Market Overview

| Study Period | 2021 - 2031 |

|---|---|

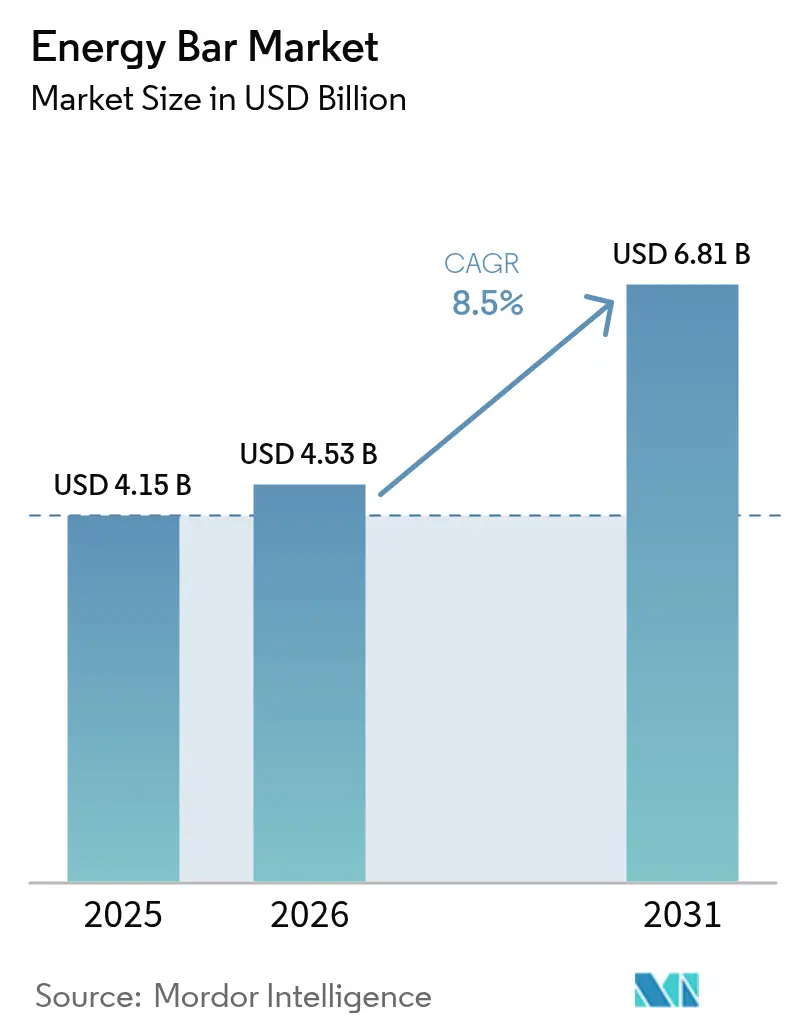

| Market Size (2026) | USD 4.53 Billion |

| Market Size (2031) | USD 6.81 Billion |

| Growth Rate (2026 - 2031) | 8.50% CAGR |

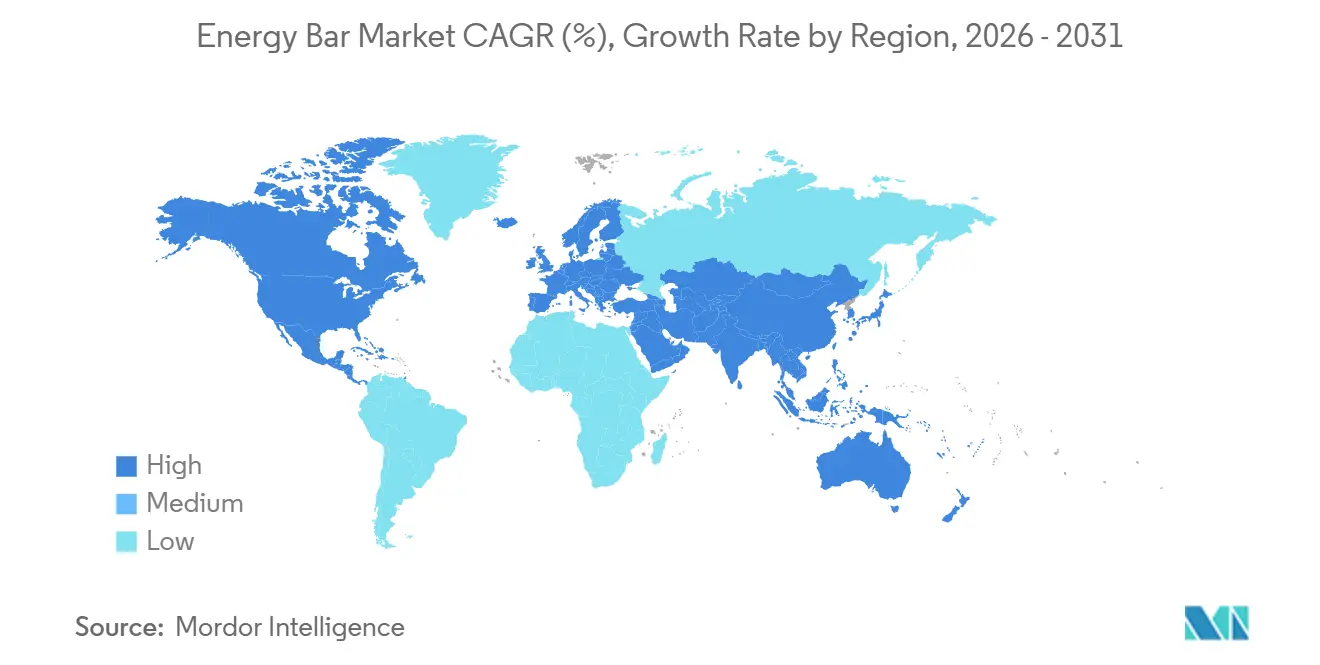

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Energy Bar Market Analysis by Mordor Intelligence

The energy bar market size was valued at USD 4.15 billion in 2025, is projected to reach USD 4.53 billion in 2026, and grow significantly to USD 6.81 billion by 2031, registering a strong CAGR of 8.50% from 2026 to 2031. Conventional formulations are expected to dominate revenue in 2025, but organic and plant-based options are gaining traction. This growth is influenced by the demand for clean-label certifications, advancements in personalized nutrition, and the increasing popularity of e-commerce subscriptions, which are reshaping consumer preferences. Manufacturers are facing challenges due to fluctuating prices of key commodities like cocoa, whey, and almonds. To mitigate these risks, they are adopting strategies such as ingredient hedging, diversifying protein sources, and pursuing vertical integration. Regulatory developments are also playing a significant role, with approvals for novel proteins and designations for next-generation sweeteners driving product reformulations. These efforts focus on reducing sugar content, improving amino-acid profiles, and supporting claims like Keto and Paleo. Geographically, growth patterns vary. While North America and Europe hold the largest market shares, the Asia-Pacific region is experiencing the fastest growth, driven by rising gym memberships and the expansion of modern retail channels.

Key Report Takeaways

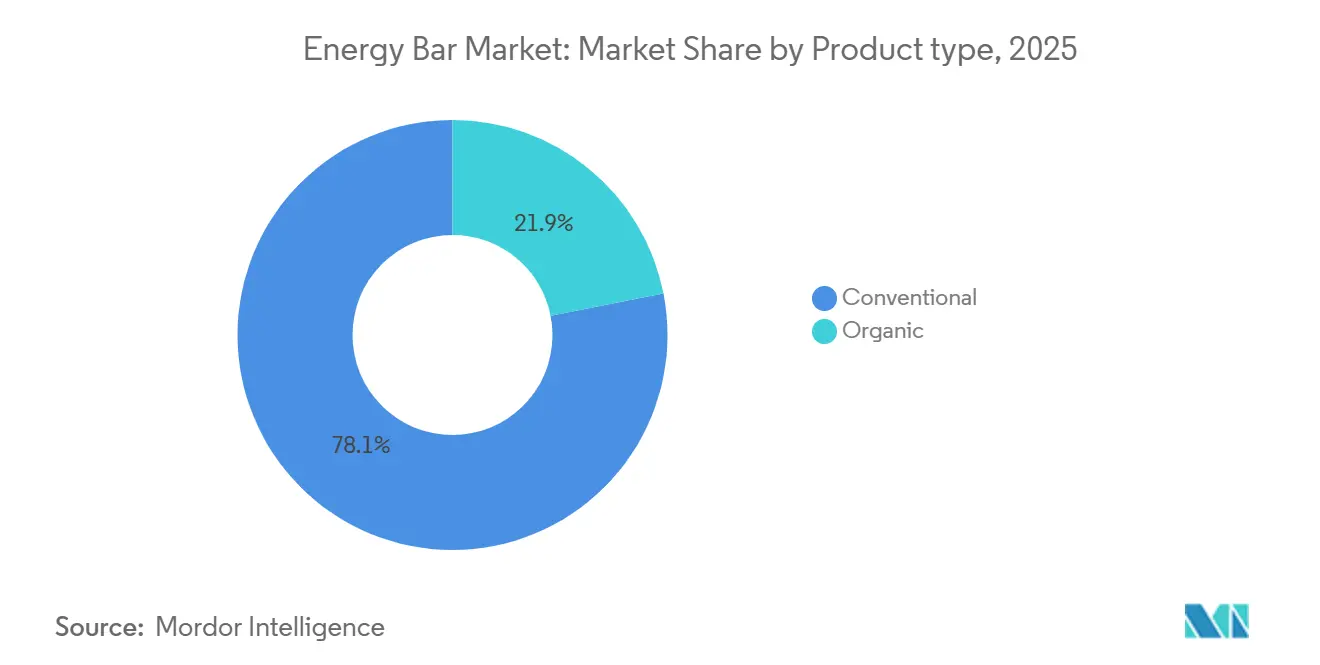

- By product type, in 2025, conventional bar dominated the energy bars market with a 78.09% share, while organic bars are projected to grow at an 8.59% CAGR from 2026 to 2031.

- By protein source, plant-based formats made up 54.24% of 2025 revenue, while animal-based bars, driven by whey and collagen, are expected to see an 8.80% CAGR growth through 2031.

- By function/application, sports and endurance nutrition accounted for 78.16% of 2025 sales, but weight-management and lifestyle-energy bars are on track to grow at a 9.17% CAGR until 2031.

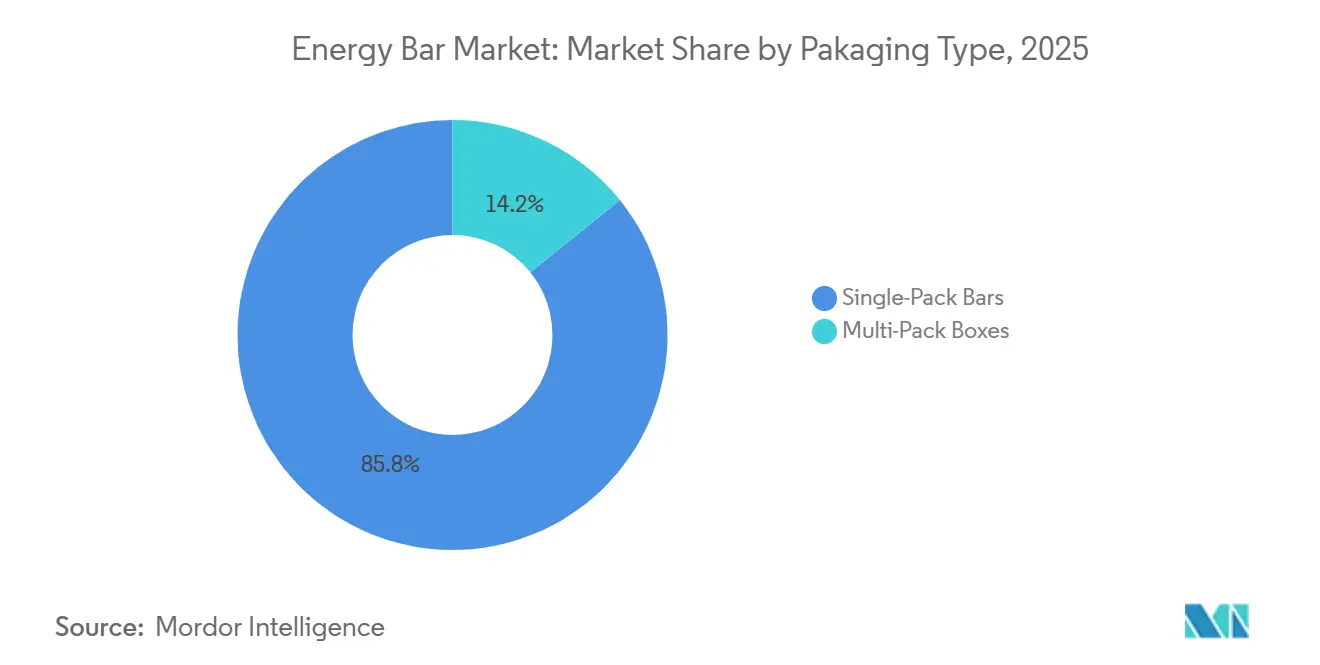

- By packaging, single-pack units took 53.21% of 2025 volume, while multi-pack boxes, boosted by online subscriptions, are projected to grow at an 8.81% CAGR from 2026 to 2031.

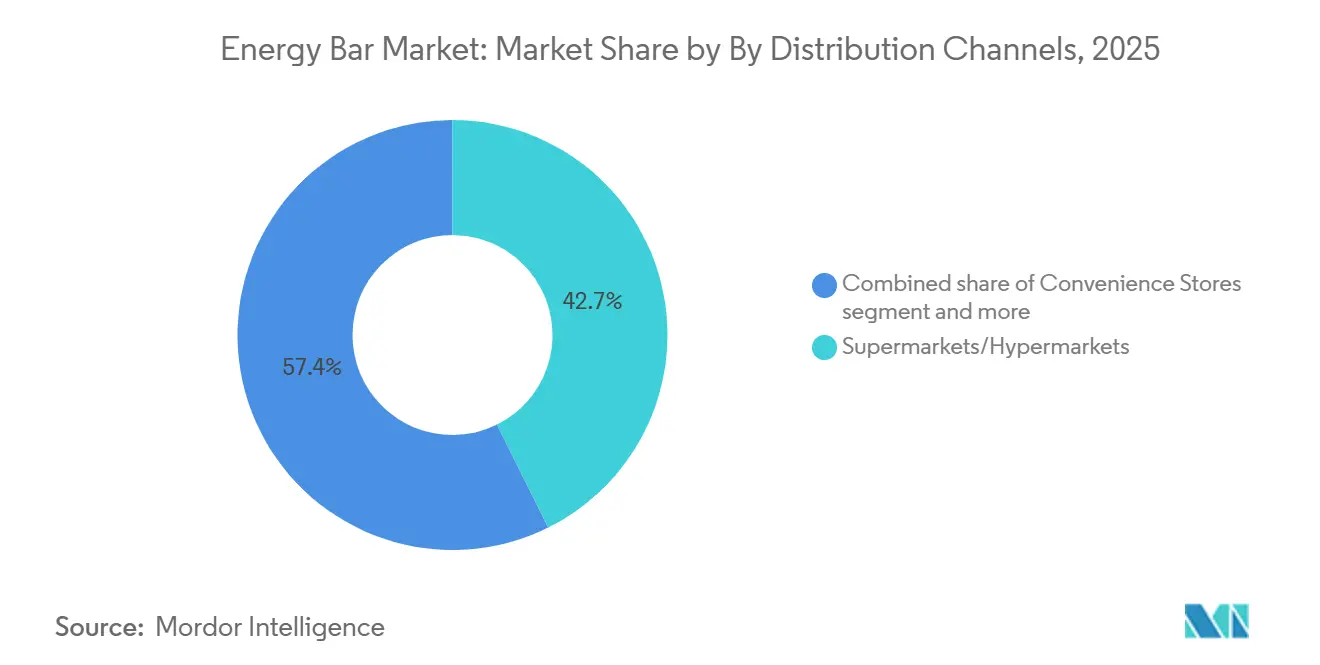

- By distribution, supermarkets/hypermarkets secured 42.65% of 2025 revenues, but online retail is set to surge with a 9.97% CAGR as direct-to-consumer brands sidestep shelf fees.

- Geographically, North America represented 41.92% of 2025's market value, while Asia-Pacific is anticipated to grow at a 9.01% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Energy Bar Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for convenient on-the-go nutrition | +1.8% | Global, with urban concentration in North America, Europe, and Asia-Pacific megacities | Short term (≤ 2 years) |

| Expansion of fitness culture in emerging markets | +1.5% | Asia-Pacific core (India, China, Southeast Asia), spill-over to Latin America and Middle East | Medium term (2-4 years) |

| Growth of plant-based and vegan energy bars | +1.3% | North America and Europe lead, Asia-Pacific accelerating due to lactose intolerance and environmental awareness | Medium term (2-4 years) |

| Sugar reduction enabled by next-gen sweetener-based launches | +1.0% | Global, with regulatory tailwinds in EU (EFSA approvals) and North America (FDA GRAS designations) | Short term (≤ 2 years) |

| Product innovation and functional ingredients incorporation | +1.2% | North America innovation hub, Europe clean-label focus, Asia-Pacific adoption of traditional botanicals | Medium term (2-4 years) |

| Premiumization and specialized positioning | +0.9% | North America and Europe affluent segments, emerging in Asia-Pacific urban centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing demand for convenient on-the-go nutrition

Urbanization and busier meal schedules are changing the way people snack. More consumers now prefer portable snacks that help boost energy and improve focus. Among working-age adults, skipping meals has increased the demand for nutrient-rich bars that combine protein and fiber. The rise of remote work has further disrupted traditional meal patterns, prompting brands to market these bars as practical choices for breakfast or mid-afternoon snacks. Americans are increasingly replacing traditional meals with snacks or smaller portions, a trend that continues to grow. In 2020, 38% of people reported substituting meals with snacks or smaller meals. By 2024, this figure rose to 56%, and it is expected to reach 62% in 2025[1]Source: International Food Information Council, "2025-IFIC-Food-Health-Survey", ific.org. Packaging innovations, such as resealable films and portion-control features, cater to the need for convenience while ensuring transparency about nutritional information.

Expansion of fitness culture in emerging markets

The expansion of fitness culture in emerging markets is becoming increasingly evident, driven by growing awareness of health and wellness. This trend is reflected in the rising participation in organized athletic events, such as marathons and relays, which have seen significant growth in recent years. For instance, the 2025 Manchester Marathon attracted 36,000 participants and hosted the England Marathon Championships, showcasing the increasing popularity of endurance sports[2]Source: England athletics, "April 2025: Performance round up", mext.go.jp. The shift toward active lifestyles is not only about individual fitness goals but also about fostering community engagement and collective motivation. Events like the Road Relays further highlight the role of teamwork and camaraderie in promoting fitness culture. This growing emphasis on healthier living presents opportunities for businesses in the fitness and wellness industry to cater to the evolving demands of this expanding market segment.

Growth of plant based and vegan energy bars

Plant based protein sources are gaining prominence in the energy bar market, driven by increasing consumer awareness of animal welfare, environmental sustainability, and lactose intolerance. Ingredients such as pea protein, rice protein, and soy isolates are being blended with chia seeds, hemp hearts, and cricket protein to create amino-acid profiles comparable to whey-based formulations. This segment is further supported by regulatory approvals that allow the use of innovative plant-based proteins in cereal bars, enabling manufacturers to achieve creamy textures without relying on dairy. Flexitarian consumers those who reduce but do not entirely eliminate animal products are an important target group. They value taste and texture over strict vegan labeling, encouraging brands to focus on sensory optimization and secure third-party non-GMO certifications. Additionally, allergen-free positioning is driving growth, as nut-free and gluten-free claims facilitate distribution in schools, hospitals, and airlines, where cross-contamination risks limit traditional bar options.

Sugar reduction enabled by next gen sweetener based launches

The energy bar market is undergoing a significant transformation as sugar reduction becomes a primary focus, driven by the adoption of next-generation sweeteners. With increasing consumer demand for healthier and functional snack options, manufacturers are incorporating innovative sweeteners such as aspartame, sucralose, and stevia-derived compounds into their formulations. These sweeteners, known for their intense sweetness compared to traditional sugar, allow producers to reduce sugar content while maintaining the desired taste and texture of energy bars[3]Source: U.S Food and Drug Administration, "Aspartame and Other Sweeteners in Food", fda.gov. Additionally, their low-calorie profile and minimal impact on blood sugar levels appeal to health-conscious consumers and those with specific dietary needs, further driving their adoption in the market. For instance, on April 28, 2025, Trek, a UK-based protein bar brand, introduced a new range of high-protein, low-sugar bars. This launch aligns with the sugar reduction trend in the energy bar market and addresses the rising demand for healthier snacking options. By leveraging next-generation sweeteners, Trek delivers reduced sugar content without compromising taste, demonstrating its commitment to innovation and setting a new benchmark in the sports nutrition category.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Intensifying competition from alternative snacks | -0.7% | Global, with pronounced effects in North America where snack innovation is highest | Short term (≤ 2 years) |

| Commodity price volatility in proteins and nuts | -0.9% | Global, with acute pressure in cocoa-dependent formulations (West Africa supply shocks) and almond-reliant bars (California drought cycles) | Short term (≤ 2 years) |

| Sustainability concerns over single-use wrappers | -0.5% | Europe (EU PPWR mandates), North America (state-level plastic bans), Asia-Pacific (emerging regulations) | Medium term (2-4 years) |

| Clean-label scrutiny limiting functional additives | -0.6% | North America and Europe, where consumer advocacy and regulatory oversight are most stringent | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Intensifying competition from alternative snacks

Energy bars face substitution pressure from protein chips, meat jerky, ready-to-drink protein shakes, and nut-butter pouches, as consumers continue to diversify their snacking portfolios. Jerky brands such as Jack Link's and Chomps have introduced grass-fed and organic variants that offer high protein content with minimal processing, appealing to paleo and carnivore-diet adherents who often perceive bars as overly processed. RTD shakes provide superior convenience no chewing required and brands like Fairlife and Premier Protein have secured refrigerated shelf space in convenience stores and gas stations, capturing impulse purchases that traditionally favored bars. Protein chips from Quest and PopCorners provide savory alternatives that satisfy cravings for crunch and salt, a sensory profile that sweet or neutral bars cannot replicate. This fragmentation impacts category growth, as retailers allocate limited shelf space across multiple snack formats, and digital advertising costs increase as brands compete for the same consumer attention. The competitive intensity is further heightened by private-label entrants that leverage retailer data to identify fast-moving SKUs and launch similar products at lower prices.

Commodity price volatility in proteins and nuts

Cocoa prices have recently declined as manufacturers, facing rising costs and tighter profit margins, have reduced their industrial demand. On the supply side, cocoa production is expected to increase during the 2025/2026 season, driven by favorable weather conditions and the maturation of newly planted cocoa trees in Ecuador. Despite the current price drop, industry projections suggest that cocoa prices may remain elevated, hovering around USD 6,000 per tonne. This sustained price level could result in higher confectionery prices, which may, in turn, impact sales volumes negatively. Similarly, the prices of whey protein concentrate and isolate have experienced fluctuations, largely influenced by shifts in the dairy market. Key factors contributing to this variability include the European Union's milk-production quotas and New Zealand's export volumes, both of which have created uncertainties on the supply side.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Organic Bars Gain Despite Conventional Dominance

In 2025, conventional energy bars accounted for 78.09% of the market revenue, supported by their extensive distribution networks, affordable pricing, and a broad range of flavors. These factors made them a popular choice among mass-market consumers who prioritize taste and cost over ingredient sourcing. Additionally, conventional bars continue to dominate in impulse-buy locations like gas stations, vending machines, and checkout aisles, where affordability and immediate energy needs drive purchasing decisions.

Organic energy bars are projected to grow at an impressive CAGR of 8.59% through 2031, outpacing the overall market. This growth is driven by rising demand from health-conscious consumers seeking USDA Organic and Non-GMO Project Verified certifications, which ensure pesticide-free ingredients and sustainable farming practices. While organic bars carry a price premium, these higher costs are justified by transparent supply chains, third-party audits, and marketing that highlights environmental and social benefits. Organic bars are also gaining momentum in natural-channel retailers like Whole Foods and Sprouts, where they represent a significant portion of total bar sales compared to conventional supermarkets.

By Protein Source: Plant-Based Leads, Animal-Based Accelerates

In 2025, plant-based protein sources dominated the market, accounting for 54.24% of the revenue. This growth was driven by the rising popularity of flexitarian diets, increasing environmental awareness, and the prevalence of lactose intolerance, which affects a significant portion of the global population. Key ingredients such as pea protein, soy isolate, and rice protein are often combined to create amino-acid profiles comparable to whey. Additionally, brands are exploring ingredients like chia seeds, hemp hearts, and cricket protein to stand out, although insect-based options face regulatory and consumer acceptance challenges. Plant-based bars are particularly successful in regions like Asia-Pacific, where vegetarianism is culturally ingrained, and Europe, where environmental regulations encourage sustainable product development.

Animal-based protein bars are emerging as the fastest-growing segment, with a projected 8.80% CAGR has slightly exceeds the overall market growth. This expansion is fueled by demand from endurance athletes and aging consumers who value the benefits of whey protein for muscle recovery and collagen peptides for joint health. Whey remains the preferred choice for post-workout recovery due to its rapid digestion and high bioavailability, a standard that plant proteins continue to strive toward. Collagen-infused bars are gaining traction as a hybrid category, addressing skin, bone, and connective tissue health, with brands like Vital Proteins and Ancient Nutrition leading innovation. The segment also benefits from clean-label trends emphasizing grass-fed and pasture-raised sourcing, which appeal to health-conscious consumers. However, regulatory compliance remains a key focus, as EFSA and FDA closely monitor health claims and labeling accuracy in this space.

By Function: Weight Management Outpaces Sports Nutrition

Sports and endurance nutrition bars dominate the market, capturing a significant share of 78.16%. This stronghold is driven by consistent demand from gym-goers, runners, and cyclists who prioritize products with balanced protein, carbohydrates, and electrolytes for hydration and recovery. Leading brands like Clif Bar, PowerBar, and Gatorade maintain their position through strategic sponsorships of marathons, triathlons, and professional sports leagues, which enhance brand equity and justify premium pricing. The segment also benefits from boutique fitness studios, such as CrossFit, Orangetheory, and Barry's Bootcamp, which sell these bars at their locations, targeting consumers immediately post-workout. However, the segment faces challenges as growth slows due to market maturity and rising competition from alternatives like ready-to-drink protein shakes and amino-acid supplements.

Weight-management and lifestyle-energy bars are the fastest-growing segment, with a projected CAGR of 9.17% through 2031. Their popularity stems from their appeal as meal replacements for busy professionals, shift workers, and parents balancing multiple responsibilities. These bars are designed to provide satiety and stabilize blood sugar, making them suitable as breakfast or lunch substitutes rather than snacks. Brands such as SlimFast, Atkins, and Zone Perfect have shifted their focus from diet-specific messaging to broader wellness themes, emphasizing balanced macronutrients and sustained energy. This repositioning has helped reduce the stigma associated with weight-loss products. Additionally, these bars are gaining traction in corporate wellness programs, where employers subsidize healthy snacks to promote employee well-being. Despite their growth, regulatory scrutiny remains a challenge, with the FDA and EFSA imposing strict guidelines on nutrient thresholds and calorie-reduction claims.

By Packaging Type: Multi-Pack Growth Reflects E-Commerce Shift

Single-pack bars accounted for 53.21% of the market in 2025, highlighting their dominance in convenience-driven retail spaces. These bars are a go-to choice for consumers making quick, impulse purchases at convenience stores, gas stations, and checkout aisles. Their popularity is further cemented by their strong presence in vending machines, gyms, and airports, where portability and portion control are essential. The convenience and accessibility of single-serve packaging ensure its continued leadership in these high-traffic, on-the-go channels.

Multi-pack boxes are positioned as the fastest-growing segment, with a projected CAGR of 8.81% through 2031. This growth is fueled by the rising adoption of e-commerce subscriptions, the expansion of warehouse-club retailers, and the increasing trend of stocking household pantries. These shifts, which gained traction during the pandemic, have become more entrenched as remote work normalizes. Multi-packs attract budget-conscious families and frequent consumers by offering cost savings and variety. Additionally, advancements in packaging, such as variety packs and sustainable materials, are helping brands cater to environmentally conscious shoppers while enhancing convenience and value.

By Distribution Channels: Online Retail Disrupts Traditional Shelf Space

Supermarkets/hypermarkets dominated the distribution market in 2025, holding a 42.65% share. Their leadership is driven by their extensive reach, ability to attract large volumes of customers, and impactful promotional strategies. These retailers effectively use techniques like prominent product placements and special offers to encourage both initial purchases and repeat buying. Additionally, traditional retailers benefit from impulse buying behavior, with strategically placed products near checkout counters prompting last-minute additions to shopping carts. In-store sampling further helps convert curious shoppers into loyal customers, reinforcing their stronghold in the market.

Online retail is the fastest-growing distribution channel, with a compound annual growth rate (CAGR) of 9.97% projected through 2031. This rapid growth is propelled by direct-to-consumer brands that bypass traditional retail costs, employ targeted digital marketing, and offer personalized subscription services to foster customer loyalty. While Amazon remains a dominant player in the online segment, niche platforms are steadily gaining traction. These platforms differentiate themselves by catering to specific dietary preferences and offering bulk purchase options, appealing to a growing base of health-conscious and convenience-driven consumers.

Geography Analysis

North America held the largest market share in 2025, contributing 41.92% of the total market value. The United States led the region, driven by its strong consumer demand and innovation in product offerings such as collagen-infused, keto-certified, and low-sugar options. Canada supported this dominance with its robust natural-channel presence, while Mexico's contract-manufacturing capabilities further enhanced the region's position. These combined factors established North America as the global leader in the market.

Asia-Pacific emerged as the fastest-growing region, with a projected compound annual growth rate (CAGR) of 9.01% through 2031. The region's growth was propelled by rising consumer spending and increasing interest in health and wellness. Both global multinationals and domestic companies played a significant role by introducing products tailored to local tastes and preferences. The region's economic progress and shifting consumer behaviors have made it a critical area for market expansion.

Other regions showcased unique growth opportunities and market dynamics. Europe focused on clean-label and sustainable products, aligning with regulatory directives on nutrient profiling and packaging waste. South America tapped into its wealth of indigenous ingredients, such as açaí and quinoa, to cater to the growing demand for natural and functional products. Meanwhile, the Middle East and Africa expanded its market through halal-certified product offerings and government-supported nutrition programs. While these regions currently trail in market share and growth rate, their localized strategies and supportive policies indicate promising potential for future development.

Competitive Landscape

The energy bar market is moderately fragmented. Large multinational companies like Mars, Mondelez, Nestlé, General Mills, and PepsiCo dominate the market, competing alongside smaller, specialized players such as Simply Good Foods (Quest, Atkins, OWYN), Glanbia (ThinkThin, Amazing Grass), and Built Brands. This competitive environment allows niche players to find opportunities by focusing on direct-to-consumer channels, personalized nutrition, and unique ingredient offerings. Simply Good Foods and Glanbia are examples of companies leveraging these strategies to strengthen their market presence, with premiumization trends driving consumer demand for clean-label and certified products.

Technological advancements are transforming the energy bar market, enabling brands to connect with consumers in innovative ways and improve operational efficiency. Augmented-reality packaging is being used to provide interactive content like recipe videos and workout tutorials, while blockchain technology ensures transparency by tracing ingredients back to their sources. Predictive analytics is helping brands manage inventory more effectively across online and physical stores. Smaller brands like FITCRUNCH are disrupting the market by using influencer collaborations, exclusive product launches, and targeted digital advertising to compete with larger players.

Opportunities in personalized nutrition are expanding as artificial intelligence enables brands to create customized products tailored to individual needs. AI-driven platforms can analyze biometric data to recommend specific macronutrient combinations, offering consumers a more personalized experience. Subscription models that include auto-replenishment and flavor customization are also gaining popularity, helping brands reduce customer-acquisition costs and build long-term loyalty. Regulatory frameworks, such as FDA and EFSA guidelines, ensure that product claims are backed by evidence, fostering trust and transparency. As technology adoption grows, companies that embrace these innovations are better positioned to meet changing consumer preferences and drive sustainable growth in the market.

Energy Bar Industry Leaders

-

General Mills Inc.

-

Mars Inc.

-

Nestlé S.A.

-

Mondelez International Inc.

-

Post Holdings, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Nutri-Grain, the cereal brand owned by Mars, debuted Nutri-Grain Crunchy in the US. This new snack bar aimed to cater to the rising consumer appetite for whole grains and fiber-rich choices.

- January 2026: Junkless has launched a Peanut Butter Chocolate Brownie protein bar, boasting 15 grams of plant-based protein, a low sugar content, and an allergen-free profile. This strategic move targets schools, hospitals, and workplaces that uphold stringent dietary standards.

- December 2025: RxBar, a Kellanova brand, has introduced Protein Energy Bites in the U.S. These bites, made from egg-white protein, dates, and nuts, come in convenient sizes for portion control and feature resealable packaging. Aimed at on-the-go consumers, the launch seeks to provide a snackable alternative to traditional bars, broadening RxBar's market reach beyond just fitness aficionados.

- January 2025: Tandem Foods merged TruFood Manufacturing with Bar Bakers, creating a vertically integrated co-manufacturing platform with an annual capacity of 200 million bars. The merger provided smaller brands access to extrusion, enrobing, and packaging capabilities, reducing equipment investment needs and accelerating innovation cycles.

Global Energy Bar Market Report Scope

An energy bar is a healthy snack with nutritional ingredients that boost energy and endurance. The energy bar market is segmented by type, distribution channel, and geography. Based on type, the market studied is segmented into organic and conventional. The market is segmented by distribution channel into supermarkets/hypermarkets, convenience stores, specialty stores, online retail stores, and other distribution channels. The report also analyzes the market studied in emerging and established regions, including North America, Europe, South America, Asia-Pacific, Middle-East, and Africa. For each segment, the market sizing and forecasts have been done based on value (in USD million).

By Product Type

| Organic |

| Conventional |

By Protein Source

| Plant-Based |

| Animal-Based |

By Function/Application

| Sports and Endurance Nutrition |

| Meal Replacement |

| Weight Management and Lifestyle Energy |

By Pakaging Type

| Single-Pack Bars |

| Multi-Pack Boxes |

By Distribution Channels

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Specialty Stores |

| Online Retail Stores |

| Other Distribution Channels |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Organic | |

| Conventional | ||

| By Protein Source | Plant-Based | |

| Animal-Based | ||

| By Function/Application | Sports and Endurance Nutrition | |

| Meal Replacement | ||

| Weight Management and Lifestyle Energy | ||

| By Pakaging Type | Single-Pack Bars | |

| Multi-Pack Boxes | ||

| By Distribution Channels | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Specialty Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the energy bars market and its CAGR through 2031?

The energy bars market size stands at USD 4.53 billion in 2026 and is projected to reach USD 6.81 billion by 2031, advancing at an 8.50% CAGR from 2026 to 2031.

Which product type leads category revenues?

Conventional formulations led with 78.09% of 2025 global value, thanks to wide distribution and lower retail prices.

What segment is expected to grow fastest?

Weight-management and lifestyle energy bars are forecast to post the quickest gains with a 9.17% CAGR through 2031.

Why are multi-pack boxes gaining popularity online?

E-commerce subscriptions, variety packs, and 15-25% per-unit savings are shifting households toward pantry-stocking multi-packs.

Page last updated on: