Metal Furniture Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 193.83 Billion |

| Market Size (2031) | USD 243.63 Billion |

| Growth Rate (2026 - 2031) | 4.68% CAGR |

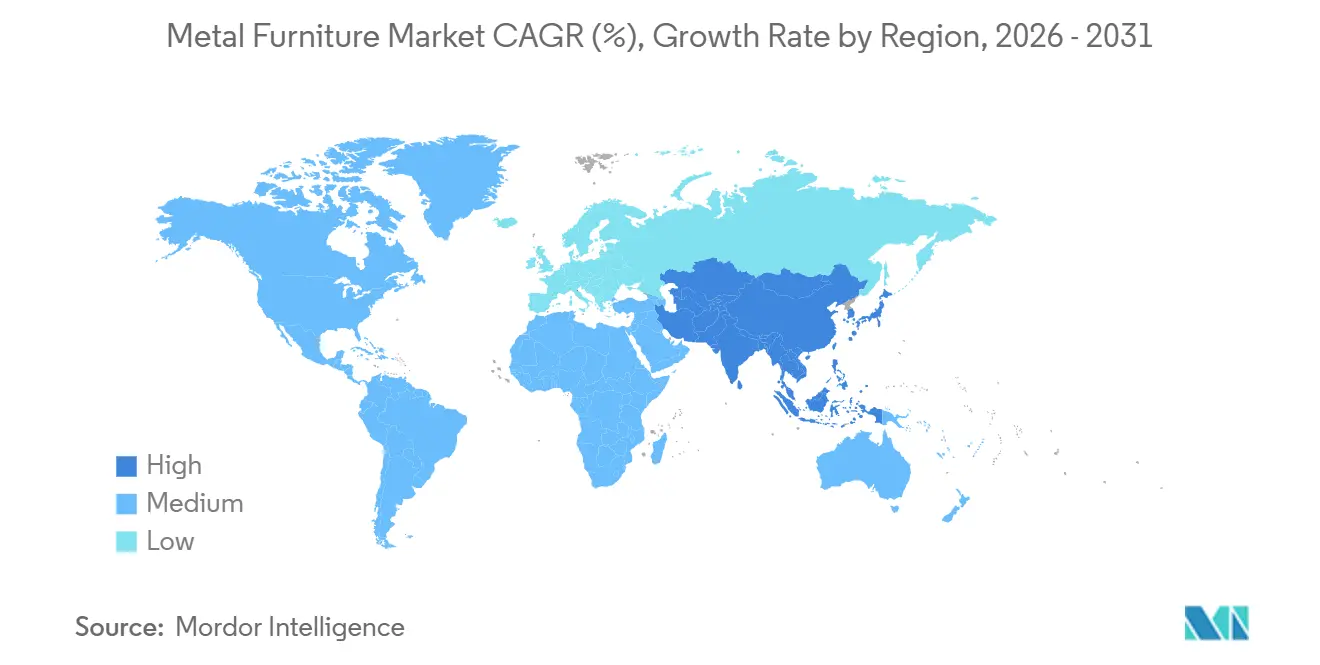

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

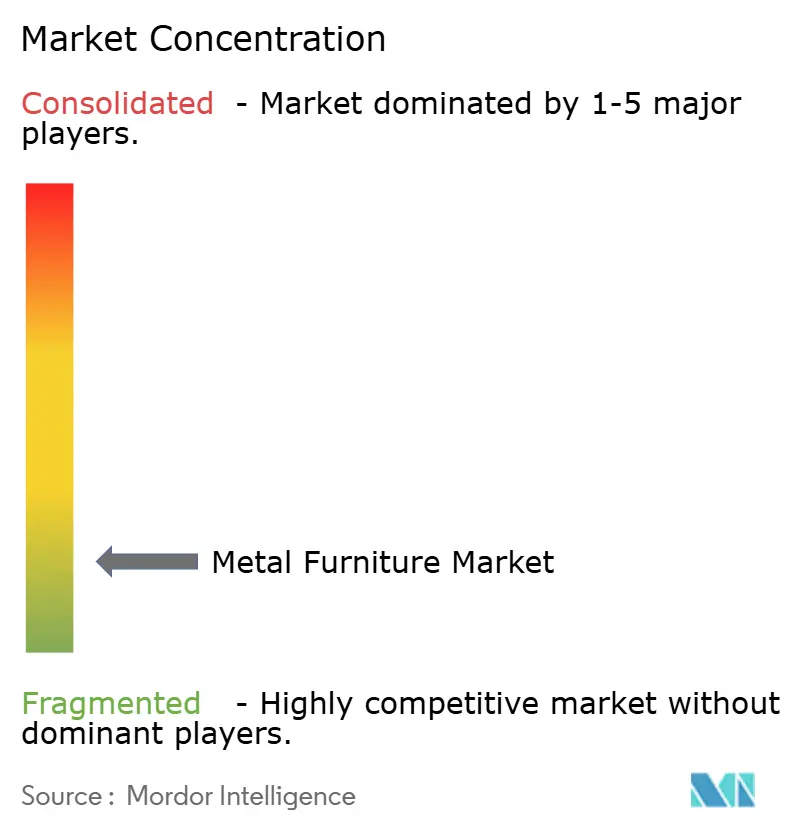

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Metal Furniture Market Analysis by Mordor Intelligence

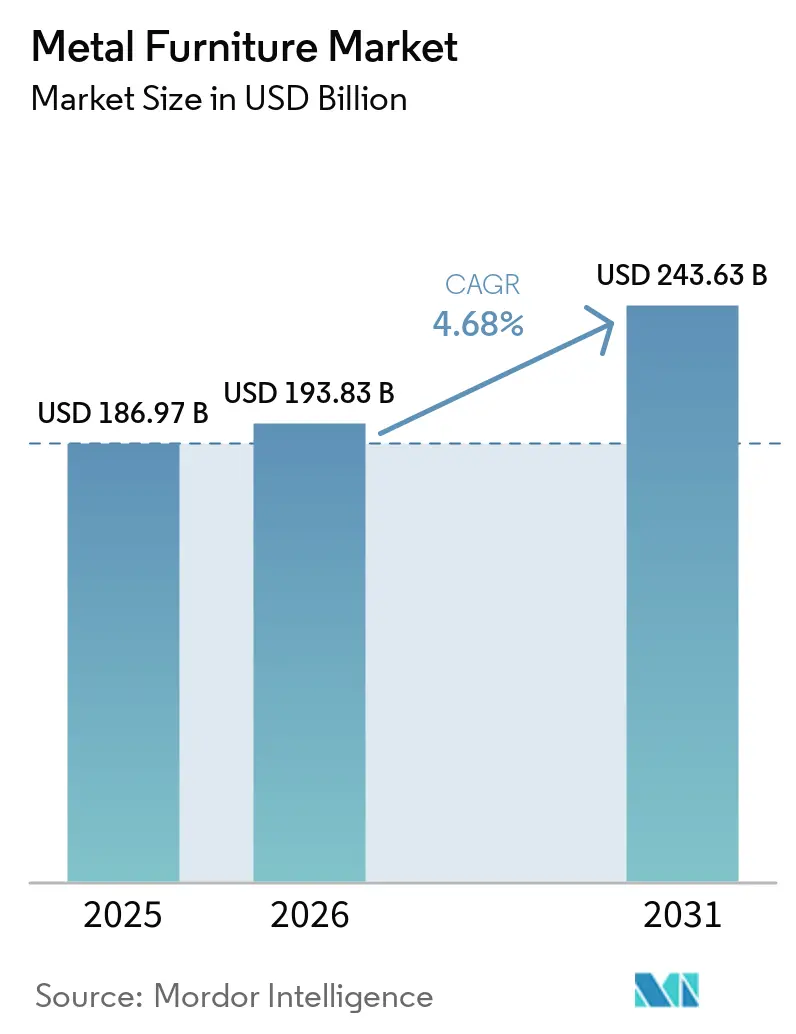

The metal furniture market size is projected to expand from USD 186.97 billion in 2025 and USD 193.83 billion in 2026 to USD 243.63 billion by 2031, registering a CAGR of 4.68% between 2026 and 2031. The metal furniture market is moving away from commodity output toward value-added categories tied to commercial fit-outs, outdoor living demand, and institutional procurement. This shift is supported by metal’s longer service life, easier cleaning, and stronger recyclability profile in high-traffic settings where buyers place more weight on lifecycle performance than upfront price. The metal furniture market also remains highly fragmented, which keeps price competition active, but it still leaves room for specification-led differentiation at the premium end. The December 2025 HNI Corporation and Steelcase combination changed the competitive balance in workplace furniture, while EU carbon-related import costs that became financially binding from January 2026 are already influencing sourcing, steel choice, and regional supply-chain planning[1]HNI Corporation, “HNI Corporation Completes Acquisition of Steelcase Inc.,” Steelcase Newsroom, steelcase.com. Material cost volatility remains the most immediate pressure point, especially for mid-tier producers that lack long-term contracts or vertically integrated logistics. At the same time, larger operators with tighter supply-chain control are better placed to absorb sudden swings in steel, aluminum, and energy costs.

Key Report Takeaways

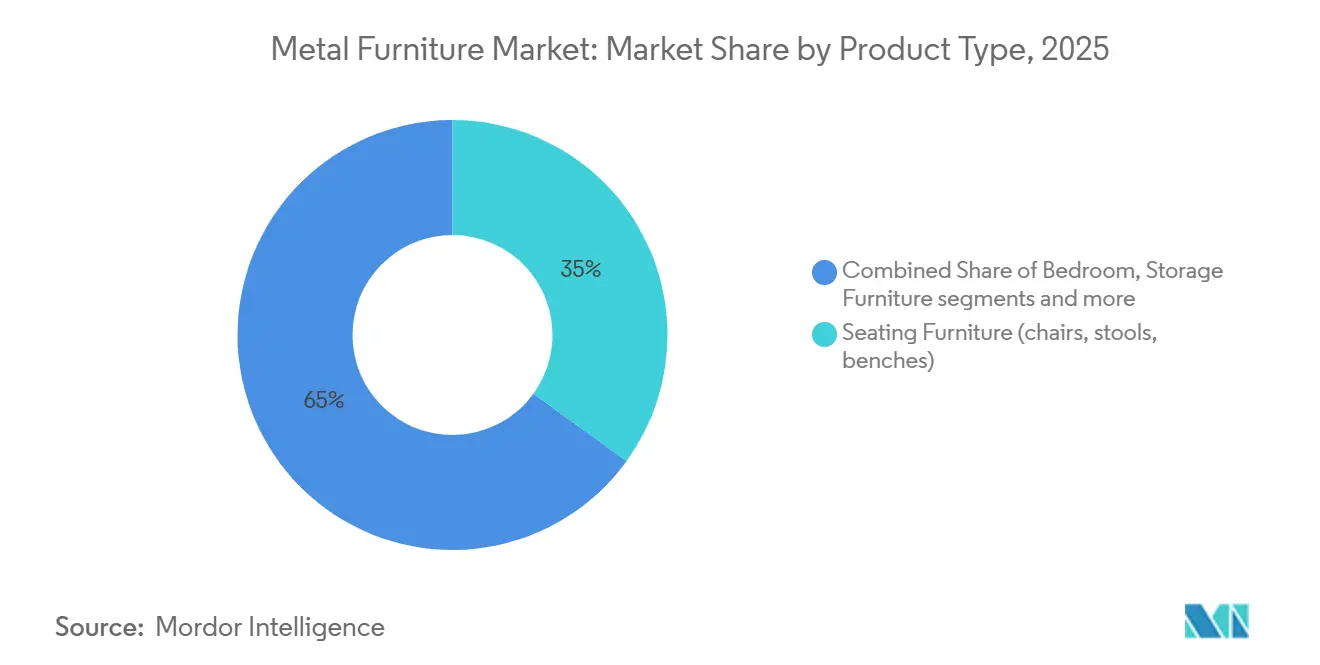

- By product type, seating furniture led with 35.00% of the metal furniture market share in 2025, while upholstered metal furniture is projected to expand at a 6.56% CAGR through 2031.

- By material type, steel held 48.21% of the metal furniture market share in 2025, whereas aluminum is forecast to grow at a 5.35% CAGR through 2031.

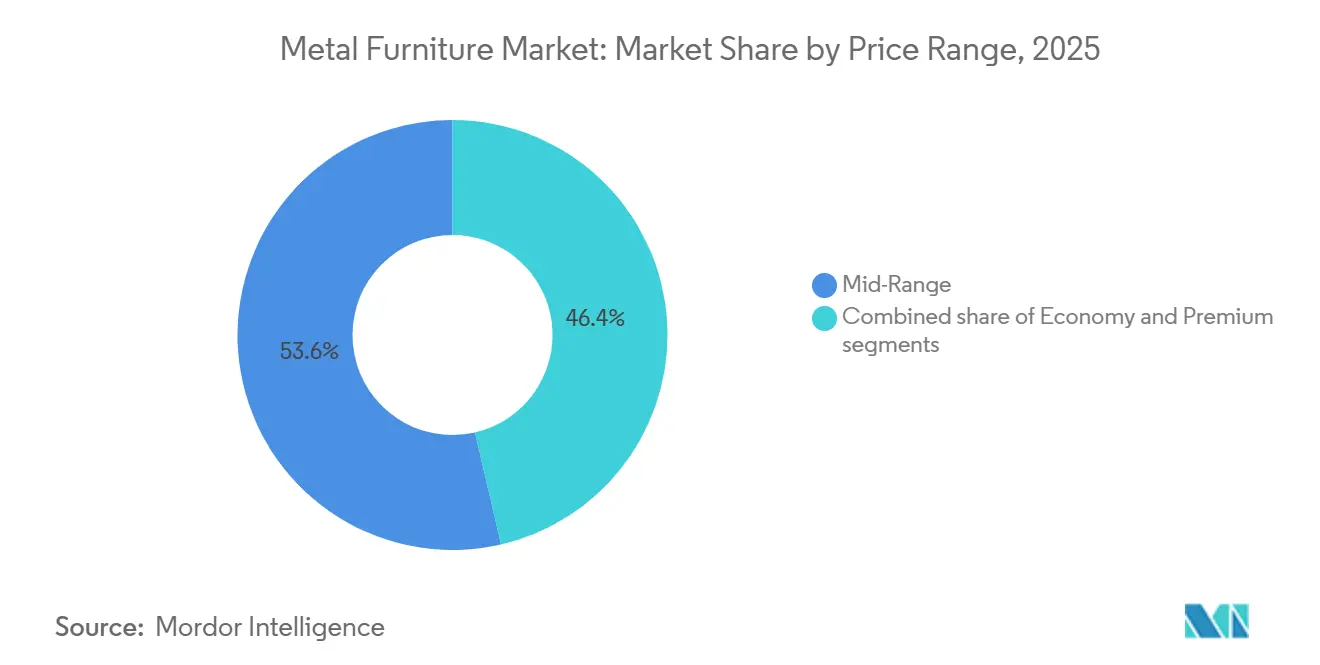

- By price range, mid-range furniture accounted for 53.62% of the metal furniture market share in 2025, while premium furniture is projected to advance at a 6.45% CAGR through 2031.

- By end-user, residential accounted for 68.95% of the metal furniture market share in 2025, whereas commercial is forecast to grow at a 4.98% CAGR through 2031.

- By distribution channel, B2C/Retail represented 72.52% of the metal furniture market share in 2025, while B2B/Project is projected to expand at a 7.01% CAGR through 2031.

- By geography, Asia-Pacific held 40.11% of the metal furniture market share in 2025 and is also forecast to register the fastest growth at a 5.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Metal Furniture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating Furniture E-Commerce Adoption For Metal SKUs | +0.6% | Global, concentrated in North America, China, and Europe | Short term (≤ 2 years) |

| Asia-Pacific Scale And Export Leadership | +0.7% | Asia-Pacific core, with spillover to North America and Europe | Long term (≥ 4 years) |

| Institutional And Commercial Refurbishments Favor Durable Metal Forms | +0.6% | North America and Europe, with Asia-Pacific growing | Medium term (2-4 years) |

| Advances In Powder Coating And Corrosion Protection | +0.4% | Global, especially Southeast Asia, the Middle East, and coastal North America | Medium term (2-4 years) |

| EU CBAM 2026 Encourages Low-Carbon Metal Sourcing | +0.3% | EU directly, with Turkey, India, and Vietnam upstream | Short term (≤ 2 years) |

| AD And CVD Actions On Chinese Metal Cabinets Diversify Supply | +0.2% | North America primarily, with Mexico, Vietnam, and India secondary | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerating Furniture E-Commerce Adoption For Metal SKUs

Online channels are changing how buyers discover, compare, and purchase metal furniture across residential categories. E-commerce for furniture and home furnishings in the United States has consistently outperformed the broader e-commerce market. Digital transactions have become a significant part of furniture purchases in the country. This matters for the metal furniture market because flat-pack and knocked-down formats fit better with digital retail economics than many assembled alternatives. Metal products shipped in compact cartons can reduce freight costs, warehousing pressure, and the risk of delivery damage when packaging is well designed. Visualization tools such as 3D configuration and room preview are also helping buyers judge scale and placement more accurately before checkout. At the same time, the channel still works best for manufacturers that can manage the difficult last mile for bulky items without eroding online margins.

Asia-Pacific Scale And Export Leadership

Asia-Pacific provides the metal furniture market with its strongest cost and supply base, as the region combines scale manufacturing, dense supplier networks, and export capacity. In 2024, furniture exports from China demonstrated the country's significant role in global trade and production. That export depth shortens lead times for buyers and allows large producers to spread tooling, finishing, and logistics costs across high output volumes. Vietnam has become a primary global furniture production hub, reporting approximately USD 17.3 billion in furniture exports in 2025 and directing over 55% of its output to the US market alone, with EVFTA-driven tariff reductions simultaneously expanding European buyer access[2]Vietnam Furniture Association, “Furniture Manufacturing in Vietnam: Opportunities, Trends, and Investment Guide 2025–2030,” Vietnam Furniture Association, Vietnam. incorp. asia. The result is a price floor that shapes how producers in North America and Europe position mid-range and contract product lines. The same regional strength also supports China+1 diversification because buyers can shift selected programs within Asia without losing access to established component and finishing ecosystems. Over time, that combination of domestic demand and export resilience should keep Asia-Pacific at the center of the metal furniture market even as sourcing becomes more distributed.

Institutional And Commercial Refurbishments Favor Durable Metal Forms

Commercial refurbishment cycles are supporting the metal furniture market, as institutional buyers continue to favor products that withstand repeated use and cleaning. The business and institutional furniture segment in North America returned to growth, supported by replacement activity and office upgrades rather than pure new construction[3]Business and Institutional Furniture Manufacturers Association, “North America Business and Institutional Furniture Market Size,” BIFMA, bifma.org. Metal performs well in hotels, hospitals, airports, schools, and offices because it combines structural durability with surface properties that are easier to maintain in high-touch environments. This preference is growing as buyers focus more on the total cost of ownership, warranty exposure, and long replacement intervals. Smaller firms also benefit from expensing rules that keep furniture upgrades financially manageable, which helps sustain steady mid-market contract demand, according to BIFMA. Another important shift is that tenders increasingly require environmental and indoor-use documentation, which tends to favor metal over chemically treated substitutes when compliance paperwork becomes part of the purchase decision.

Advances In Powder Coating And Corrosion Protection

Advances in protective finishes are expanding the use cases for metal furniture in outdoor and coastal settings. Improved powder-coating systems and corrosion-protection standards now give buyers a clearer compliance framework when they specify products for humid, marine, and high-UV environments[4]IGP Powder Coatings, “IGP-KORROPRIMER Brochure,” IGP Powder Coatings, igp-powder.com. This is important because outdoor hospitality, resort, marina, and terrace projects were historically more cautious about metal, given salt exposure and color fade that increased the risk of early replacement. Better coatings improve durability, color retention, and corrosion resistance, which reduces warranty concerns for both suppliers and procurement teams. The shift also helps metal compete more directly with teak, synthetic rattan, and other outdoor materials in premium specifications. As those performance concerns become easier to verify through certification and testing, the addressable market for outdoor metal programs continues to expand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Steel/Aluminum and Energy Price Volatility Squeezes Margins and Pricing | -0.7% | Global | Short term (≤ 2 years) |

| Bulky Last‑mile, Reverse Logistics and High Return Costs Limit Online Penetration | -0.4% | North America, Europe, and emerging Asia-Pacific e-commerce corridors | Medium term (2-4 years) |

| Coastal Corrosion Risk Without Robust Coatings | -0.2% | Southeast Asia, the Middle East, and coastal North America | Medium term (2-4 years) |

| CBAM And Emissions Data Compliance Burdens | -0.2% | Europe, Turkey, India, and Vietnam | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Steel/Aluminum and Energy Price Volatility Squeezes Margins and Pricing

Raw material inflation is the clearest near-term restraint on the metal furniture market, as steel and aluminum prices move quickly when energy or trade conditions change. EU carbon border costs became financially binding from January 2026, and CBAM certificate prices ranged from EUR 65 to 90 per tonne CO2e, equivalent to USD 70.2 to 97.2 per tonne CO2e at a 2026 average conversion rate of 1. Those added costs raise the delivered price of EU-bound steel and aluminum and tighten margins for manufacturers that cannot reprice quickly. Trade actions and tariff structures in North America add another layer of cost uncertainty for producers that depend on imported metal inputs. Large contract buyers often cap price pass-through in multi-year agreements, so part of the commodity risk stays with the manufacturer rather than the customer. That pressure is hardest on mid-sized firms in the metal furniture industry that lack hedging capacity, regional scale, or integrated procurement control.

Bulky Last‑mile, Reverse Logistics and High Return Costs Limit Online Penetration

Bulky product economics still limit how far digital expansion can go in the metal furniture market, even when online demand remains strong. Large-item returns can cost USD 300 to USD 1,500 per trip, exceeding the furniture's resale value and turning a successful sale into a loss when delivery or fit issues arise. Metal products often require scheduled delivery windows, two-person handling, stair navigation, and damage-free placement, all of which add cost beyond standard parcel models. Buyers also cannot fully judge finish, weight, and physical presence through a screen, which keeps mismatch risk elevated despite better visualization tools. Reverse logistics becomes especially expensive when an item is large, assembled, or difficult to repack after inspection. This makes dense store networks, regional warehouses, and click-and-collect capabilities more valuable than pure online reach for furniture sellers that want to scale profitably.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Seating Dominates, Upholstered Metal Gains Specification Share

Seating Furniture held 35% of the metal furniture market share in 2025, which kept it ahead of every other product group on a revenue basis. Chairs, stools, and benches appear across residential, hospitality, foodservice, workplace, and public-space settings, so no other category matches their volume base. That cross-channel breadth helps the metal furniture market maintain stable demand even when one end-use vertical slows. Seating also benefits from a wide spread of ticket prices, from mass-market household products to commercial seating built for continuous use. This broad functional reach keeps the segment central to both B2C volume and B2B project specifications.

Upholstered Metal Furniture is projected to expand at a 6.56% CAGR through 2031, making it the fastest-growing product subcategory in the metal furniture market. Growth reflects a clear shift toward soft seating that combines the strength of a metal frame with the comfort of lounge, hospitality, and premium residential environments. Metal-framed upholstered products are gaining acceptance in airport lounges, coworking spaces, and boutique hospitality interiors where fire-code compliance and heavy-duty use both matter. That change shows that metal is moving into applications once dominated by wood-based construction. Storage furniture remains important, as trade protection helps North American suppliers stay competitive in metal cabinets and filing systems, while outdoor metal furniture benefits from better coatings that reduce corrosion concerns.

By Material Type: Steel's Mass Position Challenged by Aluminum's Value Expansion

Steel, including stainless steel, accounted for 48.21% of revenue in 2025 and remained the core material base for the metal furniture market. Its position rests on a strong balance between strength and cost across seating, storage, tables, and structural components. Steel also remains hard to replace in office and storage applications, where weld integrity, load-bearing capacity, and dimensional consistency are essential. Stainless grades retain a particular advantage in healthcare and food-service environments because their surfaces are non-porous and easier to sanitize. That means steel should remain the anchor material across many large-volume applications during the forecast period.

Aluminum is projected to grow at a 5.35% CAGR through 2031, which makes it the fastest-expanding material segment in the metal furniture market. Its value lies in lower weight, natural corrosion resistance, and design flexibility in outdoor and mobility-oriented products. These features support premium outdoor seating, terrace systems, and collections that need easier handling without sacrificing visual quality. Aluminum also fits product categories where transport efficiency and assembly convenience shape buyer preference. Even so, the economics of steel will continue to matter most in cost-sensitive categories, especially as CBAM and other carbon-linked rules start to reshape procurement choices for EU-facing manufacturers.

By Price Range: Mid-Range Maintains Volume, Premium Registers Strategy-Grade Growth

Mid-Range accounted for 53.62% of revenue in 2025, making it the largest price tier in the metal furniture market. This segment benefits from wide availability across residential and light-commercial channels where buyers want durability but still watch affordability closely. Mass retail and omnichannel sellers have built strong reach in this range, helping maintain high volume. The category also works well for standardized product programs where efficient sourcing and packaging can preserve margins. As a result, mid-range remains the core volume engine even while the market becomes more segmented by design, finish, and compliance requirements.

Premium is forecast to expand at a 6.45% CAGR through 2031, showing that buyers are trading up when design quality and lifecycle value are clear. In hospitality and higher-end contract settings, buyers are increasingly willing to pay more for aluminum or stainless collections with stronger coating, sustainability, or certification credentials. The metal furniture industry is also seeing premium brands defend pricing through material innovation and modularity rather than sheer scale. USM’s January 2026 launch of Soft Panels for its classic modular steel system is one example of how premium suppliers are using product updates to keep long-standing ranges commercially fresh. Economy products still serve cost-sensitive institutional demand, but they face substitution pressure when lowest-price procurement favors molded plastic or composite alternatives over metal.

By End-User: Residential Scale Coexists with Commercial Momentum

Residential end-users accounted for 68.95% of revenue in 2025, which made households the largest demand base for the metal furniture market. The scale reflects metal’s broad role in bedrooms, balconies, gardens, storage areas, dining spaces, and compact urban homes. Residential demand also benefits from household formation, apartment living, and the appeal of durable products for indoor and semi-outdoor use. In high-density cities, metal furniture fits the need for compact, practical, and easy-to-maintain pieces. China’s urbanization path continues to support that pattern as urban living expands and space-efficient products remain relevant.

Commercial is projected to grow at a 4.98% CAGR through 2031, making it the fastest-growing end-user segment in the metal furniture market. Demand is coming from office upgrades, healthcare investment, hospitality renovation, and other replacement-led procurement cycles. In North America, contract demand has been supported by a broader recovery in business and institutional furniture orders, rather than a single narrow vertical. MillerKnoll’s Q3 FY2026 results also pointed to continuing order growth in contract activity, which supports the wider pattern of commercial recovery. Buyers in these segments place high value on cleanability, wear resistance, and documented compliance, which continues to favor metal in institutional specifications.

By Distribution Channel: B2C Infrastructure Holds Volume, B2B Captures Value Growth

B2C/Retail accounted for 72.52% of revenue in 2025, making it the largest distribution channel for the metal furniture market. Home centers, specialty stores, franchise furniture chains, and online storefronts all support this broad channel base. The segment holds volume because it addresses everyday household replacement and furnishing needs across multiple price points. Large omnichannel networks also make it easier to combine in-store discovery with digital ordering and local pickup. IKEA’s United States expansion plan for 2026 shows how physical footprints still matter when furniture sellers want to improve convenience and fulfillment efficiency.

B2B/Project is forecast to grow at a 7.01% CAGR through 2031, which marks it as the fastest-moving channel in the metal furniture market. That pace reflects the larger order sizes and stronger margins of hospitality, healthcare, workplace, and institutional contracts. Digital tendering and specification tools are also making contract buying easier for smaller organizations that once relied on retail channels. Supplier relationships matter more here because documentation, installation, project timing, and after-sales support all influence contract awards. KOKUYO and Lamex reinforced this direction at the China International Furniture Fair in March 2026 by pairing product launches with a workplace white paper that supports a more consultative B2B sales model.

Geography Analysis

Asia-Pacific accounted for 40.11% of global revenue in 2025 and recorded the fastest regional CAGR of 5.12% through 2031, putting it in a rare position of leading both scale and growth. China remains the core production and consumption center for the metal furniture market across the region. It exported USD 36.44 billion in furniture in 2024, confirming the depth of its manufacturing ecosystem and export reach. CNFA trade data also showed continued momentum in China’s furniture trade with ASEAN in 2025, supporting the view that regional supply chains are becoming more interconnected rather than less. This gives Asia-Pacific a strong mix of domestic consumption, export scale, and flexible sourcing options for global buyers.

India is expected to remain one of the key growth markets within Asia-Pacific as urban housing demand, modern retail, and project activity widen the addressable customer base. Southeast Asia also matters more to the metal furniture market because it offers both consumption growth and alternative manufacturing capacity for global sourcing programs. Vietnam continues to benefit from China+1 supply diversification, even though the stronger point is not only export growth, but its deeper integration into premium buyer programs. North America remains the leading center for premium-specification contract metal furniture, where office, healthcare, and institutional replacement demand continues to support it. The December 2025 HNI and Steelcase combination created a pro forma revenue entity of USD 5.8 billion, strengthening scale at the upper end of the workplace furniture market in the region. BIFMA data and company commentary also suggest that retrofit and ergonomic upgrades are more important today than greenfield office build-outs, which keeps replacement demand active.

Europe remains important for premium design, institutional purchasing, and outdoor applications, but carbon-linked import costs are reshaping sourcing decisions. From January 2026, steel and aluminum importers into the EU have had to account for CBAM certificate purchases tied to EU ETS prices, which directly affect delivered cost structures. This gives lower-emission upstream producers a clearer route to competitiveness in EU-bound supply chains. The Middle East, Africa, and South America remain smaller today, but all act as frontier growth zones for the metal furniture market. In the Middle East, hospitality and commercial projects in the UAE and Saudi Arabia support durable contract demand. At the same time, in South America, opportunities are tied more to urban residential growth, retail expansion, and local fabrication potential. These regions still face logistics and import-cost constraints, which is why local and regional manufacturing can become more important than brand visibility alone over time.

Competitive Landscape

The metal furniture market remains extremely fragmented, which keeps its structure very different from categories dominated by a few global leaders. The largest companies have scale in office, storage, or branded retail, but the wider market is still spread across many regional manufacturers, specialists, and custom fabricators. That fragmentation keeps price pressure high in mid-market categories and limits any single company's ability to dictate global terms. It also means that distribution reach, specification capability, and finishing quality often matter more than headline size in securing share.

The most important recent consolidation move was HNI Corporation's acquisition of Steelcase in December 2025, valued at approximately USD 2.2 billion. The combined entity had pro forma annual revenue of approximately USD 5.8 billion, strengthening scale in the workplace and contract segments. MillerKnoll has pursued a different path by operating a multi-brand structure that spreads exposure across contract, healthcare, and global retail channels rather than relying on a merger of a similar size. Bisley offers another example of strategic positioning through product capability, with BeSmart smart locking helping defend its steel storage portfolio through software-linked features rather than simple price competition. USM has taken a parallel route by adding recycled-content Soft Panels to its modular steel system, thereby extending the premium relevance without changing the core platform architecture.

Technology, documentation, and product development now clearly separate specification-grade suppliers from commodity producers. KOKUYO’s workplace positioning and product launches in 2025 and 2026 show how larger players are pairing furniture design with research-led commercial selling. White space remains strongest in South Asia, the Middle East, and parts of Africa, where service networks and procurement systems are still developing. That leaves room for regional challengers that combine local fabrication with direct B2B selling. It also means international firms cannot rely only on brand equity if they lack local delivery, installation, and maintenance capability. The metal furniture market, therefore, remains open to selective consolidation at the premium end, while the mid-market continues to reward operational discipline, regional responsiveness, and compliance readiness.

Metal Furniture Industry Leaders

Steelcase

MillerKnoll

HNI Corporation

IKEA

KOKUYO

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: At NeoCon 2026 in Chicago, Okamura introduced the Muku task chair, developed in collaboration with Foster + Partners Industrial Design. The chair includes a compact multi-axis adjustment mechanism made from aluminum and recycled nylon. It is intended for office, commercial, and home use, with a commercial release planned for November 2026. This collaboration reflects Okamura's focus on global contract specifications through partnerships with design houses.

- June 2026: IKEA opened its first dedicated product development center in Bengaluru, India. The facility is designed to accelerate the creation of metal and composite furniture tailored to Indian spatial, climatic, and cultural requirements. This initiative supports IKEA's expansion strategy in South Asia.

- May 2026: On May 1, 2026, KOKUYO moved its global headquarters to KOKUYO HQ at Grand Green Osaka. The facility functions as an open experimental workplace accessible to corporate customers and partner companies. This relocation aligns with KOKUYO's strategy to accelerate global growth, with a focus on the Kansai region.

- March 2026: Fermob presented its 2026 collection at Salone del Mobile. The collection includes the Rivage modular outdoor lounge system and the GOOSTO outdoor kitchen, both constructed from aluminum and HPL. A new solar floor lamp was also introduced. This collection highlights Fermob's expansion into outdoor culinary living and the integration of furniture for interior and exterior spaces.

Global Metal Furniture Market Report Scope

Metal furniture refers to furniture products manufactured primarily from metal materials such as steel, aluminum, wrought iron, cast iron, and other alloys. These products are valued for their durability, strength, low maintenance requirements, and suitability for both indoor and outdoor applications across residential and commercial settings. The metal furniture market is segmented by product type, material type, price range, end user, distribution channel, and geography. By product type, the market is segmented into seating furniture (chairs, stools, benches), bedroom furniture (beds, bunk beds), tables and desks, storage furniture (wardrobes, lockers, cabinets, shelving), upholstered metal furniture (sofas, loungers), and outdoor metal furniture. By material type, the market is segmented into steel (including stainless steel), aluminum, wrought/cast iron, and other alloys. By price range, the market is segmented into economy, mid-range, and premium products. By end user, the market is segmented into residential and commercial. By distribution channel, the market is segmented into B2C/retail and B2B/project channels. The B2C/retail segment is further categorized into home centers, specialty furniture stores, online channels, local workshops, and other distribution channels. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. The report provides the market size in USD for all the above-mentioned segments.

| Seating Furniture (chairs, stools, benches) |

| Bedroom Furniture (beds, bunk beds) |

| Tables & Desks |

| Storage Furniture (wardrobes, lockers, cabinets, shelving) |

| Upholstered Metal Furniture (sofas, loungers) |

| Outdoor Metal Furniture |

| Steel (incl. stainless) |

| Aluminum |

| Wrought/Cast Iron |

| Other Alloys |

| Economy |

| Mid-Range |

| Premium |

| Residential |

| Commercial |

| B2C/Retail | Home Centers |

| Specialty Furniture Stores | |

| Online | |

| Local Workshops | |

| Other Distribution Channels | |

| B2B/Project |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and the Philippines) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of the Middle East and Africa |

| By Product Type | Seating Furniture (chairs, stools, benches) | |

| Bedroom Furniture (beds, bunk beds) | ||

| Tables & Desks | ||

| Storage Furniture (wardrobes, lockers, cabinets, shelving) | ||

| Upholstered Metal Furniture (sofas, loungers) | ||

| Outdoor Metal Furniture | ||

| By Material Type | Steel (incl. stainless) | |

| Aluminum | ||

| Wrought/Cast Iron | ||

| Other Alloys | ||

| By Price Range | Economy | |

| Mid-Range | ||

| Premium | ||

| By End User | Residential | |

| Commercial | ||

| By Distribution Channel | B2C/Retail | Home Centers |

| Specialty Furniture Stores | ||

| Online | ||

| Local Workshops | ||

| Other Distribution Channels | ||

| B2B/Project | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and the Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of the Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the metal furniture market by 2031?

The metal furniture market is forecast to reach USD 243.63 billion by 2031, rising from USD 193.83 billion in 2026 at a 4.68% CAGR.

Which product category leads global demand for metal furniture?

Seating Furniture led the market in 2025 with a 35% share because chairs, stools, and benches serve residential, hospitality, workplace, and public-space demand.

Which material is growing fastest in metal furniture applications?

Aluminum is the fastest-growing material segment, with a 5.35% CAGR through 2031, supported by lower weight and natural corrosion resistance.

Why is the Asia-Pacific so important for this space?

Asia-Pacific accounted for 40.11% of global revenue in 2025 and is also the fastest-growing region, with a 5.12% CAGR, supported by China’s export scale and deeper regional manufacturing.

What is driving growth in contract and project-based sales?

B2B or Project is forecast to grow at 7.01% CAGR through 2031 as hospitality, healthcare, workplace, and institutional buyers increase refurbishment-led procurement.

What is the biggest near-term risk for manufacturers?

Material and energy cost volatility remains the main risk, as steel and aluminum prices are affected by tariffs, energy price swings, and EU carbon-related import costs.

Page last updated on: