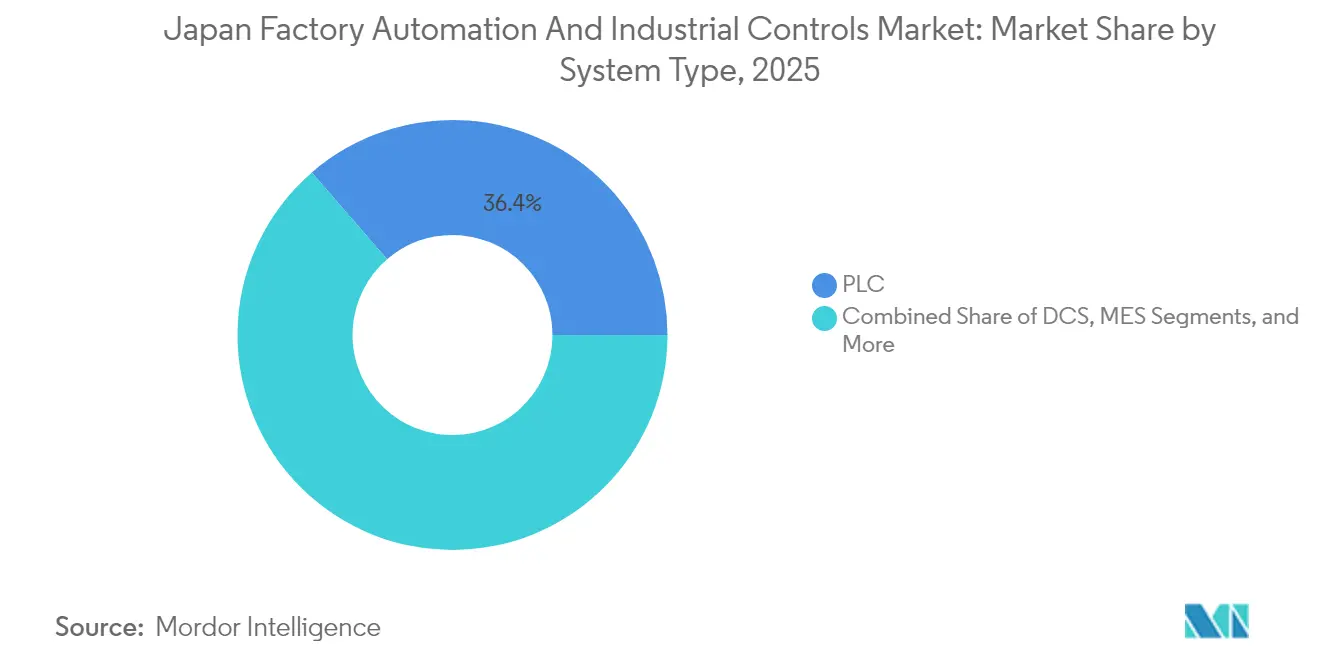

- By system type, PLC solutions accounted for 36.35% of the 2025 revenue in the Japan factory automation and industrial controls market, and the MES segment is expected to accelerate at a 9.95% CAGR.

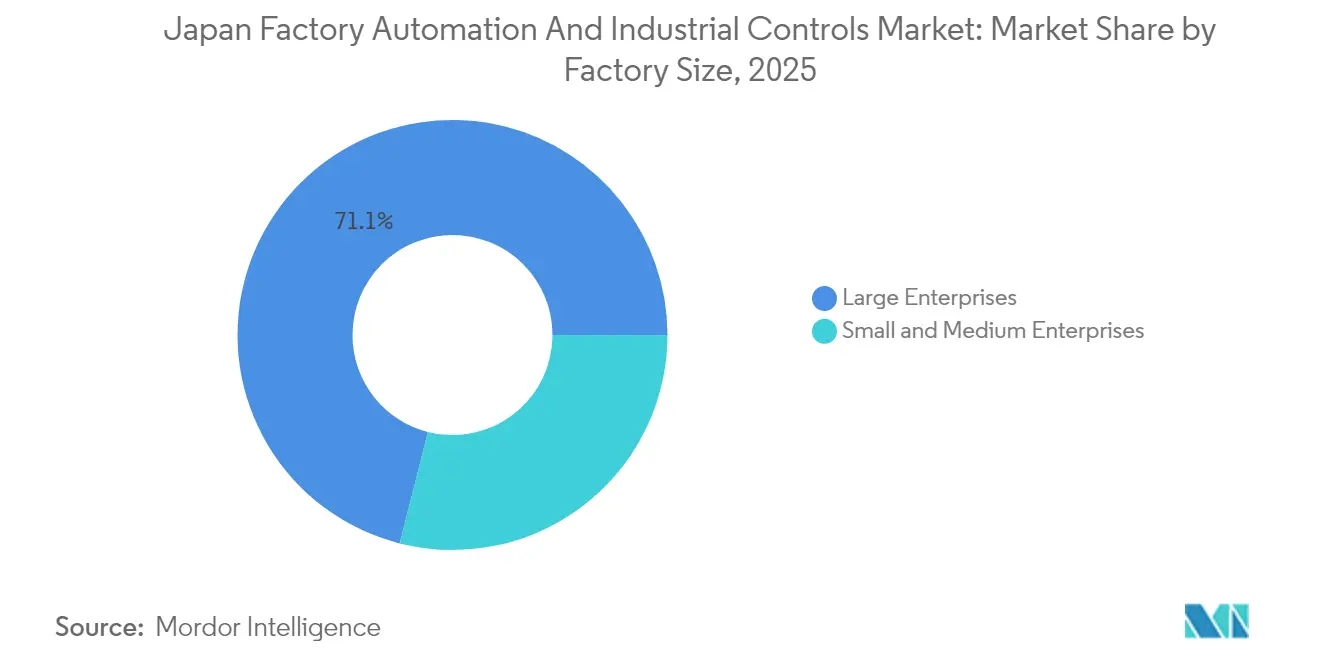

- By factory size, large enterprises secured 71.05% of the 2025 revenue in the Japan factory automation and industrial controls market, while SMEs are expanding at a 10.68% CAGR.

- By end-user industry, automotive and transportation accounted for 30.15% of 2025 demand in the Japan factory automation and industrial controls market; electronics and semiconductor fabrication is forecast to grow at a 9.86% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Japan Factory Automation And Industrial Controls Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Carbon-neutrality mandates and energy-efficiency regulations | +1.8% | National, strongest in Kanto and Chubu industrial belts | Medium term (2–4 years) |

| Aging workforce and acute labor shortages | +2.1% | National, acute in rural manufacturing clusters | Long term (≥4 years) |

| Government's Society 5.0 / Connected Industries program | +1.5% | National, pilot zones in Osaka, Aichi, Kanagawa | Medium term (2–4 years) |

| Robust demand from automotive and electronics verticals | +1.9% | Concentrated in Aichi (automotive), Kumamoto and Hokkaido (semiconductors) | Short term (≤2 years) |

| Green-DX subsidy programme (GX Fund) accelerates automation | +1.6% | National, prioritizing SMEs in designated green-transition sectors | Short term (≤2 years) |

| Rapid piloting of OPC UA over TSN for shop-floor interoperability | +0.9% | Early adopters in automotive and electronics, limited in chemicals | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Carbon-Neutrality Mandates And Energy-Efficiency Regulations

Japan’s 2023 Energy Conservation Act revision obliges factories that consume at least 1,500 kiloliters of crude oil equivalent annually to benchmark energy intensity or face fines, which is channeling budgets into variable-frequency drives, regenerative conveyors, and real-time energy-management suites from Schneider Electric and Siemens.[1]Agency for Natural Resources and Energy, “Energy Conservation Act Amendments,” enecho.meti.go.jp The 2024 amendment broadened the scope to Scope 3 emissions, forcing tier-1 automotive suppliers to audit subcontractor footprints and sparking PLC retrofits across second-tier metal shops in Aichi and Shizuoka. Yokogawa’s OpreX Energy Management suite experienced a 340% increase in domestic installations during fiscal 2024, marking a shift from compliance spending to operational cost arbitrage.[2]Yokogawa Electric Corporation, “OpreX Energy Management,” yokogawa.com

Aging Workforce And Acute Labor Shortages

Japan’s working-age population is expected to shrink by 580,000 in 2024, with projections indicating a 12% decline in manufacturing labor by 2030. Collaborative robots are plugging gaps: Fanuc’s CRX-5iA, launched March 2024, enables fence-free assembly, while Omron’s mobile-robot-plus-vision combo cut changeover time 40% on a Panasonic battery line.[3]Fanuc Corporation, “CRX Collaborative Robot Series,” fanuc.co.jp Rising base wages, up 3.6% in spring 2024 bargaining, have shortened payback on robotics to under 24 months in packaging and logistics, where Yaskawa’s Motoman robots now outnumber humans in 60% of new warehouses.

Government’s Society 5.0 / Connected Industries Program

METI’s Connected Industries framework allocates JPY 100 billion annually to co-fund cyber-physical pilots that integrate IIoT, edge AI, and digital twins across five priority sectors. The 2024 launch of the Ouranos Ecosystem, backed by 47 firms, is standardizing predictive-maintenance data schemas, while Aichi’s Smart Manufacturing Promotion Zone offers 15% automation tax credits in exchange for anonymized production data sharing.

Robust Demand From Automotive And Electronics Verticals

Toyota plans to build 1.5 million battery EVs annually by 2026, necessitating ±0.05 mm placement accuracy only achievable with vision-guided robots. Nissan’s Tochigi plant slashed weld cycle time from 90 seconds to 52 seconds by adding 120 Kawasaki dual-arm robots. On the electronics side, TSMC’s Kumamoto Fab 1 and Rapidus’s Hokkaido project are drawing massive orders for automated material handling and clean-room controls, reinforcing semiconductors as a top-three growth driver into the next decade.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront CAPEX for SMEs | -1.2% | National, acute in rural prefectures with limited access to regional banks | Short term (≤2 years) |

| Semiconductor supply-chain disruptions | -0.9% | National, cascading impact on motor drives, sensors, and PLCs | Medium term (2–4 years) |

| Cyber-security skill gap for OT/IT convergence | -0.7% | National, most severe in SMEs lacking dedicated IT staff | Long term (≥4 years) |

| Conservative culture slowing cloud-native control adoption | -0.5% | Concentrated in traditional process industries (chemicals, steel, paper) | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

High Upfront CAPEX For SMEs

SMEs account for 99.7% of manufacturers yet face debt-service ratios below thresholds required by regional banks, making a JPY 8 million PLC-plus-vision cell equal to 6–9 months of profit. While the Monozukuri subsidy covered 1,240 projects in fiscal 2024, approval rates slipped to 32%, forcing many SMEs to defer plans or seek costly lease options.

Semiconductor Supply-Chain Disruptions

Renesas lead times on RX microcontrollers stretched to 38 weeks in late 2024, cascading into servo-drive shortages that delayed 340 SME projects. Domestic capacity additions at TSMC and Rapidus focus on sub-16 nm nodes, leaving mature 40/65 nm processes underserved until METI’s JPY 450 billion subsidy program lures trailing-edge foundries.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By System Type: Software-Defined Control Architectures Gain Traction

PLC solutions captured a 36.35% share of the Japan factory automation and industrial controls market in 2025 and MES is projected to accelerate at a 9.95% CAGR through 2031. Distributed control systems dominate process industries, where Yokogawa holds a 42% domestic share, while Mitsubishi Electric and Omron together control 60% of discrete PLC deployments.

The shift to soft PLCs and cloud historians is expanding the Japan factory automation and industrial controls market size for virtualized edge servers and digital twin platforms. Supervisory control and data acquisition platforms are moving into factories to satisfy real-time carbon reporting, and MES-PLM convergence is rising fastest in battery and semiconductor lines.

By Component: Services Surge As Integration Complexity Escalates

Hardware accounted for 58.12% of 2025 revenue; however, services revenue is growing at a rate of 10.41% per year, the fastest of any component segment. Robotics and machine vision shipped 26% more units in 2024, but OPC UA TSN rollouts, cloud historians, and predictive maintenance workloads are pushing integrators to the forefront.

This pivot is expanding the Japan factory automation and industrial controls market size for annual service contracts that bundle edge AI and cybersecurity monitoring. Hardware duopolies in drives and motors maintain pricing power, yet component-only suppliers risk margin erosion as buyers favor integrated energy-management packages.

By Factory Size: SMEs Narrow The Automation Gap

Large enterprises held 71.05% of 2025 revenue, leveraging multi-site scale and in-house engineering teams, but SMEs are advancing 10.68% annually, the fastest across all cuts. The GX Fund’s 50% subsidy, low-cost collaborative robots under ¥3 million, and plug-and-play programming tools are lowering the threshold for first-time adopters.

These dynamics widen the Japan factory automation and industrial controls market size for modular, redeployable automation cells. Regional gaps persist; Aichi and Shizuoka SMEs deploy robots at 2.5 times the national average, whereas Shimane and Tottori lag due to scarce integrator capacity and longer lead times.

By End-User Industry: Electronics And Semiconductor Fabrication Accelerate

Automotive remained the largest buyer, accounting for 30.15% of 2025 demand, while electronics and semiconductor fabrication posted the fastest growth at a 9.86% CAGR. EV battery lines require micron-level accuracy, driving the uptake of six-axis robots, while wafer fabs order clean-room AMHS and inspection platforms valued at JPY 120 billion through 2027.

These trends are expected to lift the Japan factory automation and industrial controls market share of high-precision robotics, vision systems, and environmental controls. Process-industry retrofits, tied to the High-Pressure Gas Safety Act, add a steady replacement market, although metals and mining remain sluggish outside of AI-assisted blast-furnace pilots.

Geography Analysis

Kanto and Chubu industrial belts accounted for 61.40% of 2025 installations, reflecting dense automotive and electronics clusters surrounding Tokyo and Nagoya. Aichi hosts 4,800 supplier plants that collectively deployed 18,200 robots in 2024, aided by a 15% automation tax credit for participants in the Smart Manufacturing Promotion Zone.

Kumamoto and Hokkaido are emerging semiconductor nodes. TSMC’s JPY 1.2 trillion Kumamoto Fab 1 catalyzed local service centers from Tokyo Electron and Ebara, while Rapidus’s 2 nm project convinced Siemens and ABB to open regional engineering hubs, rebalancing an historically Tokyo-centric support network. Kansai, with Panasonic battery plants and Sharp display fabs, captured 18.25% of 2025 revenue and is retrofitting lines to hit corporate carbon-neutral targets.

Rural Tohoku and Chugoku regions, together 12.10% of 2025 sales, struggle with aging demographics and limited integrator presence, but METI’s JPY 12 billion Regional Revitalization program raised SME automation adoption by 6 points in selected municipalities. Kyushu, at 8.25% of 2025 revenue, benefits from fab construction and EV battery contracts, such as Toyota’s Miyata plant, which installed 140 Fanuc robots in 2024 under a GX-Fund-subsidized project.

Competitive Landscape

The top five domestic suppliers, Mitsubishi Electric, Omron, Fanuc, Yokogawa Electric, Keyence, held a combined 48% share in 2024, leaving ample room for multi-vendor procurement strategies. Siemens, ABB, and Schneider Electric are capturing SME mindshare by bundling SaaS analytics with hardware, Siemens grew Japan revenue 19% in fiscal 2024 via MindSphere subscriptions.

Open ecosystems define current strategy. Mitsubishi Electric’s e-Factory alliance reached 4,200 partner products by mid-2024, and its digital-twin patent filing underscores a shift toward platform monetization. Fanuc is doubling collaborative-robot capacity, while Yokogawa secured governance of OPC UA guidelines through its IVI stake, positioning Synaptic Business Automation as a de facto standard for data models.

White-space opportunities include FOUNDATION Fieldbus cybersecurity retrofits worth JPY 180 billion, predictive maintenance for rotating equipment where Hitachi Lumada competes with NEC Industrial IoT, and energy-management SaaS for SMEs where Schneider and Siemens undercut legacy SCADA vendors by 30% on TCO. Preferred Networks’ deep-learning bin-picking algorithm, capitalized at JPY 20 billion in 2024 funding, exemplifies rising AI-native challengers

Japan Factory Automation And Industrial Controls Industry Leaders

Rockwell Automation

ABB Ltd

Emerson Electric

Honeywell Intenational Inc

Schneider Electric

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Fanuc Corporation announced a ¥50 billion expansion of its Tsukuba robotics plant.

- February 2025: Mitsubishi Electric Corporation and Nvidia Corporation signed a joint-development pact to embed Omniverse into the e-F@ctory digital-twin suite.

- January 2025: Yokogawa Electric Corporation acquired a 51% stake in Industrial Value Chain Initiative (IVI) for JPY 3.2 billion.

Japan Factory Automation And Industrial Controls Market Report Scope

The Japan factory automation and industrial controls market report is segmented by System Type (Distributed Control System (DCS), Programmable Logic Controller (PLC), Supervisory Control and Data Acquisition (SCADA), Product Lifecycle Management (PLM) Software, Manufacturing Execution System (MES), Human-Machine Interface (HMI), Other System Types), Component (Hardware, Software; Services), Factory Size (Small and Medium Enterprises, Large Enterprises), and End-user Industry (Chemical and Petrochemical, Power and Utilities, Food and Beverage, Automotive and Transportation, Electronics and Semiconductor, Pharmaceuticals, Metals and Mining, Other End-user Industries). Market Forecasts are Provided in Terms of Value (USD).

By System Type

| Distributed Control System (DCS) |

| Programmable Logic Controller (PLC) |

| Supervisory Control and Data Acquisition (SCADA) |

| Product Lifecycle Management (PLM) Software |

| Manufacturing Execution System (MES) |

| Human-Machine Interface (HMI) |

| Other System Types |

By Component

| Hardware | Machine Vision |

| Industrial Robotics | |

| Sensors and Transmitters | |

| Motors and Drives | |

| Safety Systems | |

| Other Hardwares | |

| Software | |

| Services (Integration, Consulting, Maintenance) |

By Factory Size

| Small and Medium Enterprises |

| Large Enterprises |

By End-user Industry

| Oil and Gas |

| Chemical and Petrochemical |

| Power and Utilities |

| Food and Beverage |

| Automotive and Transportation |

| Electronics and Semiconductor |

| Pharmaceuticals |

| Metals and Mining |

| Other End-user Industries |

| By System Type | Distributed Control System (DCS) | |

| Programmable Logic Controller (PLC) | ||

| Supervisory Control and Data Acquisition (SCADA) | ||

| Product Lifecycle Management (PLM) Software | ||

| Manufacturing Execution System (MES) | ||

| Human-Machine Interface (HMI) | ||

| Other System Types | ||

| By Component | Hardware | Machine Vision |

| Industrial Robotics | ||

| Sensors and Transmitters | ||

| Motors and Drives | ||

| Safety Systems | ||

| Other Hardwares | ||

| Software | ||

| Services (Integration, Consulting, Maintenance) | ||

| By Factory Size | Small and Medium Enterprises | |

| Large Enterprises | ||

| By End-user Industry | Oil and Gas | |

| Chemical and Petrochemical | ||

| Power and Utilities | ||

| Food and Beverage | ||

| Automotive and Transportation | ||

| Electronics and Semiconductor | ||

| Pharmaceuticals | ||

| Metals and Mining | ||

| Other End-user Industries | ||

Key Questions Answered in the Report

How large is the Japan factory automation and industrial controls market in 2026?

It stands at USD 18.39 billion and is on track to hit USD 28.57 billion by 2031 at a 9.21% CAGR.

Which segment is expanding fastest inside Japanese factories?

Integration, consulting, and predictive-maintenance services are growing 10.41% annually, outpacing hardware demand.

Why are SMEs now adopting automation more quickly?

GX-Fund subsidies, plug-and-play collaborative robots priced below ¥3 million, and easier lease financing have shortened payback periods for smaller firms.

What role does the semiconductor boom play in future demand?

New fabs in Kumamoto and Hokkaido require automated material handling and clean-room controls, making electronics the fastest-growing end-user segment at a 9.86% CAGR.

Which technology standard is key for interoperability?

OPC UA over TSN, ratified as IEC/IEEE 60802, delivers deterministic networking that supports cloud-native control loops across mixed-vendor equipment.

Page last updated on: