Rocket And Missiles Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 67.76 Billion |

| Market Size (2030) | USD 87.70 Billion |

| Growth Rate (2025 - 2030) | 5.29% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Rocket And Missiles Market Analysis by Mordor Intelligence

The rocket and missiles market size reached USD 67.76 billion in 2025 and is forecasted to attain USD 87.7 billion by 2030, advancing at a 5.29% CAGR. Rising defense budgets, shifting doctrines that favor long-range precision fires, and accelerating hypersonic programs form the core demand drivers for the rocket and missiles market. Heightened geopolitical friction in Eastern Europe, the Indo-Pacific, and the Middle East forces governments to redirect funds toward integrated air-and-missile defense ecosystems. Liquid-propellant designs remain widespread, yet scramjet and other advanced propulsion concepts are gaining traction as militaries seek greater speed, maneuverability, and survivability. Persistent raw-material supply risks and stringent export-control regimes temper growth but have also spurred nations to localize production and diversify suppliers.

Key Report Takeaways

- By product type, ballistic missiles led with 39.57% revenue share in 2024, while hypersonic glide vehicles are forecasted to expand at a 6.98% CAGR through 2030.

- By propulsion type, liquid systems accounted for 41.47% of the 2024 base, yet scramjet designs are projected to post the fastest 7.48% CAGR.

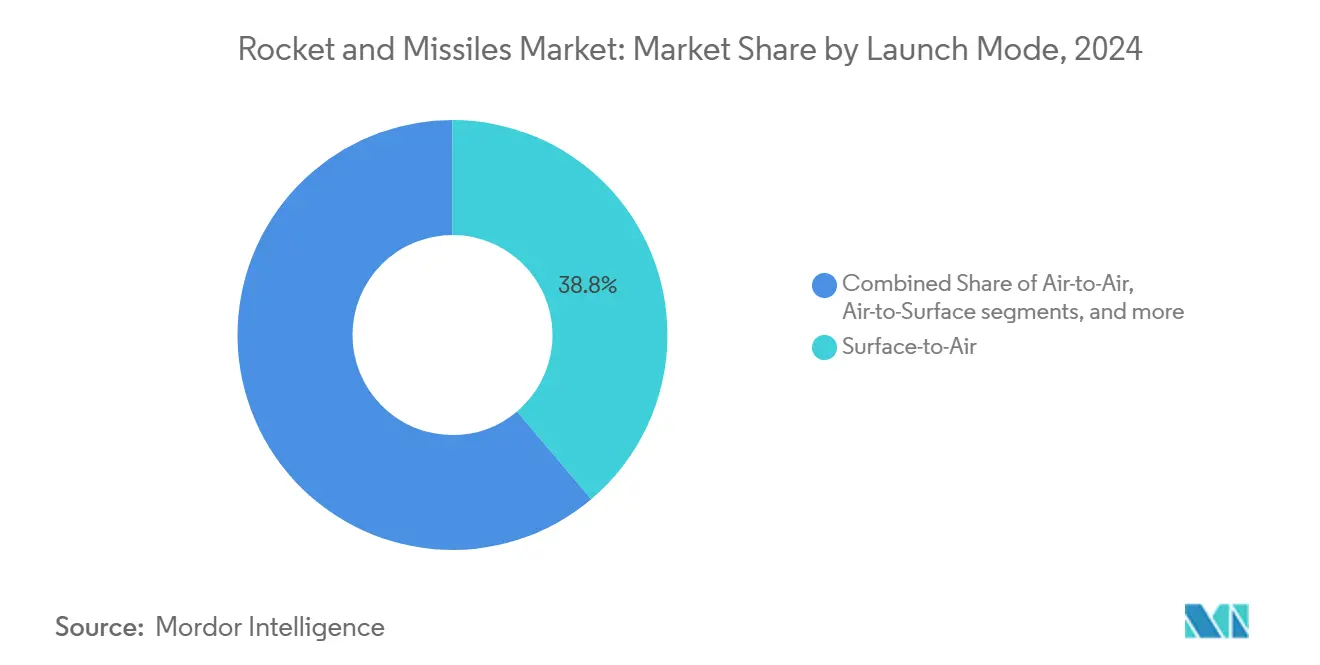

- By launch mode, surface-to-air platforms captured 38.84% of 2024 spending; air-to-air missiles show the highest 7.18% CAGR outlook.

- By guidance mechanism, guided weapons held a 58.49% share in 2024, whereas unguided rockets are slated to grow at a 6.28% CAGR.

- By product type, ballistic missiles led with 39.57% revenue share in 2024, while hypersonic glide vehicles are forecast to expand at a 6.98% CAGR through 2030.

Global Rocket And Missiles Market Trends and Insights

Drivers Impact Analysis*

| Driver | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating geopolitical tensions and defense modernization | +1.80% | Eastern Europe, Indo-Pacific, Middle East | Medium term (2-4 years) |

| Growing demand for precision-guided munitions (PGMs) | +1.50% | North America, Europe, Asia-Pacific | Long term (≥4 years) |

| Emergence of hypersonic missile R&D funding | +1.20% | United States, China, Russia | Long term (≥4 years) |

| Low-cost small-sat launch platforms demand | +0.80% | North America, Europe | Medium term (2-4 years) |

| AI-enabled guidance and swarm tactics adoption | +1.00% | Advanced military powers | Medium term (2-4 years) |

| Missile-defense race spurring offensive investments | +0.90% | Globally contested regions | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Escalating Geopolitical Tensions and Defense Modernization

Rising interstate rivalry is prompting capability-centric, rather than platform-centric, procurement. Germany’s EUR 100 billion (USD 117.57 billion) modernization fund exemplifies how European budgets now prioritize missile stockpiles and new ammunition lines.[1]Alisa Laufer, Howard J. Shatz, and Omar Danaf, “Implications of Russia’s War on Ukraine for the U.S. and Allied Defense Industrial Bases,” RAND Corporation, rand.org Similar GDP-linked funding proposals in Brazil illustrate the global reach of this trend. Modern operational concepts observed in Ukraine emphasize that sufficient inventories of precision rockets, not tank counts, decide battlefield endurance. The rocket and missiles market gains predictable funding streams as governments embed 3.5% of GDP defense targets. Medium-term impacts materialize through multi-year contracts that shield suppliers from annual budget uncertainty.

Growing Demand for PGMs

US multi-year procurement of anti-ship and long-range missiles illustrates how stockpile consumption rates in high-intensity conflicts outstrip peacetime planning.[2]Stacie Pettyjohn and Hannah Dennis, “Production Is Deterrence,” Center for a New American Security, cnas.org Precision engagement minimizes collateral damage, an imperative in urbanized theaters. In recent conflicts, systems like HIMARS and ATACMS delivered operational overmatch, igniting parallel acquisition programs across NATO and Indo-Pacific allies. Industrial-based expansion funds now target fuse, seeker, and warhead capacity to avert future bottlenecks. Long-term effects include wider adoption of ordinary missile families that simplify training and sustainment.

Emergence of Hypersonic Missile R&D Funding

Washington’s USD 1 billion award to Lockheed Martin and USD 670 million to Dynetics for hypersonic prototypes underscores the race to field Mach 5-plus systems. Comparable initiatives in China and Russia elevate global spending, while Japan’s new indigenous program shows rapid technology diffusion. Hypersonic glide vehicles compress strategic decision timelines and bypass many current missile-defense layers, creating parallel demand for detection and interception solutions. These projects fuel specialized propulsion, thermal-protection, and sensor markets over the long term.

Low-Cost Small-Satellite Launch Platforms Demand

Proliferated LEO constellations require responsive launchers capable of frequent sorties at marginal cost. Shared industrial processes with tactical rockets reduce unit prices and provide surge capacity for defense customers. North American and European agencies use venture-class launch contracts to nurture startups, a strategy that filters innovations into military programs. Medium-term spillovers include simplified modular avionics and lightweight composite structures.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Export controls and arms-treaty limitations | −0.7% | Global, particularly among technology-sharing allies | Long term (≥ 4 years) |

| Propellant raw-material price volatility | −0.5% | Regions dependent on imported energetic materials | Short term (≤ 2 years) |

| Cyber-security certification delays | −0.6% | United States, Europe, and allied Asia-Pacific nations | Medium term (2-4 years) |

| Budget shift toward cyber and unmanned systems | −0.4% | Advanced military powers worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Export Controls and Arms-Treaty Limitations

Revised US ITAR rules retain stringent coverage of Category IV missile technologies, slow multinational development cycles by as much as 18 months, and elevate compliance costs for midsize contractors.[3]U.S. Department of State, “International Traffic in Arms Regulations: Changes to Category IV,” state.gov Missile Technology Control Regime thresholds on range and payload further compel specific buyers to bankroll costly indigenous programs when import licenses are denied. The extra legal reviews, re-export approvals, and end-user verifications lengthen contract negotiations and can trigger schedule penalties written into performance clauses. Over time, this regulatory friction fragments the global supply base, curbs technology diffusion even among close allies, and trims projected CAGR gains for the rocket and missiles market.

Propellant Raw-Material Price Volatility

Key energetic ingredients such as ammonium perchlorate come from a handful of qualified suppliers, so geopolitical shocks or factory outages quickly ripple through program budgets.[4]U.S. Department of Defense, “Industrial Base Report on Solid Rocket Motors,” defense.gov The 2024 industrial-base review showed raw materials can equal 25% of a missile’s total build cost, meaning a single-digit price swing erodes already thin margins on fixed-price contracts. Short-term volatility forces program managers to rephase production lots or seek incremental funding, delaying deliveries of low-margin tactical rounds. Mitigation measures like Defense Production Act grants and strategic stockpiles help. Yet, supplier consolidation keeps systemic risk elevated and can prompt governments to underwrite new entrants or expand public-sector production lines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Hypersonic Systems Drive Innovation

Ballistic missiles held a 39.57% rocket and missiles market share in 2024. Hypersonic glide vehicles, though nascent, are projected to post a 6.98% CAGR, the highest within the product taxonomy. This momentum stems from the strategic premium placed on time-critical strike options that can penetrate layered defenses. Tactical rockets such as HIMARS maintain relevance for cost-effective area saturation, while cruise missiles evolve with AI-assisted seekers for sea-skimming routes.

R&D pipelines reveal a pivot toward multi-role weapons that combine speed, maneuverability, and precision. Nations adopting GDP-linked defense budgets channel funds into strategic deterrence and rapid-response arsenals. Demonstrations of China’s DF-27 and the US Army’s Precision Strike Missile signal broader future deployments. Therefore, the rocket and missiles market balances legacy ballistic inventories with surging hypersonic demand.

By Propulsion Type: Scramjet Technology Leads Innovation

Liquid engines accounted for 41.47% of 2024 revenue, underpinning most strategic systems within the rocket and missile market. Scramjet prototypes, however, are forecasted to expand at a 7.48% CAGR as hypersonic ambitions mature. Solid motors retain tactical dominance due to storage stability and rapid launch readiness, while hybrids offer throttling flexibility critical for responsive space access.

The propulsion supply chain faces dual pressures: meeting higher temperature tolerances for scramjets and alleviating single-supplier exposure in solid energetics. Joint government-industry initiatives fund new foundries and advanced additive-manufacturing lines. Success in these areas unlocks next-generation warfighting concepts that hinge on extended range and reduced flight time.

By Launch Mode: Air-to-Air Applications Expand Rapidly

Surface-to-air batteries captured 38.84% of 2024 spending, reflecting renewed emphasis on homeland and forward-base defense. Air-to-air weapons, bolstered by fifth-generation fighter programs, are projected to rise at a 7.18% CAGR. Beyond-visual-range interceptors such as AIM-260 merge networked targeting with low-observable carriage, enhancing first-shot probabilities.

Multi-domain doctrines drive integrated launch solutions that blur historical platform lines. Naval vertical-launch systems now deploy traditionally land-based interceptors, and rotary-wing aircraft field precision rockets adapted from ground variants. This interoperability enlarges addressable volumes for the rocket and missiles market.

By Guidance Mechanism: Autonomous Systems Gain Traction

Guided weapons dominated with a 58.49% share in 2024, yet unguided munitions still attract interest for cost-sensitive suppression roles and are expected to grow at a 6.28% CAGR. GPS-denied navigation, multi-mode seekers, and onboard AI transform missiles into adaptive, all-weather tools. At the same time, modern fire-control systems elevate the accuracy of formerly unguided artillery rockets.

Cyber-hardened datalinks and encrypted software updates extend life-cycle relevance amid electronic warfare (EW) threats. Autonomy also promises lower operator workloads and reduced engagement timelines, reinforcing the premium positioning of advanced guidance within the rocket and missile market.

Geography Analysis

North America represented 40.65% of 2024 expenditures, buoyed by sustained hypersonic, missile defense, and PGM programs funded through the FY-2025 budget. Multi-year block buys stabilize production lines at prime contractors and their Tier-2 suppliers. Canada’s investment in NORAD modernization and Mexico’s aerospace cluster expansion further anchor regional demand.

Asia-Pacific is forecasted to record a 5.98% CAGR, the fastest across regions, as China, India, Japan, South Korea, and Australia bolster inventories. Indigenous R&D—exemplified by India’s Akash and Japan’s scramjet demonstrator—reduces import reliance and seeds local industrial bases. US-aligned nations additionally procure interoperable systems to close capability gaps, reinforcing the rocket and missiles market across the Indo-Pacific.

Europe’s spending uptick follows the NATO pledge to allocate at least 2% of GDP to defense, with several members now targeting 3.5%. Germany’s special modernization fund and France-Italy joint missile projects illustrate cooperative approaches that share development costs and widen export prospects. Ongoing efforts to standardize munitions calibers and data links promise long-term efficiencies.

Competitive Landscape

The rocket and missile market is moderately concentrated, with Lockheed Martin Corporation, RTX Corporation, and Northrop Grumman Corporation securing most top-line contracts through legacy relationships and classified capabilities. Multi-year awards for hypersonic prototypes and missile-defense interceptors sustain double-digit order backlogs. Emerging entrants such as Anduril leverage software-defined payloads and additive manufacturing to compress development cycles, challenging incumbents in select niches.

Incumbents respond by adopting digital thread methodologies and partnering with cloud and AI specialists to reduce design iterations. Vertical integration strategies—especially around solid-motor capacity—seek to mitigate supplier risk after recent shortages. Cross-border mergers, like proposed investments in Brazil’s Avibras, illustrate how capital inflows from Gulf and Australian entities diversify global footprints.

New production runs for low-cost precision rockets attract private-equity funding that traditionally avoided defense. Meanwhile, governments tighten security-clearance prerequisites, creating a barrier that helps established primes and incentivizes consortium models for smaller innovators. Overall, sustained R&D outlays and the race to field hypersonic and autonomous systems uphold a dynamic yet concentrated competitive field.

Rocket And Missiles Industry Leaders

Lockheed Martin Corporation

RTX Corporation

Northrop Grumman Corporation

The Boeing Company

MBDA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: L3Harris Technologies secured a USD 292 million contract to continue manufacturing propulsion systems for the Javelin weapon system. The five-year production extension represents the largest propulsion production contract in the Javelin program's history.

- July 2025: The Brazilian Navy and SIATT signed an agreement to co-develop the MANAER air-launched and an accompanying surface-to-air anti-ship missile based on MANSUP technology.

- January 2025: Avibras and Saudi-based Black Storm Military Industries entered advanced investment talks to revive the MTC-300 tactical cruise missile line while retaining Brazilian manufacturing.

Global Rocket And Missiles Market Report Scope

| Strategic Missiles |

| Tactical Missiles |

| Cruise Missiles |

| Ballistic Missiles |

| Rockets (Artillery) |

| Hypersonic Glide Vehicles |

| Solid Propellant |

| Liquid Propellant |

| Hybrid Propellant |

| Ramjet |

| Scramjet |

| Turbojet |

| Surface-to-Surface |

| Surface-to-Air |

| Air-to-Surface |

| Air-to-Air |

| Subsea-to-Surface |

| Guided |

| Unguided |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Product Type | Strategic Missiles | ||

| Tactical Missiles | |||

| Cruise Missiles | |||

| Ballistic Missiles | |||

| Rockets (Artillery) | |||

| Hypersonic Glide Vehicles | |||

| By Propulsion Type | Solid Propellant | ||

| Liquid Propellant | |||

| Hybrid Propellant | |||

| Ramjet | |||

| Scramjet | |||

| Turbojet | |||

| By Launch Mode | Surface-to-Surface | ||

| Surface-to-Air | |||

| Air-to-Surface | |||

| Air-to-Air | |||

| Subsea-to-Surface | |||

| By Guidance Mechanism | Guided | ||

| Unguided | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Singapore | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the rocket and missiles market in 2025?

The rocket and missiles market size reached USD 67.76 billion in 2025 and is forecasted to attain USD 87.7 billion by 2030, advancing at a 5.29% CAGR.

Which region grows fastest for rocket and missile programs?

Asia-Pacific posts the quickest 5.98% CAGR due to heightened security tensions and indigenous R&D.

What segment sees the highest growth?

Hypersonic glide vehicles lead with a 6.98% CAGR between 2025-2030.

Who are the major vendors?

Lockheed Martin Corporation, RTX Corporation, Northrop Grumman Corporation, and emerging firms such as Anduril dominate contract awards.

Which propulsion technology is gaining momentum?

Scramjet engines record the highest 7.48% CAGR as hypersonic projects move toward prototyping.

How do export controls influence procurement?

ITAR and MTCR rules delay delivery schedules and encourage domestic development, slightly dampening future growth.

Page last updated on: