Home and Property Improvement

27th MayStrategic Expansion in the Russia Laundry Appliances Market

3 Min Read

The North America Home Appliances Market Report is Segmented by Product Type (Major Home Appliances Including Refrigerators, Freezers, Washing Machines, Dishwashers, Ovens, Air Conditioners, and More), Distribution Channel (Multi-Brand Stores, Exclusive Brand Outlets, Online, Other Distribution Channels), and Geography (United States, Canada, Mexico). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

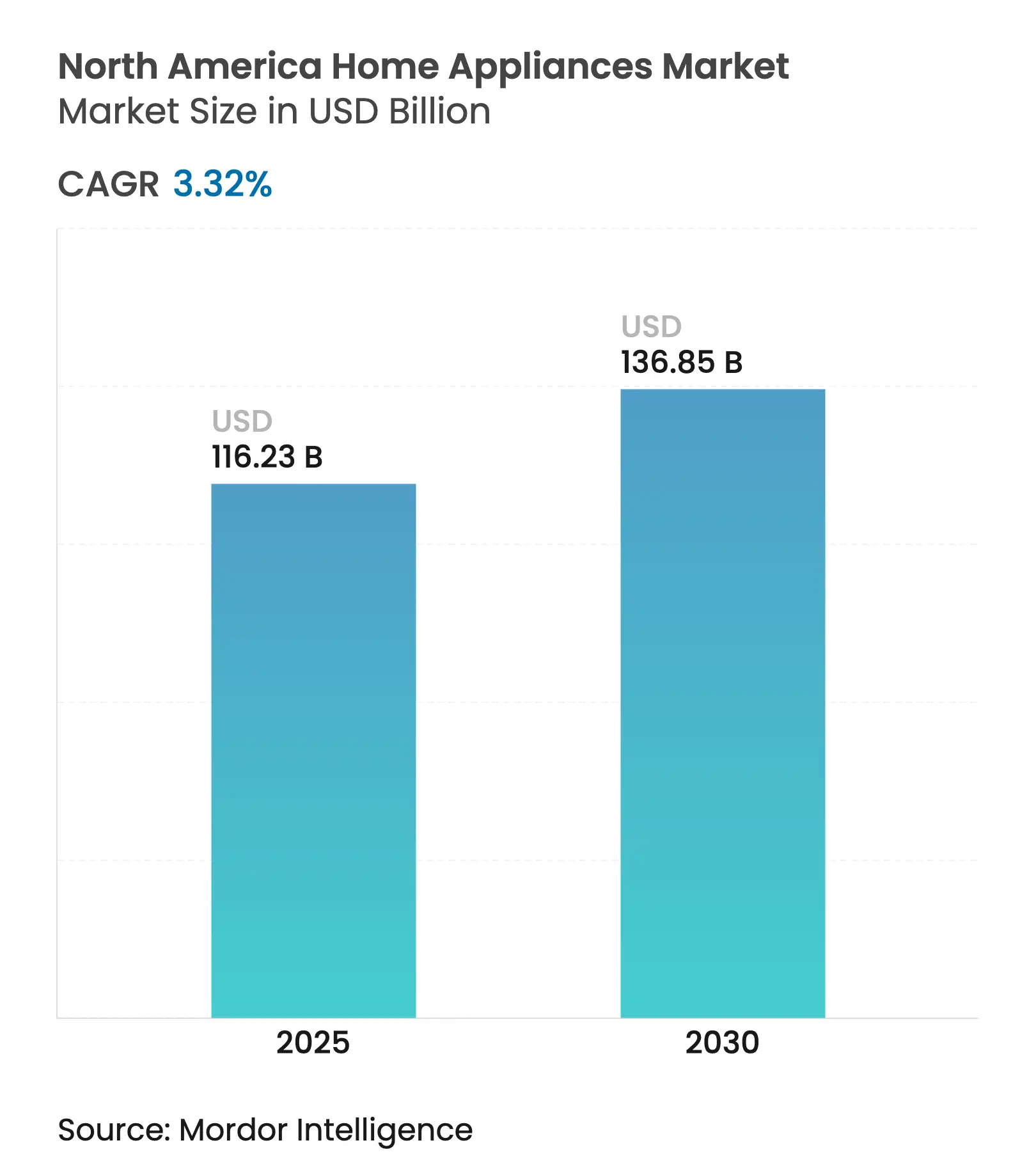

| Market Size (2025) | USD 116.23 Billion |

| Market Size (2030) | USD 136.85 Billion |

| Growth Rate (2025 - 2030) | 3.32 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The North America home appliances market size reached USD 116.23 billion in 2025 and is projected to advance to USD 136.85 billion by 2030, reflecting a 3.32% CAGR over the forecast window. Smart-home connectivity, expanding e-commerce fulfilment, and energy-efficiency mandates continue to add fresh revenue streams that temper the maturity of traditional replacement demand across the North America home appliances market. Manufacturers are redirecting capital toward Matter-compliant platforms, heat-pump compressors, and induction technologies to satisfy regulatory timelines and earn utility incentives. Nearshoring investments in Mexico, combined with rising tariff barriers on Asian imports, are restructuring regional cost bases while semiconductor shortages and freight volatility still weigh on lead times. Competitive dynamics therefore concentrate around incumbents capable of funding R&D, managing compliance, and sustaining omni-channel service models across the North America home appliances market.

Key Report Takeaways

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Smart-home

penetration & IoT integration

Smart-home

penetration & IoT integration

| +0.8% | North America, strongest in U.S. urban markets | Medium term (2-4 years) |

(~) % Impact on

CAGR Forecast

:

+0.8%

|

Geographic

Relevance

:

North America,

strongest in U.S. urban markets

|

Impact Timeline

:

Medium term (2-4

years)

|

Energy-efficiency

regulations & ENERGY STAR incentives

Energy-efficiency

regulations & ENERGY STAR incentives

| +0.6% | United States and Canada, with spillover to Mexico | Long term (≥ 4 years) | |||

Residential

remodelling surge post-COVID

Residential

remodelling surge post-COVID

| +0.5% | North America, concentrated in suburban U.S. markets | Short term (≤ 2 years) | |||

E-commerce channel

expansion & last-mile innovation

E-commerce channel

expansion & last-mile innovation

| +0.4% | North America, strongest growth in Canada and Mexico | Medium term (2-4 years) | |||

State heat-pump

appliance mandates

State heat-pump

appliance mandates

| +0.3% | U.S. West Coast and Northeast states | Long term (≥ 4 years) | |||

Utility-funded

low-income replacement rebates

Utility-funded

low-income replacement rebates

| +0.2% | United States, focused on low-income communities | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Smart-Home Penetration & IoT Integration

Connected adoption is broadening beyond early adopters as interoperability standards stabilize and installation complexity falls. In 2024, BSH introduced the first consumer-available Matter-enabled French-door refrigerator, signalling a shift from positioning IoT as a premium add-on toward embedding connectivity across mainstream models[1]BSH, “Bosch Home Appliances Announces Distribution Partnership with The Home Depot,” BSH-Group News, bsh-group.com. Partnerships linking appliance OEMs with major automation platforms now support onboarding processes that take minutes rather than hours, which lifts conversion rates in the North American home appliances market. LG and Samsung are placing equal emphasis on software updates and hardware refreshes, turning over-the-air upgrades into a post-sale engagement tool that can lengthen customer lifetime value. As a result, network-ready features are becoming table stakes even in mid-price segments of the North American home appliances market. Companies lacking native software expertise face rising integration costs or must rely on white-label solutions that erode brand differentiation.

Energy-Efficiency Regulations & ENERGY STAR Incentives

Department of Energy standards effective from 2024 tighten allowable kilowatt-hour consumption across all core categories, forcing accelerated R&D spending on variable-speed compressors, induction coils, and heat-pump dryers[2]U.S. Department of Energy, “Appliance and Equipment Standards Program,” Energy Efficiency & Renewable Energy, energy.gov. Canada’s parallel framework creates harmonization benefits for manufacturers operating integrated regional supply chains, while Mexico’s draft norms foreshadow continent-wide convergence. On the demand side, the Inflation Reduction Act rebates provide up to USD 840 for qualifying electric dryers, nudging households toward efficient models and boosting unit value in the North American home appliances market. Yet fragmented state-level administration produces uneven sales lift, requiring granular channel planning. Smaller brands struggle to recover certification expenses, which expands scale advantages for incumbents already active across the North America home appliances industry.

Residential Remodeling Surge Post-COVID

Elevated kitchen and bath renovation activity, fuelled by hybrid work lifestyles, still runs above pre-pandemic averages even as mortgage rates dampen discretionary outlays. Professional-grade ranges, column refrigerators, and dual-drawer dishwashers capture upside as homeowners convert daily cooking into an experiential pursuit. Demand is geographically skewed toward high-income suburban zip codes, creating pockets of premium growth inside the broader North America home appliances market. Prolonged contractor backlogs extend appliance lead times, compelling retailers to refine inventory forecasting and cross-dock logistics. Although remodelling momentum is normalizing, the installed base of recently upgraded homes locks in higher ASPs and embedded smart-hub penetration through 2030.

E-Commerce Channel Expansion & Last-Mile Innovation

Online penetration is rising as white-glove delivery, haul-away services, and same-day installation mitigate the complexity of moving 300-pound appliances. Bosch’s February 2025 listing on HomeDepot.com illustrates how premium brands leverage omnichannel partner infrastructure to reach do-it-yourself consumers without sacrificing service quality[3]BSH, “Bosch Home Appliances Announces Distribution Partnership with The Home Depot,” BSH-Group News, bsh-group.com. Discount refurbishers such as QG Appliances 4 Less use factory-certified returns to target value-oriented shoppers, opening new sub-segments within the North America home appliances market. Augmented-reality kitchen planners and AI-based product configurators now replicate in-store consultation online, lifting digital conversion. The resulting share gains challenge multi-brand showrooms to differentiate with experiential merchandising and same-day store pickup.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Semiconductor &

logistics supply constraints

Semiconductor &

logistics supply constraints

| -0.7% | North America, strongest on U.S. manufacturing | Short term (≤ 2 years) |

(~) % Impact on

CAGR Forecast

:

-0.7%

|

Geographic

Relevance

:

North America,

strongest on U.S. manufacturing

|

Impact Timeline

:

Short term (≤ 2

years)

|

Inflation-driven

consumer price sensitivity

Inflation-driven

consumer price sensitivity

| -0.5% | North America, concentrated in the middle-income segments | Medium term (2-4 years) | |||

PFAS &

refrigerant phase-out compliance costs

PFAS &

refrigerant phase-out compliance costs

| -0.3% | United States and Canada | Long term (≥ 4 years) | |||

Declining home

mobility is dampening replacement cycles

Declining home

mobility is dampening replacement cycles

| -0.2% | United States suburban markets | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Semiconductor & Logistics Supply Constraints

The North American home appliances market continues to face challenges due to persistent chip shortages, which are driving redesigns around available microcontrollers. This situation is increasing bill-of-materials costs and raising quality-control risks. Additionally, port congestion and tariff hikes are escalating inbound freight rates, further pressuring manufacturers to localize production. BSH's USD 238 million refrigeration plant in Monterrey highlights the growing trend of near shoring to reduce lead times and mitigate trans-Pacific shipping risks. However, greenfield capacity investments require a multiyear payback period, limiting immediate benefits. OEMs that fail to secure dual-sourcing options for components risk losing shelf space to competitors leveraging forward-buy contracts to ensure supply chain stability.

Inflation-Driven Consumer Price Sensitivity

Between 2023 and 2025, average selling prices are projected to increase by 11%, driven by higher material, freight, and labor costs passed through to retail prices. This trend is prompting middle-income households to delay replacements or shift toward refurbished units, which is diverting volumes from new-unit sales and compressing gross margins in the North America home appliances market. The expansion of the refurbished channel is exerting downward pressure on profitability. Financing promotions and entry-level product launches are mitigating demand erosion but may dilute premium brand equity. If disposable income growth remains sluggish, price elasticity could intensify, compelling manufacturers to adjust their portfolios strategically to maintain profitability. Balancing affordability and brand positioning will be critical for sustaining market competitiveness.

By Product Type: Major Appliances Drive Market Foundation

Refrigerators retained the leading 25.34% North America home appliances market share in 2024, supported by their essential status, large cubic-foot capacities, and premiumization through smart cooling algorithms. Washing machines posted the highest 4.12% CAGR outlook, propelled by heat-pump dryer combos and AI-enabled load sensing that optimize water and power use, thereby leveraging utility rebates to unlock incremental upgrades. The shift to induction cooktops is equally notable as state gas bans draw builders toward electric specifications, enriching the average transaction value within the North America home appliances market size for cooking appliances. Air conditioners confront dual challenges of refrigerant transitions and seasonal demand volatility, yet inverter technology adoption stabilizes margins. Dishwashers and ovens benefit from sustained residential remodelling and restaurant-at-home cooking trends, although extended lead times persist due to semiconductor allocation. Across categories, IoT firmware updates extend functional life, but also raise expectations for continual software support, an obligation that favours scale players with dedicated digital teams. Continuous integration of voice-assistant compatibility further embeds appliances into broader smart-home ecosystems, a linkage that can stimulate ancillary accessory sales.

Consumers increasingly evaluate total ownership cost, combining energy savings, maintenance alerts, and potential resale premiums when selecting major appliances in the North American home appliances market. Consequently, R&D expenditure tilts toward sensor arrays and machine-learning on-device inference that calibrates cycles dynamically, while hardware innovation, such as variable-capacity compressors, maintains steady but incremental progress.

Note: Segment shares of all individual segments available upon report purchase

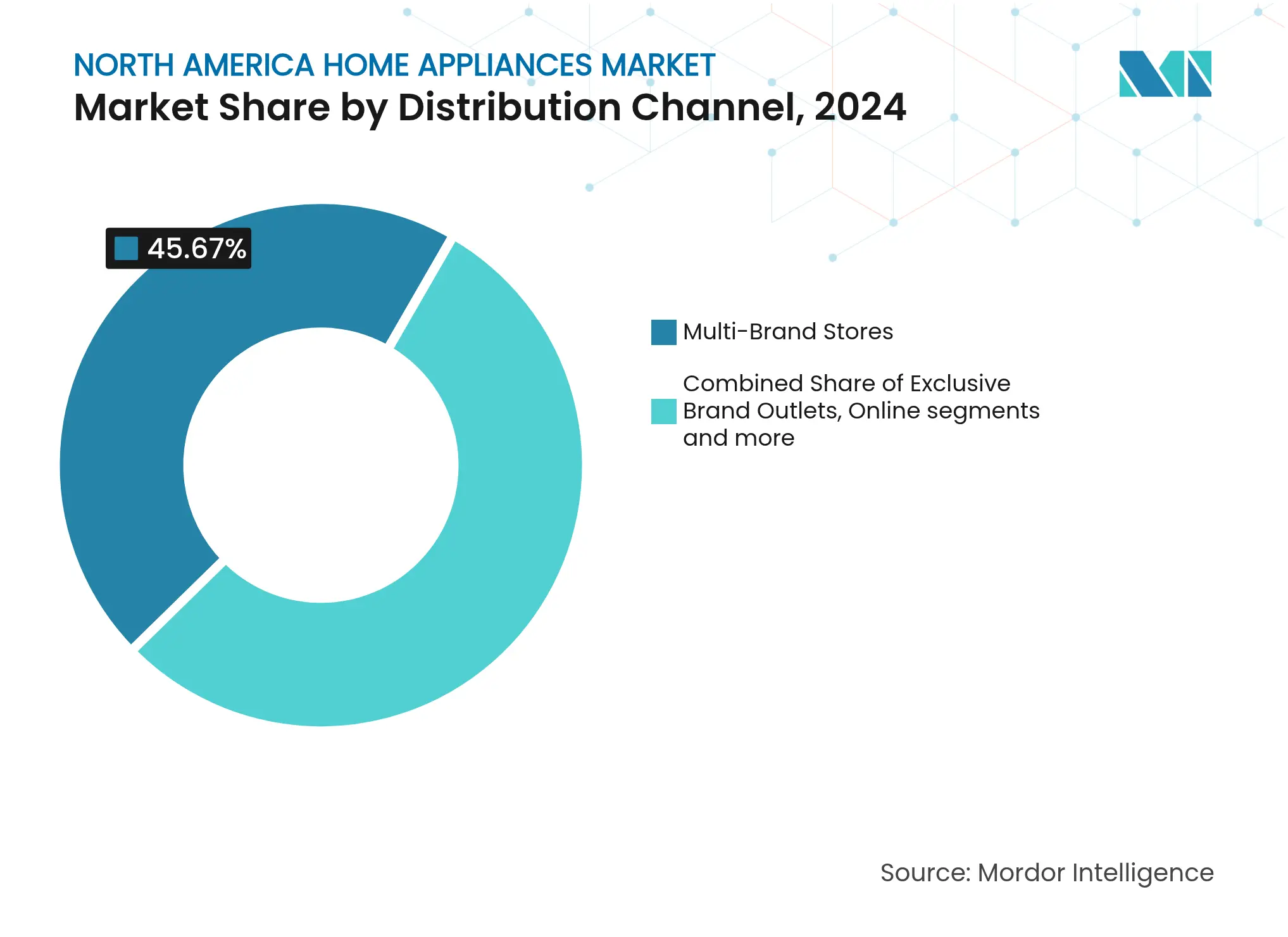

By Distribution Channel: Online Growth Challenges Traditional Retail

Multi-brand showrooms commanded 45.67% share of the North America home appliances market size in 2024, owing to their comparative product displays, financing desks, and established installation crews. Nevertheless, online channels record a 4.61% CAGR as logistics providers perfect white-glove delivery that includes haul-away and same-day hookup, removing legacy barriers in the North American home appliances market. Consumers leverage 3-D configurators, augmented-reality overlays, and AI chat agents to finalize complex purchases without store visits, cutting transaction friction. Pure-play e-commerce operators partner with regional service technicians to meet warranty obligations, blurring the historical service gap between digital and physical channels.

Exclusive brand boutiques preserve a higher gross margin, especially for luxury labels where personalized consultation justifies appointment-only showrooms, while builder-direct sales pipelines secure large batch orders tied to residential developments. Warehouse clubs maintain competitive relevance via bulk-buy pricing, though their limited SKU breadth restricts premium assortment. Meanwhile, discount refurbishers inject price transparency, nudging full-line retailers to introduce certified-pre-owned sections to protect share inside the North America home appliances market.

Note: Segment shares of all individual segments available upon report purchase

The United States retained 77.12% of regional value in 2024, anchoring the North America home appliances market with deep installed bases, mature service networks, and robust smart-home adoption. Heat-pump incentives under the Inflation Reduction Act elevate electrification adoption, while California and New York gas-exit regulations drive induction range demand. Yet slower home mobility narrows full-suite replacement frequency, obliging brands to focus on feature-driven upsell campaigns rather than volume expansion.

Mexico delivers the fastest 4.82% CAGR through 2030, buoyed by rising middle-class incomes, urbanization, and continuous residential construction that embraces modern kitchen layouts. BSH’s Monterrey plant underscores investor confidence in local demand and regional export potential, cutting lead times and tariff exposure for the wider North America home appliances market. Improved grid reliability and credit access accelerate penetration of energy-intensive products such as air conditioners and electric dryers.

Canada exhibits steady growth that mirrors U.S. trends, although a smaller population caps absolute revenue despite similar per-capita unit density. Energy-efficiency policy symmetry with the United States enables platform commonality, reducing SKU proliferation. Premium positioning gains traction through design-centric marketing exemplified by Monogram’s partnership with designer Lauren Kyle McDavid, which targets renovation projects in affluent urban cores[4]Monogram, “Monogram Luxury Appliances Launches Partnership with Celebrity Designer Lauren Kyle McDavid,” Newswire, newswire.ca. Cold-climate heating loads continue to shape demand for high-efficiency dryers and dual-fuel ranges, requiring modest product adaptations even within shared regulatory frameworks.

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

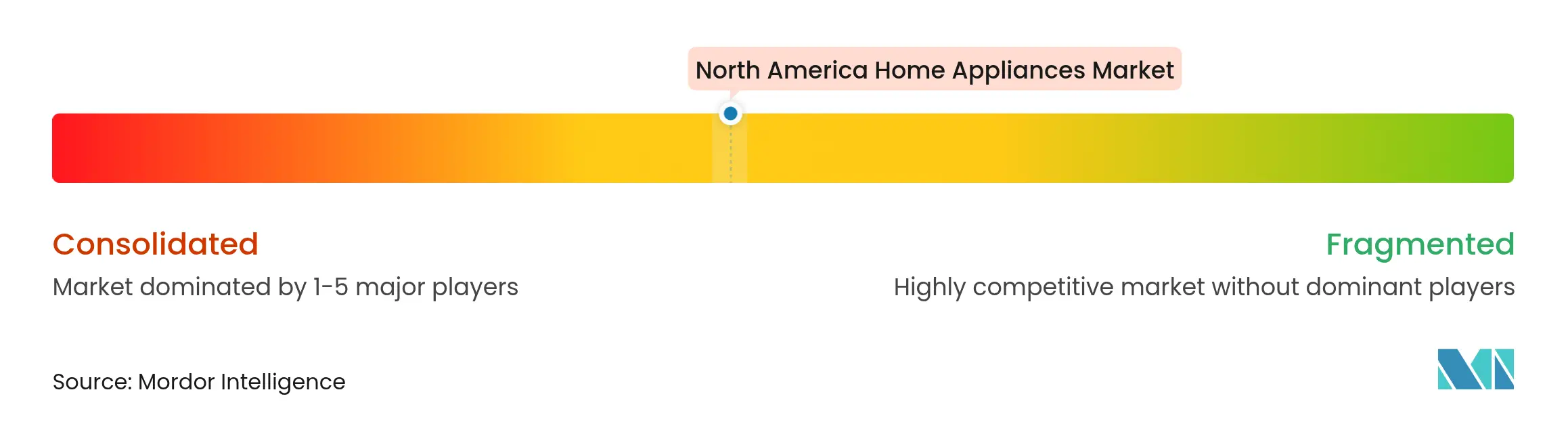

Market Concentration

Competition remains moderate yet intensifying as Whirlpool, GE Appliances, LG, and Samsung deploy vertical integration, IoT differentiation, and near-shoring to retain share inside the North America home appliances market. BSH’s early Matter adoption establishes interoperability leadership, while GE Appliances links major units to ABB smart panels to deliver unified household energy dashboards. These initiatives bind appliances to broader residential electrification ecosystems, raising switching costs.

Scale advantages manifest in component procurement, certification throughput, and continuous software support, reinforcing barriers for smaller brands. Nonetheless, challengers like SharkNinja exploit social media engagement and direct-to-consumer logistics to carve niches, especially in countertop appliances adjacent to the core North America home appliances market. Strategic M&A activity, such as NIBE’s acquisition of Miles Industries’ Valor hearth business, signals entry avenues for HVAC players seeking cross-selling into kitchen and laundry.

Supply-chain uncertainties keep spare-part inventories tight; accordingly, integrated OEM-retailer collaborations emphasize predictive maintenance and subscription replacement programs that lock customers into brand ecosystems. Regulatory compliance around PFAS and refrigerants elevates R&D budgets, but also underpins premium positioning by allowing brands to market health and sustainability credentials. Those unable to absorb escalating costs may exit, accelerating consolidation momentum in the North America home appliances industry.

*Disclaimer: Major Players sorted in no particular order

1. Introduction

2. Research Methodology

3. Executive Summary

4. Market Landscape

5. Market Size & Growth Forecasts (Value in USD)

6. Competitive Landscape

7. Market Opportunities & Future Outlook

A gadget that helps with household chores like cooking, cleaning, and food preservation is called a home appliance, sometimes known as a domestic appliance, an electric appliance, or a household appliance. The report contains a complete background analysis of the North American home appliances market, which includes an assessment of the industry associations, overall economy, and emerging market trends by segment. Moreover, significant changes in the market dynamics and market overview are covered in the report. The North American home appliances market is segmented by major appliances, which include refrigerators, freezers, dishwashing machines, washing machines, cookers, and ovens; by small appliances, including vacuum cleaners, small kitchen appliances, hair clippers, irons, toasters, grills, and roasters, and hair dryers; and by distribution channel including supermarkets/hypermarkets, specialty stores, and e-commerce stores. The report offers market size and forecast values for the North American home appliances market in USD for the above segments.

Strategic Expansion in the Russia Laundry Appliances Market

3 Min Read

A Leading Sanitaryware Company’s Journey in Saudi Arabia

4 Min Read

Mapping Real Estate Opportunities in Bali

4 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.