Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2025 - 2031 |

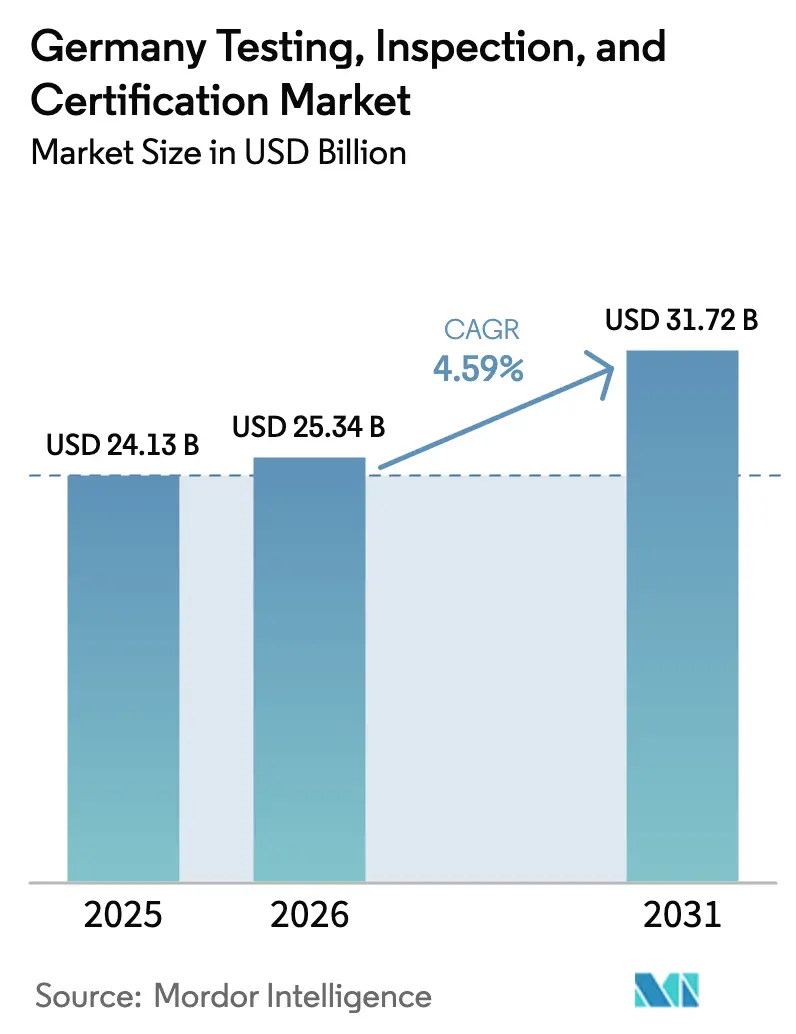

| Base Year Market Size (2025) | USD 24.13 Billion |

| Market Size (2026) | USD 25.34 Billion |

| Market Size (2031) | USD 31.72 Billion |

| Growth Rate (2025 - 2030) | 4.59% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Testing, Inspection, And Certification Market Analysis by Mordor Intelligence

The Germany testing, inspection, and certification market size is expected to increase from USD 24.13 billion in 2025 to USD 25.34 billion in 2026 and reach USD 31.72 billion by 2031, growing at a CAGR of 4.59% over 2026-2031. Rapid electrification across automotive and industrial equipment, digital-twin deployment in asset management, and tighter circular-economy reporting rules are reshaping the quality-assurance landscape. Testing retained scale advantages in 2025, but certification is expanding faster as the European Union adds new categories that must secure third-party attestations. Outsourced services are gaining ground because small and medium enterprises face the dual challenge of capital-intensive laboratories and a shortage of accredited personnel. Providers also pivot toward remote inspection platforms that blend drones, edge analytics, and secure data hubs to cut downtime and achieve continuous compliance monitoring. Competitive intensity remains moderate, with national champions relying on software-as-a-service extensions and targeted mergers to defend share against niche specialists.

Key Report Takeaways

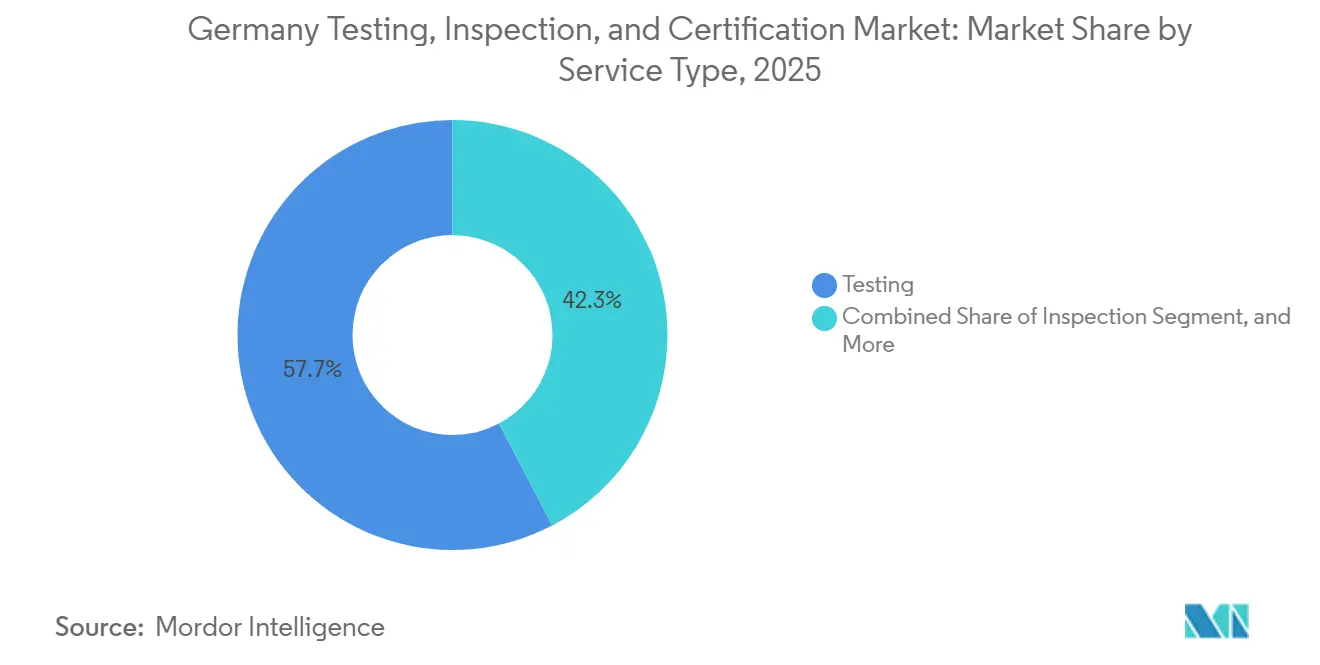

- By service type, testing led with 57.68% revenue share in 2025, while certification is projected to record a 5.03% CAGR through 2031.

- By sourcing type, in-house operations held 60.47% of the Germany testing, inspection, and certification market share in 2025, yet outsourced services are forecast to expand at a 5.12% CAGR to 2031.

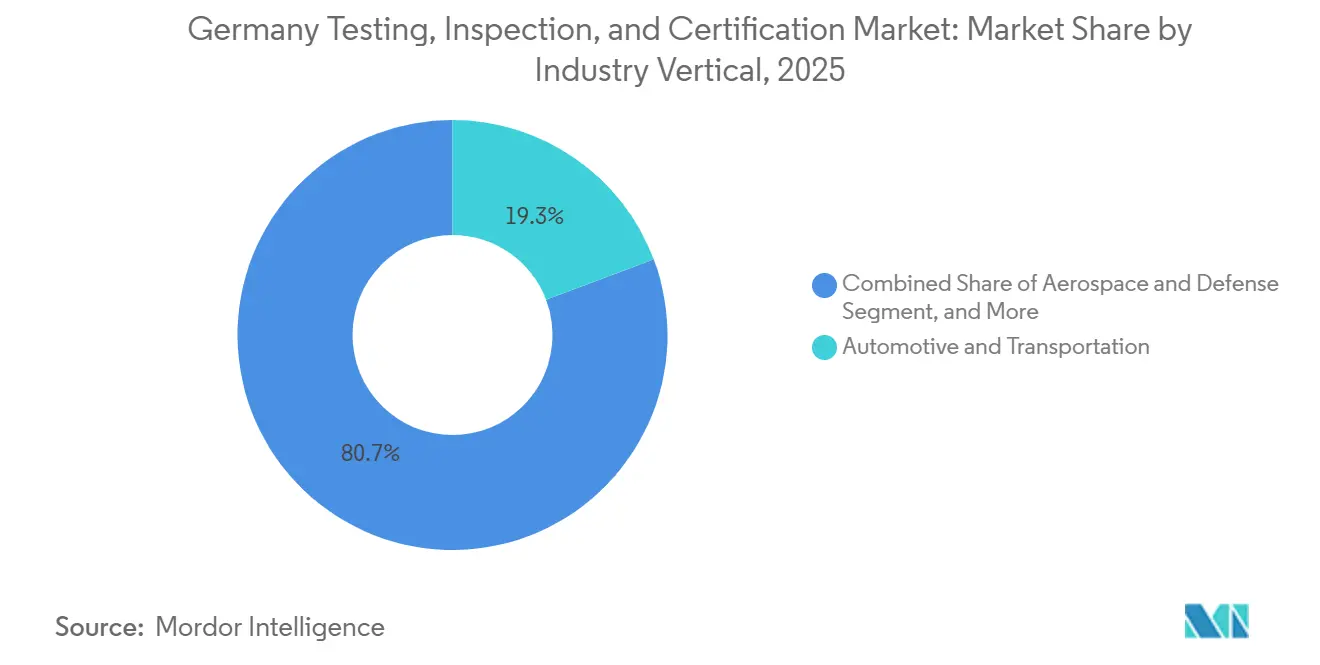

- By industry vertical, automotive and transportation commanded 19.26% of the Germany, testing inspection, and certification market size in 2025, whereas life sciences and healthcare is set to grow at a 5.76% CAGR through 2031.

- By mode of service delivery, on-site work retained 52.43% share in 2025, while remote and digital inspection is expected to advance at a 6.07% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany Testing, Inspection, And Certification Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Electric Vehicle Adoption and Battery Gigafactories | +1.2% | National, concentration in Brandenburg and Saxony | Medium term (2-4 years) |

| Stricter EU Regulatory Enforcement in Safety Critical Industries | +1.0% | National, aligned with EU directives | Long term (≥ 4 years) |

| Rising Complexity of Industry 4.0 and IoT Enabled Supply Chains | +0.9% | National, strongest in Baden Württemberg and Bavaria | Medium term (2-4 years) |

| Growing Demand for ESG and Circular Economy Certifications | +0.7% | National, early adoption in Frankfurt and Munich | Medium term (2-4 years) |

| Emergence of Hydrogen Economy Test Protocols | +0.6% | National, pilot regions in Lower Saxony and Hamburg | Long term (≥ 4 years) |

| Digital Twin Based Remote Inspection Platforms | +0.5% | National, acceleration in energy and utilities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerated Electric Vehicle Adoption and Battery Gigafactories

Germany assembled 1.2 million electric vehicles in 2025, and domestic cell plants reached 180 GWh of annual capacity, which created sustained demand for third-party verification of thermal-runaway containment, dendrite formation risk, and state-of-health analytics.[1]Verband der Automobilindustrie, “German Automobile Production Statistics,” vda.de Gigafactories operated by Northvolt in Heide and CATL in Erfurt must clear IEC 62619 and UN 38.3 schemes before shipping packs to carmakers, generating recurring inspection revenue each time production scales. The EU Battery Regulation’s battery-passport clause obliges manufacturers to disclose embedded carbon footprints and recycled-content ratios through blockchain anchored certificates, driving an audit workload that only accredited laboratories can satisfy. TÜV Rheinland enlarged its Cologne center by 40% in 2025, adding thermal-abuse chambers and nail-penetration rigs to absorb the queue of prototype cells seeking clearance. The convergence of EUR 10 billion (USD 11.3 billion) in greenfield capital outlays and a pivot away from combustion engines gives this driver a 1.2 percentage point lift to forecast CAGR.

Stricter EU Regulatory Enforcement in Safety Critical Industries

The EU Machinery Regulation that becomes fully applicable in January 2027 moves scores of collaborative robots and autonomous vehicles from self-declaration to notified-body review, shifting liability toward independent assessors and unlocking fresh certification streams. Germany already hosts 38 notified bodies, and each must evaluate software safety life cycles under ISO 13849 and cybersecurity hardening under IEC 62443-4-1 before a CE mark can be affixed.[2]Federal Institute for Occupational Safety and Health, “List of Notified Bodies,” baua.de The Medical Device Regulation eliminated grandfathering in 2024 and forced backlogs of legacy implants into recertification queues, a monetization corridor that TIC providers address via expedited review lanes. In chemical processing, the addition of 200 substances of very high concern to the REACH candidate list in 2025 triggers new safety-data-sheet audits and exposure scenario validations. Heightened regulatory vigilance therefore contributes a full 1.0 percentage point to market growth.

Rising Complexity of Industry 4.0 and IoT Enabled Supply Chains

Manufacturers connected 420,000 industrial IoT endpoints in 2025, and every node requires electromagnetic compatibility checks, cybersecurity penetration tests, and functional safety validation before integration. Predictive algorithms that feed maintenance scheduling must pass SIL 2 or SIL 3 target verification to avoid false positives that could halt operations or mask critical degradation IEC.CH. Tier-1 suppliers in Baden Württemberg now demand blockchain verified certificates of conformity for each semiconductor batch, which TIC laboratories issue by linking laboratory information management systems into distributed ledgers.[3]Bosch, “Blockchain Traceability Pilot,” bosch.com Edge gateways aggregating machine data face dual certification burdens because a compromised gateway can inject malicious commands that jeopardize human safety. The sheer volume of connected devices transforms TIC from a one-time gate into a subscription style continuous service, adding 0.9 percentage point to forecast CAGR.

Growing Demand for ESG and Circular Economy Certifications

Germany implemented the Corporate Sustainability Reporting Directive in 2025, compelling around 15 000 firms to disclose scope 3 emissions and waste diversion rates, metrics that investors insist be assured by accredited third parties. Circular badges such as Cradle to Cradle and the EU Ecolabel rose sharply, with TÜV SÜD reporting a 35% surge in 2025 audits.[4]TÜV SÜD, “Cradle to Cradle Certification Demand,” tuvsud.com Green bond issuers in Frankfurt request second-party opinions that proceeds genuinely finance renewable assets, another niche that certification houses are filling. Extended producer responsibility laws for packaging and electronics intensify material analysis workloads as brands must document recycled content percentages, landfill diversion pathways, and safe end of life routes. Those overlapping forces add 0.7 percentage point to CAGR as sustainability claims transition from marketing slogans to audited fact.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of Accredited Laboratory Capacity in Key Hubs | -0.8% | Bavaria, Baden Württemberg, North Rhine Westphalia | Short term (≤ 2 years) |

| Fragmented Federal State Regulations Slowing Approvals | -0.6% | National, acute in hydrogen and construction sectors | Medium term (2-4 years) |

| Client Pushback on TIC Price Escalation amid Cost Pressures | -0.4% | National, concentrated among SMEs | Short term (≤ 2 years) |

| Cyber Security Risks to Connected Test Equipment | -0.3% | National, highest in automotive and aerospace testing | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of Accredited Laboratory Capacity in Key Hubs

Bavaria and Baden Württemberg deliver 38% of national manufacturing output yet face 10 to 14 week waits for electromagnetic compatibility chambers, double the 2023 benchmark, forcing some firms to truck prototypes abroad for faster slots.[5]Automobilwoche, “Laboratory Wait Times Double,” automobilwoche.de Accreditation under ISO 17025 takes up to two years, and the national body cleared only 42 new facility applications in 2025, well below demand from batteries and hydrogen components.[6]Deutsche Akkreditierungsstelle, “Annual Report 2025,” dakks.de Wage premiums of up to 30% for high voltage or cryogenic specialists inflate cost bases and slow expansion. Hesitant capacity growth delays product launches, compresses test cycles, and trims margins when clients bargain priority fees that providers cannot fully pass through. Collectively the bottleneck drags the Germany testing inspection and certification market CAGR by 0.8 percentage point.

Fragmented Federal State Regulations Slowing Approvals

Germany’s Länder retain authority over building codes, environmental permits, and fire safety, so a hydrogen refueling station cleared in North Rhine Westphalia can still require extra dossiers in Hesse that tack on three to six months. A wind turbine foundation inspected in Lower Saxony may need fresh geotechnical reviews once a project crosses into Schleswig Holstein, duplicating load tests and lifting costs. Construction product approvals issued in one state are not always accepted in a neighbor, compelling manufacturers to repeat fire resistance trials that consume chamber time and capital. The resulting friction reduces nationwide rollout appetite and chips 0.6 percentage point from CAGR projections.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Certification Momentum Outpaces Testing

Testing held 57.68% of the Germany testing, inspection, and certification market in 2025 because material analysis, emissions measurement, and electrical safety remain prerequisites across automotive and machinery clusters. Certification however is on track for a 5.03% CAGR through 2031, buoyed by fourteen new product families that the EU moved into compulsory notified-body oversight between 2024 and 2026. The Germany testing, inspection, and certification market size for certification services therefore expands faster than for purely operational inspections, a shift that steers budget allocations toward documentation, software review, and cybersecurity audits. Laboratories are racing to upgrade scopes so that a single site can sign off on functional safety, electromagnetic compatibility, and penetration testing in one integrated workflow. Testing continues to evolve through digital twin models and accelerated aging protocols for battery cells that DEKRA and SGS launched in 2025. Inspection, traditionally anchored in annual crane and pressure vessel checks, is now augmented by condition based monitoring which converts many visits into data-driven remote verifications. These dynamics reinforce that share gains accrue to providers that couple classical destructive or non-destructive testing with regulation grade attestation services.

Margins on cybersecurity certification already exceed those on legacy electrical compliance because a Common Criteria EAL4+ review for an automotive control unit can invoice up to EUR 180 000 (USD 198 000) per product family, double the average ISO 26262 functional safety assessment. Laboratories with deep firmware expertise thus capture premium pricing and long tail re-assessment revenues every time a manufacturer pushes an over the air update. Inspection still anchors stable recurring work on Germany’s 1.2 million regulated assets, yet the cadence shifts from calendar based routines to sensor triggered interventions. Fraunhofer’s 3D SmartInspect platform cut turbine down-time from eight hours to ninety minutes, demonstrating tangible cost reduction for operators who adopt drone assisted visual checks. The Germany testing, inspection, and certification market share of inspection will therefore remain solid although growth lags certification given the deferral impact of predictive analytics.

By Sourcing Type: Outsourcing Rises as Complexity and Capital Costs Escalate

In-house capabilities represented 60.47% of 2025 spend, chiefly within automotive OEMs that maintain powertrain, durability, and emissions labs on-site. Outsourced work however is forecast to grow 5.12% annually to 2031 because the Germany testing, inspection, and certification market size for outsourced contracts benefits from economies of scale not feasible for mid tier suppliers. A single battery safety chamber capable of UN 38.3 trials costs EUR 1.2 million to EUR 1.8 million (USD 1.32 million to USD 1.98 million) an outlay many suppliers cannot justify for sporadic projects. Bosch signaled the shift by redirecting 34% of its electromagnetic compatibility tests to external labs in 2024 when 5G frequency work exceeded its internal range. Life sciences shows an even sharper pivot because the Medical Device Regulation mandates annual biocompatibility confirmation that firms prefer to bundle under multi year service level agreements with Eurofins or SGS.

Hybrid approaches blend proximity control with accreditation leverage. Volkswagen and DEKRA co-located a cybersecurity test lab at Wolfsburg in 2025 so that engineers retain design secrecy yet still deliver notified body ready conclusions. Larger manufacturers keep core validation for proprietary systems behind the firewall while farming out routine conformity repeats to third parties. This operating model widens the addressable Germany testing inspection and certification market for specialist houses that can guarantee slot availability and ten day turnaround times. Consequently the outsourced slice inches upward each year as testing sophistication continues to ratchet higher.

By Industry Vertical: Healthcare Leads Growth While Automotive Maintains Scale

Automotive and transportation delivered 19.26% of 2025 revenue due to Germany’s production of 2.6 million vehicles and stringent vehicle homologation rules. The Germany testing, inspection, and certification market share attributable to life sciences is thinner today but this vertical advances at a 5.76% CAGR to 2031 because the post market surveillance clauses inside the Medical Device Regulation created queues of legacy devices awaiting review. TÜV SÜD disclosed that its pipeline for high risk Class III submissions swelled 47% year on year, extending average assessment lead times to 14 months. Pharmaceutical biologics add further workload as cold chain audits become routine for cell and gene therapies.

Telecom and information technology contributed near ten percent of 2025 billings as 47 000 5G base stations demanded radio frequency exposure assessments under Bundesnetzagentur guidance. Energy and utilities leverage inspection for offshore wind foundations, subsea cables, and hydrogen pipeline integrity, partly balancing the retreat in fossil fuel refinery throughput. Aerospace remains niche but stringent traceability for composite parts under EASA Part-21 is driving non destructive testing collaborations with Applus+ and Element Materials. Consumer goods and food testing expanded only modestly, although EU Farm to Fork pesticide thresholds keep German ports busy screening imports.

By Mode of Service Delivery: Remote Platforms Gather Momentum

On-site work still dominated at 52.43% in 2025 because cranes, pressure vessels, and elevators require physical examination under statutory rules. Yet remote and digital inspection grows at 6.07% a year because the Germany testing, inspection, and certification market size for data driven oversight now includes drone imaging, lidar scans, and secure telemetry feeds. Fraunhofer IFF’s AutoInspect demonstrated 94% defect detection accuracy, shrinking weld review time by 63% during a Volkswagen pilot. DEKRA integrated digital twin analytics into industrial inspection so that BASF can simulate reactor stress cycles without dismantling hardware.

Laboratory based testing retains a 35% stake given the need for controlled emissions chambers and biohazard suites. Regulatory clarity improved in 2025 when the German Accreditation Body confirmed that ISO 17020 allows remote inspections if physical audits occur at least every two years, legitimizing hybrid models. SAP’s Asset Intelligence Network logged 2.3 billion inspection datapoints in 2024, evidence that asset owners value continuous visibility over point in time snapshots. Cybersecurity concerns persist however as Fraunhofer SIT exploited vulnerable industrial protocols in demonstration hacks, prompting VDE to issue supplemental hardening guidance in March 2025. Providers that bundle secure connectivity and real time analytics therefore stand to capture the fastest growing slice of future demand.

Geography Analysis

Bavaria, Baden Württemberg, and North Rhine Westphalia together generated an estimated 58% of Germany testing inspection and certification market demand in 2025. Bavaria’s automotive cluster around Munich and Ingolstadt sent 1.7 million type approval files to the Kraftfahrt Bundesamt, representing over one third of national submissions. Baden Württemberg reported 1 200 accredited laboratories by December 2025 and anchors electromagnetic compatibility and machinery safety work for Bosch, ZF, and Daimler Truck. North Rhine Westphalia remains the chemicals heartland, feeding steady pressure vessel and environmental testing volumes to TIC hubs operated by TÜV Rheinland and DEKRA.

Northern states such as Hamburg, Lower Saxony, and Schleswig Holstein gain visibility from offshore wind and maritime hydrogen pilots. Hamburg Port Authority catalogued 340 component certificates required to convert its cargo handling fleet to hydrogen drives, a pipeline now served by TÜV Nord and DNV. Lower Saxony hosts Volkswagen’s battery investments while Brandenburg houses Tesla’s Grünheide plant, yet only three local laboratories held UN 38.3 accreditation at end 2025, compelling sample shipments southward and perpetuating capacity shortages.

Eastern Germany including Saxony, Thuringia, and Saxony Anhalt benefits from 4.2 GW of new solar in 2024 and 2025 that requires photovoltaic module testing and grid interconnection certificates handled by SGS Germany and Bureau Veritas from Leipzig outposts. Regulatory divergence still complicates nationwide rollouts because Bavaria retains stricter fire resistance rules for high rises than North Rhine Westphalia, adding more than four months to approval timelines on average. Maritime projects must also clear Federal Maritime and Hydrographic Agency inspections for subsea cables, reinforcing demand for offshore specialized vessels operated by DNV and Lloyd’s Register. Geographic concentration thus mirrors industrial density, yet scarcity of hydrogen and battery test infrastructure in the north and east remains a bottleneck that investors are only beginning to address.

Competitive Landscape

The five largest providers, TÜV SÜD, TÜV Rheinland, DEKRA, SGS Germany, and Bureau Veritas, held about 62% of Germany testing, inspection, and certification market revenue in 2025, but none exceeds an 18% individual share, reflecting enduring fragmentation driven by regional accreditation and sector specialization hurdles. Generalists pursue software enabled differentiation. TÜV Rheinland launched battery passports that embed QR coded lifecycle data directly onto each cell, quickly landing BMW and Volkswagen contracts. DEKRA’s digital twin inspection portfolio, unveiled late 2024, secured BASF and Covestro deals by letting operators run failure simulations on virtual plant replicas and schedule maintenance before shutdowns.

Specialists thrive in niches the giants under serve. Hohenstein Laboratories leverages decades of textile knowhow to win flammability and microplastic shedding tests for fashion brands, while Testo couples cloud sensors with HVAC calibrations that cut building energy use. Hydrogen purity and component safety stand out as a white space where TÜV Rheinland moved first with the H2.21 mark that Air Liquide and Linde already adopt. Regulatory convergence may lower entry barriers for pan European challengers once the European Commission completes infringement actions against Länder level construction product approvals, potentially intensifying price competition.

Technology race lines sharpen further. Fraunhofer IFF’s AutoInspect platform hit 94% defect detection accuracy, suggesting machine learning could commoditize manual weld inspection. Incumbents must therefore buy or license AI analytics or risk margin erosion as clients internalize simple visual checks. Moderate consolidation continues as Bureau Veritas bought Element’s Hamburg site in late 2025, adding ultrasonic weld and corrosion testing for offshore wind structures together with 45 engineers.[7]Bureau Veritas, “Hamburg Laboratory Acquisition Press Release,” bureauveritas.com Similar tuck in deals are expected in 2026 as players shore up gaps in hydrogen, cybersecurity, and digital twin validation.

Germany Testing, Inspection, And Certification Industry Leaders

TÜV SÜD AG

TÜV Rheinland AG

DEKRA SE

TÜV Nord Group

SGS Germany GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: TÜV SÜD opened a EUR 25 million (USD 27.3 million) battery test center in Stuttgart with thermal runaway chambers, nail penetration rigs, and accelerated aging ovens able to process 500 modules per month.

- January 2026: DEKRA partnered with Siemens Energy to create a hydrogen component laboratory in Essen that targets ISO 19880 services for refueling stations and electrolyzers.

- December 2025: SGS Germany completed an EUR 18 million (USD 19.8 million) expansion of its Hamburg port laboratory, adding ultrasonic weld and corrosion testing for offshore wind monopiles.

- November 2025: Bureau Veritas acquired Element Materials Technology’s Hamburg laboratory, adding non destructive testing capacity and 45 engineers to its maritime portfolio.

Germany Testing, Inspection, And Certification Market Report Scope

The testing, inspection, and certification sector comprises conformity assessment bodies that offer several services, including auditing and inspection, testing, verification, certification, and quality assurance. Testing represents the industrial activities to ensure that individual components, manufactured products, and multicomponent systems are adequate for their intended usage. Testing and inspection are the operational parts of quality control, an essential factor in the survival of any manufacturing company.

The Germany Testing Inspection and Certification Market Report is Segmented by Service Type (Testing, Inspection, and Certification), Sourcing Type (In-house, and Outsourced), Industry Vertical (Consumer Goods and Retail, ICT and Telecom, Automotive and Transportation, Aerospace and Defense, Oil, Gas and Petrochemicals, Energy and Utilities, Industrial Manufacturing and Machinery, Chemicals and Materials, Construction and Infrastructure, Life Sciences and Healthcare, Food Agriculture and Beverage, and Other Industry Verticals), and Mode of Service Delivery (On-site, Off-site and Laboratory, and Remote and Digital). The Market Forecasts are Provided in Terms of Value (USD).

By Service Type

| Testing |

| Inspection |

| Certification |

By Sourcing Type

| In-house |

| Outsourced |

By Industry Vertical

| Consumer Goods and Retail |

| ICT and Telecom |

| Automotive and Transportation |

| Aerospace and Defense |

| Oil, Gas and Petrochemicals |

| Energy and Utilities |

| Industrial Manufacturing and Machinery |

| Chemicals and Materials |

| Construction and Infrastructure |

| Life Sciences and Healthcare |

| Food, Agriculture and Beverage |

| Other Industry Verticals (Environment and Sustainability) |

By Mode of Service Delivery

| On-site |

| Off-site and Laboratory |

| Remote and Digital |

| By Service Type | Testing |

| Inspection | |

| Certification | |

| By Sourcing Type | In-house |

| Outsourced | |

| By Industry Vertical | Consumer Goods and Retail |

| ICT and Telecom | |

| Automotive and Transportation | |

| Aerospace and Defense | |

| Oil, Gas and Petrochemicals | |

| Energy and Utilities | |

| Industrial Manufacturing and Machinery | |

| Chemicals and Materials | |

| Construction and Infrastructure | |

| Life Sciences and Healthcare | |

| Food, Agriculture and Beverage | |

| Other Industry Verticals (Environment and Sustainability) | |

| By Mode of Service Delivery | On-site |

| Off-site and Laboratory | |

| Remote and Digital |

Key Questions Answered in the Report

How large will Germany’s testing inspection and certification market be by 2031?

The sector is projected to reach USD 31.72 billion by 2031, up from USD 25.34 billion in 2026.

Which service line is growing fastest inside German quality assurance?

Certification activities are forecast to expand at 5.03% annually through 2031, outpacing testing and inspection.

Why are companies outsourcing more laboratory work?

Capital intensive battery and cyber test rigs cost up to USD 1.98 million each, so mid tier suppliers increasingly prefer pay-per-test contracts with accredited providers.

Which industry vertical drives the next wave of demand?

Life sciences and healthcare leads growth with a 5.76% CAGR because stricter medical device rules require continuous third-party oversight.

How are remote inspection platforms changing service delivery?

Drone imaging and digital twins are trimming downtime by more than 60% on wind turbines and industrial welds, shifting spend from on-site audits toward data driven remote verification.

What threat does regulatory fragmentation pose?

Divergent state rules can add three to six months to hydrogen station approvals and duplicate testing costs, reducing the national CAGR by an estimated 0.6 percentage point.

Page last updated on: