Germany NDT Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

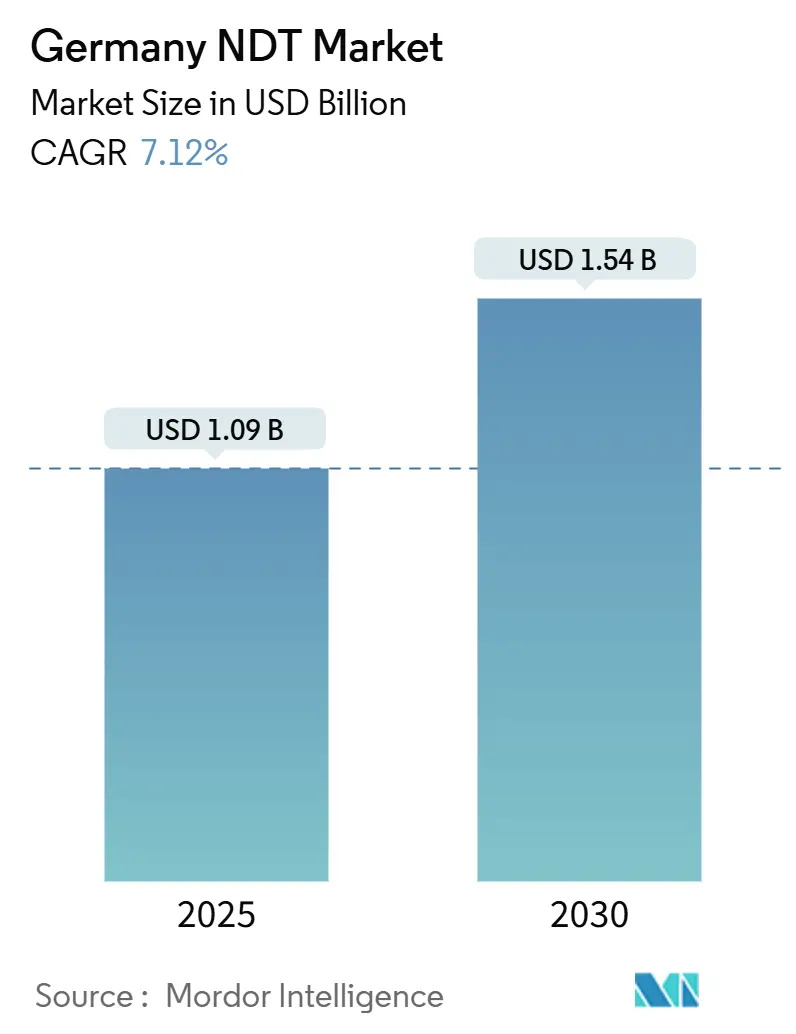

| Market Size (2025) | USD 1.09 Billion |

| Market Size (2030) | USD 1.54 Billion |

| Growth Rate (2025 - 2030) | 7.12% CAGR |

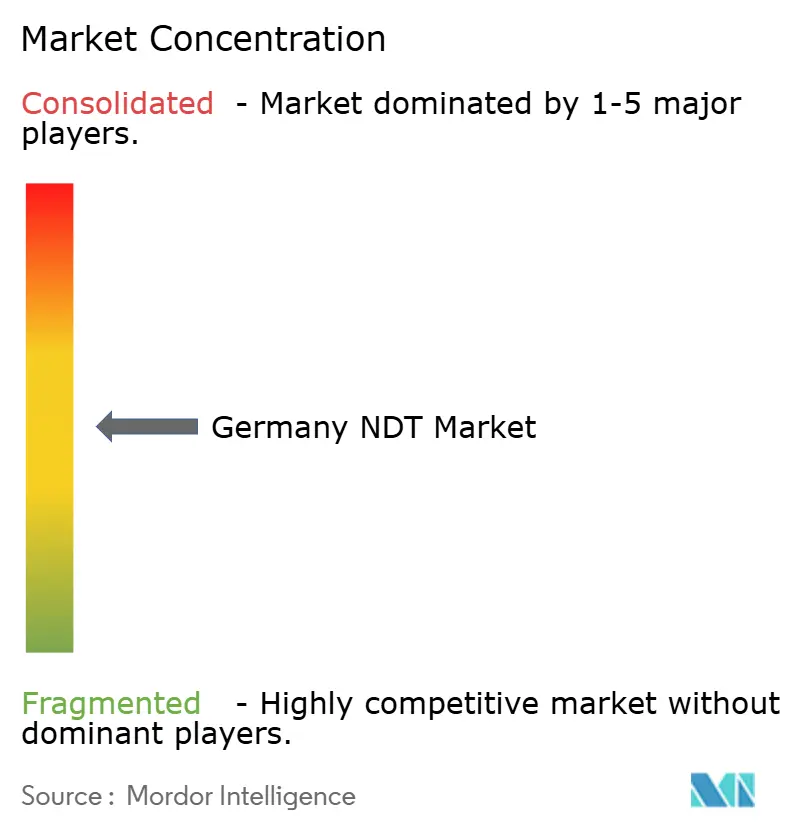

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany NDT Market Analysis by Mordor Intelligence

Germany's NDT market size stands at USD 1.09 billion in 2025 and is forecast to expand to USD 1.54 billion by 2030, translating into a 7.12% CAGR over the period. This trajectory reflects sustained capital expenditure on inspection solutions as German manufacturers align with stricter export quality rules, evolving EU safety directives, and data-driven production models. Industry 4.0 programs embed ultrasonic, eddy-current, and thermography sensors directly on the line, shifting nondestructive testing (NDT) from periodic audits to continuous monitoring. The rapid electrification of vehicle platforms drives demand for advanced battery-pack inspection, while turbine repowering and hydrogen infrastructure projects open up new service niches. Competitive differentiation centers on integrating software analytics and automation to offset certified labor shortages and reduce turnaround cycles, thereby ensuring established providers maintain pricing power in high-complexity applications.

Key Report Takeaways

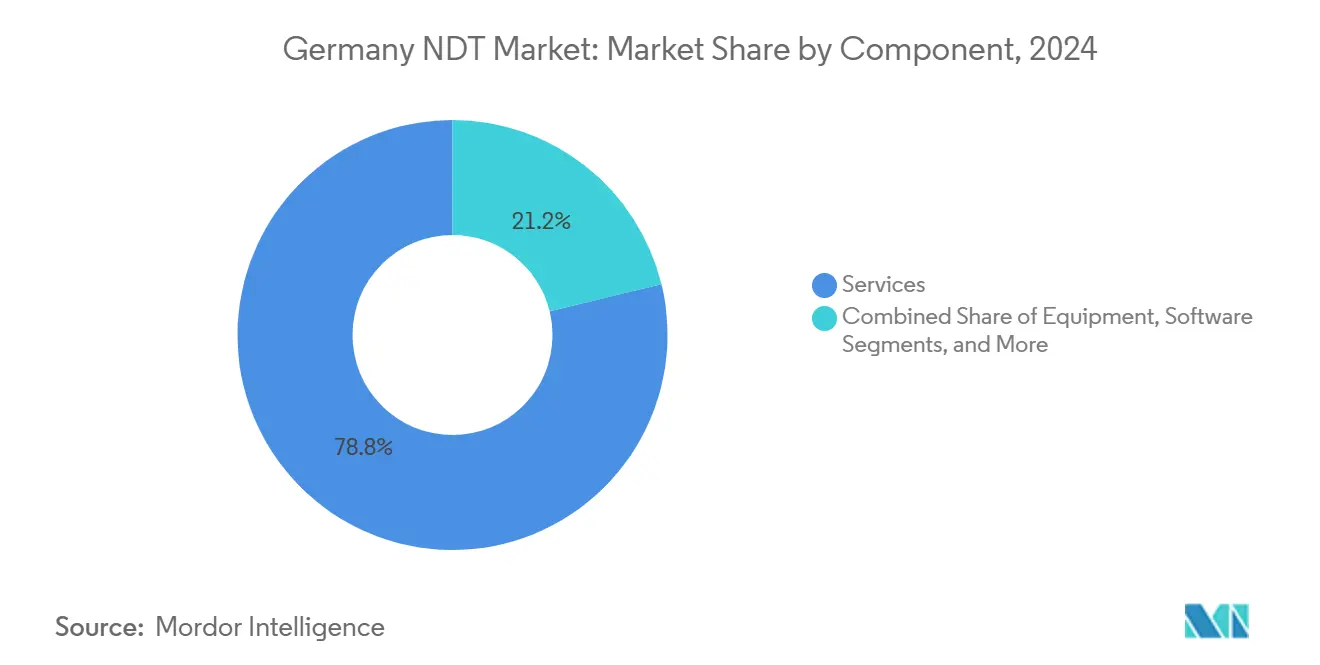

- By component, services led with 78.8% of Germany's NDT market share in 2024; software is projected to expand at an 11.4% CAGR through 2030.

- By testing method, ultrasonic testing accounted for a 27.5% share of the German NDT market size in 2024 and is projected to advance at a 6.9% CAGR through 2030.

- By technique, traditional methods held 87.9% of Germany's NDT market share in 2024, while AI-enabled systems are forecast to expand at a 14.5% CAGR to 2030.

- By end-user industry, the oil and gas sector accounted for a 25.1% share of the German NDT market size in 2024, whereas the automotive and transportation sector is projected to grow at an 8.3% CAGR to 2030.

Germany NDT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for quality assurance in German automotive exports | +1.8% | Baden-Württemberg, Bavaria, North Rhine-Westphalia | Medium term (2-4 years) |

| Mandatory periodic inspection norms under Druckgeräterichtlinie | +1.5% | Nationwide, industrial regions | Long term (≥ 4 years) |

| Repowering of aging onshore wind turbines | +1.2% | Northern and coastal Germany, Brandenburg | Medium term (2-4 years) |

| Adoption of Industry 4.0 enabled in-line NDT systems | +1.4% | Manufacturing hubs nationwide | Long term (≥ 4 years) |

| Defense aviation MRO capacity expansion at Bundeswehr sites | +0.8% | Military installations | Short term (≤ 2 years) |

| Hydrogen pipeline build-out requiring advanced inspection | +1.0% | Industrial corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Quality Assurance in German Automotive Exports

Vehicle shipments worth EUR 230 billion (USD 246.1 billion) in 2024 placed quality compliance at the center of production economics. Tier 1 suppliers introduced phased-array ultrasonic scanners into electric-vehicle battery lines to detect weld flaws in aluminum housings without halting the flow of cells. Automated computed-tomography (CT) cabinets now verify the dimensional integrity of cast e-motor frames within cycle times compatible with just-in-sequence assembly. Bosch embedded cloud-connected inspection dashboards across multiple plants, giving real-time defect maps that feed back into process controls.[1]DGZfP, “Quality Assurance Trends in Automotive Exports,” dgzfp.de As export regulations converge on zero-defect tolerances, OEMs treat advanced NDT as production infrastructure rather than an assurance afterthought, shifting budgets from capex on stand-alone rigs to multi-year service agreements that guarantee availability.

Mandatory Periodic Inspection Norms Under Druckgeräterichtlinie

Germany transposed the EU Pressure Equipment Directive into national law, mandating risk-based inspections for pressure vessels exceeding specified pressure limits. Operators that formerly relied on film radiography migrated to digital radiography and pulsed eddy-current techniques to comply with record-keeping and uptime targets. TÜV Rheinland documented a jump in vessel certificates issued after clients upgraded to guided-wave ultrasonics that inspect through insulation with the plant online. The rule’s staged deadlines extend beyond 2030, ensuring a steady queue of boilers, heat exchangers, and reactors that require recertification using validated NDT procedures.

Repowering of Aging On-Shore Wind Turbines

More than 25,000 turbines installed before 2010 approach design life, prompting operators to squeeze additional megawatt-hours while securing repowering permits. Blade inspection demand rose as thermographic drones mapped subsurface delamination in composite skins. ROSEN transferred pipeline acoustic-emission algorithms to tower weld monitoring, reducing rope-access labor by half. Grid operators scheduling foundation upgrades commission CT scans of flange bolts to validate preload retention under higher nacelle weights.[2]Bundesverband WindEnergie, “Repowering Roadmap 2025,” bwe.de The repowering cycle aligns with federal targets for growth in the share of renewable energy, anchoring a multi-year service pipeline for NDT contractors.

Adoption of Industry 4.0 Enabled In-Line NDT Systems

German factories utilize compact phased-array probes with on-board digitizers, designed by Waygate Technologies, which eliminates bulky cables and allows for the direct routing of raw A-scans into MES platforms. Machine-learning models classify defect signatures in milliseconds, guiding robotic welders to remediate misruns before they occur in downstream operations. Although GDPR limits cloud analytics on production data, domestic software houses offer on-prem inference engines that satisfy plant security teams. Continuous monitoring converts inspection data into predictive-maintenance inputs, reducing unplanned downtime while improving first-pass yield.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of certified NDT personnel (ISO 9712) | -1.2% | Germany, Austria, Switzerland | Medium term (2-4 years) |

| High CAPEX of high-energy CT and phased-array UT equipment | -0.9% | Nationwide, especially SMEs | Long term (≥ 4 years) |

| Data privacy restrictions are delaying AI model training | -0.7% | Nationwide, EU-wide implications | Short term (≤ 2 years) |

| Slow approval cycles for novel methods by Germanischer Lloyd | -0.4% | Maritime and offshore sectors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of Certified NDT Personnel

DGZfP recorded proctor queues exceeding six months for Level II phased-array exams, reflecting limited training slots and an aging technician cohort. Manufacturers that internalized inspection a decade ago now outsource to maintain production tempo, inflating service day rates. Universities have updated their curricula, yet advanced CT reconstruction and multi-modal algorithm modules remain electives, prolonging the ramp-up for new entrants. Companies, therefore, accelerate the adoption of automation to decouple throughput from manual certification bottlenecks.

High CAPEX of High-Energy CT and Phased-Array UT Equipment

A 450-kV micro-focus CT rig, along with a bunker retrofit, can exceed EUR 500,000 (USD 535,000) before installation. SMEs defer such investments, preferring mobile CT-as-a-Service vans developed by Fraunhofer IIS, which park outside the plant on demand.[3]Fraunhofer IIS, “Mobile CT-as-a-Service Concept Note,” fraunhofer.de While service rentals cut capital ties, batch scheduling may not suit takt-time assembly, forcing hybrid models where critical parts ship to centralized labs. Rapid sensor innovation further increases the risk of obsolescence, complicating ROI justifications for outright purchases.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Dominate Through Expertise Premium

Services accounted for 78.8% of Germany's NDT market share in 2024, reflecting industrial preference for third-party certification and the scarcity of ISO 9712 Level III resources. Large refinery turnarounds, avionics life-extension programs, and automotive launch validations all rely on multidisciplinary crews equipped with ultrasonic phased-array carts, digital radiography panels, and eddy-current arrays. The prevalence of outsourcing insulates end-users from capital expenditures while ensuring compliance traceability. Equipment revenue trails due to prolonged depreciation cycles, whereas consumable revenue grows steadily with routine inspection volumes.

Software exhibits the fastest 11.4% CAGR, propelled by AI-driven defect classification and cloud-native reporting that transform raw signals into actionable analytics. DRIVE NDT, DÜRR’s subscription platform, links probe IDs to weld maps and archives results for auditors, giving suppliers a clear path from inspection to part release. Services firms increasingly bundle such software within long-term framework agreements, generating recurring fees while lowering entry barriers for mid-tier manufacturers. In parallel, equipment vendors are launching pay-per-scan offerings to broaden coverage without straining cash flow, underscoring the service-centric pivot shaping the German NDT market.

By Testing Method: Ultrasonic Leadership Faces Eddy-Current Disruption

Ultrasonic testing held a 27.5% share of the German NDT market in 2024, due to its versatility across various materials, including steels, composites, and welds. Phased-array and total-focusing-method (TFM) units deliver sub-millimeter resolution, enabling single-sided inspection of complex geometries on power-train housings. Adoption continues in heavy engineering, but incremental growth moderates as most plants already own conventional sets. Eddy-current testing, however, is climbing at an 8.4% CAGR, favored for high-frequency inspection of thin aluminum sheets in electric-vehicle body-in-white lines and aircraft fuselage panels. Handheld array probes map crack propagation around rivet rows without surface preparation, aligning with takt-time constraints.

Radiography transitions from film to flat-panel digital, reducing dose and archiving files electronically, yet regulatory handling of ionizing sources limits penetration into SME workshops. Magnetic particle and liquid penetrant testing remain niche but indispensable for ferromagnetic forgings and leak-tight castings. Thermography benefits from drone-mounted cameras that sweep solar farms and wind blades, while CT retains premium status for electronics and additive-manufactured parts. Hybrid consoles combining UT, ET, and thermography are emerging, illustrating converging method boundaries —a trait that will define future competitive architectures across the German NDT market.

By Technique: AI-Enabled Systems Challenge Traditional Dominance

Traditional workflows still command 87.9 of % German NDT market share in 2024, underpinned by established codes and inspector familiarity. Standard operating procedures for weld UT or magnetic particle tests are deeply embedded in aerospace and petrochemical guidelines, making them difficult to displace overnight. Nonetheless, AI-enabled techniques are growing at a 14.5% CAGR as firms digitize to address workforce gaps and enhance feedback loops. Image-based neural networks now flag voids in composite parts within milliseconds, while anomaly-detection models trained on baseline signals trigger alarms in hydrogen pipelines long before leak thresholds are reached.

Regulators demand rigorous validation; therefore, suppliers conduct extensive round-robin trials with DGZfP before rolling out production. Early adopters cluster in high-volume automotive plants, where even fractional scrap reduction offsets algorithm licensing fees. In defense of MRO, AI supports defect trending over fleet life cycles, informing proactive interventions. Over time, algorithm quality and continuous-learning frameworks could outpace hardware as the primary value driver, marking an inflection point where the German NDT market prioritizes data stewardship above probe specification.

By End-User Industry: Oil and Gas Leadership Yields to Automotive Acceleration

Oil and gas retained 25.1 of % German NDT market share in 2024, reflecting pipeline girth-weld surveillance, refinery turnaround cycles, and LNG tank construction. High-resolution magnetic flux leakage pigs and guided-wave collars inspect hundreds of kilometers annually, underpinning a predictable baseline for service revenue. However, the automotive and transportation sector is expected to expand at an 8.3% CAGR through 2030, as electric-vehicle exports surge. Battery canisters rely on CT scans to confirm internal weld penetration, and lightweight aluminum chassis parts undergo eddy-current mapping to ensure structural integrity.

Power generation’s turbine rotor inspections and steam-cycle component audits sustain demand, while repowering projects in wind energy inject new work scopes for composite blade thermography. Aerospace benefits from Bundeswehr base overhauls and renewed narrow-body deliveries, necessitating the use of ultrasonic immersion tanks for complex titanium blanks. Chemical plants maintain corrosion-mapping campaigns, whereas rail and shipbuilding each exhibit cyclical scheduling aligned with fleet renewal. Electronics producers use micro-focus CT to detect voids in solder joints of high-density boards, reinforcing diversification across verticals that collectively stabilize the German NDT market.

Geography Analysis

Southern Germany anchors inspection demand through automotive and precision-engineering clusters in Baden-Württemberg and Bavaria. Stuttgart-area OEMs embed in-line phased-array bars in battery pack lines, while Munich aerospace suppliers run multi-modal CT labs to validate additive-manufactured parts. These regions host dense networks of DGZfP-accredited training schools, enabling rapid mobilization of certified personnel even under tight launch schedules. The concentration of tier-1 factories ensures continuous service calls, shielding local NDT providers from macroeconomic volatility.

North Rhine-Westphalia combines petrochemical plants in the Rhine corridor with heavy steel mills, generating high-value contracts for corrosion-under-insulation surveys and weld overlay inspections. Labs in Cologne leverage flat-panel digital radiography to certify thick-wall reactors during turnarounds, reinforcing a robust pipeline of outage-driven revenue. In eastern states such as Saxony and Brandenburg, wind-blade composites and rail-rolling-stock plants create pockets of specialized thermography and ultrasonic immersion testing. Federal subsidies for hydrogen research corridors further spread equipment sales as pilot pipelines install fiber-optic acoustic sensing.

Along the North Sea and Baltic coasts, offshore grid connections and shipyards underpin cyclic demand for underwater acoustic-emission systems and hull thickness gauging. Cross-border harmonization with Austria and Switzerland under the DACH framework facilitates inspector mobility, pooling scarce Level III expertise across wider catchment zones. Universities at Berlin’s BAM and multiple Fraunhofer hubs provide nationwide R&D support, ensuring geographic parity in the diffusion of technology. The distribution pattern reveals a mature yet regionally nuanced Germany NDT market, where service capability aligns with the industrial heat map rather than population density.

Competitive Landscape

The German NDT market remains moderately fragmented, with top service brands, such as TÜV Rheinland, DEKRA, and SGS Germany, dominating regulated inspections. Meanwhile, technology specialists, including Waygate Technologies, Institut Dr. Foerster, and ROSEN, control premium instrumentation. Recent consolidation sharpened solution breadth: Foerster acquired Prüftechnik NDT GmbH to merge eddy-current instrument leadership with vibration monitoring, and LK Metrology bought ProCon X-Ray to add micro-focus CT benches to coordinate-measuring-machine portfolios.[4]LK Metrology, “Purchase of ProCon X-Ray GmbH,” lkmetrology.com These tie-ups illustrate a strategic pivot toward full-stack offerings that bundle hardware, analytics, and contract services.

Competitive intensity lies in AI integration. Waygate embeds neural-network segmentation in Phoenix CT scanners, whereas DEKRA pilots cloud-edge inference engines on mobile ultrasonic carts. Smaller firms differentiate via niche capabilities: Microvista’s van-mounted CT rigs service foundries lacking bunker space, and Deeplify’s GDPR-compliant vision models attract privacy-sensitive automotive plants. Market entry barriers arise from ISO 9712 certification and DGZfP procedural validation, discouraging greenfield startups unless they target narrow applications such as drone-based thermography.

Pricing power persists in high-complexity sectors. Aerospace primes bundle inspection with life-extension analytics; oil majors sign multi-year pipeline integrity pacts; and automotive OEMs negotiate availability-based contracts where penalties apply for missed takt-time. Against this backdrop, personnel scarcity amplifies labor costs, urging incumbents to automate routine tasks and upskill remaining technicians. The resulting landscape is one where scale, certification depth, and data analytics prowess, rather than pure equipment counts, decide long-term leadership across the German NDT market.

Germany NDT Industry Leaders

TÜV Rheinland Industrie Service GmbH

SGS Germany GmbH

Applus RTD Deutschland GmbH

MISTRAS Group GmbH

Waygate Technologies (Baker Hughes Germany)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: LK Metrology acquired ProCon X-Ray GmbH, adding modular CT lines and extending metrology coverage from tactile probes to X-ray volumetric inspection.

- July 2025: VisiConsult X-ray Systems and Solutions GmbH purchased DEMA Dieter Enghausen Maschinenbau GmbH, safeguarding the supply of large radiation-protection cabins for aircraft and pipe-inspection.

- May 2025: Waygate Technologies showcased Phoenix V|tome|x M Neo high-resolution CT at Control 2025 in Stuttgart, underlining Germany’s pivotal role for advanced NDT launches.

- March 2025: Institut Dr Foerster completed the acquisition of Prüftechnik NDT GmbH, expanding global service reach and eddy-current R&D resources.

Germany NDT Market Report Scope

| Equipment |

| Software |

| Services |

| Consumables |

| Ultrasonic Testing |

| Radiographic Testing |

| Magnetic Particle Testing |

| Liquid Penetrant Testing |

| Visual Inspection Testing |

| Eddy-Current Testing |

| Acoustic Emission Testing |

| Thermography / Infrared Testing |

| Computed Tomography Testing |

| Traditional / Conventional |

| AI-enabled |

| Oil and Gas |

| Power Generation |

| Aerospace |

| Defense |

| Automotive and Transportation |

| Manufacturing and Heavy Engineering |

| Construction and Infrastructure |

| Chemical and Petrochemical |

| Marine and Ship Building |

| Electronics and Semiconductor |

| Mining |

| Medical Devices |

| Others |

| By Component | Equipment |

| Software | |

| Services | |

| Consumables | |

| By Testing Method | Ultrasonic Testing |

| Radiographic Testing | |

| Magnetic Particle Testing | |

| Liquid Penetrant Testing | |

| Visual Inspection Testing | |

| Eddy-Current Testing | |

| Acoustic Emission Testing | |

| Thermography / Infrared Testing | |

| Computed Tomography Testing | |

| By Technique | Traditional / Conventional |

| AI-enabled | |

| By End-user Industry | Oil and Gas |

| Power Generation | |

| Aerospace | |

| Defense | |

| Automotive and Transportation | |

| Manufacturing and Heavy Engineering | |

| Construction and Infrastructure | |

| Chemical and Petrochemical | |

| Marine and Ship Building | |

| Electronics and Semiconductor | |

| Mining | |

| Medical Devices | |

| Others |

Key Questions Answered in the Report

What is the current size of Germany’s non-destructive testing sector in 2025?

The sector is valued at USD 1.09 billion in 2025.

How quickly is Germany’s NDT sector projected to expand by 2030?

It is forecast to reach USD 1.54 billion by 2030, reflecting a 7.12% CAGR.

Which component category accounts for the largest spending share?

Services dominate with a 78.8% share in 2024 because most end-users rely on third-party certified expertise.

How does the automotive export segment influence NDT demand?

Export-oriented vehicle production drives the adoption of in-line phased-array ultrasonic and CT systems to meet stringent quality standards.

What impact does the shortage of ISO 9712-certified personnel have on German NDT providers?

Scarce Level II and Level III technicians drive up service prices and prompt companies to adopt greater automation.

Which testing methods are gaining traction for electric-vehicle parts?

Eddy-current arrays and computed tomography are rising fastest as they detect surface cracks and internal voids in lightweight battery and chassis components.

Page last updated on: