Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

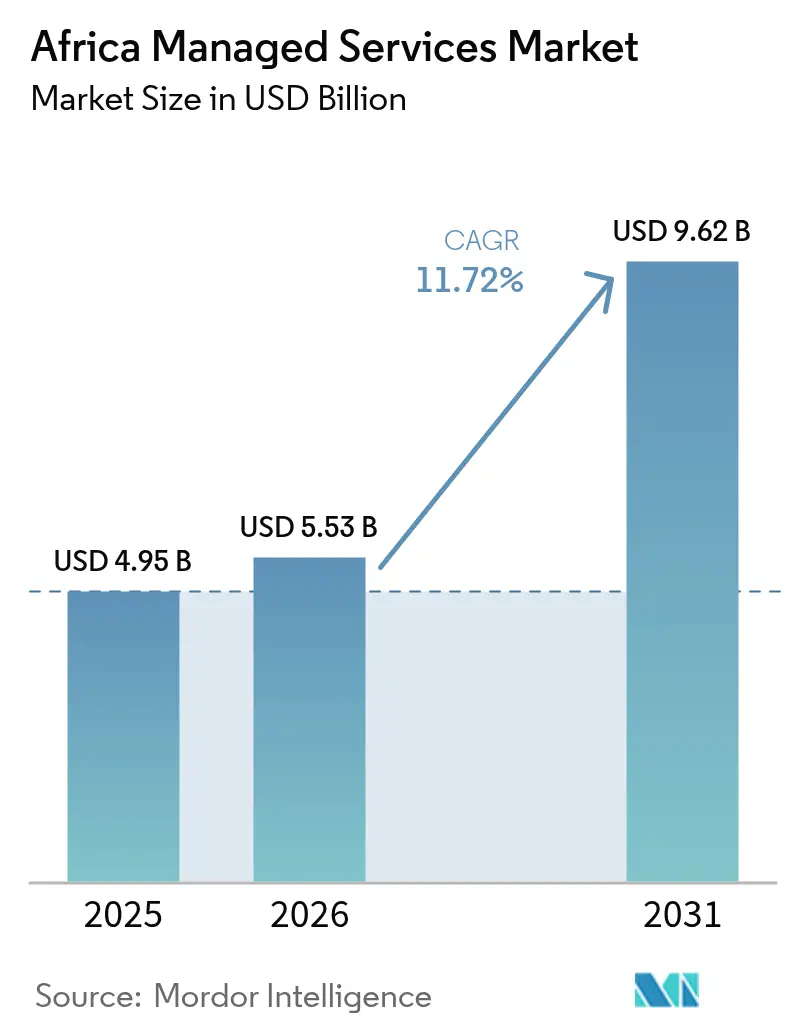

| Base Year Market Size (2025) | USD 4.95 Billion |

| Market Size (2026) | USD 5.53 Billion |

| Market Size (2031) | USD 9.62 Billion |

| Growth Rate (2026 - 2031) | 11.72% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Africa Managed Services Market Analysis by Mordor Intelligence

The Africa managed services market size was valued at USD 4.95 billion in 2025 and estimated to grow from USD 5.53 billion in 2026 to reach USD 9.62 billion by 2031, at a CAGR of 11.72% during the forecast period (2026-2031). Sustained expansion rests on sovereign data-residency rules, fast-growing pan-African fibre routes and an accelerating shift from capital expenditure to subscription-based IT procurement. Currency volatility simultaneously restrains new infrastructure outlays yet strengthens the business case for outsourcing as organisations limit balance-sheet risk. Intensifying cyber-crime that costs the continent nearly 10% of GDP each year further propels managed security spending. Competition remains active, with hyperscalers, regional telcos and specialist providers all seeking scale advantages across multiple high-growth verticals and underserved geographic niches.

Key Report Takeaways

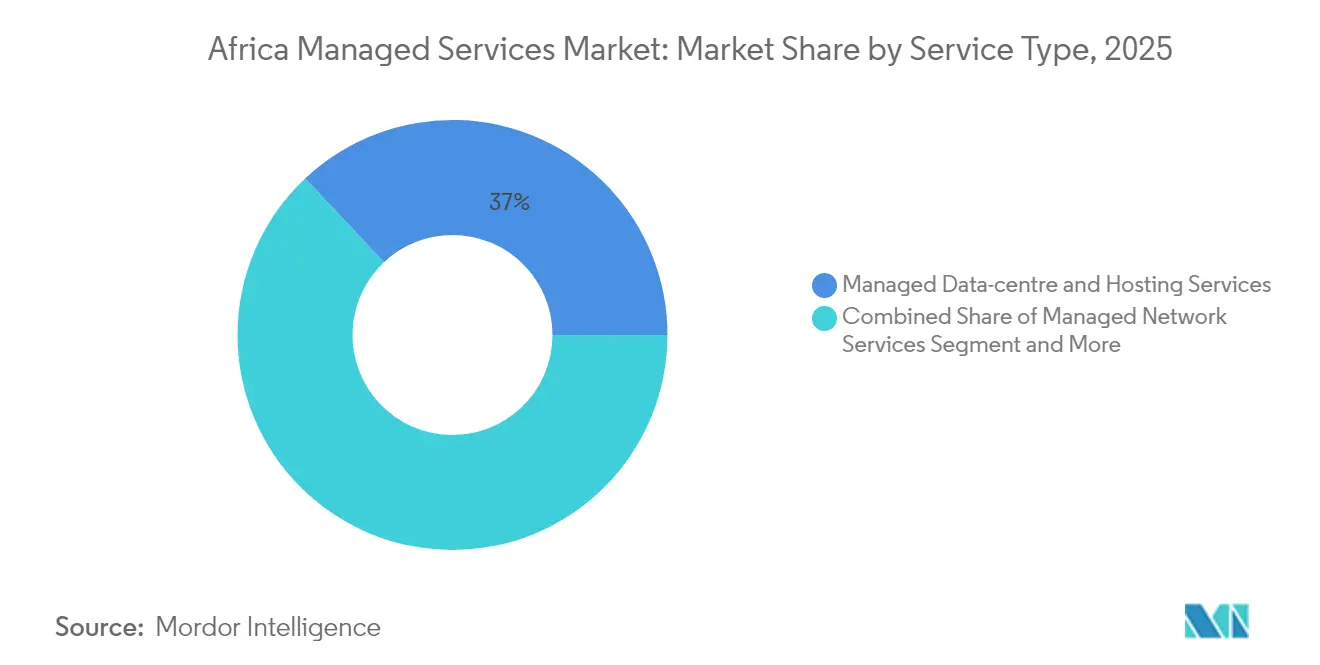

- By service type, managed data-centre and hosting services led with 37.02% of Africa managed services market share in 2025, while managed security services are advancing at a 12.28% CAGR through 2031.

- By deployment model, the public-cloud segment held a 76.65% share of Africa managed services market size in 2025 and is expanding at a 12.75% CAGR to 2031.

- By organisation size, SMEs captured 55.72% of Africa managed services market size in 2025; the segment is growing at 11.84% CAGR to 2031.

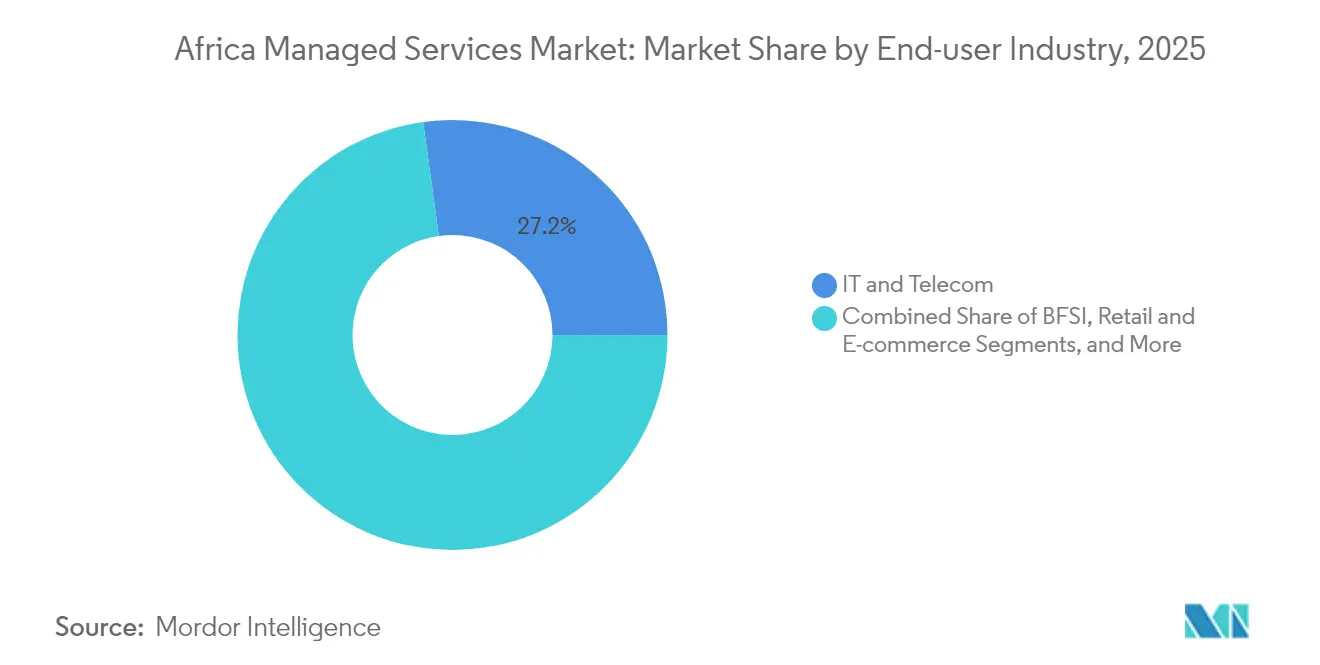

- By end-user industry, IT and telecommunications accounted for 27.18% revenue in 2025, whereas healthcare is set to grow fastest at 12.33% CAGR to 2031.

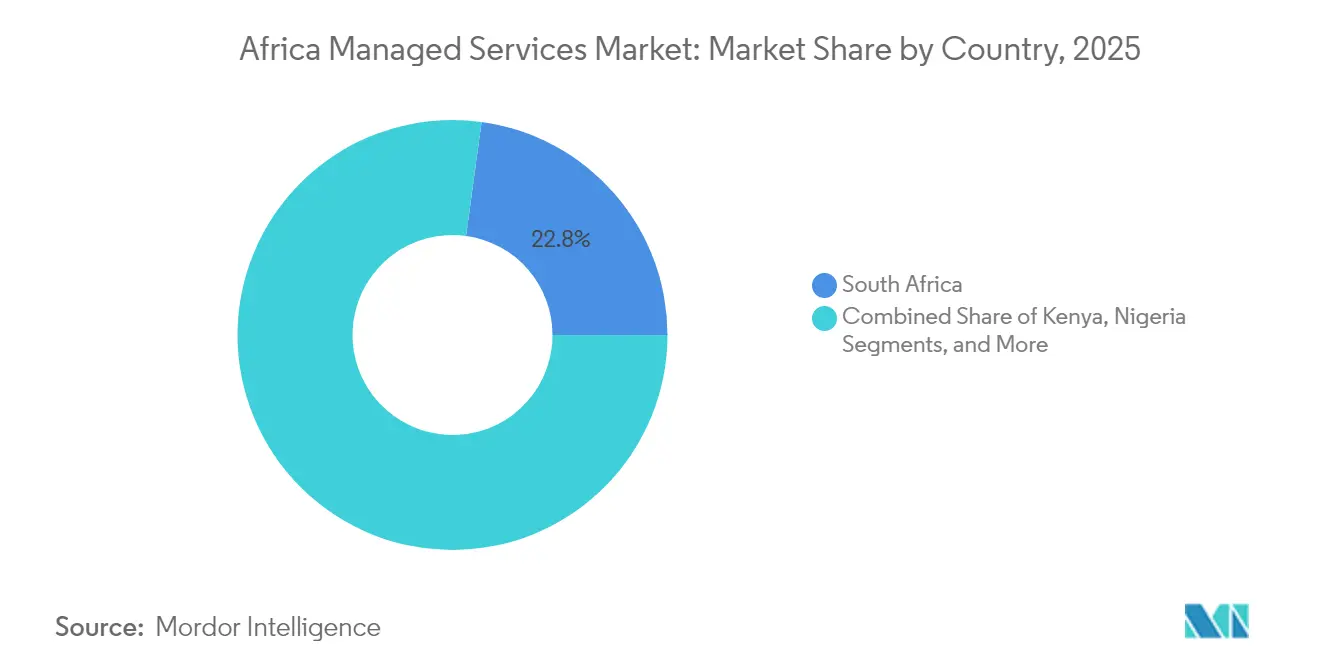

- By geography, South Africa commanded 22.84% market share in 2025, while Egypt records the highest forecast CAGR at 12.98% for 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Africa Managed Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Favorable trends in big data and analytics and growing ICT spend | +2.1% | Global, with concentration in South Africa, Kenya, Nigeria, Egypt | Medium term (2-4 years) |

| SME-led surge in managed cloud adoption | +2.8% | Global, strongest in Nigeria, Ghana, Kenya | Short term (≤ 2 years) |

| Rise of pan-African fibre networks lowering latency | +1.9% | Cross-border corridors, West-East Africa connectivity | Long term (≥ 4 years) |

| National data-sovereignty policies driving local MSP demand | +2.3% | Nigeria, South Africa, Egypt, Kenya | Medium term (2-4 years) |

| Mining and resource sector's OT-IT convergence needs | +1.2% | South Africa, Ghana, DRC, Zambia | Long term (≥ 4 years) |

| Greenfield smart-city projects requiring outsourced IT | +0.9% | Kenya (Konza), Nigeria (Eko Atlantic), Egypt (New Administrative Capital) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

SME-led Surge in Managed Cloud Adoption

Small and medium enterprises increasingly anchor the Africa managed services market as currency depreciation makes on-premises hardware unaffordable. Nigerian SMEs now choose naira-denominated cloud bundles that avoid foreign-exchange shocks, lowering total cost of ownership by up to 40%. Similar shifts appear in Ghana where a stronger cedi lets firms channel savings into subscription-based analytics platforms. Providers such as Nebula and Nobus use volume pricing to profitably serve thousands of small customers, fuelling predictable recurring revenue across the Africa managed services market. Scalable multi-tenant architectures let these MSPs maintain margins even as average contract value falls. Over the next two years, SME demand remains the most immediate growth catalyst for providers that can automate onboarding and support functions.

National Data-sovereignty Policies Driving Local MSP Demand

Domestic data-residency laws in Egypt, Nigeria, South Africa and Kenya have re-ordered procurement priorities. Egypt’s 120-petabyte Government Data and Cloud Computing Center anchors local workload hosting mandates and draws hyperscaler partnerships that reinforce the Africa managed services market.[1]Government Opens Egypt’s First Data Center,” Egypt Today, egypttoday.comFinancial institutions in Nigeria similarly divert workloads to local operators to comply with 2024 data-protection rules, granting indigenous MSPs strategic advantage. Liquid Intelligent Technologies posted 10.3% revenue growth after packaging compliance-ready cloud, connectivity and security services for regulated clients. As more governments formalise localisation, in-country capacity becomes a non-negotiable tender criterion, reshaping vendor shortlists and underwriting mid-term market expansion.

Rise of Pan-African Fibre Networks Lowering Latency

Submarine projects such as the 45,000-km 2Africa cable cut international bandwidth costs by up to 80%, driving a leap in cross-border application performance.[2]2Africa Cable Overview,” 2Africa Consortium, 2africacable.org Complementary terrestrial builds from WIOCC connect landlocked states, trimming latency by 40-60 ms and enabling centralised service delivery from fewer data centres. These network economics unlock new locations for backup, disaster recovery and AI inference workloads within the Africa managed services market. As construction phases complete over the next four years, providers can aggregate regional traffic into scale hubs, sharpening price competitiveness while sustaining quality of service for multinational clients.

Mining and Resource Sector’s OT-IT Convergence Needs

Underground Wi-Fi, autonomous haul trucks and sensor-laden conveyor belts have turned African mine sites into data-rich environments that outstrip traditional IT staffing models. Two Rivers Platinum’s partnership with Datacentrix illustrates the operational gains from real-time monitoring of critical equipment underground.[3]Datacentrix Delivers Underground Wi-Fi,” IM Mining, im-mining.com Managed service providers combining industrial protocols, cyber-safety and analytics deliver this functionality faster than in-house teams can acquire expertise. Demand is strongest in South Africa and Ghana where remote-operations mandates lift safety and productivity. Over the long term, specialised MSPs are set to carve defensible niches that broaden the addressable Africa managed services market beyond classic enterprise IT.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic power-supply instability increasing OPEX | -1.8% | Sub-Saharan Africa, excluding South Africa | Short term (≤ 2 years) |

| Data-privacy and cybersecurity skill gaps | -1.1% | Global, most acute in Central and West Africa | Medium term (2-4 years) |

| Slow cross-border bandwidth upgrades in Central Africa | -0.7% | Central African Republic, Chad, Cameroon, Gabon | Long term (≥ 4 years) |

| Depreciating local currencies squeezing ICT budgets | -2.2% | Nigeria, Ghana, Kenya, Zambia, Egypt | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Chronic Power-supply Instability Increasing OPEX

Frequent outages mean Nigerian data centres operate diesel generators 8-12 hours daily, driving energy bills 60-80% higher than grid-reliant peers and compressing margins across the Africa managed services market. South Africa’s scheduled load-shedding still forces dual-feed designs that raise capital outlays. Providers deploy battery storage and micro-grid solutions yet capital intensity limits entry for smaller firms. Clients also bear hidden costs through higher connectivity pricing as operators amortise redundancy investments. Although renewable deployments promise relief, unreliable power remains the single largest operational expense headwind through 2027.

Depreciating Local Currencies Squeezing ICT Budgets

Twenty-one African currencies are set to weaken against the US dollar in 2025, inflating the landed cost of imported equipment and cloud licences. MTN Nigeria signalled profits could fall 90% after naira losses, illustrating the revenue shock to key MSP customers. Enterprises now demand local-currency contracts, shifting forex risk onto service providers inside the Africa managed services market. Some MSPs respond by structuring variable-price clauses or sourcing regionally produced hardware. While depreciation elevates outsourcing’s appeal by deferring capital spend, it also curbs near-term budget headroom, making flexible payment models a competitive necessity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Security Services Accelerate Past Infrastructure

Managed data-centre and hosting services retained the largest 37.02% revenue slice in 2025, underscoring infrastructure’s foundational role. Managed security solutions, however, are growing at 12.28% CAGR, elevating their importance within the Africa managed services market. Heightened attack frequency against banks and telcos drives continuous monitoring, incident response and zero-trust architecture demand. The Africa managed services industry also benefits from chronic cybersecurity talent shortages, prompting enterprises to outsource advanced protection stacks.

Increasing ransomware claims spur regulatory scrutiny, bolstering spend on compliance-aligned managed detection and response. At the same time, multi-tenant SOC platforms allow providers to amortise tooling across dozens of clients, lifting margins. As African boards attach financial penalties to breaches, security retainer contracts lengthen from annual renewals to multi-year-plus extensions, embedding steady cash flow into the Africa managed services market.

By Deployment Model: Public Cloud Dominance Masks Hybrid Shift

Public cloud captured 76.65% of 2025 revenues and is projected to climb with a 12.75% CAGR, yet data-sovereignty rules catalyse a pivot toward hybrid frameworks. Nigerian firms now blend hyperscale compute with local nodes to comply with residency mandates without sacrificing elasticity. Providers integrate edge devices and regional availability zones to maintain sub-50 ms latency for consumer applications, demonstrating the Africa managed services market’s agility.

Private cloud persists in heavily regulated banking and government workloads where direct control remains paramount. Hybrid orchestration tools from Microsoft and VMware thus experience rising adoption, indicating that deployment decisions are becoming workload-specific rather than binary. Over time, hybrid models are likely to narrow the public-cloud share even as absolute volumes expand, reshaping architecture design principles within the Africa managed services market.

By Organisation Size: SMEs Drive Market Transformation

SMEs accounted for 55.72% of the Africa managed services market share in 2025 and will expand at 11.84% CAGR to 2031 as subscription-priced ERP, CRM and analytics platforms reach mass affordability. Bundled voice, connectivity and cloud security offerings lower barrier-to-entry for firms with limited in-house skills. Providers employing AI-driven self-service dashboards minimise support costs while improving transparency.

SME scale compels MSPs to automate ticketing, patching and billing to remain profitable at lower average revenue per user. This volume-oriented playbook contrasts with enterprise-focused bespoke engagements and tilts competition toward those able to fund platform development. By 2030, micro-enterprises employing under 20 staff are expected to represent a third of total contracted endpoints, cementing SMEs as the structural growth engine of the Africa managed services market.

By End-user Industry: Healthcare Transformation Accelerates

Digital health outlays are soaring as telemedicine platforms bridge clinician shortages of 1.55 per 1,000 people. The sector’s 12.33% CAGR outpaces all others and relies on MSPs for HIPAA-like data protection, real-time imaging and remote-device management. Hospitals leverage outsourced SOCs to guard against ransomware that threatens patient safety, positioning healthcare as a priority sub-segment.

IT-telecom retook spending leadership with 27.18% of 2025 revenues, leveraging in-house expertise to co-design customised network and edge solutions. Banking and financial services follow closely due to rising mobile-money penetration and stringent compliance obligations. Together these industries deepen vertical specialisation across the Africa managed services market, encouraging providers to acquire domain-specific certifications.

By Country: Egypt’s Infrastructure Investment Drives Growth

South Africa held 22.84% revenue share in 2025 but Egypt will post the fastest 12.98% CAGR thanks to its USD 2.7 billion 5G build-out and 120-petabyte government cloud. Strategic geography linking Europe, Asia and Africa plus newly manufactured fibre cables in Ain Sokhna underpin Egypt’s hub ambitions.

Nigeria’s depreciation shock slows imported-gear purchases, yet spurs ingenuity as local MSPs create naira-priced bundles. Kenya capitalises on the 2Africa landing and AI Strategy 2025-2030 to attract data-science workloads, while Ghana’s stronger currency gives SMEs fresh purchasing power. Collectively, these trajectories reinforce the need for providers to balance local footprints with regional breadth across the Africa managed services market.

Geography Analysis

South Africa combines advanced telecoms, skilled labour and relative regulatory clarity to act as a continental springboard. Microsoft’s ZAR 5.4 billion hybrid-cloud investment demonstrates confidence in long-term demand, even as load-shedding mandates multi-feed power designs that inflate costs. Johannesburg and Cape Town data-centre clusters already host most regional disaster-recovery sites, reinforcing market gravity.

Egypt delivers the fastest expansion underpinned by state-backed infrastructure programmes and a goal of USD 9 billion outsourcing revenue by 2026. Situated on critical subsea cable crossroads, the nation provides single-digit-millisecond latencies to Gulf and European customers, encouraging MSPs to locate regional SOCs and multilingual support centres there.

Kenya, Nigeria and a wide Rest-of-Africa grouping together form a diversified growth frontier for the Africa managed services market. Kenya’s Konza Technopolis pilots smart-city managed services; Nigeria’s vast addressable base is tempered by foreign-exchange volatility; and Ghana plus Rwanda illustrate how favourable policy reforms can accelerate digital adoption. Cross-border fibre corridors increasingly let providers serve multiple states from a single metro, enabling economies of scale.

Competitive Landscape

Competition is balanced between global hyperscalers, regional telecom-affiliated MSPs and agile local specialists. IBM, Microsoft and Cisco pursue enterprise contracts that demand integrated AI, security and network solutions, using global reference sites as proof points. Liquid Intelligent Technologies, MTN Business and BCX leverage local points-of-presence and currency billing to undercut imports and comply with residency laws.

Partnership ecosystems widen the field: Liquid C2’s tri-party agreement with Google Cloud and Anthropic layers generative AI atop African-resident infrastructure, while MTN and Huawei’s Joint Innovation Lab aligns 5G and cloud advances for pan-African roll-outs. Emerging cloud start-ups focus on cost-led disruption—especially in Nigeria where naira pricing resonates.

Consolidation remains plausible as platform scale becomes key to funding automation and energy-efficient facilities. Nonetheless, regulatory diversity and currency risk deter a single entity from dominating, ensuring that the Africa managed services market retains a moderately fragmented character over the medium term.

Africa Managed Services Industry Leaders

Cisco Systems

IBM Corporation

Accenture PLC

Fujitsu Ltd.

HP Development Company LP

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Orange partnered with Eutelsat OneWeb to extend low-earth-orbit satellite services across remote African regions, enhancing MSP reach.

- June 2025: PCCW Global, Sparkle, Telecom Egypt and ZOI commenced AAE-2 subsea-cable construction to link Asia, Africa and Europe.

- May 2025: Orange and International Finance Corporation launched a multi-country digital-transformation programme, opening fresh MSP project avenues.

- May 2025: Cassava Technologies and Nvidia unveiled plans for Africa’s first AI factory in South Africa, with future sites in Egypt, Kenya, Morocco and Nigeria.

- May 2025: Kenya published its AI Strategy 2025-2030, setting regulatory guardrails favourable to AI-centric managed services.

Africa Managed Services Market Report Scope

Managed services are outsourcing on a proactive basis, with specific processes and functions intended to improve operations and cut expenses. They simplify IT operations, increase user satisfaction, and enhance service quality while reducing operating costs. Managed services options range from short-term post-go-live assistance to long-term application operations. The study's scope includes segmentation by deployment, type of services, end-user industry, and country. The research also focuses on the impact of COVID-19 on the market ecosystem. In the report scope, the existing service provider landscape is also covered, consisting of major market players.

Africa Managed Services Market is Segmented by Type of Service (Managed Network Services, Managed Security Services, Managed Mobility Services), Deployment (Private, Public, Hybrid), End-user Industry (IT & Telecom, BFSI, Retail, Healthcare), and Country (South Africa, Kenya, Rest of Africa). The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

By Service Type

| Managed Network Services |

| Managed Security Services |

| Managed Mobility Services |

| Managed Cloud Services |

| Managed Data-centre and Hosting Services |

| Other Services |

By Deployment Model

| Private Cloud |

| Public Cloud |

| Hybrid Cloud |

By Organization Size

| Large Enterprises |

| Small and Medium-sized Enterprises (SMEs) |

By End-user Industry

| IT and Telecom |

| BFSI |

| Retail and E-commerce |

| Healthcare |

| Government and Public Sector |

| Manufacturing |

| Other Industries |

By Country

| South Africa |

| Kenya |

| Nigeria |

| Egypt |

| Rest of Africa |

| By Service Type | Managed Network Services |

| Managed Security Services | |

| Managed Mobility Services | |

| Managed Cloud Services | |

| Managed Data-centre and Hosting Services | |

| Other Services | |

| By Deployment Model | Private Cloud |

| Public Cloud | |

| Hybrid Cloud | |

| By Organization Size | Large Enterprises |

| Small and Medium-sized Enterprises (SMEs) | |

| By End-user Industry | IT and Telecom |

| BFSI | |

| Retail and E-commerce | |

| Healthcare | |

| Government and Public Sector | |

| Manufacturing | |

| Other Industries | |

| By Country | South Africa |

| Kenya | |

| Nigeria | |

| Egypt | |

| Rest of Africa |

Key Questions Answered in the Report

What is the current value of the Africa managed services market?

The Africa managed services market size is USD 5.53 billion in 2026 and is projected to grow to USD 9.62 billion by 2031.

Which service segment is growing fastest?

Managed security services are expanding at 12.28% CAGR for 2026-2031 thanks to rising cyber-threat exposure among African enterprises.

Why are SMEs critical to future growth?

SMEs already command 55.72% revenue share in 2025 and prefer subscription models that avoid large capital outlays, driving a 11.84% CAGR.

How do data-sovereignty laws affect provider strategies?

Regulations in Egypt, Nigeria and South Africa force workloads to stay onshore, favouring MSPs with local data-centre footprints.

Page last updated on: