North America Feed Flavors and Sweeteners Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

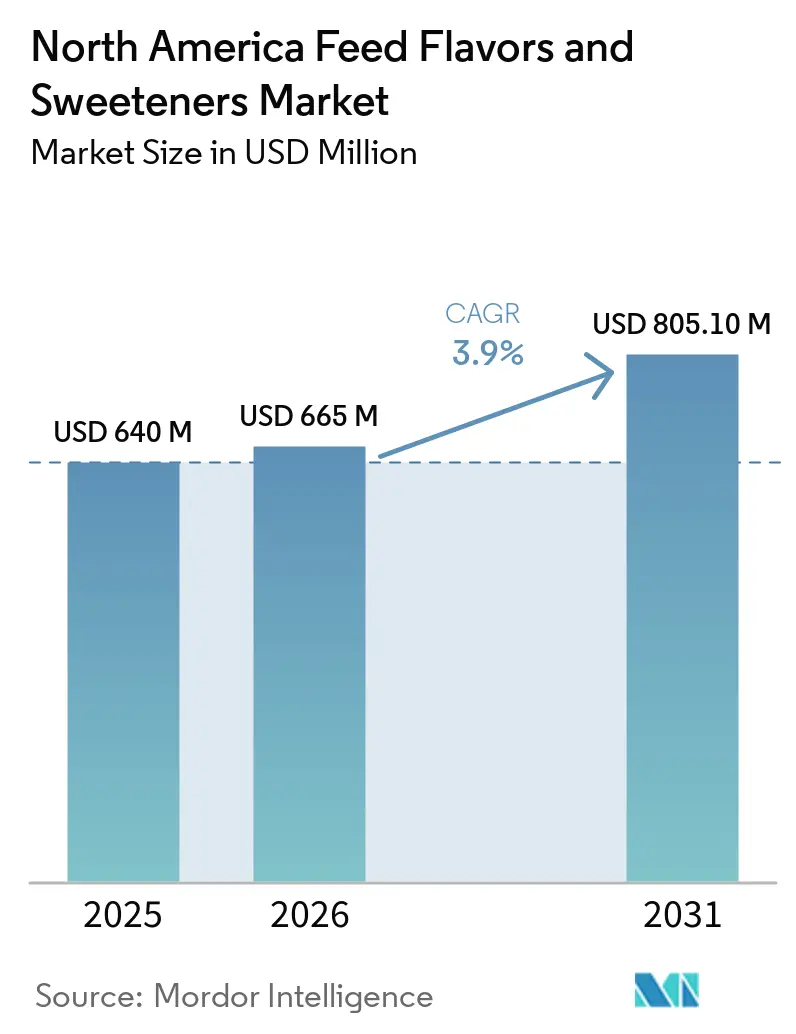

| Base Year Market Size (2025) | USD 640 Million |

| Market Size (2026) | USD 665 Million |

| Market Size (2031) | USD 805.10 Million |

| Growth Rate (2026 - 2031) | 3.90% CAGR |

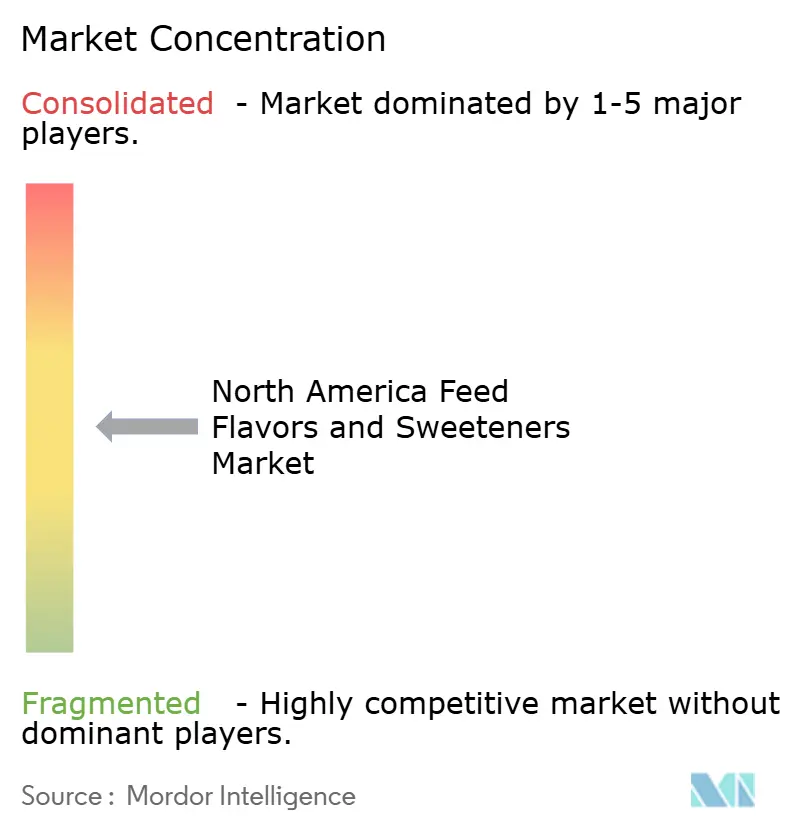

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Feed Flavors and Sweeteners Market Analysis by Mordor Intelligence

The North America feed flavors and sweeteners market was valued at USD 640 million in 2025, projected to be USD 665 million by 2026, and is estimated to reach USD 805.1 million by the end of the forecast period, growing at a CAGR of 3.9% from 2026 to 2031. The market's growth is driven by the shift in livestock production toward fewer, larger operating units that purchase additives in bulk and require consistent intake support across extensive feed programs. In 2025, the United States accounted for 65.5% of regional consumption, while Mexico is anticipated to experience the fastest growth through 2031 as its compound feed industry becomes increasingly commercialized. The market is also benefiting from advancements in precision feeding tools, which facilitate the monitoring of intake changes. These tools enable suppliers to position palatability additives as measurable performance inputs rather than discretionary expenses. Additionally, the growing use of methane-reduction ingredients and alternative proteins in animal diets has increased demand for masking systems to address bitter or unfamiliar sensory profiles introduced by these new feed inputs. Competition in the North America feed flavors and sweeteners market remains moderate. The joint venture between ADM and Alltech, announced in February 2026, is anticipated to enhance supply-side scale while still providing opportunities for specialist and mid-tier suppliers to compete effectively.

Key Report Takeaways

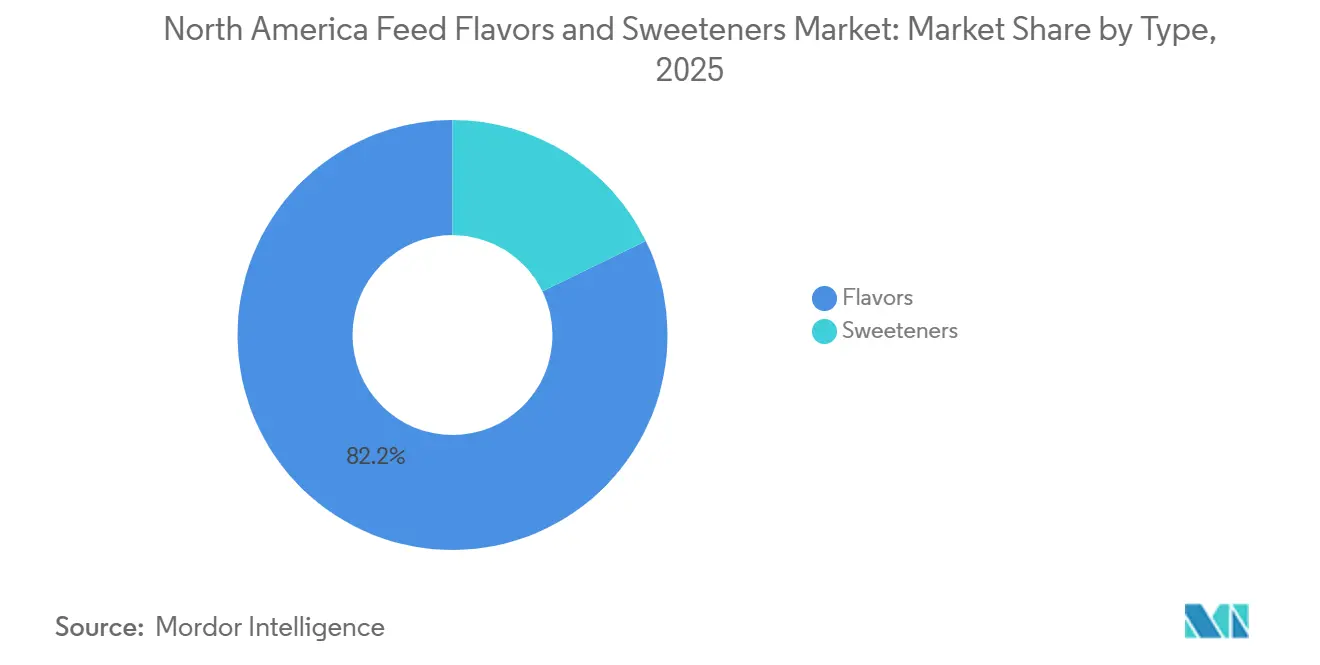

- By type, flavors accounted for 82.2% of the North America feed flavors and sweeteners market size in 2025, while sweeteners are projected to expand at a 5.8% CAGR through 2031.

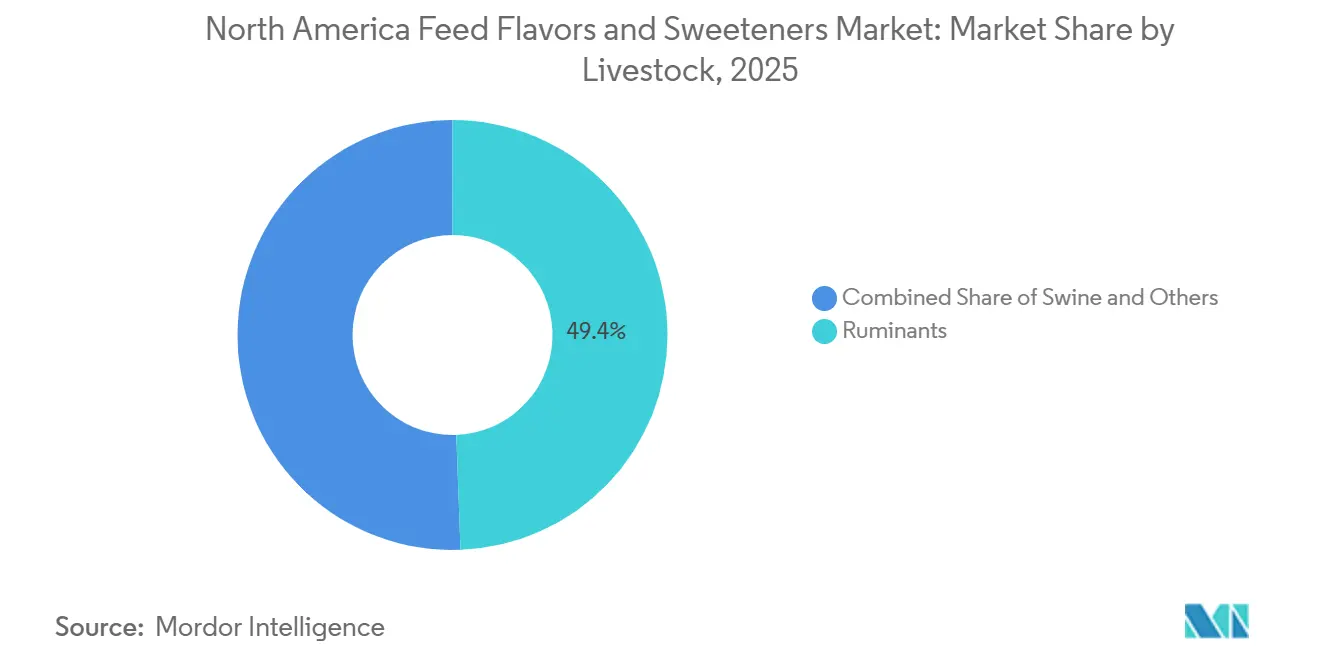

- By livestock, ruminants held 49.4% of North America feed flavors and sweeteners market share in 2025, while swine is forecast to grow at a 6.2% CAGR through 2031.

- By country, the United States accounted for 65.5% of revenue in 2025, while Mexico is projected to record the fastest growth at a 4.6% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Feed Flavors and Sweeteners Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher compound feed throughput and feed mill scale | +0.9% | United States, Canada, and Mexico | Medium term (2-4 years) |

| Antibiotic reduction programs increasing demand for intake support additives | +0.8% | United States, Canada, and Mexico | Short term (≤ 2 years) |

| Premium meat, and dairy requirements lifting palatability standards | +0.8% | United States, Canada, and Mexico | Medium term (2-4 years) |

| Clean-label and natural additive adoption in premium feed | +0.7% | United States, Canada, and Mexico | Medium term (2-4 years) |

| Precision feeding and AI-based intake monitoring improving palatability ROI visibility | +0.5% | United States, Canada, and Mexico | Long term (≥ 4 years) |

| Taste-masking demand from alternative proteins, by-products, and methane-reduction rations | +0.5% | United States, Canada, and Mexico | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Higher Compound Feed Throughput and Feed Mill Scale

Industrial feed output continues to drive the North American feed flavors and sweeteners market toward a wider, more stable demand base. According to the Alltech Feed Survey, Mexico’s compound feed output increased by 2% from 2024 to 2025 and had expanded by 7.7% since 2020, indicating that the country is adding real volume to swine feed manufacturing. Additionally, Canada also provides a solid base through 429 commercial feed mills that process 28.9 million metric tons annually, and that scale supports organized additive procurement at the mill level[1]Source: Alltech, “2026 Agri-Food Outlook,” alltech.com. As more feed moves through commercial systems rather than on-farm mixing, purchasing decisions become more centralized and more technical. That favors suppliers that can offer stable delivery forms, application support, and consistent supply across multiple species. It also makes established programs harder to replace once a product is built into mill specifications and performance records. This operating structure continues to support growth in the North America feed flavors and sweeteners market because commercial mills buy at scale and seek additives that fit standardized feed production.

Antibiotic-Reduction Programs Increasing Demand for Intake-Support Additives

Antibiotic reduction programs are enhancing the functional role of flavors and sweeteners in commercial feed. With the reduction of antibiotic growth promoters, producers increasingly rely on improved feed acceptance in early-life diets to maintain intake and daily weight gain. This is particularly critical in nursery swine and young ruminant programs, where reduced appetite can quickly impact performance and health outcomes. Flavors and sweeteners are now viewed as essential tools for supporting feed intake rather than optional enhancements. Additionally, large-scale swine studies have demonstrated that plant-based additive systems can reduce antibiotic dependence while maintaining pig performance, further emphasizing the importance of palatability support. As a result, antibiotic stewardship has become a key driver for the North America feed flavors and sweeteners market.

Premium Meat, and Dairy Requirements Lifting Palatability Standards

Increasing product standards in meat and dairy are driving higher expectations for feed acceptance across North America. Producers catering to premium markets exhibit lower tolerance for inconsistent feed intake, as it can negatively impact carcass quality, milk composition, feeding behavior, and overall product consistency. In dairy systems, advancements such as robotic milking and digital herd monitoring have made feed response more observable, highlighting issues such as poor palatability in daily operations. As a result, premiumization remains a significant growth driver in the North America feed flavors and sweeteners market, as improved feed acceptance enhances performance across both livestock and companion animal segments.

Clean-Label and Natural Additive Adoption in Premium Feed

Clean-label preferences are increasingly influencing feed and ingredient specifications, extending beyond finished products. Premium livestock supply chains are prioritizing ingredient systems that are simpler to communicate to buyers and consumers. Natural ingredients dominate the North America feed flavors and sweeteners market, indicating a significant shift in regional demand. Suppliers are developing saccharin-free systems that incorporate stevia, thaumatin, and related compounds to meet the demand for more label-friendly solutions. This trend is particularly impactful in high-value livestock programs but is also beginning to influence broader additive sourcing decisions. The growing preference for natural ingredient portfolios supports value growth in the North America feed flavors and sweeteners market, as these portfolios can command higher pricing in applications where ingredient transparency is important.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lengthy regulatory review and ingredient approval pathways | -0.6% | United States and Canada | Medium term (2-4 years) |

| Cost inflation and ROI scrutiny among feed formulators and integrators | -0.5% | United States, Mexico, and Canada | Short term (≤ 2 years) |

| Ingredient transition uncertainty under evolving FDA and AAFCO frameworks | -0.4% | United States, Mexico, and Canada | Medium term (2-4 years) |

| Citrus and molasses input volatility affecting flavor and sweetener economics | -0.3% | United States, Mexico, and Canada | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Lengthy Regulatory Review and Ingredient Approval Pathways

Regulatory review continues to be a significant constraint on the pace at which new products can scale in the North America feed flavors and sweeteners market. Novel flavor actives and high-intensity sweeteners for animal use often face extended approval processes under 21 CFR Part 573 and related ingredient-definition procedures. Smaller companies are disproportionately affected, as regulatory compliance can consume a substantial portion of their available investment before commercial launch. This dynamic tends to favor larger companies with greater financial resources and dedicated regulatory teams. Additionally, it delays the introduction of newer masking and sweetening systems compared to similar advancements in human food. This remains a notable limitation, as the North America feed flavors and sweeteners market relies on approved ingredients, and prolonged review timelines hinder portfolio innovation.

Cost Inflation and ROI (Return on Investment) Scrutiny Among Feed Formulators and Integrators

Cost pressures continue to influence purchasing decisions in feed manufacturing and livestock integration. Elevated costs for freight, raw materials, and animal production are driving buyers to evaluate whether premium additives can deliver measurable performance improvements within a short production cycle. As a result, flavor and sweetener products experience delays in adoption or reduced inclusion rates as their economic benefits are not clearly demonstrated. AFB International has observed that palatability response does not increase proportionally with higher inclusion rates, highlighting the importance of customer education alongside product performance. This trend often benefits larger suppliers capable of integrating palatability systems into comprehensive nutritional programs and service offerings. Conversely, smaller specialists, despite having effective products, may face challenges when procurement teams prioritize immediate cost control. Consequently, Return on Investment (ROI) scrutiny remains a significant constraint on the North America feed flavors and sweeteners market, particularly in cost-sensitive livestock segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Flavors Remain Dominant While Sweeteners Grow Faster

Flavors accounted for 82.2% of the North American feed flavors and sweeteners market in 2025, maintaining a dominant position. This significant share reflects their routine use across ruminant and swine feeds, where they are essential for masking undesirable odors and ensuring consistent feed intake. Flavors are an integral part of commercial feed formulations, with their demand driven by regular inclusion rather than occasional specialty use. This consistent utilization positions flavors as a core component of both standard compound feed and premium formulations in the North American feed flavors and sweeteners market.

Sweeteners are projected to grow at a CAGR of 5.8% from 2026 to 2031, outpacing flavors. This accelerated growth is attributed to their role in sensitive diets where stimulating feed intake is critical, particularly in early-life feeding, transition diets, and formulations containing bitter-tasting bioactives. Sweeteners are also gaining importance in dairy rations that incorporate methane-reduction ingredients and in nursery swine diets, where feed acceptance directly impacts performance[2]Source: Frontiers in Veterinary Science, “Bioactive Feed Additives in Animal Nutrition Bridging Innovation, Health, and Sustainability,” frontiersin.org. Consequently, while flavors remain the largest segment, sweeteners are emerging as the primary growth driver in the North American feed flavors and sweeteners market.

By Livestock: Ruminants Lead Revenue While Swine Expands Faster

Ruminants accounted for 49.4% of the North America feed flavors and sweeteners market share in 2025, making them the largest livestock segment. This dominance is attributed to the extensive dairy and beef cattle feeding systems in the United States and Canada, where consistent feed intake is critical at a commercial scale. Palatability additives play a significant role in ruminant feed, as ration acceptance impacts milk yield, feed efficiency, and adaptation to dietary changes. This widespread and stable application positions ruminants at the core of the North America feed flavors and sweeteners market.

Swine is projected to grow at a CAGR of 6.2% through 2031, making it the fastest-growing segment. This growth is driven by the increasing importance of starter feed performance and heightened sensitivity to feed refusal among young piglets, both of which influence the growth of the swine population. While other animals currently represent a smaller base than established terrestrial livestock categories, they offer a stronger growth trajectory for targeted flavor and sweetener applications. The North American feed flavors and sweeteners market is projected to maintain a steady, ruminant-led revenue structure while capitalizing on rapid growth opportunities in swine during the forecast period.

Geography Analysis

The United States accounted for 65.50% of the North America feed flavors and sweeteners market in 2025, maintaining its position as the largest country market in the region. This leading position is supported by the scale of commercial livestock production, a large compound feed base, and extensive pet food manufacturing capacity. Additionally, the country exhibits the highest adoption of specialty feed additives across swine, ruminants, and other animals. These factors position the United States as the core demand center for the North American feed flavors and sweeteners market.

Canada represents a stable regional market, supported by its organized feed manufacturing base and steady livestock production systems. According to Alltech, the country processes 28.9 million metric tons of animal feed annually through 429 mills, ensuring consistent additive demand at the mill level. Canadian demand is further driven by the dairy and swine industry, where formulation quality and feed acceptance are critical. As a result, Canada remains significant as both a consumption market and a technology base in the North America feed flavors and sweeteners market

Mexico is projected to grow at the fastest rate in the region, with a 4.6% CAGR from 2026 to 2031. This growth is attributed to the ongoing modernization of the compound feed sector and increased integration in ruminant and swine production. As feed manufacturing becomes more commercialized, the use of specialty additives is shifting from basic nutrition to performance-driven applications. Mexico is also gaining importance for suppliers establishing local and regional production facilities. This regional structure highlights the United States as the largest market, Canada as a stable developed market, and Mexico as the fastest-growing opportunity in the North America feed flavors and sweeteners market.

Competitive Landscape

The North America feed flavors and sweeteners market is moderately fragmented, with key players including Cargill Incorporated, ADM, Kemin Industries Inc., Alltech, and Adisseo. While the market structure provides large suppliers with a competitive advantage, it still allows smaller, specialized companies to compete effectively by offering targeted product lines and expertise in livestock applications. Competition is particularly intense in areas where suppliers can demonstrate species-specific performance, reliable delivery formats, and direct support for feed mill customers. As a result, the market remains accessible to focused suppliers, even though the top-tier companies control a significant share of the revenue.

ADM has bolstered its position in the sweeteners segment with its SUCRAM range, which includes saccharin-free systems such as Sucram M’I Sweet and Sucram Specifeek. These products gained attention for their application in swine feed following their showcase at EuroTier 2024. Similarly, in 2024, Norel S.A. introduced saccharin-free feed sweetener options, including DULCOAPETENTE NT-75 and DULCOAPETENTE NEO[3]Source: Norel S.A., “Sweetener Solution from Norel, Saccharin-Free,” Norel S.A., norel.net. Adisseo has also demonstrated strong growth, reporting a 12% increase in its palatability business during the first half of 2025 and a 24% growth in the same segment in Q1 2025. This growth has been driven by its focus on North American ruminant and swine channels. These developments highlight the market's evolution, driven by reformulation, technical specialization, and enhanced species-specific product positioning.

Strategic collaborations and initiatives are influencing the competitive landscape of the North America feed flavors and sweeteners market. The joint venture between ADM and Alltech, which formed Akralos Animal Nutrition, integrated Hubbard Feeds, Masterfeeds, and ADM’s feed operations in North America. This consolidation has redefined the regional feed platform, supporting future additive commercialization. Kemin Industries Inc. continues to play a significant role in the market, leveraging product approval activities and formulation support to maintain its relevance in technically demanding feed applications. Despite the competitive nature of the market, opportunities remain in areas such as cleaner-label sweetener systems, liquid palatability products, and data-driven additive programs tailored for large cattle operations. These gaps indicate that while the market is competitive, it has not yet reached saturation with equally specialized suppliers.

North America Feed Flavors and Sweeteners Industry Leaders

ADM

Kemin Industries Inc.

Alltech

Adisseo

Cargill, Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: ADM and Alltech have officially launched Akralos Animal Nutrition, a North American joint venture in animal feed. This collaboration integrates Alltech's Hubbard Feeds (US) and Masterfeeds (Canada) with ADM's feed operations in the United States. The resulting entity establishes a vertically integrated feed manufacturing and specialty nutrition network. It also gains direct access to palatability solutions through Pancosma's sweetening platform and Alltech's young-animal flavoring programs, making it a significant development in the livestock feed flavors and sweeteners market in North America.

- April 2025: Adisseo's palatability business delivered 12% growth in H1 2025 and 24% growth in its palatability segment in Q1 2025, driven by strong volume gains across North American ruminant and swine channels, where Maxarome, Optisweet, and Krave AP palatability platforms sustained commercial momentum in antibiotic-reduction and precision feeding programs, including feed flavors and sweeteners.

- November 2024: ADM introduced 2 new saccharin-free in-feed sweeteners at EuroTier 2024 in Hanover: Sucram M'I Sweet, the first animal nutrition product incorporating monk fruit juice, and Sucram Specifeek, developed in collaboration with the University of Liverpool based on swine sweet-taste receptor research. These products offer North American swine producers species-specific, natural alternatives to sodium saccharin for weaner and nursery diets.

North America Feed Flavors and Sweeteners Market Report Scope

Feed flavors and sweeteners are additives intentionally incorporated into animal diets to enhance aroma, mask unpleasant tastes, and improve overall palatability. The North America feed flavors and sweeteners market report is segmented by type (flavors and sweeteners), by livestock (swine, ruminants, and others), and by country (United States, Canada, Mexico, and Rest of North America). The market forecasts are provided in terms of value (USD) and volume (metric tons).

| Flavors |

| Sweeteners |

| Swine | |

| Ruminants | Dairy Cattle |

| Beef Cattle | |

| Others | |

| Others |

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Type | Flavors | |

| Sweeteners | ||

| By Animal | Swine | |

| Ruminants | Dairy Cattle | |

| Beef Cattle | ||

| Others | ||

| Others | ||

| By Country | United States | |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

Key Questions Answered in the Report

What is the outlook for the North America feed flavors and sweeteners market through 2031?

The market is projected to rise from USD 640 million in 2025 to USD 805.1 million by 2031 at a 3.9% CAGR.

Which type segment leads the North America feed flavors and sweeteners market?

Flavors led the market with an 82.2% share in 2025, reflecting their broad use across routine livestock feed formulations.

Which type segment is growing faster in North America feed flavors and sweeteners?

Sweeteners are projected to grow faster at a 5.8% CAGR through 2031, supported by early-life diets and harder-to-mask feed formulations.

Which livestock category contributes the most revenue?

Ruminants led with 49.4% of revenue in 2025 because dairy and beef systems in the United States and Canada consume very large feed volumes.

Which country offers the strongest growth opportunity in the region?

Mexico is estimated to grow the fastest at a 4.6% CAGR through 2031 as commercial feed production continues to expand and modernize.

Page last updated on: