Sound Recognition Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

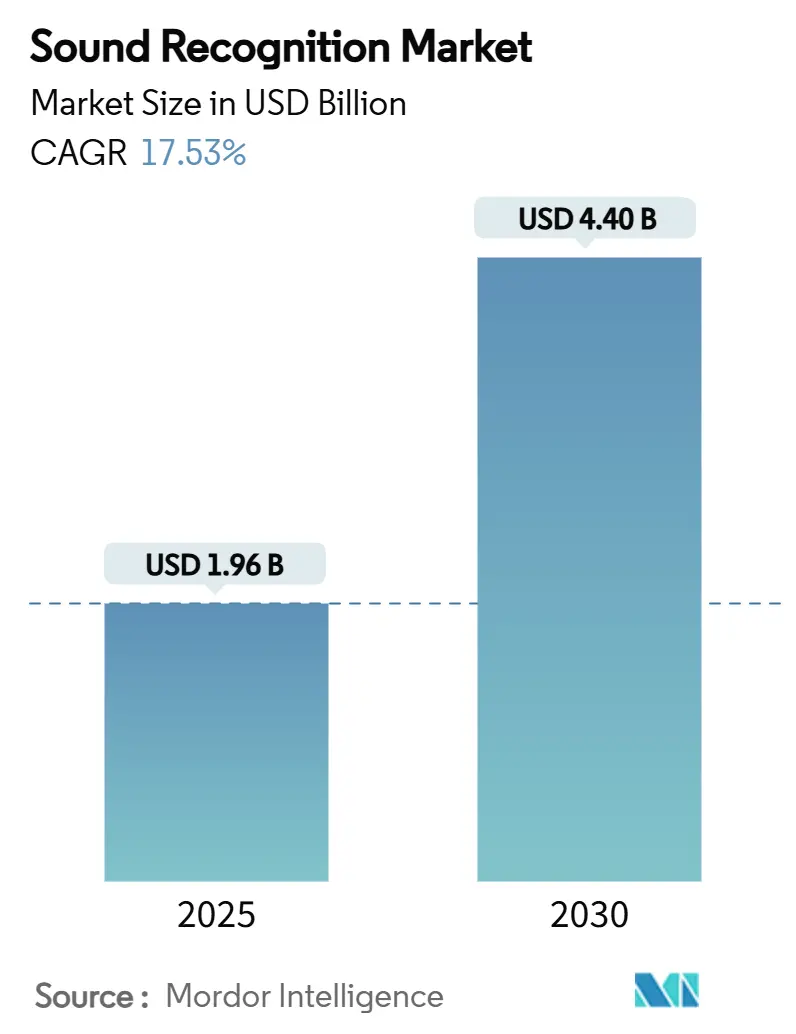

| Market Size (2025) | USD 1.96 Billion |

| Market Size (2030) | USD 4.40 Billion |

| Growth Rate (2025 - 2030) | 17.53% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sound Recognition Market Analysis by Mordor Intelligence

The sound recognition market size is USD 1.96 billion in 2025 and is forecast to climb to USD 4.40 billion by 2030, translating into a 17.53% CAGR over the period. Heightened demand for real-time audio analytics on battery-powered devices, tighter privacy legislation that favors on-device processing, and stricter industrial monitoring mandates collectively propel the sound recognition market. Technology suppliers are blending ultra-low-power edge-AI chips with traditional digital signal processing to meet latency targets without compromising energy budgets. In parallel, automotive safety rules that mandate acoustic warnings for electric vehicles, as well as consumer enthusiasm for voice-first interfaces, continue to broaden the adoption base. Supply-chain nearshoring and multi-foundry sourcing strategies help mitigate recent semiconductor shortages, supporting healthy expansion for the sound recognition market through 2030.

Key Report Takeaways

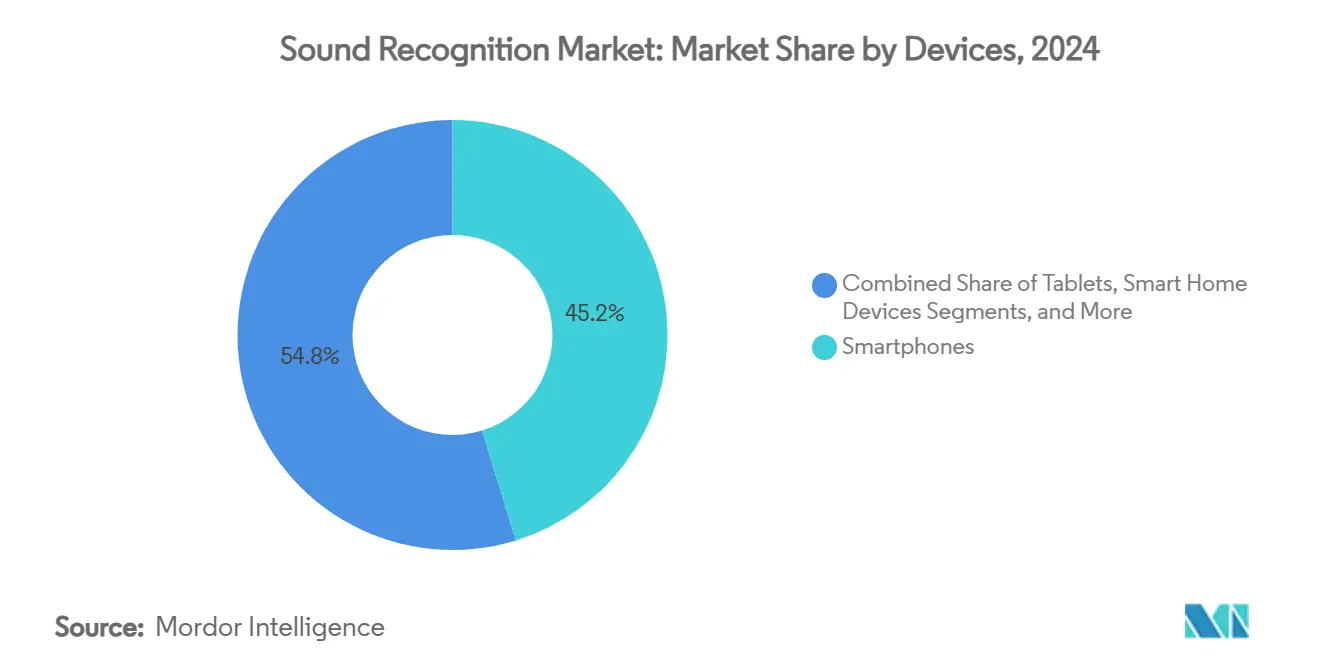

- By devices, smartphones led with 45.23% revenue share in 2024, while connected cars recorded the fastest 17.58% CAGR through 2030.

- By deployment mode, cloud solutions accounted for 68.89% of the sound recognition market share in 2024; edge processing is advancing at a 17.83% CAGR as privacy rules tighten.

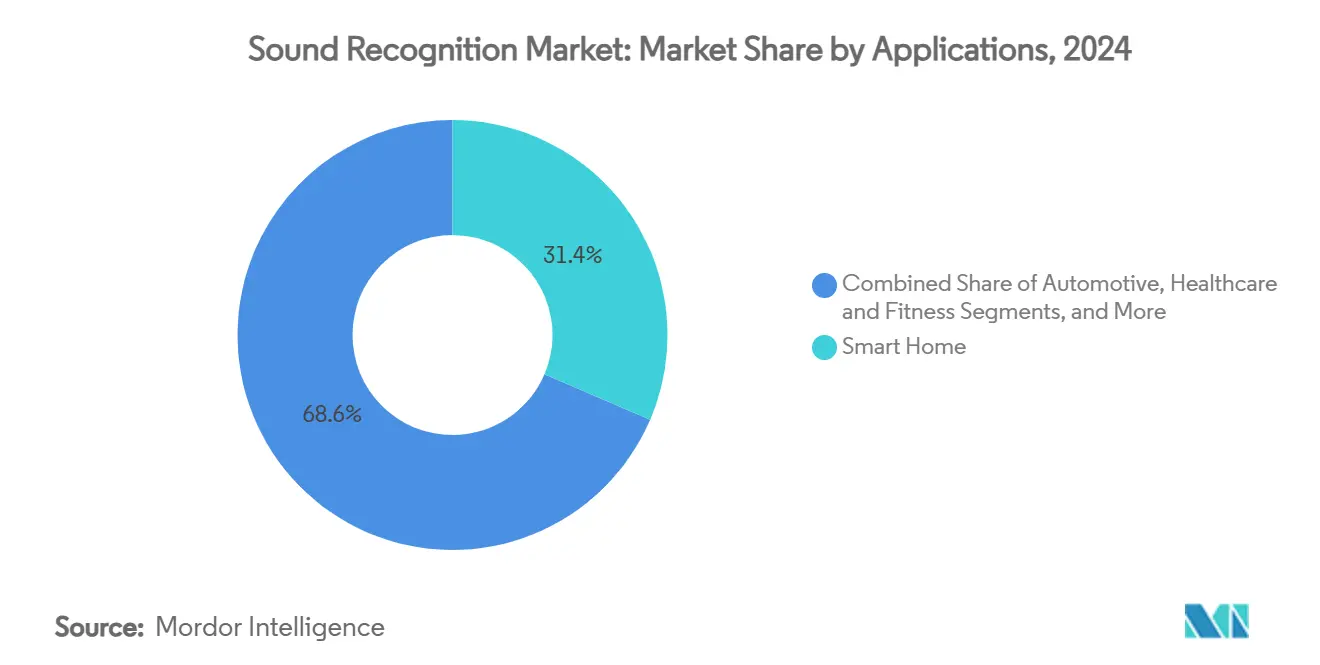

- By application, smart-home systems represented a 31.44% slice of the sound recognition market size in 2024, whereas automotive use cases are expanding at a 17.93% CAGR to 2030.

- By technology, traditional DSP approaches retained 40.86% share in 2024, yet edge-AI-optimized chips are scaling at a 17.87% CAGR.

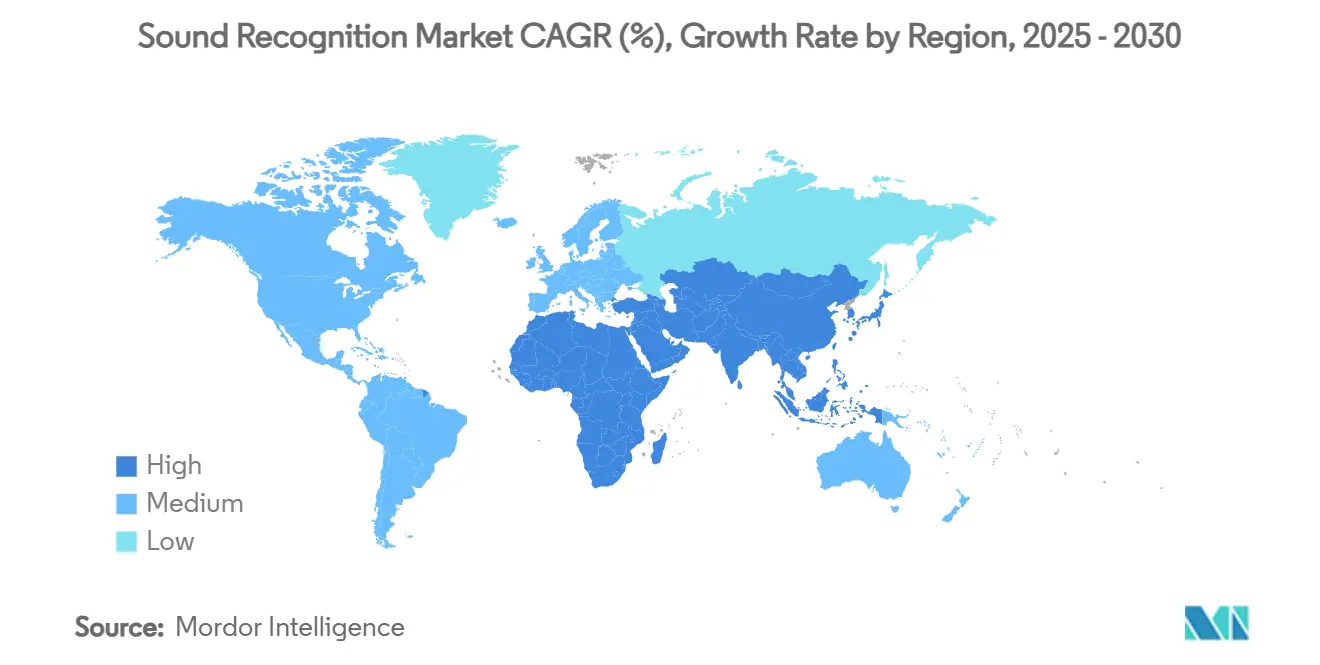

- By geography, North America dominated with 35.27% share in 2024, while Asia-Pacific is accelerating at an 18.11% CAGR.

Global Sound Recognition Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of voice-enabled virtual assistants | +3.2% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Growing demand for sound-based security and surveillance | +2.8% | Global, with emphasis on industrial regions in Asia-Pacific and North America | Long term (≥ 4 years) |

| Integration in automotive ADAS and infotainment | +3.5% | North America, Europe, and Asia-Pacific automotive manufacturing hubs | Medium term (2-4 years) |

| Proliferation of IoT and smart-home nodes | +2.9% | Global, with early adoption in developed markets | Long term (≥ 4 years) |

| Regulatory push for acoustic anomaly detection in industry | +2.1% | North America and Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Edge-AI chips enabling ultra-low-power on-device analytics | +3.8% | Global, with manufacturing concentration in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Integration in Automotive ADAS and Infotainment

Updated safety codes obligate electric and hybrid vehicles to broadcast artificial warning sounds, creating a USD 2.3 billion addressable electronics opportunity over the forecast horizon. [1]Qualcomm Technologies, “Snapdragon 8 Elite Launch,” qualcomm.comAutomakers now embed multi-channel acoustic sensors that detect emergency-vehicle sirens and construction alerts to complement radar and vision stacks. Qualcomm’s latest Snapdragon 8 Elite platform delivers sub-100 millisecond classification latency, meeting stringent automotive functional-safety budgets. Electric-vehicle makers also use sound signatures as brand differentiators, strengthening customer recognition while satisfying regulations. These mandates, paired with consumer demand for hands-free infotainment control, elevate the sound recognition market across connected-vehicle ecosystems.

Edge-AI Chips Enabling Ultra-Low-Power On-Device Analytics

Semiconductor vendors have shrunk inference power budgets from milliwatts to microwatts by introducing neural decision processors such as Syntiant’s NDP120, which draws under 140 µW while streaming audio continuously. [2]Institute of Electrical and Electronics Engineers, “The Internet of Sounds,” ieee.org Airoha’s AB1595 system-on-chip adds machine-learning engines directly inside Bluetooth headsets, slashing round-trip latency to below 20 milliseconds and eliminating cloud dependencies. These advances unlock always-listening functions in hearables, wearables, and smart sensors without eroding battery life. The result is a broader addressable surface for the sound recognition market, especially in health monitoring, language translation, and biometric authentication use cases.

Growing Demand for Sound-Based Security and Surveillance

Factories adopt acoustic analytics to flag equipment anomalies before catastrophic failure, complying with Occupational Safety and Health Administration noise-monitoring directives. Predictive-maintenance deployments in Mexico’s semiconductor hubs have already cut unplanned downtime by up to 50% according to facility reports. [3]Co-Production International, “Semiconductor Manufacturing in Mexico,” co-production.net Surveillance firms integrate acoustic classifiers that detect glass breakage, aggression, or firearm discharges, raising situational awareness in public spaces. These security imperatives amplify enterprise spending and sustain double-digit growth in the sound recognition market.

Proliferation of IoT and Smart-Home Nodes

Voice-assistant penetration in mature economies provides a ready installed base for ambient sound monitoring. Amazon’s Alexa Guard showcases the value of passive listening by alerting users to smoke alarms or breaking glass without explicit commands. Smart-home platforms now pair acoustic fingerprinting with power-meter data to optimize appliance usage, yielding documented household energy savings of up to 20%. Edge frameworks distribute inference loads across multiple endpoints, trimming cloud bandwidth while tightening response loops-dynamics that continuously widen the sound recognition market footprint.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High false-positive rate and ambient-noise interference | -2.1% | Global, with greater impact in urban environments | Short term (≤ 2 years) |

| Data-privacy concerns with always-listening devices | -2.8% | Europe and North America, with GDPR and similar regulations | Medium term (2-4 years) |

| Lack of standardized evaluation benchmarks | -1.4% | Global, affecting interoperability and adoption | Long term (≥ 4 years) |

| Fragmented patent landscape and royalty-stacking risk | -1.9% | Global, with concentration in technology hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data-Privacy Concerns with Always-Listening Devices

GDPR classifies biometric audio as sensitive data, obligating explicit consent and data minimization. Apple responded by shifting initial Siri parsing to on-device neural engines and adding differential-privacy masking during cloud retraining. Similar approaches raise bill-of-materials costs, squeezing margin-sensitive consumer tiers. Healthcare deployments must also encrypt biomarker streams, creating extra processing overhead. Unless silicon costs fall, privacy safeguards could slow the adoption cadence within the sound recognition market in regulated economies.

High False-Positive Rate and Ambient-Noise Interference

City soundscapes routinely exceed 70 dB, masking critical acoustic cues and reducing classifier precision. Benchmark studies from the Detection and Classification of Acoustic Scenes and Events (DCASE) initiative show only 65-75% accuracy in real-world noise conditions. False alarms erode user trust, particularly in security systems where nuisance alerts drain operational budgets. Vendors are therefore investing in multi-microphone beamforming and noise-robust models, but the added hardware raises power draw-an unwelcome trade-off for battery-based products within the sound recognition market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Devices: Smartphones Lead as Connected Cars Accelerate

Smartphones held 45.23% of the sound recognition market share in 2024, leveraging annual silicon upgrades that integrate edge-AI tensors and array microphones. These volumes cement smartphones as the economic anchor of the sound recognition market. Hearables and smart wristbands follow close behind, propelled by health-monitoring capabilities such as arrhythmia detection delivered through micro-speaker analysis. Luxury automakers deploy active-road-noise cancellation and siren detection, resulting in a robust 17.58% CAGR that is repositioning connected cars as the next growth engine. Tablets and smart speakers remain stable but show lower elasticity because replacement cycles lengthen in developed regions.

Continuous silicon evolution pushes the sound recognition market size higher in mobile domains, while automotive platforms benefit from longer design cycles but richer bill-of-materials. In-cabin acoustic analytics shape advanced driver-assistance features, extend battery range by optimizing HVAC blower noise, and deliver personalized infotainment profiles. The smartphone ecosystem, meanwhile, pioneers federated-learning techniques that keep raw voice data on the handset, reinforcing privacy compliance and seeding downstream improvements for other device classes.

By Deployment Mode: Cloud Dominance Faces Edge Momentum

Cloud processing owned 68.89% of value in 2024 because training large acoustic models still demands hyperscale resources. This segment secures recurring revenue via usage fees, anchoring cash-flow predictability for major providers. Edge instances, however, are expanding at a 17.83% CAGR as regulatory bodies endorse local inference to curb data leakage. The hybrid pattern, where models train centrally but execute locally, is becoming the default architecture and sustains balanced capex across data-center and device layers.

As semiconductor firms ramp domestic fabs under the CHIPS Act, unit availability of specialized edge AI processors is forecast to rise, tempering cost premiums and lifting edge adoption further. Enterprises with strict data-sovereignty mandates-especially in healthcare and defense-prefer on-premise clusters that deliver millisecond decision loops without opening traffic to the public internet. Together, these vectors reinforce a segmented yet symbiotic deployment fabric underlying the broader sound recognition market.

By Applications: Smart Home Leadership Yields to Automotive Growth

Smart homes generated 31.44% of 2024 revenue, capitalizing on the extensive footprint of voice assistants and DIY security kits. Nonetheless, automotive revenue is advancing at a 17.93% CAGR thanks to legal necessities for acoustic vehicle-alerting systems and emerging driver-monitoring algorithms. Healthcare and fitness wearables extract respiratory and cardiac signals from body-borne microphones, a field that promises premium reimbursements once clinical validation finalizes.

Security and surveillance span both consumer and enterprise segments, using sound analytics to detect aggression, gunshots, or mechanical anomalies. Such deployments often combine acoustic channels with cameras, raising precision while reducing false positives. As the automotive pipeline scales, the sound recognition market size for vehicle platforms is projected to leapfrog residential revenues in the second half of the decade, though final ordering will depend on macroeconomic vehicle-production volumes.

By Technology: DSP Leads, Edge-AI Chips Surge

Legacy digital signal processing commanded 40.86% revenue in 2024 because the technique delivers deterministic latency without heavy memory loads, crucial for safety-critical systems. Machine-learning overlays refine these pipelines by adding adaptable pattern recognition. The most vigorous trajectory emerges from edge-AI-optimized chips that post a 17.87% CAGR, embedding convolutional layers directly in silicon for microwatt consumption. Deep-learning stacks serve niche verticals such as medical diagnostics where data patterns are complex and accuracy gains outweigh compute cost.

Hybrid architectures now pair classical DSP filters with neural post-processors, extracting higher-order features while constraining power budgets. The resulting silicon road-map underpins the expansion of the sound recognition market, as vendors can scale performance tiers from entry-level smart tags to flagship mobiles.

Geography Analysis

North America kept 35.27% of sector revenue in 2024 through early consumer uptake of voice-enabled speakers and robust automotive safety statutes. Federal incentives encouraging domestic wafer fabs aim to insulate supply lines for edge-AI chipsets, a move likely to preserve the region’s leadership kernel until the next decade. Canada contributes by subsidizing smart-city pilots that integrate acoustic gunshot detection into municipal safety networks, reinforcing the region’s ecosystem depth.

Asia-Pacific is tracking an 18.11% CAGR, fueled by large-scale electronics manufacturing, aggressive 5G rollouts, and rising middle-class consumption of connected devices. China’s conversational-AI services maintain break-neck growth, while Japan funds voice-controlled elder-care robots to mitigate caregiver shortages. South Korea’s handset OEMs preload multi-language offline speech models to serve overseas markets, further expanding the regional export footprint within the sound recognition market.

Europe sustains steady expansion under privacy-centric policy frameworks that accelerate on-device processing. Germany’s industrial automation boom feeds demand for acoustic predictive-maintenance modules, whereas Nordic utilities deploy underwater sound sensors to monitor offshore wind turbines. Southern European nations leverage EU recovery funds for smart-infrastructure retrofits that embed acoustic surveillance into transport corridors. Emerging regions in Middle East, Africa, and South America record nascent adoption curves but benefit from telecom upgrades and nearshoring initiatives that attract assembly facilities and engineering talent.

Competitive Landscape

Competition is moderately fragmented, placing a premium on ecosystem breadth and silicon ownership. Apple, Google, Amazon, and Microsoft embed proprietary neural accelerators-such as Apple’s Neural Engine and Google’s Tensor Processing Unit-across their hardware line-ups, creating closed-loop optimization between software and chips. These vertical stacks lower latency, cut energy draw, and erect platform lock-in moats that steer developer allegiance.

Specialists like SoundHound AI, Sensory, and Audio Analytic chase vertical niches ranging from automotive voice assistants to industrial safety monitoring. SoundHound’s USD 80 million acquisition of Amelia AI in January 2025 enlarges its enterprise footprint and fortifies conversational depth. Patent licensing remains a two-edged sword: royalty streams reward early innovators, yet cross-claims elevate legal risk and can stall commercialization timelines.

Reshoring megaplans-highlighted by Texas Instruments’ USD 60 billion multistate fab buildout-aim to dilute supply fragility after recent chip shortages. Foundry diversity benefits smaller chipmakers such as Syntiant and Ambiq that fab specialized audio processors. Over the forecast window, M&A is expected to intensify as general-purpose cloud vendors seek edge portfolios, and as automotive Tier 1 suppliers purchase software houses to secure feature roadmaps for autonomous platforms within the sound recognition market.

Sound Recognition Industry Leaders

Apple Inc.

Alphabet Inc. (Google)

Amazon.com Inc.

Microsoft Corporation

Samsung Electronics Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Texas Instruments committed USD 60 billion to seven U.S. fabs to secure supply of analog and embedded processors for audio analytics.

- January 2025: SoundHound AI acquired Amelia AI for USD 80 million, broadening enterprise conversational offerings.

- December 2025: Qualcomm released the Snapdragon 8 Elite with a dedicated audio NPU offering 50× prior-generation AI throughput.

- November 2025: Apple reported USD 85.8 billion quarterly revenue, underscoring increased capex on privacy-centric on-device audio processing.

Global Sound Recognition Market Report Scope

| Smartphones |

| Tablets |

| Smart Home Devices |

| Smart Speakers |

| Connected Cars |

| Hearables |

| Smart Wristbands |

| On-premise |

| Cloud |

| Automotive |

| Healthcare and Fitness |

| Smart Home |

| Security and Surveillance |

| Traditional DSP Algorithms |

| Machine-Learning Models |

| Deep-Learning Models |

| Edge-AI Optimized Chips |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Devices | Smartphones | ||

| Tablets | |||

| Smart Home Devices | |||

| Smart Speakers | |||

| Connected Cars | |||

| Hearables | |||

| Smart Wristbands | |||

| By Deployment Mode | On-premise | ||

| Cloud | |||

| By Applications | Automotive | ||

| Healthcare and Fitness | |||

| Smart Home | |||

| Security and Surveillance | |||

| By Technology | Traditional DSP Algorithms | ||

| Machine-Learning Models | |||

| Deep-Learning Models | |||

| Edge-AI Optimized Chips | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the sound recognition market?

The sound recognition market size is USD 1.96 billion in 2025 and is projected to reach USD 4.40 billion by 2030.

Which device category contributes the most revenue?

Smartphones contribute 45.23% of 2024 revenue thanks to their vast installed base and annual hardware refresh cycles.

Why are connected cars viewed as a key growth area?

Regulatory mandates for acoustic vehicle-alerting systems and demand for voice-driven infotainment push connected-car revenue at a 17.58% CAGR through 2030.

How are privacy regulations shaping technology adoption?

GDPR and comparable rules favor on-device inference, driving a 17.83% CAGR for edge deployments as vendors minimize cloud audio transfers.

Which region is expanding the fastest?

Asia-Pacific leads with an 18.11% CAGR, propelled by consumer electronics scale, 5G coverage, and government AI initiatives.

What is the biggest technological shift in the sector?

The integration of ultra-low-power neural processors into everyday devices enables always-listening features without draining batteries, broadening the sound recognition market.

Page last updated on: