Metal Carboxylates Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

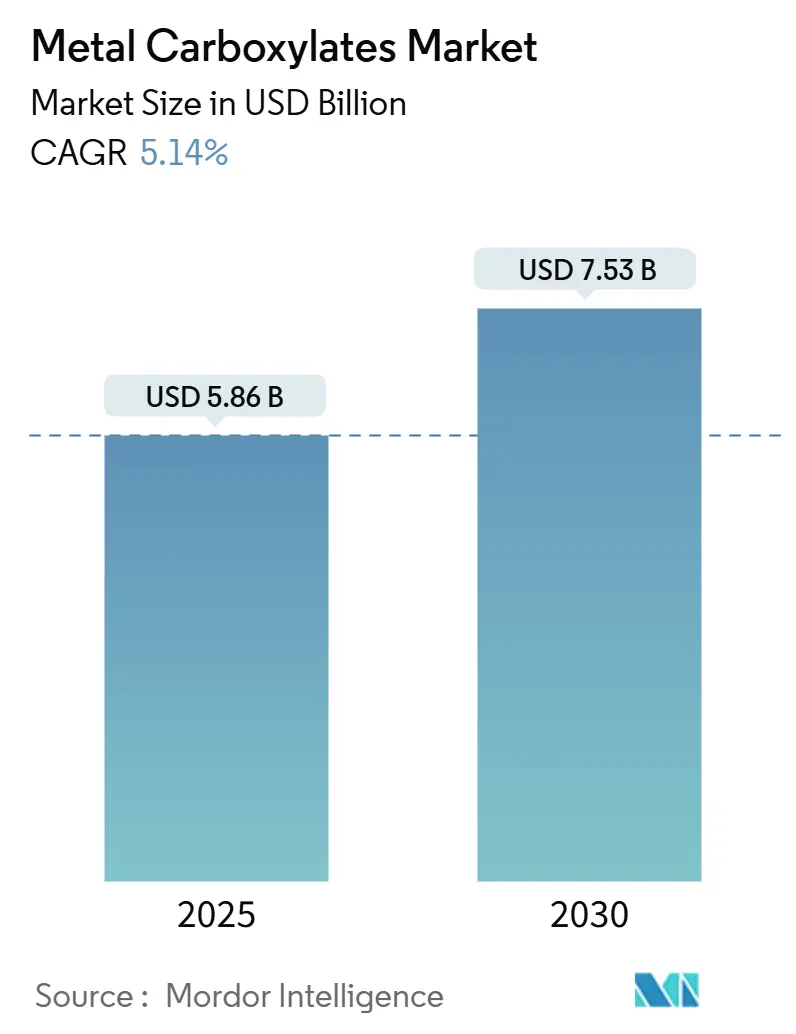

| Market Size (2025) | USD 5.86 Billion |

| Market Size (2030) | USD 7.53 Billion |

| Growth Rate (2025 - 2030) | 5.14% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Metal Carboxylates Market Analysis by Mordor Intelligence

The Metal Carboxylates Market size is estimated at USD 5.86 billion in 2025, and is expected to reach USD 7.53 billion by 2030, at a CAGR of 5.14% during the forecast period (2025-2030). This growth reflects the sector’s ability to substitute cobalt-based driers under tightening safety laws, meet rising construction-chemical demand, and support renewable-energy infrastructure through high-performance additives. Manufacturers gain from robust coatings consumption, an accelerating shift toward calcium and zinc stabilizers in PVC, and the rollout of manganese-based catalysts that balance performance with lower toxicity. Consolidation is unfolding as leading suppliers lock in fatty-acid and metal-oxide feedstocks, yet the market remains sufficiently fragmented to reward niche innovators. The Metal Carboxylates market continues to benefit from vertical integration strategies that secure raw material availability while enabling rapid response to regulatory change.

Key Report Takeaways

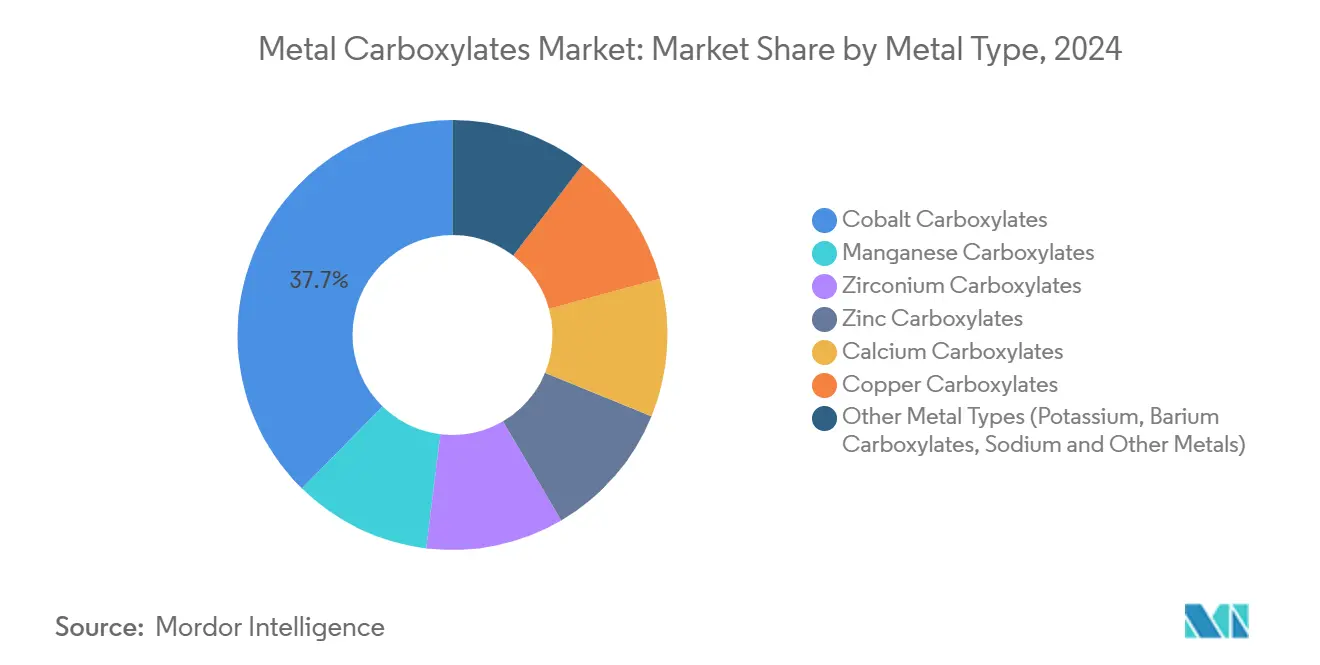

- By metal type, cobalt led with 37.65% of the Metal Carboxylates market share in 2024, while manganese is projected to expand at a 5.69% CAGR through 2030.

- By function, driers and catalysts accounted for 54.27% of the Metal Carboxylates market size in 2024 and corrosion inhibitors are advancing at a 5.84% CAGR to 2030.

- By application, paints and coatings held 46.24% revenue share in 2024; “other applications” are forecast to expand at 6.28% CAGR through 2030.

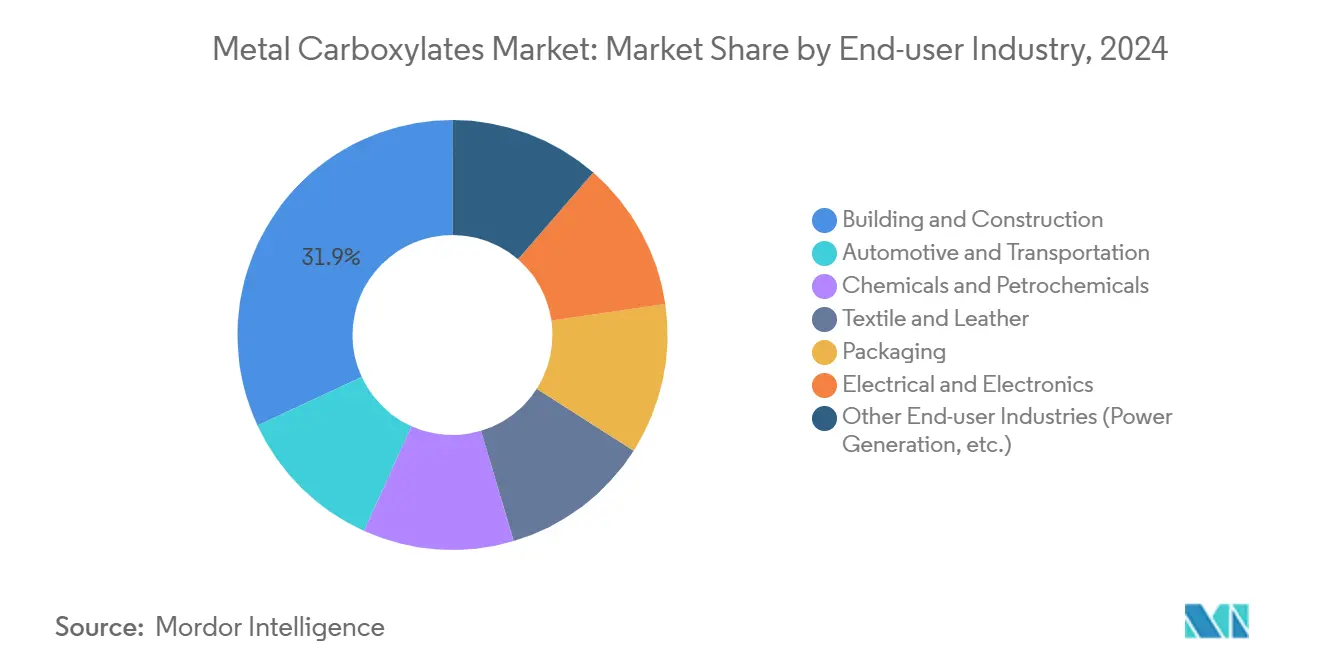

- By end-user industry, building and construction commanded 31.91% of demand in 2024 and electronics is growing fastest at a 6.27% CAGR over 2025-2030.

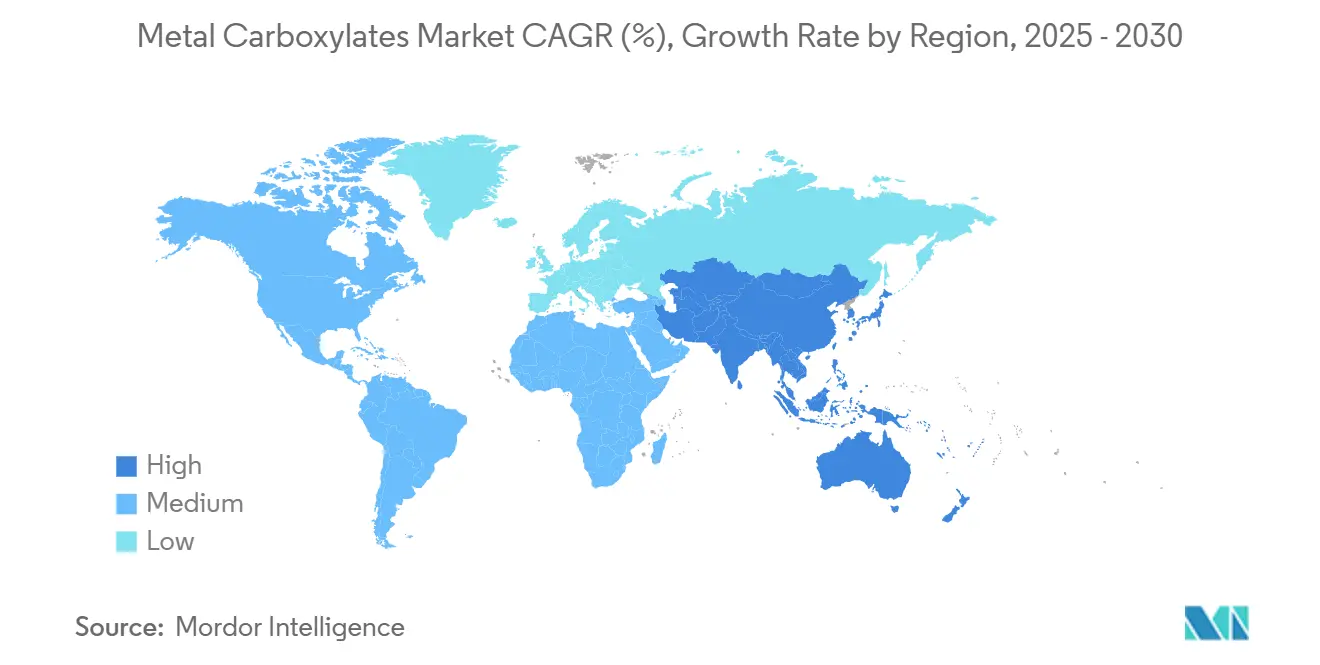

- By geography, Asia-Pacific controlled 52.26% of the Metal Carboxylates market in 2024 and is expected to rise at a 6.12% CAGR to 2030.

Global Metal Carboxylates Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for High-Performance Driers in Alkyd and Water-Borne Coatings | +1.2% | Global, with concentration in Europe and North America | Medium term (2-4 years) |

| Expansion in PVC Stabilizers, Lubricant and Catalyst Uses | +0.9% | APAC core, spill-over to Europe | Long term (≥ 4 years) |

| Fast-Growing Construction Sector Creating Demand | +1.1% | APAC core, with growth in India and China | Short term (≤ 2 years) |

| Adoption of Cobalt-Free Manganese and Zirconium Carboxylates | +0.8% | Global, led by Europe due to REACH compliance | Medium term (2-4 years) |

| Growing Utilization from Automotive Industry | +0.7% | Global, with strength in APAC and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for High-Performance Driers in Alkyd and Water-Borne Coatings

Coating formulators increasingly seek accelerated oxidative curing while avoiding cobalt reclassification. Venator’s NUODEX® DryCoat series illustrates these gains by raising film hardness without elevating VOCs. European producers lead adoption because REACH forces cobalt substitution and favors manganese(III) acetylacetonate, which matches drying speed at lower treat rates. In water-borne systems, encapsulated metal complexes prevent premature oxidation yet deliver rapid surface set on exposure to air, improving throughput in automotive refinishing lines. Bio-alkyd resins that include azelaic acid achieve 70% biodegradability while keeping mechanical performance intact, signalling a commercial path toward fully sustainable coatings.

Expansion in PVC Stabilizers, Lubricant and Catalyst Uses

Calcium-based stabilizers are replacing legacy lead systems in PVC pipe and profile production, with Baerlocher packages cutting density and lowering additive costs for construction firms in India and China. At the same time, algae-oil extreme-pressure lubricants introduced by DIC Corporation curb carbon footprints while preserving gear-box wear resistance, meeting OEM decarbonization targets. Metal carboxylates now catalyze lipid deoxygenation pathways used in sustainable aviation fuel pilot plants, where their selectivity reduces hydrogen demand and process energy. These multi-function roles create premium opportunities for suppliers that can validate both regulatory safety and enhanced performance over the product life cycle.

Fast-Growing Construction Sector Creating Demand

Infrastructure programs across Asia-Pacific are fueling growth in concrete admixtures, sealants and protective coatings that depend on metal carboxylate chemistry to quicken cure cycles and raise durability. Sika’s investments in Peru and China expand access to CHF 110 billion worth of addressable construction-chemicals demand by adding local capacity for carboxylate-modified acrylics. Self-healing coatings infused with zinc carboxylates close micro-cracks when exposed to moisture, extending façade life and paralleling Germany’s specification standards for public buildings. Green-building certifications require lower solvent levels, encouraging the uptake of water-borne formulations that integrate manganese driers with low hazard profiles.

Adoption of Cobalt-Free Manganese and Zirconium Carboxylates

REACH’s carcinogen listing for cobalt compounds has swung demand toward manganese and zirconium complexes that achieve comparable cure rates while avoiding hazardous-waste designation[1]European Chemicals Agency, “Cobalt Compounds Classification,” echa.europa.eu . Manganese driers, however, necessitate color-control strategies such as ligand modification to avert yellowing in white coatings. Zirconium carboxylates excel in marine topcoats, enduring 90 °C service and brine exposure, which positions them well for offshore wind projects. Patent filings covering polydentate nitrogen donor ligands enhance iron and manganese catalytic activity, opening additional uses in polyurethane pre-polymer synthesis.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Prices of Fatty Acids and Metal Oxides | -0.8% | Global, with acute impact in commodity-dependent regions | Short term (≤ 2 years) |

| Stringent VOC / Hazardous-Waste Rules on Cobalt and Lead Driers | -0.6% | Europe and North America, expanding globally | Medium term (2-4 years) |

| Cobalt Price Collapse causing Producer Margin Stress | -0.4% | Global, with concentrated impact on cobalt-dependent producers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile Prices of Fatty Acids and Metal Oxides

World Bank indices show a 9% rise in metals and minerals prices during 2024, eroding margins for drier producers that rely on cobalt, manganese and zinc oxides. Simultaneous palm-oil supply disruptions spike feedstock costs for octoates and naphthenates, pushing formulators toward shorter contracts and hedging strategies. Specialty-chemical distributors experienced destocking since mid-2022, forcing price concessions and inventory write-downs that reduced profitability across the chain. Vertically integrated players partially offset volatility by owning oleochemical capacity, yet this capital-intensive model challenges mid-tier participants in the Metal Carboxylates market.

Stringent VOC / Hazardous-Waste Rules on Cobalt and Lead Driers

December 2024 amendments to REACH Annex XVII impose fuller labeling, registration fees and workplace-exposure monitoring for cobalt, while California’s Automotive Refinishing Program drafts airborne-toxic measures to eliminate cadmium and hexavalent chromium. Compliance costs weigh heavily on small manufacturers that must requalify formulations and change plant procedures, accelerating consolidation as scale becomes a defensive asset. Canada’s ban on high-PAH sealants illustrates regulatory spill-over that multiplies complexity for exporters. Customers delay orders until new specifications stabilize, temporarily dampening demand within the Metal Carboxylates market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Metal Type: Cobalt Leadership Under Pressure

Cobalt carboxylates captured 37.65% of Metal Carboxylates market size 2024. Yet manganese compounds are set to outpace at a 5.69% CAGR because they comply with carcinogen restrictions without compromising cure speed. The Metal Carboxylates market share of cobalt is forecast to fall below 30% by 2030 as regulatory rulings take effect. Zirconium, zinc and calcium compounds combine niche thermal stability, PVC stabilization and cement compatibility strengths, each expanding in double-digit volume as formulators diversify metal portfolios. Copper carboxylates preserve anti-fouling uses in marine coatings thanks to biocidal performance accepted by IMO guidelines, illustrating that metal-specific advantages continue to determine end-use preference.

Formulators in Europe move fastest toward cobalt-free portfolios in response to REACH, whereas Asia-Pacific users keep dual sourcing to manage cost and performance risk. Patented ligand modifications improve the latent activity of iron and manganese congeners, narrowing the efficiency gap with cobalt and justifying premium pricing. These shifts reinforce a value-over-volume dynamic that stabilizes dollar revenue even as cobalt tonnage moderates.

By Function: Driers Remain Core Amid Broader Adoption

Driers and catalysts accounted for 54.27% of Metal Carboxylates market share in 2024, reflecting their foundational role in alkyd curing and polymerization. Auxiliary drier blends that pair manganese with calcium boost through-dry, enabling high-solids decorative paints to pass ISO touch-dry tests under 60 minutes. Corrosion-inhibitor demand is growing fastest as infrastructure owners replace chromates with zirconium and zinc carboxylates for galvanic protection on steel bridges. Lubricants and PVC stabilizers hold steady volume while undergoing green-chemistry upgrades such as algae-derived esters. Plasticizer-like surface modifiers emerge as new growth pockets, especially zinc ricinoleate used for odor removal in flexible packaging, showing how the Metal Carboxylates market extends into consumer-exposed applications.

By Application: Coatings Supremacy with Rising Electronics Uses

Paints and coatings accounted for 46.24% of Metal Carboxylates market share in 2024, supported by steady building renovation and stricter VOC targets. Automotive OEM lines specify faster curing to cut bake time, and metal carboxylates enable 90 °C flash-off while maintaining gloss retention. “Other applications” including catalysts for bio-jet fuel are scaling quickest, reflecting airline sustainability commitments. PVC processing benefits from lead substitution, while construction chemicals see heightened take-up of calcium carboxylates in self-levelling flooring compounds. Semiconductor fabricators adopt manganese driers for solder-mask coatings, indicating electronics as a long-run demand pillar.

By End-user Industry: Construction Dominates; Electronics Accelerates

Building and construction accounted for 31.91% of Metal Carboxylates market share in 2024 because metal carboxylates enhance protective performance in façades, sealants and concrete. Electrification trends push electronics demand higher; circuit-board makers favor low-residue driers that pass ion-chromatography cleanliness tests, fostering a 6.27% CAGR outlook. Automotive maintains relevance through corrosion-resistant chassis coatings, while chemicals and petrochemicals integrate in-house catalyst loops that utilize cobalt and manganese octoates. Textile finishers deploy specialty carboxylates for antimicrobial and water-repellent fabrics sold into activewear segments.

Geography Analysis

Asia-Pacific generated captured 52.26% of Metal Carboxylates market size in 2024 and is positioned for a 6.12% CAGR through 2030 due to China's coating plants and India’s housing push. BASF’s USD 10 billion Zhanjiang hub, powered solely by renewables, will supply nearly half of regional demand for fatty-acid derived intermediates. Japan and South Korea leverage metal carboxylates in advanced chip packaging, capturing incremental value despite modest domestic coatings growth. ASEAN economies broaden the base with PVC window-frame production that shifts to calcium-zinc stabilizers, reinforcing regional demand diversity.

North America remains technology-focused, with aerospace and automotive OEMs insisting on cobalt-free drier certification. Mexico grows as an export platform because of the USMCA trade framework, absorbing metal carboxylate coatings for automotive bodies. Europe’s share is pressured by strict chemical policies; nevertheless, REACH-compliant manganese systems command premium pricing that shelters margins. South America adds opportunity in Brazil’s construction pipeline and copper mine equipment coatings. Middle East and Africa offer smaller but steadily rising demand, anchored by Saudi mega-projects and South African mining gear requiring high-temperature lubricants with metal carboxylate additives.

Competitive Landscape

The Metal Carboxylates market shows moderate concentration. Top 10 suppliers control under 50% of revenue, leaving space for regional specialists. BASF’s plan to report Metal Solutions separately from 2025 underscores its strategic emphasis on high-margin carboxylate streams. Umicore leverages recycling access to secure cobalt yet diversifies into manganese technologies to future-proof its drier portfolio. Shepherd Chemical invests in US-based fatty-acid plants to reduce import risk. Milliken’s acquisition of Borchers adds cobalt-free know-how and global oxide dispersion assets, an important defense as regulatory scrutiny intensifies[2]Milliken & Company, “Milliken Completes Acquisition of Borchers,” milliken.com . PPG operates a robust patent estate covering zirconium pretreatments that integrate molybdenum for superior corrosion performance, aligning with automaker substrate-thinning strategies. The fragmentation encourages collaboration; several mid-sized Asian producers partner with European R&D boutiques to co-develop water-borne packages with rapid market access.

Metal Carboxylates Industry Leaders

Dura Chemicals Inc.

Milliken & Company

Umicore

Valtris Specialty Chemicals

Shepherd Chemical Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: BASF introduced BASF-Metalcat, a new range of transition metal carboxylates for catalysis applications. These catalysts enhance reactivity and stability across industrial processes, including polymerization and fine chemical synthesis.

- September 2024: Alfa Aesar, a Thermo Fisher Scientific company, released a series of actinide metal carboxylates, comprising uranium and thorium-based compounds. These compounds serve applications in nuclear chemistry and radiopharmaceuticals.

Global Metal Carboxylates Market Report Scope

| Cobalt Carboxylates |

| Manganese Carboxylates |

| Zirconium Carboxylates |

| Zinc Carboxylates |

| Calcium Carboxylates |

| Copper Carboxylates |

| Other Metal Types (Potassium, Barium Carboxylates, Sodium and Other Metals) |

| Driers and Catalysts |

| Lubricants and Stabilizers |

| Corrosion Inhibitors |

| Others (Plasticizers, Surface Modifiers) |

| Paints and Coatings |

| Plastics and Rubber Processing |

| Construction Chemicals |

| Lubricants and Greases |

| Textiles and Leather Finishing |

| Printing Inks and Adhesives |

| Others Applications (Catalysts, Cosmetics, Electronics) |

| Building and Construction |

| Automotive and Transportation |

| Chemicals and Petrochemicals |

| Textile and Leather |

| Packaging |

| Electrical and Electronics |

| Other End-user Industries (Power Generation, etc.) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Metal Type | Cobalt Carboxylates | |

| Manganese Carboxylates | ||

| Zirconium Carboxylates | ||

| Zinc Carboxylates | ||

| Calcium Carboxylates | ||

| Copper Carboxylates | ||

| Other Metal Types (Potassium, Barium Carboxylates, Sodium and Other Metals) | ||

| By Function | Driers and Catalysts | |

| Lubricants and Stabilizers | ||

| Corrosion Inhibitors | ||

| Others (Plasticizers, Surface Modifiers) | ||

| By Application | Paints and Coatings | |

| Plastics and Rubber Processing | ||

| Construction Chemicals | ||

| Lubricants and Greases | ||

| Textiles and Leather Finishing | ||

| Printing Inks and Adhesives | ||

| Others Applications (Catalysts, Cosmetics, Electronics) | ||

| By End-user Industry | Building and Construction | |

| Automotive and Transportation | ||

| Chemicals and Petrochemicals | ||

| Textile and Leather | ||

| Packaging | ||

| Electrical and Electronics | ||

| Other End-user Industries (Power Generation, etc.) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the Metal Carboxylates market in 2025?

The Metal Carboxylates market size stands at USD 5.86 billion in 2025.

The Metal Carboxylates market size stands at USD 5.86 billion in 2025.

The market is expected to grow at a 5.14% CAGR from 2025 to 2030.

Which metal type is growing fastest inside the market?

Manganese carboxylates are the fastest-growing metal type with a 5.69% CAGR.

Manganese carboxylates are the fastest-growing metal type with a 5.69% CAGR.

REACH reclassification of cobalt as a carcinogen accelerates the shift toward manganese and zirconium systems.

Page last updated on: