France NDT Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

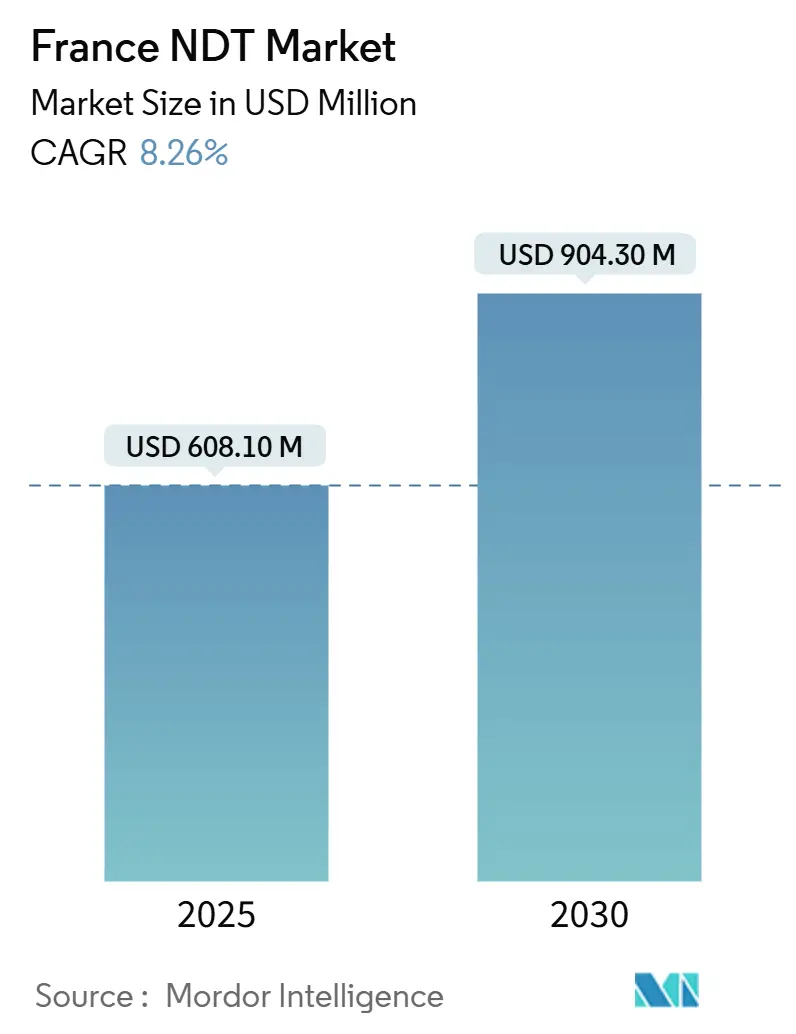

| Market Size (2025) | USD 608.10 Million |

| Market Size (2030) | USD 904.30 Million |

| Growth Rate (2025 - 2030) | 8.26% CAGR |

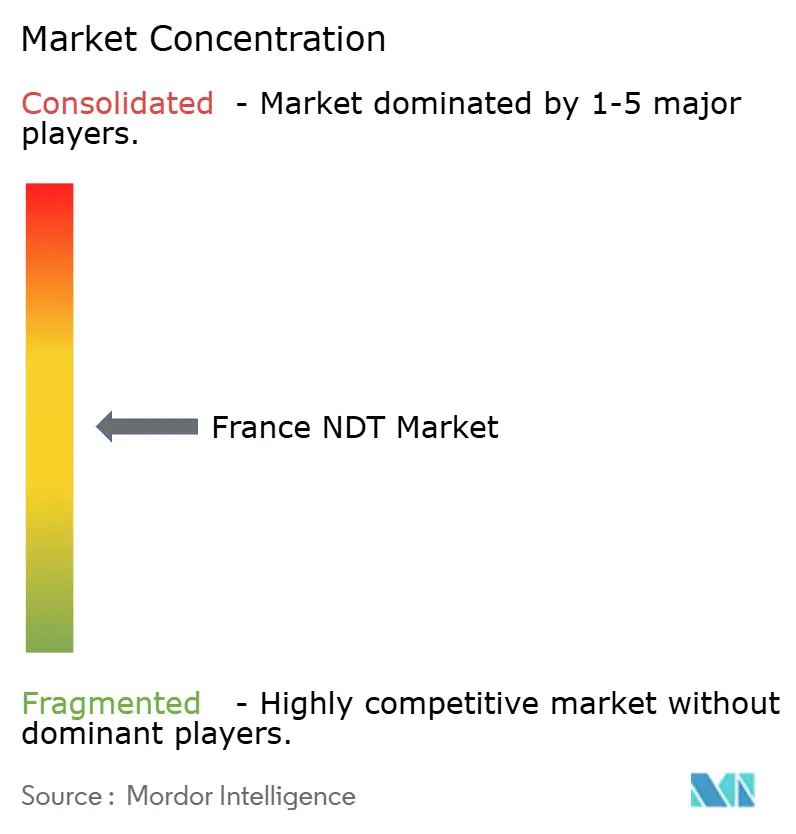

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France NDT Market Analysis by Mordor Intelligence

The France NDT market size stood at USD 608.1 million in 2025 and is forecast to expand to USD 904.3 million by 2030, reflecting an 8.26% CAGR driven by accelerated reindustrialization, nuclear life-extension programs, and stringent equipment‐safety regulations. Growth momentum is expected to benefit from 201 net industrial site openings in 2023, rising composite adoption in the aerospace sector, and sustained capital spending on offshore wind and pipeline integrity projects. Increasing digitalization, exemplified by AI-enabled ultrasonic platforms and predictive analytics, further lifts inspection volumes while moderating cost per test. Moderate market concentration encourages regional specialists to differentiate via advanced techniques, whereas multinationals acquire niche firms to secure domain expertise. Regulatory harmonization under the European Pressure Equipment Directive (PED) and EN ISO 9712 certification elevates service demand while ensuring inspection quality.

Key Report Takeaways

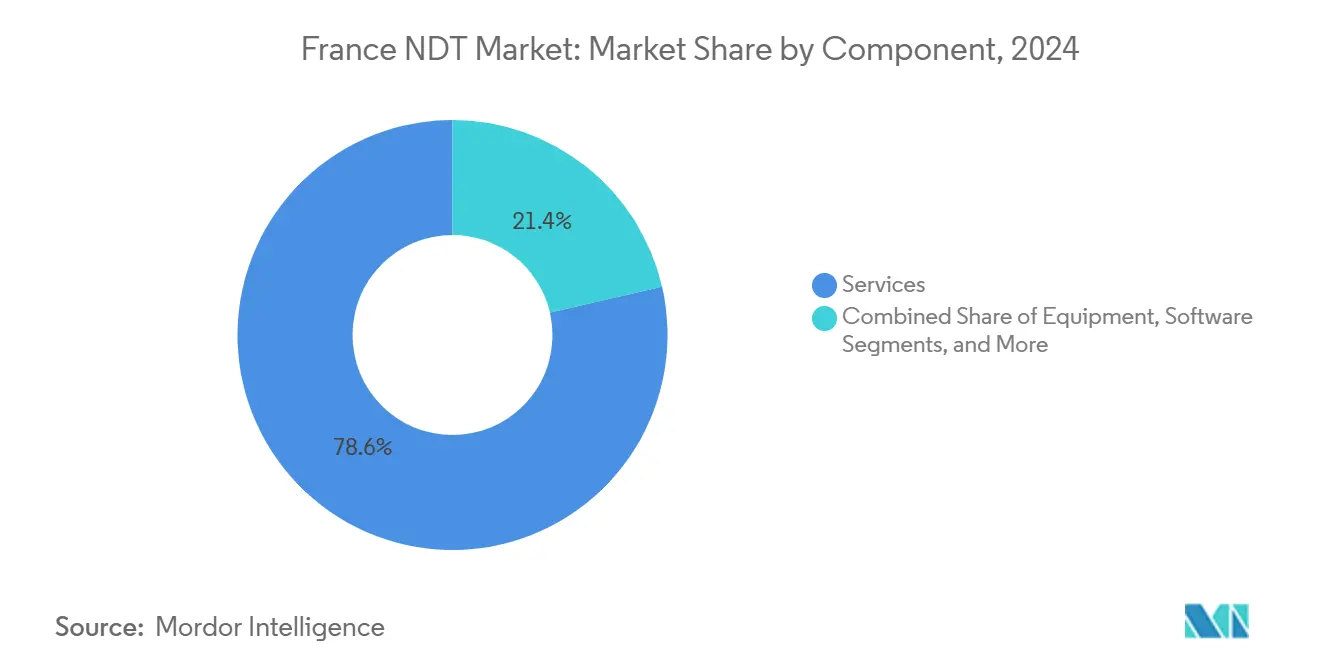

- By component, services held 78.6 of % France NDT market share in 2024, while software posted the fastest 13.1% CAGR through 2030.

- By testing method, ultrasonic accounted for 27.3% of the France NDT market size in 2024; eddy-current is projected to advance at a 10.1% CAGR between 2025-2030.

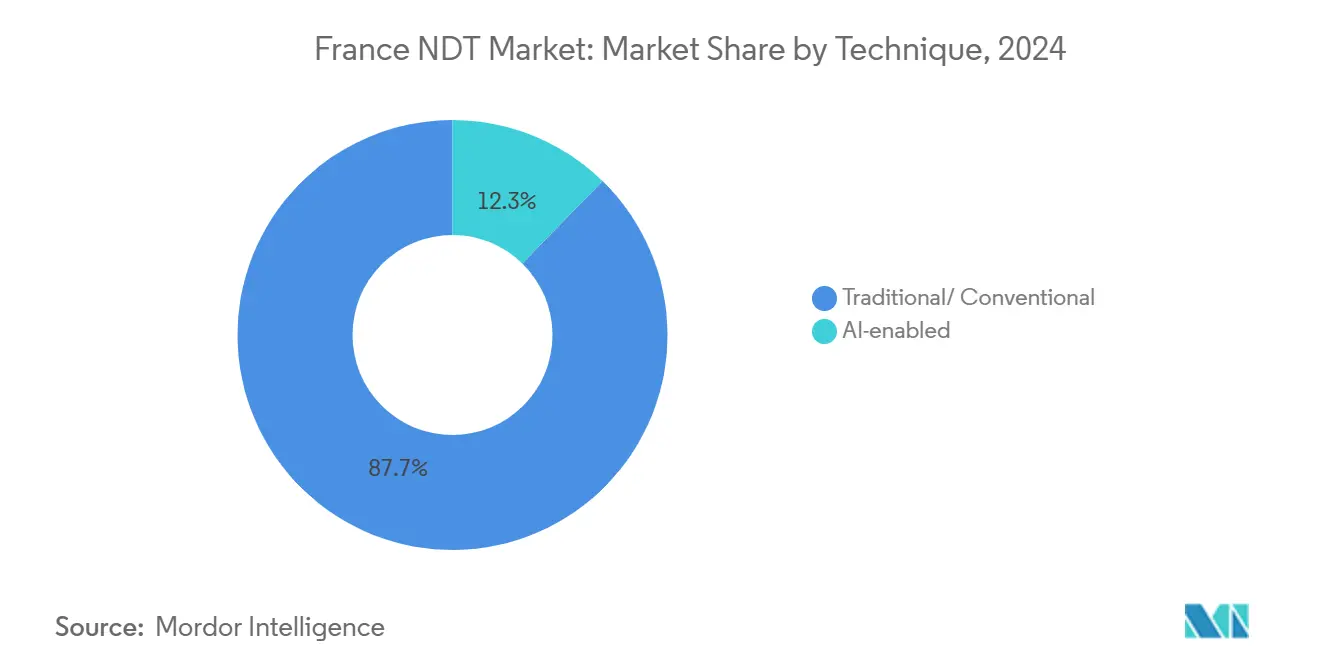

- By technique, traditional approaches dominated the France NDT market, with a 87.7% share in 2024; yet, AI-enabled solutions are rising at a 16.2% CAGR over the same horizon.

- By end-user, the oil and gas sector commanded 24.8% of the French NDT market size in 2024, while the automotive and transportation sector is projected to track a 9.9% CAGR to 2030.

France NDT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ageing power infrastructure life-extension demand | +2.1% | National, concentrated in nuclear regions | Medium term (2-4 years) |

| European PED compliance pressure | +1.8% | National, emphasis on industrial zones | Short term (≤ 2 years) |

| Surge in composite usage in aerospace programs | +1.4% | Toulouse, Bordeaux, and Paris aerospace clusters | Medium term (2-4 years) |

| Industry 4.0-driven on-site digital UT and analytics | +1.2% | Major industrial regions, Auvergne-Rhône-Alpes | Long term (≥ 4 years) |

| Offshore wind deployment – underwater inspection need | +0.9% | Atlantic and Mediterranean coastal regions | Medium term (2-4 years) |

| AI-enabled robotics to offset technician shortage | +0.8% | National priority in nuclear and aerospace hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ageing Nuclear Fleet Life-Extension Programs

France operates 56 reactors, averaging more than 35 years old, each subject to decennial in-depth inspections and 18-month interim checks that mandate extensive ultrasonic, eddy-current, and radiographic evaluations.[1]EDF, “Grand Carénage: Lifetime Extension of the French Nuclear Fleet,” edf.fr Lifetime-extension projects adopt phased-array UT for pressure-vessel welds and steam-generator tubes, generating steady multi-year workloads for qualified service providers. Government targets for 100,000 new nuclear jobs by 2030 expand the technician talent pool and boost training revenues. Regularized schedules create predictable cash flow, encouraging providers to invest in high-productivity automated scanners. AI-assisted image recognition shortens analysis times, enhancing throughput and freeing scarce experts for complex calls.

European PED Compliance Requirement

The European Pressure Equipment Directive requires the inspection of more than 10,000 French pressure installations, including annual routines, quinquennial external examinations, and 10-year out-of-service assessments. Compliance accelerates the demand for ultrasonic thickness measurement, magnetic particle testing, and digital radiography within chemical, petrochemical, and energy plants. Recent regulatory updates have tightened documentation rules, compressing operator timelines and driving the need for urgent outsourcing to COFREND-certified firms. SME operators lacking in-house capability rely on third-party teams, preserving the services skew of the France NDT market. PED adherence also steers investments toward data-rich techniques capable of generating auditable digital records.

Composite Surge in Aerospace Production

Airbus and its suppliers are scaling the use of carbon-fiber structures, thereby increasing demand for thermography, shearography, and computed tomography, which detect delamination and fiber misalignment.[2]Université Paris-Saclay, “FANTOM Project Summary,” univ-paris-saclay.fr TESTIA reports a rise in CT orders for wing covers and battery casings, while the FANTOM project funds automated robotic cells that combine ultrasonic and thermographic scans. Composite use spreads to electric vehicles, extending demand to automotive clusters in Hauts-de-France and Grand Est. Advanced inspection ensures that lightweight parts meet fatigue tolerance, a critical requirement for certifying next-generation aircraft and e-mobility platforms.

Industry 4.0 Digital UT and Analytics

France invests EUR 26.8 billion annually in plant modernization, catalyzing the adoption of cloud-linked ultrasonic arrays and predictive maintenance suites.[3]Cour des comptes, “10 ans de politiques publiques en faveur de l’industrie,” ccomptes.fr EXTENDE’s CIVA software integrates finite-element acoustic modelling with machine learning defect libraries, enabling virtual procedure qualification before field deployment. Start-ups such as Fluiidd embed AI into pipeline scanners, offering real-time corrosion mapping for water and petroleum lines. Automotive and aerospace OEMs now stream NDT data into enterprise resource planning systems, shortening decision cycles and underpinning zero-defect manufacturing goals.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital cost of radiographic and CT systems | -1.5% | National, particularly affecting SMEs | Short term (≤ 2 years) |

| Stringent radiation-safety approval timelines | -1.2% | National, nuclear, and industrial zones | Medium term (2-4 years) |

| Fragmented service landscape compressing margins | -0.8% | National, regional market variations | Medium term (2-4 years) |

| Low SME awareness of predictive maintenance ROI | -0.6% | Regional industrial clusters outside major metros | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost of Radiographic and CT Systems

Industrial CT units exceed EUR 500,000 (USD 545,000) after shielding and facility modifications, deterring SMEs from direct ownership. Service providers absorb depreciation by sharing capacity across multiple clients, reinforcing the dominance of services within the France NDT market. Leasing and pay-per-scan models emerge, yet they remain constrained by financing hurdles and training costs for operators. Capital intensity hinders the adoption of 3D CT in automotive prototyping and turbine-blade inspection, particularly outside aerospace clusters.

Stringent Radiation-Safety Approval Timelines

ASN authorization for new radiography bays typically lasts 12-18 months, requiring the development of exhaustive radiation protection plans, operator dosimetry, and regular emergency drills. Delays increase project costs, prompting users to consider ultrasonic or eddy-current alternatives that minimize exposure to ionizing radiation. Digital radiography rules introduced in 2024 promise dose reduction; however, additional validation studies are prolonging the certification process. Ongoing compliance includes periodic audits and dosimeter calibration, which adds fixed overhead to providers and limits entry for small firms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Sustain Dominance as Software Accelerates

Services captured 78.6% of the France NDT market in 2024, reflecting a business culture that outsources inspection to specialist contractors certified under COFREND and EN ISO 9712. Equipment demand remains stable in nuclear and aerospace factories, yet its share inches down as test benches stretch over long life cycles. Software is rising at a 13.1% CAGR as operators migrate to digital workstreams that integrate inspection with asset-management dashboards. The France NDT market size for software is expected to triple between 2025 and 2030, as cloud analytics enable predictive maintenance of turbines, pressure vessels, and rolling stock. Consumables remain resilient due to their continued use in legacy radiography, although digital conversion is gradually reducing the volumes of film and chemicals.

Digital twins created in EXTENDE CIVA cut qualification costs by simulating probe coverage before field trials, encouraging manufacturers to license software seats rather than buy additional hardware. Service providers expand subscription-based portals that log results, photographs, and videos for clients, adding sticky recurring revenue. Equipment revenues benefit from EDF’s inspection-robot renewal and aerospace CT upgrades, but price pressure keeps margins tight. A growing mix of software and data analytics reshapes skill requirements, pushing technicians toward hybrid IT-inspection roles.

By Testing Method: Ultrasonic Leads; Eddy-Current Gains Momentum

Ultrasonic testing accounted for 27.3% of the France NDT market share in 2024, due to its broad utility in weld inspection, pressure vessel integrity, and aircraft component control. Phased-array instruments and full matrix capture help image defects in thick nuclear steels and composite stacks. Radiography ranks second, being essential where volumetric coverage and permanent records are prized, notably in nuclear steam generator tubing. Eddy-current, registering the fastest 10.1% CAGR, benefits from automation and the ability to sense surface-breaking cracks under coatings, powering pipeline and heat-exchanger monitoring.

Thermography adoption is growing as infrared cameras become more affordable, allowing for rapid aircraft-skin surveys. Acoustic emission is explored for real-time bridge monitoring, complementing ultrasonic spot checks. Computed tomography, despite its high cost, is now standard for complex additive-manufactured aerospace parts, enabling dimensional metrology without the need for sectioning. Magnetic and liquid penetrant methods remain prevalent in automotive crankshaft factories due to their speed and cost advantages, although robotic spraying has improved repeatability. The diverse method mix lifts demand for multi-technique inspectors, stimulating advanced COFREND Level 3 certifications.

By Technique: Traditional Methods Prevail but AI-Enabled Inspection Accelerates

Traditional procedures held an 87.7% share in 2024, grounded in well-documented codes such as RSE-M for nuclear and EN 4179 for aerospace. Technicians and regulators favor proven reliability, creating a barrier to the adoption of disruptive tools. However, AI-enabled inspection exhibits a robust 16.2% CAGR as confidence grows in machine learning algorithms that flag anomalies faster than manual screen review.

EDF pilot projects with CIVA AI demonstrated improvements in defect detection for thick-section welds, prompting a gradual rollout across the fleet. Fluid’s scanner merges high-speed fluid dynamics with convolutional networks that identify pitting in pipelines in near real-time. Automotive OEMs deploy machine-vision systems on production lines to score spot-weld quality, reducing downstream rework. Standards bodies are drafting guidance for AI-assisted reporting that strikes a balance between human accountability and the benefits of algorithmic speed. Over the forecast window, AI adoption will shift inspector roles toward supervision and validation.

By End-User Industry: Oil and Gas Anchors Demand; Automotive Surges

Oil and gas generated 24.8% of France's NDT market revenue in 2024, driven by legacy refineries, 10,000 km of pipelines, and maturing offshore fields in the Channel and Mediterranean. Regular corrosion mapping, weld seam checks, and turnaround shutdowns generate constant call-offs for radiography and ultrasonic crews. Power generation, led by nuclear maintenance, follows closely, leveraging eddy-current arrays for steam-generator tubes and phased-array UT for reactor welds.

The automotive and transportation sector is the growth engine, with a 9.9% CAGR, spurred by electric-vehicle battery cell weld inspection, aluminum body quality checks, and composite part validation. Aerospace maintains premium pricing for CT and thermography on carbon-fiber wings and turbine-disk bores. Manufacturing and heavy engineering reap dividends from the government’s Territoire d’Industrie program, which finances turnkey plant sites needing commissioning inspections. Chemical facilities need PED compliance checks, while construction firms deploy acoustic emission sensors on bridges. Across sectors, predictive maintenance budgets are shifting spending from interval-based to condition-based inspections, aligning with the uptake of software.

Geography Analysis

The France NDT market clusters around Auvergne-Rhône-Alpes, which accounted for more than 35% of 2023 industrial site openings and about 40% of green industry investments, especially in battery gigafactories. Reactor locations in Centre-Val de Loire, Grand Est, and Normandy create enduring inspection baseloads, with multi-year outage calendars booked by Bureau Veritas and SGS crews. Occitanie, Nouvelle-Aquitaine, and Île-de-France host Airbus, Safran, and Dassault plants, driving composite and engine component NDT ranging from CT to shearography.

Coastal regions along the Atlantic and Mediterranean are witnessing the development of new offshore wind farms, whose subsea jackets necessitate automated ultrasonic and visual ROV surveys. Northern revitalization under France 2030 channels funds into EV driveline plants, tilting demand toward magnetic particle and eddy-current testing. COFREND sustains six regional committees to balance certification capacity with market needs, yet skills shortages persist outside nuclear corridors, leading to premium wage offers for Level 3 specialists.

Research infrastructure, including CEA LIST near Paris and ONERA labs in Toulouse, bolsters method innovation, encouraging start-ups to pilot AI-enabled probes locally before rolling them out globally. Variations in industrial mix dictate technique choice: ultrasonic and eddy-current dominate nuclear heartlands, while thermography and CT thrive in aerospace hubs. Emerging heavy-industry pockets in Hauts-de-France and Bourgogne are integrating digital inspection at the plant design stage, shortening qualification cycles and reinforcing demand for service-software hybrids.

Competitive Landscape

The France NDT market exhibits moderate concentration, with the top five players holding a significant combined share. Bureau Veritas leads through a diversified portfolio, reporting EUR 6.24 billion (USD 6.8 billion) in revenue for 2024, alongside 10 strategic acquisitions focused on sustainability and digital services. SGS leverages a nationwide lab footprint and petrochemical pedigree, while Apave maintains strength in construction and utilities. International equipment vendors Olympus and Waygate Technologies supply phased-array and CT systems, partnering with local integrators for support.

Technology investment differentiates competitors: EXTENDE’s CIVA 2025 release adds finite-element UT modules that shorten probe qualification cycles for SAFRAN and Naval Group. Vulcain Engineering’s acquisition of NAUDIN expands its nuclear machining expertise, aligning with the demand for reactor life extension.[4]Le Journal des Entreprises, “Vulcain Engineering Acquires NAUDIN,” lejournaldesentreprises.com White-space entrants like Fluiidd attract venture capital to commercialize AI-embedded scanners that enable unattended pipeline inspection, challenging legacy service models.

Margins tighten as commodity tasks become commoditized, pushing firms to bundle analytics and risk-based inspection advisory services. Certification remains a barrier; only providers with COFREND Level 3 staff and UISARE qualifications secure nuclear outage contracts. Cross-border opportunities emerge in Belgium and Spain, where French providers export expertise under mutual recognition schemes, diversifying revenue. The competitive field is expected to consolidate further as mid-tier firms seek scale to fund digital platforms.

France NDT Industry Leaders

SGS SA

Mistras Group Inc.

Eddyfi Technologies Inc.

Olympus Corporation

Zetec Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Bureau Veritas confirmed EUR 6.24 billion (USD 6.8 billion) 2024 revenue, 10.2% organic growth, and a new 2028 expansion roadmap emphasizing digital inspection.

- September 2025: Vulcain Engineering acquired Naudin, adding precision machining capacity for nuclear and naval programs.

- August 2025: EXTENDE rolled out CIVA 2025 with a full FEM UT engine, enhancing ultrasonic simulation accuracy.

- July 2025: Fluid secured EUR 1.2 million to industrialize AI-driven high-speed fluid scanners targeting oil pipelines by 2026.

France NDT Market Report Scope

| Equipment |

| Software |

| Services |

| Consumables |

| Ultrasonic Testing |

| Radiographic Testing |

| Magnetic Particle Testing |

| Liquid Penetrant Testing |

| Visual Inspection Testing |

| Eddy-Current Testing |

| Acoustic Emission Testing |

| Thermography / Infrared Testing |

| Computed Tomography Testing |

| Traditional / Conventional |

| AI-enabled |

| Oil and Gas |

| Power Generation |

| Aerospace |

| Defense |

| Automotive and Transportation |

| Manufacturing and Heavy Engineering |

| Construction and Infrastructure |

| Chemical and Petrochemical |

| Marine and Ship Building |

| Electronics and Semiconductor |

| Mining |

| Medical Devices |

| Others |

| By Component | Equipment |

| Software | |

| Services | |

| Consumables | |

| By Testing Method | Ultrasonic Testing |

| Radiographic Testing | |

| Magnetic Particle Testing | |

| Liquid Penetrant Testing | |

| Visual Inspection Testing | |

| Eddy-Current Testing | |

| Acoustic Emission Testing | |

| Thermography / Infrared Testing | |

| Computed Tomography Testing | |

| By Technique | Traditional / Conventional |

| AI-enabled | |

| By End-user Industry | Oil and Gas |

| Power Generation | |

| Aerospace | |

| Defense | |

| Automotive and Transportation | |

| Manufacturing and Heavy Engineering | |

| Construction and Infrastructure | |

| Chemical and Petrochemical | |

| Marine and Ship Building | |

| Electronics and Semiconductor | |

| Mining | |

| Medical Devices | |

| Others |

Key Questions Answered in the Report

How large is the France NDT market today?

The France NDT market size is valued at USD 608.1 million in 2025 and is projected to reach USD 904.3 million by 2030.

Which segment is growing fastest?

Software, driven by AI-enabled analytics, is projected to expand at a 13.1% CAGR between 2025 and 2030.

Why is ultrasonic testing dominant in France?

Ultrasonics’ versatility across nuclear, pipeline, and aerospace applications gives it a 27.3% market share, the highest among all methods.

How will PED regulations influence demand?

The European PED mandates periodic inspections of over 10,000 pressure systems, resulting in a 1.8% incremental increase to the market’s CAGR through 2030.

Which regions generate the most inspection work?

Auvergne-Rhône-Alpes leads due to battery gigafactories and industrial renewals, while Normandy and Centre-Val de Loire see steady nuclear inspection volumes.

Page last updated on: