Brazil NDT Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

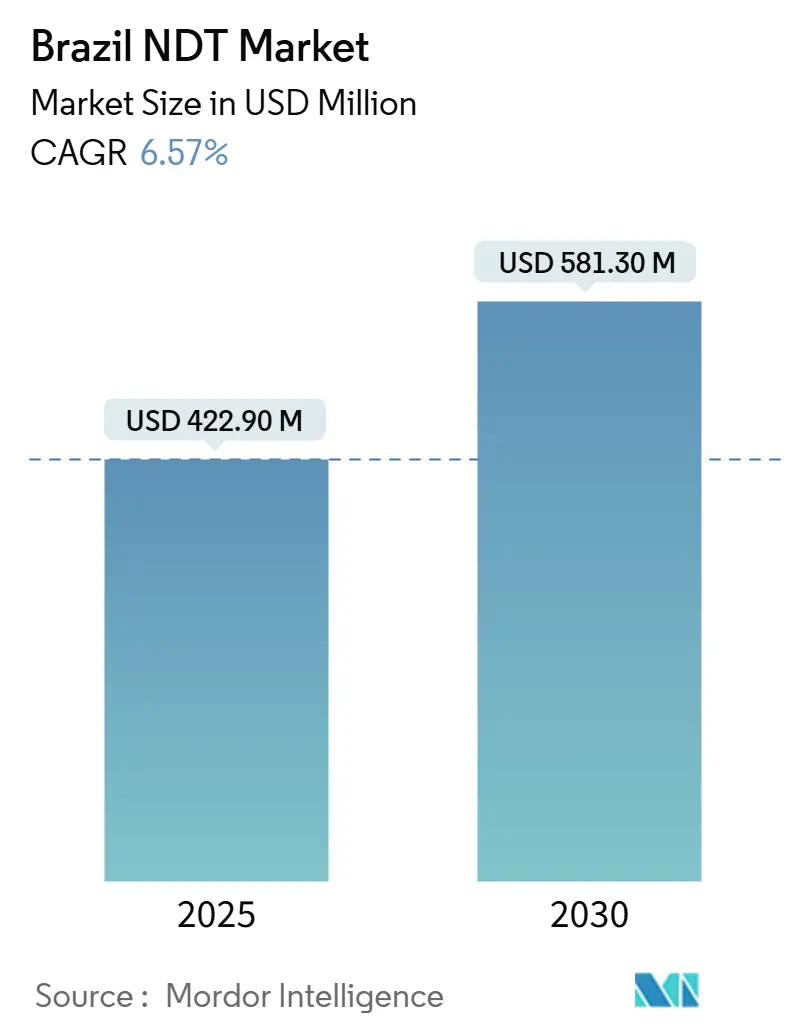

| Market Size (2025) | USD 422.90 Million |

| Market Size (2030) | USD 581.30 Million |

| Growth Rate (2025 - 2030) | 6.57% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil NDT Market Analysis by Mordor Intelligence

The Brazil NDT market size is valued at USD 422.9 million in 2025 and is forecast to reach USD 581.3 million by 2030, expanding at a 6.57% CAGR. Growth stems from stricter safety mandates in offshore oil activities, accelerating pre-salt exploration, and large-scale upgrades of aging power assets. Brazil’s deep industrial base in petrochemicals, aerospace, and automotive continues to commission complex inspection programs, while tax incentives for local NDT consumable manufacture and software-driven automation expand service possibilities. Competitive strategies focus on bundled service contracts, AI-enabled robotics, and joint ventures that secure regional talent pipelines. Persistent challenges around isotope import licensing and Level III professional scarcity outside the Southeast temper near-term adoption of advanced radiography, but also spur demand for remote monitoring and centralized expertise.

Key Report Takeaways

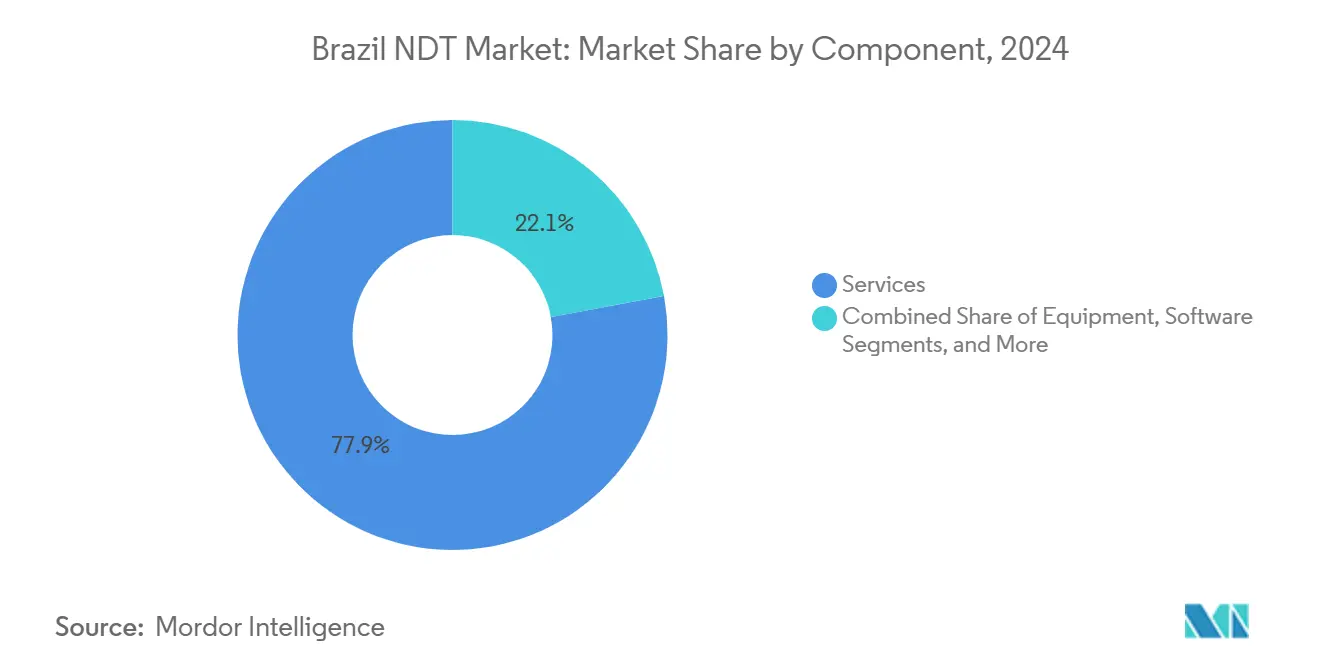

- By component, services held 77.9% of the Brazil NDT market share in 2024; software is projected to grow at a 9.9% CAGR through 2030.

- By testing method, ultrasonic testing is expected to lead with a 26.7% revenue share in 2024; eddy-current testing is expected to expand at a 6.9% CAGR through 2030.

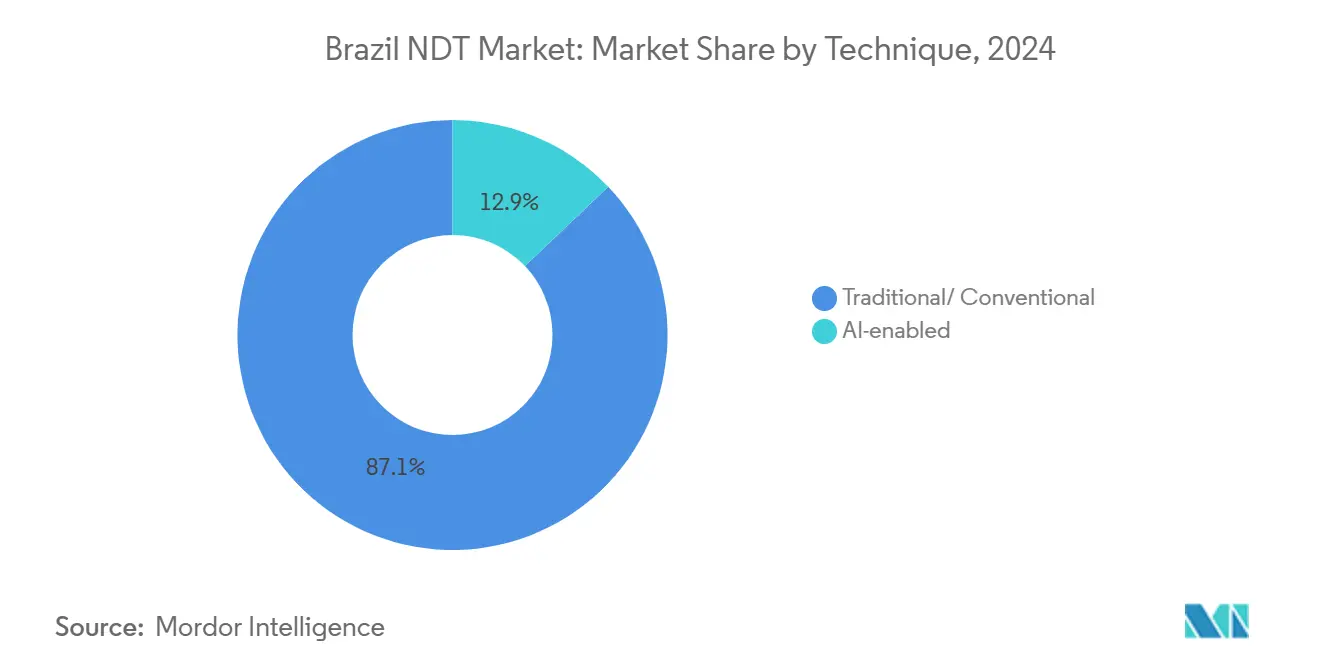

- By technique, traditional approaches accounted for an 87.1% share of the Brazilian NDT market size in 2024, while AI-enabled techniques are expected to advance at a 13.1% CAGR to 2030.

- By end-user industry, the oil and gas sector contributed 24.2% to the Brazil NDT market size in 2024; the automotive and transportation sector is growing at the fastest rate, with a 6.8% CAGR through 2030.

Brazil NDT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent safety regulations in the oil and gas industry | +1.8% | National – Rio de Janeiro and Espírito Santo | Medium term (2-4 years) |

| Aging infrastructure in power and petrochemical plants | +1.2% | National – São Paulo, Minas Gerais, Rio de Janeiro | Long term (≥ 4 years) |

| Expansion of offshore pre-salt exploration | +1.5% | Santos and Campos basins | Medium term (2-4 years) |

| AI-enabled ultrasonic robots in aerospace MRO hubs | +0.7% | São Paulo – São José dos Campos | Short term (≤ 2 years) |

| Tax incentives for local NDT consumables | +0.4% | Zona Franca de Manaus | Long term (≥ 4 years) |

| Lithium battery gigafactory investments | +0.6% | São Paulo, Minas Gerais, Goiás | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Safety Regulations in Oil and Gas Drive Compliance-Based Inspection Demand

Enhanced CNEN oversight of radiographic sources and Petrobras-specific integrity rules now obligate comprehensive ultrasonic and radiographic surveys on subsea pipelines, flowlines, and production units.[1]Engineering Directorate, “Safety Management in Pre-salt Fields,” Petrobras, petrobras.com.br Operators face non-discretionary inspection costs, even during periods of price volatility, which are often embedded in recurring service contracts. The regulatory push aligns with rising pre-salt output, ensuring the Brazil NDT market receives consistent work scopes tied to asset lifecycle integrity programs.

Aging Infrastructure in Power and Petrochemical Plants Accelerates Replacement Cycles

Thermal power stations and dams built in the 1970s and 1980s now exceed their design life thresholds. Utilities respond with tighter inspection intervals that employ phased-array ultrasonics, infrared thermography, and concrete integrity scans. Petrochemical complexes similarly combat corrosion in high-temperature loops, creating predictable demand for turnaround-based NDT programs that remain insulated from macroeconomic shifts.

Expansion of Offshore Pre-Salt Oil Exploration Creates Specialized Inspection Demand

Pre-salt wells lie beneath 2 km of water and 5 km of salt, exposing equipment to extreme pressures and corrosion. Diver-less robotic crawlers, real-time acoustic monitors, and advanced ultrasonics capture integrity data under these conditions, commanding premium pricing. Providers holding proven subsea credentials now enjoy high entry barriers that protect margins in the Brazil NDT market.

AI-Enabled Ultrasonic Robots Transform Aerospace MRO Operations

Embraer’s São José dos Campos campus pilots AI-guided scanners that inspect composite wings in minutes and cut technician hours by double-digits. Automation offsets Level III labor shortages and enhances inspection repeatability, encouraging airline MRO centers to transition toward software-centric service models that integrate defect images with digital twin records.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost of digital radiography equipment | -0.8% | Nationwide – pronounced in smaller centers | Short term (≤ 2 years) |

| Scarcity of certified Level III professionals outside the Southeast | -1.1% | North, Northeast, Center-West | Long term (≥ 4 years) |

| Import licensing delays for isotope sources | -0.6% | National | Medium term (2-4 years) |

| Legacy inspection data incompatibility with AI analytics | -0.4% | Established industrial facilities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of Digital Radiography Equipment Constrains SME Adoption

A complete digital X-ray set costs approximately BRL 177,800 (USD 34,200) at 2024 exchange rates, a level that exceeds the budgets of many small inspection firms. Limited financing and additional training expenses hinder the migration from film to digital, perpetuating a two-tier ecosystem where larger multinationals secure contracts that require advanced imaging.

Scarcity of Certified Level III Professionals Outside the Southeast Limits Regional Growth

The majority of ISO 9712 Level III holders reside in São Paulo and Rio de Janeiro. Projects in the North and Center-West must either fly in experts or endure delays while local technicians certify, which inflates service costs and lengthens shutdowns.[2]Regulatory Affairs, “ISO 9712 Certification Data 2025,” ABENDI, abendi.org.br Remote auditing and AI-assisted reviews partially mitigate gaps but cannot fully replace on-site presence in many regulated industries.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component – Services Retain Lead as Outsourcing Prevails

Services captured 77.9% of the Brazilian NDT market share in 2024, as energy majors and OEMs opted for turnkey inspection contracts over in-house staffing. Petrobras bundles personnel, equipment, and data interpretation inside multi-year frameworks that stabilize provider revenues. Software revenues, although modest, are rising at a 9.9% CAGR, driven by cloud-based dashboards that integrate ultrasonic, radiographic, and thermographic data for centralized decision support, thereby easing geographic talent mismatches.

Equipment outlays lag because advanced PAUT arrays, CT scanners, and digital radiography systems demand hefty capital and calibration budgets. Nonetheless, portable phased array sets and ruggedized thickness gauges gain traction among EPC contractors executing maintenance shutdowns. Software-centric business models, combined with remote monitoring, redefine value propositions, encouraging alliances between inspection houses and analytics vendors to safeguard data continuity.

By Testing Method – Ultrasonic Dominance Endures While Eddy-Current Gains Speed

Ultrasonic testing contributed 26.7% of Brazil's NDT market revenue in 2024, thanks to its cross-sector adaptability, which ranges from subsea pipeline welds to aerospace composite spars. Phased array and time-of-flight diffraction variants expand coverage, while thickness gauging remains a workhorse in power boilers. Eddy-current volumes grow at the fastest rate, with a 6.9% CAGR, driven by automotive EV motor manufacturing and electronics PCB flaw checks that rely on high-frequency surface probes.

Computed tomography and acoustic emission see niche adoption in battery cell validation and bridge cable monitoring, respectively. Radiographic testing still underpins critical weld acceptance, but it faces isotope sourcing delays and high shielding costs that tilt demand toward digital X-ray panels, where budgets allow. Visual inspection, augmented by drones and AI crack classifiers, closes the loop on first-line detection.

By Technique – Conventional Practices Prevail but AI Momentum Builds

Conventional techniques accounted for 87.1% of 2024 spending as risk-averse operators trust decades-proven film, MPI, or dye penetrant procedures. Yet, AI-enabled platforms advance at a 13.1% CAGR, especially in aerospace depots, where robotic scanners are being installed to map composite delaminations with pixel-level precision. Hybrid workflows—combining AI suggestions with human verification—speed up disposition decisions while satisfying regulatory requirements. Automotive plants utilize machine-learning algorithms on eddy-current signals to detect micro-cracks in drive shafts, thereby enhancing the first-pass yield.

Integration hurdles persist: legacy data often lacks the necessary metadata consistency for AI training, and regulators still require human sign-off on critical decisions. Even so, successful cases in aircraft wing inspections and refinery tank corrosion mapping reinforce confidence that AI augments, rather than replaces, skilled technicians.

By End-User Industry – Oil and Gas Leads, Automotive Rises Fast

Oil and gas supplied 24.2% of the 2024 value as pre-salt wells and FPSOs require life-of-field inspection programs that include subsea AWS crawlers and topside weld radiography. Exploration investments secured under recent production-sharing rounds provide multiyear visibility for inspection budgets. The automotive and transportation sector is the fastest-growing sector, with a 6.8% CAGR through 2030, as OEMs electrify their fleets, implement Industry 4.0, and tighten dimensional tolerances on lightweight alloys.

Aging hydro and thermal units in power generation underpin regular outage-driven testing, while Embraer’s global fleet keeps aerospace MRO lines busy with composite-centric NDT. Emerging segments, such as electronics and lithium battery gigafactories, demand CT and high-frequency ultrasound to ensure microstructural integrity, thereby diversifying revenue streams for providers willing to invest in specialized tooling.

Geography Analysis

Industrial density cements the Southeast’s dominance, with São Paulo hosting automotive giants, petrochemical complexes, and Embraer’s aerospace cluster. Rio de Janeiro anchors offshore oil integrity work, while Minas Gerais adds steel and mining throughput. High concentrations of certified personnel, laboratories, and training centers create a virtuous cycle that reinforces regional leadership in the Brazilian NDT market.

The Northeast accelerates on the back of wind corridors, solar parks, and port modernization. Blade composite inspections, inverter thermography, and CT scanning of battery casings top service lists as Bahia and Pernambuco expand industrial footprints. Regional authorities incentivize renewable projects, introducing new inspection mandates that smaller local firms can meet by upgrading to digital methods.

The North and Center-West corridors emerge through agribusiness logistics hubs, rail expansions, and mining beneficiation plants, yet they still suffer from Level III shortages.[3]Investment Promotion Agency, “Renewable Build-out Map 2025,” SEBRAE, sebrae.com.br Providers offering mobile rigs and remote-expert platforms win early contracts. Amazonian humidity and remoteness trigger demand for corrosion monitoring and drone-based visual scans, while Center-West grain terminals prioritize food-grade sanitary inspections uniquely tailored to agricultural machinery.

Competitive Landscape

Global TIC majors maintain Brazilian subsidiaries, leveraging international equipment fleets and standardized training curricula to enhance operational efficiency. Domestic specialists focus on regional networks and niche capabilities such as thermographic dam inspections or eddy-current rotor checks. Mergers like the proposed union of Bureau Veritas and SGS, valued at over USD 30 billion, could reconfigure market shares by combining complementary laboratories and client rosters.[4]Editorial Desk, “BV-SGS Merger Talks Advance,” OnestopNDT, onestopndt.com

Players differentiate through AI roadmaps, remote collaboration portals, and scholarship programs that seed future Level III cohorts. Subsea robotics suppliers partner with inspection companies to field diver-less crawlers, while software vendors license analytics engines that harmonize disparate data sets. Renewable energy and battery testing represent white-space arenas where early movers can emulate pre-salt service models.

Barriers to entry stay high: ISO 9712 certification, expensive CT tubes, and documented critical-service references safeguard incumbents. Yet digital disruption enables smaller software-first entrants to provide value without asset-heavy balance sheets, nudging incumbents to acquire or license algorithms that keep service bundles relevant.

Brazil NDT Industry Leaders

Mistras Group Inc.

SGS Brasil Ltda.

Olympus Scientific Solutions Americas do Brasil LTDA (Evident)

Eddyfi Technologies Inc. - Brazil

Zetec Inc. - Unidade Brasil

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: ABENDI and NDTSS sign an MoU to recognize personnel credentials and co-publish technical guides, fostering Brazil-Singapore standard harmonization.

- July 2025: Nissan América Latina introduces AI-powered risk mapping that saves USD 700,000 in downtime at its Brazilian plant, demonstrating cross-sector digitalization gains.

- June 2025: Timbro assumes operation of Jaguar Land Rover’s powertrain test laboratory in Itatiaia to serve multiple OEMs and create 30 jobs.

- January 2025: Bureau Veritas and SGS enter advanced merger talks valued at over USD 30 billion, a move that could reshape Brazil’s inspection services hierarchy.

Brazil NDT Market Report Scope

| Equipment |

| Software |

| Services |

| Consumables |

| Ultrasonic Testing |

| Radiographic Testing |

| Magnetic Particle Testing |

| Liquid Penetrant Testing |

| Visual Inspection Testing |

| Eddy-Current Testing |

| Acoustic Emission Testing |

| Thermography / Infrared Testing |

| Computed Tomography Testing |

| Traditional/Conventional |

| AI-enabled |

| Oil and Gas |

| Power Generation |

| Aerospace |

| Defense |

| Automotive and Transportation |

| Manufacturing and Heavy Engineering |

| Construction and Infrastructure |

| Chemical and Petrochemical |

| Marine and Ship Building |

| Electronics and Semiconductor |

| Mining |

| Medical Devices |

| Others |

| By Component | Equipment |

| Software | |

| Services | |

| By Testing Method | Consumables |

| Ultrasonic Testing | |

| Radiographic Testing | |

| Magnetic Particle Testing | |

| Liquid Penetrant Testing | |

| Visual Inspection Testing | |

| Eddy-Current Testing | |

| Acoustic Emission Testing | |

| Thermography / Infrared Testing | |

| Computed Tomography Testing | |

| By Technique | Traditional/Conventional |

| AI-enabled | |

| By End-user Industry | Oil and Gas |

| Power Generation | |

| Aerospace | |

| Defense | |

| Automotive and Transportation | |

| Manufacturing and Heavy Engineering | |

| Construction and Infrastructure | |

| Chemical and Petrochemical | |

| Marine and Ship Building | |

| Electronics and Semiconductor | |

| Mining | |

| Medical Devices | |

| Others |

Key Questions Answered in the Report

What is the size of the Brazilian NDT market in 2025?

The market is expected to reach USD 422.9 million in 2025 and is projected to increase to USD 581.3 million by 2030.

Which testing method generates the most revenue in Brazil?

Ultrasonic testing accounts for 26.7% of 2024 revenue, owing to its versatility in pipelines, composites, and power equipment.

What is driving the fastest growth in Brazil’s NDT end-user segments?

The automotive and transportation sectors lead with a 6.8% CAGR as electrification and Industry 4.0 elevate quality control needs.

Why do services dominate Brazil’s NDT spending?

Outsourcing avoids the fixed costs of equipment ownership and leverages third-party expertise, resulting in services accounting for a 77.9% share in 2024.

How are labor shortages being addressed?

AI-enabled robotics, cloud analytics, and remote expert platforms help mitigate Level III scarcity outside the Southeast.

What impact will the Bureau Veritas-SGS merger have?

Combining two TIC giants may concentrate expertise, widen service portfolios, and intensify competition for multinational contracts in Brazil.

Page last updated on: