Smart Harvest Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

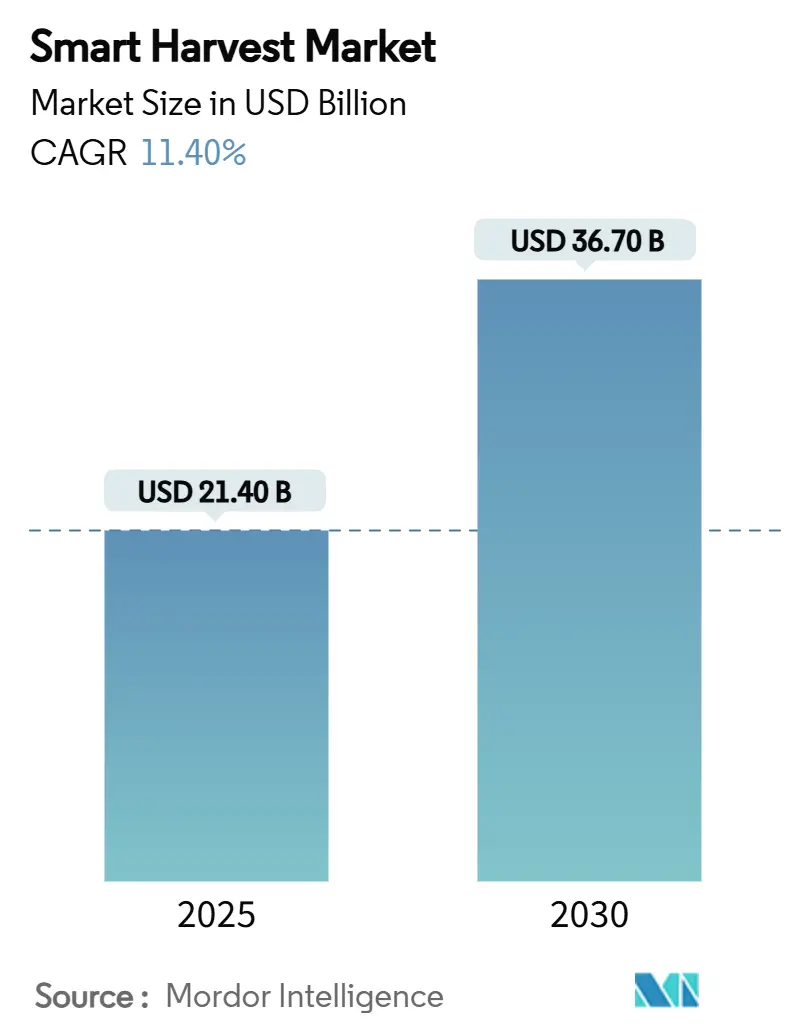

| Market Size (2025) | USD 21.40 Billion |

| Market Size (2030) | USD 36.70 Billion |

| Growth Rate (2025 - 2030) | 11.40% CAGR |

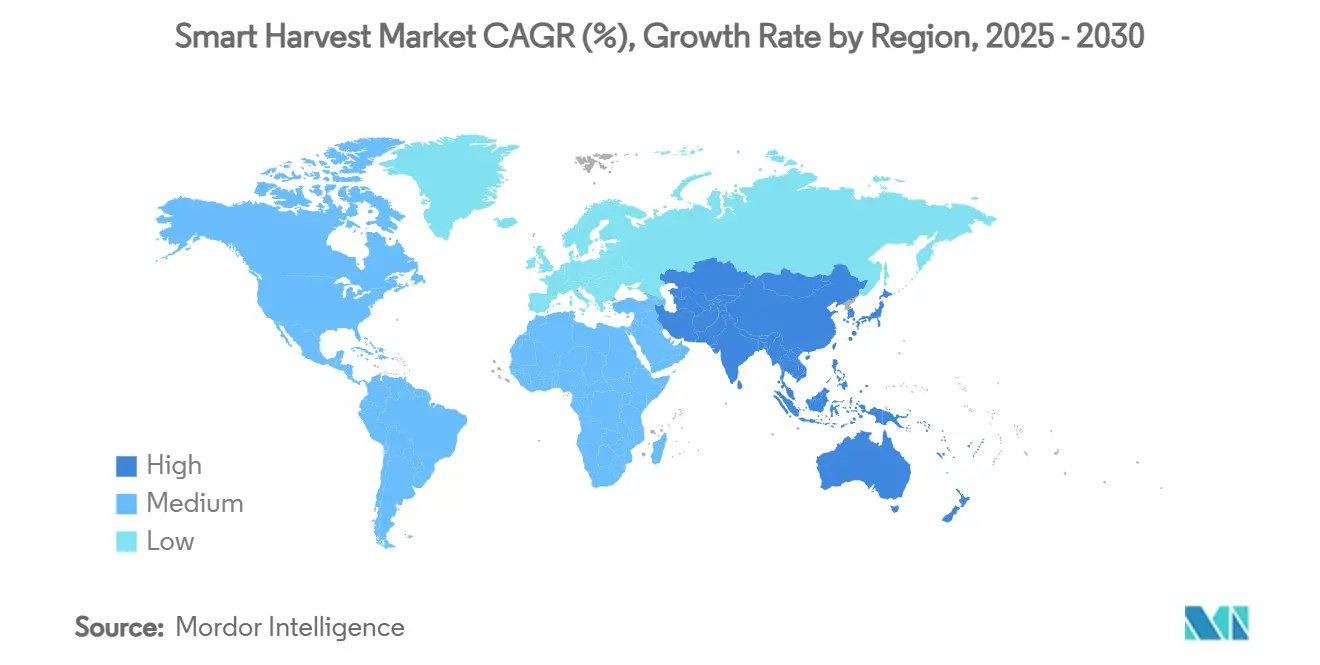

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Smart Harvest Market Analysis by Mordor Intelligence

The smart harvest market size is estimated at USD 21.40 billion in 2025 and is projected to reach USD 36.70 billion by 2030, at a CAGR of 11.40% during the forecast period (2025-2030). Sustained momentum stems from growers embracing harvesting robots, machine vision, and edge AI analytics to counter labor scarcity, lower input waste, and meet retailer demands for pesticide-free produce. Hardware vendors dominate revenue as agricultural enterprises initially choose tangible robotic systems, then layer on software and services once proof of return is clear. Component costs are easing because imaging sensors and on-device processing chips now follow steep semiconductor learning curves, pushing per-unit prices down even while performance climbs. Competitive intensity is rising as traditional farm-equipment majors integrate automation platforms while pure-play robotics start-ups accelerate niche breakthroughs. Policy support from Europe’s Common Agricultural Policy, digital incentives to Asia-Pacific subsidy schemes, further underpins scale-up opportunities across both intensive greenhouse and increasingly challenging open-field environments.

Key Report Takeaways

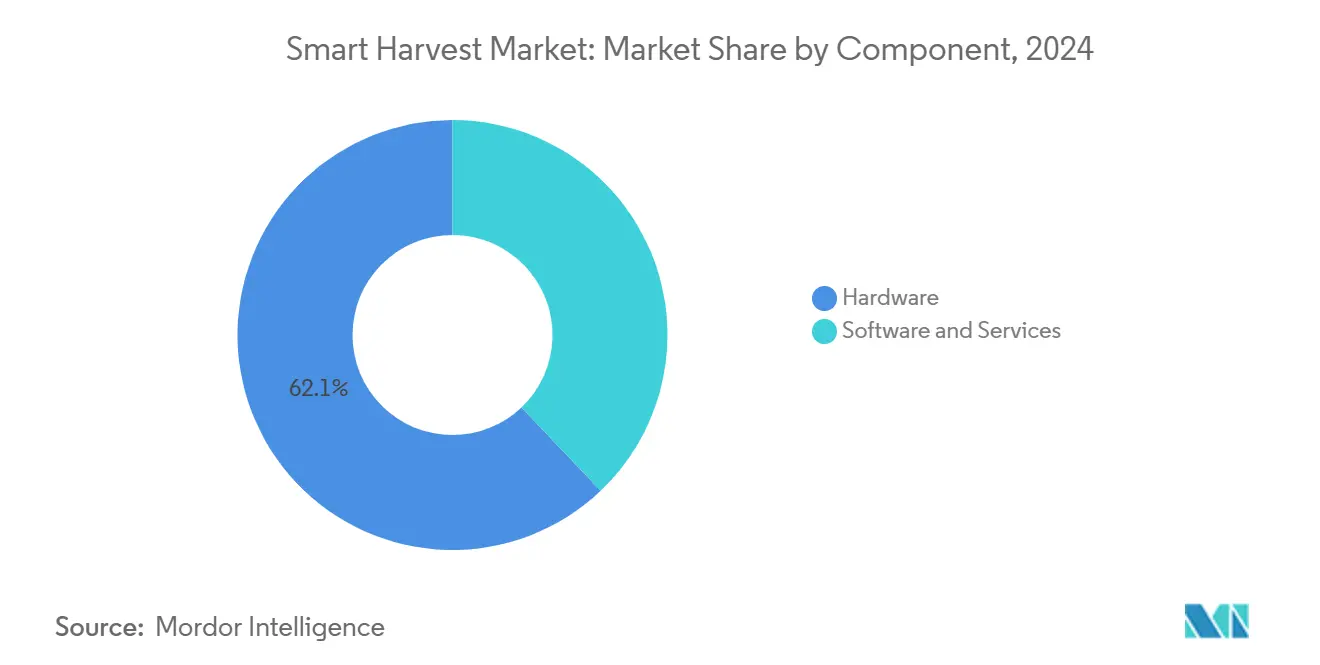

- By component, hardware led with 62.1% revenue share in 2024; software is on track for the fastest 15.1% CAGR through 2030.

- By technology, robotic automation systems captured 48.3% of the smart harvest market share in 2024, whereas edge cloud and edge data analytics is projected to race ahead at an 18.3% CAGR to 2030.

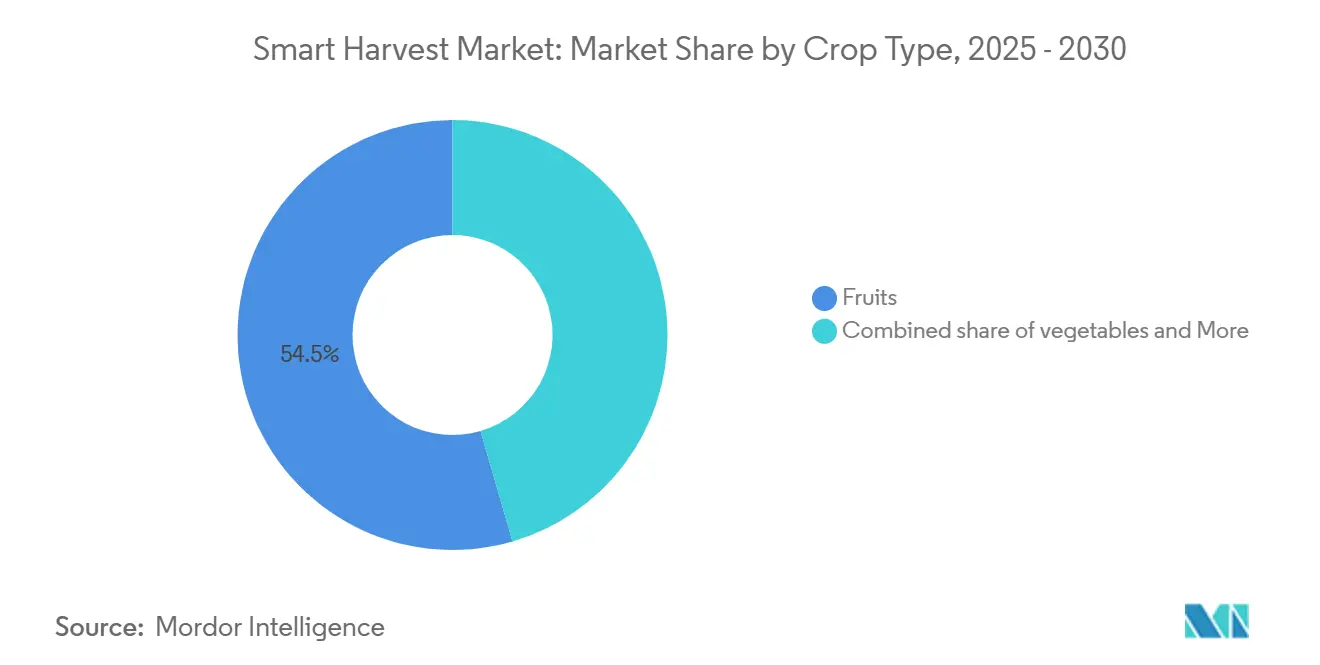

- By crop type, fruits accounted for 54.5% of the smart harvest market size in 2024, while nuts recorded the strongest 14.2% CAGR outlook to 2030.

- By farm environment, greenhouse deployments commanded 58.2% of 2024 revenue, yet open-field systems are growing briskly at a 12.6% CAGR.

- By geography, Europe retained 33.5% revenue leadership in 2024; Asia-Pacific is forecast to expand at a 14.2% CAGR through 2030.

- Deere and Company, Trimble, Robert Bosch, CNH Industrial, and Agrobot jointly controlled 51% market share in 2024.

Global Smart Harvest Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Labor-shortage-led automation push | +3.2% | North America and Europe | Medium term (2-4 years) |

| Government subsidies for farm robotics | +2.8% | Europe, North America, Asia-Pacific | Short term (≤ 2 years) |

| Declining sensor costs and IoT penetration | +2.1% | Global developed markets | Long term (≥ 4 years) |

| Rising demand for quality produce | +1.9% | North America, Europe, and urban centers in Asia-Pacific | Medium term (2-4 years) |

| Carbon-credit programs rewarding low-waste harvesting | +1.1% | Europe and California | Long term (≥ 4 years) |

| Edge-AI on-device processing reduces connectivity needs | +1.5% | Rural zones worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Labor-Shortage-Led Automation Push

Workforce availability in agriculture keeps shrinking as rural populations age and immigration rules tighten. Wages rise faster than crop prices, driving labor costs to 30-50% of total harvest expense for many fruit and vegetable growers.[1]USDA Economic Research Service, “Ag and Food Statistics Charting the Essentials,” usda.gov Rising wages raise harvest costs to 30-50% of total expenditure for delicate crops. Governments attempt stop-gap relief, such as the United Kingdom lifting seasonal-worker visas to 45,000 in 2024,[2]UK Department for Environment, Food and Rural Affairs, “Seasonal Worker Visa Route Expansion 2024,” gov.uk yet growers treat robotics as the only structural answer. Autonomous pickers that run day and night sustain throughput and secure produce quality regardless of labor cycles, making up-front capital easier to justify as crop value per acre climbs. Together these factors make labor scarcity the most immediate catalyst for smart-harvest spending growth.

Government Subsidies for Farm Robotics

National and regional programs lower investment risk by covering 30-50% of equipment cost for qualified buyers. The United States allocates USD 50 million a year in precision-agriculture grants, and the European Union ties subsidy eligibility to digital-farming benchmarks. These incentives shorten payback periods for medium-sized farms that lack deep capital reserves. Subsidies also stimulate local dealer networks, which improves service coverage and user confidence. As policies evolve, compliance reporting often requires onboard data logging, nudging growers toward integrated robotic solutions.

Declining Sensor Costs and IoT Penetration

Between 2023 and 2025, average factory-gate prices for agriculture-grade multispectral cameras and 3-D lidar modules fell by 27% as new stacked-pixel CMOS designs reached mass production. The latest sensors deliver 1.6 times higher effective resolution while cutting power draw by nearly one-third, widening their use in battery-powered field robots. Lower component costs let mid-tier equipment brands bundle machine vision into harvesters priced under USD 200,000, broadening appeal beyond corporate farms. Simultaneously, expanded private 5G and low-orbit satellite coverage push reliable connectivity into remote croplands, enabling real-time data offload for AI model refinement.[3]Australian Bureau of Statistics, “Telecommunications Coverage on Agricultural Land, 2025,” abs.gov.au Together, cheaper high-performance sensors and better rural broadband accelerate annual deployments of vision-enabled harvesting robots.

Rising Demand for Quality Produce

Consumers now expect more than just basic safety from fresh food; they also look for peak freshness, higher nutrient levels, an attractive appearance, and a reliable flavor. Smart harvesting enables growers to pick crops at the precise moment of optimal ripeness, which helps preserve nutrition and reduce spoilage from field to shelf. Robots equipped with cameras and chemical sensors continuously monitor sugar levels, firmness, and surface defects as they operate, ensuring only top-grade produce enters the supply chain. Premium items often command price mark-ups of 15-30%, which offsets the higher capital cost of robotic systems and supports faster payback periods. Large grocery chains and food-service buyers now favor suppliers that prove consistent, traceable quality, further steering farms toward technology that delivers uniform results.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront CAPEX for integrated robotic systems | −2.9% | Global emerging markets | Short term (≤ 2 years) |

| Fragmented farm landholdings limiting ROI | −2.2% | Asia-Pacific, Africa, South America | Long term (≥ 4 years) |

| Lack of open interoperability standards across OEM hardware | −1.8% | Worldwide | Medium term (2-4 years) |

| Limited rural service networks for robot maintenance | −1.4% | Developing regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront CAPEX for Integrated Robotic Systems

Full-featured harvest robots cost USD 150,000–USD 500,000, an outlay that few smallholders can absorb. Financing tools lag because lenders still view robotics as high-risk assets with unclear resale value. Leasing models exist but often require steep collateral or multi-year volume contracts. Without financial innovation, many growers defer purchases despite proven efficiency gains. This price barrier slows adoption in cost-sensitive regions even when labor shortages are acute.

Fragmented Farm Landholdings Limiting ROI

In India and Indonesia average plots measure under 2 hectares, far below the scale needed to fully utilize robotic systems. Low utilization stretches payback periods well past five years, deterring investment. Cooperative ownership models could solve this problem, yet land-tenure laws complicate shared-asset arrangements. Slow progress on consolidation keeps many emerging-market farmers tied to manual methods. As a result, global growth forecasts depend heavily on larger farms in developed economies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Hardware Dominance Drives Scale Benefits

Hardware commanded 62.1% of the smart harvest market revenue in 2024. Mechanical pickers, articulated arms, and vision modules deliver immediate labor substitution benefits, explaining growers’ bias toward capital goods over intangible software. The services layer covering training and predictive maintenance grows steadily as installed fleets expand and uptime expectations rise. Robotics vendors now bundle multi-year service contracts that price in sensor replacement and over-the-air firmware updates, shifting part of the margin mix from one-time sales to recurring fees. Parts financing and pay-per-use models offered by equipment dealers further widen access for medium-sized farms that lack cash reserves.

Software nevertheless stands out as the fastest-growing component, advancing at a 15.1% CAGR through 2030. Subscription analytics packages continuously refine yield models, while over-the-air updates extend robot functionality without extra metal. Newer platforms integrate crop-insurance modules that automatically trigger claims when vision systems log weather damage, strengthening the value proposition beyond basic task automation. API availability also lets third-party developers build add-on applications such as disease-detection plug-ins, improving ecosystem stickiness. As a result the smart harvest market size for software is projected to double during the forecast window, reinforcing recurring-revenue dynamics and raising lifetime customer value.

By Technology: Robotic Automation Systems Retain Command as Edge AI Surges

Robotic Automation Systems held 48.3% of 2024 revenue because they replace repetitive picking tasks and generate instantaneous payback in high-value orchards. Their embedded stereoscopic cameras discern fruit maturity, and soft grippers minimize bruising. Latest generation arms employ variable-rigidity actuators that adapt grip force in real time, allowing a single robot to handle multiple crop types with minimal tooling change. Machine-vision subsystems now fuse RGB, hyperspectral, and thermal inputs to detect subsurface defects that traditional cameras miss, lifting first-pass accuracy above 95%. Integration of LiDAR-based navigation further cuts downtime by mapping obstacle-dense orchards on the fly.

Edge AI analytics is racing ahead at an 18.3% CAGR. Local neural-network inference chips cut latency below 50 milliseconds, enabling real-time decisions without costly bandwidth. MLOps toolchains automate model retraining using anonymized field data, so performance improves season after season without manual coding. Cloud-edge orchestration also enables split-processing workloads where heavy training runs in the cloud while inference stays on the robot, optimizing both cost and speed. These advances strengthen the smart harvest industry’s pivot toward data-centric value capture and create new revenue streams from agronomic insights sold back to input suppliers.

By Crop Type: Fruits Rule, Nuts Accelerate

Fruit applications delivered 54.5% of the smart harvest market share in 2024 because strawberries, apples, and citrus demand gentle, selective picking. Robots equipped with RGB-D cameras and soft robotics outperform manual crews on consistency, leading to rapid orchard retrofits. Retailer scorecards that rate blemish incidence and sugar content reward producers who adopt precision harvest, further cementing technology adoption. Specialty-berry exporters in Chile and Spain deploy autonomous harvesters to hit narrow air-freight windows, reducing post-harvest losses by up to 20%.

Nut harvesting records the fastest 14.2% CAGR to 2030, driven by shaking rigs and ground-based vacuums that automate formerly labor-intensive tasks. Almond and pistachio groves in California and Australia adopt autonomous shakers that dislodge nuts within seconds, cutting collection time by 70%.[4]Almond Board of California, “Mechanized Harvest Efficiency Study,” almonds.com Compliance with dust-emission rules, enforced after the 2024 wildfire season, pushes growers toward low-dust robotic collectors that satisfy environmental audits. Vegetable and “other” specialty crops also gain traction as modular gripper designs and machine-vision libraries expand, allowing rapid adaptation to new plant geometries each season.

By Farm Environment: Greenhouses Dominate, Open Fields Catch Up

Greenhouse projects attracted 58.2% of 2024 spending. Uniform lighting, controlled humidity, and fixed plant spacing simplify vision-based fruit detection, pushing return on investment below three seasons for tomatoes and cucumbers. Year-round production in controlled environments means robots accumulate higher utilization hours, accelerating depreciation recovery. Growers increasingly link robotic pickers to vertical-farm conveyor belts, enabling continuous flow from vine to pack-house without human touch. Predictive climate-control algorithms fed by robot-captured crop data fine-tune carbon dioxide and light levels, lifting yields by 7-10% versus manual operations.

Open-field adoption is climbing at a 12.6% CAGR. Improvements in high-precision RTK-GPS, multi-sensor fusion, and ruggedized chassis designs allow pick-and-place arms to tolerate dust, rain, and slopes up to 15 degrees. AI-driven route planners now integrate real-time weather feeds, dynamically rerouting harvesters to minimize downtime from sudden showers. Swarm concepts—using smaller, lighter robots working in parallel, reduce soil compaction and improve redundancy during peak harvest windows. As carbon-credit markets start valuing reduced fuel burn and lower soil disturbance, open-field robots gain an additional economic lever beyond labor savings.

Geography Analysis

European growers led with 33.5% global revenue in 2024, reflecting coordinated subsidy frameworks and dense dealer networks. The Netherlands earmarked EUR 680 million (USD 740 million) through its 2024–2027 AgriTech Catalyst program to accelerate farm-robotics commercialization and AI-driven crop-management pilots. Germany funds sustainability demonstrations that couple carbon-credit measurement with automated harvest logs, enabling farmers to monetize verified emission reductions. France’s tech clusters in Brittany and Occitanie supply vision-system start-ups, and Spain integrates robots for delicate stone-fruit crops under severe labor shortages.

Asia-Pacific is the fastest-growing territory at a 14.2% CAGR. China’s state-backed 1-trillion-yuan (USD 138 billion) robotics fund channels significant allocations to smart farming, and provincial buyers leverage bulk orders to reduce per-robot pricing. Japan’s agricultural-drone fleet surpassed 400,000 units in 2025, up 33% year-on-year, illustrating readiness for hybrid air-ground platforms. Australia experiments with private 5G base stations on vast wheat properties where 65% of acreage sits in cellular shadows, enhancing remote equipment control.

North America maintains deep installed capacity owing to large-scale specialty crop estates. California’s Salinas Valley retrofitted entire lettuce lines with automated cutters that halve reliance on seasonal workers. In 2025, John Deere invested USD 20 billion in autonomy, pairing robotic harvesters with digitally twinned planters and sprayers. Canada’s Prairie provinces pilot swarm robotics for canola harvesting, while Mexico positions export-oriented berry growers to adopt pay-per-use robotic services once cross-border leasing regulations finalize.

Competitive Landscape

The smart harvest market shows moderate concentration, with the five largest vendors together controlling 51% of global revenue in 2024. Traditional agricultural-equipment manufacturers still anchor the field, but pure-play robotics specialists are scaling rapidly and diluting legacy dominance. Competitive intensity is rising as platform economics shift from one-off machine sales to data-driven recurring revenue. Vendor differentiation increasingly depends on integrating hardware, edge AI, and cloud analytics into seamless end-to-end offerings.

Incumbents expand their portfolios through heavy Research and Development and targeted acquisitions. Deere and Company committed USD 20 billion to autonomy programs and now embeds machine-vision modules across its harvesting line. Trimble broadened its guidance ecosystem by adding LiDAR-based fruit-picking software, while Bosch introduced a modular sensor suite that retrofits to third-party robots. CNH Industrial partnered with Bluewhite to deploy driverless orchard tractors in California, and Yamaha Motor’s 2025 purchase of Robotics Plus marked its formal entry into ground robotics after years in agricultural drones.

Specialist start-ups focus on narrow high-value applications to outmaneuver slower incumbents. Agrobot’s soft-grip strawberry picker runs robotics-as-a-service contracts that lower customer CAPEX, and Harvest CROO Robotics pilots swarm lettuce harvesters that reduce field time by 40%. Patent filings on end-effector design exceeded 200 in 2024, signaling rising entry barriers for newcomers without deep IP. Standards groups such as the Agricultural Industry Electronics Foundation push interoperability, yet most vendors still guard proprietary data formats. Overall, the landscape earns a concentration score of 6, reflecting solid yet not overwhelming control by the leading suppliers.

Smart Harvest Industry Leaders

Deere & Company

Trimble Inc.

Robert Bosch GmbH

Agrobot

Harvest CROO Robotics LLC.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Biro Power, established by Rajnish Kumar in Bihar, develops battery-powered smart harvesters designed for smallholder farmers in India. The company expanded its production of modular, IoT-integrated machines between 2023 and 2025 to help farmers reduce crop losses and fuel expenses. Biro Power plans to deploy 100,000 harvesters across 10,000 villages by 2030.

- March 2025: Trimble introduced IonoGuard, an RTK GNSS technology that maintains accurate signal tracking during solar storms, reducing disruptions in precision agriculture operations. The technology ensures continuous satellite guidance, improving the reliability of autonomous and smart harvesting systems.

- February 2025: John Deere's 2026 combine harvesters incorporate automated features, including predictive ground speed control and automated harvest settings adjustments, which improve operational efficiency and minimize operator effort. The combines integrate grain sensing technology, automated unloading cameras, and satellite connectivity to increase accuracy and output across varying field environments.

- February 2025: Yamaha Motor Co.'s acquisition of Robotics Plus Ltd. and the formation of Yamaha Agriculture Inc. strengthened its position in the smart harvest market. The integration of robotic orchard vehicles, including Prospr, enables precision spraying, weed control, and yield analytics. These technologies improve harvest efficiency, reduce labor dependency, and support sustainable agricultural practices in Australia, New Zealand, and North America.

Global Smart Harvest Market Report Scope

| Hardware | Harvesting Robots |

| Imaging and Sensor Suites | |

| GPS and Guidance Controllers | |

| Software | |

| Services |

| Robotic Automation Systems |

| Machine Vision and Imaging |

| Autonomous Navigation |

| Cloud and Edge Data Analytics |

| Fruits |

| Vegetables |

| Nuts |

| Others (Herbs, Mushrooms, etc.) |

| Greenhouses |

| Open Fields |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Component | Hardware | Harvesting Robots |

| Imaging and Sensor Suites | ||

| GPS and Guidance Controllers | ||

| Software | ||

| Services | ||

| By Technology | Robotic Automation Systems | |

| Machine Vision and Imaging | ||

| Autonomous Navigation | ||

| Cloud and Edge Data Analytics | ||

| By Crop Type | Fruits | |

| Vegetables | ||

| Nuts | ||

| Others (Herbs, Mushrooms, etc.) | ||

| By Farm Environment | Greenhouses | |

| Open Fields | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the smart harvest market?

The smart harvest market size is USD 21.4 billion in 2025.

How fast is the smart harvest market anticipated to grow?

It is projected to register an 11.4% CAGR and achieve USD 36.7 billion by 2030.

Which component segment leads revenue generation?

Hardware dominates with 62.1% share, reflecting widespread adoption of physical robotic systems.

Which region is growing the fastest in smart harvesting?

Asia-Pacific shows the highest growth, expanding at a 14.2% CAGR through 2030.

Page last updated on: