Sugarcane Harvesters Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

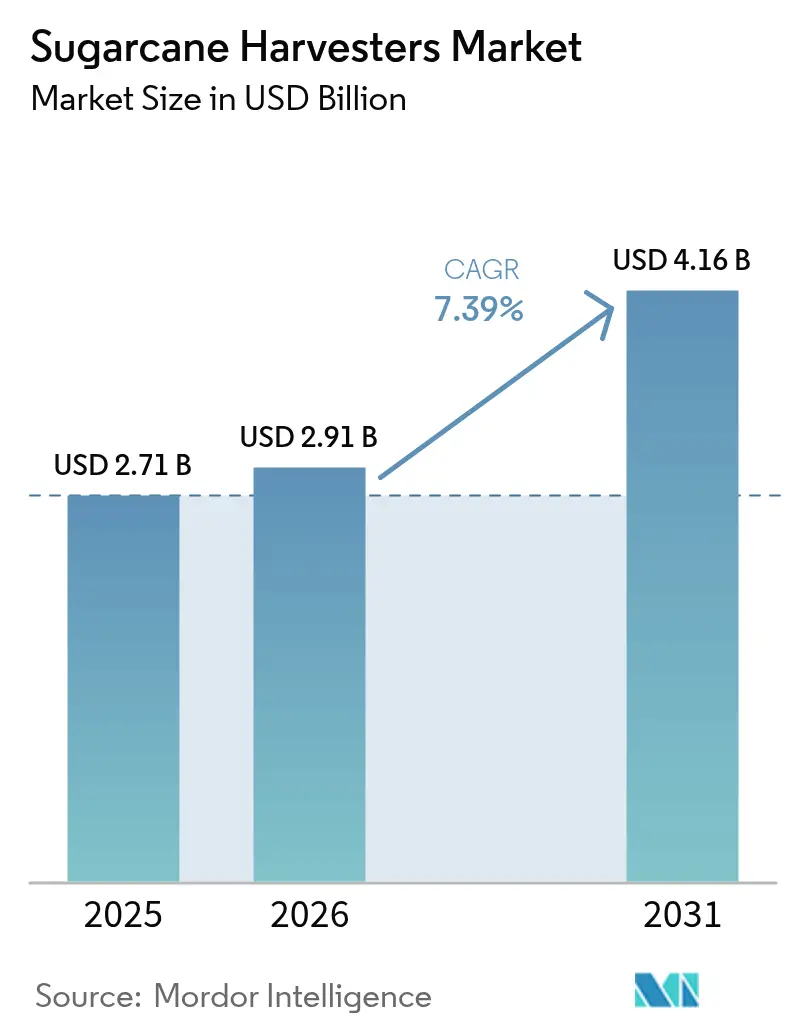

| Market Size (2026) | USD 2.91 Billion |

| Market Size (2031) | USD 4.16 Billion |

| Growth Rate (2026 - 2031) | 7.39% CAGR |

| Fastest Growing Market | Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sugarcane Harvesters Market Analysis by Mordor Intelligence

The sugarcane harvesters market size in 2026 is estimated at USD 2.91 billion, growing from 2025 value of USD 2.71 billion with 2031 projections showing USD 4.16 billion, growing at 7.39% CAGR over 2026-2031. The market growth is primarily driven by increased mechanization in agriculture, labor shortages, and stricter regulatory requirements. Brazil's agricultural sector demonstrates this trend, with almost complete mechanization of its sugarcane harvesting operations, as reported by Energy Research Company (EPE). CNH Industrial N.V.'s investment in Bem Agro's artificial intelligence mapping technology improves sugarcane harvesting operations through efficient field navigation, reduced maintenance downtime, and sustainable agricultural practices in major sugarcane-producing regions.[1]Source: CNH Industrial, “CNH takes minority investment in drone imaging AI company Bem Agro,” Media.cnh.com The Asia-Pacific region holds the largest market share due to extensive sugarcane cultivation in China, India, Thailand, and Indonesia. According to FAOSTAT, the sugarcane harvested area in India and Thailand increased by 13.7% and 14.8%, respectively, from 2022 to 2023. Africa represents an emerging market opportunity, supported by agricultural modernization programs and improved access to equipment financing.

Key Report Takeaways

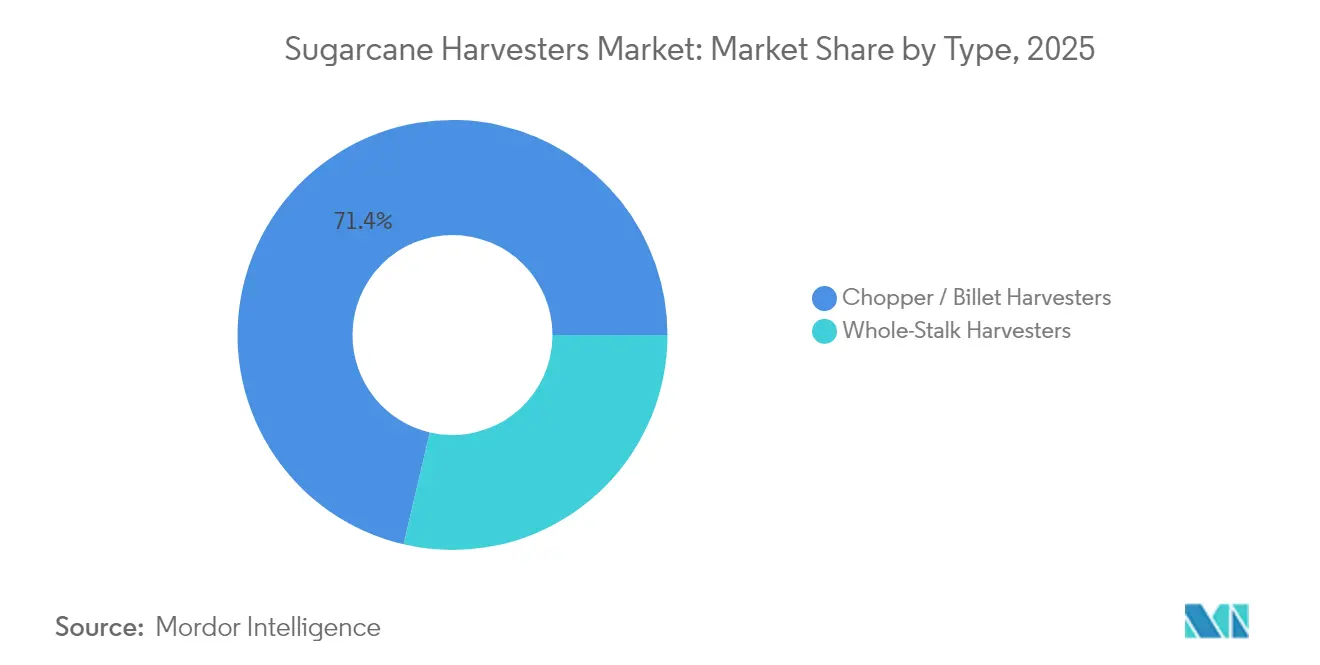

- By type, chopper/billet units led with 71.35% of the sugarcane harvester market share in 2025, whole-stalk harvesters maintain a CAGR of 6.89% to 2031.

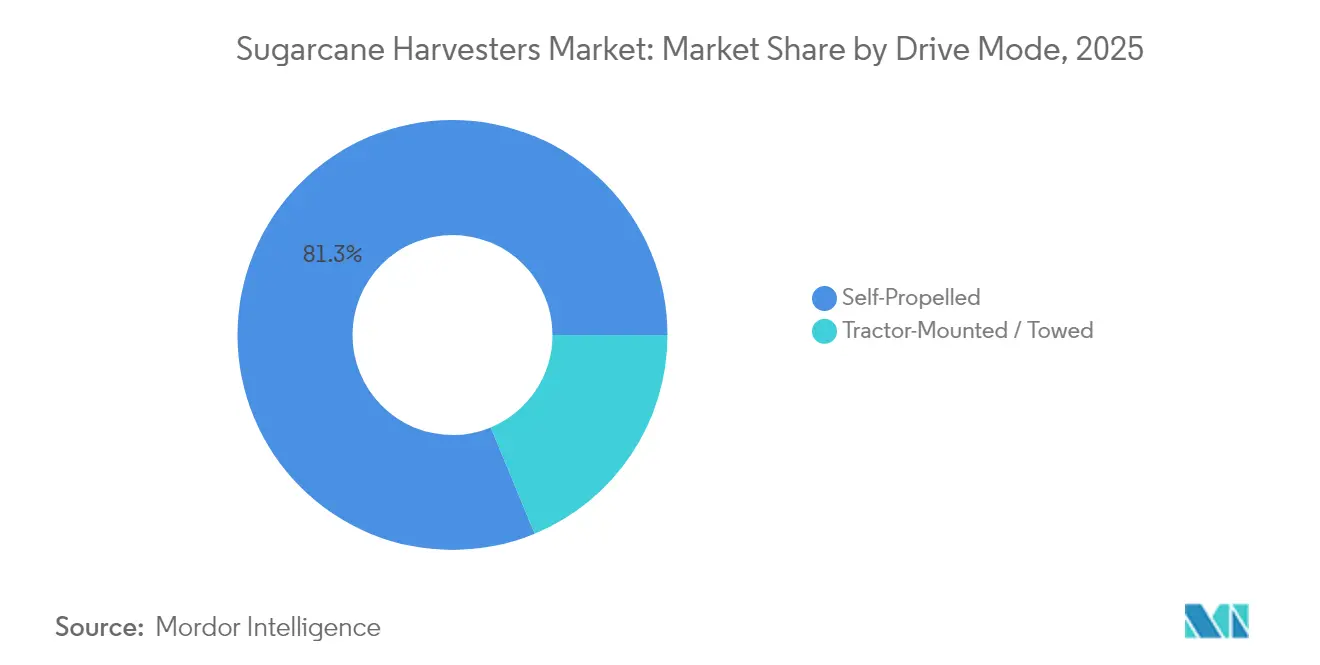

- By drive mode, self-propelled machines held 81.25% of the sugarcane harvesters market size in 2025, while the same segment is on track to advance at an 8.23% CAGR through 2031.

- By row capacity, single-row configurations accounted for 67.20% of the sugarcane harvesters market size in 2025, multi-row systems are poised to grow at a 7.55% CAGR between 2026 and 2031.

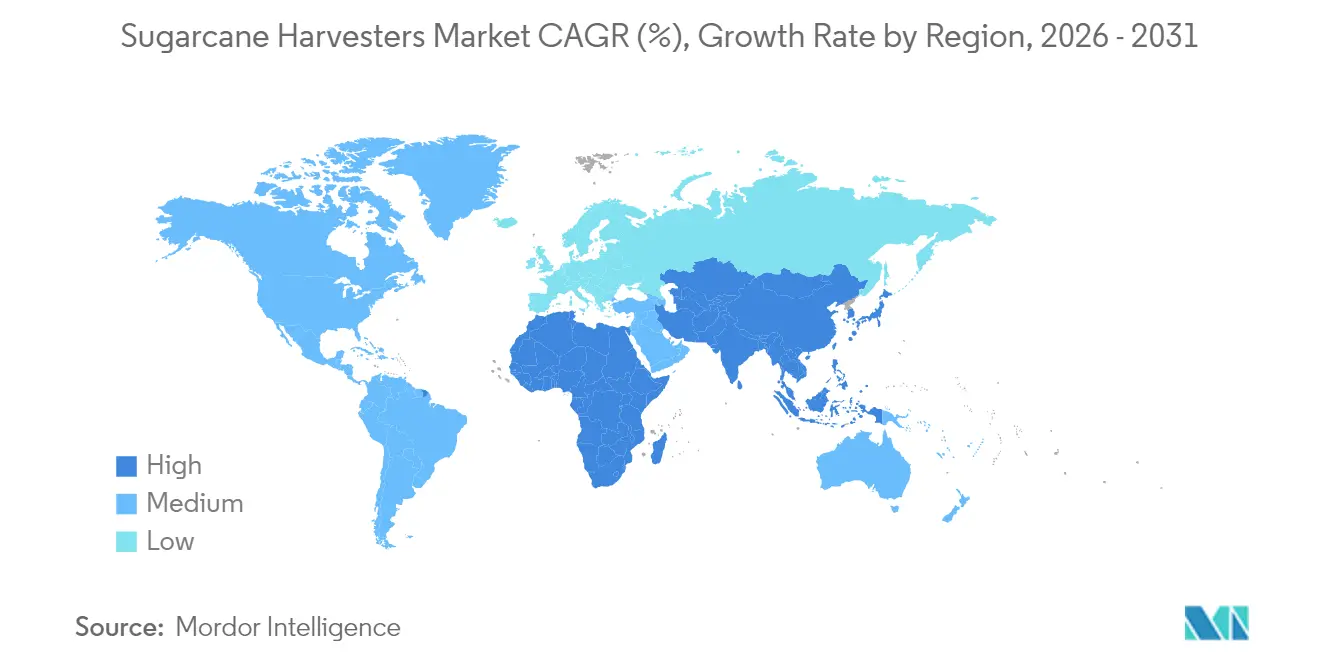

- By geography, Asia-Pacific held 54.65% of global revenue in 2025, whereas Africa shows the fastest 7.49% CAGR to 2031.

- CNH Industrial N.V. and Deere and Company together controlled the majority of the market share in 2024, underscoring high competitive concentration.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Sugarcane Harvesters Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mechanized-harvesting Mandates in Major Producing Countries | +1.8% | Brazil, India, Thailand, China | Medium term (2-4 years) |

| Permanent Farm-labor Shortages Pushing Adoption of Compact Self-propelled Units | +1.5% | Asia-Pacific, South America | Long term (≥ 4 years) |

| Sugar-ethanol Flex-mill Expansion Demanding Higher Field-throughput Machinery | +1.2% | Brazil, India, Thailand | Medium term (2-4 years) |

| Carbon-credit Premiums for Green-cane Harvesting (No Field-burn) Driving Equipment Spend | +0.9% | Vietnam, Brazil, global pilot zones | Long term (≥ 4 years) |

| OEM Telematics / AI Modules that Cut Billet Losses | +0.8% | North America, Europe, advanced Asia-Pacific | Short term (≤ 2 years) |

| Multi-row Harvester Introductions Lowering Operating Cost | +0.7% | Large farms worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Mechanized-harvesting Mandates in Major Producing Countries

Government regulations prohibiting pre-harvest burning and mandating mechanical harvesting are transforming sugarcane production practices. The Office of the Cane and Sugar Board (OCSB), Thailand, has set an ambitious target to reduce the burning of sugar cane plantations prior to harvest by up to 90% during the 2024-25 harvest season, with the aim of significantly lowering harmful PM2.5 fine particle emissions. Brazil's implementation of these regulations reduced labor requirements by 64%, establishing mechanical harvesting as the primary method.[2]Source: Food and Agriculture Organization, “Labor impacts of agricultural automation,” Openknowledge.fao.org These regulatory measures indicate a fundamental shift toward mechanized, efficiency-focused sugarcane production.

Permanent Farm-labor Shortages Pushing Adoption of Compact Self-propelled Units

Demographic changes and urban migration are reducing the agricultural workforce, necessitating increased mechanization and higher wages. In China, the National Bureau of Statistics (NBS) reported urbanization reached 66.16% in 2023, as younger populations moved from rural areas. The adoption of portable harvesters has enhanced operational efficiency and reduced manual labor requirements. According to Eurostat, in the European Union, agricultural wages increased by 12% to USD 34.4 per hour, primarily due to reduced seasonal immigrant labor availability, highlighting the necessity of compact self-propelled sugarcane harvester units.

Sugar-ethanol Flex-mill Expansion Demanding Higher Field-throughput Machinery

Increased sugar production and growing biofuel demand drive mill expansion and processing upgrades. Significant machinery investments indicate a shift toward integrated processing systems. Large-scale production projects increase field capacity requirements, necessitating rapid modernization by growers and processors. The integrated sugar-ethanol mill model becomes essential for sugarcane production regions, combining energy generation with sugar refining.

OEM Telematics / AI Modules that Cut Billet Losses

Equipment now incorporates sensors that optimize cutting height and billet quality during operation. Manufacturing companies expand these technological capabilities throughout primary sugarcane production regions. The implementation of predictive maintenance systems improves equipment reliability and reduces operational interruptions, enhancing harvesting fleet management. These monitoring systems enable field-level data analysis, improving yield and equipment durability.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High-price for High-capacity Machines in Developing Regions | -1.2% | Africa, Southeast Asia, South America | Medium term (2-4 years) |

| Limited After-sales Service Network in Rural Areas | -0.8% | Developing regions worldwide | Long term (≥ 4 years) |

| Cane-variety Mismatch with Existing Cutter-base Designs Raising Stool Damage | -0.6% | India, China, minor geographies | Medium term (2-4 years) |

| Financing Barriers as Harvesters Seldom Qualify for Green-asset Tax Credits | -0.5% | Small farms in emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High-price for High-capacity Machines in Developing Regions

The significant capital requirements for high-capacity harvesting equipment prevent many small-scale growers from mechanizing their operations. This limited access to modern machinery has led to productivity declines in several regions. While mechanical harvesting reduces per-ton costs over time, the substantial initial investment remains prohibitive. The industry is exploring financing options and cooperative ownership models as potential solutions. However, without broader access to technology, mechanization may increase existing inequalities within the sugarcane sector.

Limited After-sales Service Network in Rural Areas

The concentration of equipment dealers in urban areas results in delayed repairs during critical harvest periods, affecting crop quality and timing. Rural farmers experience extended downtimes and logistical challenges when equipment malfunctions. While predictive maintenance technologies show potential, their effectiveness depends on reliable data connectivity. The inconsistent digital infrastructure in many agricultural regions limits the use of remote diagnostics. Improving service coverage across all farming areas is crucial for realizing the full benefits of mechanization.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Chopper Designs Dominate Efficiency Gains

Chopper-style harvesters dominate the sugarcane harvesters market size, accounting for 71.35% of the 2025 revenue. These machines are the primary choice for large-scale operations due to their compatibility with high-tonnage mills and performance in leafy cane conditions. The machines feature upgraded blades and extractors that increase throughput and minimize downtime. Integration with smart systems enables automatic adjustment of knife pressure and trash separation, improving operational efficiency across varying field conditions. Whole-stalk harvesters retain their market presence in specialized segments where minimal juice loss is essential, particularly in premium sugar production.

Whole-stalk harvesters maintain a CAGR of 6.89%, supported by demand from premium sugar producers and regions focusing on juice retention through 2031. With increasing field burn restrictions, chopper designs provide enhanced residue management capabilities and reduced clogging. Manufacturers are developing chopper configurations specific to regional agronomic requirements, combining mechanical reliability with precise harvesting capabilities to address environmental regulations and operational requirements.

By Drive Mode: Self-propelled Units Lead Automation

Self-propelled sugarcane harvesters constitute the market's automation core, capturing 81.25% of the sugarcane harvesters market share in 2025 and achieving an 8.23% CAGR. These machines optimize operations through thousands of automatic adjustments daily to improve fuel efficiency and minimize human error. Their market position reflects the transition to precision agriculture, incorporating GPS, yield monitors, and machine-to-machine connectivity as standard features. Tractor-mounted and towed equipment remain relevant for diversified farms, offering cross-crop flexibility despite limited automation capabilities.

Self-propelled units connect to cloud-based platforms for performance analysis and operational guidance. These harvesters integrate into smart farming strategies through expanding digital ecosystems. Manufacturers are developing driver-optional technologies toward autonomous harvesting. Self-propelled systems address rising labor costs and sustainability requirements while providing scalable solutions.

By Row Capacity: Multi-row Systems Gain Traction

Single-row harvesters maintain 67.20% market share in 2025 due to existing field layouts, while multi-row systems advance at a 7.55% CAGR. Dual-row and larger heads demonstrate efficiency benefits, reducing field passes and fuel usage. Brazil's Center-South region exemplifies this transition to wider rows. Manufacturers address soil compaction and machine weight through lighter alloys and wide-contact tracks.

Field tests demonstrate increased biomass recovery without compromising billet quality in multi-row systems. Variable row-spacing capabilities allow broad heads to operate in mixed-width plantations. Multi-row harvesters provide efficiency advantages while minimizing environmental impact, offering practical solutions for modernizing harvesting operations.

Geography Analysis

Asia-Pacific holds a 54.65% of the Sugarcane Harvester market share, supported by extensive cultivation areas and government policies. China and India are increasing their mechanization investments to address labor shortages and operational costs. In India, Maharashtra's cooperative mills are providing joint financing for mechanical harvesters to ensure efficient harvesting and reduce reliance on seasonal workers. Thailand's government is offering subsidies to increase adoption among mid-sized farmers. The region is seeing increased collaboration between local manufacturers and global equipment makers to develop harvesting technologies suited to local conditions.

Africa, despite its current smaller market share, is growing at a 7.49% CAGR. Research indicates substantial cost reductions through mechanization compared to manual harvesting, particularly in Sudan. South Africa is advancing technologically by incorporating innovations like spray drones for crop management. African governments are working with international financial institutions to create equipment financing options, indicating an industry-wide transition to mechanized and data-based farming practices.

South America maintains its market position, with Brazil producing 705 million metric tons in 2023/24. Colombia and Peru follow Brazil in the adoption of mid-capacity harvester models. Environmental regulations are directing farmers toward green-cane harvesting and ethanol production, while digital solutions enhance operations. In North America, Louisiana's sugar industry is implementing automation to manage labor costs and comply with trade requirements. Europe and the Middle East, with smaller market shares, are prioritizing sustainable and specialty sugar production, increasing demand for efficient, environmentally conscious harvesting equipment.

Competitive Landscape

The sugarcane harvester market remains moderately consolidated, with the top five manufacturers controlling a major share of the sugarcane harvester market size. CNH Industrial N.V. and Deere & Company lead through comprehensive product portfolios and digital platforms. These companies invest in AI, sensor technologies, and connectivity solutions to improve machine intelligence and field performance. Their market dominance provides significant bargaining power with growers, enabling them to influence pricing, service models, and technology standards across regions. The companies expand their presence in emerging markets through strategic partnerships with domestic manufacturers.

Companies compete through new product launches, acquisitions, and regional collaborations. Service differentiation has become crucial, with dealers providing uptime guarantees, remote diagnostics, and integrated software packages that combine agronomic insights with machine analytics. Contract-harvest service providers have emerged as key buyers, focusing on total ownership costs, rapid parts availability, and fleet management tools for mixed-brand operations. Regional manufacturers in China and Thailand gain market share by serving cost-sensitive buyers through local service networks, increasing competition, and emphasizing operational efficiency and service reliability.

Regional manufacturers from Asia are expanding into the mid-tier segment with products designed for cost-sensitive buyers. The market competition now focuses on predictive maintenance, automation capabilities, and financing packages with sustainability incentives. Safety and emissions regulations continue to create entry barriers for new companies while reinforcing the position of multinational brands in the sugarcane harvester market.

Sugarcane Harvesters Industry Leaders

Deere & Company

CNH Industrial N.V.

AGCO Corporation

Zoomlion Heavy Industry Science and Technology Co., Ltd.

Tirth Agro Technology Private Limited (Shaktiman Agro)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: CNH Industrial N.V.'s Case IH developed and tested an ethanol-powered Austoft 9000 sugarcane harvester in Brazil. The current model uses an FPT Cursor 11 diesel engine, and the company is developing ethanol-compatible technology to support sustainable farming practices.

- May 2024: LiuGong launched its S935TA sugarcane harvester at Agrishow Brazil. The company initiated field trials across Brazil to optimize the harvester's performance across different cultivation conditions, emphasizing the machine's durability and fuel efficiency.

- July 2023: Case IH has launched its latest Austoft 9000 sugarcane harvester series in the Middle East and Africa region. It integrates a more powerful 420 hp FPT Cursor 11 engine with an intelligent hydraulic system, delivering increased working capacity at reduced operating costs.

Global Sugarcane Harvesters Market Report Scope

A sugarcane harvester is a large piece of agricultural machinery used to harvest and partially process sugarcane by cutting the stalks at the base, stripping leaves, and removing dust and dirt particles. The sugarcane harvesters market is segmented by type into whole stalk harvesters and chopper harvesters and geography into North America, Europe, Asia-Pacific, South America, and Africa. The report offers the market size and forecasts for volume (units) and value (USD) for all the above segments.

| Whole-Stalk Harvesters |

| Chopper / Billet Harvesters |

| Self-Propelled |

| Tractor-Mounted / Towed |

| Single-Row |

| Multi-Row |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | France |

| Spain | |

| Portugal | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Thailand | |

| Indonesia | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Sudan | |

| Rest of Africa |

| By Type | Whole-Stalk Harvesters | |

| Chopper / Billet Harvesters | ||

| By Drive Mode | Self-Propelled | |

| Tractor-Mounted / Towed | ||

| By Row-Capacity | Single-Row | |

| Multi-Row | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | France | |

| Spain | ||

| Portugal | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Thailand | ||

| Indonesia | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Sudan | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the Sugarcane Harvesters Market in 2026?

It is valued at USD 2.91 billion, rising toward USD 4.16 billion by 2031.

Which region leads sales of sugarcane harvesters?

Asia-Pacific accounts for 54.65% of global revenue due to extensive cultivation in China, India, Thailand, and Indonesia.

What segment grows the fastest in drive mode?

Self-propelled units register an 8.23% CAGR, driven by labor constraints and automation benefits.

Who are the top players in the market?

CNH Industrial N.V. and Deere & Company together hold nearly half of the total revenue, followed by a small group of other global OEMs.

Page last updated on: