Professional Audio Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 13.26 Billion |

| Market Size (2031) | USD 17.82 Billion |

| Growth Rate (2026 - 2031) | 6.10% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Professional Audio Market Analysis by Mordor Intelligence

The professional audio market size was valued at USD 12.50 billion in 2025 and estimated to grow from USD 13.26 billion in 2026 to reach USD 17.82 billion by 2031, at a CAGR of 6.1% during the forecast period (2026-2031). Demand shifts from equipment ownership to experience-driven solutions, live-event resurgence, and enterprise hybrid-work upgrades form the core growth pillars. Networked protocols such as AES67 and Dante reduce interoperability barriers, encouraging facilities to refresh legacy infrastructure.[1]Source: QSC, “AES-67 and the Future of Interoperability,” qscaudio.com

Supply chain redesigns that minimize semiconductor exposure and a pivot toward software-defined features strengthen recurring revenue streams. Meanwhile, convergence of building systems with audio, evidenced by Acuity Brands’ acquisition of QSC, signals new competitive dynamics where lighting, HVAC, and sound platforms interconnect.

Key Report Takeaways

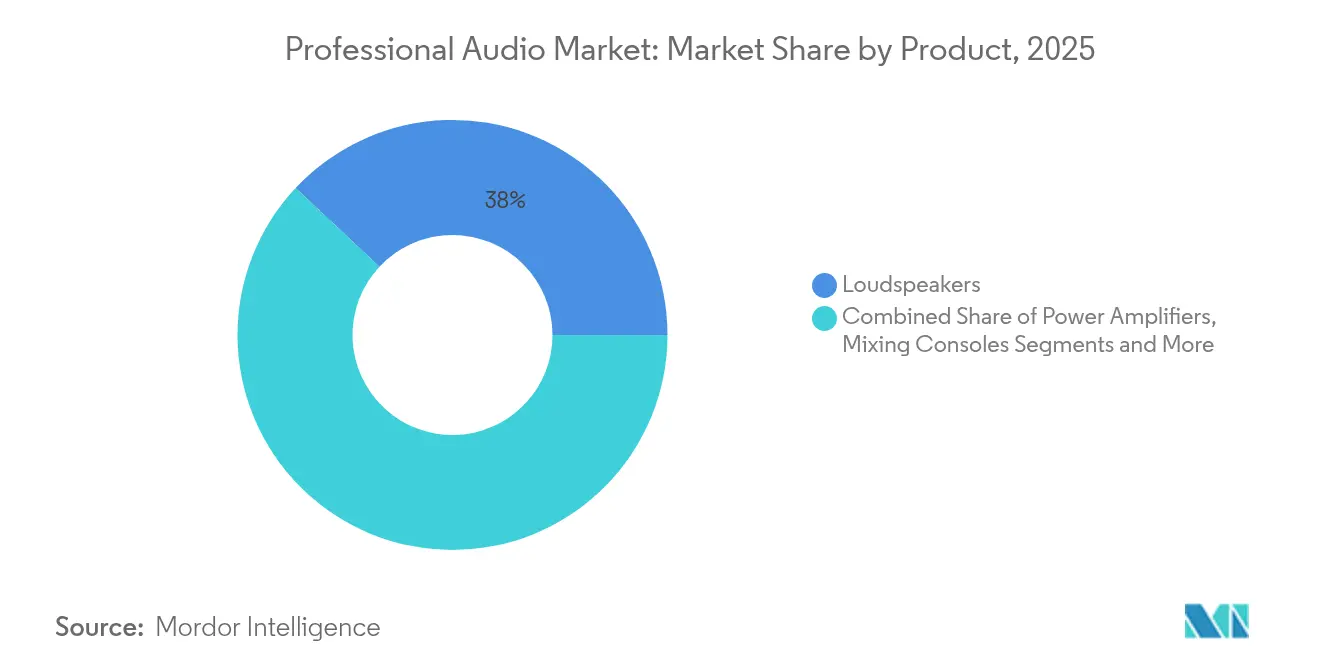

- By product category, loudspeakers led with 38.02% revenue share in 2025, while wireless microphones posted the highest growth at an 7.45% CAGR through 2031.

- By connectivity, wired systems accounted for 56.85% share in 2025, whereas wireless solutions are forecast to expand at a 7.22% CAGR to 2031.

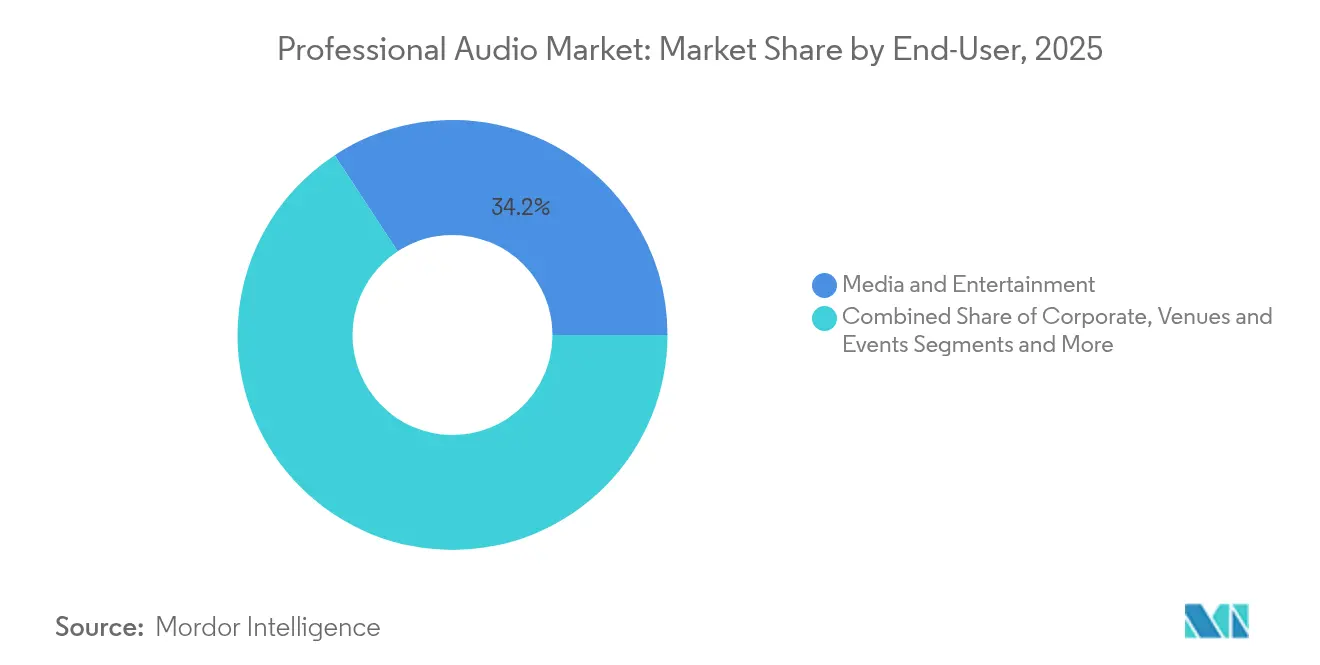

- By end-user, media and entertainment captured 34.23% share in 2025; venues and events record the fastest trajectory at a 6.9% CAGR through 2031.

- By application, live Sound reinforcement captured 32.25% share in 2025; broadcast and streaming record the fastest trajectory at a 7.35% CAGR through 2031.

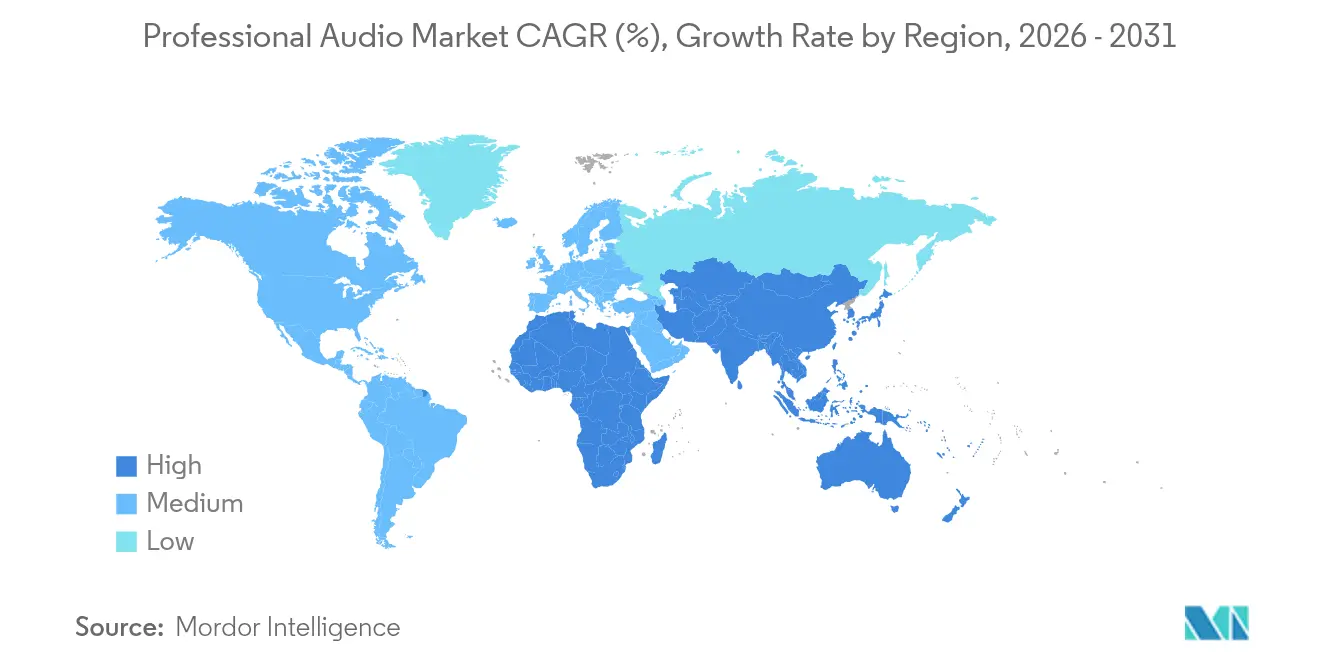

- By geography, North America held 33.12% of the professional audio market share in 2025, and Asia-Pacific is set to grow at a 7.22% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Professional Audio Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid live-events and experiential marketing rebound | +1.8% | North America and Europe | Medium term (2–4 years) |

| Creator-economy demand for studio gear | +1.2% | Asia-Pacific and North America | Short term (≤2 years) |

| Expansion of networked-AV interoperability | +1.0% | North America and Europe | Long term (≥4 years) |

| Rise of immersive and spatial formats | +0.9% | Premium global markets | Medium term (2–4 years) |

| Hybrid-work spending on high-fidelity conferencing | +0.8% | North America and Europe | Short term (≤2 years) |

| Smart-city public-address funding | +0.5% | Asia-Pacific and Middle East and Africa | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of Live-Events and Experiential Marketing

Ticket volumes at major concerts increased 26% year over year in 2024, spurring rental firms and venues to replace aging arrays with cardioid sub-array systems that meet stricter noise ordinances while preserving punch[2]Source: Live Nation Entertainment, “2024 Form 10-K,” livenationentertainment.com. Festival operators monetize premium sound zones that tie experiential marketing to sponsorship revenue, as seen at Ultra Music Festival 2025[3]Source: BizBash, “5 Music Event Trends Making Noise in 2025,” bizbash.com. Hybrid corporate shows need low-latency bridging between onsite and virtual audiences, driving sales of scalable digital consoles. Sphere Entertainment’s 167,000-speaker install illustrates how immersive architecture elevates brand engagement[4]Source: InAVate, “Immersive Tech to Bring Out Unheard Audio From The Wizard Of Oz at Sphere,” inavateonthenet.net. The professional audio market therefore sees elevated demand for flexible loudspeaker configurations and high-density wireless channels that streamline quick show turnovers.

Surging Creator-Economy Demand for Studio-Grade Gear

China logged 747 million online audio users in 2024, generating a sector worth USD 68.86 billion, underlining how individual content creators influence professional purchasing decisions. Global podcast revenue surpassed USD 30 billion the same year, pushing microphone makers to launch USB-XLR hybrids that combine convenience with expandability. Visual brand aesthetics matter; larger broadcast-style microphones improve on-camera credibility, boosting uptake of units such as Shure’s MV7i that integrate real-time voice processing. Mid-tier manufacturers capitalize by bundling software plug-ins alongside hardware, converting first-time buyers into subscription clients. This driver enlarges the addressable professional audio market by expanding the end-user base beyond traditional studios.

Growth of Networked-AV and AES67/Dante Interoperability

AES67 allows Dante, RAVENNA, and Livewire+ devices to coexist, easing historical vendor lock-in issues. More than 3,000 certified Dante products create a network effect that accelerates adoption of unified control software, even while QoS settings must be meticulously planned to avoid packet-loss dropouts in mixed-protocol environments. Collaboration between L-Acoustics and d&b audiotechnik on Milan Manager demonstrates how fierce competitors collaborate on transport layers to satisfy integrators’ demand for open ecosystems. As facilities migrate to IP, integrators with network optimization expertise gain strategic importance. These developments guide the professional audio market toward platform-based competition rather than discrete hardware rivalry.

Shift to Immersive and Spatial-Audio Formats

In 2024, 93% of Billboard Top 100 tracks released Dolby Atmos masters, turning immersive rendering into a mainstream requirement. Automotive rollouts by Cadillac and Audi confirm cross-industry momentum as vehicles integrate 3D sound domains starting 2025. Theater producers adopt spatial canvases that blend infrasound and haptics, evidenced by King Lear’s run at The Shed in New York City. Equipment chains now need dedicated render engines, multichannel monitoring, and object-based routing; Audient’s ORIA interface typifies how vendors align new SKUs with format adoption. The professional audio market benefits as broadcasters and studios retool control rooms, driving upgrades across consoles, monitors, and metering software.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Semiconductor supply-chain volatility | -1.5% | Global, high Asia exposure | Medium term (2–4 years) |

| High total cost of ownership for tour systems | -0.8% | Global, mid-tier venues hit hardest | Short term (≤2 years) |

| Counterfeit and grey-market components | -0.6% | Price-sensitive regions | Long term (≥4 years) |

| Rising e-waste compliance costs | -0.4% | Europe and North America | |

| Source: Mordor Intelligence | |||

Persistent Semiconductor Supply-Chain Volatility

Lead times for DSP cores and RF transceivers extend past 60 weeks, forcing design teams to qualify substitute parts or strip advanced features. U.S. semiconductor imports reached USD 139 billion in 2024 amid tariff hikes that raised landed costs. Smaller audio brands compete against large tech firms for wafer allocation, often paying premiums or shrinking production runs. Component obsolescence accelerates, leading some vendors to sunset digital SKUs in favor of analog lines requiring fewer chips. The professional audio market thus faces margin compression until fab capacity aligns with demand.

High Total Cost of Ownership for Tour-Grade Systems

A complete modern line array can exceed USD 500,000, limiting adoption to major arenas and top-tier rental companies. Raw material inflation, particularly neodymium for drivers, inflates bill-of-materials costs despite weight reductions delivered by next-generation magnets. Insurance premiums climb as replacement values rise, while skilled-technician shortages increase labor cost for rigging and tuning. Venues with constrained budgets phase projects, extending equipment life cycles and slowing the professional audio market upgrade pace. Mid-range manufacturers respond with modular products that allow incremental expansion rather than full system overhauls.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Loudspeakers Anchor Revenue Streams

Loudspeakers contributed 38.02% of the professional audio market size in 2025, confirming their centrality across touring, fixed install, and hybrid venues. Replacement cycles accelerated after pandemic-era downtime, with many arenas adopting cardioid sub-arrays that improve low-frequency directionality while complying with municipal noise codes. Meanwhile, wireless microphones advance at an 7.45% CAGR on the back of regulatory spectrum reallocations that compel users to retire analog UHF units. Manufacturers answer with encrypted digital platforms that fit within shrinking frequency bands, safeguarding performance in congested RF environments.

The loudspeaker segment drives value-added demand for amplification, rigging, and control software that elevate system performance through FIR-based beam steering. Vendors unlock software subscriptions that activate prediction modules, converting one-time hardware sales into recurring revenue. Microphone makers explore WMAS-based ecosystems, such as Sennheiser’s Spectera, which delivers 64 channels inside a single 6 MHz block and illustrates how advanced modulation counters spectrum scarcity. Accessories like Dante breakout boxes and PoE-powered stage boxes fill integration gaps, rounding out wallet share captured by vendors inside the professional audio market.

By Connectivity: Wireless Momentum Gathers Pace

Wired solutions retained 56.85% share of the professional audio market size in 2025 thanks to mission-critical applications that resist RF risk, including government chambers and broadcast studios. Cat6a cable and redundant ring topologies guarantee near-zero latency and facilitate power distribution through PoE++. Yet wireless units are forecast to post a 7.22% CAGR to 2031 as Wi-Fi 7 unlocks 6 GHz channels and improves deterministic scheduling. Early Dante-over-Wi-Fi prototypes demonstrate sub-5 ms latency, narrowing the performance gap against Ethernet.

Battery innovation extends runtime to 40 hours at moderate SPL for portable PA boxes, widening addressable outdoor use cases. Managed-frequency coordination apps powered by cloud databases simplify deployment, lowering expertise barriers for volunteer operators. Despite counterfeit RF modules adding complexity, educational initiatives by industry bodies help mitigate interference through standardized scanning protocols. Wired and wireless ecosystems coexist as integrators design fail-over architectures that blend both, ensuring the professional audio market satisfies reliability and flexibility expectations simultaneously.

By End-User: Media and Entertainment Sustains Leadership

Media and entertainment delivered 34.23% revenue in 2025, buoyed by immersive mastering suites and premium broadcast trucks that adopt IP audio to handle rising channel counts. Sports rights competition accelerates upgrades as networks seek immersive fan experiences. Venues and events, growing at a 6.9% CAGR, benefit from corporate activations where audio quality now doubles as a branding tool. Hybrid ticketing models expand rental inventories of scalable line arrays that transition from stadiums to convention centers overnight.

Corporate adopters outfit meeting rooms with ceiling arrays and AI-driven echo cancellation to harmonize in-person and remote voices. Education and houses of worship pursue compliance with accessibility standards while combining traditional sermons with multimedia experiences. Retail and hospitality chains install branded soundscapes that increase dwell time, demonstrated by boutique hotels embracing object-based playback to differentiate guest experiences. Such cross-vertical deployments enlarge the professional audio market beyond its historic entertainment core.

By Application: Live Sound Reinforcement Remains Dominant

Live sound reinforcement controlled 32.25% share of the professional audio market size in 2025 as touring activity rebounded with 26% higher ticket sales. New portable line arrays balance fast deployment with pattern control, serving both festivals and corporate gigs. Broadcast and streaming applications accelerate at a 7.35% CAGR to 2031, driven by 4K and 8K video mandates that necessitate object-based audio to match ultra-high-definition visuals.

Studio renovations emphasize Dolby Atmos rooms that command premium booking rates from label and independent clients, spurring sales of multichannel monitors and bass management processors. Installed sound in public-address grows steadily due to smart-city upgrades; Princeton University Chapel illustrates how historic structures integrate digitally steerable arrays connected over Dante for discreet yet intelligible coverage. Remote monitoring dashboards that predict component failure reduce downtime and spread subscription revenues across the professional audio market.

Geography Analysis

North America accounted for 33.12% of the professional audio market in 2025, backed by the world’s densest concentration of arenas, megachurches, and broadcast facilities requiring rolling technology refreshes. FCC spectrum reallocation compels wireless replacements, while accessibility laws push venues to adopt assistive-listening transmitters. Corporate real-estate teams prioritize conference-room modernization that unifies in-room and remote voices via AES67 networks. Regional resilience is reinforced by local manufacturing clusters in California and Illinois that shorten lead times during global supply disruptions.

Asia-Pacific records the fastest pace, advancing at a 7.22% CAGR through 2031 as national stadium programs in China and India embed Dante-native public-address systems from blueprint stages. China’s “ear economy” shapes procurement by requiring consumer-facing venues to adopt premium audio as a competitive differentiator. Indian integrators benefit from government incentives that localize assembly, lowering tariffs on imported components. The region’s creative-class boom fuels demand for affordable studio interfaces, expanding the professional audio market base among gig-economy musicians and podcasters. Currency fluctuations remain a planning risk, yet manufacturers hedge by denominating contracts in USD where possible.

Europe demonstrates stable demand across cultural institutions and corporate campuses. Renovation of heritage theaters prioritizes recyclable loudspeaker cabinets and low-power amplifiers to align with EU sustainability targets. Brexit spurs dual-certification costs but also motivates continental distributors to hold buffer stock, maintaining supply continuity. German trade fairs like Prolight + Sound drive product visibility, while the United Kingdom broadcast sector accelerates adoption of ST 2110-compatible consoles. The professional audio market in Europe thus evolves through regulatory compliance and green design, rather than large-scale capacity increases.

Competitive Landscape

The professional audio market shows moderate fragmentation with mounting consolidation. Acuity Brands’ USD 1.215 billion take-over of QSC integrates audio control into building management portfolios, illustrating how buyers value converged platforms. Legacy leaders such as Shure, Sennheiser, and Harman leverage deep patent libraries to protect RF and DSP technologies, while emerging entrants introduce cloud-native management that decouples hardware cycles from software upgrades.

Interoperability remains a technical battleground. Vendors race to certify AES67 endpoints and publish REST APIs that facilitate third-party control, satisfying integrators who demand vendor neutrality. AI enhancement now differentiates microphones by offering automatic gain optimization and context-aware noise suppression. Apple’s patent on ambience-compressed encoding underscores broader tech-sector interest in immersive sound.

Supply chain resilience is turning into a competitive metric. Companies diversify semiconductor sourcing and establish regional assembly plants to mitigate geopolitical risk. Those able to guarantee sub-12-week deliveries win contracts even at modest price premiums. As software subscriptions widen, recurring revenue smooths cash flow volatility, rewarding firms that pivot from one-time sales to lifetime engagement models within the professional audio market.

Professional Audio Industry Leaders

Harman International Industries Inc.

Yamaha Corporation

Shure Incorporated

Sennheiser electronic GmbH & Co. KG

Bose Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Acuity Brands has successfully acquired QSC, LLC for USD 1.215 billion. This move integrates QSC's audio platform, Q-SYS, into Acuity's Intelligent Spaces Group, bolstering the convergence of building management and audio-visual systems.

- January 2025: At NAMM 2025, Shure unveiled its Nexadyne™ Instrument Microphones, equipped with Revonic™ Dual-Engine Transducer Technology. The three models, Nexadyne 2, 5, and 6, are priced from USD 219 and are designed for modern touring applications, emphasizing durability and sound clarity.

- May 2025: The Freedman Group, bolstering its portfolio of professional audio brands, has acquired Lectrosonics, a global frontrunner in UHF wireless audio technology, solidifying its foothold in the wireless microphone arena.

- March 2025: At CinemaCon 2025, Meyer Sound unveiled the ASTRYA Screen Channel Loudspeaker, highlighting its cutting-edge innovations tailored for the future of cinema audio technology.

Global Professional Audio Market Report Scope

| Loudspeakers |

| Power Amplifiers |

| Mixing Consoles |

| Microphones |

| Headphones |

| Accessories and Others |

| Wired |

| Wireless |

| Corporate |

| Venues and Events |

| Retail and Hospitality |

| Media and Entertainment |

| Education and Houses-of-Worship |

| Live Sound Reinforcement |

| Recording Studios |

| Broadcast and Streaming |

| Installed Sound / Public-Address |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Singapore | ||

| Australia | ||

| Malaysia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Product | Loudspeakers | ||

| Power Amplifiers | |||

| Mixing Consoles | |||

| Microphones | |||

| Headphones | |||

| Accessories and Others | |||

| By Connectivity | Wired | ||

| Wireless | |||

| By End-User | Corporate | ||

| Venues and Events | |||

| Retail and Hospitality | |||

| Media and Entertainment | |||

| Education and Houses-of-Worship | |||

| By Application | Live Sound Reinforcement | ||

| Recording Studios | |||

| Broadcast and Streaming | |||

| Installed Sound / Public-Address | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Chile | |||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Singapore | |||

| Australia | |||

| Malaysia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the professional audio market in 2026?

It stands at USD 13.26 billion and is forecast to grow to USD 17.82 billion by 2031, reflecting a 6.1% CAGR.

Which product category leads revenue?

Loudspeakers generated 38.02% of 2025 revenue, driven by venue refurbishments and touring upgrades.

What segment is expanding fastest?

Wireless microphones show an 7.45% CAGR through 2031 due to spectrum reallocations and creator-economy demand.

How is hybrid work influencing demand?

Enterprises retrofit meeting rooms with networked beam-forming arrays, boosting sales of high-fidelity conferencing gear.

Page last updated on: