Agricultural Pheromones Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

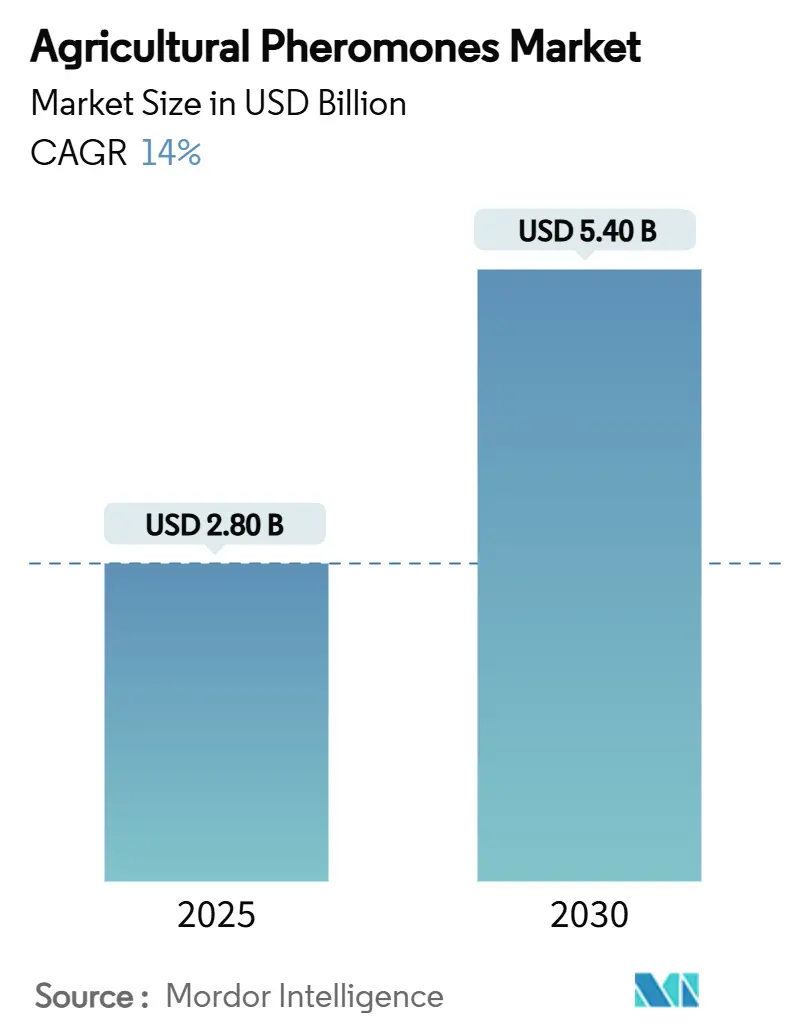

| Market Size (2025) | USD 2.80 Billion |

| Market Size (2030) | USD 5.40 Billion |

| Growth Rate (2025 - 2030) | 14.00% CAGR |

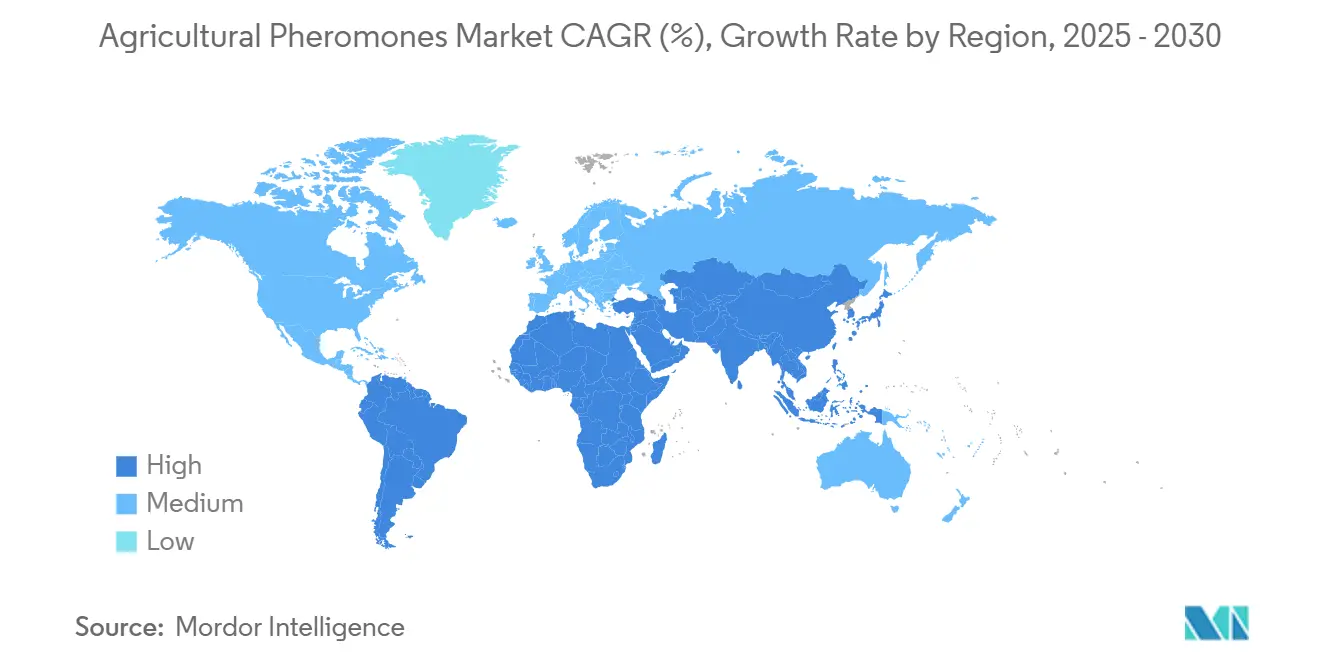

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Agricultural Pheromones Market Analysis by Mordor Intelligence

The agricultural pheromones market size is valued at USD 2.8 billion in 2025 and is on track to reach USD 5.4 billion by 2030, expanding at a 14.0% compound annual growth rate (CAGR). Robust demand stems from growers integrating pheromones into mainstream integrated pest management (IPM) programs that lower residue risk, meet export requirements, and slow chemical-resistance development. Clearer regulatory pathways, such as the United States Environmental Protection Agency (EPA) tolerance exemptions for multiple lepidopteran pheromones applied at rates up to 150 g/acre, accelerate product registration and scale economics. Manufacturers also benefit from steady cost declines in raw materials and encapsulation technologies, making sprayable pheromones competitive with conventional insecticides. Regionally, Europe commands the largest share on the back of strict maximum-residue regulations, while Asia-Pacific registers the fastest growth as government-backed IPM initiatives and high-value horticulture expand acreage. Moderate market consolidation leaves room for both incumbents and start-ups to capture unmet needs in labor-saving formulations and multi-species blends.

Key Report Takeaways

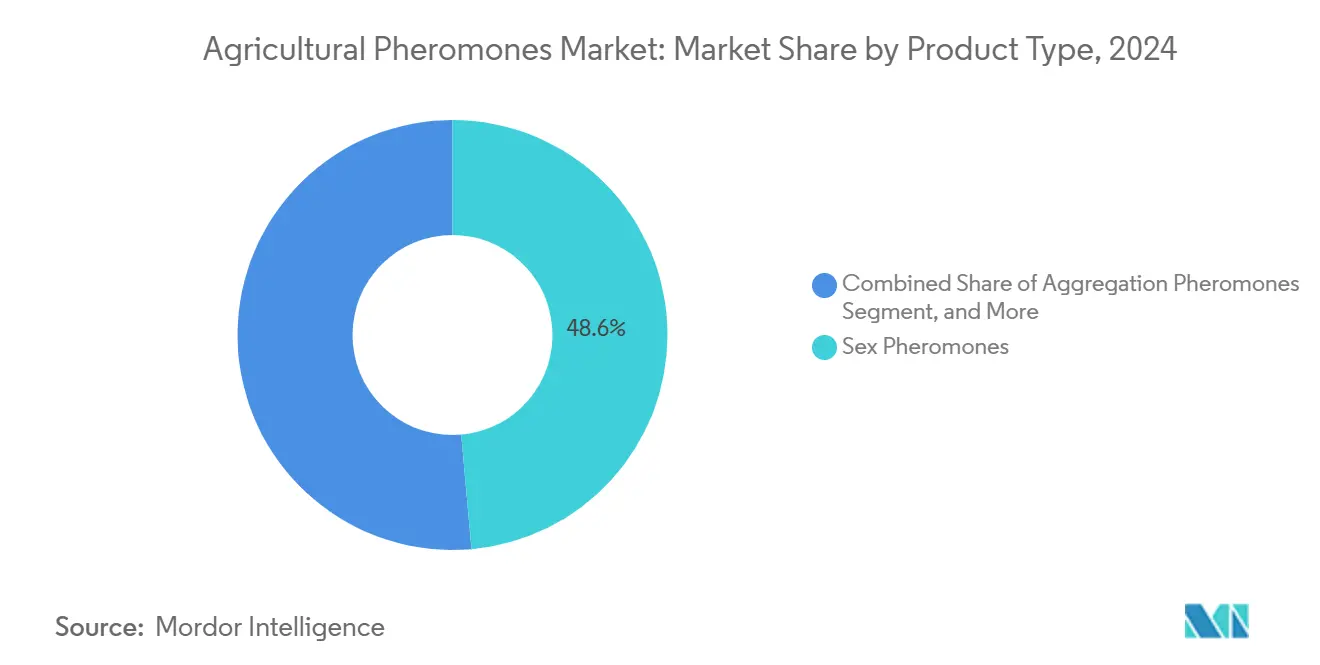

- By product type, sex pheromones led with 48.6% of the agricultural pheromones market share in 2024, while aggregation pheromones are forecast to grow at 18.2% CAGR to 2030.

- By function, mating disruption accounted for a 42.1% share of the market in 2024, and mass trapping is projected to expand at a 16.6% CAGR through 2030.

- By mode of application, dispensers held 54.4% revenue share in 2024, while sprayable pheromones are set to rise at a 21.8% CAGR over 2025-2030.

- By formulation, solid matrix systems commanded a 37.6% share in 2024, whereas microencapsulated products are poised for a 19.1% CAGR to 2030.

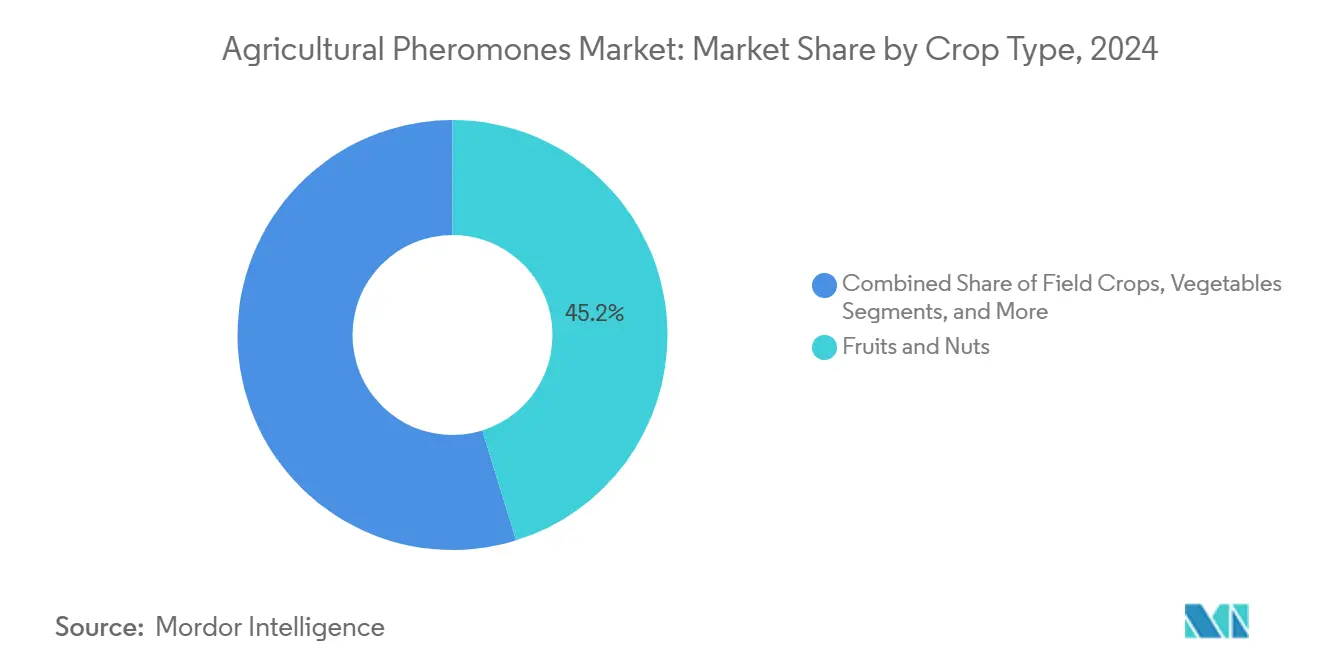

- By crop type, fruits and nuts captured a 45.2% share of the agricultural pheromones market size in 2024, and vegetables represented the fastest-growing segment at a 17.1% CAGR from 2024 to 2030.

- By geography, Europe led with 33.2% revenue share in 2024, and Asia-Pacific is anticipated to grow at 16.4% CAGR to 2030.

- The top five vendors, Suterra (The Wonderful Company), Shin-Etsu Chemical Co., Ltd., Koppert Biological Systems (Koppert Group), Russell IPM Ltd., and Provivi, Inc., collectively controlled 60.5% of global revenue in 2024.

Global Agricultural Pheromones Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent maximum-residue regulations | +3.2% | Europe, North America, and Asia-Pacific | Medium term (2–4 years) |

| Rapid adoption of integrated pest management programs | +2.8% | Global | Short term (≤ 2 years) |

| Expansion of high-value fruit and nut acreage | +2.1% | North America, Europe, and Asia-Pacific | Long term (≥ 4 years) |

| Nano-encapsulation to extend field stability | +1.9% | Global, early adoption in Asia-Pacific | Medium term (2–4 years) |

| Drone-enabled precision dispensing | +1.7% | North America, Europe, and Asia-Pacific | Medium term (2–4 years) |

| Carbon-credit incentives for low-GHG crop protection | +1.4% | Europe, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Maximum-Residue Regulations

Regulatory tightening on pesticide residues pushes growers toward pheromone-based solutions that leave no detectable residues. EPA tolerance exemptions for tomato pinworm and lepidopteran pheromones at application rates up to 200 g/acre streamline registrations and eliminate costly residue studies, lowering barriers for new entrants[1]Source: Environmental Protection Agency, “Pheromone Tolerance Exemptions,” Environmental Protection Agency, epa.gov. Europe’s farm-to-fork strategy and the United Kingdom Sustainable Farming Incentive that pays growers GBP 45/ha (USD 58.5/ha) for eliminating insecticide use directly improve the return on investment for pheromones. These measures accelerate adoption in export-oriented sectors where residue compliance is critical.

Rapid Adoption of Integrated Pest Management Programs

The agricultural pheromones market benefits from multi-year government funding that validates biological controls and trains growers. The USDA Applied Agriculture Research and Development Program channels grants toward pheromone discovery and extension services, reducing perceived risk for producers[2]Source: U.S. Department of Agriculture, “Crop Protection and Pest Management Program 2024 Awards,” U.S. Department of Agriculture, usda.gov. The Food and Agriculture Organization highlights pheromone tools in its regional plant-protection roadmaps, while Asia-Pacific field schools integrate mating-disruption modules for rice and cotton growers[3]Source: Food and Agriculture Organization, “Regional IPM Roadmap for Asia-Pacific,” Food and Agriculture Organization, fao.org. Public endorsement shortens the learning curve and widens market reach, especially among smallholders.

Expansion of High-Value Fruit and Nut Acreage

Rising acreage devoted to premium apples, almonds and wine grapes makes pheromone programs economically attractive. Field studies in European orchards show mating disruption curbs insecticide sprays by 90% and cuts overall pest-management spend by 25% over 10 years, safeguarding profit margins even at higher per-acre costs. Export premiums for residue-free fruit further tilt the equation in favor of pheromones, and chemical-resistance pressures reinforce the switch.

Nano-Encapsulation to Extend Field Stability

Nano-encapsulated and core-shell micro-fiber systems protect active ingredients from UV degradation and offer controlled release over 60-80 days,double the life of conventional dispensers. These innovations eliminate cold-chain dependence, enabling deployment in hot climates and lowering application frequency. Companies scaling encapsulation capacity can price competitively, boosting volumes and accelerating global penetration.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost versus conventional insecticides | -2.4% | Global, strongest in developing regions | Short term (≤ 2 years) |

| Narrow pest-spectrum efficacy | -1.8% | Global | Medium term (2–4 years) |

| Lengthy registration timelines | -1.2% | Europe and North America | Long term (≥ 4 years) |

| Cold-chain logistics for shelf-life | -0.9% | Hot-climate regions | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High Cost Versus Conventional Insecticides

Conventional insecticides often cost a fraction of pheromone programs, limiting uptake among price-sensitive growers. Emerging production pathways, such as genetically modified Camelina that biosynthesizes pheromone precursors, could slash per-hectare costs from USD 400 to USD 70-125 and remove a key hurdle for broad-acre crops. Sprayable formulations that piggyback on existing equipment further shrink total program costs by eliminating manual dispenser placement.

Narrow Pest-Spectrum Efficacy

Pheromones excel at single-species control but struggle in polyculture systems where growers battle multiple pests simultaneously. Researchers are experimenting with pheromone cocktails and oviposition-deterring blends to widen target coverage, though regulatory review for multi-species products adds complexity. Advances in bioinformatics and semiochemical libraries promise faster identification of synergistic blends that could address this gap.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Sex Pheromones Retain Primacy While Aggregation Emerges

Sex pheromones hold 48.6% of the agricultural pheromones market share in 2024 on the strength of well-documented efficacy in mating-disruption orchards. Their long commercialization history means growers and regulators trust performance claims. Aggregation pheromones, although currently smaller, are growing at 18.2% CAGR as mass-trapping programs expand in stored-grain and palm plantations. The agricultural pheromones market size for aggregation blends is forecast to accelerate once unit costs fall and multi-lure dispensers enter the market.

Ongoing innovation focuses on sprayable sex pheromones such as Suterra CheckMate VMB-F that fit standard air-blast rigs and provide eight-week residual control. Adoption widens across California vineyards and Turkish stone-fruit orchards, where labor shortages limit manual dispenser deployment. Aggregation pheromones gain traction in warehouse pest management, where non-toxic mass-trapping helps food processors maintain zero-tolerance standards.

By Function: Mating Disruption Dominates but Mass Trapping Gains Speed

Mating disruption generated 42.1% of total revenue in 2024 of the agricultural pheromones market, supported by wide regulatory acceptance and consistent grower ROI. This functional lead reflects the agricultural pheromones market preference for season-long suppression of reproductive cycles in codling moth, peach twig borer, and navel orangeworm. Mass trapping, at 16.6% CAGR, benefits from innovations in high-capacity lures and smart traps that transmit catch data to phones, enabling rapid treatment decisions.

China’s intelligent mating-disruption network showcased 92.3% efficacy against rice stem borer while lowering insecticide sprays in Guangxi paddies. Such data reinforce the status of mating disruption as a standalone control in high-value crops. Mass-trapping vendors utilize IoT sensors that alert growers when thresholds are triggered, prompting additional lure placement or spot sprays, thereby bridging monitoring and control in a single device.

By Mode of Application: Dispensers Maintain Lead as Sprayables Accelerate

Dispenser systems, whether hand-applied twist ties or reservoir clips, commanded 54.4% revenue share in 2024 of the agricultural pheromones market, owing to reliable dose delivery across entire seasons. They remain preferred in perennial crops where a single application protects multiple flushes of fruit. The segment still captures the bulk of the agricultural pheromones market revenues, even as sprayable pheromones experience a 21.8% CAGR.

Sprayables’ momentum stems from its compatibility with farm sprayers and drones, which can trim labor by up to 60% and facilitate large-acreage coverage in a single day. Early adopters report a 90% reduction in navel orangeworm damage in almonds when using micro-encapsulated sprays that adhere to tree bark and slowly off-gas active volatiles. Trap-based modes continue serving monitoring niches in precision agriculture workflows.

By Crop Type: Fruits and Nuts Anchor Revenue, Vegetables Accelerate

Fruit and nut orchards accounted for 45.2% of the agricultural pheromones market's 2024 sales, as premium output prices offset higher per-acre costs and residue-free certificates unlock export markets. The agricultural pheromones market size in orchards is anticipated to continue expanding as labor-saving sprayables address installation bottlenecks. Vegetables, advancing at 17.1% CAGR, are the breakout opportunity.

Protected-culture tomato and cucumber farms utilize pheromone mass trapping to meet retailer pesticide-reduction commitments. Field crops lag, but partnerships, such as Syngenta and Provivi’s Yellow Stem Borer Eco-Dispenser for rice, aim to shift perceptions. Cost-cutting breakthroughs in biologically produced pheromones are anticipated to catalyze entry into corn and soybean rotations by 2030.

By Formulation: Solid Matrix Holds Share but Microencapsulation Surges

Solid-matrix captured 37.6% of the 2024 agricultural pheromones market sales due to its proven season-long release and straightforward manufacturing. Microencapsulated records the fastest uptake at 19.1% CAGR as suppliers fine-tune wall materials that resist UV and moisture. The agricultural pheromones market share for encapsulated offerings is poised to expand further once production costs drop.

Microcapsules maintain a stable pheromone payload at 40 °C, making them particularly attractive in equatorial regions where cold-chain reliability is limited. Core-shell nanofiber research shows 60% active release over 80 days, outperforming slow-release clay granules by a wide margin. Liquid suspensions also simplify blend customization, allowing rapid prototyping of multi-species products.

Geography Analysis

Europe retained 33.2% market share in 2024 of the agricultural pheromones market owing to stringent residue limits and well-funded advisory networks that disseminate IPM protocols. Germany, France, and Spain integrate mating-disruption checklists into national crop insurance guidelines, effectively normalizing adoption. Public subsidies, such as the Sustainable Farming Incentive, which pays GBP 45/ha (USD 58.5/ha) for insecticide-free practices, boost pheromone profitability and sustain leadership.

Asia-Pacific is the fastest mover at 16.4% CAGR through 2030. China’s ministry-sponsored demonstration plots document 92.3% rice stem-borer control with networked dispensers, building local confidence. India’s horticulture clusters in Maharashtra and Karnataka embrace sprayable pheromones to protect export-oriented grapes and mangoes. Japan and Australia deploy drones for precision dispensing in tea and almond orchards, respectively. Multilateral programs, such as the BRAINS initiative with CAD 20 million (USD 15 million) in funding, extend biological-control training into Southeast Asian and African smallholder systems, thereby widening the addressable base.

North America advances steadily at 12.1% CAGR as EPA tolerance exemptions spur accelerated launches and the USDA Crop Protection and Pest Management grants finance university extension trials. California’s specialty-crop belt remains the largest single user of sex-pheromone dispensers, while Washington apple growers pilot drone swarms for large-scale deployment. Canada’s berry sector tests microencapsulated sprays to meet retailer residue mandates, reinforcing regional momentum.

Competitive Landscape

The agricultural pheromones market shows moderate concentration, with the top five suppliers accounting for 60.5% of global revenue, leaving meaningful headroom for innovators. Suterra (The Wonderful Company) leads with the most prominent share, leveraging vertical integration within The Wonderful Company to pilot products across extensive orchard acreage and compress development cycles. Shin-Etsu Chemical Co., Ltd. follows with a dominant position with strong Asia presence and proprietary polymer technology for long-life dispensers.

Strategic alliances are accelerating. Syngenta Biologicals is allied with Provivi to co-develop region-specific lures for the Yellow Stem Borer and Fall Armyworm in Asian cereals, due for a 2026 rollout. BASF signaled renewed focus on its BioSolutions platform and is weighing an IPO of its Agricultural Solutions division to unlock capital for acquisitions and scale encapsulation plants. Meanwhile, start-ups target cost disruption: researchers demonstrated Camelina-based biosynthesis that could bring pheromone production costs down to USD 70-125 per kg versus current USD 400.

Incumbents respond by expanding manufacturing footprints. Givaudan doubled its encapsulation capacity in Mexico to serve Latin American citrus and coffee estates, while Koppert ramps up dispenser assembly in the Netherlands to shorten lead times for European customers. Digital integration is another battleground. RapidAim’s IoT moth-detection network feeds real-time alerts into farm-management software, positioning the company as a data-driven partner rather than a pure input vendor.

Agricultural Pheromones Industry Leaders

Suterra (The Wonderful Company)

Shin-Etsu Chemical Co., Ltd.

Koppert Biological Systems (Koppert Group)

Russell IPM Ltd.

Provivi, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Givaudan expanded its encapsulation capacity at the Pedro Escobedo site in Mexico, doubling output to meet demand in South America.

- October 2024: BASF announced it is considering an IPO for its Agricultural Solutions division to accelerate growth in biologicals.

- September 2024: Syngenta Biologicals and Provivi unveiled a partnership to commercialize YSB Eco-Dispenser and FAW Eco-Granules for Asian rice and corn systems, targeting 2026 launch.

- July 2024: Researchers published proof-of-concept results for genetically modified Camelina plants that cut pheromone production costs by more than 70%.

Global Agricultural Pheromones Market Report Scope

| Sex Pheromones |

| Aggregation Pheromones |

| Others |

| Mating Disruption |

| Mass Trapping |

| Monitoring and Detection |

| Dispensers |

| Traps |

| Sprayable Pheromones |

| Microencapsulated |

| Solid Matrix |

| Liquid Formulations |

| Field Crops |

| Fruits and Nuts |

| Vegetables |

| Other Crops |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Kenya | |

| Rest of Africa |

| By Product Type | Sex Pheromones | |

| Aggregation Pheromones | ||

| Others | ||

| By Function | Mating Disruption | |

| Mass Trapping | ||

| Monitoring and Detection | ||

| By Mode of Application | Dispensers | |

| Traps | ||

| Sprayable Pheromones | ||

| By Formulation | Microencapsulated | |

| Solid Matrix | ||

| Liquid Formulations | ||

| By Crop Type | Field Crops | |

| Fruits and Nuts | ||

| Vegetables | ||

| Other Crops | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the agricultural pheromones market in 2025?

The market is valued at USD 2.8 billion in 2025, reflecting growing adoption in mainstream IPM programs.

How fast is the agricultural pheromones market anticipated to grow?

It is projected to expand at a 14.0% CAGR, reaching USD 5.4 billion by 2030.

Which region holds the largest market share today?

Europe leads with 33.2% share due to strict maximum-residue regulations and robust IPM infrastructure.

Why are sprayable pheromone formulations gaining attention?

Sprayables align with existing farm equipment, cut labor up to 60% and are growing at a 21.8% CAGR.

What is the biggest obstacle to wider adoption of pheromones?

High per-hectare costs relative to conventional insecticides remain the primary barrier, although new biosynthesis methods may cut costs by more than 70%.

Which crop segment is expanding the fastest for pheromone use?

Vegetables show the highest growth at a 17.1% CAGR as protected cultivation seeks residue-free solutions.

Page last updated on: