Multi-Launch Rocket Systems (MLRS) Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

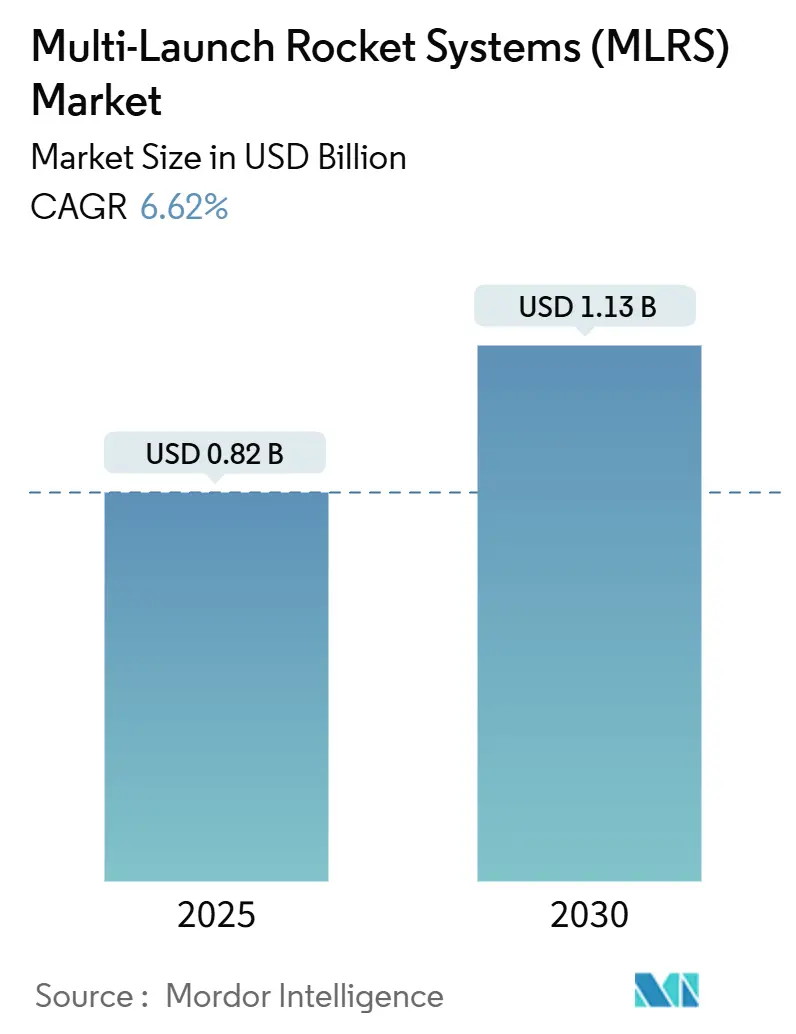

| Market Size (2025) | USD 0.82 Billion |

| Market Size (2030) | USD 1.13 Billion |

| Growth Rate (2025 - 2030) | 6.62% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Multi-Launch Rocket Systems (MLRS) Market Analysis by Mordor Intelligence

The Multi-Launch Rocket Systems (MLRS) market size stands at USD 0.82 billion in 2025 and is forecasted to reach USD 1.13 billion by 2030, advancing at a 6.62% CAGR. This expansion reflects sustained recapitalization programs, defense budget increases, and a shift toward precision-guided, extended-range rockets. Sovereign initiatives like the US Army’s USD 451 million M270A2 upgrade and Finland’s USD 450 million modernization effort underscore global commitment to refreshing Cold War-era inventories. Asia-Pacific remains the primary growth engine as regional security tensions spur accelerated procurement, while modular launcher designs and network-centric command-and-control integration open new capability pathways. Competitive intensity mounts because loitering munitions and swarming drones threaten legacy fire-support roles, pressing incumbents to add counter-drone and AI-enabled targeting features. Supply-chain constraints in propellant chemicals and artillery barrels place added pressure on delivery schedules, though joint-production offsets—exemplified by Poland’s USD 1.6 billion Chunmoo deal—help diversify manufacturing footprints.

Key Report Takeaways

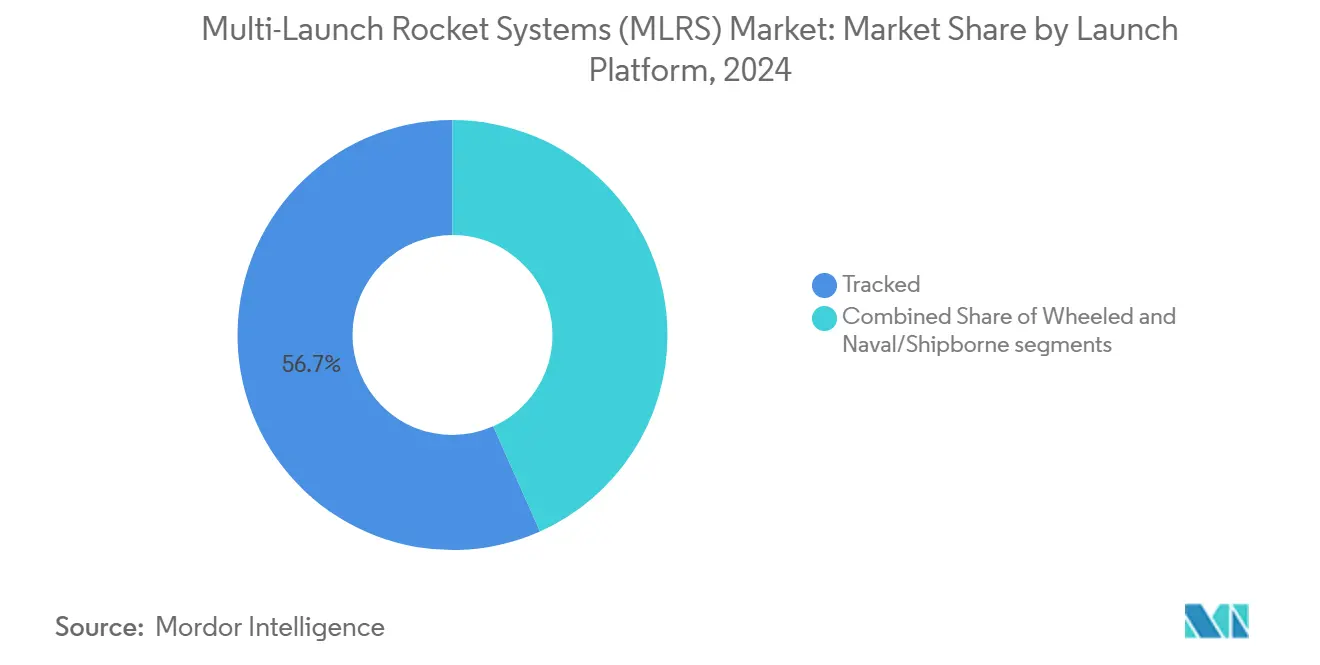

- Tracked platforms led with 56.67% of the MLRS market share in 2024; wheeled platforms are projected to post an 8.01% CAGR through 2030.

- Systems exceeding 300 mm commanded a 40.01% share of the MLRS market in 2024 and are predicted to grow at a 7.24% CAGR over the forecast horizon.

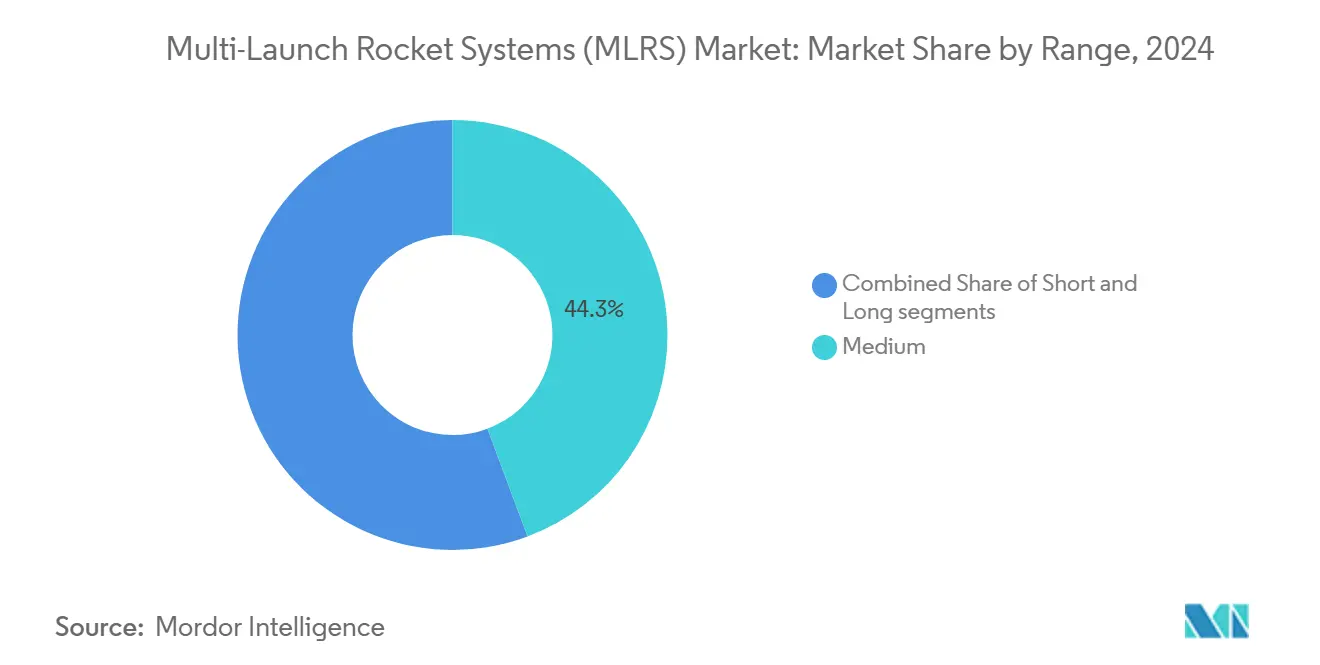

- Medium-range launchers accounted for 44.32% of the MLRS market in 2024, while long-range systems are forecasted to register a 7.75% CAGR by 2030.

- Launchers carrying 16 to 40 pods captured 53.22% of the MLRS market share in 2024 and are advancing at a 7.89% CAGR during the study period.

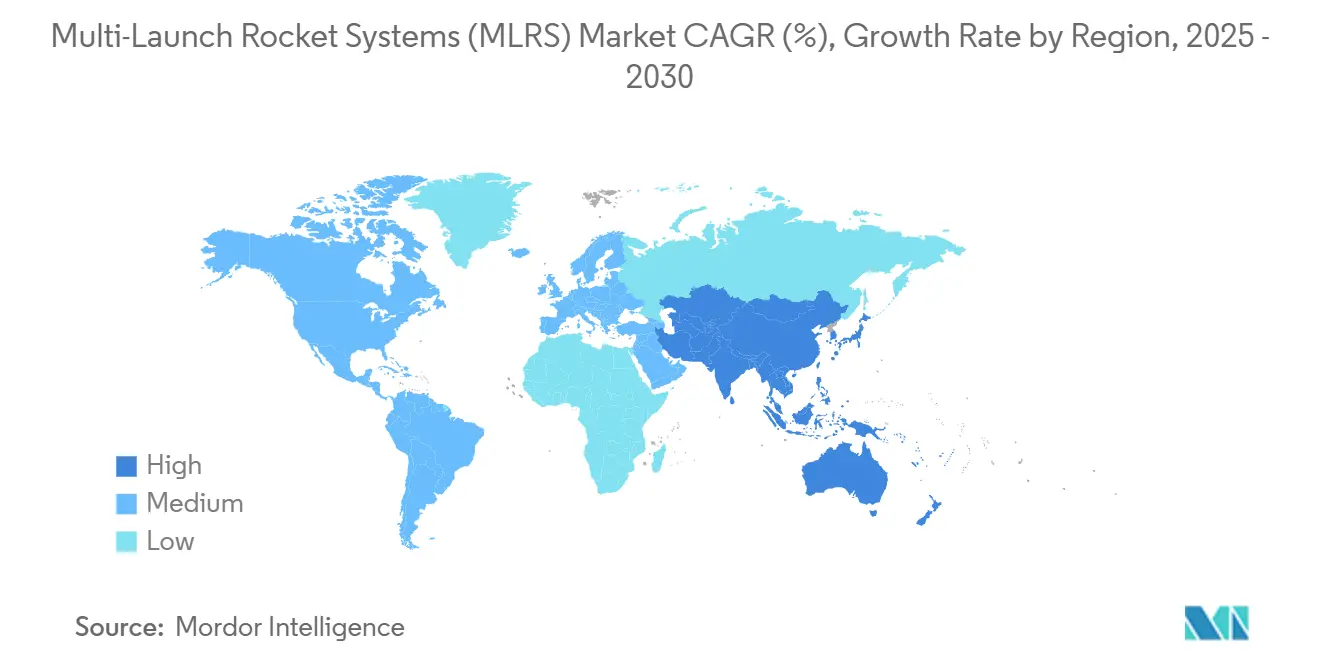

- Asia-Pacific held 34.85% of the MLRS market in 2024 and is expanding at a 7.37% CAGR through 2030.

Global Multi-Launch Rocket Systems (MLRS) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Modernization-driven recapitalization programs | +1.8% | Global, concentrated in North America and Europe | Medium term (2–4 years) |

| Rising defense budgets amid regional security tensions | +1.5% | Asia-Pacific core, spill-over to Europe and Middle East | Short term (≤ 2 years) |

| Shift toward precision-guided, extended-range rockets | +1.2% | Global, led by technologically advanced nations | Long term (≥ 4 years) |

| Integration of MLRS into advanced network-centric command and control (C2) systems | +0.9% | North America and EU, expanding to Asia-Pacific | Medium term (2–4 years) |

| Growth in international exports through joint production and offset programs | +0.7% | Global, emerging-market focus | Long term (≥ 4 years) |

| Advancements in modular launcher designs enabling multi-caliber flexibility | +0.6% | Global | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Modernization-Driven Recapitalization Programs

Nations are systematically retiring legacy rocket artillery and embracing digital launchers with enhanced mobility, as illustrated by the US Army’s M270A2 contract valued at USD 451 million. Finland’s USD 450 million upgrade, Poland’s USD 1.6 billion Chunmoo acquisition, and the UK’s decision to double its M270 fleet confirm an urgent modernization cycle. These programs bundle new fire-control software, GPS-enabled guidance, and survivability kits to capitalize on lessons from recent conflicts where precision rocket artillery proved decisive. The push drives baseline demand for launch vehicles and reload pods, cementing a positive outlook for the MLRS market.

Rising Defense Budgets Amid Regional Security Tensions

Global defense outlays reached USD 2.72 trillion in 2024, up 9.4% yearly, directly boosting MLRS procurement.[1]Stockholm International Peace Research Institute, “Global Defense Expenditure 2024,” sipri.org Europe accelerated spending by 17% after Russia’s Ukraine invasion, prompting Baltic-state HIMARS orders totaling USD 495 million. Asia-Pacific mirrors the trend as China positions PHL-16 batteries near contested borders and India invests USD 10.1 billion in PINAKA rockets. Heightened readiness requirements sustain a funding environment favorable to MLRS market expansion.

Shift Toward Precision-Guided, Extended-Range Rockets

Lockheed Martin’s ER-GMLRS extends reach to 150 km with GPS/INS packages and is ramping to 19,000 rockets annually by FY 2028. India’s Guided Pinaka delivers 30 m CEP at 75 km and entered mass production after 2024 validation tests. Precision capabilities minimize collateral damage and unlock new target sets, broadening routine MLRS usage. Cost curves fall as volume production scales, reinforcing adoption across the MLRS market.

Integration of MLRS into Advanced Network-Centric Command and Control Systems

Launchers act as networked nodes, pulling UAV and satellite cues into fire-control loops through platforms like EuroPULS.[2]Rheinmetall, “EuroPULS Modular Systems,” rheinmetall.com France’s forthcoming Foudre couples ODIN communications with Aarok drones to form sensor-to-shooter chains under 60 seconds. AI algorithms recommend munition types in real time, elevating MLRS lethality and inter-allied interoperability, a capability that strengthens the MLRS market’s strategic relevance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Budgetary fluctuations affecting long-term procurement cycles | -1.1% | Global, heavier on developing nations | Short term (≤ 2 years) |

| Stringent international export controls and ITAR compliance restrictions | -1.0% | Global, with primary impact on US and European exporters | Long term (≥ 4 years) |

| Rising competition from loitering munitions and unmanned aerial swarm systems | -0.8% | Technologically advanced markets | Medium term (2–4 years) |

| High lifecycle costs and logistical challenges in sustaining MLRS operations | -0.7% | Global, greater impact on smaller militaries | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Budgetary Fluctuations Affecting Long-Term Procurement Cycles

Annual appropriations add uncertainty to multiyear launcher contracts, as highlighted by US Congressional reports on procurement challenges. European programs have slid timelines amid fiscal pressures, while emerging economies often split purchases into smaller tranches, prolonging delivery schedules. Uneven cash flows complicate supplier planning and may delay shipments in the MLRS market.

Rising Competition From Loitering Munitions and Unmanned Aerial Swarm Systems

Estonia’s SkyStriker acquisition shows the armed forces valuing lower-cost, precision loitering drones. FPV quadcopters offer point-target strike for a fraction of rocket costs, pressuring MLRS budgets. Yet MLRS retains advantages in payload mass, range, and all-weather performance, ensuring a complementary role rather than outright displacement in the MLRS market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Launch Platform: Tracked Dominance, Wheeled Acceleration

Tracked launchers held a 56.67% share in 2024, reflecting survivability and cross-country mobility valued for high-tempo operations. The MLRS market size for tracked vehicles is projected to expand steadily amid continuing M270A2 retrofits and similar programs. Wheeled launchers, paced by the M142 HIMARS, are growing 8.01% CAGR as forces favor C-130 transportability and rapid shoot-and-scoot tactics. Tracked systems remain essential for protracted campaigns, while wheeled assets underpin expeditionary or allied quick-reaction forces, positioning both as complementary pillars of the MLRS market.

The modular trend blurs platform lines; the Czech RM-70 Modular offers chassis types and eases caliber swaps. Naval adaptations—such as US proposals for shipboard launch cells—extend MLRS's reach into littoral zones. Integration of active protection and counter-UAV suites across chassis further differentiates offerings in the MLRS market.

By Caliber: Large-Caliber Momentum

Launchers exceeding 300 mm amassed a 40.01% share in 2024 and led growth at 7.24% CAGR, backed by China’s PHL-16 and India’s Guided Pinaka upgrades.[3]SP’s MAI, “China Deploys Long Range MLRS,” spsmai.com These systems marry deep-strike reach with sizable warheads, allowing commanders to engage strategic nodes once reserved for missiles, lifting the segment's MLRS market size. Smaller calibers still serve saturation or urban-support roles where volume fire holds value.

Precision guidance enhances large-caliber relevance; complex seeker packages fit more easily in 300 mm-plus bodies, opening longer-range, reduced-CEP engagements that sharpen the MLRS market proposition.

By Range: Medium-Range Core, Long-Range Upswing

Medium-range launchers maintained a 44.32% share in 2024, balancing ammunition load and tactical reach for most mission sets. Long-range variants, however, accelerate at 7.75% CAGR thanks to ER-GMLRS and France’s Foudre ambitions exceeding 500 km. As counter-battery threats intensify, long-range standoff grows attractive, lifting MLRS market adoption beyond traditional battlefields.

Short-range assets persist for urban or mountainous terrain where rapid repositioning trumps distance, ensuring the portfolio breadth necessary to satisfy evolving doctrines in the MLRS market.

By Pod Capacity: High-Capacity Preference

Systems loading 16–40 pods took 53.22% share in 2024 and outpaced the field at 7.89% CAGR, driven by India’s PINAKA batteries that discharge 72 rockets in 44 seconds. Extended engagement windows reduce resupply frequency, a premium in contested logistics environments. Lower-capacity systems still fill niche quick-reaction roles and facilitate air transport, preserving diverse options inside the MLRS market.

Automated reloaders and palletized launcher designs shrink turnaround times, strengthening high-capacity platforms’ pull on procurement budgets.

Geography Analysis

Asia-Pacific captured a 34.85% share in 2024 and posts a 7.37% CAGR through 2030 as China fields PHL-16 near the Line of Actual Control and India channels USD 10.10 billion into PINAKA series rockets.[4]Business Standard, “MoD Signs Rs 10k cr PINAKA Deals,” business-standard.com South Korea’s K239 Chunmoo exports and Australia’s indigenous GMLRS production reinforce regional manufacturing self-reliance, while Japan scales island-defense rocket emplacements. Integration of local industry and offset clauses positions Asia-Pacific to remain the cornerstone of the MLRS market growth.

Europe accelerates acquisitions after Ukraine conflict lessons. Poland’s USD 1.6 billion Chunmoo purchase, Baltic HIMARS deliveries worth USD 495 million, and the UK’s decision to double M270 fleets signal a pivot toward long-range fires. Indigenous projects like France’s Foudre reduce import reliance and support NATO interoperability goals. European modernization thus elevates the MLRS market despite budgetary scrutiny.

North America sustains demand through technology upgrades rather than new platform counts. The M270A2 retrofit and ER-GMLRS serial production underpin stable MLRS market revenues, while Canada’s exploratory programmes and Mexico’s emergent defense requirements add incremental potential. The Middle East and Africa show nascent but promising uptake driven by border security and anti-access needs, often facilitated via technology-transfer contracts.

Competitive Landscape

The multi-launch rocket systems (MLRS) market is moderately consolidated. Lockheed Martin Corporation anchors the field with HIMARS and GMLRS, backed by the USD 451 million M270A2 award and ramp-up to 19,000 rockets annually. Hanwha Corporation leverages K239 Chunmoo's success in penetrating Europe and Southeast Asia, while BAE Systems plc remains a critical subsystem supplier. Disruption from loitering munitions spurs incumbents to integrate counter-drone kits and AI-enabled targeting, further differentiating portfolios.

White-space expansion favors players offering technology transfer. India's PINAKA programme underscores indigenous maturation and export potential to Armenia and Nigeria. Elbit Systems' PULS and Rheinmetall's EuroPULS stress modularity and multi-caliber support, sharpening competition. Vertical-integration strategies that fuse launchers, guided rockets, and C2 software resonate with buyers seeking turnkey solutions, defining success factors in the MLRS market.

Multi-Launch Rocket Systems (MLRS) Industry Leaders

Lockheed Martin Corporation

Hanwha Corporation

Elbit Systems Ltd.

BAE Systems plc

KNDS N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: The US Department of Defense (DoD) awarded Lockheed Martin a USD 214 million contract to upgrade M270 MLRS to the A2 configuration.

- February 2025: India’s Ministry of Defence (MoD) signed INR 10,147 crore (USD 1.2 billion) contracts with Economic Explosives Limited and Munitions India Limited for advanced PINAKA rocket systems

- August 2024: The Defence Technology Institute (DTI) of Thailand, in collaboration with Elbit Systems Ltd., delivered a prototype of the D11A MLRS to the Royal Thai Army.

Global Multi-Launch Rocket Systems (MLRS) Market Report Scope

| Tracked |

| Wheeled |

| Naval/Shipborne |

| 100 to 180 mm |

| 180 to 240 mm |

| More than 300 mm |

| Short |

| Medium |

| Long |

| Up to 16 |

| 16 to 40 |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Launch Platform | Tracked | ||

| Wheeled | |||

| Naval/Shipborne | |||

| By Caliber | 100 to 180 mm | ||

| 180 to 240 mm | |||

| More than 300 mm | |||

| By Range | Short | ||

| Medium | |||

| Long | |||

| By Pod Capacity | Up to 16 | ||

| 16 to 40 | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the Multi-Launch Rocket Systems market in 2025?

The Multi-Launch Rocket Systems (MLRS) market size is USD 0.82 billion in 2025, and is forecasted to reach USD 1.13 billion by 2030

What CAGR is expected for Multi-Launch Rocket Systems through 2030?

The market is projected to grow at a 6.62% CAGR between 2025 and 2030.

Which region leads future demand for Multi-Launch Rocket Systems?

Asia-Pacific holds the largest share at 34.85% and records the fastest 7.37% CAGR.

Which platform type shows the fastest expansion?

Wheeled launchers grow at an 8.01% CAGR due to rapid-deployment advantages.

Why are precision-guided rockets important for MLRS upgrades?

Precision guidance extends range, reduces collateral damage, and broadens target sets, enhancing overall system value.

Page last updated on: