India Pet Nutraceuticals Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

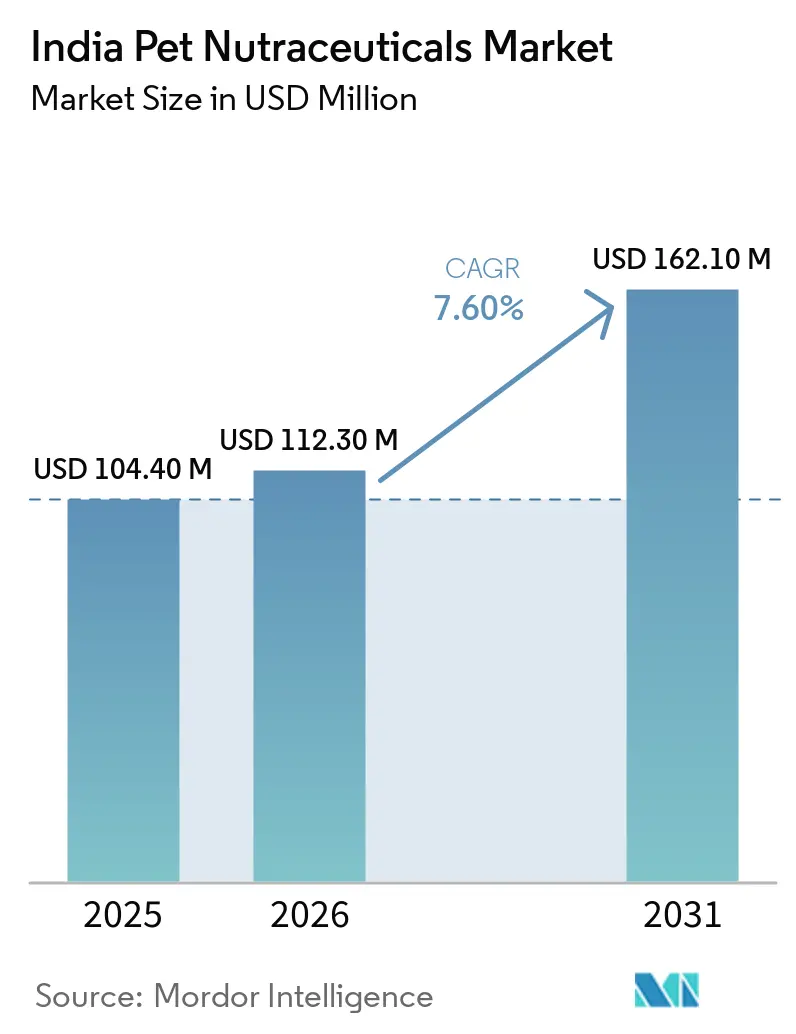

| Base Year Market Size (2025) | USD 104.40 Million |

| Market Size (2026) | USD 112.30 Million |

| Market Size (2031) | USD 162.10 Million |

| Growth Rate (2026 - 2031) | 7.60% CAGR |

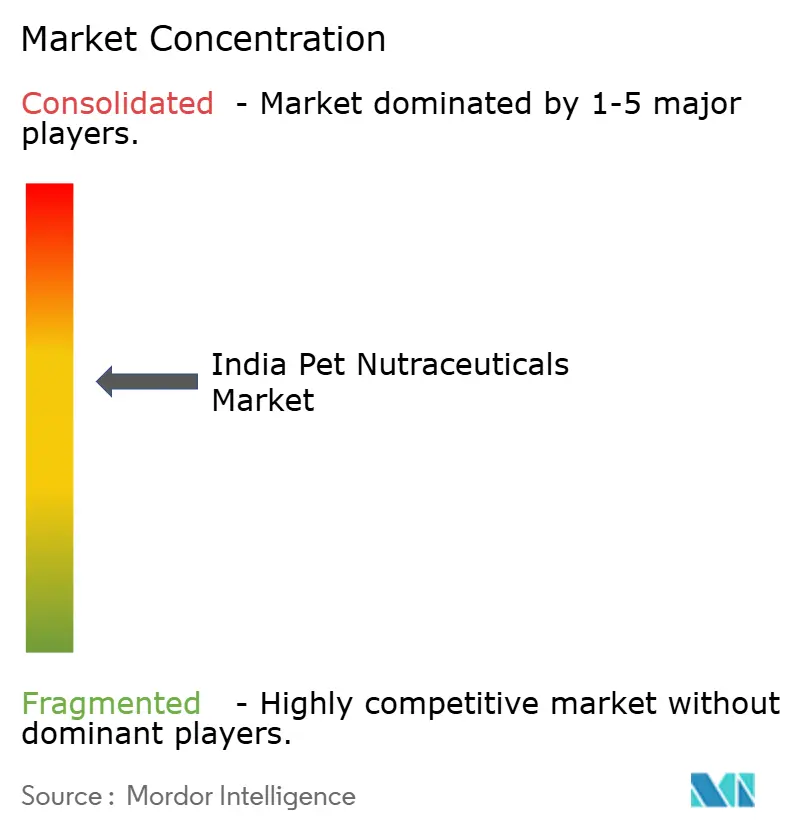

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Pet Nutraceuticals Market Analysis by Mordor Intelligence

The India pet nutraceuticals market is projected to grow from USD 104.4 million in 2025 to USD 112.3 million in 2026, reaching USD 162.1 million by 2031, with a CAGR of 7.6% during 2026-2031. Online order volumes for pet care products in India increased by 95% in FY2025 compared to FY2024, highlighting the rapid expansion of digital purchasing, which facilitates repeat supplement purchases. In 2025, Investments by major companies, such as Nestlé SA’s minority stake in Drools Pvt. Ltd., Reliance Consumer Products’ launch of Waggies, and Wipro Consumer Care Ventures’ investment in Goofy Tails, indicate growing interest in the market as a space for brand development, portfolio diversification, and consolidation. Additionally, the re-operationalization of the 2022 nutraceutical regulations by FSSAI (Food Safety and Standards Authority of India) in July 2024 has emphasized the importance of labeling and claim compliance, benefiting organized players with robust compliance systems. Improvements in local packaging, fresh food processing, and clinic expansions are expanding the supply chain's reach and accessibility for pet owners, driving adoption beyond metropolitan areas. These developments are positioning the market on a steady premium-growth trajectory, though smaller brands continue to face challenges such as tighter profit margins, increased compliance requirements, and limited access to specialized ingredients.

Key Report Takeaways

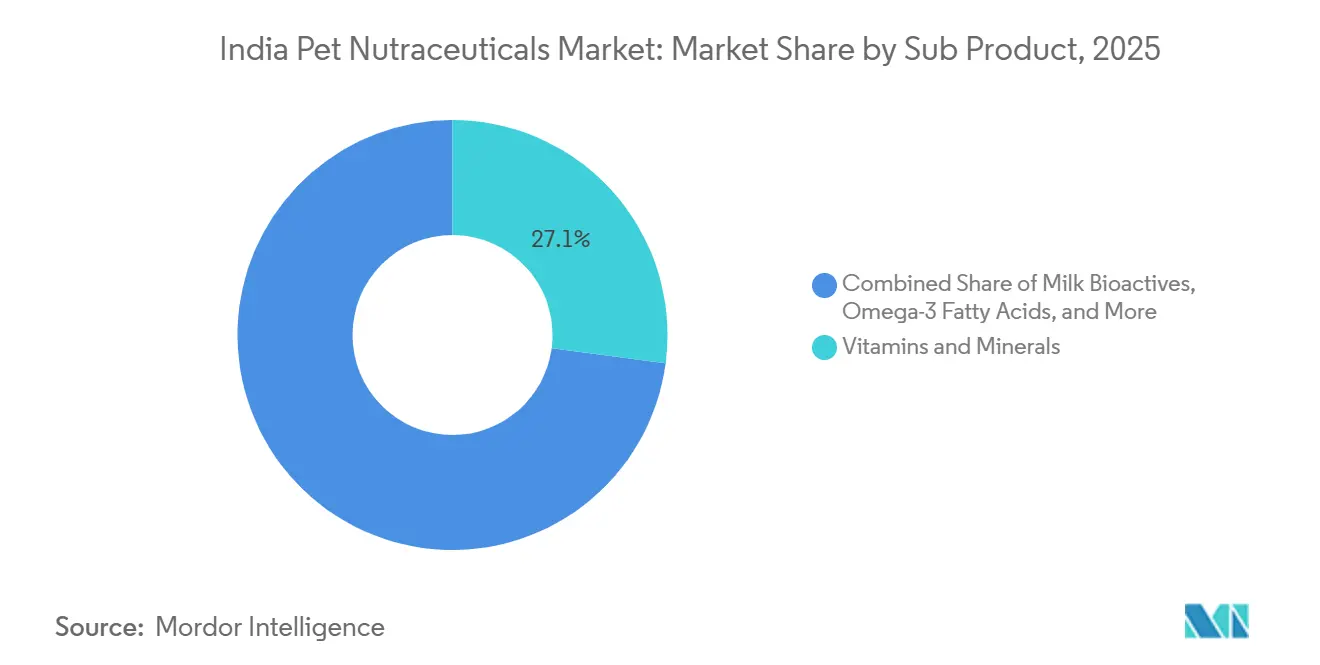

- By sub product, vitamins and minerals accounted for 27.1% share of the India pet nutraceuticals market size in 2025, while probiotics is forecast to expand at a 10.5% CAGR through 2031.

- By pets, dogs held 74% of the India pet nutraceuticals market share in 2025, while cats recorded the highest projected CAGR at 9.5% through 2031.

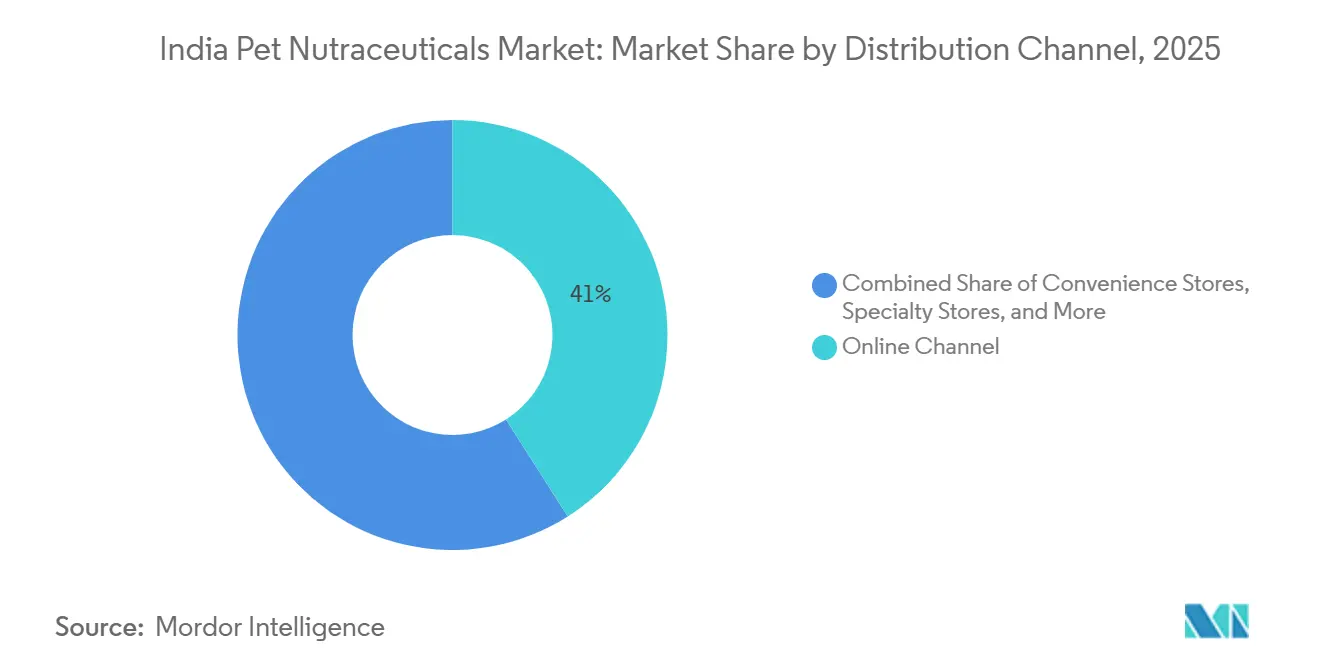

- By distribution channel, the online channel accounted for 41% share of the India pet nutraceuticals market size in 2025 and is advancing at a 12.6% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Pet Nutraceuticals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Pet Humanization in Urban India | +2.0% | National, with concentration in Delhi NCR, Mumbai, Bengaluru, Hyderabad, and Chennai | Short term (≤ 2 years) |

| Expansion of Preventive Veterinary Care | +1.5% | National, strongest in Tier 1 cities with spillover to Tier 2 cities | Medium term (2-4 years) |

| Premiumization of Pet Wellness Spending | +1.2% | Tier 1 cities and higher income urban households nationally | Medium term (2-4 years) |

| Growth of Online and D2C Discovery | +1.5% | National, with rapid penetration in Tier 2 and Tier 3 cities via quick commerce | Short term (≤ 2 years) |

| Demand for Breed Specific and Life Stage Formulations | +0.8% | Tier 1 cities, with early gains in Bengaluru, Mumbai, and Pune | Medium term (2-4 years) |

| Local Manufacturing of Functional and Herbal Formulations | +0.9% | National, with manufacturing hubs in Karnataka, Maharashtra, and Chhattisgarh | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Pet Humanization in Urban India

Pet ownership in major Indian cities is increasingly integrated into daily family routines, driving growth in the India pet nutraceuticals market. According to Flipkart trend data, pet care order volumes grew by over 50% year-over-year in 2025, primarily driven by Gen Z and millennial consumers who actively research wellness products online. This shift is significant as buyers are no longer waiting for veterinary visits to consider supplements for digestion, mobility, skin health, and immunity. Instead, they are comparing ingredients, reading reviews, and purchasing multiple products in a single order, which boosts both conversion rates and basket values in the market. Additionally, supplements are easier to reorder than larger discretionary pet accessories, which contributes to stronger customer retention. In 2026, Royal Canin projected that India could account for 30% of emerging market pet adoption growth over the next five years, indicating a growing customer base for preventive care. With more first-time pet owners entering the market, the India pet nutraceuticals market is transitioning from occasional treatment purchases to consistent wellness-focused spending.

Expansion of Preventive Veterinary Care

The growing emphasis on preventive care is strengthening clinical advice as a key driver in the India pet nutraceuticals market. India has approximately 4,000 to 5,000 practicing veterinarians, primarily concentrated in urban and semi-urban areas, where organized clinic networks play a significant role in raising awareness about supplements. Supertails Pvt. Ltd. is leveraging this trend through its network of over 100 veterinarians and more than six clinics in Bengaluru, integrating consultations with direct product recommendations and ongoing care. This approach enhances trust in product categories such as probiotics, joint support, omega-3, and calming formulations, as pet owners encounter these products in a clinical setting rather than solely in retail environments. Additionally, it streamlines the process from diagnosis to purchase, boosting conversion rates for organized brands with veterinary outreach in the India pet nutraceuticals market. Over time, tele-veterinary and clinic-led models are anticipated to reduce awareness disparities between metropolitan areas and emerging urban centers. Consequently, preventive care is anticipated to remain a significant driver of demand in the India pet nutraceuticals market during the forecast period.

Premiumization of Pet Wellness Spending

Premium buying behavior is increasingly evident in the India pet nutraceuticals market, particularly among higher-income households in major urban areas. In 2025, Nestlé SA’s USD 1 billion investment in Drools Pet Food Pvt. Ltd. highlights the interest of large food companies in premium positioning and long-term brand growth in pet nutrition and wellness products. Similarly, in 2024, Royal Canin established a packaging center in Bhiwandi, supported by an INR 100 crore (USD 12.2 million) investment, underscoring its commitment to enhancing premium supply and availability in India. Additionally, in 2025, Elanco’s launch of Pet Protect demonstrates that global animal health companies recognize the potential of a premium segment for veterinarian-formulated supplements for dogs and cats. These developments are significant because premium buyers tend to remain loyal to trusted product lines once efficacy and safety are proven. This loyalty enables brands to expand from core nutrition products into related supplement categories without compromising consumer trust. Consequently, premiumization is driving both pricing stability and broader product adoption in the India pet nutraceuticals market.

Growth of Online and D2C Discovery

Digital commerce plays a significant role in the India pet nutraceuticals market, as it facilitates both discovery and repeat purchases within the same platform. Online sales of pet care products in India increased by 95% in FY2025, highlighting the rapid adoption of digital channels for recurring purchase categories. Quick commerce platforms such as Blinkit, Zepto, and Instamart are enhancing access to daily-use and wellness SKUs, reducing barriers to replenishment purchases. This trend benefits brands that excel in search rankings, ratings, reviews, and subscription models, rather than relying solely on shelf visibility. It also supports smaller, digital-first brands that effectively communicate product benefits and ensure reliable fulfillment. Supertails Pvt. Ltd.'s USD 30 million fundraising in 2026, with a portion allocated to technology and personalization, underscores the growing importance of platform quality as a competitive advantage in the India pet nutraceuticals market. As digital adoption expands in Tier 2 and Tier 3 cities, online discovery is projected to remain one of the fastest-growing demand channels in this market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Price Sensitivity Outside Tier 1 Cities | -1.8% | Tier 2 and Tier 3 cities nationally, and rural India | Medium term (2-4 years) |

| Limited Veterinary Recommendation Depth in Smaller Cities | -1.1% | Tier 2 and Tier 3 cities and smaller towns across states | Medium term (2-4 years) |

| Regulatory Uncertainty for Pet Health Claims | -0.8% | National | Short term (≤ 2 years) |

| Import Dependency for Select Actives and Premium Inputs | -0.7% | National, with higher impact on importers in Mumbai and Delhi | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Price Sensitivity Outside Tier 1 Cities

Price sensitivity remains a significant constraint on the growth of the India pet nutraceuticals market, particularly beyond major urban centers. According to the Ministry of Food Processing Industries, pet food demand is primarily concentrated in urban areas, highlighting the uneven distribution of organized spending across the country in 2025[1] Source: Ministry of Food Processing Industries, Government of India, “Pet Food Sector Profile,” MOFPI Knowledge Centre, mofpi.gov.in. In Tier 2 and Tier 3 cities, pet owners tend to prioritize packaged staple nutrition over supplementary products, delaying the adoption of nutraceuticals. This progression slows the uptake of higher-priced products, even as online awareness increases. Premium wellness brands face challenges relying solely on visibility and often need additional strategies, such as consumer education, smaller packaging options, or endorsements from veterinary clinics, to drive volume growth. Local companies with lower cost structures are better positioned to adapt their packaging and pricing strategies to meet these market conditions. Until household spending on companion animal care increases significantly outside metropolitan areas, growth in the India pet nutraceuticals market is likely to remain moderated.

Limited Veterinary Recommendation Depth in Smaller Cities

The India pet nutraceuticals market continues to rely significantly on veterinary recommendations in smaller cities, where independent supplement purchasing is less prevalent. The concentration of veterinarians in urban areas limits access to regular consultations and product guidance in smaller areas [2]Source: India Brand Equity Foundation, “Decoding the Rise of the Pet Care Industry in India,” IBEF, ibef.org. This is particularly important, as pet owners are more likely to delay purchasing supplements than essential products like basic food or deworming treatments when uncertain about their necessity or effectiveness. Farmina’s AI health coach, introduced in late 2024 and gaining recognition in 2025, aims to address this gap by providing digital nutrition guidance accessible beyond clinic hours. However, in smaller towns, trust is built gradually, and many pet owners prefer in-person advice before committing to recurring supplement purchases. This results in a larger gap between awareness and purchase compared to cities like Delhi, Mumbai, Bengaluru, or Chennai. Without faster expansion of tele-veterinary services and clinic networks, the depth of recommendations will remain a limiting factor for the growth of the India pet nutraceuticals market in the coming years.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sub Product: Probiotics and Vitamins Leading in a Diversifying Portfolio

Vitamins and minerals accounted for 27.1% of the India pet nutraceuticals market size in 2025, maintaining their leading position within the sub-product mix. This dominance is attributed to their widespread application for both dogs and cats, established prescribing practices among veterinarians, and greater consumer familiarity compared to more specialized formulations. Additionally, the current FSSAI (Food Safety and Standards Authority of India) regulatory framework encourages the purchase of labeled and documented products, favoring organized brands within this broad category. In the India pet nutraceuticals market, vitamins and minerals are the most accessible entry point for first-time supplement users.

Probiotics are projected to grow at a 10.5% CAGR through 2031, making them the fastest-growing sub-product in the India pet nutraceuticals market. This growth is driven by increasing awareness of the interconnectedness of digestion, immunity, stool quality, and skin health, which are now being addressed as related concerns rather than isolated issues. Initiatives such as Virbac’s Veterinary HPM 2025 nutritional platform and Elanco’s Pet Protect launch reflect the broader trend toward condition-specific, science-based wellness products for companion animals[3]Source: Virbac, “Veterinary HPM 2025, A New Lease of Life for Animal Nutrition,” Virbac Corporate, corporate.virbac.com . Additionally, omega-3 fatty acids, proteins and peptides, milk bioactives, and other nutraceuticals are expanding the product portfolio to address mobility, coat health, recovery, stress management, and overall vitality. Natural Remedies’ Ashwa.30 launch demonstrates how herbal ingredients can be effectively integrated into this growing functional mix when sourcing and positioning are strategically managed.

By Pets: Dogs Dominate Market Share, While Cat Nutrition Drives Growth

In 2025, dogs accounted for 74% of the India pet nutraceuticals market share, reflecting the market's strong reliance on canine ownership and spending trends. Dog supplements benefit from established care routines, as owners are accustomed to structured regimens addressing joints, skin, digestion, and multivitamin needs. This fosters consistent purchasing behavior for organized brands and ensures predictable reordering throughout a dog's life cycle. Royal Canin’s focus on precision nutrition aligns well with this segment of the India pet nutraceuticals market, as breed and life stage-specific needs are easier to communicate for dogs compared to other pets.

Cats are estimated to grow at a CAGR of 9.5% through 2031, marking the highest growth rate within the pet segment of the India pet nutraceuticals market. Urban apartment living supports this trend, as cats are better suited to smaller living spaces and have lower outdoor dependency. Nestlé Purina India’s expansion of its cat-focused portfolio in 2025 highlights the increasing recognition of feline wellness and specialized nutrition as a growth opportunity, as reported by MediaInfoline. Cat-specific formulas targeting urinary care, hairball control, and sterilization needs can enhance average value through their targeted approach. While other pets represent a smaller market share, they contribute niche demand driven by hobby ownership and premium care practices.

By Distribution Channel: Online Channels Redefine the Way to Repeat Purchase

The online channel accounted for 41.0% of the India pet nutraceuticals market size in 2025 and is projected to grow at a CAGR of 12.6% through 2031. This makes digital platforms the largest and fastest-growing route to purchase in the India pet nutraceuticals market. Online channels are particularly suited for supplements, as they allow shoppers to compare benefits, review ingredients, and schedule repeat deliveries without visiting physical stores. Supertails Pvt. Ltd.’s 2026 funding round and its planned investment in personalization highlight how platform design is evolving into a competitive factor, extending beyond backend functionality alone.

Specialty stores continue to play a significant role by supporting product discovery, building trust, and enabling assisted selling, particularly for products that benefit from expert recommendations. For instance, Heads Up For Tails operated more than 105 stores across 20 Indian cities by early 2025, enhancing the role of organized retail in premium pet product purchases. Supermarkets and hypermarkets cater to convenience-driven buyers, while quick commerce and smaller local channels address the need for urgent replenishment of common SKUs. FSSAI (The Food Safety and Standards Authority of India) enforces licensing and labeling regulations across all channels, giving larger distributors and established brands an advantage in managing compliance at scale

Geography Analysis

North India leads the broader pet food demand base in 2025, providing a strong foundation for the India pet nutraceuticals market in Delhi NCR and nearby urban clusters. These areas benefit from higher household incomes, larger dog-owning populations, and greater access to veterinary clinics and specialty retail outlets. Consequently, the market remains concentrated in metropolitan demand centers rather than being evenly distributed across the country. Key cities such as Bengaluru, Hyderabad, Chennai, Mumbai, Pune, and Delhi drive demand for premium wellness products due to stronger digital adoption and better access to organized care. South India is also gaining prominence, combining tech-enabled purchasing behavior with a growing startup and clinic ecosystem.

Maharashtra has emerged as a significant supply and consumption center within the India pet nutraceuticals market, with production and premium demand converging in the region. In April 2024, Royal Canin inaugurated its Bhiwandi packaging center, investing INR 100 crore (USD 12.2 million) to enable faster local fulfillment of premium pet nutrition products. Additionally, Drools expanded domestic capacity in April 2026 with an INR 180 crore (USD 21.6 million) investment in fresh pet food processing in collaboration with Tetra Pak. These developments enhance local availability, reduce supply chain friction, and strengthen organized distribution across western India.

Tier 2 cities such as Jaipur, Lucknow, Indore, Bhubaneswar, and Chandigarh represent the next growth phase for the India pet nutraceuticals market. While pet adoption is increasing in these areas, awareness of supplements remains lower compared to metropolitan locations. Limited veterinary infrastructure also means that pet owners often discover wellness products later in their care journey. Heads Up For Tails is targeting cities like Jaipur, Amritsar, Indore, and Bhubaneswar for store expansion, aiming to provide certified products in trusted retail environments. Although organized companion animal spending in eastern India is less developed, adoption trends are aligning with those in larger metros. As online education and assisted retail improve, these cities are anticipated to contribute to a broader second wave of demand in the India pet nutraceuticals market.

Competitive Landscape

In 2025, the India pet nutraceuticals market was moderately concentrated and organized, with the major players being Mars Incorporated, Nestlé Purina, Drools Pet Food Pvt Ltd., Himalaya Wellness Company, and Vivaldis. While the market remains open to local competitors with strong digital strategies or veterinary-focused positioning. Multinational companies maintain an edge in formulation credibility, portfolio diversity, and structured distribution networks. However, domestic brands excel in understanding local market dynamics, adapting quickly, and offering competitive pricing. Drools Pvt Ltd. achievement of unicorn status following Nestlé SA’s May 2025 acquisition of a minority stake underscores the potential for Indian brands to scale and attract global strategic investments.

Competitive advantages in the India pet nutraceuticals market are increasingly driven by clinical positioning, digital customer engagement, and localized supply chains, rather than solely by shelf presence. For instance, in 2024, Royal Canin’s Bhiwandi packaging center enhances supply reliability for premium nutrition products and strengthens local execution. Similarly, in 2025, Elanco’s launch of Pet Protect extends its established animal health expertise into veterinarian-formulated supplements. Virbac’s focus on Veterinary HPM 2025 demonstrates how companies are aligning nutritional products with specific health needs and clinical communication. These strategies create differentiation that is more sustainable and less reliant on price competition.

Technological advancements are reshaping competition in the India pet nutraceuticals market. Zoetis expanded its capability center in Hyderabad in 2024 to support AI-driven diagnostics and digital solutions, signaling a shift toward data-driven care prompts that can directly influence wellness-related purchases. Farmina’s Genius AI platform, recognized in 2025, exemplifies how digital advisory tools can engage pet owners between clinic visits and guide them toward specialized product choices. Consequently, the market is estimated to remain dominated by a few large-scale brands while providing opportunities for niche players focusing on specific conditions, ingredient narratives, or tailored customer experiences.

India Pet Nutraceuticals Industry Leaders

Mars Incorporated

Nestlé Purina

Drools Pet Food Pvt. Ltd.

Himalaya Wellness Company

Vivaldis

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Supertails Pvt. Ltd. raised USD 30 million in a funding round led by Singapore-based Venturi Partners, with participation from Nippon India Alternative Investments, Titan Capital, and existing investors. The capital is designated for expanding pet clinics beyond Bengaluru, scaling the quick commerce delivery infrastructure, and personalizing the company’s technology platform, thereby increasing pet owners' awareness and sales of pet veterinary diets nationwide.

- September 2025: Virbac India Private Limited globally launched Vikaly, the world’s first medicated feed for cats, combining renal kibble with a veterinary prescription drug, with an India rollout planned subsequently. This product creates a new therapeutic nutrition category with direct implications for veterinary channel nutraceutical sales in India.

- May 2025: Drools Pet Food Pvt. Ltd. received a minority financial investment from Nestlé SA, marking Nestlé’s first investment in an Indian brand and valuing Drools Pet Food Pvt. Ltd. at USD 1 billion. The company maintained operational independence while gaining access to global manufacturing expertise from Nestlé’s Purina division and introducing Drools' nutraceutical products to the market.

- February 2025: Elanco India Private Limited launched Pet Protect, a line of veterinarian-formulated supplements for dogs and cats covering joint health, immune support, and stress management. The launch directly expands Elanco’s presence in companion animal preventive health and nutraceutical products.

India Pet Nutraceuticals Market Report Scope

Pet nutraceuticals are non-drug substances produced from food or natural extracts. Administered orally, they bridge the gap between nutrition and medicine, offering health benefits like preventing disease or supporting normal body functions

The India Pet Nutraceuticals Market Report is segmented by sub product (Milk Bioactives, Omega-3 Fatty Acids, Probiotics, Proteins and Peptides, Vitamins and Minerals, and Other Nutraceuticals), by pets (Cats, Dogs, and Other Pets), and by distribution channel (Convenience Stores, Online Channel, Specialty Stores, Supermarkets and Hypermarkets, and Other Channels). The market forecasts are provided in terms of value in USD.

| Milk Bioactives |

| Omega-3 Fatty Acids |

| Probiotics |

| Proteins and Peptides |

| Vitamins and Minerals |

| Other Nutraceuticals |

| Cats |

| Dogs |

| Other Pets |

| Convenience Stores |

| Online Channel |

| Specialty Stores |

| Supermarkets/Hypermarkets |

| Other Channels |

| By Sub Product | Milk Bioactives |

| Omega-3 Fatty Acids | |

| Probiotics | |

| Proteins and Peptides | |

| Vitamins and Minerals | |

| Other Nutraceuticals | |

| By Pets | Cats |

| Dogs | |

| Other Pets | |

| By Distribution Channel | Convenience Stores |

| Online Channel | |

| Specialty Stores | |

| Supermarkets/Hypermarkets | |

| Other Channels |

Key Questions Answered in the Report

What is the size of the India pet nutraceuticals market in 2026 and 2031?

The India pet nutraceuticals market is valued at USD 112.3 million in 2026 and is forecast to reach USD 162.1 million by 2031 at a 7.6% CAGR.

Which sub product leads demand in India pet nutraceuticals?

Vitamins and Minerals led with a 27.1% share in 2025, while Probiotics is the fastest growing sub product with a 10.5% CAGR through 2031.

Why are online channels so important for pet supplements in India?

The online channel held 41% share in 2025 and is projected to grow at a 12.6% CAGR during 2026-2031, because supplements fit repeat ordering, search based discovery, and subscription buying.

Which pet category drives the highest spending on nutraceuticals in India?

Dogs remain the core demand base with 74% share in 2025, supported by higher ownership depth and more structured wellness routines.

What is pushing growth in cat focused pet wellness products in India?

Cats are forecast to grow at a 9.5% CAGR through 2031 as apartment living increases feline adoption and higher demand for urinary care, hairball control, and sterilized cat formulations.

Page last updated on: