Audio Codec Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 8.10 Billion |

| Market Size (2031) | USD 10.43 Billion |

| Growth Rate (2026 - 2031) | 5.18% CAGR |

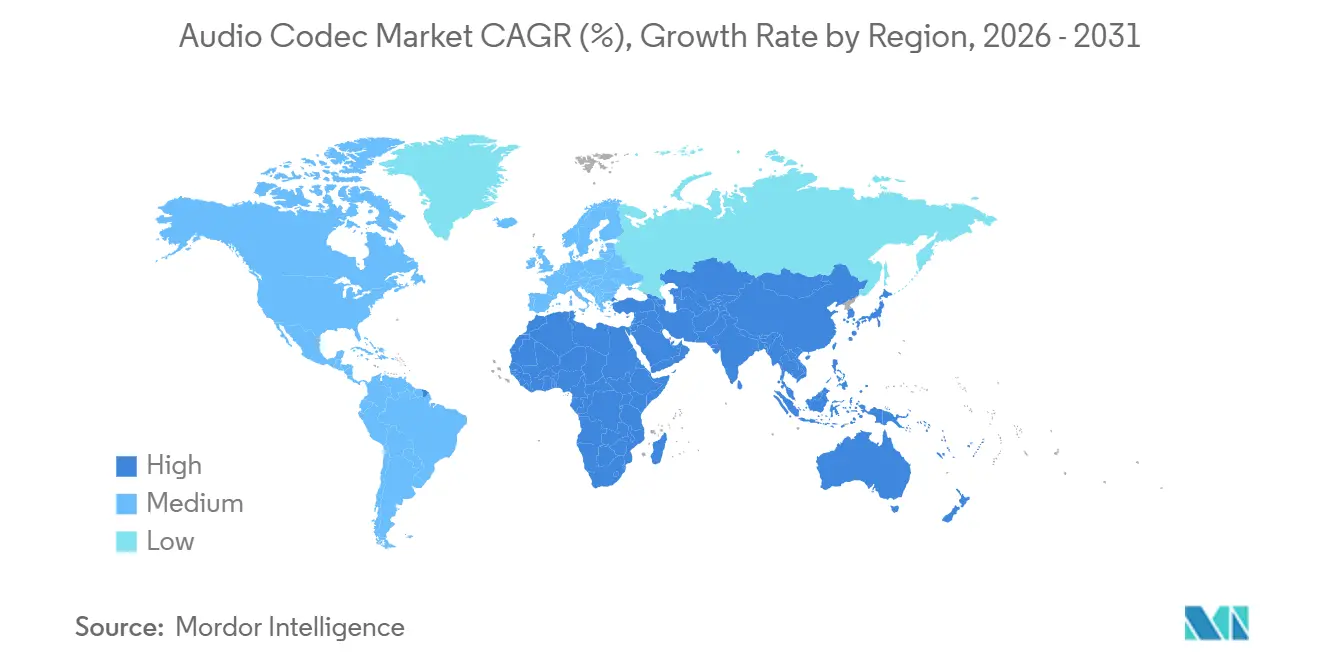

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Audio Codec Market Analysis by Mordor Intelligence

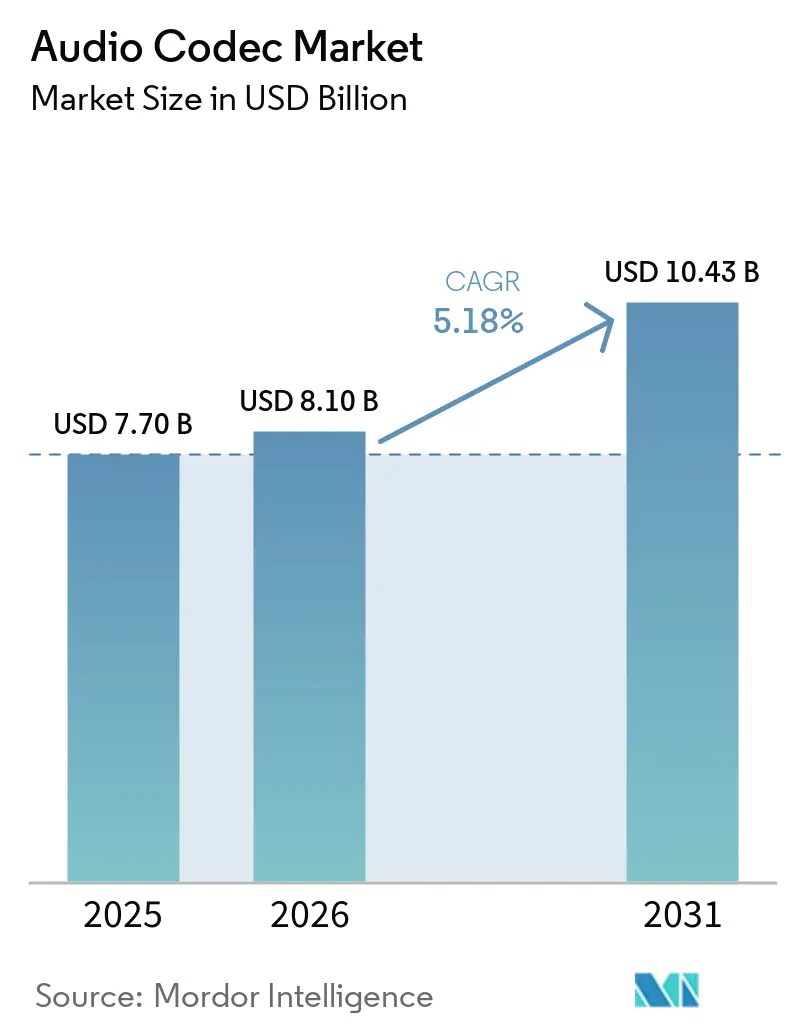

The audio codec market size is expected to grow from USD 7.70 billion in 2025 to USD 8.10 billion in 2026 and is forecast to reach USD 10.43 billion by 2031 at 5.18% CAGR over 2026-2031. In 2025, hardware-based DSP IP cores still controlled 60.19% of revenue, yet software frameworks are scaling faster as original-equipment manufacturers (OEMs) push over-the-air updates that add new formats without changing silicon. Bluetooth LE Audio’s LC3 specification, ratified in 2024, introduced a royalty-free option that challenges entrenched Advanced Audio Coding (AAC) implementations while amplifying interest in devices able to switch among codec families on demand. Lossless compression is gaining because premium streaming subscriptions emphasize bit depth over song catalog, and consumer appetite for USD 200-plus true-wireless-stereo (TWS) earbuds supports higher licensing fees in exchange for longer battery life and lower latency. Geographically, Asia-Pacific remains the manufacturing hub and lead adopter, but greenfield 5G broadcast rollouts in the Middle East and Africa are widening future addressable demand for next-generation codecs.

Key Report Takeaways

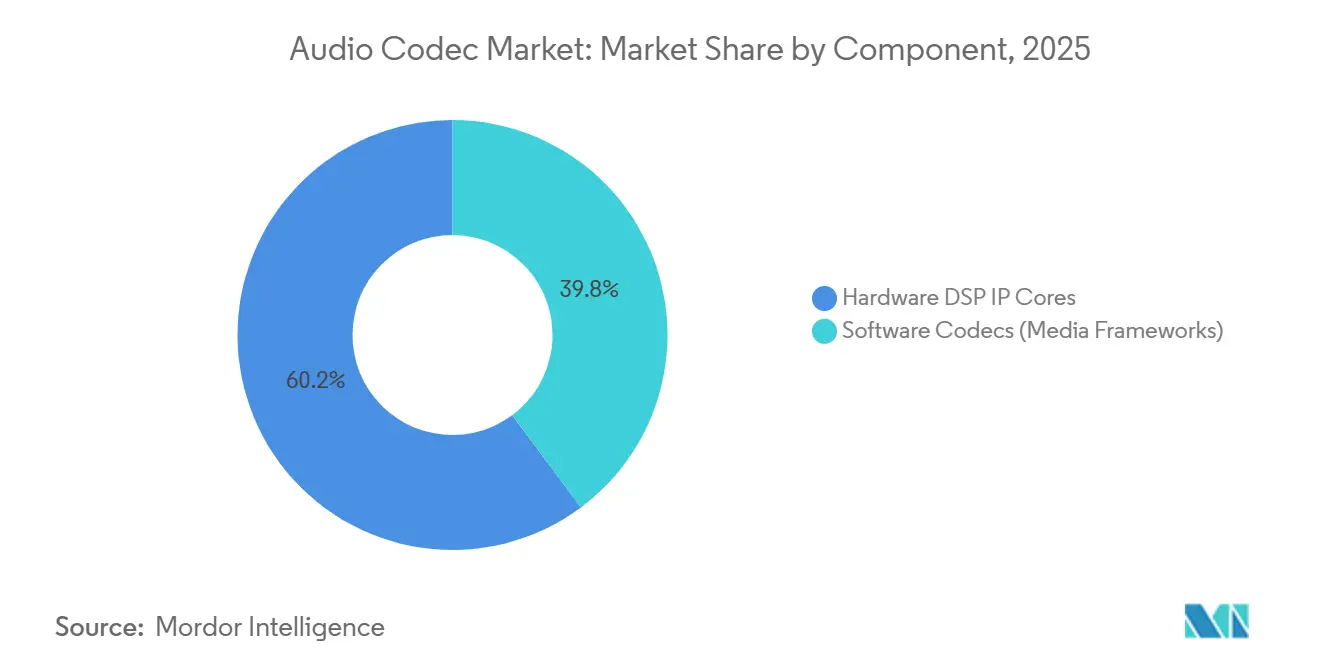

- By component, hardware DSP IP cores held 60.19% of the audio codec market share in 2025, whereas software codec frameworks are projected to advance at a 6.01% CAGR through 2031.

- By codec type, AAC commanded 45.27% revenue share of the audio codec market in 2025, while Dolby codecs are set to deliver the fastest 5.95% CAGR to 2031.

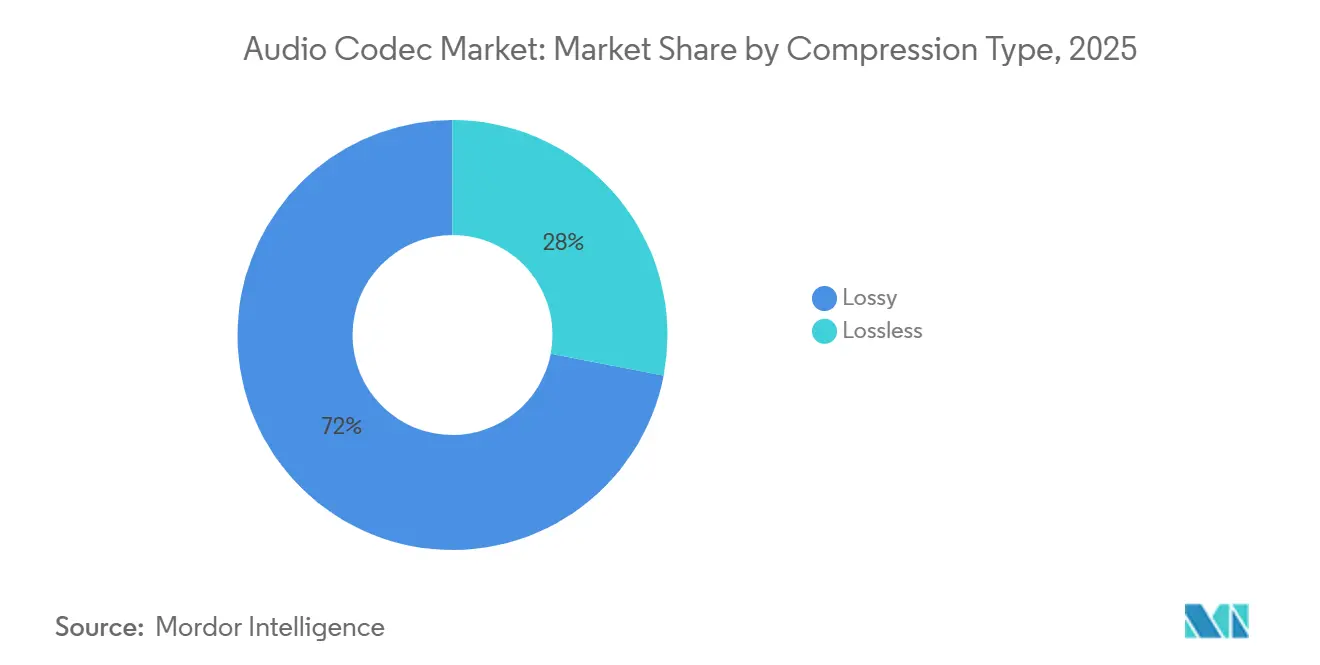

- By compression type, lossy formats accounted for 71.99% of the audio codec market share in 2025, whereas lossless alternatives are poised for a 6.11% CAGR out to 2031.

- By end-use industry, consumer electronics led with 43.38% of the audio codec market share in 2025, and the TWS and earbud segment is tracking a 5.78% CAGR through 2031.

- By geography, Asia-Pacific captured 34.83% of the audio codec market share in 2025, yet the Middle East and Africa region is on course for a 5.85% CAGR across the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Audio Codec Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Streaming Audio and Video Adoption | 1.2% | Global, peak North America and Europe | Medium term (2–4 years) |

| Smartphone and Wireless-Earbud Volume Growth | 1.0% | Asia-Pacific core, spillover Middle East and Africa | Short term (≤ 2 years) |

| Standardization of Codecs in 5G Broadcast | 0.9% | Asia-Pacific, Middle East, select European markets | Long term (≥ 4 years) |

| Growing Adoption of Bluetooth LE Audio (LC3) in Hearables | 0.8% | Global, led by North America and Asia-Pacific | Medium term (2–4 years) |

| Automotive In-Cabin Personalized Sound Zones | 0.6% | North America and Europe premium, China EV tier | Medium term (2–4 years) |

| On-Device AI-Enabled Neural Codecs for IoT Sensors | 0.4% | Global, niche satellite and industrial IoT | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Streaming Audio and Video Adoption

Streaming platforms are splitting into mainstream tiers capped at 256 kilobits-per-second AAC and premium tiers offering lossless or spatial catalogs, which transfers royalty flows from cloud decoding to device-side IP embedded in phones, smart speakers, and infotainment head units.[1]Apple Inc., “Apple Music Lossless Audio Announcement,” apple.com The 3rd Generation Partnership Project (3GPP) finalized the Immersive Voice and Audio Services (IVAS) codec in Release 18, allowing telecom operators to bundle spatial audio in 5G data plans. Broadcast engineers are already inserting object-based MPEG-H tracks so viewers can select personalized commentary, a feature that legacy stereo codecs cannot replicate without server re-encoding.[2]IEEE Broadcast Technology Society, “5G Broadcast and ATSC 3.0 Deployment Update,” ieee.org Compliance with ITU-R loudness guidelines maintains uniform playback levels across adaptive-bit-rate streams, reducing churn caused by listener fatigue.

Smartphone and Wireless-Earbud Volume Growth

Global smartphone shipments steadied at roughly 1.2 billion units in 2025, but mid-tier devices now integrate multi-codec stacks such as Qualcomm Snapdragon Sound, which packages aptX Lossless, aptX Adaptive, and LC3 in one library.[3]Qualcomm Technologies, “Snapdragon Sound Technology,” qualcomm.com Shipments of TWS earbuds crossed 350 million the same year, and average selling prices rose as brands added active noise cancellation that demands sub-20 millisecond latency. Samsung’s Galaxy Buds3 Pro dynamically selects among SBC, AAC, and Samsung Scalable Codec to minimize dropouts.[4]Samsung Electronics, “Galaxy Buds3 Series Product Specifications,” samsung.com Bluetooth Special Interest Group (SIG) data show LC3-certified devices topping 50 million cumulative units, concentrated in hearing aids, where 50% lower bit rate extends battery life.

Standardization of Codecs in 5G Broadcast

ATSC 3.0 mandates AC-4 or MPEG-H Audio for U.S. over-the-air TV, and early deployments in Phoenix have shown that viewers can mix home-team and away-team commentary without a return channel. South Korea moved all major terrestrial broadcasts to MPEG-H in 2024, and Release 19 of 3GPP will extend IVAS to augmented-reality audio experiences in 2026. Point-to-multipoint architecture lowers per-user streaming cost by 90%, making high-bit-rate immersive audio viable for stadium events. Regulatory alignment remains patchy: European broadcasters still favor HE-AAC for backward compatibility, whereas Middle Eastern operators plan to jump straight to MPEG-H to avoid legacy encumbrances.

Growing Adoption of Bluetooth LE Audio (LC3) in Hearables

LC3 delivers perceptual parity to SBC at half the bit rate, directly translating into longer battery runtime for coin-cell earbuds. Qualcomm’s QCC30xx SoCs ship with LC3 plus aptX Adaptive, so brands can upsell premium codecs without changing hardware. Fraunhofer IIS tests show LC3 maintains speech intelligibility even with 10% packet loss, outperforming AAC in congested 2.4 gigahertz environments. Auracast broadcast audio based on LC3 entered airports and conference venues in 2025, letting travelers tune in to gate announcements directly through standard earbuds.

Restraints Impact Analysis of Audio Codec Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Licensing Cost and Patent-Pool Complexity | -0.7% | Global, acute in price-sensitive markets | Short term (≤ 2 years) |

| Rise of Royalty-Free Codecs (Opus, FLAC) | -0.5% | North America and Europe enterprise, Asia-Pacific consumer | Medium term (2–4 years) |

| Edge-AI Compression Reducing External Codec Demand | -0.3% | Global, premium tiers | Long term (≥ 4 years) |

| Sustainability-Driven Bit-Rate Caps in Consumer Devices | -0.2% | Europe mandate, voluntary North America | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High Licensing Cost and Patent-Pool Complexity

Via Licensing charges USD 0.10-0.98 per unit for AAC, while MPEG-H and IVAS layers can push total royalties beyond USD 1.50 on premium car head units. Minimum annual guarantees squeeze low-volume OEMs and divert them toward royalty-free SBC or LC3. Chinese smartphone brands have lobbied for compulsory FRAND terms as IVAS adds a third licensing layer. Cross-complaints between Fraunhofer and Dolby in German and U.S. courts heighten uncertainty, and importers in Africa and South America face shipment delays when they must negotiate directly with patent pools.

Rise of Royalty-Free Codecs (Opus, FLAC)

Opus, published in RFC 6716, provides <5 millisecond latency and zero per-unit fees, making it the default for Google Meet, Microsoft Teams, and Meta WhatsApp voice calls. FLAC expanded across Tidal and Qobuz catalogs in 2025, bypassing USD 0.10-per-stream royalties for ALAC and MQA. Vectis IP’s 2025 attempt to monetize an Opus pool at USD 0.15 per device stalled after open-source backlash. Automotive Tier 1 suppliers such as Harman are trialing Opus for in-cabin hands-free to avoid AAC fees on multi-zone systems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Audio Codec Market Segment Analysis

By Component:

Software Gains Under OTA UpdatesSoftware frameworks added 6.01% CAGR momentum through 2031 as OEMs use firmware pushes to insert new formats post-launch, an agility that hardware IP cannot match. ARM’s Cortex-M85 with Helium vectors now decodes LC3 and Opus on sub-USD 5 microcontrollers, unlocking the audio codec market for IoT wearables. The automotive domain still favors hardware because ISO 26262 safety assessments demand deterministic paths, and Synopsys supplies pre-verified DSP cores with embedded AAC and aptX that ship in automotive system-on-chips.

Hardware DSP IP cores, nonetheless, held 60.19% audio codec market share in 2025. Automotive infotainment and smart-TV manufacturers rely on fixed accelerators to minimize per-channel power. Yet software-defined architectures such as Tesla’s are decoupling codec refresh cycles from silicon roadmaps, allowing a fast pivot to LC3 or IVAS without waiting for a new chip tape-out.

By Codec Type:

AAC Dominance Confronts Dolby’s Premium PushAAC retained 45.27% of 2025 revenue because iOS and Android include it as a mandatory decode. Qualcomm aptX and Sony LDAC play in premium Bluetooth headphones, whereas SBC stays in budget accessories for its zero-royalty position. Dolby’s portfolio, spanning AC-3, AC-4, and Dolby Atmos, is growing 5.95% to 2031 as streaming and automotive segments license object-based rendering.

Next-gen value is shifting from compression to authoring and rendering. Dolby Atmos Music, now exceeding 10,000 tracks, encodes up to 128 audio objects so playback devices can tailor output to any speaker array. Chinese EV makers, however, choose MPEG-H to avoid per-vehicle fees topping USD 50, signaling a pricing challenge for Dolby in cost-sensitive geographies.

By Compression Type:

Lossless Ascends As Quality DifferentiatorLossy streams generated 71.99% of 2025 revenue, but lossless formats are tracking a 6.11% CAGR. Apple Music’s move to deliver ALAC at no extra cost forced rivals to accelerate FLAC adoption, and flagship smartphones now ship with 256 gigabytes of base memory, easing local caching of large files APPLE.COM.

Electric vehicles accentuate cabin quietness, revealing artifacts in lossy audio and nudging premium automakers toward lossless playback. Sustainability rules may require future apps to disclose carbon per song, which encourages hybrid codecs such as aptX Lossless that switch between modes depending on available bandwidth.

By End-Use Industry:

Consumer Electronics Leads While TWS AcceleratesConsumer electronics accounted for 43.38% of revenue in 2025, with smartphones serving as both licensors and decoders. TWS earbuds have a smaller base but a faster 5.78% CAGR, thanks to users' willingness to pay USD 150-USD 300 for latency-sensitive audio. Smart speakers integrate multiple codecs in a single firmware build, balancing AAC for Apple streams and Opus for YouTube content.

Media and entertainment services are splitting into ad-supported tiers that minimize royalties and premium tiers touting spatial or lossless audio. Enterprise unified-communications platforms standardized on Opus to remove per-seat fees, shaving an estimated USD 200 million off proprietary vendor revenue.

Geography Analysis

APAC Audio Codec Market

Asia-Pacific accounted for 34.83% of 2025 revenue, with China dominating smartphone and TWS production. Regional politics spur Chinese OEMs to adopt homegrown codecs such as Huawei HWA to cut reliance on U.S. IP. The Bluetooth SIG notes LC3 penetration lags in low-cost accessories but leaps ahead in premium LDAC or aptX Lossless devices.

MEA Audio Codec Market

The Middle East and Africa are forecast to grow at a 5.85% CAGR, driven by operators deploying 5G broadcast and IVAS without legacy constraints. UAE carriers ran MPEG-H trials in Dubai, streaming multi-language sports commentary, and South Africa’s digital TV transition mandates AC-4 and MPEG-H decoders, creating a one-off licensing windfall for IP owners.

The Americas and Europe Audio Codec Market

North America and Europe see premiumization of codecs rather than unit growth. European broadcasters’ dual-codec period slows HE-AAC sunset, and North American EV makers integrate Dolby Atmos as a differentiator. South America remains price sensitive; gray-market imports often ship without proper licenses, reducing capture rates for pools.

Competitive Landscape

Dolby Laboratories, Qualcomm Technologies, and Fraunhofer-Gesellschaft collectively supply IP that underpins an estimated 55% of global shipments, resulting in moderate concentration in the audio codec market. Dolby is rebalancing from mobile to automotive and streaming after smartphone royalty revenue fell 8% year over year, while automotive and OTT deals grew 22%, buoyed by partnerships with Lucid and Netflix. Qualcomm filed 47 codec-related patents in 2025, signaling an attempt to monetize LC3 through ancillary IP rather than core compression.

Silicon IP vendors such as ARM, Synopsys, and Cadence are embedding codec engines upstream, capturing value before assembly. Synopsys’ ARC HS4x DSP core ships with hardware IVAS and MPEG-H decoders and already counts eight auto-chip licensees. Smaller players, including Cirrus Logic and Analog Devices, integrate decoders inside amplifiers or PMICs to shave bill-of-materials costs in mid-tier smartphones.

Royalty-free momentum intensifies. Meta shifted 2 billion-user WhatsApp calls to Opus in 2025, cutting USD 50 million annual fees. Alibaba DAMO Academy and Xiph.Org continue internal codec R&D to avoid third-party licenses, and automotive Tier 1 suppliers develop bespoke object renderers that bypass Dolby fees. Patent-pool disputes in German and U.S. courts introduce lingering uncertainty that deters smaller OEMs from adopting premium codecs.

Audio Codec Industry Leaders

Dolby Laboratories Inc.

Qualcomm Technologies Inc.

Fraunhofer-Gesellschaft

Technicolor SA

Apple Inc.

- *Disclaimer: Major Players sorted in no particular order

Audio Codec Market Companies Covered in this Report

- Dolby Laboratories Inc.

- Qualcomm Technologies Inc.

- Fraunhofer-Gesellschaft

- Sony Corporation

- Microsoft Corporation

- DTS LLC (Subsidiary of Xperi Inc.)

- Audio Coding Technologies LLC

- RealNetworks Inc.

- Alibaba DAMO Academy

- Meta Platforms Inc.

- Samsung Electronics Co., Ltd.

- Bose Corporation

- Harman International Industries Inc.

- Synopsys Inc.

- Cadence Design Systems Inc.

- ARM Ltd.

- Imagination Technologies Ltd.

- Analog Devices Inc.

- Cirrus Logic Inc.

- Texas Instruments Inc.

Recent Industry Developments in Audio Codec Market

- February 2026: Cirrus Logic announced the CS35L45 smart amplifier with built-in AAC and SBC decode for mid-tier smartphones.

- January 2026: Qualcomm introduced Snapdragon Sound S7 and S5 Gen 3 platforms integrating LC3 and aptX Lossless with sub-20 millisecond latency for gaming headsets.

- November 2025: Dolby and Lucid Motors partnered to embed Dolby Atmos with personalized zones in the 2026 Lucid Gravity SUV.

- October 2024: Texas Instruments released the TAS2563 amplifier supporting I²S and TDM interfaces for firmware-updateable codec paths.

Global Audio Codec Market Report Scope

The Audio Codec Market Report is Segmented by Component (Hardware DSP IP Cores, Software Codecs), Codec Type (AAC, aptX Variants, SBC, Dolby Codecs, Other Codec Types), Compression Type (Lossy, Lossless), End-Use Industry (Consumer Electronics, Media and Entertainment, Telecom and VoIP, Enterprise Unified Communications, Other End-Use Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Segmentation Overview

| Hardware DSP IP Cores |

| Software Codecs (Media Frameworks) |

| AAC (Advanced Audio Coding) |

| aptX / aptX HD / aptX Lossless |

| SBC (Sub-Band Coding) |

| Dolby Codecs |

| Other Codec Types |

| Lossy |

| Lossless |

| Consumer Electronics | Smartphones |

| True Wireless Stereo / Earbuds | |

| Smart Speakers | |

| Televisions and Set-Top Boxes | |

| Automotive Infotainment | |

| Media and Entertainment | Music and Podcast Streaming |

| Broadcast and OTT Video | |

| Telecom and VoIP | |

| Enterprise Unified Communications | |

| Other End-Use Industries |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East & Africa |

| By Component | Hardware DSP IP Cores | |

| Software Codecs (Media Frameworks) | ||

| By Codec Type | AAC (Advanced Audio Coding) | |

| aptX / aptX HD / aptX Lossless | ||

| SBC (Sub-Band Coding) | ||

| Dolby Codecs | ||

| Other Codec Types | ||

| By Compression Type | Lossy | |

| Lossless | ||

| By End-Use Industry | Consumer Electronics | Smartphones |

| True Wireless Stereo / Earbuds | ||

| Smart Speakers | ||

| Televisions and Set-Top Boxes | ||

| Automotive Infotainment | ||

| Media and Entertainment | Music and Podcast Streaming | |

| Broadcast and OTT Video | ||

| Telecom and VoIP | ||

| Enterprise Unified Communications | ||

| Other End-Use Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East & Africa | ||

Key Questions Answered in the Report

What is the projected value of the audio codec market by 2031?

The audio codec market is forecast to reach USD 10.43 billion by 2031.

Which component segment is expanding fastest?

Software codec frameworks are growing at a 6.01% CAGR as OEMs rely on over-the-air updates.

How large is AAC’s footprint among codec types?

AAC commanded 45.27% of 2025 sales, the largest share among all codec formats.

Why are lossless codecs gaining traction?

Streaming services use lossless catalogs to differentiate premium tiers, and quieter electric-vehicle cabins expose artifacts in lossy audio.

Which region is expected to grow quickest?

The Middle East and Africa region is forecast for a 5.85% CAGR through 2031 due to greenfield 5G broadcast deployments.

How does LC3 benefit battery-powered earbuds?

LC3 achieves comparable quality to SBC at half the bit rate, extending earbud battery life while enabling new broadcast-audio use cases.

Page last updated on: