South Africa NDT Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

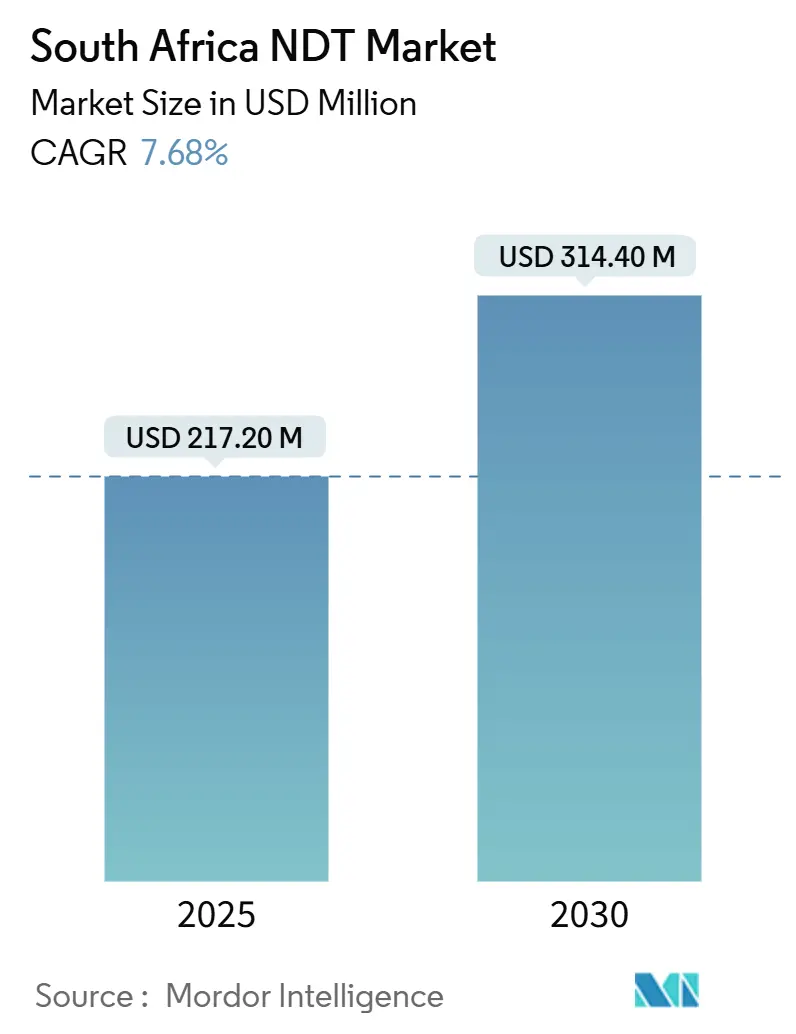

| Market Size (2025) | USD 217.20 Million |

| Market Size (2030) | USD 314.40 Million |

| Growth Rate (2025 - 2030) | 7.68% CAGR |

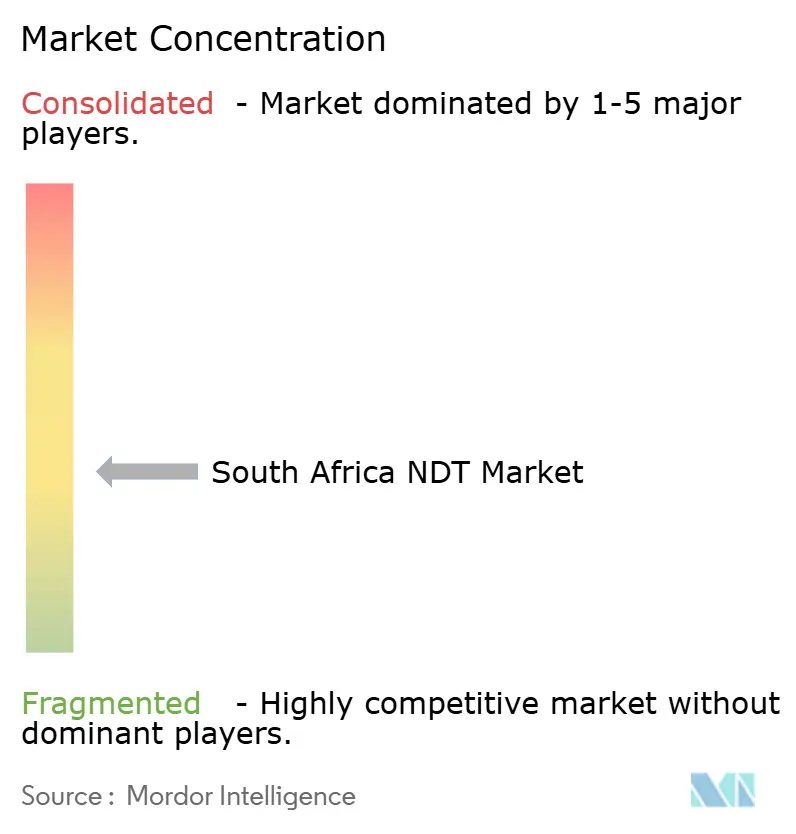

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Africa NDT Market Analysis by Mordor Intelligence

The South African NDT market size is estimated at USD 217.2 million in 2025 and is projected to register a 7.68% CAGR, reaching USD 314.4 million by 2030. Intensifying inspection requirements across energy, mining, and transport assets, together with new safety regulations, underpin sustained growth momentum. Government commitments—such as R50 billion for transmission upgrades and an estimated R100 billion for rail integrity restoration—are expanding the project pipeline and creating recurring demand for outsourced testing services. Persistent load-shedding is prompting investments in backup power systems and renewables, each requiring commissioning and preventive inspection programs. Meanwhile, skills shortages and high capital costs incline asset owners toward specialist service contracts, reinforcing the dominance of service-led revenue streams. International suppliers are strengthening local partnerships, signaling a rise in technology inflows and competitive differentiation through advanced modalities.

Key Report Takeaways

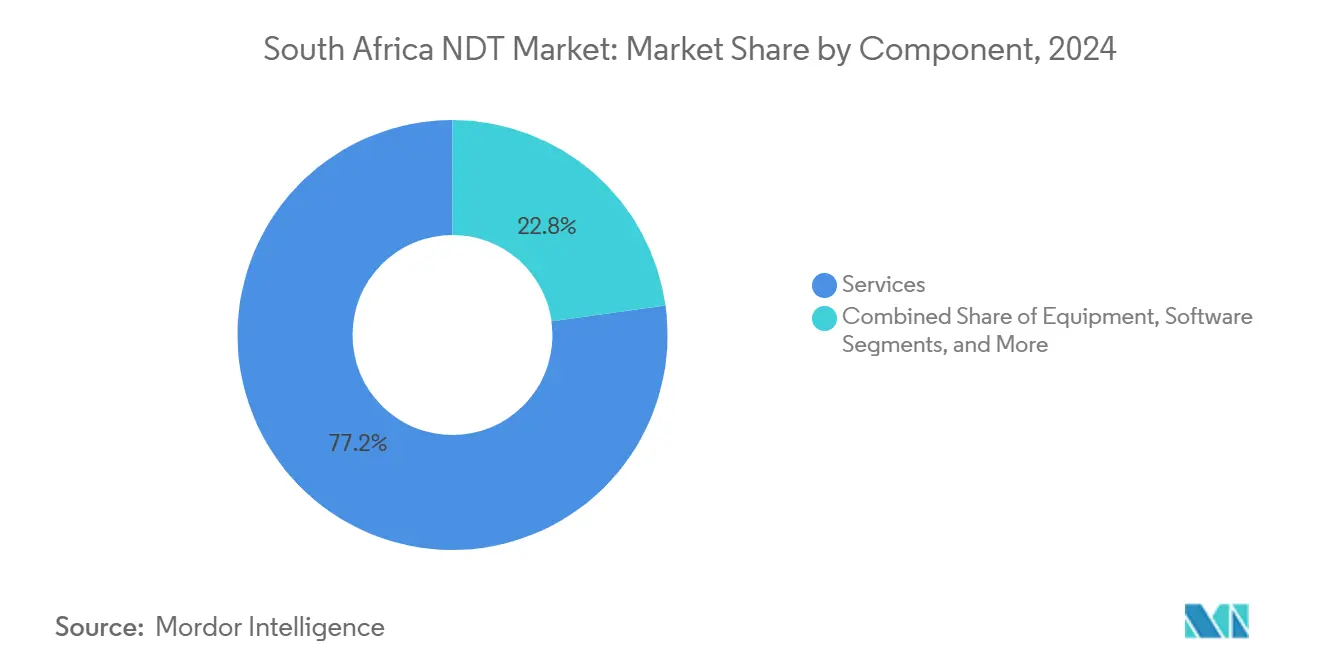

- By component, services held 77.2% of the South Africa NDT market share in 2024; software is projected to grow at a 11.1% CAGR through 2030.

- By testing method, ultrasonic testing is expected to lead with a 25.9% revenue share in 2024; eddy-current testing is projected to grow at an 8.1% CAGR through 2030.

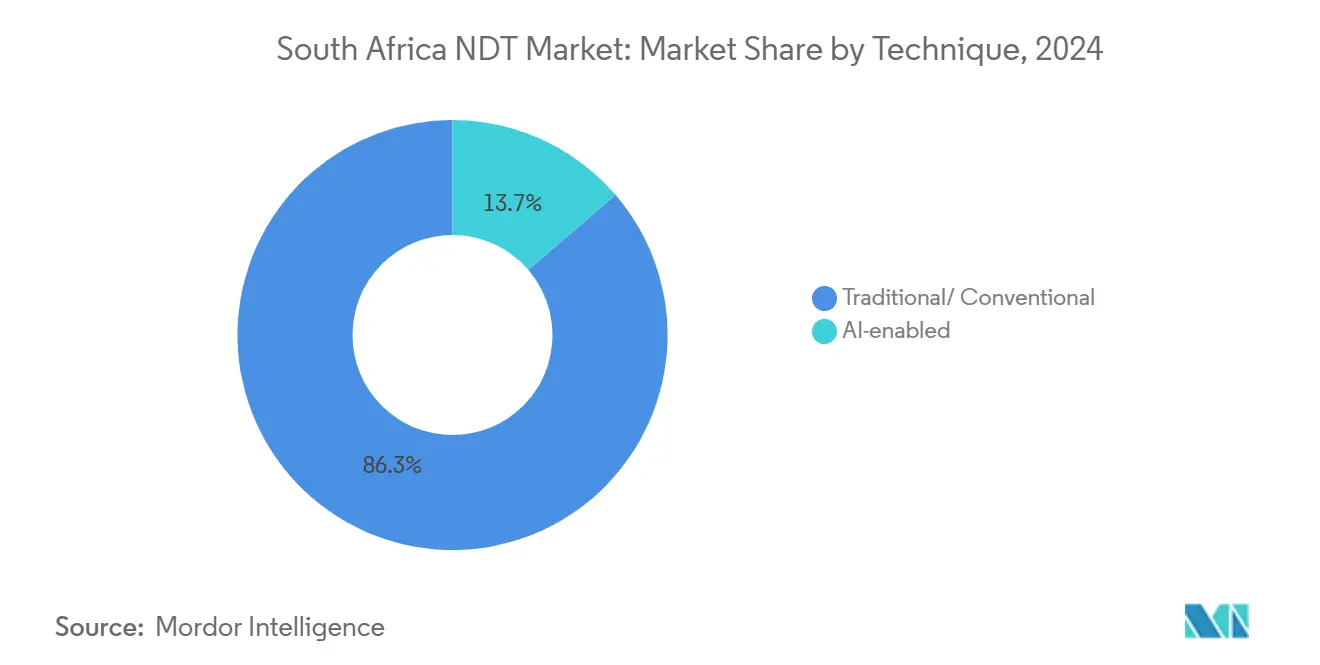

- By technique, traditional inspection accounted for an 86.3% share of the South Africa NDT market size in 2024, whereas AI-enabled methods are advancing at a 14.2% CAGR to 2030.

- By end-user, the oil and gas sector commanded 23.4% of the South African NDT market size in 2024; the automotive and transportation sector is forecast to expand at a 7.9% CAGR through 2030.

South Africa NDT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging oil and gas infrastructure inspection demand | +1.8% | National, concentrated in Gauteng and the Western Cape | Medium term (2-4 years) |

| Maintenance needs of aging power generation assets | +2.1% | National, focused on the Mpumalanga coal belt and renewable zones | Long term (≥ 4 years) |

| Regulatory safety compliance in the mining and petrochemical sectors | +1.5% | National, strongest in Gauteng, North West, and Northern Cape | Short term (≤ 2 years) |

| Expansion of automotive export-oriented manufacturing | +1.2% | Eastern Cape, Gauteng automotive corridors | Medium term (2-4 years) |

| Defense localisation incentives boosting aerospace MRO inspections | +0.8% | Gauteng aerospace hubs, Western Cape | Long term (≥ 4 years) |

| Composite wind-blade inspection requirements in renewables | +0.9% | Northern Cape, Western Cape wind corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Aging Oil and Gas Infrastructure Inspection Demand

South Africa’s petroleum assets, many of which were built during the 1970s and 1980s, face corrosion and fatigue issues that necessitate rigorous non-destructive testing. Sasol’s Secunda complex and coastal refineries undergo continuous ultrasonic wall-thickness mapping, while Transnet’s 12-inch aviation-fuel pipeline is subject to inline crack detection tenders issued in 2025. Service providers deploy Time-of-Flight Diffraction and advanced corrosion-mapping crawlers, which are adapted to African field conditions. Compliance with API 653 and ISO 9712 sustains demand for certified inspectors and calibrated equipment. The resulting workload positions the South Africa NDT market as an indispensable risk-mitigation partner for petroleum operators.[1]Petro-Base Group, “Petro-Base Group South Africa,” petrobasegroup.com

Maintenance Needs of Aging Power Generation Assets

Eskom’s coal fleet averages over 40 years in service with availability below 51% in late 2024, compelling extensive condition assessments and weld integrity checks.[2]Laure de Nervo, “South Africa’s energy trap,” Crédit Agricole Études Économiques, etudes-economiques.credit-agricole.com TÜV Rheinland South Africa now performs high-temperature TOFD scanning on partially filled welds, enabling real-time repairs during outages. Wind farms add complexity to inspections because blade defects increase as installed capacity grows; newer projects, for instance, record seven blade repairs per turbine, thereby deepening long-term inspection workloads. These factors collectively enhance the relevance of the South African NDT market across both conventional and renewable power segments.

Regulatory Safety Compliance in Mining and Petrochemical Sectors

Mandatory Codes of Practice, effective October 2025, require mines to adopt SANS-aligned inspection programs and utilize SABS/SANAS-accredited laboratories. Conveyor belts, fire-suppression systems, and mobile machinery now require documented test evidence, enlarging the client base for qualified inspection firms. Certification adherence increases demand for ISO 17025 laboratories and technicians with Level II or higher qualifications. Immediate compliance needs are elevating short-term service backlogs and reinforcing the business case for outsourcing in the South Africa NDT market.

Expansion of Automotive Export-oriented Manufacturing

OEM investments, including Ford’s USD 275 million hybrid pickup expansion and Mercedes-Benz’s plug-in line upgrade, are heightening quality-control thresholds in the Eastern Cape and Gauteng corridors. Eddy-current and radiography methods verify weld seams, castings, and microdot security marks mandated by the 2024 National Road Traffic Amendment Act. Export homologation rules from the National Regulator for Compulsory Specifications require traceable inspection records, stimulating continuous testing contracts. As volumes rise, automotive plants integrate automated X-ray systems, further expanding revenue potential for software and service specialists.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of advanced equipment and skilled labour shortage | -1.4% | National, acute in rural and secondary cities | Medium term (2-4 years) |

| Cyclical capex cuts in mining and energy | -1.1% | Mining provinces: North West, Northern Cape, Limpopo | Short term (≤ 2 years) |

| Fragmented certification framework across industries | -0.7% | National regulatory inconsistencies | Long term (≥ 4 years) |

| Import duties and logistics delays for specialised consumables | -0.6% | Port-dependent regions, inland logistics hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Equipment and Skilled Labor Shortage

Imported phased-array systems and digital radiography units incur currency depreciation premiums and import duties that can double landed cost, discouraging capital spending by mid-tier providers. Technician shortages persist despite expanded training by the NASA Non-Destructive Academy of South Africa and SAIW; workforce pipelines require up to three years to produce competent Level II personnel.[3]South African Institute of Welding, “Eddy Current Testing (ECT): SAIW,” saiw.co.za Consequently, some mines import technicians on short-term contracts, which elevates service costs and prolongs inspection cycles in the South African NDT market.

Cyclical Capex Cuts in Mining and Energy

Commodity price downturns prompt miners to defer non-statutory inspections, reducing order visibility for testing firms. Similar spending constraints at Eskom hinder the adoption of predictive maintenance programs despite clear operational benefits. Although new mining safety codes require baseline inspection activity, the higher compliance costs can trigger further rationalization of marginal assets. These cyclical patterns impede steady revenue realization and temper the South Africa NDT market’s CAGR trajectory.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component – Services Dominance Reflects Outsourcing Trend

Services contributed 77.2% of the South Africa NDT market in 2024. The preference for contracting specialists stems from acute skills gaps and the need for surge capacity during plant shutdowns. Multi-disciplinary firms such as Steel Test manage assignments across Africa from their Vereeniging hub, leveraging approximately 74 staff. Software, albeit starting from a smaller base, is projected to grow at an 11.1% CAGR through 2030 as cloud data platforms and AI-enabled defect recognition become embedded into routine workflows. Equipment outlays remain sensitive to USD/ZAR volatility, prompting many users to opt for rental agreements. Consumables enjoy recurring demand but face periodic shipping delays for radioactive sources, which constrain turnaround times.

By Testing Method – Ultrasonic Leadership Amid Emerging Technologies

Ultrasonic testing accounted for a 25.9% revenue share in 2024. Its ability to perform volumetric weld assessments without radiation restrictions aligns with safety regulations across the mining and petrochemical industries. Phased-array and TOFD upgrades are extending capability into thick-wall and complex-geometry inspections. Eddy-current testing is forecasted to grow at an 8.1% CAGR due to rising adoption in aerospace fastener checks and aluminum body panels. Magnetic particle and liquid penetrant testing continue to serve ferromagnetic parts, whereas radiography remains a viable option for castings, despite logistical challenges associated with isotopes. Drone-assisted visual inspection is expanding its reach to wind towers and transmission lines, indicating a gradual broadening of the method mix within the South Africa NDT market.

By Technique – Traditional Methods Dominate Despite AI Advancement

Traditional techniques generated 86.3% of the revenue in 2024. Regulatory familiarity and established training pipelines underpin this advantage, particularly in high-risk environments such as those involving pressure vessels. AI-enabled solutions, however, are growing at a 14.2% CAGR. Stellenbosch University’s AI image-segmentation research demonstrates 30% faster flaw localization in industrial X-ray data, promising productivity gains. Adoption hurdles remain, most notably, integration costs and certification acceptance, but early wins in radiography and weld analytics suggest a progressive uptake through 2030.

By End-User – Oil and Gas Leadership Amid Automotive Growth

Oil and gas retained 23.4% of 2024 revenue, reflecting stringent integrity management across refineries, storage tanks, and pipelines. Automotive and transportation, benefiting from export-led plant expansions and new traffic-safety rules, is anticipated to chart a 7.9% CAGR. Power generation will stay a substantial client due to Eskom life-extension projects and renewable build-outs that require blade and tower inspections. Mining demand intensifies under the 2025 Codes of Practice, expanding the scope of mandatory inspections. Collectively, these sectors define a resilient opportunity set for the South Africa NDT market.

Geography Analysis

Gauteng dominates national demand through its dense cluster of mining headquarters, refineries, and aviation facilities. The African NDT Centre’s BINDT and NADCAP accreditations enable it to provide services to aerospace OEMs and MROs from its Johannesburg base. The Western Cape ranks second, driven by automotive manufacturing, port activities, and wind corridors requiring blade maintenance. Mpumalanga’s aging coal fleet generates consistent ultrasonic and radiographic workloads, whereas the Northern Cape’s solar and wind build-outs spur infrared and drone visual inspection assignments.

The Eastern Cape’s automotive corridor accelerates eddy-current and dimensional X-ray checks for vehicle exports. KwaZulu-Natal’s maritime hub supports hull thickness and refinery checks around Durban harbour. Free State gold mines and Limpopo’s platinum operations utilize magnetic particle and ultrasonic weld inspections, albeit with cyclical fluctuations tied to commodity prices. Across these provinces, load-shedding mitigation projects stimulate commissioning inspections of gensets and battery storage installations, broadening territorial penetration for the South Africa NDT market.

Competitive Landscape

The South Africa NDT market features moderate fragmentation. Gammatec NDT Supplies, under NTP Radioisotopes/NECSA ownership, controls a niche in isotope sourcing and equipment distribution; yet, no player tops a double-digit market share. Techtra holds exclusive regional distribution for Olympus, Magnaflux, and Sonaspection, helping equipment OEMs reach local service firms. Steel Test, African NDT Centre, and Quest Technical Services adopt multi-technology portfolios to win shutdown contracts across mines and power plants.

Strategic moves focus on technology differentiation. VisiConsult’s 2024 alliance with Bestbier Inspection Solutions introduced turnkey X-ray systems backed by local service capacity, signaling inbound investment from European OEMs.[4]VisiConsult, “VisiConsult partners with Bestbier,” onestopndt.com TÜV Rheinland’s high-temperature TOFD launch underscores specialization as a competitive lever. Providers targeting renewables and AI analytics occupy emerging white spaces, given the limited presence of incumbents. ISO 17025 and SANAS accreditation requirements raise entry barriers, favoring firms with mature quality systems and international approvals.

South Africa NDT Industry Leaders

SGS South Africa (Pty) Ltd.

Bureau Veritas South Africa (Pty) Ltd.

Applus+ Velosi South Africa (Pty) Ltd.

TUV Rheinland Inspection Services (Pty) Ltd.

Olympus South Africa (Evident Scientific)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: SAIW introduced an eddy-current testing course to alleviate technician shortages.

- March 2025: Mintek procured an arc/spark OES spectrometer to enhance analytical support for inspection programs.

- March 2025: Transnet issued a tender for ultrasonic inspection of a critical aviation-fuel pipeline.

- January 2025: TÜV Rheinland South Africa expanded into high-temperature TOFD weld testing.

South Africa NDT Market Report Scope

| Equipment |

| Software |

| Services |

| Consumables |

| Ultrasonic Testing |

| Radiographic Testing |

| Magnetic Particle Testing |

| Liquid Penetrant Testing |

| Visual Inspection Testing |

| Eddy-Current Testing |

| Acoustic Emission Testing |

| Thermography / Infrared Testing |

| Computed Tomography Testing |

| Traditional / Conventional |

| AI-enabled |

| Oil and Gas |

| Power Generation |

| Aerospace |

| Defense |

| Automotive and Transportation |

| Manufacturing and Heavy Engineering |

| Construction and Infrastructure |

| Chemical and Petrochemical |

| Marine and Ship Building |

| Electronics and Semiconductor |

| Mining |

| Medical Devices |

| Others |

| By Component | Equipment |

| Software | |

| Services | |

| Consumables | |

| By Testing Method | Ultrasonic Testing |

| Radiographic Testing | |

| Magnetic Particle Testing | |

| Liquid Penetrant Testing | |

| Visual Inspection Testing | |

| Eddy-Current Testing | |

| Acoustic Emission Testing | |

| Thermography / Infrared Testing | |

| Computed Tomography Testing | |

| By Technique | Traditional / Conventional |

| AI-enabled | |

| By End-user Industry | Oil and Gas |

| Power Generation | |

| Aerospace | |

| Defense | |

| Automotive and Transportation | |

| Manufacturing and Heavy Engineering | |

| Construction and Infrastructure | |

| Chemical and Petrochemical | |

| Marine and Ship Building | |

| Electronics and Semiconductor | |

| Mining | |

| Medical Devices | |

| Others |

Key Questions Answered in the Report

What is the forecast value of the South Africa NDT market in 2030?

The market is projected to reach USD 314.4 million by 2030.

Which component generates the highest revenue?

Services lead the revenue mix, accounting for a 77.2% share in 2024.

Which testing method is growing fastest?

Eddy-current testing is forecasted to expand at an 8.1% CAGR from 2025 to 2030.

How do new mining regulations influence demand?

Mandatory Codes of Practice, effective October 2025, compel accredited inspections, thereby expanding the client base for NDT providers.

Why is ultrasonic testing dominant?

Its volumetric flaw detection, which eliminates radiation hazards, suits power, mining, and petrochemical applications and contributed a 25.9% revenue share in 2024.

What limits faster market growth?

High equipment costs and a shortage of certified technicians are reducing the expansion pace, despite robust underlying demand.

Page last updated on: