Soil Monitoring Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

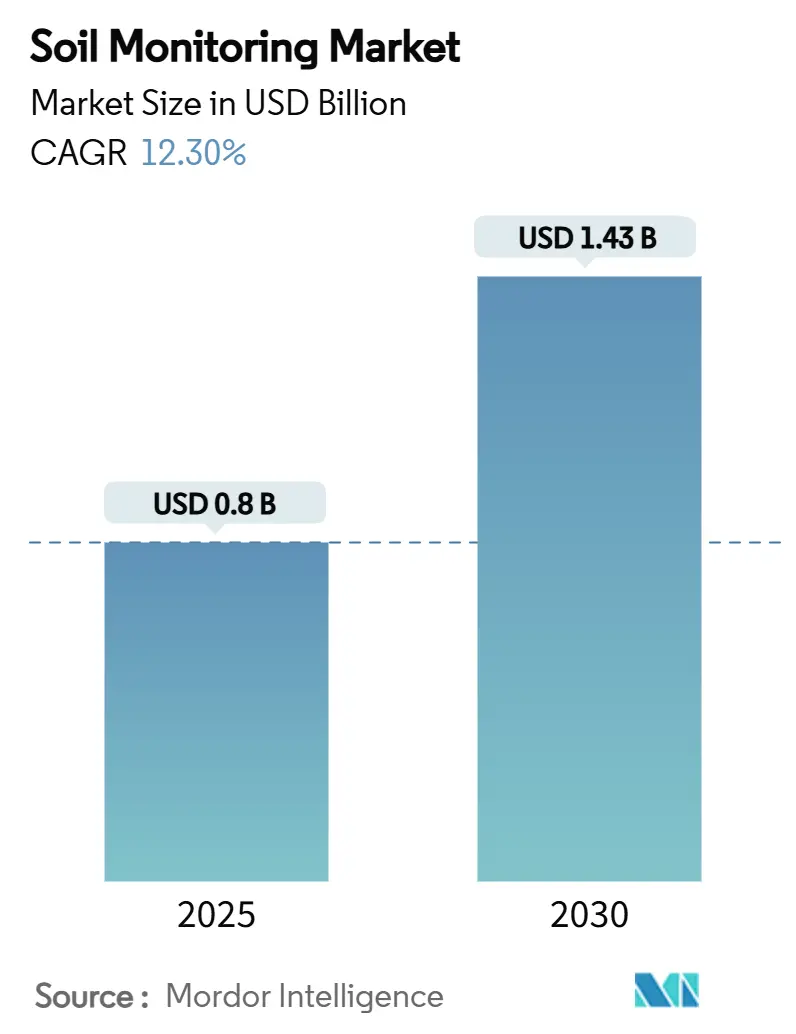

| Market Size (2025) | USD 0.8 Billion |

| Market Size (2030) | USD 1.43 Billion |

| Growth Rate (2025 - 2030) | 12.30% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Soil Monitoring Market Analysis by Mordor Intelligence

The soil monitoring market size reached USD 0.80 billion in 2025 and is projected to grow to USD 1.43 billion by 2030, at a CAGR of 12.30%. The market growth is driven by increasing climate variability, stricter water regulations, and broader adoption of precision agriculture practices. Hardware components constitute the largest market segment, while analytics services show significant growth potential. The expansion of wireless and satellite IoT networks improves connectivity in agricultural regions, and continuous venture capital funding supports innovations in sensor technology, edge computing, and AI applications. North America maintains market leadership, with the Asia-Pacific region projected to experience the highest growth rate due to supportive agricultural policies and digital transformation initiatives.

Key Report Takeaways

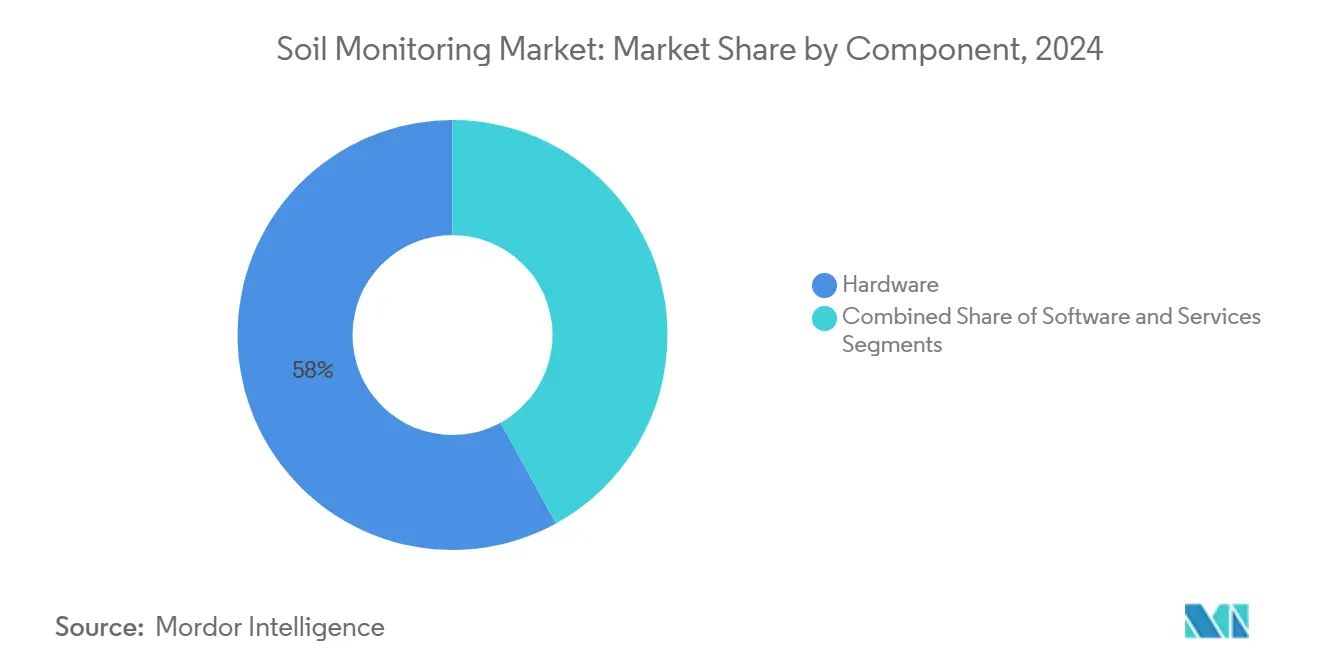

- By component, hardware led with 58% of the soil monitoring market share in 2024, whereas services are projected to expand at a 16.30% CAGR through 2030.

- By product type, in-situ sensors accounted for 46% of the soil monitoring market size in 2024, while remote-sensing platforms are on track for an 18.10% CAGR to 2030.

- By connectivity technology, wireless solutions held 70% of revenue in 2024, and it is forecast to grow at a 19.80% CAGR.

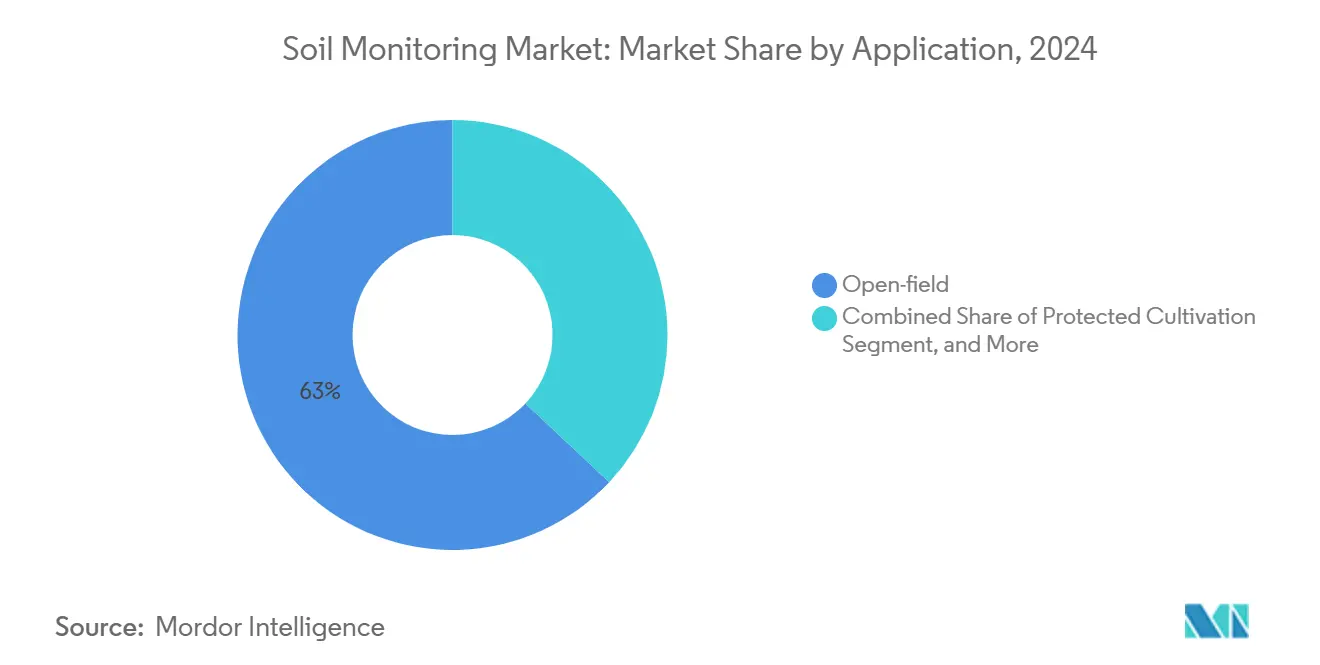

- By application, open field application commanded 63% of spending in 2024, and protected cultivation is projected to post a 14.20% CAGR.

- By end user, large commercial farms captured a 42% share of the soil monitoring market in 2024, whereas research institutes are projected to grow at a 14.60% CAGR.

- By geography, North America led with a 31% revenue share in 2024, and the Asia-Pacific region is advancing at a 14.20% CAGR through 2030.

- Major players in the market include METER Group, Stevens Water Monitoring Systems, and Sentek Technologies.

Global Soil Monitoring Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-driven precision agriculture adoption | +3.2% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Climate-linked crop-insurance prerequisites | +2.1% | North America, Europe, and emerging in Asia-Pacific | Long term (≥4 years) |

| Integration with farm management software suites | +1.8% | Global, concentrated in developed markets | Short term (≤2 years) |

| Subsidies for water-use-efficient irrigation | +2.4% | Asia-Pacific, Middle East, and selective uptake in Africa | Medium term (2-4 years) |

| Below-ground IoT network standardization | +1.5% | North America and Europe lead | Long term (≥4 years) |

| Venture funding for soil-health analytics platforms | +1.7% | North America, Europe, and growing in Asia-Pacific | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Data-driven Precision Agriculture Adoption

Government initiatives, such as the United States Department of Agriculture (USDA)'s USD 3.1 billion climate-smart program in 2022, have established real-time soil data monitoring as an essential farming requirement.[1]United States Department of Agriculture, “Manager’s Report 2025 Crop Year,” usda.gov Farmers implementing sensor networks with machine-learning analytics have achieved water savings of up to 30% and reduced fertilizer usage by 40%, resulting in improved profit margins. Current platforms combine hyperspectral imaging with field sensors to map organic-carbon and moisture levels with accuracy rates of 90% or higher. On-site edge processing has reduced data latency, enabling automated irrigation systems to respond within minutes. The integration of continuous soil monitoring data supports Agriculture 5.0 applications, including digital twins and robotic systems, establishing soil monitoring systems as fundamental agricultural infrastructure.

Climate-linked Crop Insurance Prerequisites

Insurers are embedding sensor-verified soil metrics into actuarial models, offering premium discounts once devices are installed. Early European pilots recorded 15–20% fewer claims after farms adopted end-to-end monitoring. Satellite-based moisture layers streamline loss verification, cutting administrative overhead. Joint ventures between carriers and sensor firms bundle hardware with coverage, boosting adoption and analytics revenue. These integrations enable dynamic risk profiling, informing seasonal policy adjustments and subsidies. In India, the National Mission for Sustainable Agriculture (NMSA) and Soil Health Management (SHM) guidelines support insurance-linked soil data through standardized testing and nutrient mapping.[2]Ministry of Agriculture & Farmers Welfare, “Soil Health Management Guidelines,” agricoop.nic.in

Integration with Farm Management Software Suites

The Agricultural Industry Electronics Foundation has formalized wireless in-field communication standards, dismantling long-standing data silos. Adoption of the OGC (Open Geospatial Consortium) SensorThings protocol enables seamless data flow between soil probes, weather stations, and machinery. Cloud platforms apply machine learning to deliver yield-prediction accuracy of 85% when continuous soil metrics are included. Farmers retain data ownership through permissioned platforms, while aggregated regional datasets unlock benchmarking insights for input suppliers.[3]Source: United Nations World Data Forum, “Farmer-Centric Data Governance Models,” unstats.un.org

Subsidies for Water-use-efficient Irrigation

India’s Pradhan Mantri Kisan Urja Suraksha evam Utthan Mahabhiyan (PM-KUSUM) program funds up to 60% of the capital cost of solar pumps bundled with soil sensors, lowering payback periods for smallholders. Australia’s On-Farm Connectivity Grant reimburses digital agribusiness purchases, including soil probes, to reduce drought risk. In Europe, the Common Agricultural Policy devotes EUR 386.6 billion (USD 425.3 billion) to 2027, with eco-schemes that reward verifiable soil-health monitoring. Subsidies tied to measurable conservation outcomes strengthen steady demand for soil monitoring market solutions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented ownership of smallholder farms | −1.8% | Asia-Pacific, Africa, and pockets of South America | Long term (≥4 years) |

| Sensor fouling and calibration drift in saline soils | −1.2% | Global, concentrated in arid and coastal zones | Medium term (2-4 years) |

| Limited cellular/LPWAN coverage in rural areas | −1.5% | Global, acute in developing regions | Medium term (2-4 years) |

| Uncertain ROI for low-value row crops | −0.9% | Global, higher in commodity-centric areas | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Fragmented Ownership of Smallholder Farms

Small farm sizes below 5 hectares in Asia and Africa increase the per-hectare cost of sensors, resulting in payback periods exceeding five years for staple crops. While cooperative models like Brazil's Connected Farm enable shared IoT infrastructure across multiple farms, barriers in digital literacy and cultural adoption remain. Sensor manufacturers now offer basic, lower-priced models, though their limited capabilities affect user trust. In response to scale challenges, pilot initiatives in India and Kenya are testing seasonal sensor rental programs. Non-governmental organizations are providing subsidies for sensor deployment to support climate resilience projects, making the technology more accessible to small-scale farmers.

Limited Cellular/LPWAN Coverage in Rural Areas

Limited cellular coverage and insufficient Low Power Wide Area Network (LPWAN) gateway infrastructure restrict many farms to periodic data uploads, which delays critical decision-making. While satellite IoT addresses coverage gaps, its operational costs remain prohibitive for small-scale users. Edge computing and hybrid connectivity solutions offer partial remedies, but standardized roaming protocols are incomplete. To improve connectivity, certain agricultural technology companies are testing solar-powered mesh networks that enable neighboring farms to serve as data relay points. Government initiatives, including rural connectivity funding and spectrum policy reforms, aim to enhance last-mile infrastructure. However, the absence of unified agricultural IoT device standards continues to impede large-scale implementation due to interoperability challenges.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Hardware Dominance Drives Infrastructure Investment

Hardware components accounted for 58% of the soil monitoring market size in 2024, driven by farms expanding their sensor probe networks and communication gateway installations. The decreasing sensor prices and extended battery life, which now reaches 10 years for certain wireless probes, have reduced initial investment concerns. Large enterprises continue to show strong adoption rates, considering in-ground instrumentation essential for autonomous machinery operations. The services component is growing at a 16.30% CAGR as farmers require professional analysis of soil data. Subscription-based dashboards that convert sensor readings into fertigation schedules are replacing traditional software licensing models.

This transition to services increases recurring revenue predictability and expands market reach to customers without internal analytics capabilities. Vendors are establishing partnerships with agronomists and farm consultants to integrate advisory services with sensor subscriptions, strengthening customer relationships. The market offers additional revenue streams through supplementary features for pest prediction, carbon tracking, and yield optimization, all utilizing soil data. The integration of hardware, data analysis, and agricultural expertise has established soil monitoring as a core component of digital farming operations.

By Product Type: In-situ Sensors Lead Despite Remote-sensing Surge

In-situ probes captured 46% of the soil monitoring market size in 2024, driven by their ability to measure moisture, temperature, and salinity directly at root depth. The soil monitoring market for in-situ devices is anticipated to grow steadily, supported by integration with variable-rate irrigation valves. Remote-sensing platforms, though representing a smaller market share, are growing at an 18.10% CAGR as hyperspectral satellites and Unmanned Aerial Vehicles (UAVs) enable large-scale soil mapping. The combination of point sensors with imagery provides both spatial context and temporal continuity, improving decision-making accuracy.

Portable test kits maintain popularity among agricultural consultants who require quick diagnostic assessments across multiple fields. However, despite their economic appeal to small-scale farmers, these kits face limitations due to accuracy compromises and labor-intensive operations. Calibration variations across different soil types create reliability issues for portable kits in areas with diverse subsurface conditions. Research efforts are focusing on developing universal calibration standards to integrate mobile tools effectively into enterprise-level monitoring systems.

By Connectivity Technology: Wireless Networks Enable Scalable Deployment

Wireless links accounted for 70% of the soil monitoring market share in 2024, driven by LPWAN (Low Power Wide Area Network), cellular NB-IoT, and proprietary sub-GHz solutions that provide extensive coverage without trenching costs. Long Range Wide Area Network (LoRaWAN)'s increasing adoption stems from its energy efficiency and open ecosystem standards, making it the primary choice for mid-range backhaul in row-crop farming. The wireless segment also represents the fastest-growing segment with a 19.80% CAGR, particularly in Australia and South America, where remote agricultural areas extend beyond terrestrial network coverage.

Wired connectivity market share has decreased, remaining relevant primarily in specialized greenhouses where consistent bandwidth and power supply justify Ethernet infrastructure. Edge computing nodes process sensor data on-site, enabling real-time alerts during network interruptions. Systems now incorporate predictive buffering to preserve and transmit essential data after connectivity restoration. Multi-band gateways combining terrestrial and satellite connections provide enhanced network reliability for farms in remote locations.

By Application: Open-field Leads with Protected Cultivation Gaining Momentum

Open-field agriculture accounted for 63% of total revenue in 2024, driven by increased adoption of precision irrigation, fertigation, and carbon-credit verification systems. Protected cultivation recorded the highest growth rate at 14.20% CAGR, supported by climate-resilient farming practices and controlled-environment agriculture. Growers in protected systems utilize real-time soil and substrate moisture monitoring to optimize closed-loop irrigation systems, improving fruit quality and reducing resource waste.

The market expansion extends to forestry management, where deep-profile sensors help monitor nutrient cycles and assess wildfire risks. The integration of agricultural and environmental monitoring creates operational efficiencies through unified data collection. Manufacturers are responding by developing adaptable platforms that support both agricultural and environmental applications. The improved data accessibility enables stakeholders to use soil information for multiple purposes, including ecosystem restoration and yield forecasting. The protected cultivation segment continues to attract investment in vertical farming and urban agriculture projects, contributing to its market growth.

By End User: Commercial Farms Drive Adoption While Research Institutions Accelerate Innovation

Large commercial farms account for 42% of spending in 2024. These enterprises typically deploy hundreds of probes per site, benefiting from economies of scale and supporting dedicated data science teams. The soil monitoring market in research institutes is growing at 14.60% CAGR, driven by universities conducting controlled trials to study cultivar responses to micro-zone soil variations.

Government initiatives provide shared sensor infrastructure to cooperatives, demonstrating the technology's effectiveness for smallholder farmers. However, fragmented land ownership and capital constraints limit adoption in developing regions, highlighting the importance of consolidated service models. Cooperatives are implementing data-sharing agreements that enable individual farmers to compare their results against collective soil health benchmarks. Mobile analytics dashboards have become essential tools, converting sensor data into practical recommendations for farmers with basic technical knowledge.

Geography Analysis

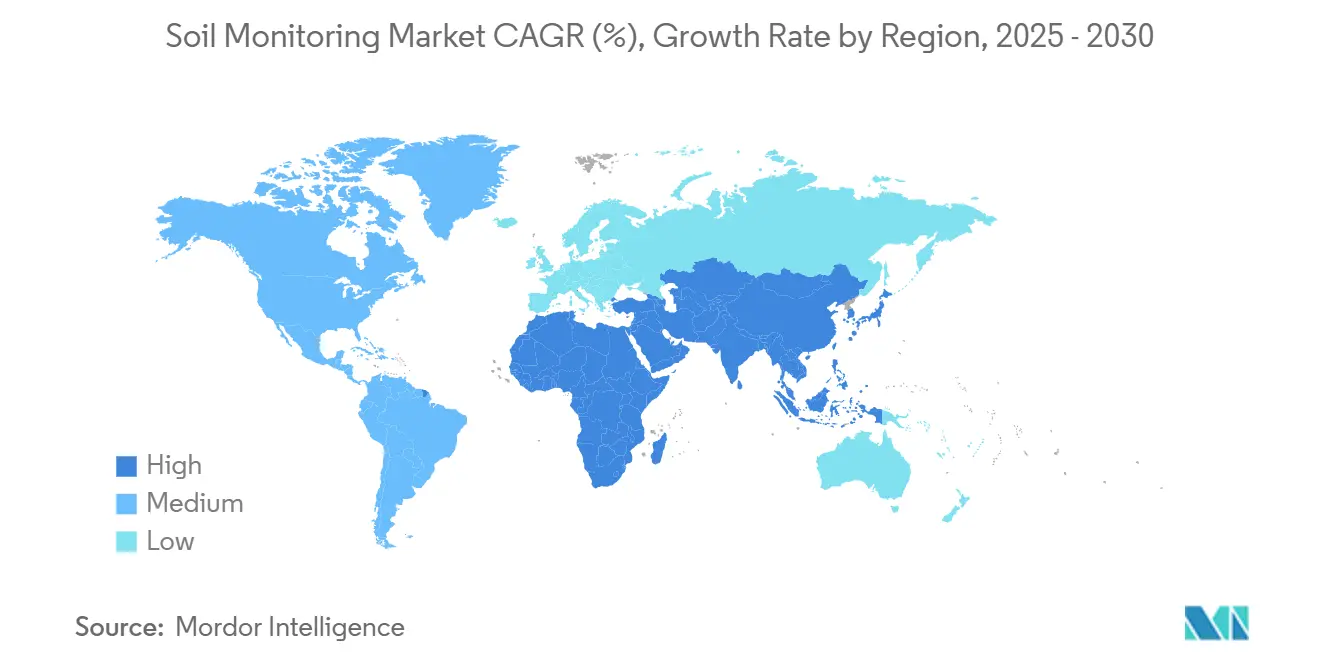

North America dominates the soil monitoring market, accounting for 31% of global revenue in 2024. The region's high agricultural mechanization, extensive Low Power Wide Area Network (LPWAN) infrastructure, and insurance-driven incentives drive market growth. Farms in the United States and Canada demonstrate advanced implementation through the integration of soil probes with autonomous irrigation systems. The region's established precision agriculture practices, combined with extensive R&D activities and supportive regulations that encourage data-driven risk management, strengthen the market position. The collaboration between agricultural technology companies and academic institutions enhances innovation, while increasing requirements for carbon-credit verification drive sensor adoption in large farming operations.

The Asia-Pacific region shows the highest growth rate, with a projected CAGR of 14.20% through 2030. Government initiatives, including India's Pradhan Mantri Kisan Urja Suraksha evam Utthan Mahabhiyan (PM-KUSUM) and China's smart-farming subsidies, support sensor implementation across extensive agricultural areas. The expansion of rural broadband and Long Range Wide Area Network (LoRaWAN) networks improves connectivity in remote agricultural regions. The growth of agricultural technology startups and increased participation from younger farmers accelerate market development. Environmental factors, including climate variability and water scarcity, drive the adoption of precision irrigation systems, while mobile-based monitoring platforms increase data accessibility for small-scale farmers.

European market growth remains stable, driven by environmental regulations and cooperative farming practices. In South America, Brazil's large agricultural businesses show high sensor adoption rates, while mountainous Andean regions face geographical and financial limitations. African markets demonstrate potential through donor-supported initiatives, though cost and technical support remain significant challenges. Middle Eastern countries, particularly Saudi Arabia and the UAE, focus on irrigation efficiency in desert agriculture, implementing satellite-IoT systems to optimize groundwater usage and remote monitoring. Adaptable sensor systems and mixed connectivity solutions gain popularity, particularly in areas with limited ground-based infrastructure.

Competitive Landscape

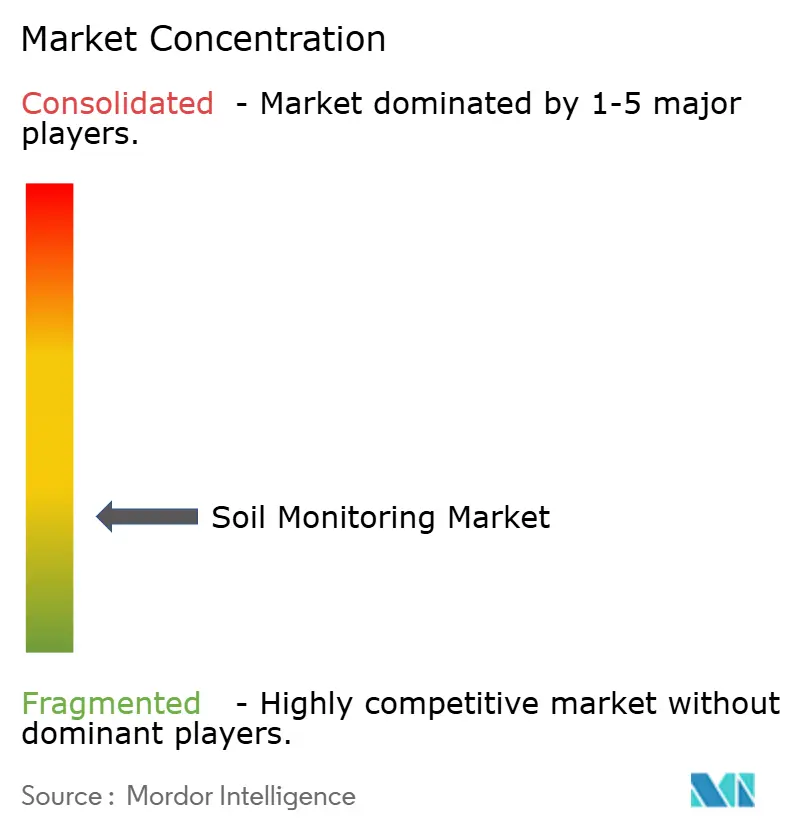

The soil monitoring market shows fragmentation, with the top five suppliers accounting for nearly one-third of global revenue. METER Group maintains market leadership through its capacitance probes and ZENTRA software suite. Stevens Water Monitoring Systems and Sentek Technologies hold substantial market positions through established dealer networks and industry reputation. The market structure continues to evolve through ongoing consolidation.

AGCO Corporation's acquisition of 85% of Trimble Ag for USD 2 billion in early 2025, creating the PTx Trimble joint venture, represents significant market consolidation by combining soil sensing capabilities with autonomous machinery control. The market now centers on integrated platforms that unite hardware, analytics, and automation, responding to increasing demands for precision agriculture, sustainability, and operational efficiency. These systems enable farmers to implement data-driven decisions using soil telemetry, weather information, and crop modeling.

New market entrants are advancing technological innovation. GroGuru has developed a subterranean probe with six sensors and a 10-year battery life for continuous root-zone monitoring with reduced maintenance requirements. EarthOptics combines ground-penetrating radar with machine learning to provide detailed carbon mapping through a data-as-a-service model. These venture capital-supported companies are transforming the market through scalable, AI-enabled solutions that integrate agronomic science, connectivity, and sustainability practices. The sector's growth potential increases as systems become more interoperable and cloud integration advances, attracting both commercial agricultural operations and research institutions.

Soil Monitoring Industry Leaders

METER Group

Stevens Water Monitoring Systems, Inc.

Sentek Technologies

CropX Inc.

SGS SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: The Toro Company and TerraRad have partnered to develop soil moisture monitoring software. The Spatial Adjust software integrates with the Toro Lynx Central Control platform. This irrigation control software enables automatic irrigation schedule modifications based on system recommendations.

- January 2025: Lindsay Corporation acquired a 49.9% stake in Pessl Instruments to strengthen its precision irrigation technology. The integration of Pessl's METOS soil monitoring systems with FieldNET enables farmers to make data-driven irrigation decisions based on real-time soil conditions, improving water efficiency and crop yields.

- November 2024: EarthOptics, a soil digitization company, secured USD 24 million in Series B funding. The company plans to use this investment to expand its soil digitization services and strengthen its position in the soil monitoring market.

- April 2024: AGCO Corporation and Trimble completed their joint venture agreement, establishing PTx Trimble to combine precision agriculture technologies. The joint venture integrates soil monitoring systems with autonomous machinery, allowing farms with diverse equipment to implement open, data-driven platforms for efficient and scalable

Global Soil Monitoring Market Report Scope

| Hardware |

| Software |

| Services |

| In-situ Sensors |

| Remote Sensing Platforms |

| Portable Probes and Test Kits |

| Wired |

| Wireless (LPWAN, Cellular, Satellite) |

| Open Field |

| Protected Cultivation |

| Forestry |

| Large Commercial Farms |

| Smallholder and Cooperative Farms |

| Research Institutes and Universities |

| Government and NGOs |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| France | |

| Spain | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Rest of Africa |

| By Component | Hardware | |

| Software | ||

| Services | ||

| By Product Type | In-situ Sensors | |

| Remote Sensing Platforms | ||

| Portable Probes and Test Kits | ||

| By Connectivity Technology | Wired | |

| Wireless (LPWAN, Cellular, Satellite) | ||

| By Application | Open Field | |

| Protected Cultivation | ||

| Forestry | ||

| By End-User | Large Commercial Farms | |

| Smallholder and Cooperative Farms | ||

| Research Institutes and Universities | ||

| Government and NGOs | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| France | ||

| Spain | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the soil monitoring market?

The soil monitoring market size is valued at USD 0.80 billion in 2025.

How fast is the soil monitoring market anticipated to grow?

The market is projected to register a 12.30% CAGR, reaching USD 1.43 billion by 2030.

Which component dominates spending today?

Hardware accounts for 58% of 2024 revenue, reflecting continued investment in probes, data loggers, and gateways.

Which region will grow the fastest through 2030?

Asia-Pacific is forecast to post a 14.20% CAGR, supported by subsidy programs and rural connectivity upgrades.

Why are satellite IoT links gaining share?

Satellite IoT addresses rural coverage gaps, enabling reliable data backhaul for farms located beyond terrestrial networks.

Page last updated on: