Solid Rocket Motors Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

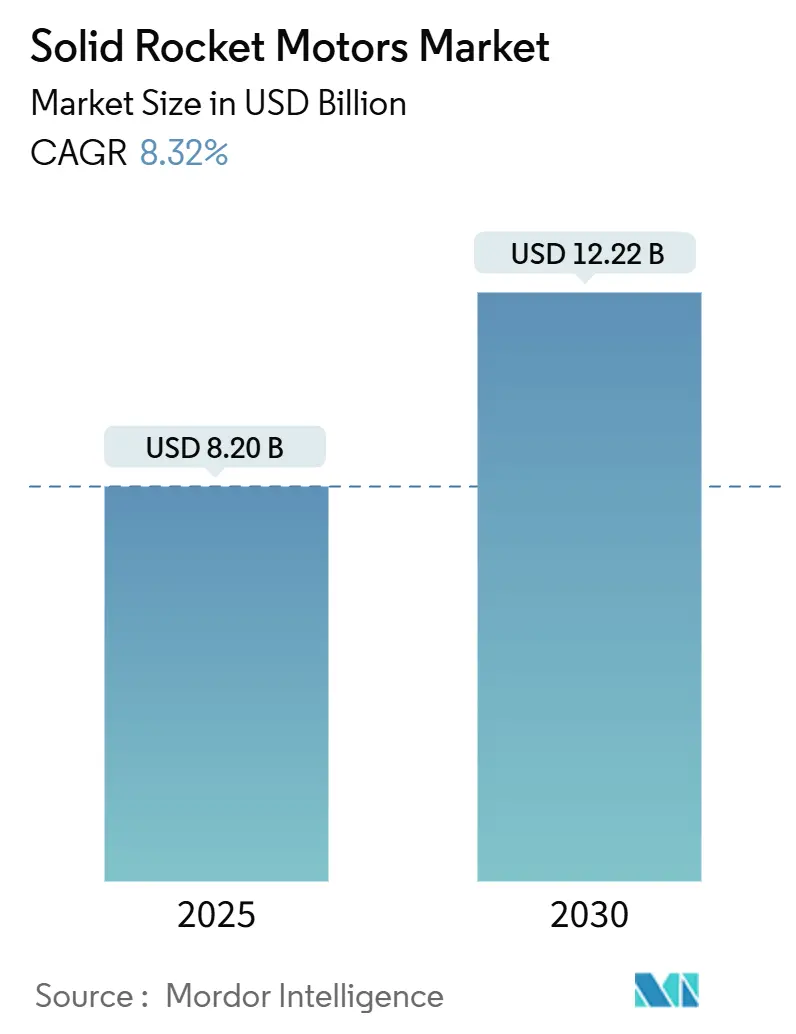

| Market Size (2025) | USD 8.20 Billion |

| Market Size (2030) | USD 12.22 Billion |

| Growth Rate (2025 - 2030) | 8.32% CAGR |

| Fastest Growing Market | Europe |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Solid Rocket Motors Market Analysis by Mordor Intelligence

The solid rocket motors market size stands at USD 8.20 billion in 2025 and is projected to reach USD 12.22 billion by 2030, reflecting an 8.32% CAGR over the forecast period. Substantial defense-modernization budgets, the democratization of commercial space access, and rapid adoption of additive manufacturing underpin this expansion. Heightened missile procurement among NATO allies and Indo-Pacific nations boosts demand, while the surge in small-satellite constellations opens new launch opportunities. Composite propellant innovation and smart-ignition electronics further improve performance and reliability, widening the addressable base for the solid rocket motors market. Simultaneously, collaborative ventures between incumbents and venture-backed entrants shorten development cycles and diversify supply, tempering traditional entry barriers.

Key Report Takeaways

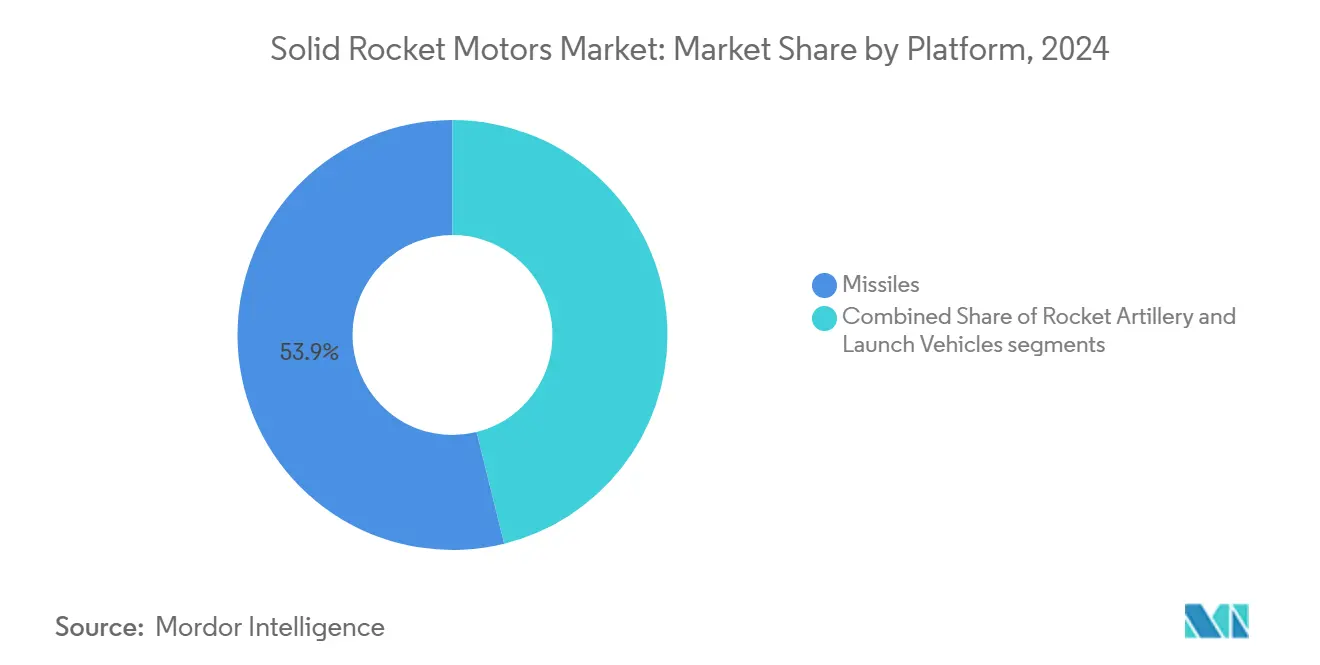

- By platform, missiles led with 53.87% revenue share in 2024. Launch vehicles are projected to expand at a 9.43% CAGR through 2030.

- By component, propellants captured a 47.38% share in 2024. Igniters are forecasted to grow at a 9.67% CAGR through 2030.

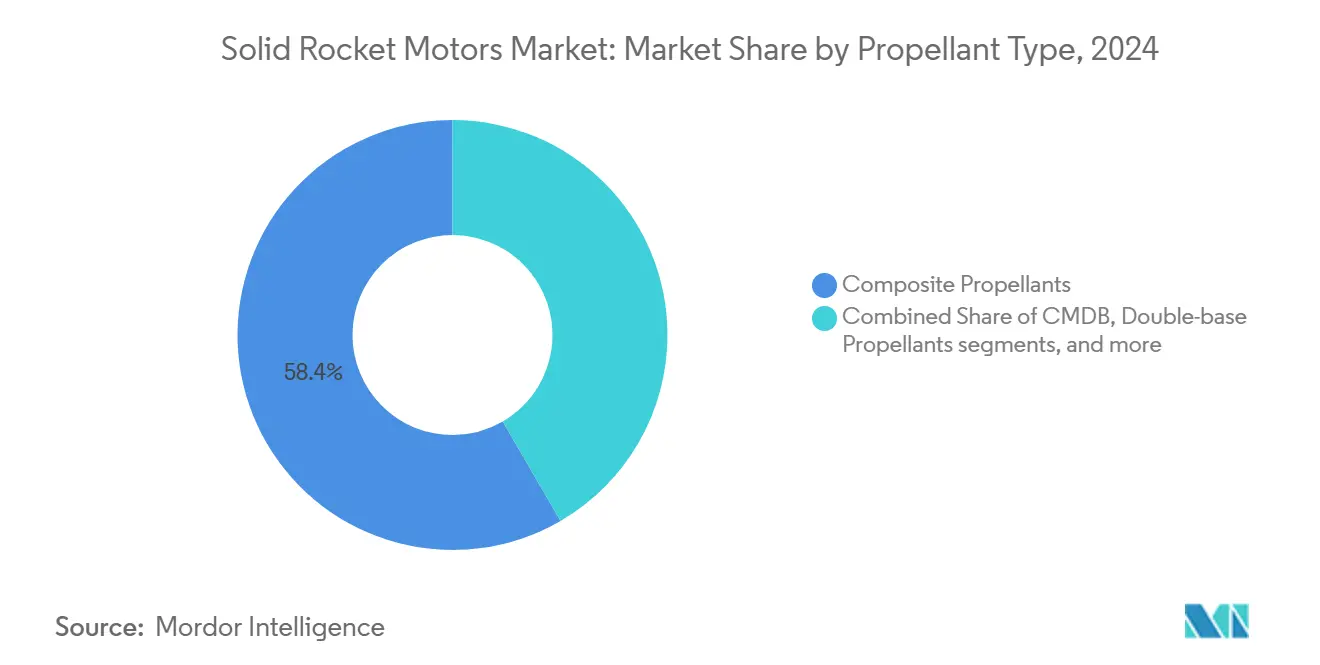

- By propellant type, composite formulations secured a 58.38% share in 2024. Composite modified double-base propellants are set to accelerate at a 10.94% CAGR through 2030.

- By end user, defense and government applications held a 69.48% share in 2024. Commercial space applications are advancing at an 8.23% CAGR through 2030.

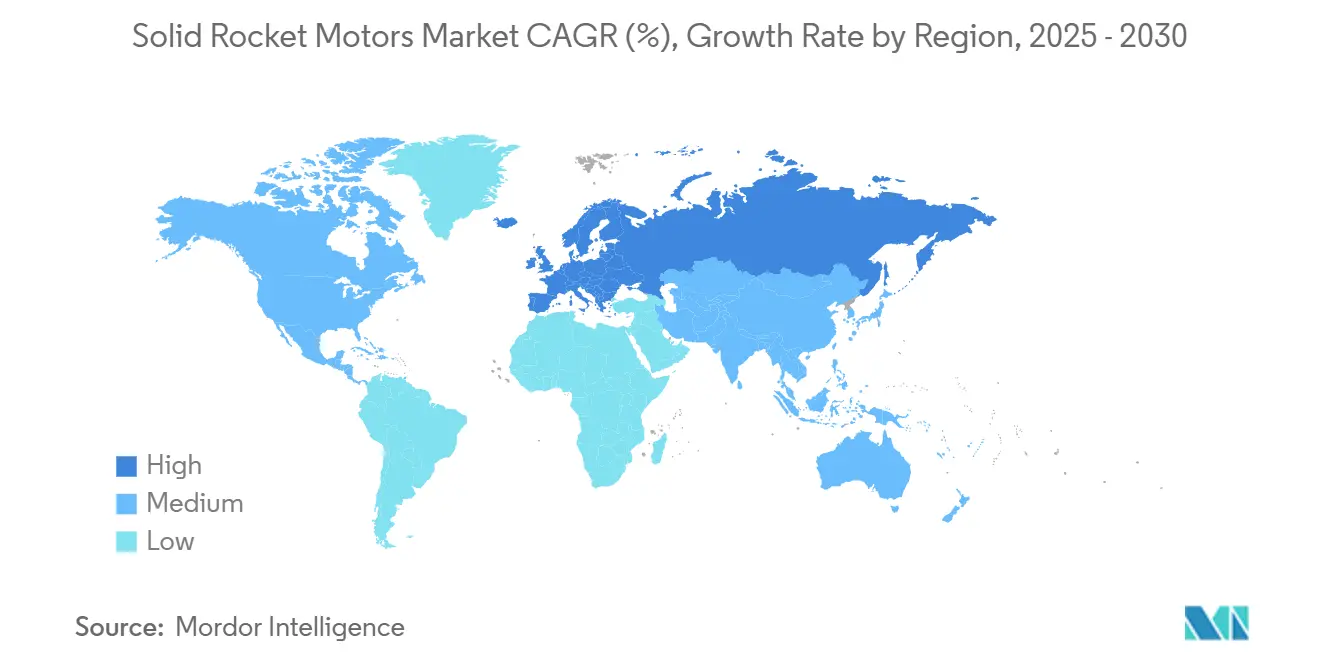

- By geography, North America commanded a 39.59% share in 2024. Europe is poised to register a 9.01% CAGR through 2030.

Global Solid Rocket Motors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing strategic missile procurement programs | +2.80% | Global; strongest in North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Rising commercial small‐satellite launch demand | +2.10% | Global; led by North America and Europe | Medium term (2-4 years) |

| Replacement cycles of legacy ICBM and SLBM boosters | +1.90% | North America, Europe, China, Russia | Long term (≥ 4 years) |

| Miniaturized solid-propellant additive manufacturing | +1.40% | North America, Europe; spillover to Asia-Pacific | Medium term (2-4 years) |

| Dual-use solid propulsion for hypersonic air-breathing vehicles | +1.60% | Global major powers | Long term (≥ 4 years) |

| Strategic alliances and joint ventures | +1.20% | Global; cross-regional technology partnerships | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Strategic Missile Procurement Programs

Defense-modernization imperatives have lifted missile budgets to record levels. The Pentagon allocated USD 14.3 billion for missile procurement in fiscal 2025, and solid rocket motors account for roughly one-quarter of that outlay.[1]Defense News Staff, “Pentagon Budget Allocates $14.3 Billion for Missile Procurement in 2025,” Defense News, defensenews.com NATO members are moving toward the 2%-of-GDP spending pledge to replenish tactical and strategic stockpiles, while Japan and South Korea are escalating counterstrike and launch-vehicle programs. Combined with rising demand for hypersonic weapons, these factors reinforce long-cycle revenue visibility for the solid rocket motors market. Technology transfer clauses within ITAR frameworks encourage co-production, fostering capacity growth in allied nations.

Rising Commercial Small-Satellite Launch Demand

Small-satellite deployments jumped 85% to more than 2,400 units in 2024, creating fresh launch slots for cost-sensitive constellation operators.[2]Jeff Foust, “Small Satellite Launches Surge 85% in 2024,” SpaceNews, spacenews.com Solid motors underpin the kick stages of dedicated small-lift vehicles by Rocket Lab and Firefly Aerospace, offering streamlined ground operations and rapid turnaround. FAA licensing reforms shorten approval times, accelerating flight cadence for emerging providers. As rideshare payload volumes climb, demand shifts toward solid-propelled orbital transfer vehicles that reduce constellation build-out timelines. These trends strengthen the commercial pillar of the solid rocket motors market.

Replacement Cycles of Legacy ICBM and SLBM Boosters

The USD 95 billion Ground-Based Strategic Deterrent program drives wholesale replacement of Minuteman III boosters and sustains large-scale solid motor production into the 2030s. In parallel, France’s M51 and the UK’s Trident refreshes require multi-stage composite motors with higher energy densities. China’s migration toward road-mobile, solid-fueled strategic assets underscores the global shift. Long development and certification cycles lock in multi-decade demand, cementing the segment’s significance within the solid rocket motors market.

Miniaturized Solid-Propellant Additive Manufacturing

Air Force Research Laboratory investments in 3D-printed grain geometries cut propellant waste by 40% while enabling custom burn profiles.[3]AFRL Public Affairs, “3D Printing Advances Solid Propellants,” Air Force Research Laboratory, afrl.af.mil Northrop Grumman reports 30–50% shorter lead times after adopting printed tooling and nozzle inserts, compressing production cycles for urgent-need programs. Rapid prototyping enables smaller firms to enter limited-quantity tactical missile niches without building capital-intensive casting lines, intensifying price competition across the supply base. NASA and the US DoD are drafting common qualification standards that will let vendors certify additively manufactured motors once and reuse data packages across multiple platforms, speeding adoption. As testing databases grow, insurers are expected to offer more favorable premiums for printed components, reinforcing the technology’s commercial case.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Environmental restrictions on perchlorate emissions | −0.9% | Global; strictest in North America and Europe | Short term (≤ 2 years) |

| Volatile aluminium powder supply chain | −0.7% | Global; most acute in Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Export-control tightening on dual-use grain‐bonding agents | −0.6% | Global; primarily US and European regulatory regimes | Medium term (2-4 years) |

| Space-launch shift toward reusable liquid stages | −0.5% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Environmental Restrictions on Perchlorate Emissions

The US EPA’s 15 ppb perchlorate limit and California’s stricter 6 ppb cap require manufacturers to install closed-loop filtration systems that cost USD 2–5 million per facility and add recurring monitoring expenses. European REACH regulation labels ammonium perchlorate a substance of very high concern, obligating producers to seek time-limited authorizations or switch to alternative oxidizers, which raises R&D outlays and qualification timelines. Firms that achieve full compliance gain reputational advantages in defense solicitations, yet the added overhead squeezes margins in price-sensitive commercial launch programs. Some suppliers respond by relocating batch-mixing operations to jurisdictions with less stringent water-discharge rules, though they must still meet export-market standards. These dynamics encourage accelerated investment in nitrate-based or green-binder propellants that promise lower lifecycle remediation costs.

Volatile Aluminium Powder Supply Chain

Aluminum powder prices surged 35% in 2024 as energy inflation, transport delays, and smelter outages tightened availability, directly inflating composite propellant bills of material. China controls roughly 60% of global capacity, so geopolitical tensions prompt Western prime contractors to stockpile strategic reserves and negotiate dual-source contracts to reduce single-country exposure. Aerospace-grade powders require narrow particle-size distributions and ultra-low impurity levels, limiting the pool of qualified vendors and lengthening lead times for new entrants. Buyers increasingly deploy price-escalation clauses and hedging instruments to stabilize budgets over multiyear missile programs. Companies that embed real-time supplier-risk dashboards and long-horizon inventory models gain differentiation in competitive bids, highlighting supply-chain resilience as a selling point.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform: Missiles Drive Market Leadership

Missiles accounted for 53.87% of the solid rocket motor market share in 2024 on the back of strategic deterrent upgrades across major defense economies. Launch vehicles registered the highest 9.43% CAGR and are set to widen adoption as small-satellite launch frequencies climb. The solid rocket motors market size attributed to missile platforms is projected to rise steadily through 2030 as hypersonic programs transition from development to production. Beyond strategic systems, guided MLRS and next-generation tactical missiles sustain recurring demand. Competitive intensity increases as Anduril scales its new production line under a USD 14.3 million Pentagon contract. Parallel civil-space expansion positions solid-propelled launch vehicles as a cost-efficient alternative to reusable liquids for dedicated nano-sat flights, although the latter’s reusability advantage narrows certain margins.

Launch-vehicle momentum stems from simplified ground infrastructure, all-weather readiness, and shorter integration timelines that appeal to constellation operators. Providers such as Virgin Orbit exploit air-launch architectures to maximize schedule flexibility, reinforcing the attractiveness of solid motors for responsive access. Over the forecast period, dual-use transfer stages employing solid kick motors will further intertwine defense and commercial revenue streams within the solid rocket motors market.

By Component: Propellants Dominate Value Chain

Propellants captured 47.38% of component revenue in 2024 and remain the primary value driver. Rising aluminum and ammonium perchlorate costs amplify their impact on bill-of-materials outlays. The solid rocket motors market size contribution from propellants is expected to expand in absolute terms despite stabilization of input prices after 2026. Manufacturers pursue supply-chain resilience through multi-year offtake deals and in-house milling investment, strategies that favor well-capitalized incumbents.

Igniters, the fastest-growing component at a 9.67% CAGR, reflect surging demand for smart-ignition modules that integrate health-monitoring electronics. These systems mitigate misfire risk and extend mission-readiness windows. Growth cascades to insulation and case-bond liners that must accommodate higher burn temperatures, enlarging addressable volume for specialist materials suppliers. The component mix evolution raises technical thresholds for new entrants and consolidates bargaining power among integrated prime contractors in the solid rocket motors market.

By Propellant Type: Composite Formulations Lead Innovation

Composite propellants commanded a 58.38% share in 2024, leveraging the high specific impulse of aluminium–perchlorate mixes. Ongoing R&D targets lower-toxicity oxidizers and greener binders in response to environmental strictures. Composite modified double-base propellants will log a 10.94% CAGR through 2030 as their higher energy densities enable longer-range tactical systems without enlarging airframe envelopes. The solid rocket motors market size allocated to CMDB formulations could almost double by the end of the forecast window.

Additive manufacturing breakthroughs allow intricate slotting and honeycomb grains that fine-tune regression rates, boosting thrust-to-weight ratios. Meanwhile, double-base formulas keep niche roles where extreme cold-soak tolerance and rapid burn are indispensable. Academic-industry consortia across Europe investigate nitrate-based oxidizers to phase down ammonium perchlorate use, a trend that may reshape sourcing maps over the next decade.

By End User: Defense Dominance with Commercial Growth

Defense and government fleets held 69.48% revenue share in 2024, reflecting multi-year modernization programs. The US Minuteman replacement alone secures steady volumes through the mid-2030s, maintaining the largest slice of the solid rocket motors market. Export-control regimes insulate incumbents but prompt allied nations to seek domestic production under licensing, expanding the global footprint of trusted primes.

Commercial space, advancing at an 8.23% CAGR, benefits from reduced insurance premiums tied to the inherent simplicity of solid propulsion. The segment’s growth taps into national broadband projects and earth-observation demands. As insurers build performance histories on new solid-based launch vehicles, favorable rates could lift payload reservations further, reinforcing a dual-pillar growth model for the solid rocket motors market.

Geography Analysis

North America generated 39.59% of revenue in 2024, anchored by the Pentagon’s USD 800 billion-plus annual budget and the world’s largest commercial launch cluster. The region’s lead persists as Northrop Grumman scales delivery under the Ground-Based Strategic Deterrent and L3Harris expands Aerojet Rocketdyne production lines. The solid rocket motors market size tied to North American buyers continues to swell with rising tactical missile procurements. Canada boosts outlays on air-defense rockets, and Mexican aerospace hubs widen sub-tier supply participation, reinforcing regional vertical integration.

As strategic autonomy drives investment, Europe is the fastest-growing territory at a 9.01% CAGR through 2030. MBDA’s EUR 400 million (USD 469.54 million) purchase of Roxel consolidates the continent’s propulsion expertise, while Avio’s EUR 150 million (USD 175.04 million) CAMM-ER win showcases demand for extended-range air-defense solutions. France’s M51 missile line and Germany’s expanded defense budget underpin consistent order flow. Simultaneously, REACH-driven environmental mandates foster R&D in perchlorate-free propellants, potentially yielding exportable intellectual property and carving new niches within the solid rocket motors market.

Asia-Pacific is highly fragmented yet offers long-run upside as China scales Gravity-1 and Long March 8A developments, India accelerates Pinaka rocket variants, and Japan pursues counterstrike systems. South Korea’s indigenous launch vehicle entering service in 2024 illustrates accelerating regional competence. Supplier ecosystems mature as local firms partner with US and European primes to meet offset requirements. The Middle East and Africa remain modest contributors but secure periodic boosts from interceptor acquisitions and emerging small-sat initiatives, rounding out global demand diversity.

Competitive Landscape

The solid rocket motors market shows moderate concentration. Northrop Grumman Corporation, L3Harris Technology, Inc. and Rafael Advanced Defense Systems Ltd. control strategic programs and proprietary propellant IP, generating economies of scale and regulatory moats. They leverage decades-deep security clearances and vertically integrated supply chains. Revenue visibility from defense backlogs sustains elevated R&D funding that outpaces smaller peers.

Disruptors such as Anduril Industries and Ursa Major Technologies deploy agile engineering and additive manufacturing to compress prototype cycles, attracting venture capital and rapid contracts. Their focus on commercial and responsive-launch niches circumvents heavy bureaucracy, yet qualification hurdles slow incursions into nuclear-deterrent classes. Strategic partnerships bloom as incumbents acquire equity stakes or form joint ventures to co-opt emergent capabilities, exemplified by the USD 175 million Kratos–RAFAEL Prometheus Energetics venture.

Technology differentiation centers on high-energy CMDB propellants, reusable insulation liners and printed nozzles with embedded sensors. End-to-end digital twins cut test firings and bring data-driven validation into mainstream workflows. Although ITAR confines foreign access, allied license production broadens global sourcing footprints. Environmental stewardship around perchlorate effluents is evolving into a competitive selling point, influencing contract awards as governments factor lifecycle compliance into procurement scoring.

Solid Rocket Motors Industry Leaders

Northrop Grumman Corporation

Rafael Advanced Defense Systems Ltd.

L3Harris Technology, Inc.

Nammo AS

Anduril Industries, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Kratos and RAFAEL formed Prometheus Energetics, investing USD 175 million in advanced motor production slated for a 2027 start-up.

- January 2025: The US Pentagon awarded Anduril Industries a USD 14.3 million solid rocket motor expansion contract to enhance tactical-missile responsiveness.

Global Solid Rocket Motors Market Report Scope

| Missiles |

| Rocket Artillery |

| Launch Vehicles |

| Propellants |

| Nozzles |

| Igniters |

| Motor Casing |

| Other Components |

| Composite Propellants |

| Double-base Propellants |

| Composite Modified Double-base (CMDB) |

| Other Advanced Formulations |

| Defense and Government |

| Commercial Space |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Platform | Missiles | ||

| Rocket Artillery | |||

| Launch Vehicles | |||

| By Component | Propellants | ||

| Nozzles | |||

| Igniters | |||

| Motor Casing | |||

| Other Components | |||

| By Propellant Type | Composite Propellants | ||

| Double-base Propellants | |||

| Composite Modified Double-base (CMDB) | |||

| Other Advanced Formulations | |||

| By End User | Defense and Government | ||

| Commercial Space | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| Israel | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the solid rocket motors market in 2030?

It is forecasted to reach USD 12.22 billion by 2030 based on an 8.32% CAGR.

Which platform segment is expanding the fastest?

Launch vehicles are growing at a 9.43% CAGR through 2030, fueled by small-satellite deployment needs.

Which region shows the highest growth rate?

Europe is expected to post a 9.01% CAGR as strategic autonomy drives defense spending.

How significant is defense demand compared with commercial space?

Defense and government buyers hold 69.48% share, but commercial space is advancing at an 8.23% CAGR.

What environmental regulation most affects manufacturers?

Tightening perchlorate-emission limits, notably the US EPA’s 15 ppb cap and stricter state thresholds, add compliance costs.

Which technological trend is reshaping production economics?

Additive manufacturing of propellant grains and motor components cuts waste by up to 40% and accelerates prototyping.

Page last updated on: