Sodium Silicate Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

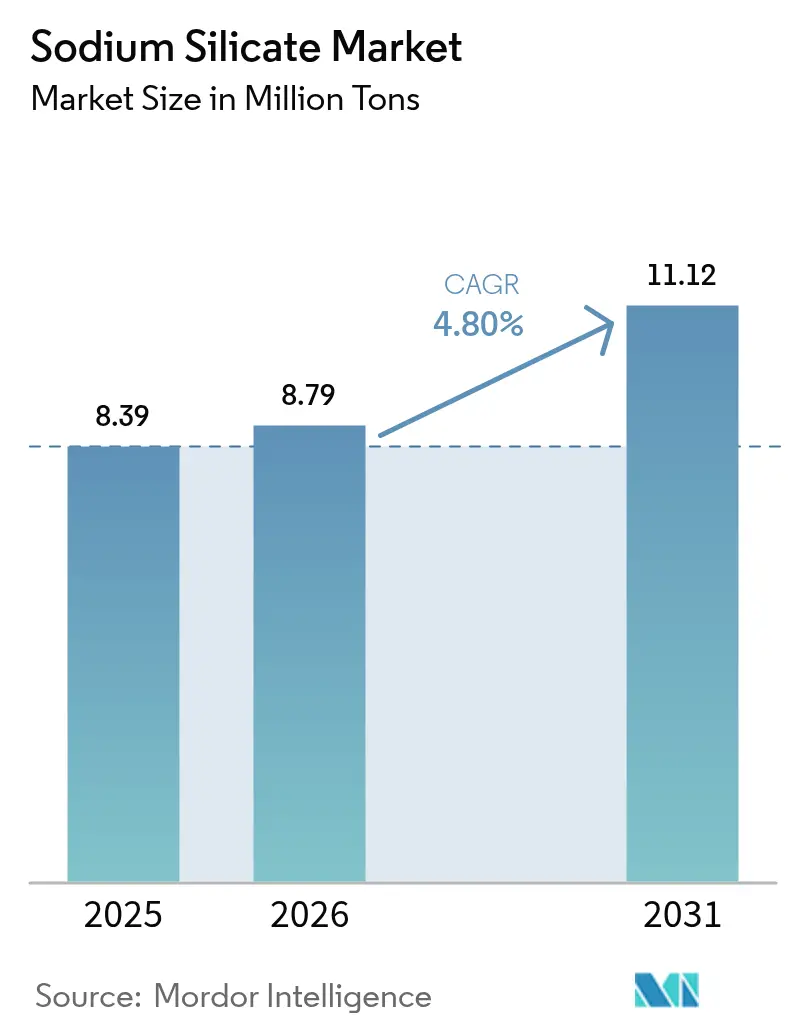

| Market Volume (2026) | 8.79 Million tons |

| Market Volume (2031) | 11.12 Million tons |

| Growth Rate (2026 - 2031) | 4.80% CAGR |

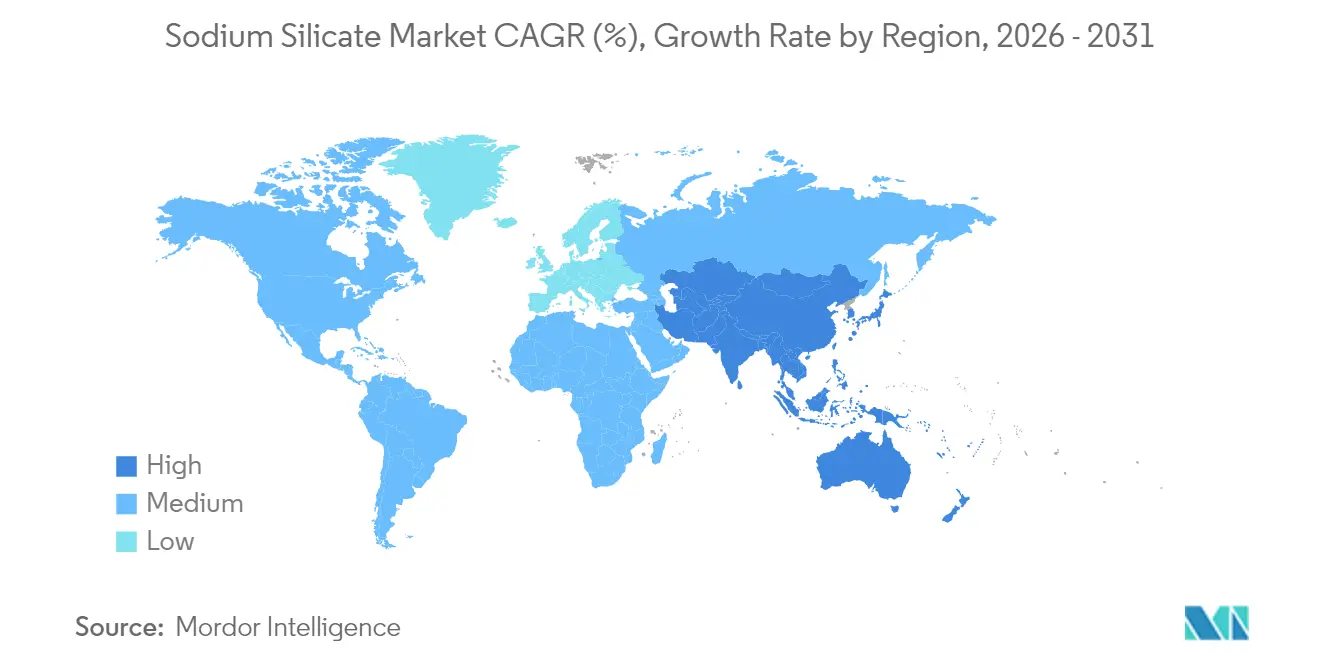

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sodium Silicate Market Analysis by Mordor Intelligence

The Sodium Silicate market size is expected to grow from 8.39 million tons in 2025 to 8.79 million tons in 2026 and is forecast to reach 11.12 million tons by 2031 at 4.8% CAGR over 2026-2031. The expansion reflects the chemical’s growing relevance in applications that support resource-efficient manufacturing and circular economy practices. Increased adoption in detergent formulations, advanced adhesive systems, and low-carbon construction materials underpins volume growth, while demand for high-purity grades lifts the overall value trajectory. Competitive differentiation hinges on process automation, product customization, and vertical integration, enabling leading suppliers to maintain resilient margins despite fluctuations in raw material prices. Regulatory tightening in major economies deepens the moat for well-capitalized producers that can meet stricter effluent and workplace safety standards; yet, these same rules also catalyze innovation in eco-friendly formulations and closed-loop recycling.

Key Report Takeaways

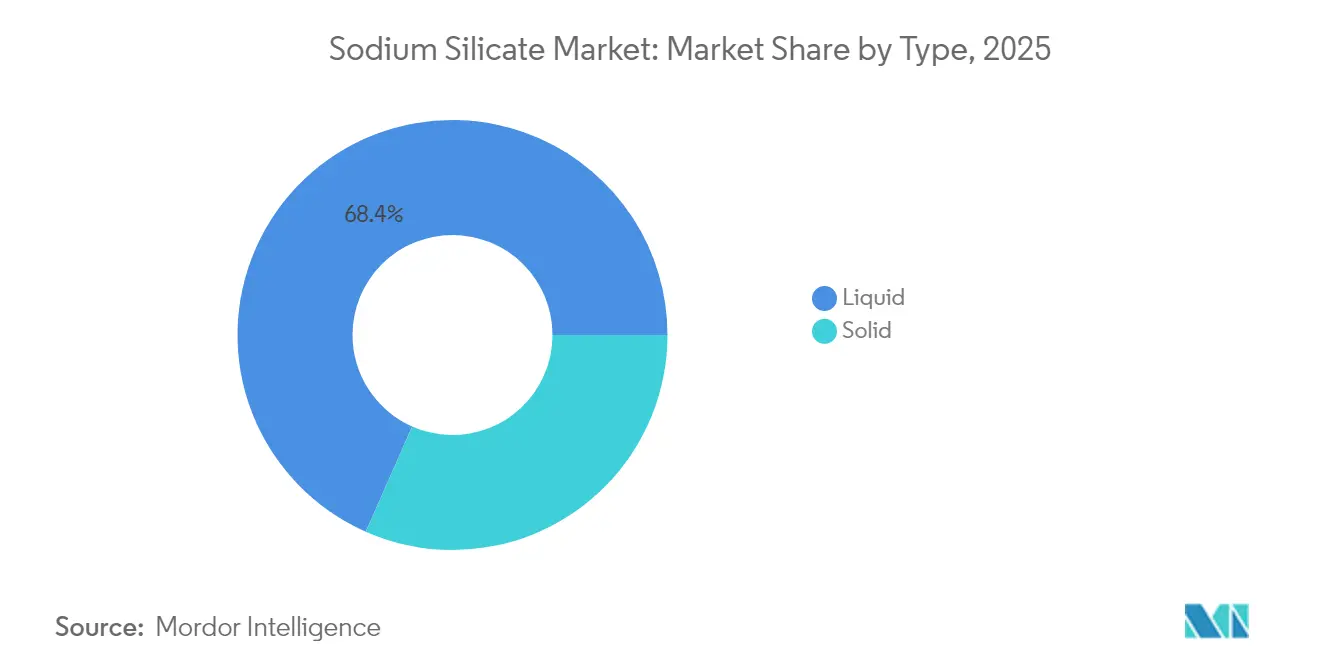

- By type, liquid sodium silicate held 68.39% of the Sodium Silicate market share in 2025. Moreover, liquid sodium silicate is forecast to grow at a 5.05% CAGR to 2031.

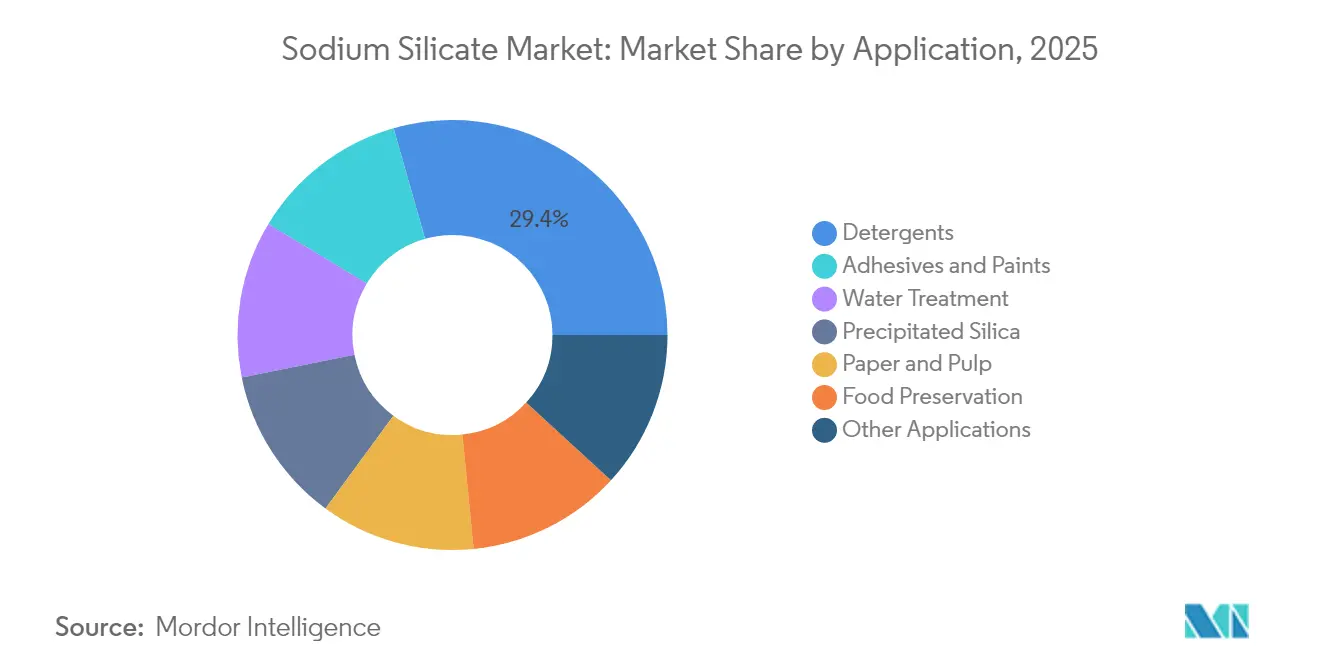

- By application, the detergent segment accounted for a 29.42% share of the Sodium Silicate market size in 2025. By application, adhesives and paints are expected to post the fastest 5.39% CAGR through 2031.

- By geography, the Asia-Pacific region led with a 42.12% volume share in 2025; it is set to expand at a 5.70% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Sodium Silicate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mounting demand for waste-paper recycling | +0.8% | Global, concentrated in North America & Europe | Medium term (2-4 years) |

| Rising usage of precipitated silica in "green" tyres | +1.2% | Global, led by Asia-Pacific automotive hubs | Long term (≥ 4 years) |

| Growth of powder detergents in low-income economies | +0.9% | Asia-Pacific, Middle East & Africa | Short term (≤ 2 years) |

| Rapid industrial-scale uptake of geopolymer cement | +1.1% | Global, early adoption in Australia, Europe | Long term (≥ 4 years) |

| Circular-economy push for closed-loop glass recycling | +0.7% | Europe, North America, expanding to Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Mounting Demand for Waste-Paper Recycling

Government mandates for higher recycled-content packaging accelerate the use of sodium silicate in flotation deinking processes[1]“Enhanced Brightness in Deinked Pulps,” BioResources, bioresources.ca. Modern mills consume 8–12 kg of sodium silicate per ton of recovered paper, and the chemical’s alkalinity control prevents ink particle re-agglomeration, allowing printers to meet exacting brightness and cleanliness standards. Demand intensifies as plastic substitution drives an additional fiber requirement, especially in Europe, where the Single-Use Plastics Directive prompts converters to shift toward paper-based formats. Suppliers able to deliver consistent pH buffering grades secure long-term contracts with integrated paper groups.

Rising Usage of Precipitated Silica in “Green” Tires

Each ton of precipitated silica requires roughly 1.3 tons of sodium silicate feedstock, creating a direct pull-through effect as tire makers lower rolling resistance to meet evolving fuel-economy labeling rules. High-purity sodium silicate grades with narrow silica-to-soda ratios command premium prices because they yield silica with controlled surface area and porosity—critical parameters for next-generation electric vehicle tires. Capacity additions in Southeast Asia reinforce regional demand momentum.

Growth of Powder Detergents in Low-Income Economies

Powder laundry products remain the value option in emerging economies. Local formulators maintain sodium silicate inclusion levels at 8–15% to maximize sequestration and anti-caking efficiency in humid climates. As urbanization drives retail penetration, supply agreements increasingly stipulate granular silicate grades tailored for high-speed spray-drying operations, ensuring free-flowing detergent powders on store shelves.

Rapid Industrial-Scale Uptake of Geopolymer Cement

Government-funded infrastructure pilots in Australia and the European Union showcase geopolymer concrete that cuts lifecycle CO₂ by up to 80% compared with Portland cement. Sodium silicate serves as the primary alkaline activator, dissolving aluminosilicate precursors at ambient temperatures and enabling rapid strength development. Public procurement targets for low-carbon building materials are expected to lock in structural demand over the next decade.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health and safety hazards of high-alkali silicates | -0.60% | Global, stricter enforcement in developed markets | Short term (≤ 2 years) |

| Volatility in soda-ash prices | -0.90% | Global, acute impact in import-dependent regions | Short term (≤ 2 years) |

| Tightening EU effluent-discharge limits on silicate liquor | -0.80% | Europe | Medium term (2-4 years) |

| Competitive threat from bio-based binders in foundry cores | -0.50% | Global, initial penetration in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Health and Safety Hazards of High-Alkali Silicates

Regulators classify concentrated sodium silicate as corrosive, prompting stricter workplace exposure limits and tighter personal protective equipment mandates[2]“Workplace Hazardous Materials Information System,” Health Canada, hwc.gc.ca. Small and mid-size users face higher compliance costs, which can delay adoption in price-sensitive industries such as craft foundries and micro-scale detergent blenders. Large producers that embed advanced closed-loop handling systems and remote monitoring safeguard operations and credibility with downstream customers.

Volatility in Soda-Ash Prices

Soda ash accounts for up to 45% of the Sodium Silicate manufacturing cost. While prices softened in late 2024, historical cycles show sharp rebounds tied to energy-price shifts and export policies in key producing nations. Contract buyers are increasingly adding hedging clauses to supply agreements, but margin compression remains a near-term risk for producers unable to pass through cost spikes to end-users. Geographic diversification of soda-ash sourcing is rising on boardroom agendas across Europe and South America.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Liquid Grades Extend Their Lead

Liquid products controlled 68.39% of the sodium silicate market in 2025 and are projected to expand at a 5.05% CAGR through 2031. Automated feed systems in water-treatment plants favor liquid chemistry because they eliminate dissolution lag and enable tighter dosage control. Concentrated 50° Baumé innovations deliver 25% freight savings while preserving reactivity, a benefit that resonates with export-oriented detergent makers. Solid beads and powder forms retain relevance where shelf life, remote storage, or ultrahigh alkalinity are paramount, yet the value gap narrows as logistics-optimized liquids capture incremental territory.

Manufacturers utilize membrane filtration to fine-tune silica-to-soda ratios in liquid grades, resulting in performance-tailored intermediates for high-purity precipitated silica and specialty adhesive applications. This machinery-intensive capability creates technological barriers to entry, particularly in regions where utilities and skilled labor are scarce. Portfolio breadth in liquids explains why integrated suppliers sustain higher EBITDA margins and secure long-term supply agreements with multinational fast-moving consumer goods companies.

By Application: Detergent Leadership with Adhesives Accelerating

Detergents supplied 29.42% of total demand in 2025, translating into 2.47 million tons of sodium silicate feedstock. Growth remains linked to middle-class expansion in South and Southeast Asia, where cost-sensitive consumers prioritize powder formulations. Meanwhile, the adhesives and paints segment is forecast to rise at a 5.39% CAGR, driven by infrastructure projects that specify mineral adhesives for fire resistance and by automotive body shops transitioning to water-glass-based paints for lightweight substrates.

Precipitated silica production remains a robust offtake stream as global tire makers align with stricter fuel-efficiency scoring. Water-treatment utilities adopt silicate blends for corrosion inhibition in aging distribution networks, a trend reinforced by federal infrastructure budgets. Food preservation, although niche, is gaining momentum as studies reveal up to 79.7% fungal inhibition in stored maize at a 100 mM sodium silicate dosage. Overall, widening end-use diversity cushions demand against cyclical swings in any single application vertical.

Geography Analysis

The Asia-Pacific region accounts for the largest share of global consumption at 42.12% in 2025. Domestic producers in China, including facilities such as Taicang Sinoch’s 300,000-ton plant, back-integrate from soda ash to solid and liquid silicates, supporting exports across Southeast Asia. India’s detergent industry accelerates the installation of spray-drying towers that rely on liquid silicate dosing control, while Australia fosters the early adoption of geopolymer cement in government-funded transport projects.

North American demand benefits from federal spending on water infrastructure upgrades that specify silicate-based corrosion inhibitors. Shale-basin operators use sodium silicate as a drilling fluid additive that stabilizes clay formations, keeping regional offtake stable even when overall rig counts fluctuate. Premium electronics-grade volumes cluster along the West Coast semiconductor corridor, where high-purity grades support the fabrication of scratch-free glass.

Europe maintains a quality-over-quantity orientation. Stricter effluent discharge rules under the Water Framework Directive increase compliance costs but also favor producers equipped with closed-loop water recycling systems. Consolidation trends, such as Qemetica’s November 2024 acquisition of PPG’s silica assets, tighten supply in precipitated-silica value chains that primarily feed the regional tire industry. Demand for closed-loop glass recycling chemicals further anchors volume stability.

Competitive Landscape

The Sodium Silicate market is moderately concentrated. Multinationals such as BASF, PQ Corporation, and Tokuyama lead in terms of capacity scale, R&D depth, and technical support coverage, while regional specialists capture niche domestic demand through proximity and cost agility. Integrated players that own feedstock, production, and downstream precipitated-silica assets enjoy cross-segment synergies and cushion margin exposure to soda-ash swings. Geographic diversification of manufacturing footprints hedges against trade-policy risk and currency volatility.

Sodium Silicate Industry Leaders

PQ Corporation

QEMETICA

BASF

Nippon Chemical Industrial CO., LTD.

Tokuyama Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: PQ Corporation completed its acquisition of Sibelco's specialty silicate business operations in Sweden, expanding European production capacity and strengthening its position in high-performance applications. The transaction enhances PQ Corporation's ability to meet the growing demand for specialized sodium silicate grades in water treatment and industrial applications, while providing geographic diversification of its manufacturing assets.

- November 2024: Qemetica finalized the acquisition of PPG Industries' precipitated silica business, adding production capabilities that complement its sodium silicate operations and create vertical integration opportunities. The strategic move positions Qemetica to capture value across the sodium silicate-to-precipitated silica value chain, particularly in automotive tire applications.

Global Sodium Silicate Market Report Scope

Sodium silicate, commonly known as 'water glass,' is prominent due to its wide commercial and industrial applications. It is often composed of an oxygen-silicon polymer backbone housing water in molecular matrix pores. The market is segmented based on type, application, and geography. By type, the market is segmented into solid and liquid. By application, the market is segmented into adhesives and paints, detergents, food preservation, precipitated silica, paper production, water treatment, and other applications (construction, metal casting). The report offers market size and forecasts for 15 countries across major regions. For each segment, market sizing and forecasts have been done on the basis of volume (tons) for all the above segments.

| Solid |

| Liquid |

| Adhesives and Paints |

| Detergents |

| Food Preservation |

| Precipitated Silica |

| Paper and Pulp |

| Water Treatment |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Type | Solid | |

| Liquid | ||

| By Application | Adhesives and Paints | |

| Detergents | ||

| Food Preservation | ||

| Precipitated Silica | ||

| Paper and Pulp | ||

| Water Treatment | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What volume growth is expected for global sodium silicate demand by 2031?

Consumption is forecast to rise from 8.79 million tons in 2026 to 11.12 million tons in 2031, representing a 4.80% CAGR.

Which region will contribute the most incremental tonnage through 2031?

Asia-Pacific will add the largest absolute volume, underpinned by expanding detergent and construction industries.

Why are liquid grades gaining share over solid forms?

Liquid products eliminate dissolution steps, enable automated dosing, and newer 50° Baumé grades cut freight volumes by 25%.

How do soda-ash price swings affect producer margins?

Soda ash represents up to 45% of production cost, so price spikes can compress margins unless offset by contract pass-through or diversified sourcing.

Which emerging application offers the fastest growth outlook?

Adhesives and paints are set to register the highest CAGR at 5.39% thanks to infrastructure build-out and automotive lightweighting.

Page last updated on: