North America Commercial LED Lighting Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

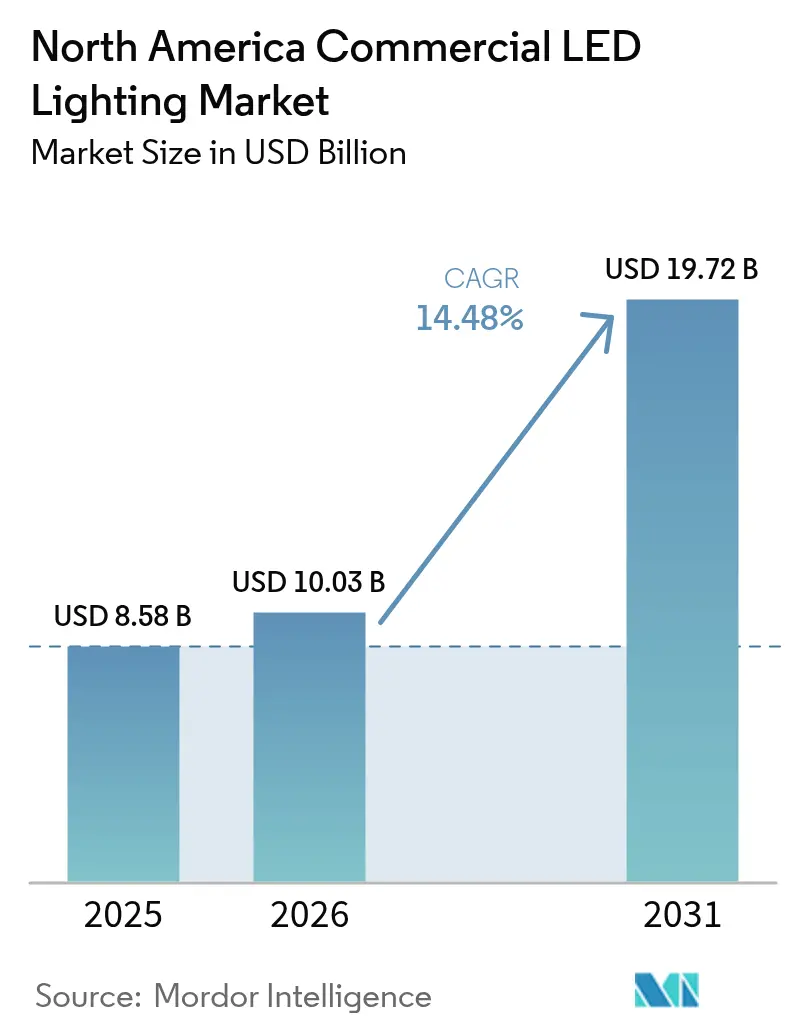

| Base Year Market Size (2025) | USD 8.58 Billion |

| Market Size (2026) | USD 10.03 Billion |

| Market Size (2031) | USD 19.72 Billion |

| Growth Rate (2026 - 2032) | 14.48% CAGR |

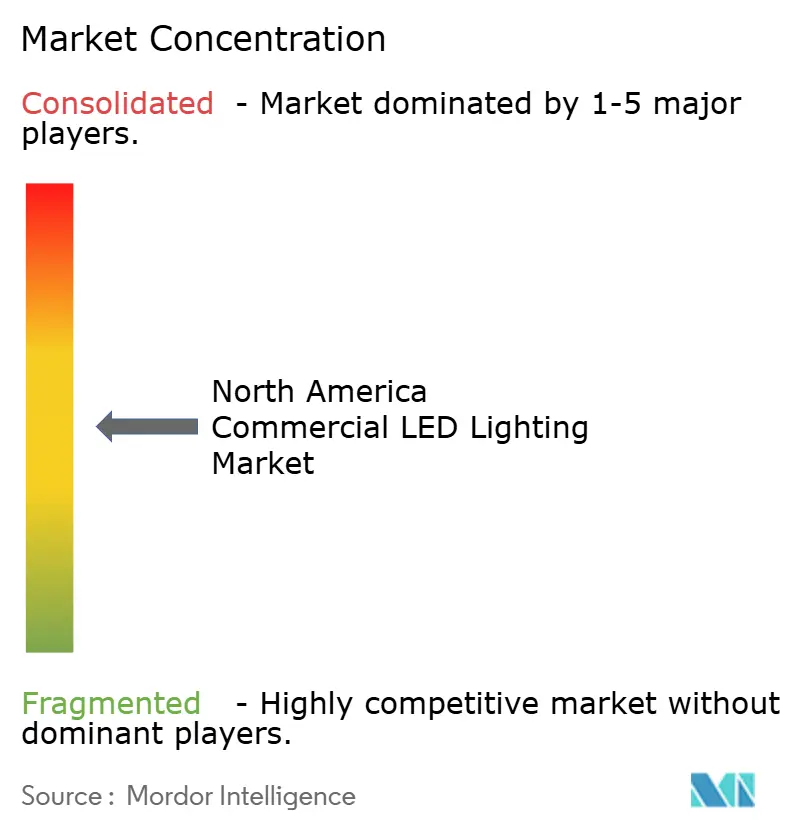

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Commercial LED Lighting Market Analysis by Mordor Intelligence

The North America commercial LED lighting market size is projected to expand from USD 8.58 billion in 2025 and USD 10.03 billion in 2026 to USD 19.72 billion by 2031, registering a CAGR of 14.48% between 2026 and 2031. Regulatory pressure, corporate decarbonization programs, and the growing role of connected luminaires are reshaping procurement decisions across offices, factories, and vertical farms. Vendors now differentiate through integrated controls, data analytics, and Lighting-as-a-Service contracts rather than through hardware efficiency alone. Tariff realignments under the United States-Mexico-Canada Agreement encourage regional manufacturing, while component shortages and interoperability hurdles complicate rollouts. Overall, retrofit demand dominates as roughly 1 billion fluorescent fixtures remain in service across the region.

Key Report Takeaways

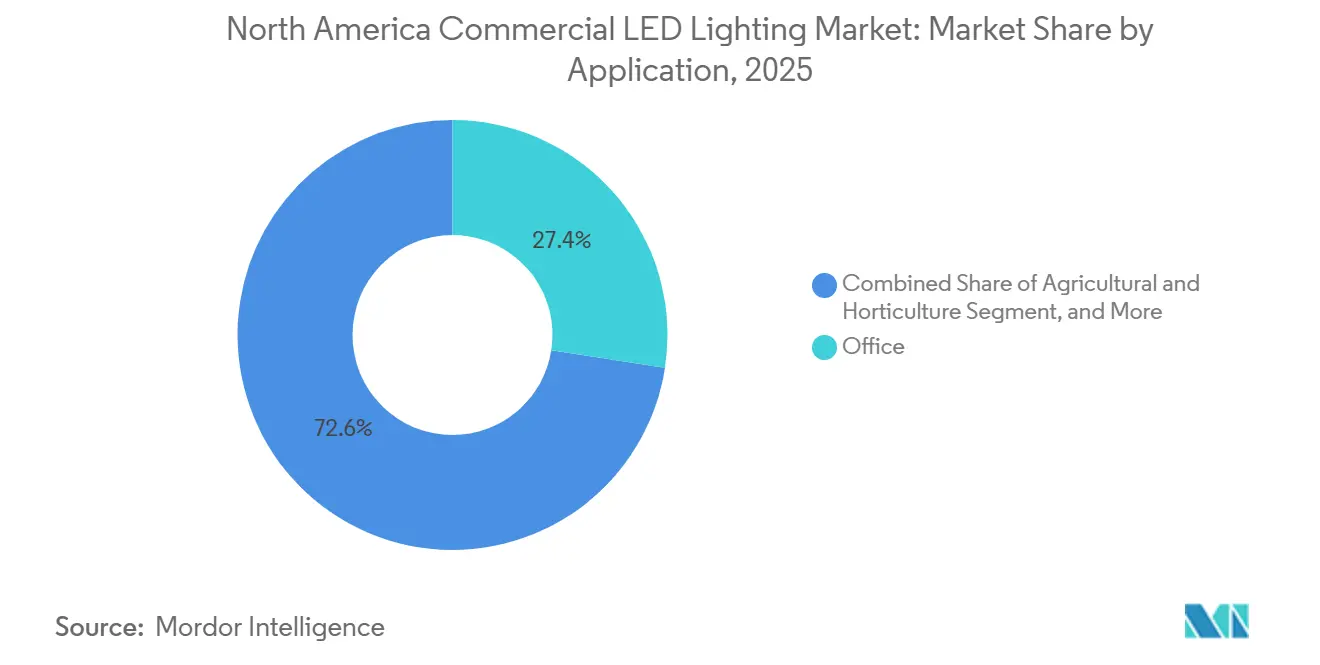

- By application, office spaces led with 27.43% revenue share in 2025, whereas agricultural and horticulture lighting is poised to post the fastest 14.89% CAGR through 2031.

- By form factor, troffers commanded 23.17% revenue share in 2025, while track lights are on track for the highest 14.94% CAGR over 2026-2031.

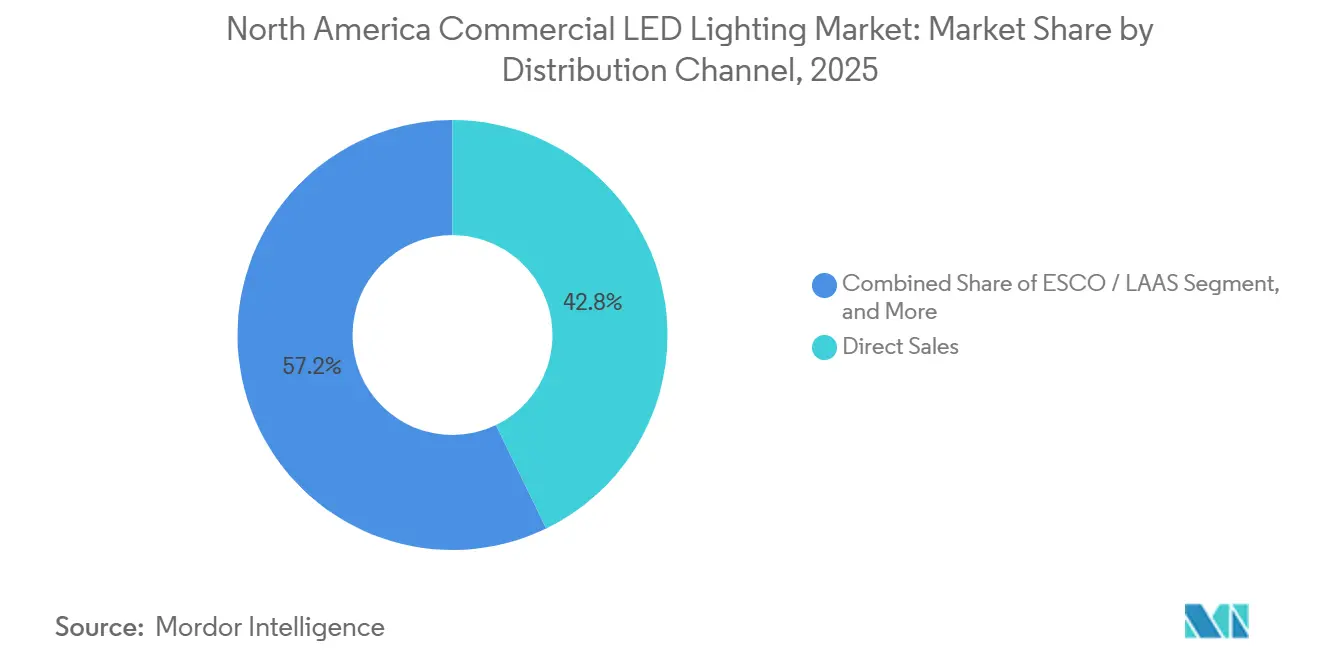

- By distribution channel, direct sales represented 42.82% of 2025 turnover, whereas Energy Service Company and Lighting-as-a-Service providers are forecast to expand at a 15.23% CAGR between 2026 and 2031.

- By installation type, retrofit projects generated 64.53% of 2025 spending and are projected to grow at a 15.04% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Commercial LED Lighting Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Energy-Efficiency Regulations and Building Codes | +2.10% | United States, Canada (provincial codes), Mexico (NOM standards) | Medium term (2-4 years) |

| Declining LED Luminaire Prices and Total Cost-of-Ownership Advantage | +1.80% | North America-wide | Short term (≤ 2 years) |

| Growth of Smart, Connected and IoT-Enabled Lighting Systems | +2.30% | United States (major metros), Canada (Toronto, Vancouver), Mexico (industrial corridors) | Medium term (2-4 years) |

| Shift Toward Human-Centric and Wellness-Focused Lighting in Workplaces | +1.40% | United States, Canada (office-dense cities) | Medium term (2-4 years) |

| Corporate Net-Zero and ESG Targets Accelerating Retrofit Demand | +2.00% | United States, Canada (corporate headquarters clusters) | Short term (≤ 2 years) |

| Demand from Indoor Vertical Farming and Micro-Fulfillment Centers | +1.60% | United States (urban peripheries), Canada (Ontario, British Columbia) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Energy-Efficiency Regulations and Building Codes

New federal and provincial standards eliminate most legacy lamps, so owners replace fluorescents even when payback modelling is incomplete. U.S. rules finalized in 2024 ban halogen and incandescent options, while Canada’s 2025 code lifts minimum efficacy thresholds. Mexico’s NOM-030-ENER sets LED-equivalent baselines in public buildings. As catalogue lines for non-compliant products disappear, distributors standardize on LEDs, making code-driven conversions the default in healthcare and education.

Declining LED Luminaire Prices and Total-Cost-of-Ownership Advantage Accelerate Commercial Adoption

Rapid cost compression across LED packages and drivers lowers upfront fixture prices, enabling projects to justify payback periods shorter than two years in many commercial retrofits. Contemporary troffer designs deliver 110 lm/W efficacy 40% higher than fluorescent references, while extending rated life to roughly 85,000 hours; maintenance cycles drop proportionally, cutting operating expenses for facility managers.[1]Michael P. Weinold et al., “Rapid Technological Progress in White Light-Emitting Diodes,” Nature Energy, nature.com High-bay conversions record energy savings of 50-70% in distribution centers, generating six-figure annual utility reductions in large venues. Utility incentives across multiple U.S. states further shave 10-15% from capital costs, tipping financing decisions decisively toward LED. Together, these economic levers reinforce the North America Commercial LED Lighting market’s momentum in the short term as payback math becomes compelling even for budget-constrained property owners.[2]Signify, “Q3 2025 Results,” signify.com

Growth of Smart, Connected, and IoT-Enabled Lighting Creates New Value Propositions

LED luminaires embedded with wireless radios, environmental sensors, and edge computing transform lighting grids into data backbones for smart buildings. Power-over-Ethernet architectures carry both energy and IP connectivity, allowing facilities to orchestrate occupancy-based dimming, indoor positioning, and space utilization analytics from a single dashboard. Case studies demonstrate energy savings well above 70% when advanced controls overlay standard LED efficiencies, driving the North America Commercial LED Lighting market toward holistic building-as-a-platform models. Vendors bundle software subscriptions that automate predictive maintenance and sustainability reporting, unlocking recurring revenue streams. Open-protocol ecosystems such as Bluetooth Mesh reduce vendor lock-in fears and accelerate specification uptake in new commercial developments.[3]Inside Lighting, “Mexico and Canada Mostly Escape New Tariff Hit,” insidelighting.com

Shift Toward Human-Centric and Wellness-Focused Lighting Drives Premium Segment Growth

Employers and property developers link lighting quality to occupant productivity and well-being, spurring adoption of circadian-tuned systems that modulate spectrum and intensity over the day. Studies reveal up to 12% uplift in task performance under biologically aligned illumination, enticing corporate tenants eager to draw employees back to offices post-pandemic. Healthcare providers implement tunable-white fixtures that support patient circadian rhythms, reporting improvements in recovery metrics and sleep quality. Educational institutions cite both visual-comfort gains and 40% energy reductions after classroom upgrades, reinforcing the dual economic and human-factor returns. Although premium pricing remains a barrier for value-oriented segments, wellness-focused solutions command higher margins and diversify vendor portfolios in the North America Commercial LED Lighting market.

As package commoditization intensifies, manufacturers are increasingly compelled to either scale up or bundle their software offerings to remain competitive. This trend is driven by the need to differentiate products in a market where price sensitivity and standardization are prevalent. Meanwhile, smaller distributors face mounting challenges from online competitors who provide direct-to-contractor pricing, offering convenience and cost savings to end users. This dynamic is accelerating a wave of consolidation within the industry, as smaller players struggle to maintain profitability and market share. A notable instance of this trend is Signify, whose declining margins highlight the growing pressures faced across the sector, reflecting the broader challenges of maintaining profitability amidst shifting market dynamics.

Restraints Impact Analysis*

| Restraint | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price erosion squeezing vendor margins | -1.80% | Entire region, strongest pressure on mid-tier firms | Short term (≤ 2 years) |

| High retrofit and installation costs in legacy facilities | -1.50% | Older commercial buildings across United States and Canada | Medium term (2-4 years) |

| Critical component shortages (drivers, ICs) | -1.20% | Global supply chain, regional impact | Short term (≤ 2 years) |

| Competition from OLED/micro-LED panels | -0.90% | Niche high-end U.S. projects | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price Erosion Squeezing Vendor Margins Intensifies Competitive Pressure

Commoditization in basic luminaires fuels downward price pressure, challenging manufacturers to protect profitability. Market leaders such as Signify and mid-tier brands alike witness share price volatility as investors question growth prospects amid falling average selling prices.. Acuity Brands counters the trend by prioritizing intelligent-spaces solutions, which expanded 16.7% in fiscal 2024 and lifted earnings per share 24.9% despite a topline dip. Smaller manufacturers lacking scale or specialization explore mergers or exit, accelerating consolidation within the North America Commercial LED Lighting market. Tariff uncertainty, especially proposals to levy 25% duties on Mexican-assembled luminaires, adds cost risk, complicating pricing strategies for vendors with cross-border supply chains.

High Retrofit and Installation Costs in Legacy Facilities Limit Market Penetration

Buildings constructed before 1990 frequently require panel upgrades, conduit installations, and ceiling reinforcements, leading to labor costs of USD 50-150 per fixture. These additional requirements can significantly increase the overall project budget, making upgrades more challenging for businesses operating on tight margins. Heritage restrictions on fixture selections further complicate the process, as they limit the available options and often necessitate custom solutions, which can extend project timelines. Furthermore, small businesses lacking dedicated facility teams often postpone these upgrades, even when the financial returns are appealing, due to the upfront costs, logistical challenges, and the absence of internal expertise to manage such projects effectively.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Agricultural Facilities Lead Growth

Agricultural and horticulture installations are forecast to grow fastest at a 14.89% CAGR, benefiting from spectrum-tuned fixtures that support vertical farms. This niche already shows 66% LED penetration, yet supplemented greenhouses remain largely untapped. Office installations, although holding 27.43% of 2025 revenue, slow as hybrid work reduces density. Healthcare and retail adopt high-CRI fixtures for patient comfort and merchandising, respectively. Industrial warehouses adopt high-bay LEDs topping 180 lumens per watt, while educational sites prioritize daylight harvesting to satisfy ASHRAE 90.1.

Niche segments such as architectural facades command premium rates for 3D-printed metal optics. Downstream, the North America commercial LED lighting market size for vertical farming is projected to rise rapidly, while offices maintain the largest North America commercial LED lighting market share through 2031.

By Form Factor: Track Lights Gain on Retail Demand

Track lights are set to post a 14.94% CAGR, propelled by museums and retailers needing beam flexibility and colour fidelity. Troffers, with 23.17% of 2025 revenue, continue large-scale replacements but see limited price upside. High-bay fixtures exceed 100,000 lumens for cold-storage; downlights tighten colour bins to half a MacAdam ellipse for uniform ceilings. Linear strips and suspended systems provide continuous-line aesthetics.

The North America commercial LED lighting market size for track lights will therefore widen, while troffers keep the highest North America commercial LED lighting market share based on installed base.

By Distribution Channel: Direct Sales Stability Coupled With ESCO Momentum

Energy Service Companies and LaaS providers are set to outpace other routes, reflecting a broader industry shift from capex to opex financing. This transition is driven by the increasing preference for operational flexibility and reduced upfront costs, which align with evolving customer demands and financial strategies.

Direct sales, driven by spec-focused projects, maintain dominance at 42.82%, as they cater to tailored requirements and ensure quality assurance for end-users. Meanwhile, wholesale distributors grapple with margin compression as e-commerce portals increasingly list commodity tubes and retrofit kits, intensifying price competition and reducing profitability. Although currently in the low teens, online channels are witnessing the fastest growth in unit volume, particularly for straightforward installations. This growth is fueled by the convenience, accessibility, and cost-effectiveness offered by online platforms, making them an attractive option for customers seeking simple and quick solutions.

By Installation Type: Retrofits Dominate

As about 1 billion fluorescent fixtures stand ready for replacement, retrofits account for 64.53% of spending in 2025 and maintain a robust 15.04% CAGR. These fixtures predominantly reside in older downtowns, where lighting power densities surpass contemporary standards, creating significant opportunities for energy savings and compliance with updated regulations. Retrofits are particularly appealing due to their cost-effectiveness and the ability to upgrade existing infrastructure without extensive modifications. While demand for new builds is modest, they incorporate advanced controls from the outset, such as smart lighting systems and IoT-enabled solutions, progressively closing performance gaps with retrofits. These advanced systems enhance energy efficiency, enable better monitoring, and support sustainability goals from the beginning of the building's lifecycle.

In the North American commercial LED lighting market, utility rebates and corporate ESG objectives play a pivotal role in driving adoption. Utility rebates reduce upfront costs, making LED solutions more accessible, while corporate ESG targets push businesses to adopt sustainable practices, including energy-efficient lighting. Together, these factors accelerate the adoption of LED lighting in both retrofit and new-build categories, contributing to the market's growth and alignment with environmental and regulatory standards.

Geography Analysis

The United States leads the North America commercial LED lighting market, supported by state codes that effectively mandate LED efficacy levels. Yet tariff surcharges on Chinese components raise cost pressure, while Mexican production enjoys USMCA exemptions. Energy Trust of Oregon and Oncor rebates offset initial costs, sustaining mid-market retrofits.

Canada follows with stringent provincial codes and performance-based utility incentives that reward sensor integration. Currency weakness trims reported vendor revenues, but joint purchasing by municipalities smooths demand. Vertical farming clusters around Ontario and British Columbia benefit from hydroelectric power pricing.

Mexico’s market, while smaller in absolute terms, grows through industrial corridor upgrades and NOM-030-ENER enforcement. Local factories supplying USMCA-compliant fixtures shorten lead times and sidestep U.S. tariffs, deepening cross-border integration. Collectively, these dynamics maintain steady expansion of the North America commercial LED lighting market.

Competitive Landscape

Signify, Acuity Brands, Hubbell, Cree Lighting, and Osram, the top five suppliers, command a share in the mid-40s, highlighting a moderate market concentration. These companies leverage their established market presence and extensive product portfolios to maintain their competitive edge. The remaining share is divided among regional specialists and emerging challengers, who often focus on niche applications or innovative technologies to differentiate themselves.

Acuity Brands' acquisition of QSC underscores its ambition for unified building platforms, aiming to integrate lighting with broader building management systems for enhanced operational efficiency. Meanwhile, Signify capitalizes on the familiarity of Philips Hue to promote its commercial Interact controls, targeting businesses seeking scalable and user-friendly lighting solutions. New entrants like Digital Lumens, with a focus on industrial applications, are utilizing wireless mesh sensing to gain traction in warehouse settings, offering solutions that enhance energy efficiency and operational insights. While support for open protocols like DALI-2 and Zigbee 3.0 is becoming a key driver in specifications, the presence of fragmented standards continues to escalate commissioning costs, posing challenges for seamless integration and adoption.

In North America, the commercial LED lighting market is shifting towards service-oriented revenues, with hardware fixtures serving as gateways to data analytics. This transition reflects the growing demand for smart lighting solutions that provide actionable insights and improve energy management. Vendors that blend robust manufacturing capabilities with comprehensive software ecosystems are poised to safeguard their margins amidst ongoing price pressures. Companies that can offer end-to-end solutions, combining high-quality hardware with advanced analytics and seamless integration, are better positioned to capture market share and address evolving customer needs in this competitive landscape.

North America Commercial LED Lighting Industry Leaders

Dialight PLC

OSRAM Licht AG

Signify Holding (Philips Lighting and Cooper Lighting)

US LED Limited

Hubbell Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Signify released Philips Hue Bridge Pro, raising device limits and processing speed to target light commercial deployments.

- September 2025: Feit Electric acquired Cree Lighting’s residential lamp brand, sharpening Cree’s focus on commercial fixtures.

- August 2025: Acuity Brands highlighted nine products in the 2025 IES Progress Report, including the REBL high bay at 186 lumens per watt.

- April 2025: The United States layered a 34% duty on Chinese lighting imports, while Mexico and Canada remained exempt under USMCA.

North America Commercial LED Lighting Market Report Scope

The North America Commercial LED Lighting Market Report is Segmented by Application (Retail Stores, Office, Hospitality, Architectural, Healthcare Facilities, Educational Institutions, Industrial and Warehouse, Outdoor Commercial, Agricultural and Horticulture), Form Factor (Troffers, Downlights, High-Bay, Track Lights, Suspended Pendants, Panel Lights, Linear Strips, Flood and Area Lights, Other Form Factors), Distribution Channel (Direct Sales, Retail/Wholesale, ESCO/Lighting-as-a-Service Providers, Online/E-Commerce), Installation Type (New Construction, Retrofit), and Geography (United States, Canada, Mexico). The Market Forecasts are Provided in Terms of Value (USD).

| Retail Stores (Showrooms, Malls, Shops) |

| Office |

| Hospitality (Restaurants, Casinos, Hotels) |

| Architectural (Decorative) |

| Healthcare Facilities |

| Educational Institutions |

| Industrial and Warehouse |

| Outdoor Commercial (Parking, Facades) |

| Agricultural and Horticulture (Vertical Farm) |

| Troffers |

| Downlights |

| High-Bay |

| Track Lights |

| Suspended Pendants |

| Panel Lights |

| Linear Strips |

| Flood and Area Lights |

| Other Form Factors |

| Direct Sales |

| Retail / Wholesale |

| ESCO / Lighting-as-a-Service Providers |

| Online / E-Commerce |

| New Construction |

| Retrofit |

| United States |

| Canada |

| Mexico |

| By Application | Retail Stores (Showrooms, Malls, Shops) |

| Office | |

| Hospitality (Restaurants, Casinos, Hotels) | |

| Architectural (Decorative) | |

| Healthcare Facilities | |

| Educational Institutions | |

| Industrial and Warehouse | |

| Outdoor Commercial (Parking, Facades) | |

| Agricultural and Horticulture (Vertical Farm) | |

| By Form Factor | Troffers |

| Downlights | |

| High-Bay | |

| Track Lights | |

| Suspended Pendants | |

| Panel Lights | |

| Linear Strips | |

| Flood and Area Lights | |

| Other Form Factors | |

| By Distribution Channel | Direct Sales |

| Retail / Wholesale | |

| ESCO / Lighting-as-a-Service Providers | |

| Online / E-Commerce | |

| By Installation Type | New Construction |

| Retrofit | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

What is the projected value of the North America commercial LED lighting market by 2031?

It is forecast to reach USD 19.72 billion by 2031.

How fast is the market expected to grow between 2026 and 2031?

It is set to register a 14.48% CAGR during the 2026-2031 period.

Which application segment is anticipated to expand the quickest through 2031?

Agricultural and horticulture lighting is projected to grow at a 14.89% CAGR.

Which form factor currently generates the largest revenue share?

Troffers held the top share at 23.17% of 2025 revenue.

Why are Lighting-as-a-Service providers gaining traction?

They let building owners shift upgrades from capital to operating expenses, and this channel is forecast to grow at a 15.23% CAGR through 2031.

What drives the dominance of retrofit projects?

About 1 billion fluorescent fixtures still in use create a large replacement pool, pushing retrofits to 64.53% of 2025 spending and a forecast 15.04% CAGR through 2031.

Page last updated on: