Soil Amendments Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

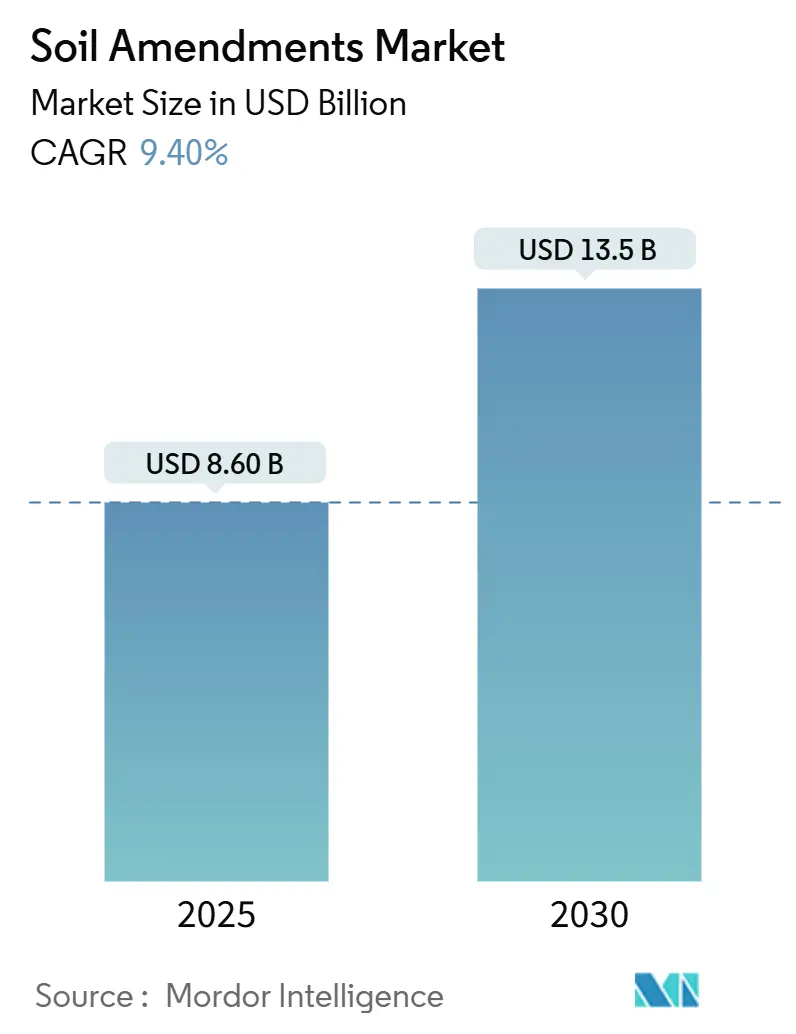

| Market Size (2025) | USD 8.60 Billion |

| Market Size (2030) | USD 13.5 Billion |

| Growth Rate (2025 - 2030) | 9.40% CAGR |

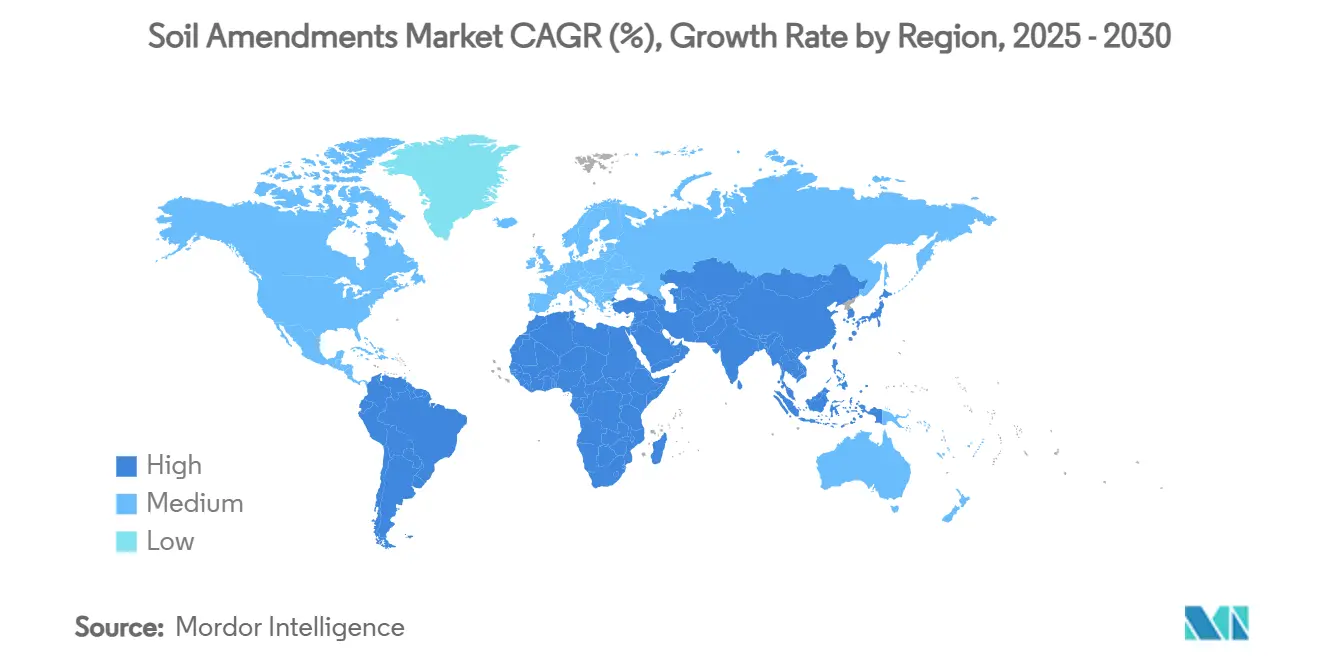

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

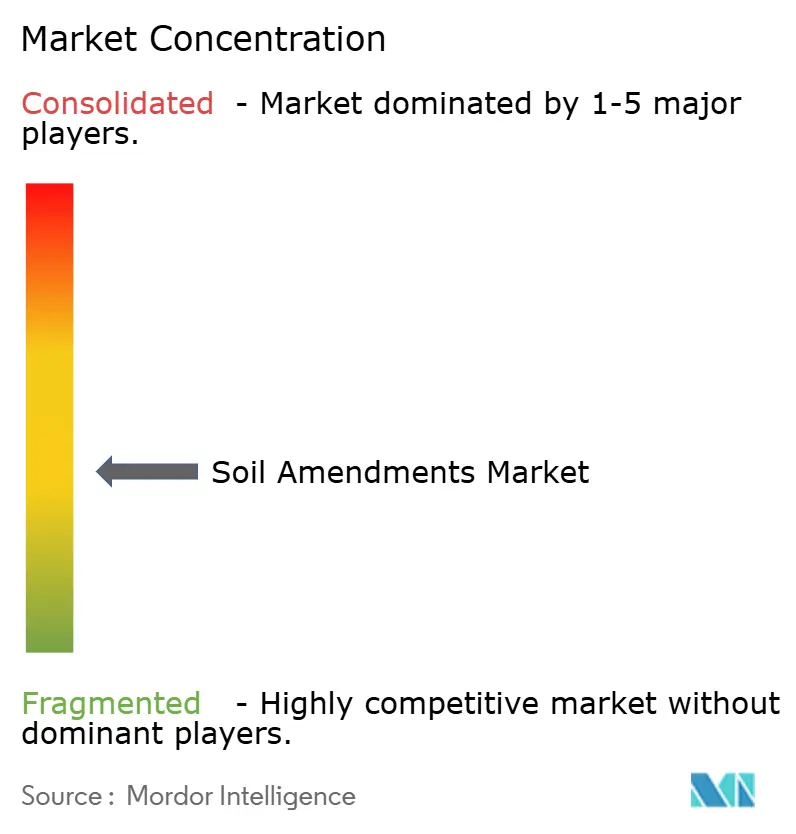

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Soil Amendments Market Analysis by Mordor Intelligence

The soil amendments market size is valued at USD 8.6 billion in 2025 and is forecast to reach USD 13.5 billion in 2030, advancing at a 9.4% CAGR. Rapid adoption of regenerative farming, the widening use of biochar for carbon sequestration, and rising carbon-credit prices underpin this expansion. Government incentives, such as the United States Department of Agriculture (USDA) Climate-Smart Agriculture grants and the European Union's Soil Deal for Europe, accelerate demand by linking soil health to subsidy eligibility. Corporate scope-3 carbon commitments, now embedded in supplier contracts for major food brands, further stimulate purchases of high-quality conditioners. North America holds the largest regional position due to federal biochar funding, while Asia-Pacific posts the fastest gains because of large-scale soil-restoration campaigns in China and India. Market headwinds include regulatory patchiness across jurisdictions and feedstock-cost volatility, but these are mitigated by continuous product innovation and digital agronomy platforms that prove return on investment to growers.

Key Report Takeaways

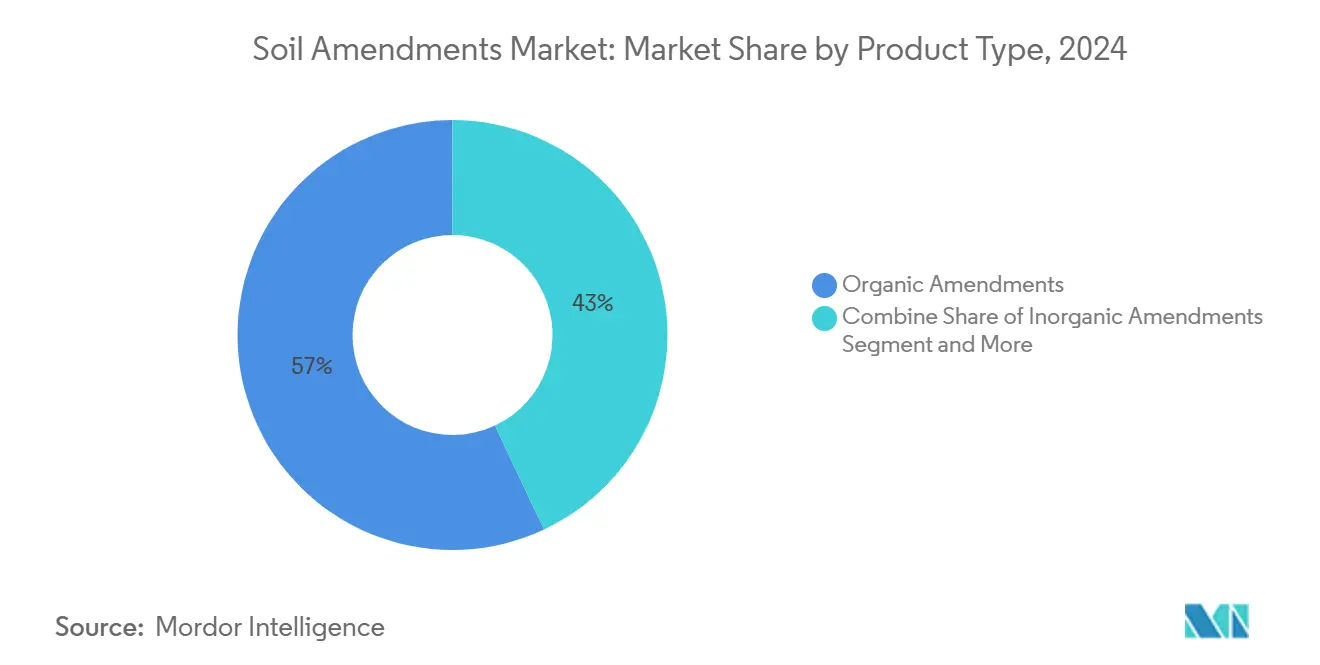

- By product type, organic amendments led with 57% of the soil amendments market share in 2024; biochar-based amendments are projected to expand at a 12.4% CAGR through 2030.

- By form, solid formulations accounted for 68% of the soil amendments market share in 2024, while liquids are forecast to grow at 11.2% CAGR.

- By application, agriculture commanded a 75% share of the soil amendments market size in 2024; environmental remediation is advancing at an 11.5% CAGR.

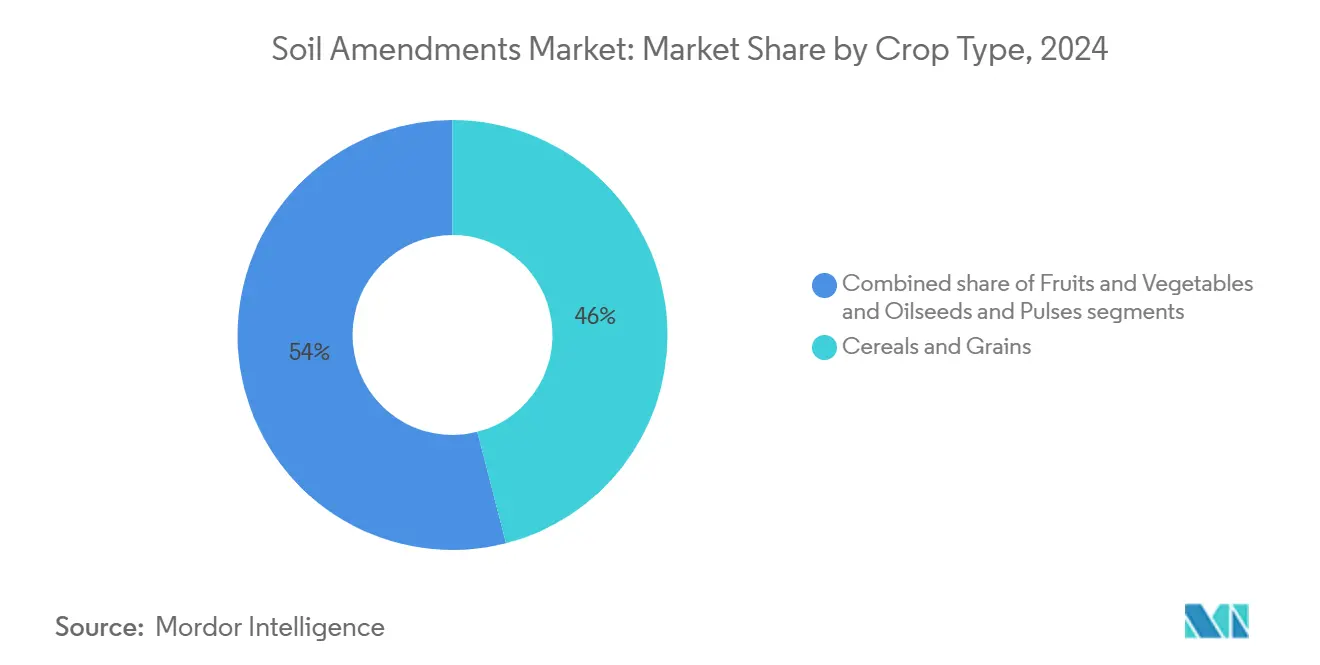

- By crop type, cereals and grains dominated with 46% revenue share in 2024; fruits and vegetables registered the highest projected CAGR at 10.6% to 2030.

- By soil type, sandy soils represented 39% of the 2024 volume, and clay-soil applications are set to climb 9.8% CAGR on structural-improvement demand.

- By geography, North America held 31% of 2024 revenue, while Asia-Pacific is forecast to record a 12.7% CAGR through 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Soil Amendments Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated transition to regenerative agriculture mandates | +2.1% | North America and Europe | Medium term (2-4 years) |

| Rising carbon credit valuation incentivizing biochar | +1.8% | Global voluntary markets | Long term (≥ 4 years) |

| Soil microbiome seed coating synergies boosting demand | +1.2% | North America and Europe, spreading to the Asia-Pacific | Medium term (2-4 years) |

| Water scarcity driving uptake of super-absorbent polymers | +1.5% | Asia-Pacific, Middle East, Africa | Short term (≤ 2 years) |

| Government bans on high-salinity synthetic fertilizers | +0.9% | Europe and Asia-Pacific | Medium term (2-4 years) |

| Net-zero supply-chain commitments | +1.3% | Multinational corporations worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated transition to regenerative agriculture mandates

Government programs are reshaping purchasing behavior by tying subsidies to verifiable soil-health improvements. The USDA allocates USD 300 million to greenhouse-gas measurement and verification in 2023, while the EU funds 100 living labs that demonstrate best practices[1]Source: U.S. Department of Agriculture (USDA), "Biden-Harris Administration Announces New Investments", www.usda.gov. Australia’s National Soil Strategy adds AUD 21.599 million (USD 14.5 million) for monitoring networks that favor conditioners with proven carbon-sequestration benefits. Banks now require soil-health documentation for farm credit, rewarding early adopters with better loan terms. These actions compound to lift the soil amendments market by expanding the addressable user base and shortening payback periods for new products.

Rising carbon credit valuation incentivizing biochar

Voluntary carbon markets price removal credits at EUR 174 (USD 190) per metric ton, and verified biochar trades between EUR 300 and EUR 2,000 (USD 327–2,180) per metric ton in Europe. Soil amendment producers embrace dual-revenue models, selling biochar to farmers and monetizing certified removals. Pilot facilities in Washington State, backed by USD 20.49 million in USDA grants, illustrate the scale-up path. Corporate buyers, such as beverage and technology firms, pre-purchase credits to meet net-zero targets, anchoring demand and improving project bankability.

Government bans on high-salinity synthetic fertilizers

Europe’s Fertilizing Products Regulation limits chloride-rich inputs, prompting growers to substitute mineral salts with organic conditioners that release nutrients gradually. Several Asian governments follow with bans on high-salinity imports to curb soil crusting. This regulatory shift widens the soil amendments market by displacing conventional amendments in sensitive horticulture systems.

Soil microbiome seed coating synergies boosting demand

Seed companies are partnering with microbial innovators to develop endophyte-enhanced coatings that rely on supportive soil conditions for full efficacy. In 2024, Syngenta's alliance with Intrinsyx Bio exemplified bundled biological and soil-focused solutions that enhance nutrient uptake and plant resilience. Emerging patents detail methods for storing live microbes within seeds to extend shelf life and improve field performance. These advances are increasing pull-through demand for soil conditioners such as compost, biochar, and humic amendments that help regulate moisture and pH, ensuring microbial survival and effectiveness.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Patchy, ambiguous global regulations for amendments | -1.4% | Emerging markets worldwide | Medium term (2-4 years) |

| Organic raw-material price volatility | -1.1% | Global with regional spikes | Short term (≤ 2 years) |

| Farmer skepticism due to inconsistent field results | -0.8% | Traditional farming regions | Medium term (2-4 years) |

| Weak distribution for live microbial products | -0.6% | Rural areas in developing regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Patchy, ambiguous global regulations for amendments

Fragmented rules on product registration delay launches and inflate compliance costs. The European Union’s shift from Regulation 2003/2003 to 2019/1009 forced re-certification of many conditioners. Canada’s modernized fertilizer code extends renewal cycles yet introduces new data requirements. Companies must keep multiple formulations for different jurisdictions, limiting economies of scale and slowing global rollouts.

Farmer Skepticism from Inconsistent Field Results

Variable soil conditions and improper application of soil amendments can lead to mixed outcomes, eroding trust among risk-averse growers. Public extension agencies are expanding demonstration plots, but coverage remains uneven. This restraint slows first adoption, especially in markets with limited technical support. Soil amendments aimed at improving long-term soil health, such as those that increase organic matter content, often produce gradual results. This delayed impact creates challenges for farmers in justifying their investment, particularly when compared to chemical fertilizers that deliver immediate, visible effects.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Organic Dominance and Biochar Momentum

Organic amendments held 57% share of the soil amendments market size in 2024, with compost, manure, and humic substances leading the category. Biochar-based products are projected to grow at a 12.4% CAGR, driven by carbon-credit opportunities and yield improvements. While inorganic products maintain their position in specialty crops, biological formulations show rapid growth through seed-coating applications. India's Minister Nitin Gadkari endorsed biochar workshops and subsidized pyrolyser technologies in May 2025, while Denmark implemented a pyrolysis-biochar strategy in October 2024, allocating EUR 13.5 million (USD 14.6 million) for R&D and EUR 1.34 billion (USD 14.5 million) in subsidies through 2027.

Organic amendments dominate the global soil amendments market due to their established usage, regulatory acceptance, and organic agriculture demand. The Department for Environment, Food and Rural Affairs reports that in 2023, Cattle FYM was the primary organic fertilizer in Great Britain, used by 47.1% of farmers, while Cattle Slurry ranked second at 16.7% adoption, offering essential nutrients while reducing chemical fertilizer requirements[2]Source: Department for Environment, Food and Rural Affairs, "THE BRITISH SURVEY OF Fertilizer Practice", www.gov.uk.

By Form: Solid Stability, Liquid Acceleration

Granules and powders account for 68% of the soil amendments market share due to storage stability and bulk-fertilizer logistics compatibility. Liquid formulations are projected at 11.2% CAGR through 2030, driven by fertigation and drone-based foliar applications. Dry solids maintained the largest market share in 2023-2024, particularly in cereal and grain cultivation, due to sustained nutrient release, soil structure improvement, and water retention properties.

Biodegradable polymer encapsulation enables controlled-release solid granules that combine liquid-like precision with practical handling. Water-soluble packaging reduces operator exposure while meeting safety and sustainability requirements. Brazil's 2024 "Precision Ag Initiative" funds liquid humic-microbe applications in soybean and orange cultivation, while the European Biostimulant Industry Council introduced guidelines in early 2025 for liquid microbial inoculants in EU fertigation systems.

By Application: Agriculture Scale and Remediation Upside

Agriculture captures 75% of the soil amendments demand because of the vast land area under cultivation and heightened focus on sustainable yields. For instance, according to the US Department of Agriculture, in 2024, the total area of land in the United States farms reached a total of 876.5 million acres[3]Source: US Department of Agriculture, "Farms and Land in Farms 2024 Summary", www.usda.gov. Environmental remediation is the fastest-moving application at 11.5% CAGR, harnessing biochar and phytoremediation to immobilize heavy metals and degrade hydrocarbons. Horticulture and turf maintain a healthy 9.2% CAGR on the back of urban-greening programs and homeowner interest in organic gardening.

Superfund restorations in the United States now specify soil amendments to rehabilitate sites, creating dedicated procurement streams. Corporate remediation of legacy industrial land similarly deploys conditioners to meet ESG disclosure requirements, opening cross-sector partnerships for suppliers.

By Crop Type: Staples Lead, High-Value Crops Surge

Cereals and grains represent the largest buyer group with a 46% share in the soil amendments market due to the farm area and the rising adoption of conservation tillage. Fruits and vegetables post the highest CAGR of 10.6% because premium pricing supports advanced soil-health inputs. Oilseeds and pulses accelerate as growers capitalize on nitrogen-fixing synergies with microbial conditioners.

Government and association efforts spotlight this shift: In 2024–25, the European Biostimulant Industry Council and USDA-supported initiatives endorsed soil amendments tailored for horticulture, backing rapid-acting liquid and microbial conditioners suited to vegetables and berries. The United Kingdom SoilPoint and Cefetra 2025 trial, backed by the Soil Association, replaced synthetic N with humic-based conditioners in fruit and vegetable rotations to improve soil fertility and reduce emissions.

By Soil Type: Sandy, Focus on Hydrogels, Clay on Structure

Sandy soils hold a 39% share in the soil amendments market, while clay soils show a CAGR of 9.8%. Sandy soils need polymer amendments due to low water retention and nutrient leaching. Clay soils require conditioners to reduce compaction and improve stability, favoring compost and biochar solutions. Loam and silt soils use biological conditioners to maintain nutrient balance. The Soil CRC's Australian sandy soils atlas demonstrates efforts to develop targeted amendment strategies across millions of hectares.

Clay soils, the fastest-growing segment, require gypsum, surfactants, and engineered conditioners to address compaction and drainage issues. In October 2024, Clemson University research showed improved soil structure and crop biomass through clay applications on sandy plots. In April 2024, Florida's Southern SARE funded a Siembra Farm pilot studying clay integration in sandy organic plots, with initial results showing improved moisture retention and cabbage yields.

Geography Analysis

North America holds 31% of 2024 revenue, underpinned by USD 120 million in federal biochar grants, robust carbon markets, and advanced precision-farming adoption. Canada’s revamped fertilizer rules and extensive extension services foster trust in biologicals. Strong farm incomes allow growers to trial premium conditioners without compromising cash flow, and the region’s research institutions shorten product-validation cycles.

Asia-Pacific records the fastest soil amendments market growth, at 12.7% CAGR to 2030. China enforces strict arable-land safeguards across 124.33 million hectares, integrating conditioners into rehabilitation mandates. India’s Dhan-Dhaanya Krishi Yojana directs subsidies toward 100 low-productivity districts, catalyzing conditioner adoption among smallholders. The region benefits from large biomass streams for organic feedstocks, though distribution and agronomic-training gaps persist.

Europe shows steady expansion, driven by the EU Soil Deal’s 100 living labs and a forthcoming Soil Monitoring Law addressing degraded land that costs EUR 50 billion (USD 54.5 billion) annually. Biochar fetches EUR 300–2,000 (USD 327–2,180) per metric ton, depending on certification status, rewarding innovators that deliver verified removals. Tight fertilizer-salinity limits and a 2050 carbon-neutral target embed conditioners into compliance pathways.

Competitive Landscape

The soil amendments market is moderately fragmented, featuring multinational agrochemical companies, bio-based innovators, and precision agriculture startups competing through sustainable solutions and market expansion. Companies like BASF, UPL, Bayer, and FMC are expanding their portfolios with bio-based and microbial soil amendments for both conventional and organic markets. BASF introduced BACTIVA, a biologically active soil amendment, in 2025, while UPL expanded its regenerative agriculture division with microbial blends for soil structure restoration.

United States-based Huma Inc. acquired Gro-Power Inc. in 2024, enhancing its carbon-rich product portfolio. American Biocarbon received OMRI certification in 2025 for its sugarcane bagasse-derived biochar, responding to increased demand for organic-certified products. AMVAC Green Solutions formed a partnership with Biome Makers in 2024 to combine microbial diagnostics with soil health products, while Key Plex collaborated with Naiad in 2025 to expand global distribution.

Living Water Agriculture launched SoilPHIX, a microbial bioreactor system integrated with irrigation, expanding across the United States. The industry is shifting toward biologically enriched, climate-focused products, particularly as soil amendments connect to carbon markets and regenerative practices. Markets in the Asia-Pacific and South America are increasing adoption to address soil degradation and support high-value crops. This growth combines traditional industry players and innovative startups advancing through technology integration, certifications (OMRI, USDA Organic), and sustainable solutions.

Soil Amendments Industry Leaders

-

Yara International ASA

-

BASF SE – Agricultural Solutions

-

Nutrien Ltd

-

ICL Group

-

UPL Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: The Fertilizer and Soil Amendments Product Roundup 2025 showcased several new products, including Aero-Blitz (a micronutrient blend for drone or plane application), Chandler Soil (an enzyme-based liquid amendment by Midwest Bio-Tech), and Sure Humate (a concentrated humic acid formulation).

- January 2025: Fargro introduced BACTIVA Soil Amendment at BTME 2025, a bio-based product containing Bacillus subtilis and Trichoderma fungi. The product aims to improve turf management through enhanced soil health, root system development, and increased resilience for sports fields and golf courses, providing an environmentally sustainable alternative to chemical treatments.

- January 2025: American BioCarbon's bagasse-derived biochar soil enhancer received OMRI (Organic Materials Review Institute) certification for use in organic agriculture. The biochar improves soil fertility and water retention while enabling carbon sequestration in agricultural operations.

- February 2024: Huma, Inc. acquired Gro-Power Inc., a granular fertilizer manufacturer, to enhance its organic fertilizer and soil conditioner capabilities while expanding the application of Micro Carbon Technology in soil amendment products.

Global Soil Amendments Market Report Scope

| Organic Amendments |

| Inorganic Amendments |

| Biological/Microbial Amendments |

| Solid |

| Liquid |

| Agriculture |

| Horticulture and Turf |

| Environmental Remediation |

| Cereals and Grains |

| Fruits and Vegetables |

| Oilseeds and Pulses |

| Sand |

| Clay |

| Loam and Silt |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Kenya | |

| Rest of Africa |

| By Product Type | Organic Amendments | |

| Inorganic Amendments | ||

| Biological/Microbial Amendments | ||

| By Form | Solid | |

| Liquid | ||

| By Application | Agriculture | |

| Horticulture and Turf | ||

| Environmental Remediation | ||

| By Crop Type | Cereals and Grains | |

| Fruits and Vegetables | ||

| Oilseeds and Pulses | ||

| By Soil Type | Sand | |

| Clay | ||

| Loam and Silt | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the soil amendments market?

The soil amendments marker stands at USD 8.6 billion in 2025 and is projected to grow to USD 13.5 billion by 2030.

Which region is the largest market for soil amendments?

North America leads with 31% of 2024 revenue, underpinned by federal biochar funding and advanced precision-agronomy adoption.

Why is biochar gaining popularity in the soil amendments industry?

Biochar delivers soil-health benefits while enabling carbon-credit revenue streams, and voluntary carbon markets price verified removals at USD 190 per tonne.

What segment is growing fastest within the soil amendments market?

Biochar-based amendments are forecast to expand at a 12.4% CAGR, driven by regenerative agriculture programs and rising carbon-credit valuations.

How do super-absorbent polymers help farmers?

Hydrogel-based amendments cut irrigation needs by up to 85% in sandy soils, aiding water-stressed regions in meeting crop-yield goals.

Page last updated on: