Soil Aerators Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

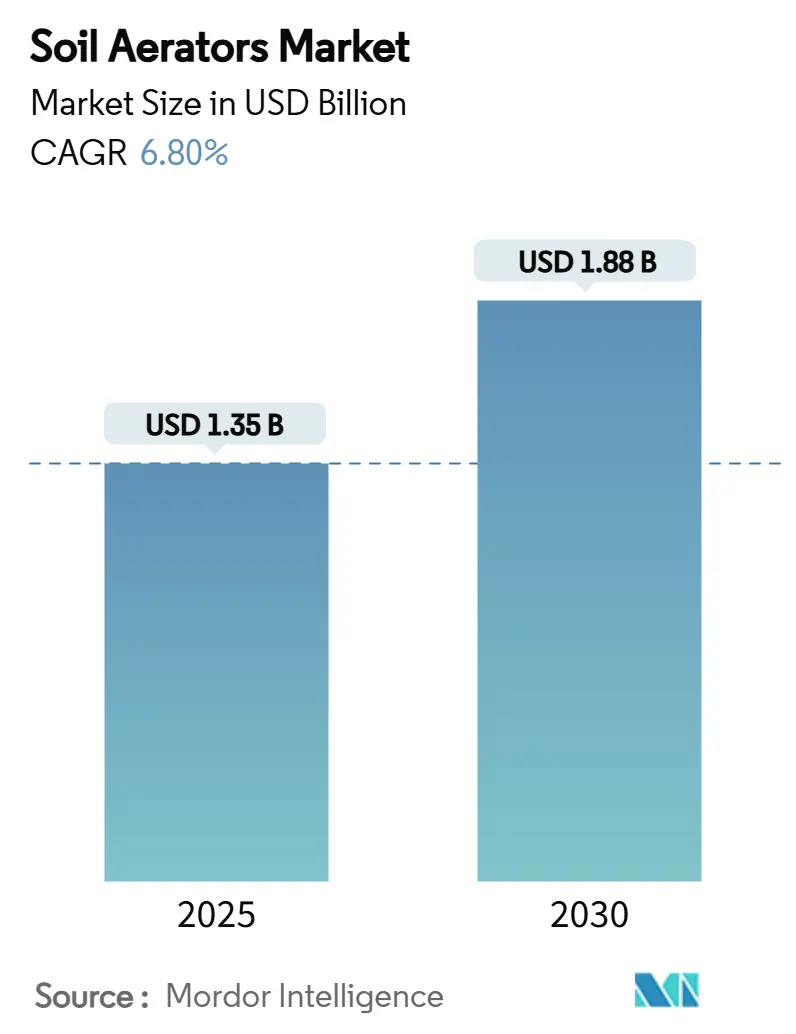

| Market Size (2025) | USD 1.35 Billion |

| Market Size (2030) | USD 1.88 Billion |

| Growth Rate (2025 - 2030) | 6.80% CAGR |

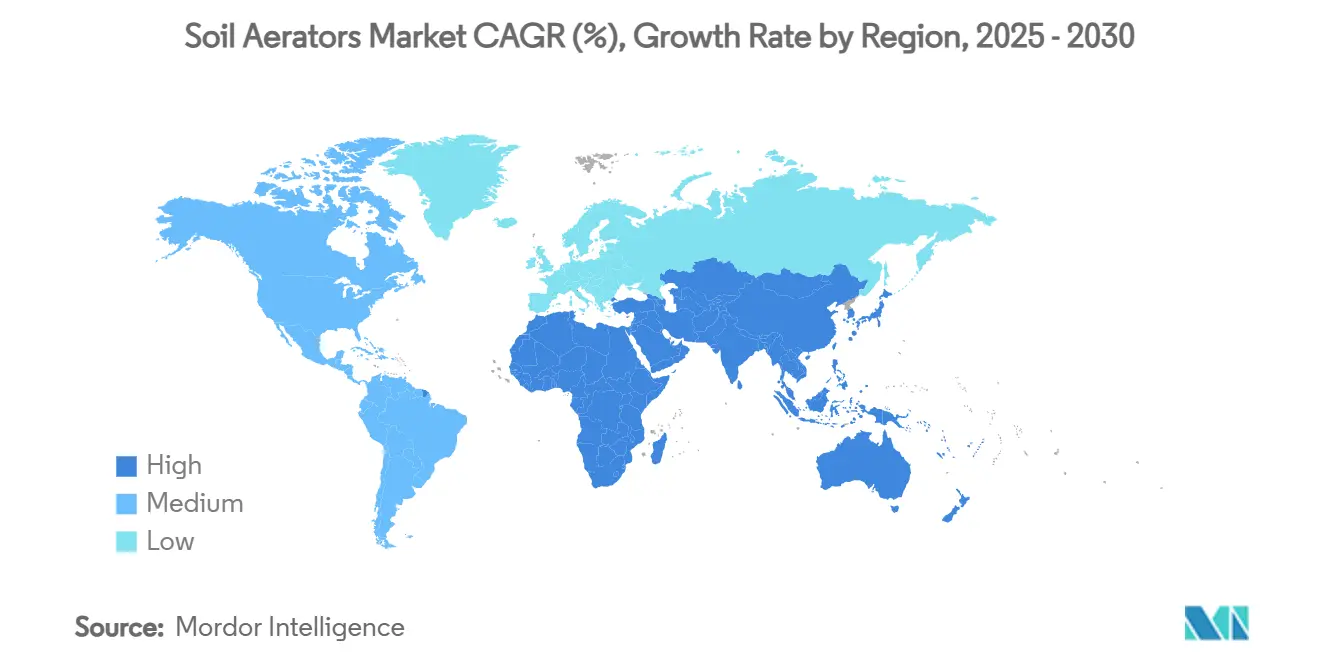

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Soil Aerators Market Analysis by Mordor Intelligence

The soil aerators market size is valued at USD 1.35 billion in 2025 and is projected to reach USD 1.88 billion by 2030, growing at a 6.80% CAGR. Rising soil compaction linked to heavy farm machinery and erratic rainfall patterns keeps demand for precision aeration equipment elevated. Precision turf-management practices, battery innovation, and government mechanization subsidies collectively expand the customer base, while autonomous guidance features enhance the value proposition for commercial buyers. North America leads the current market, but Asia-Pacific delivers the fastest growth as subsidy programs cut equipment prices by 50–80% for smallholders. Competition remains moderately fragmented, with the top five manufacturers controlling 55% share of the market, yet facing pressure from niche innovators offering autonomous and air-injection technologies. Overall, the market benefits from a balanced mix of yield-centric farming priorities, stringent turf-quality benchmarks, and steady product-upgrade cycles that emphasize connected, low-noise, battery-based platforms.

Key Report Takeaways

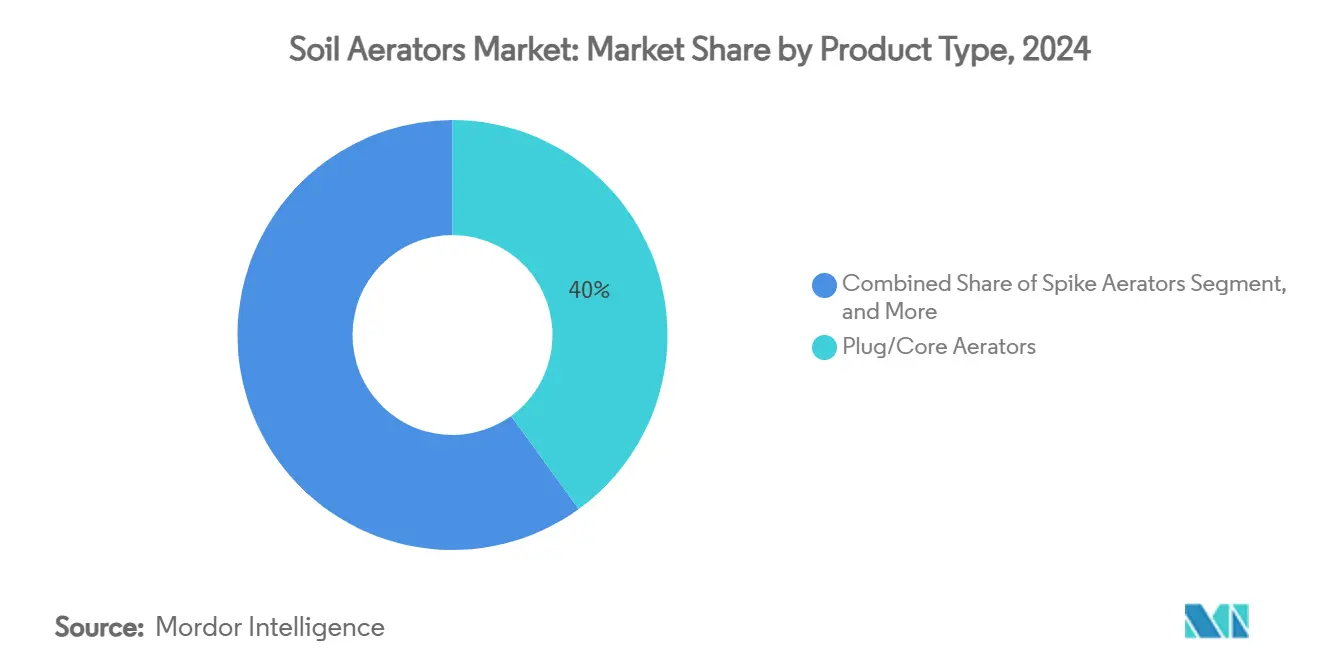

- By product type, plug/core aerators captured 40% of the soil aerators market share in 2024, and the same category is projected to record the fastest 10.5% CAGR through 2030.

- By mechanism, tractor-mounted systems accounted for 45% of the market share in 2024, while walk-behind units represent the fastest-growing mechanism segment, with a 7.8% CAGR through 2030.

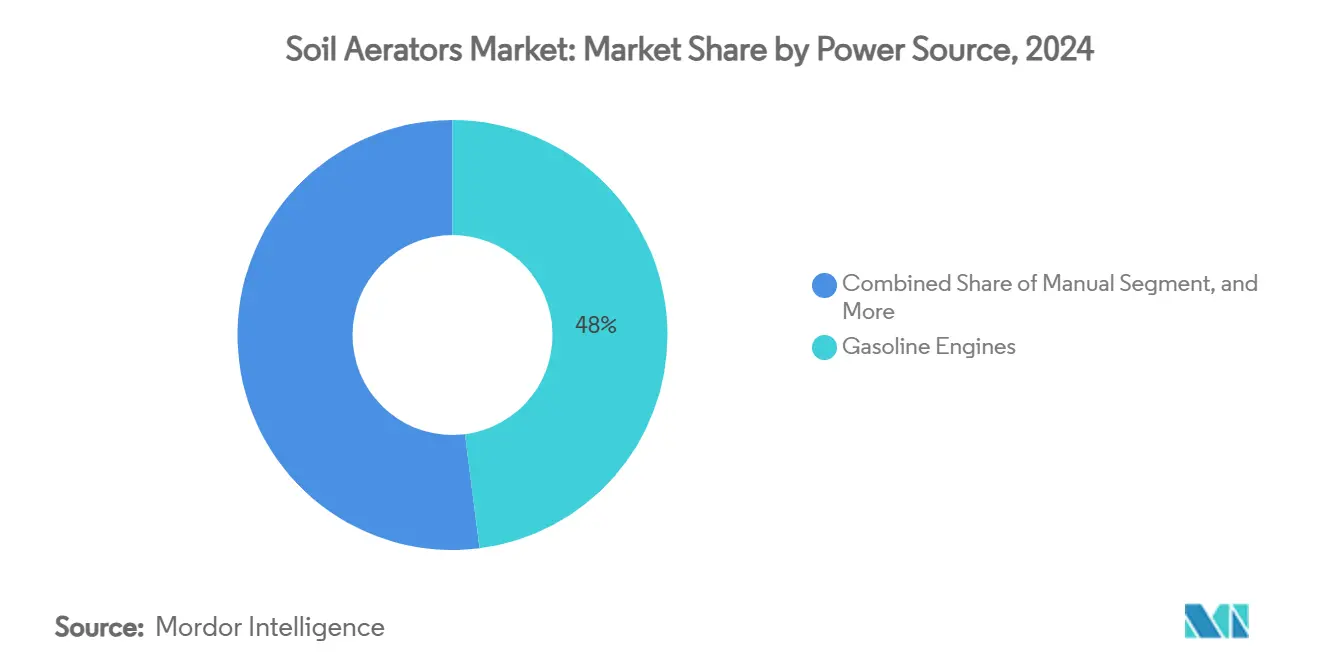

- By power source, gasoline equipment accounted for a 48% share of the market size in 2024, while electric/battery systems are advancing at an 8.5% CAGR to 2030.

- By end user, agriculture farms held 36% of the soil aerators market size in 2024, whereas sports fields represent the fastest-growing customer group with an 8.9% CAGR through 2030.

- By region, North America accounted for 33% of the market size in 2024, whereas Asia-Pacific is forecast to grow at a 9.3% CAGR over the same period.

Global Soil Aerators Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Precision turf-management uptake | +1.2% | North America and Europe | Medium term (2–4 years) |

| Smallholder farm mechanization | +1.8% | Asia-Pacific, spill-over to Africa | Long term (≥ 4 years) |

| Golf-course construction boom | +0.9% | Asia-Pacific and Middle East | Medium term (2–4 years) |

| Government farm mechanization subsidies | +1.5% | Asia-Pacific, Africa, and selective South America | Short term (≤ 2 years) |

| Battery-powered landscaping transition | +0.8% | North America and Europe, emerging Asia-Pacific | Medium term (2–4 years) |

| Climate-induced soil-compaction concerns | +1.3% | Global, intense in monsoon-affected regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Precision Turf-Management Uptake

Real-time soil-moisture sensors linked to automated irrigation systems now guide aeration decisions on golf courses, trimming water use by 30% while keeping greens playable [1]Source: Daniel King et al., “Sensor-Based Irrigation Reduces Water Usage,” Frontiers in Water, frontiersin.org. Toro’s collaboration with TerraRad places moisture detection directly on commercial mowers, allowing superintendents to schedule variable-depth passes that avoid unnecessary disruption. Injection machines such as Air2G2 reach 10–12 inch depths without removing cores, supporting continual play for sports venues. The evolution from purely mechanical metrics to data-driven agronomy shifts purchase criteria toward GPS guidance, cloud analytics, and autonomous routing. As turf managers quantify irrigation savings and surface-smoothness gains, premium pricing for technology-rich aerators becomes easier to justify.

Smallholder Farms Mechanization

Tractor density in Thailand now exceeds 50 units per 1,000 hectares, reflecting a region-wide pivot from manual labor to machine-based soil management. Custom-hiring centers let farmers rent aerators by the hour, bypassing high ownership costs yet still reducing compaction ahead of rice planting cycles. India’s Sub-Mission on Agricultural Mechanization refunds up to 80% of the equipment purchase price, fueling a projected rise in the country’s agricultural-machinery spending from USD 16.73 billion in 2024 to USD 25.15 billion by 2029. Small, PTO-compatible aerators engineered for wet-paddy soil conditions fill a growing design niche. Rural labor shortages further accelerate demand, redefining aeration as mandatory rather than optional.

Golf-Course Construction boom

Tourism strategies in Vietnam, Indonesia, and the United Arab Emirates routinely feature championship-level golf developments that open with prespecified turf-maintenance standards. Architects now write battery-powered, low-noise aeration capability into course construction briefs to satisfy neighborhood sound ordinances and sustainability certifications. Integrated soil-monitoring packages, training modules, and service contracts often decide supplier selection. Equipment reliability trumps ultra-advanced features for many new operators, nudging manufacturers to balance innovation with ruggedness. With Asia-Pacific announcing double-digit new-course pipelines through 2027, the sales window for premium aeration fleets remains wide.

Government Farm Mechanization Subsidies

Policy makers prioritize soil health within subsidy frameworks, classifying aeration attachments as eligible capital. India’s SMAM program covers 50–80% of equipment cost and mandates that at least 40% of beneficiaries be small and marginal farmers. China’s green-agriculture grants extend similar incentives, encouraging local assembly partnerships that shorten lead times [2]Source: Yiming Zhao, “Green-Agriculture Grant Framework and Local Assembly Incentives,” Sustainability, mdpi.com. These subsidies spur the Original Equipment Manufacturers (OEMs) to localize production, ensuring equipment qualifies for domestic-content thresholds. Successful schemes bundle funding with dealership expansion, ensuring technical support accompanies hardware.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront equipment costs | -1.1% | Developing regions worldwide | Short term (≤ 2 years) |

| Low farmer awareness in developing nations | -0.8% | Africa, parts of Asia-Pacific, and South America | Medium term (2–4 years) |

| Limited aftermarket service networks | -0.6% | Remote rural areas globally | Medium term (2–4 years) |

| Bio-aeration microbial alternatives | -0.4% | Developed markets with advanced practices | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Equipment Costs

Commercial aerators priced between USD 15,000 and USD 50,000 remain out of reach for many rural contractors. The premium rises when lithium-ion batteries add 20–30% to the list price. Leasing models and pay-per-use hire centers appear, yet they rely on dense dealer networks to stay profitable. Entry-level lines help the Original Equipment Manufacturer (OEMs) defend share but risk cannibalizing margins. Manufacturers increasingly pair financing packages with predictive-maintenance platforms to reassure risk-averse buyers.

Low Farmer Awareness in Developing Regions

Surveys in sub-Saharan Africa show many growers still equate soil loosening exclusively with tillage. Misuse of techniques, like operating aerators on saturated fields, can undermine benefits and deepen uncertainty. Hands-on demonstrations and agronomic workshops led by local extension agents prove more effective than pamphlets. Digital videos accessible via low-bandwidth apps broaden outreach but need translation into regional languages to resonate.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Battery Integration Accelerates Core-Aerator Evolution

Plug/core aerators commanded 40% of the soil aerators market size in 2024, owing to efficient compaction relief and water-infiltration gains. Battery integration now pushes this legacy design into low-noise commercial settings, with battery-powered plug/core aerators forecast to grow at a 10.5% CAGR to 2030. Spike units hold a significant share, favored by homeowners seeking quick surface perforation but limited in professional contracts. Liquid aerators are also gaining traction where immediate playability or crop access is required. Slit aerators support drainage improvement on heavy-clay croplands.

Product development centers on multi-function hybrids that blend coring with targeted amendment injection. Walker Manufacturing’s Perfaerator illustrates the productivity race, clocking 60,000 square feet per hour and reinforcing a premium for time-saving designs. As GPS feedback refines depth settings and hole spacing, buyer focus shifts from mechanical specs to software capabilities. Material-strength upgrades and anti-rust coatings extend service intervals, supporting total-cost-of-ownership arguments in competitive bids.

By Mechanism: Tractor-Mounted Dominance Meets Autonomous Walk-Behind Innovation

Tractor-mounted units represented 45% of the soil aerators market share in 2024 by capitalizing on existing PTO power and fleet familiarity. Their ability to cover large acreages with a single pass keeps per-acre costs low for grain producers. Walk-behind systems represent the fastest-growing mechanism segment at 7.8% CAGR through 2030, driven by precision control requirements in golf courses and sports facilities where maneuverability outweighs productivity considerations. Autonomy upgrades, such as Toro’s boundary-wire-free routing, promise labor savings and consistent hole patterns.

Tow-behind offers versatility for mixed-fleet operators and municipalities. Handheld variants are mainly used for residential touch-ups and tight-spot remediation. Modular frames enabling plug-and-play spiker decks, seeders, and topdressers find growing acceptance, reflecting a trend toward the consolidation of turf-maintenance tasks within one chassis. Data logging on pass count and depth uniformity provides proof of work to facility managers, reinforcing service-provider accountability.

By Power Source: Electrification Reshapes Design and Procurement

Gasoline engines still powered 48% of units sold in 2024, but municipal noise limits and fuel-price volatility drive change. Electric/battery models are forecasted to grow 8.5% CAGR through 2030. Lightweight aluminum decks and high-torque brushless motors help offset battery mass. Manual tools are primarily used in do-it-yourself lawn care and specialty horticulture. PTO-driven attachments are gaining traction, aligning with tractor electrification roadmaps that aim for fully electric drivetrains.

Fleet managers increasingly scrutinize kilowatt-hour cost versus gasoline usage, recording operational savings of 20–25% once battery amortization completes. Fast-swap battery docks enable round-the-clock commercial work, aligning with service-level agreements that stipulate zero daytime downtime. The Original Equipment Manufacturers (OEMs) negotiate direct cell sourcing to stabilize pack prices amid commodity-metal swings.

By End User: Agriculture Generates Volume, Sports Fields Drive Specification

Agricultural producers constituted 36% share of the soil aerators market in 2024. Their priority remains throughput and ruggedness, favoring tractor-mounted solutions with 48-inch or wider coring decks. Sports fields deliver the quickest growth at an 8.9% CAGR, adopting variable-depth, low-impact injectors that preserve playing schedules. Golf courses hold a significant share, balancing core removal with micro-tining to meet stringent surface-roll targets.

Commercial landscaping firms are expanding by differentiating contracts through low-noise, battery-powered offerings for corporate campuses and municipalities. The residential lawns continue to grow, but the rise of subscription lawn-care services gradually migrates this demand into the professional channel. Across customer groups, IoT sensors transmitting compaction maps to mobile apps steer purchase decisions toward smart-enabled machines [3]Source: Lijun Chen and Yuan Gao, “Real-Time Soil-Compaction Mapping through Low-Power Wide-Area IoT Networks,” Sensors, mdpi.com.

Geography Analysis

North America retained a 33% share of the soil aerators market size in 2024 on the back of high mechanization and early adoption of precision agronomy. John Deere’s USD 20 billion manufacturing expansion through 2035 underscores the region’s capacity for ongoing technology refresh cycles. Strict workplace-noise limits in United States metropolitan areas push contractors toward battery platforms, accelerating product turnover.

Asia-Pacific delivers the fastest 9.3% CAGR to 2030. National subsidy schemes in India, China, and Thailand lower purchase thresholds, while expanding golf and football infrastructure opens additional turf segments. Custom-hiring cooperatives spread machinery access beyond early-adopter commercial farms, lifting overall utilization rates.

Europe's growth is buoyed by Common Agricultural Policy payments that encourage soil-health interventions. Emission regulations on small engines intensify the replacement demand for electric drives. Research programs under Horizon Europe allocate grants for autonomous field equipment, nurturing start-ups that partner with established Original Equipment Manufacturers (OEMs). South America registered a stable but modest uptake as soybean producers weigh aeration benefits against tight capex buffers. The Middle East and Africa markets are driven largely by golf-course development linked to tourism diversification. Water scarcity concerns elevate demand for aeration equipment that boosts infiltration and reduces irrigation cycles, particularly on desert-based sport venues.

Competitive Landscape

The soil aerators market remains moderately fragmented. Major players, including The Toro Company, Husqvarna Group, Deere & Company, Kubota Corporation, and Briggs and Stratton, are merging their mechanical expertise with cutting-edge electronics to maintain their dominance. They are leveraging innovations like boundary-free navigation, cloud-based dashboards, and battery packs that seamlessly integrate into multi-tool ecosystems.

Mid-sized challengers specialize in air-injection technology or high-speed slitters, carving out premium niches. Strategic partnerships, such as New Holland teaming with Bluewhite on autonomous tractors, expand feature sets without organic R&D sprawl. Service depth increasingly differentiates brands, and mobile technicians equipped with IoT-driven diagnostic kits shorten downtime and support premium pricing.

White-space opportunities persist in combining biological soil conditioners with mechanical passes. The Original Equipment Manufacturers (OEMs) exploring on-board liquid-delivery add-ons can tap crossover revenue from the expanding biofertilizer sector. As buyers benchmark total soil-health outcomes, suppliers capable of one-stop agronomic solutions will strengthen customer stickiness.

Soil Aerators Industry Leaders

Deere & Company

The Toro Company

Husqvarna Group

Kubota Corporation

Briggs & Stratton LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Wiedenmann GmbH unveiled the Terra Core 8, a mid-depth precision aerator offering a 195 cm working width and 270 holes/m² capacity, at Demopark 2025, enhancing its position in the professional turf management segment.

- January 2025: Walker Manufacturing rolled out the Perfaerator, an attachment that aerates 60,000 square feet per hour, compatible with multiple Walker mowers and aimed at boosting contractor productivity.

- February 2024: Bobcat Co. expanded its groundcare equipment lineup with new turf renovation devices, including aerators, sod cutters, dethatchers, and overseeders, aimed at professional landscaping markets.

- January 2024: Z Turf Equipment introduced the Z-Aerate 50, a 50″, 12-row aerator that covers up to 3 acres per hour and features an integrated 150 lb hopper spreader, strengthening its appeal among turf professionals by combining aeration and granular application in a single pass.

Global Soil Aerators Market Report Scope

The soil aerators market covers equipment designed to alleviate soil compaction and enhance air, water, and nutrient movement in agricultural fields, sports turf, golf courses, and landscaping areas. The market is segmented by product type (plug/core aerators, spike aerators, and others), mechanism (walk-behind, tow-behind, and more), power source (manual, gasoline, and additional types), end user (agriculture farms, sports fields, golf courses, and others), and region (North America, Europe, Asia-Pacific, South America, and more). Market forecasts are provided in terms of value (USD).

| Plug/Core Aerators |

| Spike Aerators |

| Liquid Aerators |

| Slit Aerators |

| Walk-behind |

| Tow-behind |

| Tractor-mounted |

| Handheld |

| Manual |

| Gasoline |

| Electric/Battery |

| Power-take-off (PTO) |

| Agriculture Farms |

| Sports Fields |

| Golf Courses |

| Commercial Landscaping |

| Residential Lawns |

| North America | United States |

| Canada | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Product Type | Plug/Core Aerators | |

| Spike Aerators | ||

| Liquid Aerators | ||

| Slit Aerators | ||

| By Mechanism | Walk-behind | |

| Tow-behind | ||

| Tractor-mounted | ||

| Handheld | ||

| By Power Source | Manual | |

| Gasoline | ||

| Electric/Battery | ||

| Power-take-off (PTO) | ||

| By End User | Agriculture Farms | |

| Sports Fields | ||

| Golf Courses | ||

| Commercial Landscaping | ||

| Residential Lawns | ||

| By Region | North America | United States |

| Canada | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the Soil Aerators market?

The global soil aerators market size stands at USD 1.35 billion in 2025.

How fast is the Soil Aerators market forecasted to grow?

Soil aerators market is projected to reach USD 1.88 billion by 2030, registering a 6.80% CAGR.

Which region is expanding the quickest?

Asia-Pacific leads with a 9.3% CAGR owing to the subsidy-driven mechanization programs.

What segment holds the largest Soil Aerators market share?

Plug/core aerators command 40% share of the market.

Who are the major players in the Soil Aerators industry?

The Toro Company, Husqvarna Group, Deere & Company, Kubota Corporation and Briggs and Stratton LLC collectively control more than half of worldwide revenue.

Page last updated on: