Automatic Content Recognition Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.45 Billion |

| Market Size (2031) | USD 15.31 Billion |

| Growth Rate (2026 - 2031) | 22.95% CAGR |

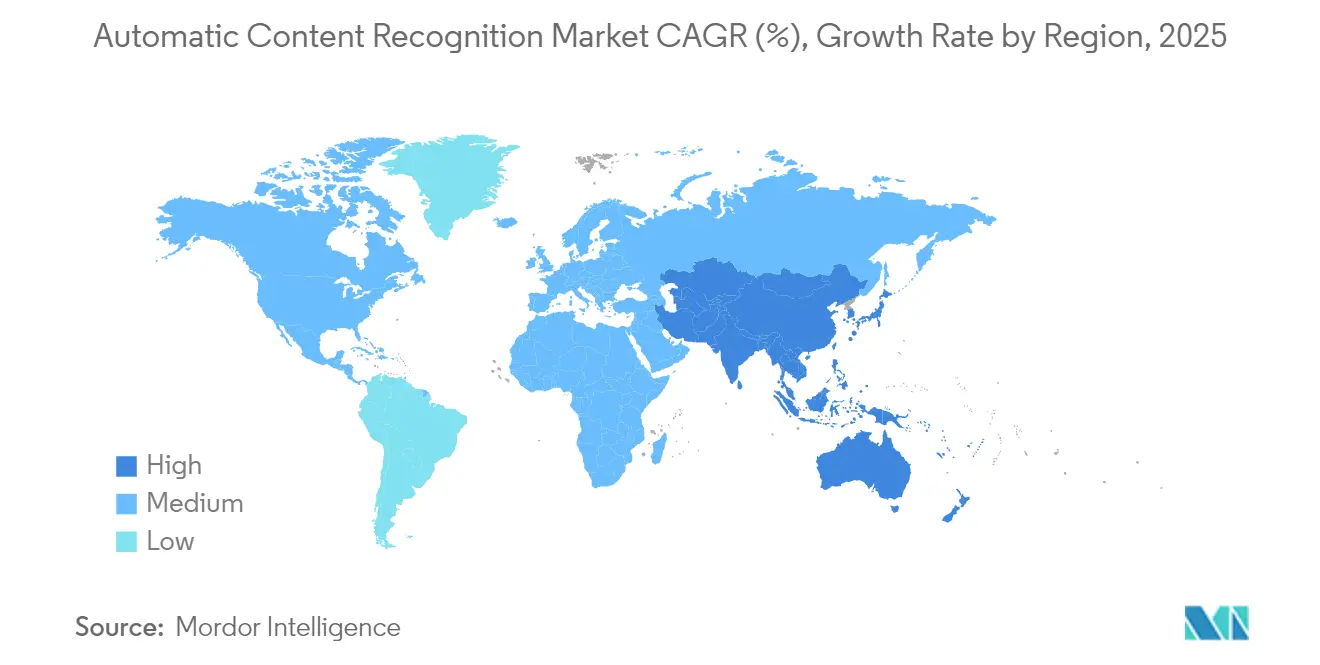

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automatic Content Recognition Market Analysis by Mordor Intelligence

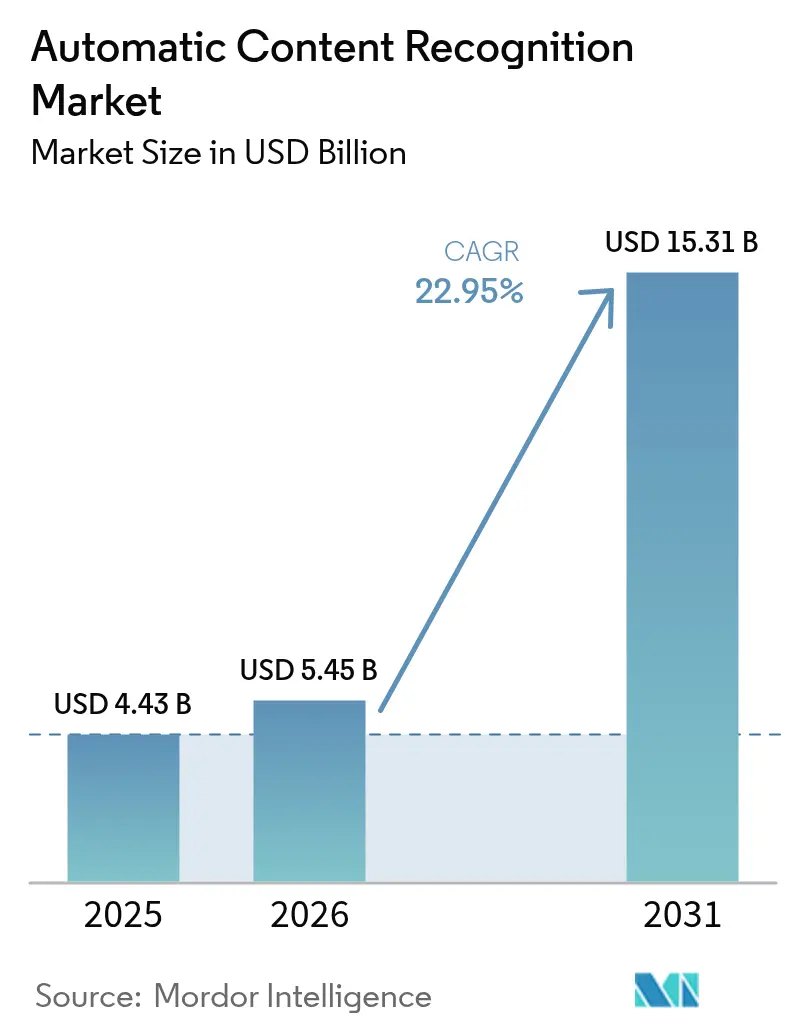

Automatic Content Recognition market size in 2026 is estimated at USD 5.45 billion, growing from 2025 value of USD 4.43 billion with 2031 projections showing USD 15.31 billion, growing at 22.95% CAGR over 2026-2031.

The 2025 baseline reflects broad-based adoption of smart TVs, a decisive budget shift toward addressable advertising, and steady improvements in edge AI that allow fingerprinting tasks to run locally with minimal energy draw. Milestone deployments such as Apple’s Shazam logging 100 billion cumulative song recognitions in 2024 showcase the scale now achieved in everyday consumer settings. Device makers routinely embed ACR silicon at the board level, enabling continuous signature extraction from linear broadcasts, streaming apps, and HDMI inputs without user intervention. This hardware pivot enlarges the Automatic Content Recognition market addressable data pool while lowering latency, a combination that keeps advertisers, broadcasters, and analytics providers firmly invested in the technology.

Key data points confirm this momentum. Software still accounts for 64% revenue but managed cloud services are expanding at a 24.48% pace as brands outsource compliance and model tuning. Audio and video fingerprinting remains the leading technology with 46% share, yet speech-driven use cases in cars and healthcare are widening fastest at 24.11% CAGR. Security and copyright protection dominate solution spending with 29% share, although real-time analytics for FAST channels is the quickest riser at 23.89% CAGR. End-user mix is led by media and entertainment at 38%, while automotive infotainment is closing the gap at 23.78% CAGR thanks to voice commerce pilots. Regionally, North America commands 41% value share, whereas Asia Pacific is compounding at 24.63% through 2030—together reinforcing the Automatic Content Recognition market’s vitality across both mature and emerging geographies.

Key Report Takeaways

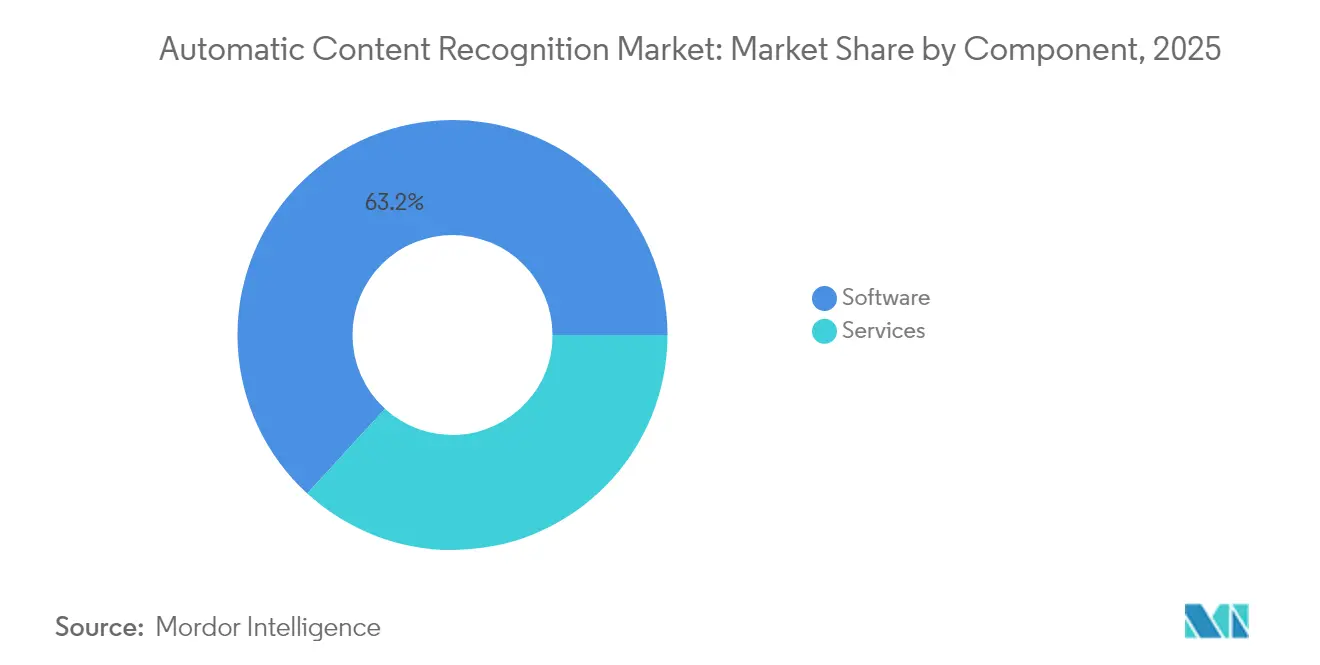

- By component, software platforms captured 63.20% of the Automatic Content Recognition market share in 2025; services are forecast to expand at a 23.95% CAGR to 2031.

- By technology, audio and video fingerprinting led with 45.30% revenue share in 2025, while speech and voice recognition is projected to accelerate at a 23.62% CAGR through 2031.

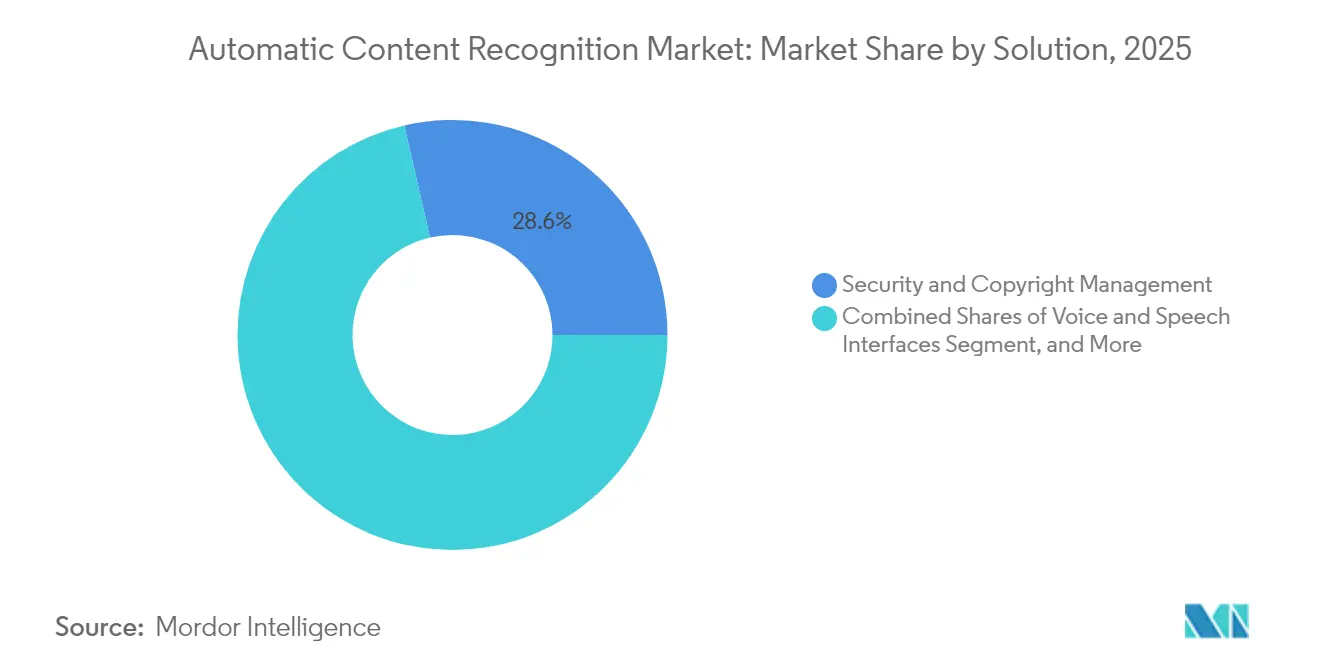

- By solution, security and copyright management accounted for 28.60% of the Automatic Content Recognition market size in 2025 and real-time content analytics is advancing at a 23.35% CAGR to 2031.

- By end-user industry, media and entertainment held 37.20% share of the Automatic Content Recognition market size in 2025; automotive applications are pacing the fastest at a 23.21% CAGR over the same horizon.

- By region, North America commanded 40.60% of the Automatic Content Recognition market share in 2025, whereas Asia Pacific is projected to post the highest regional CAGR of 24.05% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automatic Content Recognition Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of smart TVs with embedded ACR chips | +6.2% | Global; highest in North America and Asia Pacific | Medium term (2–4 years) |

| Expansion of addressable-TV advertising budgets | +5.8% | North America and Europe core; quick uptake in Asia Pacific | Medium term (2–4 years) |

| Integration of ACR into automotive infotainment systems | +4.1% | Global; premium models in North America and Europe lead | Long term (≥ 4 years) |

| Growth of FAST channels | +3.9% | Global; rapid adoption in North America and Asia Pacific | Short term (≤ 2 years) |

| Edge AI optimization lowering device power draw | +2.7% | Global; mobile and automotive benefit most | Medium term (2–4 years) |

| Emerging privacy-preserving federated learning models | +1.8% | Starts in Europe and North America; scales globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Smart TVs with Embedded ACR Chips

Smart-TV brands now route ACR processing through system-on-chip blocks situated beneath the application layer, allowing continuous fingerprint capture even when privacy toggles are off. Samsung units dispatch signatures roughly every minute, while LG models do so every 15 seconds, creating an uninterrupted telemetry stream that spans live broadcasts, streaming apps, and any HDMI source. These low-latency pipelines shorten the feedback loop for ad optimization and broaden the Automatic Content Recognition market’s data inventory.

Expansion of Addressable-TV Advertising Budgets

Advertisers are redirecting spend toward addressable formats that exploit frame-level ACR insights. Budgets dedicated to addressable TV surpassed one-third of total TV outlays in 2025 and are on track for 42% by 2027. FAST distributors pair these insights with programmatic workflows to lift engagement beyond demographic targeting, while new HbbTV-TA certifications in Europe standardize technical baselines. The Automatic Content Recognition market benefits as every incremental ad insertion relies on precise, real-time content labeling.[1]Digital TV News, “HbbTV-TA Gains Certification Across European TV Brands,” digitaltvnews.net

Integration of ACR into Automotive Infotainment Systems

Vehicle platforms are embedding ACR engines to drive voice search, content recommendations, and commerce. HARMAN’s Ready Connect 5G TCU blends Qualcomm’s digital chassis and local fingerprinting, and SoundHound AI’s agentic voice commerce stack recognizes ambient media to trigger transactions. Edge inference ensures continuity during patchy coverage, underscoring how mobility-centric deployments expand the Automatic Content Recognition market horizon.[2]HARMAN, “Ready Connect 5G TCU Integrates Qualcomm Snapdragon Digital Chassis,” harman.com

Growth of FAST (Free Ad-Supported Streaming TV) Channels

Unique FAST channels reached 1,943 as of May 2024, only 1% shy of the record, firing a 28% annual jump in ad impressions. ACR allows server-side insertion matched to scene-level context, lifting monetization without subscription fees. Yet, 31% of libraries still lack adequate genre tags, spotlighting metadata gaps that providers like Gracenote aim to close.[3]Nielsen, “Gracenote Launches FAST Program for Metadata Services,” nielsen.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter opt-in consent rules under refreshed ePrivacy law | -3.4% | Europe with spillover globally | Short term (≤ 2 years) |

| Apple/Google anti-fingerprinting moves in OS updates | -2.8% | Global; mobile and connected TV ecosystems | Medium term (2–4 years) |

| Limited SKU-level analytics from legacy linear STBs | -1.9% | North America and Europe cable networks | Long term (≥ 4 years) |

| Royalty disputes over watermark IP portfolios | -1.3% | Global; most acute in content-heavy territories | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Stricter Opt-in Consent Rules Under Refreshed ePrivacy Law

European authorities began enforcing refined consent banners and “consent-or-pay” guidance in late 2024, pressuring smart-TV vendors to create granular toggles that isolate ACR data from core functions. Compliance adds engineering overhead and may shrink data volumes, dampening the Automatic Content Recognition market growth outlook within the bloc.

Apple/Google Anti-Fingerprinting Moves in OS Updates

Apple’s App Tracking Transparency and Google’s evolving Privacy Sandbox now curb device-level identifiers. ACR providers must shift toward privacy-preserving hashes and cohort methods, adding cost and potential latency. Litigations alleging covert fingerprinting illustrate the high stakes, particularly for firms lacking scale to overhaul stacks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Acceleration Outpaces Software Dominance

Software revenue formed the lion’s share of the Automatic Content Recognition market size in 2025, thanks to code tightly woven into TV operating systems and streaming SDKs. However, cloud-hosted managed offerings are scaling at 23.95% CAGR as OEMs and broadcasters outsource model tuning, compliance, and uptime management. Digimarc’s 44% jump in annual recurring revenue to USD 23.9 million underlines how subscription billing is resonating with customers who prefer turnkey compliance amid changing privacy rules.

The services surge mirrors a broader pivot in enterprise IT toward OPEX-friendly contracts that bundle maintenance, audit logs, and SLA guarantees, for many mid-tier device brands, licensing an end-to-end service beats building an in-house stack that must keep pace with region-specific consent frameworks. Accordingly, analysts expect services to nibble incremental Automatic Content Recognition market share each year through 2031 while software remains foundational yet slower growing.

By Technology: Voice Recognition Disrupts Fingerprinting Dominance

Audio and video fingerprinting still anchors 45.30% of revenue due to its maturity and proven accuracy across live TV and on-demand libraries. Yet speech-centric recognition is the Automatic Content Recognition market’s quickest riser, compounding at 23.62% on the back of in-car voice assistants, tele-health monitoring, and contact-center analytics. NTT’s ultra-low-latency voice conversion work highlights how real-time quality now meets enterprise thresholds.

Edge silicon capable of shaving 92% power relative to cloud chains makes voice analytics feasible in battery-run devices and automotive ECUs. Meanwhile, watermarking gains renewed importance for rights holders, and optical character recognition adds incremental volume in retail. Together, these trajectories diversify the Automatic Content Recognition industry toolkit without displacing staple fingerprinting algorithms.

By Solution: Real-Time Analytics Challenge Security Applications

Security and anti-piracy suites held a 28.60% beachhead in 2025, driven by urgent needs to curb illegal restreaming, especially for live sports. Japan’s state-backed manga piracy initiative exemplifies government involvement. Nonetheless, FAST operators and connected-TV ad networks are fueling demand for sub-second analytics that let spots be stitched into a stream aligned to actual on-screen moments. This real-time segment is on a 23.35% climb and is steadily closing the revenue gap, signaling that optimization use cases now rival protection motives in steering Automatic Content Recognition market outlays.

By End-User Industry: Automotive Acceleration Challenges Media Leadership

Media and entertainment produced 37.20% of revenue in 2025 as studios, broadcasters, and OTT apps mined viewer telemetry for recommendation and rights management tasks. Automotive OEMs, however, are chalking up a 23.21% expansion trajectory by bundling voice commerce, context-aware audio search, and in-cabin personalization. SoundHound AI’s leap to USD 34.5 million Q4 2024 sales, largely underpinned by car deals, underscores this shift. Healthcare pilot projects that marry ACR to patient monitoring and retail pilots that layer watermark-based inventory audit further disperse the Automatic Content Recognition market across verticals previously outside classical media boundaries.

Geography Analysis

North America generated 40.60% of Automatic Content Recognition market revenue in 2025, benefiting from smart-TV household penetration above 75% and a well-established addressable-advertising supply chain. Platforms integrate server-side insertion that leans heavily on frame-level recognition, amplifying the region’s data advantages. While federal privacy bills remain in draft form, state-level rules and greater consumer awareness could temper data flows mid-term, prompting vendors to reinforce consent flows.

Asia Pacific is the automatic growth engine, expanding at 24.05% CAGR through 2031. Mass-market smart-TV adoption, rising disposable incomes, and policy backing for AI labs act in concert. Korea’s SK Telecom and LG CNS are adding multilingual real-time translation layers that rely on the same underlying ACR voices. Japan’s AI Bill, now progressing through the Diet, is poised to set balanced R&D guardrails, giving suppliers regulatory clarity. In China, domestic chip fabrication and algorithm houses spur localized stacks even as international players navigate export hurdles. The cumulative effect keeps the Automatic Content Recognition market vibrant across APAC sub-regions.

Europe offers a mix of opportunity and constraint. HbbTV-TA certification has harmonized technical pathways for ad replacement, but the continent’s reinforced ePrivacy and GDPR regimes make opt-in rates a swing factor. Vendors experimenting with federated learning expect to reconcile accuracy with anonymity, potentially birthing best practices that later export to other territories. The Automatic Content Recognition market outlook in Europe therefore hinges on the industry’s ability to align with regulators while sustaining data-rich workflows critical for monetization.

Mordor Intelligence provides coverage of the automatic content recognition market across other key regional markets. Detailed country-level analysis extends to United States incorporating local coverage and market participation, as required.

Competitive Landscape

Industry structure is moderately fragmented because each layer—chip, algorithm, metadata, and application—hosts distinct specialists. Shazam and Gracenote anchor audio fingerprinting, whereas edge-AI newcomers are disrupting voice and contextual analytics with lightweight models. Several players pursue vertical stacks: device makers insert proprietary chips, cloud platforms integrate recognition APIs, and content owners license enriching metadata. Patent fences remain central; filings around digital watermark resiliency and neural-network-based signature hashing are rising as firms guard differentiated IP.

Recent strategic moves highlight this dynamic. SoundHound AI nearly doubled its 2024 revenue by pushing beyond pure automotive into restaurants and finance while retaining core patents around conversational AIs. Digimarc’s anti-counterfeit suite demonstrates value in logistics and luxury goods, carving white-space outside media. The Automatic Content Recognition market, therefore, rewards both depth in a niche and breadth across converging verticals, with M&A likely as companies aim to assemble end-to-end portfolios under tightening privacy and ROI lenses.

Automatic Content Recognition Industry Leaders

Apple Inc. (Shazam Entertainment Ltd.)

Audible Magic Corporation

Digimark Corporation

ACRCloud

Nuance Communications Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: SoundHound AI posted record Q1 2025 revenue of USD 29.1 million, up 151% year over year, attributing gains to its Agentic AI voice platform.

- June 2025: AMD agreed to buy Brium, targeting faster AI model performance on Radeon-class hardware, its fourth AI-focused deal in two years.

- June 2025: Meta Platforms invested USD 14.3 billion for a 49% stake in Scale AI to boost data labeling for AGI projects.

- June 2025: AMD agreed to buy Brium, targeting faster AI model performance on Radeon-class hardware, its fourth AI-focused deal in two years.

Global Automatic Content Recognition Market Report Scope

Automatic content recognition (ACR) identifies content on media players or within media files. This identification technology allows users of ACR-supported devices to effortlessly discover details about content they recently viewed or heard, eliminating the need for manual searches. ACR provides brands a unique opportunity to engage with audiences who watch TV alongside secondary screens. This technology not only syncs second-screen content with TV programs but also empowers networks to gauge real-time audience viewership for specific shows. ACR operates by creating a digital signature from the content displayed on the television screen. This signature aids in recognizing the on-screen content and syncing it with other ACR-enabled devices, like tablets and smartphones.

The automatic content recognition market is segmented by solution (real-time content analytics, security and copyright management, voice and speech recognition), end-user industry (IT & Telecommunication, consumer electronics, media & entertainment), and geography (North America, Europe, Asia-Pacific, Latin America, Middle East & Africa).

The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Software |

| Services |

| Audio and Video Fingerprinting |

| Digital Watermarking |

| Speech and Voice Recognition |

| Optical Character Recognition |

| Real-time Content Analytics |

| Security and Copyright Management |

| Voice and Speech Interfaces |

| Data Management and Metadata |

| Others |

| Media and Entertainment |

| Consumer Electronics OEMs |

| Advertising and Marketing |

| Telecom and IT |

| Automotive |

| Healthcare |

| Others (Retail, Education) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Argentina |

| Brazil | |

| Rest of South America | |

| Europe | United Kingdom |

| France | |

| Germany | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Rest of Asia Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Rest of Middle East | |

| Africa | Nigeria |

| South Africa | |

| Rest of Africa |

| By Component | Software | |

| Services | ||

| By Technology | Audio and Video Fingerprinting | |

| Digital Watermarking | ||

| Speech and Voice Recognition | ||

| Optical Character Recognition | ||

| By Solution | Real-time Content Analytics | |

| Security and Copyright Management | ||

| Voice and Speech Interfaces | ||

| Data Management and Metadata | ||

| Others | ||

| By End-User Industry | Media and Entertainment | |

| Consumer Electronics OEMs | ||

| Advertising and Marketing | ||

| Telecom and IT | ||

| Automotive | ||

| Healthcare | ||

| Others (Retail, Education) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Argentina | |

| Brazil | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Rest of Asia Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | Nigeria | |

| South Africa | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What was the Automatic Content Recognition market size in 2026?

The market reached USD 5.45 billion in 2026, reflecting strong uptake across smart-TV, advertising, and automotive domains.

How fast is the Automatic Content Recognition market expected to grow through 2031?

It is projected to advance at a 22.95% CAGR, swelling to USD 15.31 billion by the end of the forecast period.

Which technology segment is growing the quickest

Speech and voice recognition is the fastest, expanding at a 23.62% CAGR on the back of automotive and healthcare deployments.

Which region holds the largest share today?

North America leads with 40.60% revenue share owing to high smart-TV penetration and mature addressable advertising frameworks.

What is the main restraint affecting growth in Europe?

Stricter opt-in consent requirements under the updated ePrivacy law are increasing compliance costs and restricting data collection volumes.

Why are services gaining ground over software in component terms?

Enterprises prefer managed cloud services that bundle regulatory compliance, model updates, and scalability, pushing services toward a 23.95% CAGR.

Page last updated on: