Audio Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

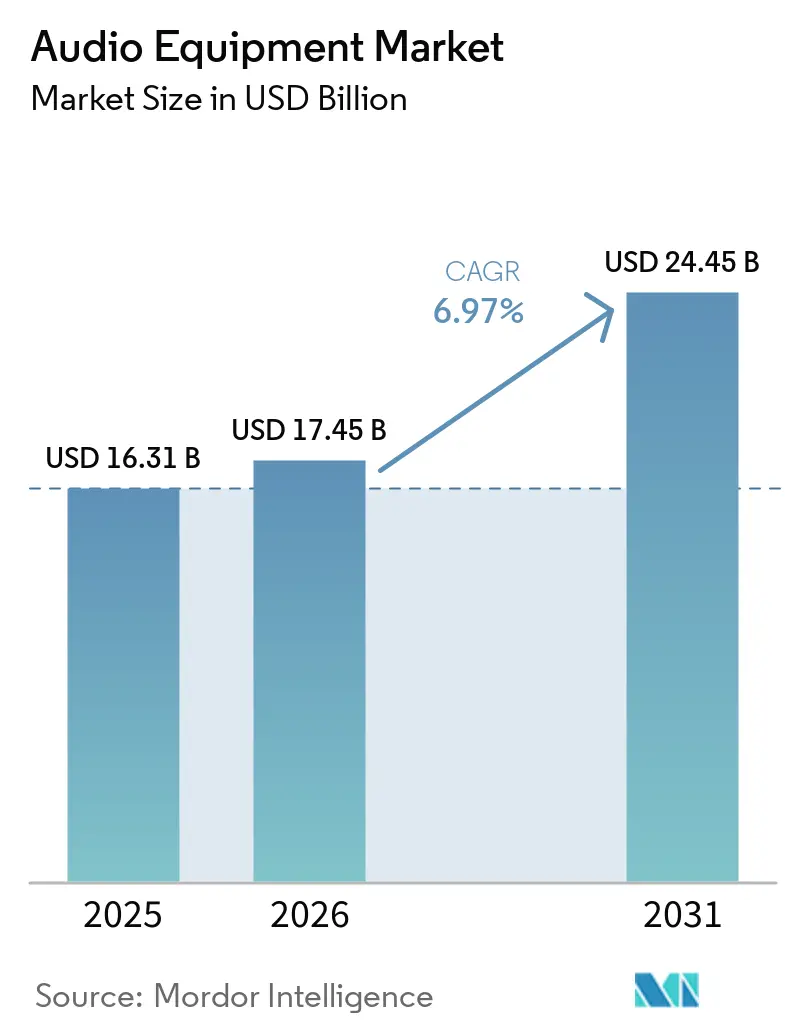

| Market Size (2026) | USD 17.45 Billion |

| Market Size (2031) | USD 24.45 Billion |

| Growth Rate (2026 - 2031) | 6.97% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Audio Equipment Market Analysis by Mordor Intelligence

Audio Equipment market size in 2026 is estimated at USD 17.45 billion, growing from 2025 value of USD 16.31 billion with 2031 projections showing USD 24.45 billion, growing at 6.97% CAGR over 2026-2031.

Growth reflects a decisive pivot from hardware-centric to software-defined listening, where 5G-enabled low-latency transmission, AI-driven adaptive processing, and sustainable materials reshape value creation. Asia-Pacific holds early-mover advantage in manufacturing scale and 5G deployment, North America leads content production and premium adoption, while Europe drives eco-design compliance. Competitive intensity rises as lighting, building-automation, and automotive electronics players acquire specialist audio firms to embed sound into wider intelligent-device ecosystems. Supply-chain visibility around rare-earth magnets and advanced semiconductors remains a critical risk vector even as ESG mandates accelerate the switch to recycled plastics, plant-fiber diaphragms, and Clean Earth Magnets.

Key Report Takeaways

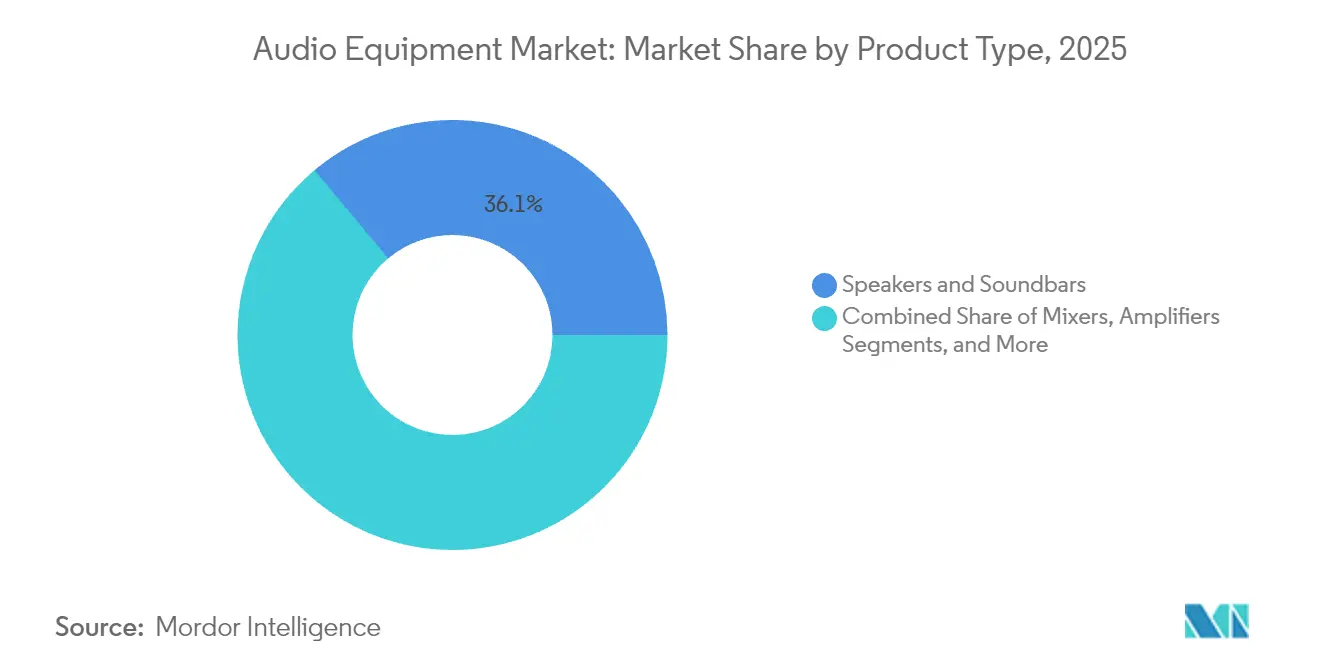

- By product type, speakers and soundbars led with a 36.10% revenue share of the audio equipment market in 2025, while headphones and earphones are forecast to expand at a 10.22% CAGR through 2031.

- By connectivity, wireless-Bluetooth accounted for 60.85% share of the audio equipment market size in 2025, whereas Wi-Fi/AirPlay connectivity is advancing at a 9.88% CAGR through 2031.

- By end user, home entertainment represented 42.30% of the audio equipment market share in 2025; automotive OEM and aftermarket is projected to grow at a 10.05% CAGR between 2026-2031.

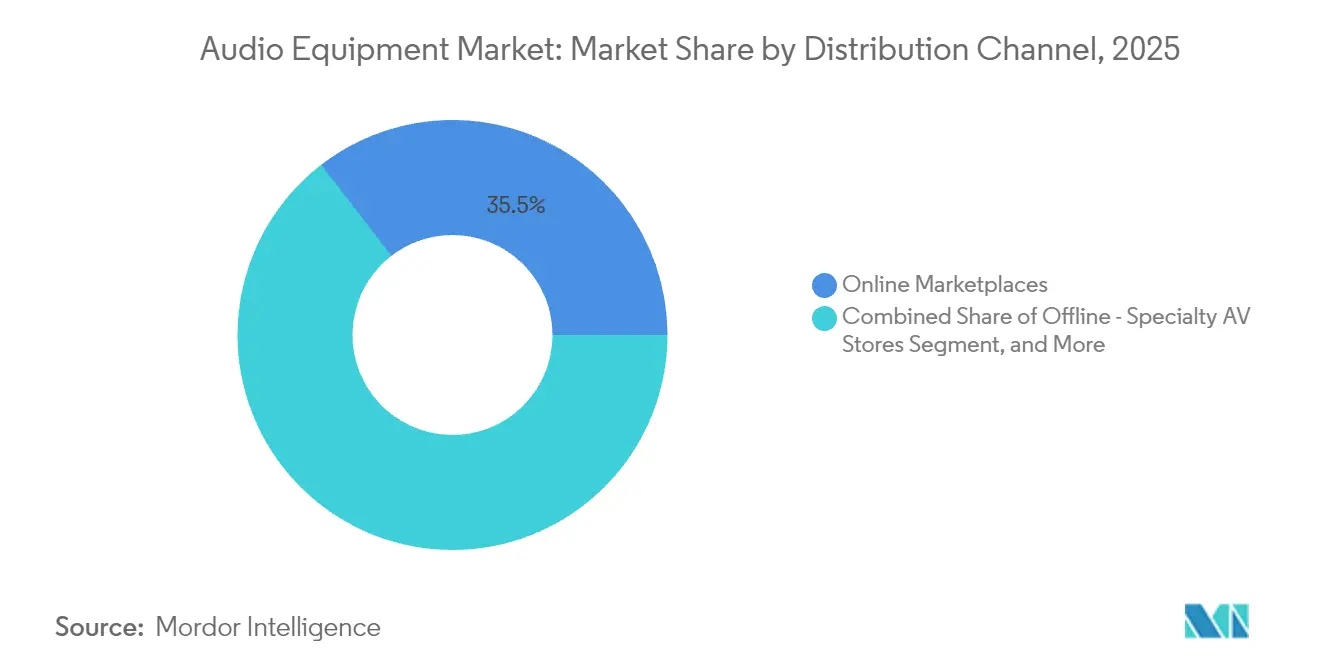

- By distribution channel, online marketplaces captured 35.45% of 2025 revenues, yet direct-to-consumer sales hold the highest projected CAGR at 9.55% through 2031.

- By price range, mid-range products priced USD 100-499 held 39.55% share of the audio equipment market size in 2025, whereas the premium audiophile tier above USD 1,000 is set to rise at a 9.48% CAGR to 2031.

- By geography, Asia-Pacific commanded 31.00% revenue share in 2025, with a forecast 8.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Audio Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising expenditure on global festivals and live concerts | +1.2% | North America, Europe | Medium term (2-4 years) |

| Growing integration of high-fidelity audio in automobiles | +1.8% | Asia-Pacific, North America | Long term (≥ 4 years) |

| Surging demand for HD and Ultra-HD sound in streaming platforms | +1.5% | North America, Europe | Short term (≤ 2 years) |

| AI-based adaptive noise-cancelling algorithms | +1.1% | North America, Asia-Pacific | Medium term (2-4 years) |

| 5G-enabled low-latency wireless audio transmission | +0.9% | Asia-Pacific, North America | Long term (≥ 4 years) |

| ESG-driven shift to eco-acoustic materials | +0.5% | Europe, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Expenditure on Global Festivals and Live Concerts

Live-music revenues climbed to USD 34.5 billion in 2023, a 29% year-over-year jump that sustained demand for next-generation line-array speakers, wireless microphones, and digital mixers[1]Bolero Music, “The Global Live Music Boom: Stadium Shows, Royalties, and Revenue,” boleromusic.com. Tier-1 tours such as Taylor Swift’s Eras and Coldplay’s Music of the Spheres push SPL, coverage, and immersive-mix standards higher, encouraging rental companies to refresh fleets sooner than past depreciation cycles. Royalty collections mirror this momentum, funneling additional capital toward venue upgrades that specify Dante-enabled networked audio and multi-track recording. Ticket-price elasticity remains high as consumers prioritize experiential spending, allowing promoters to absorb premium equipment rental costs without margin erosion. Consequently, manufacturers able to deliver lighter, power-efficient, and rider-friendly systems secure long-term framework agreements with global touring firms.

Growing Integration of High-Fidelity Audio in Automobiles

Automotive OEMs embed multi-channel Class-D amplifiers, seat-integrated transducers, and over-the-air-upgradable DSP suites during early vehicle-architecture design. Harman’s EV Plus+ solution illustrates the shift, promising 50% lower energy draw versus legacy amplifiers while preserving reference-grade playback. Quieter EV cabins amplify perceived quality gains, prompting Tesla’s 2025 Model Y to adopt a Denon-Dirac immersive platform featuring object-based rendering. Software-defined vehicles monetize audio as a post-sale service: consumers purchase sound-stage presets, nature-soundscapes, or multi-user zones much like smartphone apps. This recurring-revenue logic incentivizes chipmakers to integrate dedicated AI cores into automotive audio SoCs, widening barriers to entry for tier-2 suppliers.

Surging Demand for HD and Ultra-HD Sound in Streaming Platforms

Spotify’s 2025 Music Pro tier introduces 24-bit lossless libraries at a USD 5-6 premium, matching Apple Music and Amazon Music HD while bundling early-access concert tickets[2]The Verge, “Spotify HiFi Was Announced Four Years Ago, and It’s Almost Here—Maybe,” theverge.com. Independent service Pure Audio Streaming counters with 5.1 and 7.1.4 PCM catalogs, reinforcing consumer perception that “better files” deserve “better gear”. The result is heightened attach-rates for external DACs, high-impedance headphones, and powered speakers capable of ≥ 40 kHz frequency response. Hardware brands collaborate with services to co-market certification badges such as “Hi-Res Ready,” cementing an ecosystem loop that continuously nudges average selling prices upward.

AI-Based Adaptive Noise-Cancelling Algorithms

Machine-learning models now predict environmental signatures and personalize phase-inversion filters in real time. Meta’s contextual-awareness patents enable earbuds to auto-switch ANC levels when the wearer enters a subway or an office[3]Meta (Patent Nweon), “Contextual Awareness Subsystem for Augmented Hearing,” patent.nweon.com . NTT achieved wideband ANC in open-ear headsets—reducing 1-3 kHz noise by 13.7 dB without occluding situational awareness, a breakthrough for fitness and safety applications. AI-enabled beamforming pinpoints dominant disturbances, minimizing processor cycles while boosting battery life. Brands that pair such algorithms with bone-conduction microphones deliver clearer calls, a valued feature in hybrid-work environments where commuters demand isolation and intelligibility on the same device.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Design complexity of ultra-efficient Class-D amplifiers | –0.8% | Global high-end segment | Medium term (2-4 years) |

| RF spectrum congestion for wireless mics and in-ear monitors | –0.6% | Dense urban centers | Short term (≤ 2 years) |

| Volatility in rare-earth magnet supply chain | –0.7% | Asia-Pacific manufacturing | Long term (≥ 4 years) |

| E-waste regulations tightening life-cycle limits | –0.4% | Europe, North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Design Complexity of Ultra-Efficient Class-D Amplifiers

Gallium-nitride FETs double power density yet introduce EMI challenges that complicate filter design and certification, pushing R&D costs beyond smaller makers’ reach[4]Efficient Power Conversion (EPC), “GaN in Class-D Audio for Consumer Electronics,” epc-co.com. Silicon Intervention’s fractal topology boosts < 10 mW efficiency, but maintaining < 10 µs latency for gaming forces > 1 MHz switching that elevates thermal stress. High-end brands cannot risk audible artifacts, leading to custom ASIC programs that elongate product cycles and constrain capital for parallel innovations.

RF Spectrum Congestion for Wireless Mics and In-Ear Monitors

FCC adoption of WMAS rules improves spectral efficiency, yet 6 GHz Wi-Fi saturation still threatens dropouts at dense venues. Saudi Arabia’s 614-698 MHz reallocation to 5G shows how fast national agencies can reclaim bands, forcing performers into costlier, lower-range frequencies. Small clubs lack resources for spectrum analyzers, limiting market penetration for premium wireless systems until shared-band coordination tools become affordable.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Headphones Accelerate Personal-Audio Upswing

Speakers and soundbars accounted for a 36.10% audio equipment market share in 2025, yet headphones and earphones are expected to outpace at a 10.22% CAGR to 2031. The segment’s surge aligns with hybrid work patterns, spatial-audio proliferation, and maturing true-wireless stereo platforms. JBL’s Tour Pro 3 bundles dual drivers, head-tracking, and a transmitter-enabled charging case at USD 299.99, illustrating feature richness moving downstream. Content-creator demand lifts studio monitors and USB microphones, while integrated amps inside smart speakers pressure standalone amplifier sales. Audiophile sub-sectors-defined by > USD 1,000 pricing-find resilience in sustainable materials like flax-fiber cones that marry performance with ESG narratives.

Technological convergence sees speaker specialists invade headphone turf, as Sonos launched the Ace with TV-audio handoff capability, expanding its ecosystem stickiness. This cross-category fluidity reduces switching costs for consumers and complicates competitive moats. The premium sub-segment’s 9.48% CAGR suggests sustained pricing power, allowing margin preservation even as mid-range commoditizes.

By Connectivity: Wi-Fi Challenges Bluetooth’s Dominance

Wireless-Bluetooth solutions captured 60.85% of 2025 revenue, validating LE-Audio codecs and Auracast broadcast capability. However, Wi-Fi/AirPlay devices, fueled by Qualcomm’s XPAN 29 Mbps pipeline, are forecast at a 9.88% CAGR, promising lossless 24-bit 192 kHz streams without range anxiety. The first commercial Wi-Fi earphones, Xiaomi Buds 5 Pro, underscore imminent diversification away from Bluetooth. Wired connectivity endures in broadcast trucks and mastering suites where zero-latency is non-negotiable, while hybrid jacks emerge in gaming headsets that support both USB-C and 2.4 GHz dongles.

Bluetooth SIG’s roadmap touts 8 Mbps lossless channels yet remains two revision cycles from mass roll-out, giving Wi-Fi a timing window. Brands deploying Auracast earbuds like JBL Tour ONE M3 ease multi-listener sharing for fitness studios and airports, opening B2B revenue streams.

By End User: Automotive Segment Races Ahead

Home entertainment retained 42.30% of 2025 spending as streaming subscriptions surged; nevertheless, automotive OEM and aftermarket demand is projected to grow at a 10.05% CAGR to 2031. Seat-embedded transducers and headrest speakers from Harman’s SeatSonic transform audio into a tactile experience, monetizable via OTA-unlockable upgrades. Commercial venues-stadiums, retail, hospitality-reinvest in scalable networked solutions compatible with post-pandemic capacity norms. Education institutions adopt full-room microphone arrays such as Nureva HDL Pro for hybrid learning, cementing long-term contracts that bundle hardware with SaaS analytics.

Broadcast studios pivot toward IP-based workflows, pushing the broadcast-equipment market toward USD 7.32 billion by 2030, which cascades into demand for reference monitors and Dante-enabled consoles.

By Distribution Channel: D2C Redefines Margin Capture

Online marketplaces commanded 35.45% of 2025 revenue, but direct-to-consumer is the fastest track-growing 9.55% CAGR-as brands seek data ownership and differentiated experiences. Loop Earplugs’ climb from EUR 42 million to EUR 126.5 million within a year validates the model’s reach and community marketing leverage. Legacy brick-and-mortar responds with omnichannel services like buy-online-pick-up-in-store, bundling extended warranties and expert demos. KPMG forecasts retail e-commerce at USD 7.4 trillion by 2025, widening runway for niche audio brands that previously lacked shelf access.

Returns-management proficiency becomes a core competency as premium headphones carry high reverse-logistics costs. AI-based fit prediction and virtual try-ons lower return rates, protecting margins that D2C sellers rely on without retailer markups.

By Price Range: Premium Tier Defies Volatility

Mid-range (USD 100-499) devices hold the largest share at 39.55%, yet the premium audiophile bracket (> USD 1,000) shows the swiftest 9.48% CAGR. JBL’s Summit Series, priced up to USD 44,995, targets experience-driven consumers who equate sustainability claims and artisan craftsmanship with long-term value. Solar-powered headphones from Urbanista illustrate how novel power solutions justify premium pricing and align with eco mandates. Entry-level remains vital in emerging economies, yet global inflation pushes shoppers to seek durability, benefiting prosumer (USD 500-999) SKUs that blur professional and consumer lines.

Geography Analysis

Asia-Pacific leads the audio equipment market with a 31.00% revenue share in 2025 and is projected to grow at an 8.55% CAGR to 2031. China’s dual role as manufacturing powerhouse and expanding domestic demand center anchors the region’s strength, while early 5G roll-outs catalyze uptake of low-latency wireless devices. Japanese stalwarts such as Yamaha enlarge automotive sound-system portfolios, confirming the strategic pivot toward mobility applications.

North America benefits from high disposable incomes, robust live-music ecosystems, and rapid streaming-service adoption, reinforcing premium hardware refresh cycles. Automakers integrate immersive sound upgrades, exemplified by Tesla’s Dirac-tuned systems, and professional creators sustain demand for studio-grade monitors amid booming podcast and video production. Europe emphasizes circular-economy compliance, prompting early adoption of recycled plastics, bio-based diaphragms, and take-back programs. Stricter e-waste and packaging directives influence global design guidelines, making European standards a de facto benchmark. Middle East and Africa and South America offer nascent growth opportunities tied to urbanization and rising middle-class consumption, yet spectrum reallocation to 5G and currency volatility pose localized challenges for wireless-audio vendors.

Competitive Landscape

The market exhibits moderate concentration as legacy consumer-audio brands face convergence pressure from automotive and building-automation entrants. Acuity Brands’ USD 1.215 billion purchase of QSC exemplifies vertical integration, embedding pro-audio into smart-lighting portfolios. Patent filings in AI-audio and contextual acoustics rise, with Meta and Apple seeking intangible moats unavailable to purely hardware-centric rivals.

Three strategy archetypes dominate: (1) vertically integrated tech giants controlling silicon, software, and storefront; (2) horizontally expanding audio specialists moving into headphones, soundbars, and automotive; and (3) focused disruptors exploiting niches such as sustainable magnets or D2C community engagement. Sound United’s 2024 losses highlight the risk of overstretched multi-brand portfolios in a market that rewards agile specialization.

Consolidation is expected in mid-tier segments as rising R&D costs for ANC algorithms, codec licensing, and compliance testing squeeze margins. Conversely, premium audiophile and bespoke installation categories remain fragmented, allowing artisanal makers to command double-digit EBITDA through differentiated craftsmanship and localized supply chains.

________________________________________

Audio Equipment Industry Leaders

Sony Group Corporation

Samsung Electronics Co., Ltd.

Bose Corporation

Yamaha Corporation

Apple Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Sennheiser launched the BTD 700 Bluetooth dongle with LE-Audio and Auracast support at USD 59.95.

- May 2025: JBL debuted three Summit Series loudspeakers priced USD 19,995–44,995 at HIGH END Munich 2025.

- April 2025: JBL introduced Tour ONE M3 headphones with Smart Tx transmitter at EUR 399.99.

- March 2025: JBL rolled out Flip 7 and Charge 6 portable speakers featuring AI Sound Boost.

Global Audio Equipment Market Report Scope

The audio equipment market refers to devices that reproduce, record, or process sound. This includes establishments producing electronic audio for home entertainment, musical instrument amplification, automobiles, etc. Audio gear includes tools that replicate, capture, or manipulate sound. This consists of microphones, radios, AV receivers, CD players, tape recorders, amps, mixers, effects units, headphones, and speakers.

The audio equipment market is segmented by product type (mixers, amplifiers, microphones, audio monitors, and other product types), end user (commercial, automotive, home entertainment, and other end users), and geography (North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa). The report offers the market sizes and forecasts for all the above segments in value (USD) terms.

| Mixers |

| Amplifiers |

| Microphones |

| Audio Monitors and Studio Reference |

| Headphones and Earphones |

| Speakers and Soundbars |

| Wired |

| Wireless-Bluetooth |

| Wireless-Wi-Fi / AirPlay |

| Hybrid (Wired + Wireless) |

| Home Entertainment |

| Commercial (Hospitality, Retail, Stadiums) |

| Automotive OEM and Aftermarket |

| Professional Studios and Broadcasting |

| Institutional and Education |

| Offline - Specialty AV Stores |

| Offline - Multi-Brand Electronics Stores |

| Online Marketplaces |

| Direct-to-Consumer (Brand Webstores) |

| Entry-Level (Less than USD 100) |

| Mid-Range (USD 100 - 499) |

| Prosumer (USD 500 - 999) |

| Premium Audiophile (More than USD 1,000) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Rest of Africa |

| By Product Type | Mixers | |

| Amplifiers | ||

| Microphones | ||

| Audio Monitors and Studio Reference | ||

| Headphones and Earphones | ||

| Speakers and Soundbars | ||

| By Connectivity | Wired | |

| Wireless-Bluetooth | ||

| Wireless-Wi-Fi / AirPlay | ||

| Hybrid (Wired + Wireless) | ||

| By End User | Home Entertainment | |

| Commercial (Hospitality, Retail, Stadiums) | ||

| Automotive OEM and Aftermarket | ||

| Professional Studios and Broadcasting | ||

| Institutional and Education | ||

| By Distribution Channel | Offline - Specialty AV Stores | |

| Offline - Multi-Brand Electronics Stores | ||

| Online Marketplaces | ||

| Direct-to-Consumer (Brand Webstores) | ||

| By Price Range | Entry-Level (Less than USD 100) | |

| Mid-Range (USD 100 - 499) | ||

| Prosumer (USD 500 - 999) | ||

| Premium Audiophile (More than USD 1,000) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the global audio equipment market?

It is valued at USD 17.45 billion in 2026.

How fast is automotive audio expected to grow?

Automotive OEM and aftermarket demand is projected to expand at a 10.05% CAGR between 2026-2031.

Which connectivity technology is gaining on Bluetooth?

Wi-Fi/AirPlay solutions are forecast to grow at a 9.88% CAGR, driven by lossless high-bandwidth streaming.

Why are live concerts important for equipment sales?

Rising global festival and tour spending raises demand for advanced speakers, mixers, and wireless systems, adding about 1.15% to overall market CAGR.

What materials trend is shaping premium products?

Eco-acoustic materials such as recycled plastics, flax-fiber cones, and Clean Earth Magnets are gaining traction, supporting premium positioning.

How are brands improving margins?

Direct-to-consumer channels grow at 9.55% CAGR, giving brands higher margins and direct customer data access.

Page last updated on: