Rocket Propulsion Systems Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

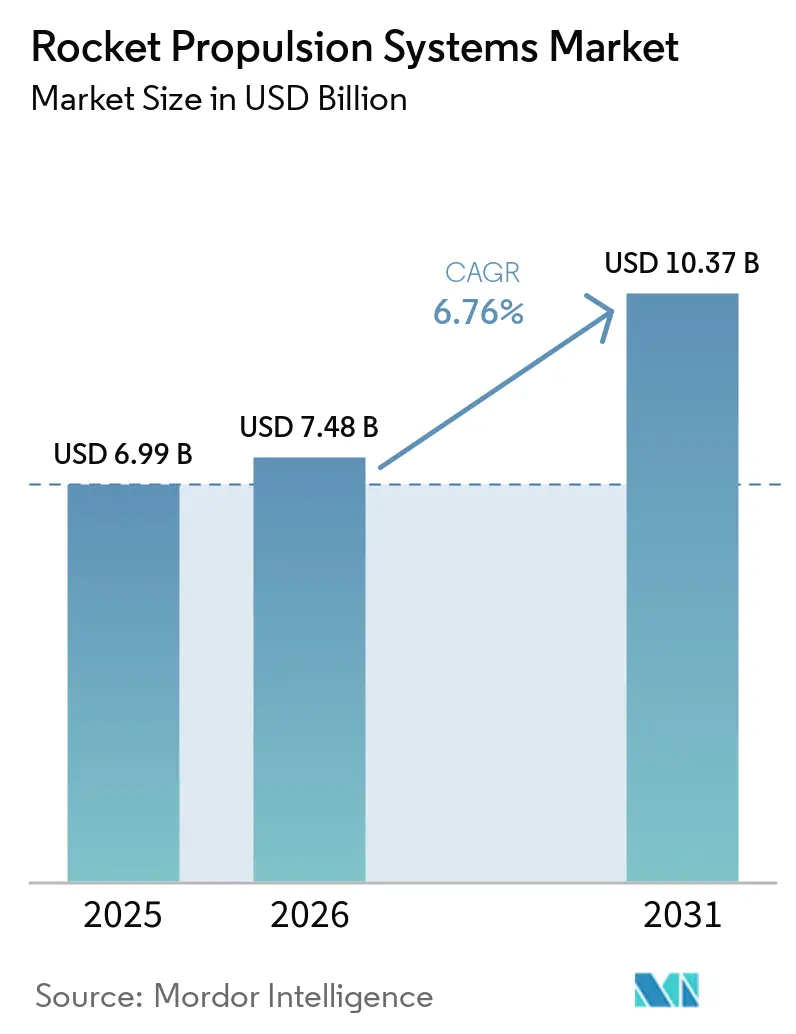

| Market Size (2026) | USD 7.48 Billion |

| Market Size (2031) | USD 10.37 Billion |

| Growth Rate (2026 - 2031) | 6.76% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Rocket Propulsion Systems Market Analysis by Mordor Intelligence

The rocket propulsion systems market size is expected to grow from USD 6.99 billion in 2025 to USD 7.48 billion in 2026 and is forecasted to reach USD 10.37 billion by 2031 at a 6.76% CAGR over 2026-2031. Momentum is shaped by reusable launch vehicles that structurally reduce unit economics, high-cadence constellation deployment that pulls propulsion into volume manufacturing, and additive manufacturing that compresses development cycles and costs. Sovereign budgets in deep-space exploration and national security launches anchor multi‑year demand for large liquid stages, solid rocket motors, and advanced air‑breathing propulsion. Capacity is scaling on the back of firm orders for constellation launches and a widening pipeline of defense programs, including hypersonic systems. These dynamics position the rocket propulsion systems market to benefit from cost deflation, faster iteration, and a broader funding base across civil and defense customers.

Key Report Takeaways

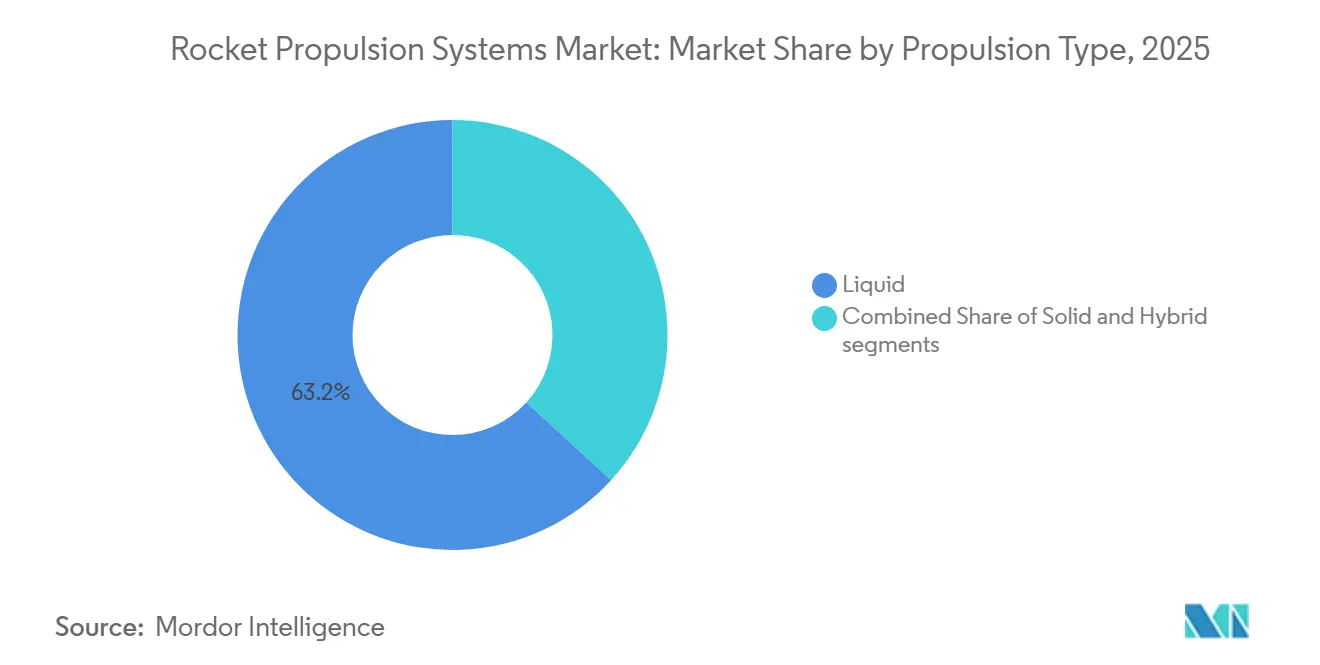

- By propulsion type, liquid propulsion led with a 63.22% share in 2025, while hybrid propulsion is forecasted to expand at an 8.91% CAGR during 2026-2031.

- By end user, civil and commercial accounted for a 58.95% share in 2025, while military and government are projected to grow at a 7.86% CAGR during 2026-2031.

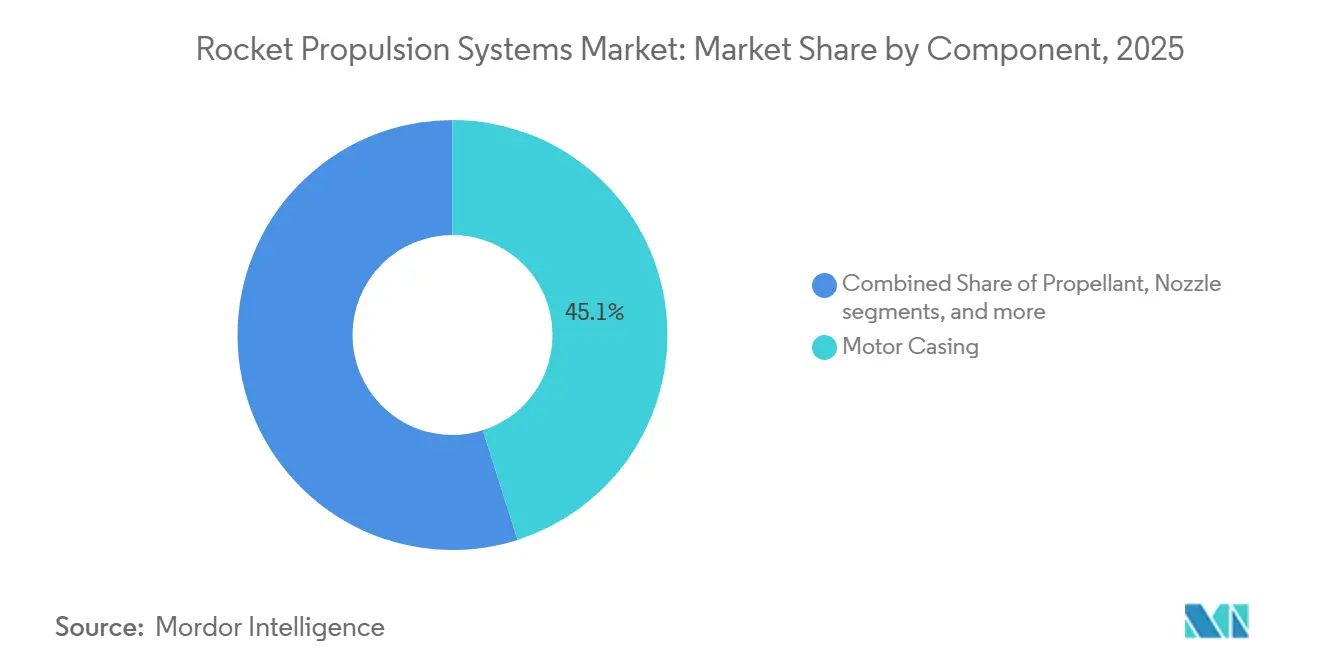

- By component, motor casings held a 45.1% share in 2025, while propellants are set to expand at a 7.62% CAGR during 2026-2031.

- By type, rocket motors commanded a 58.88% share in 2025, while rocket engines are expected to grow at an 8.05% CAGR during 2026-2031.

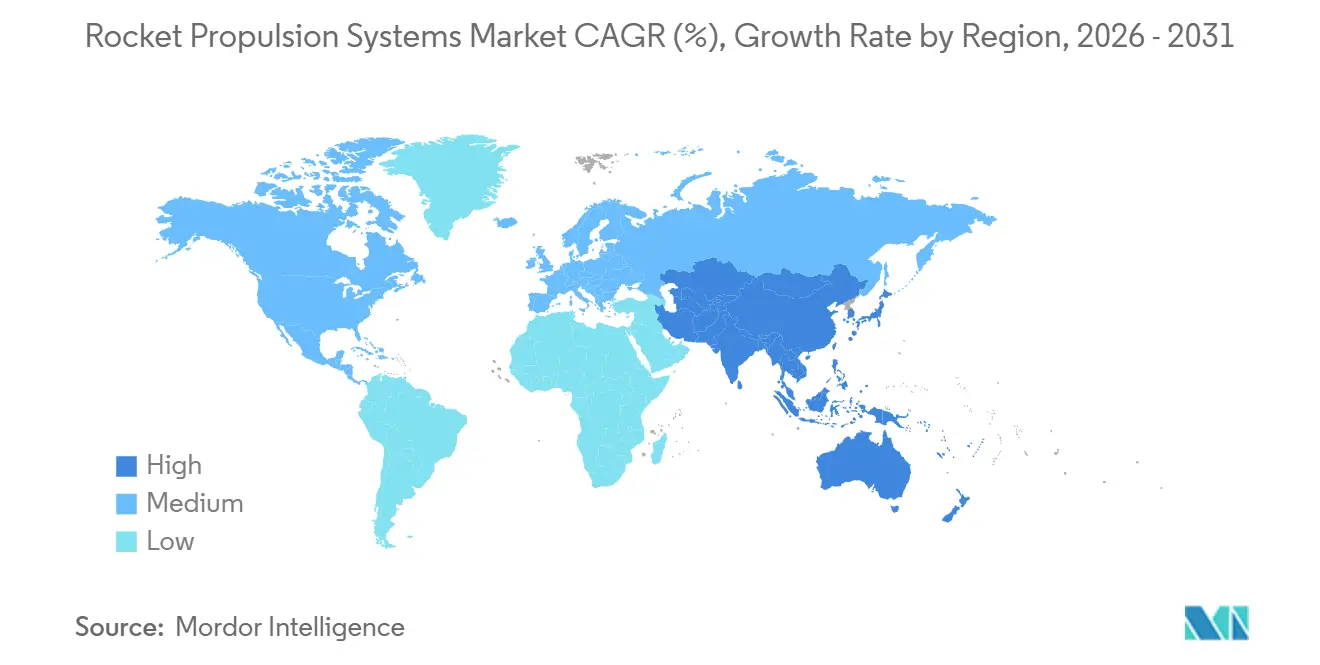

- By geography, North America held a 38.55% share in 2025, while the Asia‑Pacific is projected to grow at an 8.01% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Rocket Propulsion Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid mini-sat and mega-constellation deployment | +2.1% | Global, concentrated in North America and Asia-Pacific | Short term (≤ 2 years) |

| Reusable launch vehicle economics | +1.8% | Global, led by North America (SpaceX, Blue Origin) and Asia-Pacific (China's CAS Space) | Medium term (2-4 years) |

| Government deep-space and lunar-mission funding spike | +1.5% | North America, Europe, Asia-Pacific (India, Japan) | Medium term (2-4 years) |

| Hypersonic weapons propulsion race | +0.9% | North America, Asia-Pacific (China), Europe | Long term (≥ 4 years) |

| Additive manufacturing cost breakthroughs | +0.7% | Global, with early adoption in North America and Europe | Medium term (2-4 years) |

| Methalox and green-propellant adoption push | +0.6% | North America (SpaceX, Blue Origin), Europe (ArianeGroup), Asia-Pacific (LandSpace) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Reusable Launch Vehicle Economics: Marginal-Cost Compression Accelerates Commercial Deployment

Reusability is shifting the rocket propulsion systems market from bespoke batches to repeatable, airline‑like operations. Falcon 9’s high‑frequency cadence has proven the operational value of first‑stage recovery. At the same time, New Glenn’s first booster landing in November 2025 established a second orbital‑class reusable platform and set the stage for multi‑mission recovery cycles.[1]Blue Origin Team, “New Glenn,” Blue Origin, blueorigin.com Profitability now concentrates on sustained launch cadence, streamlined refurbishment, and vertical integration across engines, tanks, and avionics. That playbook is expanding as medium‑lift challengers prepare reusable systems to contest rideshare and dedicated constellation missions in the mid‑2026 window. The result is a structural compression of marginal cost per kilogram for commercial missions and a wider addressable market for satellite operators. These shifts reinforce a multi‑year demand cycle for reusable‑class engines and stage hardware in the rocket propulsion systems market.

Rapid Mini‑Sat and Mega‑Constellation Deployment: Launch Demand Outstrips Supply Capacity

High‑throughput constellations are moving propulsion manufacturing toward automotive‑style takt times. SpaceX conducted over 122 Falcon 9 missions in 2025 and lifted more than 3,100 Starlink satellites, which continued to scale the engine and tank production footprint into 2026. Amazon reported 212 Kuiper satellites in orbit by February 2026 and is on pace to meet mid‑2026 targets, backed by a diversified manifest across multiple launch providers.[2]Amazon Staff, “Project Kuiper satellite and rocket launch progress updates,” Amazon, aboutamazon.com OneWeb expanded its orders with Airbus by 440 satellites, locking in late‑2026 production and adding digital channelizers that increase on‑board processing complexity for propulsion-adjacent power and thermal systems. China filed with the ITU for a constellation of approximately 200,000 satellites, which would further strain engine and propellant logistics if executed at scale. Industry analysis expects non‑geostationary constellations to account for well over 95% of satcom capacity after 2026, driving higher volumes of engines, turbomachinery, and propellants across the rocket propulsion systems market.

Government Deep‑Space and Lunar‑Mission Funding Spike: Artemis and National Prestige Drive Propulsion Investment

Public budgets are underwriting heavy‑lift engines, lunar landing systems, and cislunar logistics through the decade. NASA’s FY2025 request includes USD 7.6 billion for deep‑space exploration, with major lines for the Space Launch System and the Human Landing System. At the same time, contract awards indicate sustained spending on propulsion integration and testing. Supplemental US appropriations in mid‑2025 preserved Artemis elements such as the Lunar Gateway and follow‑on SLS lots, extending the production runways for RS‑25 derivatives and upper‑stage engines into the next mission set. ESA member states committed EUR 22.3 billion (USD 26.13 billion) at the November 2025 ministerial, including EUR 2.98 billion (USD 3.49 billion) for human and robotic exploration, which sustains European engine and stage work on current and next‑generation vehicles. India’s 2026 allocation to the Department of Space supports crewed flight preparation and a next‑generation launch vehicle roadmap, signaling continued propulsion investment in Asia. These commitments lock in multi‑year test programs and production slots that flow through suppliers of turbopumps, valves, tanks, and cryogenics in the rocket propulsion systems market.

Hypersonic Weapons Propulsion Race: Strategic Competition Elevates Scramjets and Solid Rocket Motors

The transition from prototypes to early fielding is pulling hypersonic propulsion into higher‑rate production. The US Army moved its Long‑Range Hypersonic Weapon toward initial fielding after resolving integration issues, and the Navy’s Conventional Prompt Strike completed a key cold‑gas launch in May 2025 as it works toward platform deployments. Program reviews flagged schedule risk for the Air Force’s cruise missile program through 2027, yet funding and testing continued, keeping pressure on propulsion suppliers to increase throughput. In January 2026, the Pentagon invested USD 1 billion in L3Harris’ solid rocket motor business, setting up a spin‑off that targets higher output for interceptors and strike systems. Concurrent technology maturation continued as Lockheed Martin and GE Aerospace tested a rotating detonation ramjet in early 2026, aiming to extend range and improve fuel efficiency at speeds exceeding Mach 5. These shifts strengthen the link between scramjet development, solid motor capacity, and test infrastructure, sustaining demand in the rocket propulsion systems market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cryogenic-supply-chain bottlenecks | -0.8% | Global, acute in North America and Europe | Medium term (2-4 years) |

| Stringent export-control regimes (ITAR, MTCR) | -0.6% | Global, most restrictive in North America and Europe | Long term (≥ 4 years) |

| Solid propellant raw-material shortages | -0.5% | Global, affecting North America defense contractors | Short term (≤ 2 years) |

| Infrastructure limitations in emerging space nations | -0.4% | Africa, Middle East, South America (excluding Brazil) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cryogenic‑Supply‑Chain Bottlenecks: LOX and Methane Infrastructure Lags High‑Cadence Launch Schedules

High‑rate operations require resilient cryogenic sourcing, on‑site liquefaction, and stable pipeline logistics. SpaceX initiated construction of an air separation plant at Starbase in 2025 to produce liquid oxygen and nitrogen on site, a move intended to support Starship cadence while easing pressure on regional commodity markets. Orbital cryogenic management remains a technical hurdle, with standards and qualification processes still maturing for long‑duration storage and transfer in harsh thermal environments. The lack of deployed orbital depots adds complexity to refueling sequences and increases sensitivity to boil‑off and scheduling. Cold‑capable avionics and power systems for extreme lunar temperature swings also require further development and mission validation before broad adoption. These constraints can cap utilization even when engines and airframes are ready, which weighs on near‑term throughput in the rocket propulsion systems market.

Stringent Export‑Control Regimes: ITAR and MTCR Restrictions Fragment Global Propulsion Trade

Control regimes shape supplier reach, cross‑border teaming, and the addressable customer base for sensitive propulsion technologies. National security launch contracting in the United States is governed by strict export and security rules that limit foreign participation and keep critical propulsion work domestic. Certification gates for new entrants, including heavy‑lift platforms, reinforce these barriers until flight heritage and program approvals are in place. Export compliance requirements can add to document workload, increase review cycles, and impose testing constraints, stretching program timelines. As a result, sovereign propulsion development continues in markets with national launch ambitions, fragmenting standards and slowing the diffusion of technology across borders. These factors can limit how quickly new suppliers scale in the rocket propulsion systems market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Propulsion Type: Liquid Systems Dominate, Hybrid Thrives on Manned‑Mission Safety

Liquid propulsion held 63.22% of the rocket propulsion systems market share in 2025, paced by methalox engines that support rapid reuse on high‑cadence missions. SpaceX’s Raptor production has scaled to support Starship and Super Heavy testing. At the same time, Blue Origin’s BE‑4 now powers Vulcan Centaur and New Glenn operations as New Glenn advances recovery and reuse objectives. A rising share of medium‑lift and heavy‑lift platforms align around methane oxygen cycles to reduce refurbishment workload and ground turn‑times. Civil and commercial lifts across constellation deployments continue to emphasize liquid engines for their throttleability and restart capabilities, which are essential for precision orbital insertions. On the defense side, solid propulsion remains decisive where storability and magazine depth matter most. The interplay between liquid systems for commercial launches and solid motors for defense creates a balanced demand across suppliers in the rocket propulsion systems market.

Hybrid propulsion is the fastest‑growing segment at an 8.91% CAGR during 2026–2031, underpinned by safety characteristics and deep‑throttling profiles suitable for crewed and precision missions. The rocket propulsion systems market size for hybrid propulsion is projected to expand at 8.91% CAGR during 2026–2031 as programs validate designs and move toward operational deployment. Hybrid engines benefit from simplified oxidizer handling compared with bipropellant systems, which can ease pad operations and reduce ground risk. As reusability standards spread beyond the first stages, hybrids offer a path for upper‑stage maneuvering and in‑space operations where throttle range and shutdown control are critical. Suppliers are using additive manufacturing to shorten development cycles for injector heads and ports, supporting the higher cadence required by constellation support and logistics missions. These gains reinforce hybrid propulsion’s role as a complementary option alongside liquid and solid systems in the rocket propulsion systems market.

By End User: Civil and Commercial Lead, but Defense CAGR Outpaces on Hypersonic Procurement

Civil and commercial customers accounted for 58.95% of total customers in 2025, as constellation deployment dominated manifest planning and hardware volumes. SpaceX launched more than 3,100 Starlink satellites in 2025, while Amazon’s Kuiper program passed 200 satellites by February 2026 and maintained a multi‑provider launch strategy to spread risk and secure cadence. OneWeb’s new orders with Airbus extended production into late 2026 with upgraded payload processing, sustaining demand for propulsion‑adjacent structures and avionics. The rocket propulsion systems market benefits as satellite operators seek predictable pricing and frequent flights, rewarding suppliers that can support quick turns and high reliability. Commercial commitments, combined with public‑sector missions, are helping amortize engine lines and test infrastructure over larger run‑rates. This mix reduces unit costs and attracts new payload classes into orbit, reinforcing civil‑commercial leadership in the segment.

Defense and government applications are forecasted to grow at a 7.86% CAGR during 2026–2031 as hypersonic programs and interceptor inventories advance and programs transition from R&D to production. The Pentagon’s January 2026 investment in L3Harris’ motor business underscores the priority on building capacity for solid propulsion at scale. Parallel progress on hypersonic cruise propulsion and prompt-strike systems keeps demand steady for scramjets, boosters, and test-range services. Government exploration programs, including Artemis and agency science missions, further diversify defense‑heavy demand and stabilize supplier backlogs. The combined effect is a rising floor under defense‑oriented revenue within the rocket propulsion systems market.

By Component: Propellants Lead Growth as Methalox Displaces Kerosene

Motor casings held a 45.10% share in 2025, reflecting the central role of solids in air and missile defense and as strap‑on boosters for heavy‑lift vehicles. Large structural components continue to benefit from material advances and additive manufacturing that reduce mass and part count while maintaining strength. Propellants are the fastest‑growing component at a 7.62% CAGR during 2026–2031, as methane oxygen displaces RP‑1 kerosene in new launch systems and supports faster refurbishment cycles that underpin reuse. On the ground, operators are investing in air separation and cryogenic storage to smooth liquid oxygen supply, which increases local availability for frequent flight operations. These shifts reduce engine coking and cleaning workload and support quicker pad turns in the rocket propulsion systems market.

NASA and industry are working on qualification-at-speed methods for cryogenic management, helping define standards for long‑duration storage and thermal control in cislunar environments. ADN‑based monopropellants such as LMP‑103S offer a safer handling profile and a higher density‑specific impulse than legacy hydrazine, supporting their migration into operational fleets. Meanwhile, additive manufacturing is reducing cycle times for injectors, manifolds, and valve bodies, thereby tightening the coupling between component throughput and launch cadence. These factors keep propellants and associated feed systems at the center of performance and cost improvements in the rocket propulsion systems market.

By Type: Rocket Motors Anchor Defense, Rocket Engines Power Commercial Reusability

Rocket motors held 58.88% share in 2025, anchored by defense programs that prioritize storability and immediate readiness. L3Harris' solid rocket motor portfolio supports key US interceptor and strike programs, and the 2026 investment set the stage for a dedicated public company focused on this category. Northrop Grumman's propulsion portfolio spans strategic systems and large boosters, reinforcing the centrality of solid motors in deterrence and missile defense. As interceptor demand grows, suppliers are scaling capacity, qualifying new lines, and consolidating upstream materials. These actions are intended to shorten lead times and stabilize delivery for programs of record in the rocket propulsion systems market.

Rocket engines are the fastest‑growing type, with an 8.05% CAGR during 2026-2031, as liquid systems dominate commercial launch and deep‑space missions. New Glenn's entry added a second orbital‑class reusable platform and built confidence in BE‑4's path toward multi‑flight reuse. Relativity Space completed Terran R's critical design review in late 2024 and reported substantial progress on flight production and Aeon R engine testing, with a first launch targeted for late 2026. Medium‑lift competitors are targeting dedicated constellation missions with methane engines and high‑rate manufacturing methods. Combined with Starship's large payload potential, these programs keep liquid engines central to growth in the rocket propulsion systems market.

Geography Analysis

North America held a 38.55% share in 2025, anchored by SpaceX’s record annual cadence and a steady pipeline of national security launches. SpaceX launched more than 3,100 Starlink satellites in 2025 as Falcon 9 maintained high reliability and rapid turnaround times on the ground. New Glenn added capacity with a successful booster landing in November 2025, positioning Blue Origin to compete for national security launches pending certification gates. NASA’s FY2025 budget allocations for SLS and HLS reinforced multi‑year demand for heavy‑lift engines and upper stages. At the same time, the US Space Force established a five‑year outlook for dozens of missions across multiple providers. Defense investments in hypersonic propulsion capacity further tightened the regional supply chain, with a focus on motors and advanced air‑breathing systems. These pillars sustained North America’s leadership in the rocket propulsion systems market.

Asia‑Pacific is the fastest‑growing region, with an 8.01% CAGR during 2026-2031, driven by sovereign launch programs and large constellation plans. China continued to advance its Guowang constellation and filed ITU paperwork for a 200,000‑satellite system, pointing to long‑term lift and engine demand. India’s budget supports crewed flight preparation and next‑generation launch vehicles, including line items for crewed mission milestones and advanced engine development in FY2026. Regional momentum is reinforced by growing participation in multinational exploration programs and a pipeline of civil missions. These trends expand the supplier base and accelerate the adoption of standards in the rocket propulsion systems market.

Europe increased its commitments but continues to face headwinds on cost competitiveness against reusable US systems. ESA member states pledged EUR 22.3 billion (USD 26.13 billion) at the 2025 ministerial, including EUR 4.44 billion (USD 5.20 billion) for space transportation, a signal of sustained support for engine and stage development.[3]ESA Communications, “ESA Member States commit to largest contributions at Ministerial,” European Space Agency, esa.int Industrial programs include next‑generation methane engines and reusability concepts intended to close the cost gap with established reusable vehicles. The Middle East and Africa remain at an earlier stage, with investments focused on broader space infrastructure and international partnerships. South America’s activity is limited, with research programs and test facilities progressing, but with fewer near‑term launch slots. Overall, Europe’s resilience and new engine workstreams help stabilize regional demand within the rocket propulsion systems market.

Competitive Landscape

Competition is divided between vertically integrated commercial launch providers and defense primes focused on solid propulsion and advanced air-breathing systems. SpaceX continues to lead commercial cadence and progress Starship test campaigns reliant on high-rate Raptor production. Blue Origin advanced with New Glenn's orbital launch operations and a successful booster landing, positioning the company for future national security launch competition. US Space Force Phase 3 awards to multiple providers set a competitive baseline for integration, pricing discipline, and reliability. These dynamics frame a durable rivalry between the heavy-lift and medium-lift segments of the rocket propulsion systems market.

Defense propulsion remains concentrated among established primes. L3Harris received significant investment to spin off its Missile Solutions business, which produces solid rocket motors for major US programs, with the new entity expected to scale output and revenue. Northrop Grumman's propulsion portfolio spans strategic systems and large boosters, sustaining long-term positions on critical defense platforms. Technology maturation continued as Lockheed Martin and GE Aerospace tested a rotating detonation ramjet concept for hypersonic applications. These moves underscore the defense sector's commitment to propulsion innovation and capacity in the rocket propulsion systems market.

A cohort of new entrants is targeting mid-lift and heavy-lift opportunities with methane engines and additive manufacturing at the core. Relativity Space completed Terran R CDR and has begun flight-intent production, with launch timing guided by engine test results and integration progress. Suppliers are also pursuing advanced manufacturing to compress design-to-test timelines, resulting in significant reductions in propulsion component lead times in some defense use cases. This wave of capability aims to balance capacity with cost and respond to constellation demand that rewards reliability and frequency in the rocket propulsion systems market.

Rocket Propulsion Systems Industry Leaders

L3Harris Technologies, Inc.

Northrop Grumman Corporation

Antrix Corporation Limited

Mitsubishi Heavy Industries, Ltd.

Safran S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: The US Army awarded a USD 65 million contract to L3Harris Technologies, Inc., to produce rocket motors for the Army Tactical Missile System (ATACMS).

- December 2025: L3Harris Technologies, Inc. received a letter of intent for a commercial contract to produce 60 Zeus hypersonic motors for Kratos Defense & Security Solutions. This contract is expected to increase L3Harris' annual production rate of Zeus motors by over 50%, following Kratos' successful development and flight testing of the Zeus 1 and Zeus 2 motors.

- August 2025: Anduril inaugurated a solid rocket motor plant in Mississippi, becoming the third major US supplier and expanding domestic capacity for defense programs.

Global Rocket Propulsion Systems Market Report Scope

Rocket propulsion is a critical subsystem that propels a rocket from the ground into the atmosphere. This study delves into the various rocket propulsion systems that are crucial to space launch vehicles.

The rocket propulsion systems market is segmented by propulsion type, end user, component, type, and geography. Based on propulsion type, the market is segmented into solid, liquid, and hybrid. By end user, the market is segmented into civil and commercial, and military and government. By component, the market is segmented into motor casing, nozzle, propellant, and other components. By type, the market is segmented into rocket motor and rocket engine. The report also covers the market sizes and forecasts for the rocket propulsion systems market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Solid |

| Liquid |

| Hybrid |

| Civil and Commercial |

| Military and Government |

| Motor Casing |

| Nozzle |

| Propellant |

| Other Components |

| Rocket Motor |

| Rocket Engine |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Propulsion Type | Solid | ||

| Liquid | |||

| Hybrid | |||

| By End User | Civil and Commercial | ||

| Military and Government | |||

| By Component | Motor Casing | ||

| Nozzle | |||

| Propellant | |||

| Other Components | |||

| By Type | Rocket Motor | ||

| Rocket Engine | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected growth for the rocket propulsion systems market to 2031?

The rocket propulsion systems market size is expected to grow from USD 6.99 billion in 2025 to USD 7.48 billion in 2026 and is forecasted to reach USD 10.37 billion by 2031 at a 6.76% CAGR over 2026-2031.

Which propulsion type leads in share and which is growing fastest?

Liquid propulsion led with 63.22% share in 2025, while hybrid propulsion records the fastest growth at an 8.91% CAGR during 2026–2031.

Which customer segment is expanding most quickly through 2031?

Military and government is the fastest‑growing end user at a 7.86% CAGR during 2026–2031, while civil and commercial held 58.95% share in 2025.

Which region is expected to grow the fastest?

Asia‑Pacific is projected to post an 8.01% CAGR during 2026–2031, supported by large sovereign constellations and crewed‑flight programs.

How are reusable vehicles influencing industry costs and cadence?

Booster recovery and rapid refurbishment are compressing marginal costs and enabling higher launch frequency, which expands addressable demand and underpins volume manufacturing.

What role does additive manufacturing play in propulsion programs today?

Additive manufacturing cuts production time and cost for critical engine components, enabling faster design‑to‑hot‑fire cycles and supporting higher launch cadence.

Page last updated on: