Nuts And Nutmeals Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

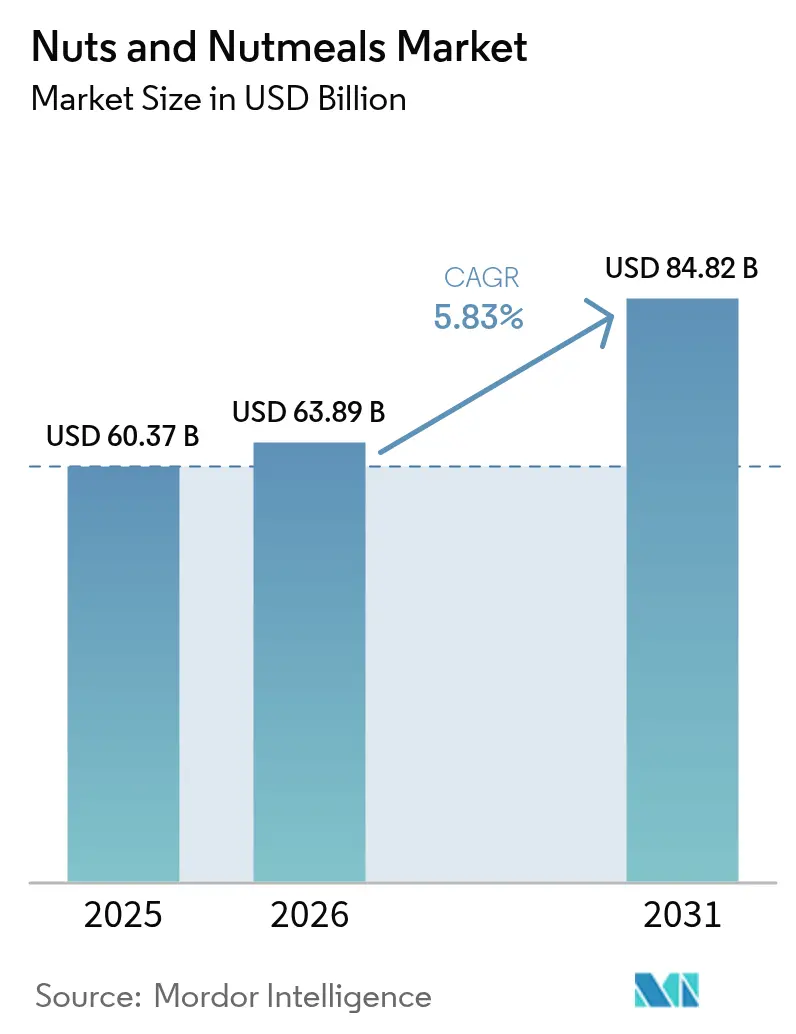

| Market Size (2026) | USD 63.89 Billion |

| Market Size (2031) | USD 84.82 Billion |

| Growth Rate (2026 - 2031) | 5.83% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nuts And Nutmeals Market Analysis by Mordor Intelligence

The global nuts and nutmeals market size was valued at USD 60.37 billion in 2025 and estimated to grow from USD 63.89 billion in 2026 to reach USD 84.82 billion by 2031, at a CAGR of 5.83% during the forecast period (2026-2031). This growth trajectory reflects the sector's resilience amid shifting consumer preferences toward plant-based nutrition and premium snacking experiences. The market's expansion is underpinned by technological advances in processing, sustainable sourcing initiatives, and the integration of artificial intelligence in quality control systems that enable real-time contamination detection and automated grading processes.

Key Report Takeaways

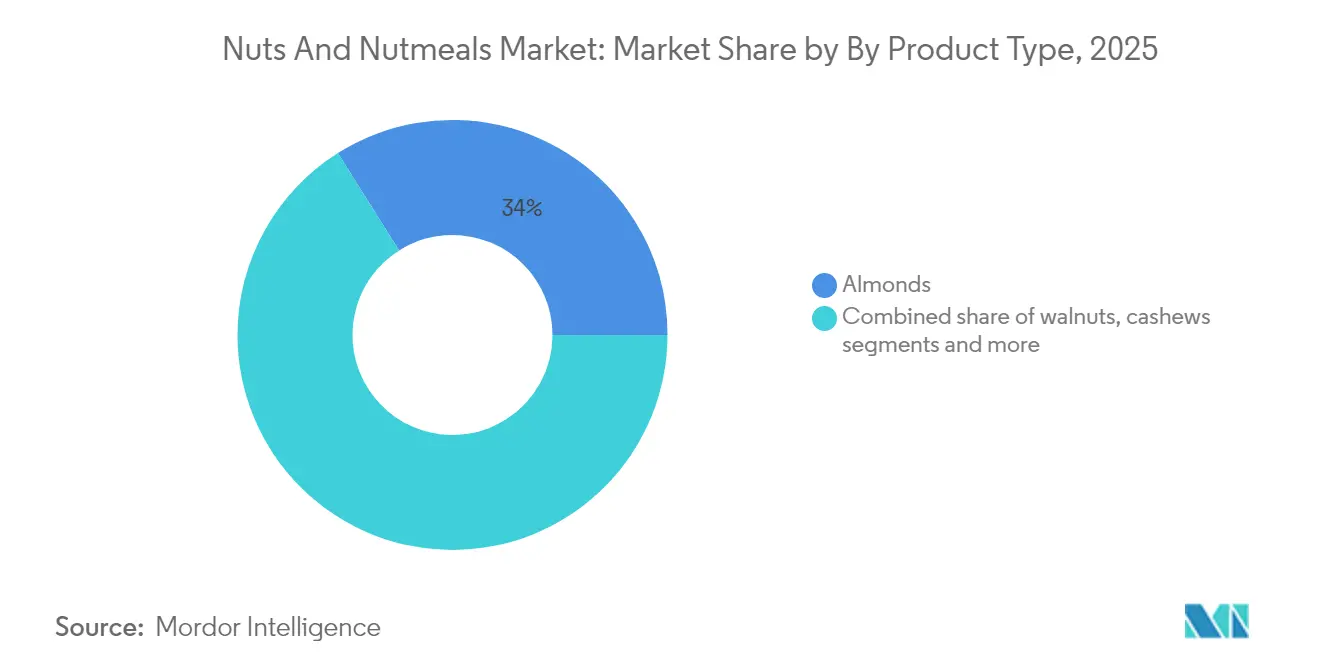

- By product type, almonds led with 33.95% of the global nuts and nutmeals market share in 2025, while pistachios are forecast to grow at a 6.75% CAGR to 2031.

- By category, conventional products accounted for 64.10% of the 2025 value, whereas organic products are projected to expand at a 7.32% CAGR through 2031.

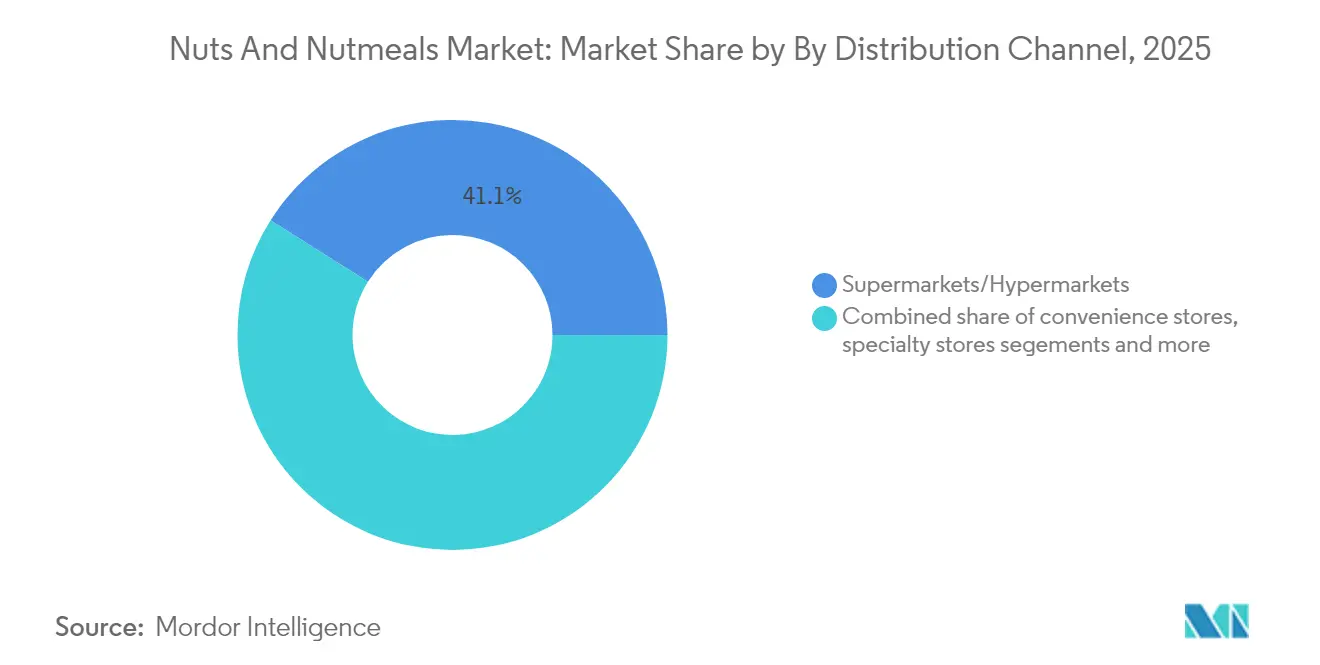

- By distribution channel, supermarkets/hypermarkets held a 41.05% share in 2025, but online retail is advancing at a 7.65% CAGR between 2026-2031.

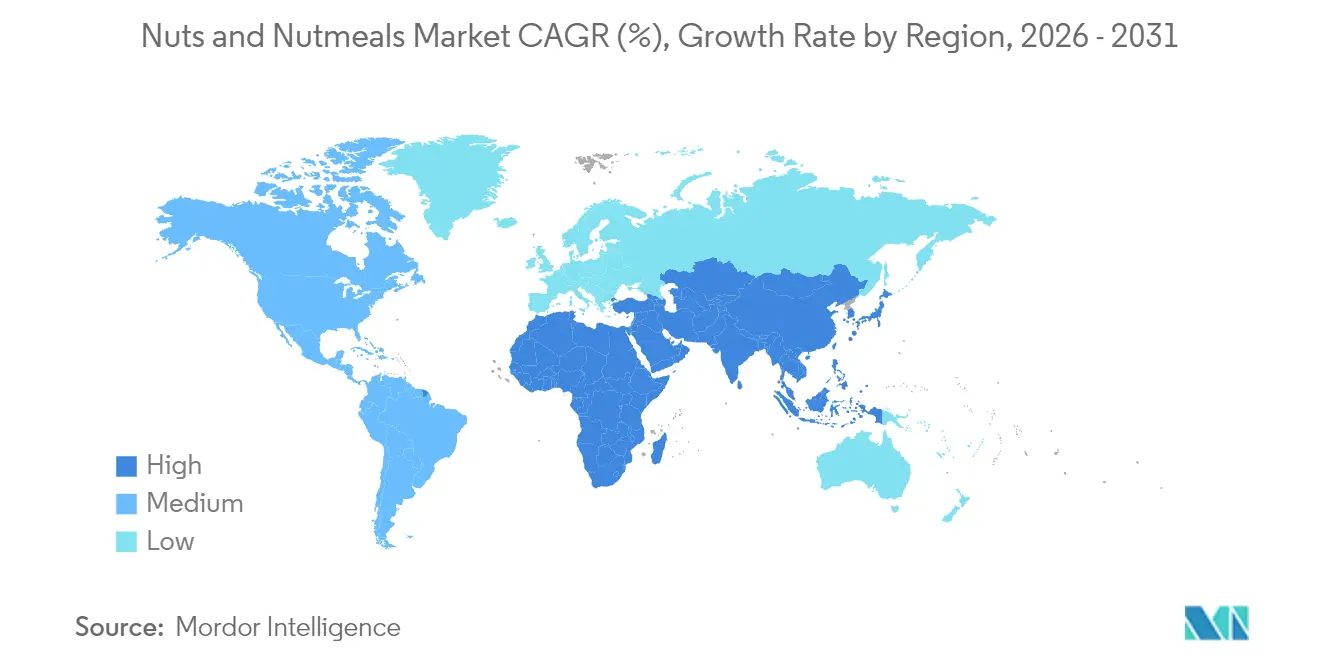

- By geography, Asia-Pacific captured 33.90% of 2025 revenue, while the Middle East and Africa region is expected to register a 6.32% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Nuts And Nutmeals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in plant-based and vegan diets | +1.2% | Global, with concentration in North America and European Union | Medium term (2-4 years) |

| Clean label and natural ingredients | +0.8% | North America and European Union, expanding to Asia-Pacific urban centers | Short term (≤ 2 years) |

| Healthy snacking trend | +1.0% | Global | Short term (≤ 2 years) |

| Innovation in flavors and formats | +0.6% | North America and European Union, with Asia-Pacific adoption | Medium term (2-4 years) |

| Culinary versatility and expansion | +0.4% | Global, led by foodservice sector growth | Long term (≥ 4 years) |

| Sustainable sourcing and traceability | +0.7% | European Union regulatory influence, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growth in Plant-Based and Vegan Diets

The global surge in plant-based and vegan dietary preferences is a major factor driving the demand for nuts and nutmeals. Consumers are increasingly shifting away from animal-derived products due to concerns related to health, sustainability, and animal welfare, and are seeking nutrient-dense, natural alternatives that can provide comparable protein, healthy fats, and essential micronutrients. Plant-based food sales in the United States reached USD 8.1 billion in 2023, according to the Plant Based Foods Association (PBFA). The market grew by 79% over the past five years, with household penetration at 62% and repeat purchase rates at 81%[1]Source: Plant Based Foods Association, “Groundbreaking PBFA Report Reveals Consumers Opt for Plant-Based when Given the Choice,” plantbasedfoods.org. Nuts, such as almonds, cashews, hazelnuts, walnuts, and pistachios, along with nutmeals derived from them, have emerged as critical ingredients in the plant-based food sector because of their high protein content, omega-3 and omega-6 fatty acids, dietary fiber, vitamins, and minerals.

Clean Label and Natural Ingredients

Consumer scrutiny of ingredient lists drives demand for minimally processed nut products with transparent sourcing credentials, creating premium pricing opportunities for producers who can demonstrate farm-to-shelf traceability. Blockchain-enabled supply chain systems now provide immutable records of cultivation practices, processing methods, and quality certifications, addressing consumer concerns about authenticity and safety. This technological infrastructure becomes particularly valuable for organic and specialty nut segments, where provenance verification directly impacts market positioning and pricing power.

Healthy Snacking Trend

The convergence of convenience and nutrition drives portion-controlled nut packaging innovations and functional blends that target specific health outcomes, from cognitive enhancement to cardiovascular support. Advanced packaging solutions now incorporate barrier technologies and resealable features that extend shelf life while maintaining nutritional integrity, enabling broader distribution and reduced food waste. This trend particularly benefits tree nuts with established health claims, as consumers increasingly view snacking as an opportunity for nutritional supplementation rather than mere indulgence.

Innovation in Flavors and Formats

Culinary experimentation with global flavor profiles and novel processing techniques creates differentiated products that command premium pricing in saturated markets. The integration of traditional spice blends, fermentation processes, and texture modifications enables nut processors to capture value beyond commodity pricing while addressing diverse regional taste preferences. Social media-driven viral food trends accelerate the adoption of innovative formats, creating rapid market opportunities for agile manufacturers who can scale production quickly.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Climate sensitivity and environmental impact | -1.4% | California, Australia, Mediterranean regions | Short term (≤ 2 years) |

| Allergen concerns and cross-contamination | -0.6% | Global, with stricter European Union and North American regulations | Medium term (2-4 years) |

| Regulatory compliance and certification | -0.4% | European Union, North America, expanding to emerging markets | Long term (≥ 4 years) |

| Variable quality standards and lack of traceability | -0.3% | Emerging markets, smallholder farming regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Climate Sensitivity and Environmental Impact

Water scarcity and extreme weather events increasingly constrain production in key growing regions, forcing strategic shifts toward drought-tolerant varieties and alternative cultivation areas. California's pistachio industry demonstrates this adaptation, with growers leveraging the crop's superior water efficiency compared to almonds during prolonged drought conditions. Australian almond producers faced similar challenges in 2024, with heat and frost events necessitating crop downgrades that rippled through global supply chains. These climate pressures accelerate investment in precision agriculture technologies, including soil moisture sensors and predictive analytics, while driving geographic diversification of production bases to reduce concentration risk.

Allergen Concerns and Cross-Contamination

Evolving regulatory frameworks for allergen management create compliance burdens that disproportionately impact smaller processors while potentially consolidating market share among larger, better-resourced operators. The U.S. Food and Drug Administration's (FDA) updated tree nut allergen guidance emphasizes quantitative risk assessment and enhanced verification protocols, requiring significant investments in testing infrastructure and process controls[2]Source: UK Food Standards Agency, “Quantitative risk assessment of food products cross-contaminated with allergens,” food.gov.uk. These requirements particularly challenge co-manufacturing facilities that process multiple allergen categories, potentially reducing processing capacity and increasing costs across the supply chain.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Almonds Lead Despite Pistachio Surge

Almonds hold the dominant market position with a 33.95% share in 2025, leveraging established cultivation infrastructure and broad applications across direct consumption, ingredient processing, and industrial uses. Pistachios demonstrate the highest growth rate at 6.75% CAGR through 2031, benefiting from their drought resistance and increased cultivation in water-scarce regions. Cashews experience growth through processing advancements and value-addition opportunities, particularly in emerging markets with developing local processing capabilities.

Walnuts retain their premium market position through omega-3 health benefits and culinary uses, despite challenges from climate variations. Brazil nuts and pecans maintain stable premium pricing in specialized market segments, while hazelnut demand fluctuates based on confectionery industry trends and harvest variations in primary growing regions. Moreover, in pistachio production, machine learning technology enhances quality grading and traceability systems, enabling premium pricing for high-quality varieties.

By Category: Organic Premiumization Accelerates

The organic segment is expected to grow at a 7.32% CAGR, driven by consumer willingness to pay higher prices for products that meet strict sustainability and chemical-free farming standards. The certification process requires producers to maintain detailed records, undergo regular inspections, and follow specific agricultural practices that exclude synthetic pesticides and fertilizers. Conventional nuts retain 64.10% market share through lower prices and widespread availability but experience margin constraints due to commodity price fluctuations and rising production costs, including labor, transportation, and storage expenses.

Consumer demand for supply chain transparency affects both organic and conventional categories, with buyers requiring detailed information about farming practices, processing methods, and distribution channels. Nigeria's organic cashew certification programs demonstrate this trend, as producers implement comprehensive tracking systems, quality control measures, and sustainable farming practices to access premium markets. The organic segment continues to gain market share as producers invest in larger-scale operations, implement efficient processing systems, and develop direct relationships with retailers, leading to reduced certification and operational costs.

By Distribution Channel: Digital Transformation Reshapes Retail

Supermarkets/hypermarkets hold a dominant 41.05% market share in 2025, supported by their extensive distribution networks and competitive pricing. The online retail segment is growing at a 7.65% CAGR as consumers increasingly purchase specialty and bulk nut products through digital channels. E-commerce platforms provide direct-to-consumer sales that reduce retail markups while offering detailed product information and customization options. Convenience stores maintain consistent sales through impulse purchases and portion-controlled packaging, and specialty stores compete by offering curated selections and expert guidance.

Online channels particularly benefit the premium and organic segments, where product information and customer reviews significantly influence purchase decisions. Other distribution channels, show moderate growth linked to economic conditions and food industry expansion. The digital marketplace allows smaller nut producers to reach global markets previously controlled by large-scale distributors, creating new competitive dynamics in the industry.

Geography Analysis

Asia-Pacific holds a 33.90% market share in 2025, primarily due to China's rapid growth in macadamia consumption and increasing middle-class purchasing power across the region. China's rising demand for macadamia kernels has positioned the country as a major global consumer, creating supply chain pressures in international markets. In addition, Australia's position as both a significant producer and consumer influences market dynamics, particularly as climate-related challenges affect domestic almond production and regional supply levels.

The Middle East and Africa region exhibits the fastest growth at 6.32% CAGR through 2031, supported by local processing investments and value-addition initiatives that capture greater shares of the nut value chain. Africa's position as a major raw material producer, particularly for cashews, creates opportunities for processing infrastructure development that could transform regional trade patterns. South Africa leads regional consumption while Nigeria, the Ivory Coast, and other West African nations focus on expanding processing capacity to reduce dependence on raw material exports. The region's young, growing population and improving economic conditions support long-term demand growth across multiple nut categories. Europe maintains significant market presence through established consumption patterns and stringent quality standards that influence global trade flows. The region's emphasis on organic certification and sustainable sourcing creates premium market segments that benefit producers willing to invest in compliance infrastructure. Furthermore, North America combines large-scale production capabilities with sophisticated processing infrastructure and strong domestic consumption. California's dominance in almond and pistachio production faces increasing scrutiny due to water usage concerns and climate change impacts, driving innovation in drought-tolerant cultivation and precision agriculture technologies.

Regulatory Landscape

International trade in nuts and nutmeals is anchored to food safety and contaminant-control frameworks such as Codex Alimentarius codes, including the Code of Practice for the Prevention and Reduction of Aflatoxin Contamination in Peanuts (CXC 55-2004, revised in 2025) and broader hygiene guidance (CXC 22-1979). These references are often used by importing markets and buyers as benchmarks for aflatoxin prevention, good hygiene practices, and verification, shaping supplier audit requirements and testing programs across major nut origins.

In 2025, the U.S. Food and Drug Administration updated food allergen labeling guidance affecting tree nut declarations, while U.S. standards of identity and related requirements for tree nut and peanut products are reflected in Title 21 CFR Part 164. In China, standard-setting has become more variety-specific: GB/T 46171-2025 for in-shell hazelnuts and kernels took effect on February 1, 2026, and GB/T 30761-2025 for almond nut and kernel took effect on March 1, 2026; QB/T 8171-2026 for dried and roasted cashew nuts was issued with an implementation date of September 1, 2026. China also notified the WTO in May 2026 of a proposed national food safety standard for nut and seed foods focused on modifying mold limits in roasted products, adding another compliance checkpoint for exporters targeting the market.

Value Chain Analysis

The nuts and nutmeals value chain runs from cultivation (including smallholder systems, notably for cashews in parts of Africa and Asia) through aggregation, primary processing (drying, shelling, sorting, roasting), and ingredient manufacturing (meals, flours, pastes), then distribution via traders, importers, branded processors, and retail and foodservice channels. Vertically integrated operators and large processors, including global suppliers such as ofi, increasingly combine sourcing, processing, and ingredient manufacturing, while industry associations such as the International Nut & Dried Fruit Council (INC) and the Peanut and Tree Nut Processors Association (PTNPA) support standardization, advocacy, and market access.

Key value-chain constraints center on input volatility and logistics, including fertilizer and energy costs, labor availability for shelling and processing, and shipping disruptions that affect transit times and quality risk. Non-tariff requirements, including phytosanitary rules, maximum residue limits, and buyer-driven certification, shape documentation and testing intensity alongside aflatoxin management. In the United States, export-market development remains an organized downstream lever: USDA Foreign Agricultural Service export development funding for fiscal year 2026 totaled USD 212 million and included allocations to tree nut bodies such as the California Walnut Commission and American Pistachio Growers, supporting coordinated demand creation and market-opening work that feeds into the distribution end of the chain.

Competitive Landscape

The global nuts and nutmeals market exhibits moderate fragmentation, creating space for both established multinational processors and emerging technology-enabled disruptors to capture market share. Strategic patterns emphasize vertical integration, with leading players like Blue Diamond Growers and The Wonderful Company controlling cultivation, processing, and distribution to capture value across the entire chain.

Companies are differentiating themselves through sustainability programs, including renewable energy adoption, waste reduction initiatives, and eco-friendly packaging solutions. The adoption of technologies like artificial intelligence in quality control processes for defect detection and automated inspections, along with blockchain systems for end-to-end supply chain traceability and product authentication, has become a basic requirement for market participation rather than a competitive advantage.

White-space opportunities emerge in specialized processing techniques, such as cashew nutshell liquid valorization for agricultural applications and regenerative farming practices that improve soil health while reducing input costs. Emerging disruptors leverage direct-to-consumer channels and specialized product formulations to challenge traditional distribution models, while established players respond through acquisition strategies and innovation partnerships that combine scale advantages with entrepreneurial agility.

Nuts And Nutmeals Industry Leaders

Archer Daniels Midland

Select Harvests

The Wonderful Company

Olam International

Blue Diamond Growers

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

The opportunity is shifting from commodity kernels to higher-value nut ingredients and intermediate products that broaden applications in plant-based foods and convenient nutrition formats. In February 2026, Plenty Foods commenced production at a commercial defatted nut powder processing facility in Kingaroy, Queensland (AUD 20 million), producing almond, macadamia, and peanut-based powders, showing active investment behind ingredient-led growth beyond whole nuts. This aligns with the report scope where technology and processing advances enable new formats such as nutmeals and powders, and supports premium positioning in online and specialty channels where ingredient transparency and use-cases are easier to communicate.

Origin-side processing and supply diversification also create visible whitespace, particularly for cashews where more value capture can occur near production regions. Robust International announced plans in February 2026 to build a cashew processing facility in Ogun State, Nigeria, to raise local processing capacity from 100 to 220 tonnes per day, and Ivory Coast expanded installed cashew processing capacity to about 830,000 tonnes per year by 2025 across 37 processing units, highlighting momentum toward domestic processing rather than exporting raw nuts. On the demand and sourcing side, investment in dedicated processing assets for specific nut types supports category depth: Ferrero announced a USD 94 million investment in May 2026 to expand hazelnut operations in Chile, including a new processing plant in Cunco (La Araucania), reinforcing supply development tied to industrial end uses such as confectionery and spreads.

Recent Industry Developments

- June 2026: Select Harvests confirmed its almond processing capacity expansion to 55,000 metric tons as part of its operational update. The move improves scale and throughput for value-added almond formats and supports more consistent supply into retail and ingredient channels.

- May 2026: Ferrero announced a USD 94 million investment to expand hazelnut operations in Chile, including a new processing plant in Cunco, La Araucania. This adds processing depth closer to origin and supports industrial demand for hazelnuts with greater control over quality and traceability.

- August 2025: Diamond Foods LLC expanded its Diamond of California line with Snack Pecans in Sea Salt and Pecan Pie varieties, launching first on Amazon with a planned broader retail rollout. The introduction signals continued premiumization in portioned nut snacks and reinforces the role of e-commerce as a launchpad for new nut formats.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the nuts and nutmeals market is defined as the value of edible nuts and nutmeals sold for human consumption through retail and foodservice channels, measured at the point where products enter commercial trade in each country.

Scope exclusions: This sizing does not count nut oils, beverages made from nuts, or non-food uses such as cosmetics and industrial ingredients.

Segmentation Overview

- By Product Type

- Almonds

- Walnuts

- Cashews

- Hazelnuts

- Pistachios

- Peanuts

- Brazil Nuts

- Pecans

- Others

- By Category

- Conventional

- Organic

- By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience Stores

- Specialty Stores

- Online Retail Channels

- Other Distribution Channels

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

- Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set market boundaries, map supply flows, and form an initial demand picture across major producing and importing countries. We referred to public data sources such as FAOSTAT for production and yield trends, ITC Trade Map and UN Comtrade for import-export values and volumes, and USDA and Eurostat updates for consumption signals and price movements.

To keep assumptions grounded, trade association publications and food standard bodies were also checked for definitions and product labeling (for example, what is typically counted as nutmeals in food formulations). Company annual reports, investor decks, and reputable news were used to understand processing capacity additions, pricing cycles, and channel shifts. In a few cases, paid subscriptions for company financials and shipment-level trade intelligence were used to fill gaps where public reporting is delayed. The sources mentioned above are illustrative and not exhaustive, and many other public documents and datasets were also referred to for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to sanity-check volume splits, price realization, and channel margins across key nut types and nutmeals. We spoke with a mix of growers and processors, importers and distributors, and packaged food buyers across APAC, EMEA, and the Americas so regional supply seasonality and demand behavior could be reflected in the model. These discussions were also used to confirm conversion factors (kernel to meal), typical grade mix, and how organic premiums move by year.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 13% | APAC: 51% |

| Mid tier: 57% | Functional/Unit leaders: 31% | EMEA: 29% |

| Smaller Players: 15% | Managers: 56% | Americas: 20% |

Market-Sizing & Forecasting

The core sizing logic uses a top-down build that reconstructs country-level value from production, processing output, and cross-border trade, which is then aligned to apparent consumption after adjusting for re-exports. Totals are corroborated with selective bottom-up checks, such as sampled supplier revenue splits, channel checks in large importing markets, and volume times average selling price calculations for a few high-share nut types.

Inputs that mattered in this market include harvested area and yields for major nuts, shelling and processing conversion rates into meals, import-export unit values, the share of retail versus foodservice demand, and organic price premiums where they are meaningful. When a data series is thin for a smaller origin country, the gap is handled using nearest-neighbor proxies based on trade partners and historic crop cycles, and then corrected through interview feedback.

For forecasting, we mainly rely on scenario analysis supported by multivariate regression on drivers that tend to move demand, such as population and income trends, snack and bakery category growth, and expected price swings tied to crop seasonality. Assumptions on price progression and mix shift were reviewed with industry participants so the forward view stays realistic for procurement and selling cycles.

Data Validation & Update Cycle

Model outputs are cross-checked against independent signals like global trade balances, price indices, and reported crop outcomes for key producing regions. If an estimate shows an unusual jump, the underlying drivers are re-tested, and sources are re-contacted when the variance cannot be explained by seasonality, tariff changes, or mix effects.

Before sign-off, the workbook is reviewed in multiple steps, covering scope alignment, math logic, and year-over-year reasonableness. Reports are refreshed annually, and interim updates are made when material events occur, such as major crop shocks or sustained price movements. Right before delivery, a fresh review pass is completed so clients receive the latest updated view.

Mordor Intelligence's Nuts and Nutmeals Market Estimate Compared With Other Published Estimates

Published market values for nuts and nutmeals can differ even when the product name sounds identical, because sources may not use the same base year, price basis, or product boundary between whole nuts, meals, and adjacent nut-derived goods.

Import-export unit values, crop outcome updates in key producing countries, and channel mix signals are the evidence checks that keep Mordor Intelligence tied to edible nuts and nutmeals only, excluding nut oils and nut-based beverages that can inflate totals when they are bundled.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 63.89 B (2026) | |

| Trade Publisher A | USD 57.01 B (2024) | Uses an earlier base year and may apply a different price timing for traded nuts, which can shift value in years when unit values and grade mix move quickly. |

| Industry Report B | USD 60.57 B (2025) | Uses a different base-year setup and horizon, and the scope detail on what counts as nutmeals versus other nut-derived ingredients is less explicit, which can move the total. |

Across the three figures, most of the spread comes from base-year choice, how pricing is averaged through the year, and how tightly nutmeals are separated from nearby nut-derived product lines. By keeping scope rules consistent and then validating with observable trade, crop, and channel signals, the final number stays traceable to inputs that can be rechecked year after year.

Key Questions Answered in the Report

What is the current value of the global nuts and nutmeals market?

The market is valued at USD 63.89 billion in 2026 and is projected to reach USD 84.82 billion by 2031.

Which product currently dominates sales?

Almonds hold the largest 2025 share at 33.95% of total revenue.

Which nut type is growing fastest?

Pistachios are forecast to expand at a 6.75% CAGR through 2031.

Which region has the highest growth outlook?

The Middle East and Africa region is expected to grow at a 6.32% CAGR due to local processing investments.

Page last updated on: