Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 12.74 Billion |

| Market Size (2031) | USD 16.48 Billion |

| Growth Rate (2026 - 2031) | 5.28% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

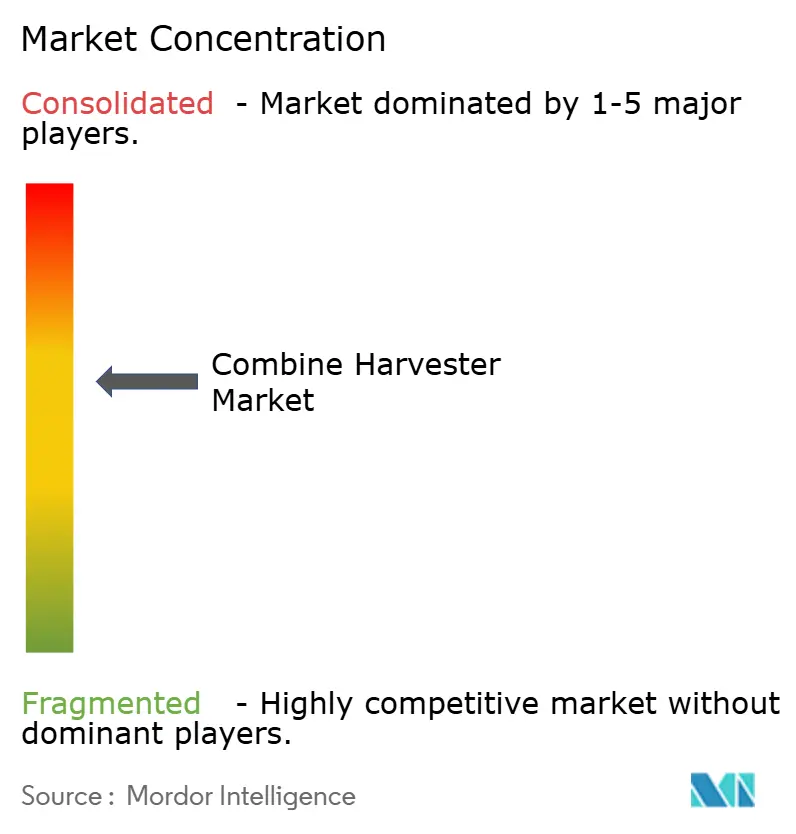

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Combine Harvester Market Analysis by Mordor Intelligence

The combine harvester market size in 2026 is estimated at USD 12.74 billion, growing from 2025 value of USD 12.10 billion with 2031 projections showing USD 16.48 billion, growing at 5.28% CAGR over 2026-2031. The outlook reflects sturdy demand for high-capacity harvesters, steady adoption of precision agriculture suites, and manufacturers' pivot toward embedded software that monetizes data analytics. Rising government subsidies for mechanization across the Asia-Pacific, persistent rural labor shortages in developed economies, and a corporate shift toward subscription-based service models collectively reinforce the upward revenue trajectory. Competitive pressure now centers on achieving throughput gains, readiness for autonomy, and soil-friendly chassis redesigns that comply with emerging compaction regulations. Rapid mechanization in China and India, supportive European programs, and North American right-to-repair legislation are reshaping buyer priorities.

Key Report Takeaways

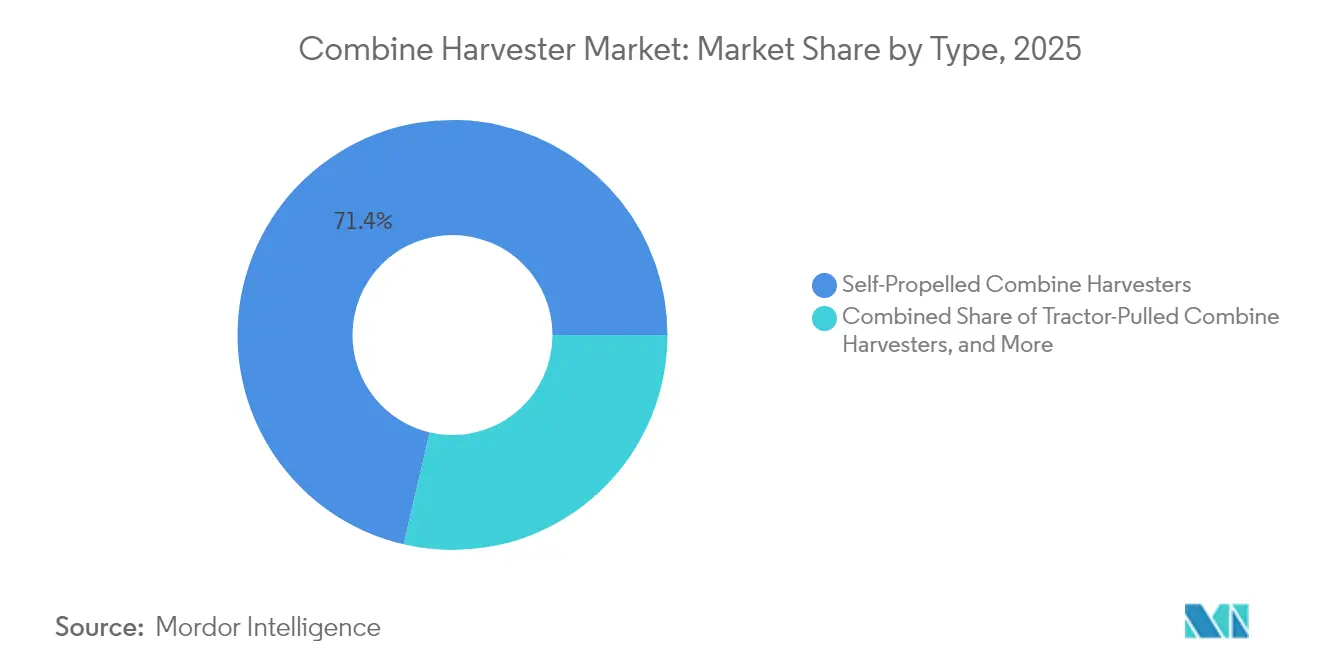

- By type, self-propelled models led the combine harvester market with a 71.35% share in 2025. The tractor-pulled combine is projected to advance at a 7.35% CAGR through 2031.

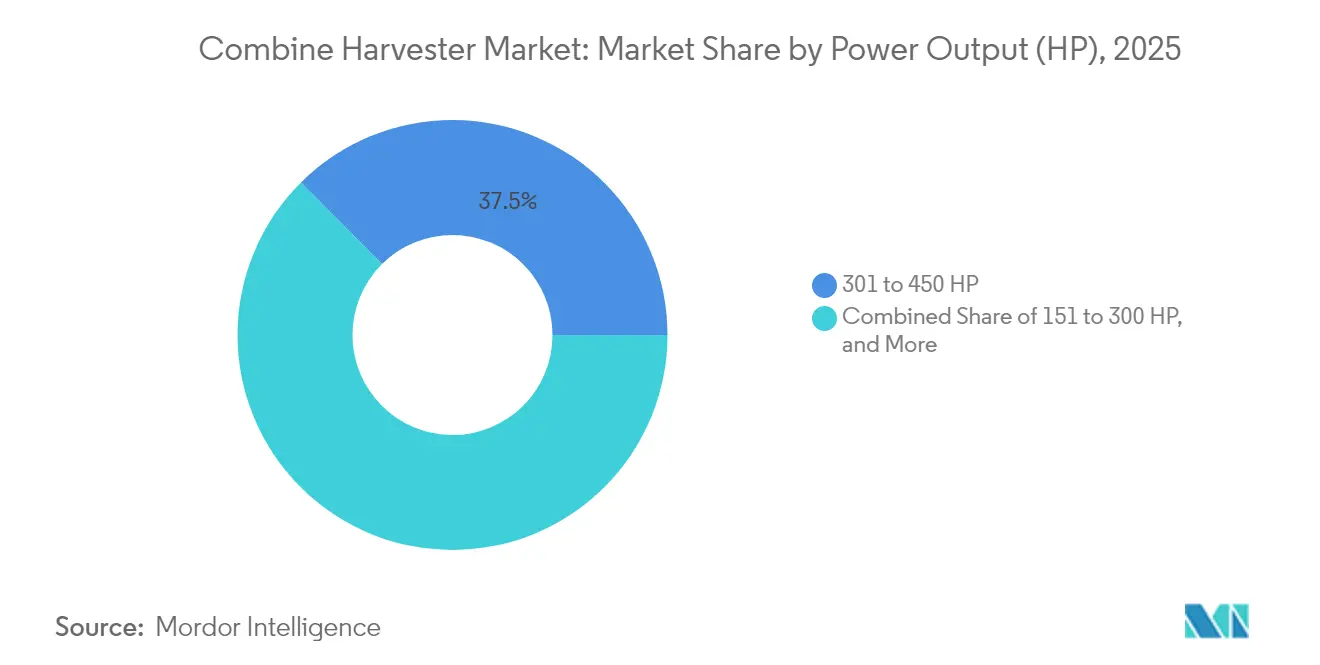

- By power output, the 301 to 450 HP class accounted for 37.45% of the combine harvester market size in 2025, while machines with a power output above 450 HP are slated to post the fastest growth rate of 7.02% from 2025 to 2031.

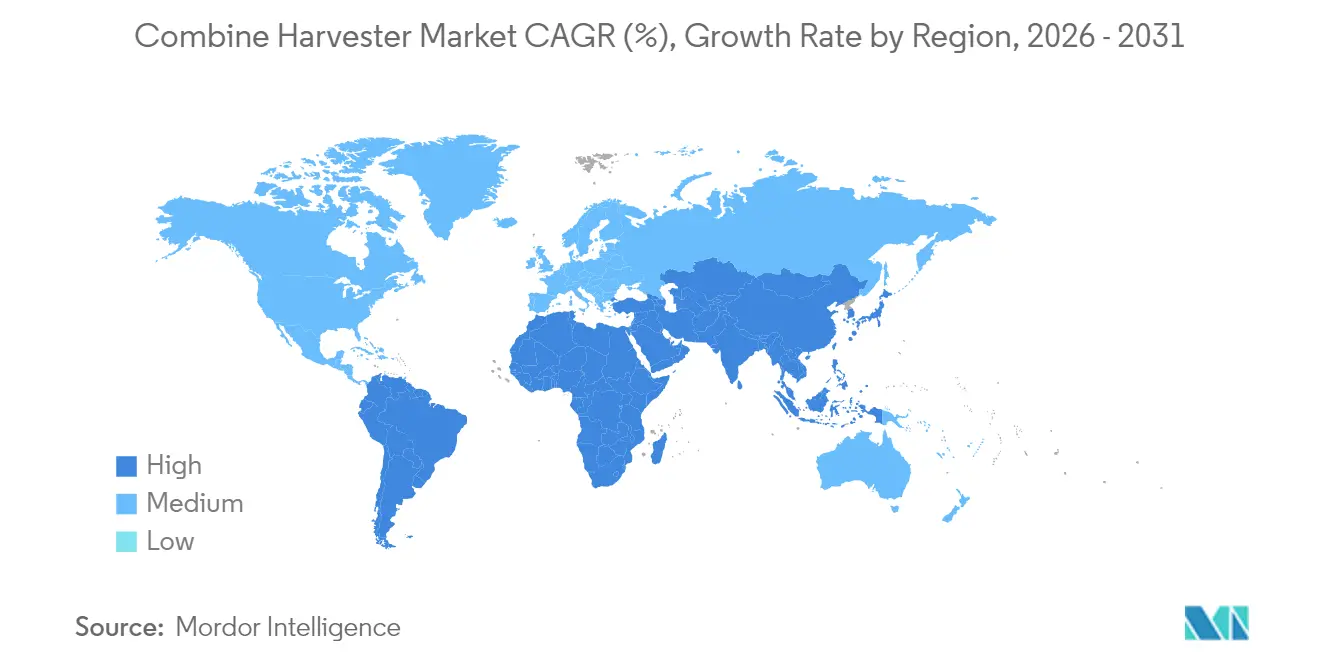

- By geography, North America retained a 31.85% revenue share in 2025, whereas the Asia-Pacific is pacing an 7.85% CAGR to 2031, which outstrips every other region.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Combine Harvester Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising farm mechanization in emerging economies | +1.8% | Asia-Pacific, Africa, and South America | Medium term (2-4 years) |

| Persistent rural labor shortage and wage inflation | +1.5% | Global, with concentration in North America and Europe | Short term (≤ 2 years) |

| Adoption of precision-ag mechanization suites | +1.2% | North America, Europe, and Australia | Medium term (2-4 years) |

| Integration of AI-enabled predictive maintenance | +0.8% | Global, early adoption in developed markets | Long term (≥ 4 years) |

| Carbon-credit monetization for low-loss harvesting | +0.5% | Global, regulatory focus in Europe and California | Long term (≥ 4 years) |

| OEM financing platforms targeting smallholders | +0.7% | Asia-Pacific, Africa, and South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Farm Mechanization in Emerging Economies

Government grants and custom-hiring hubs continue to widen equipment access. India’s Sub-Mission on Agricultural Mechanization reimburses 40–50% of purchase costs and has deployed more than 40,900 rental centers, lifting mechanization from 40% toward China’s 60% benchmark [1]Source: Press Information Bureau, “Mechanisation of Indian Agriculture,” pib.gov.in. China’s policy goal of 75% mechanization by 2025 attracts multinational suppliers into joint ventures that sidestep import tariffs [2]Source: International Trade Administration, “China Agricultural Machinery Market,” trade.gov. Similar subsidy schemes in Brazil and multiple African nations illustrate a structural push that enlarges the combine harvester market.

Persistent Rural Labor Shortage and Wage Inflation

Unemployment rates below 3% in many grain-producing regions have driven farm wages to record highs, narrowing the payback window for autonomous threshing platforms. Large United States growers now cite workforce scarcity as the primary justification for migrating to high-horsepower combines configured for one-operator, multi-shift deployment. Western Europe mirrors this tension, with dairy and arable producers trimming acreage whenever harvest labor cannot be secured in time. This labor scarcity is particularly acute during harvest seasons when timing is critical, driving demand for high-capacity combines that can maximize operational windows with minimal human intervention.

Adoption of Precision-Ag Mechanization Suites

Sensor-driven automation is transitioning from an optional overlay to an embedded standard. Leading Original Equipment Manufacturers (OEM) bundle yield-mapping, loss-monitoring, and ground-speed algorithms that promise 15–20% throughput gains for average operators. Subscription portals translate machine data into actionable agronomy advice, generating a recurring revenue layer that cushions cyclical equipment sales dips. The functionality jump cements precision software as the next competitive battleground inside the combine harvester market. These systems generate valuable data streams that enable predictive maintenance and operational optimization, creating recurring revenue opportunities through subscription-based services.

Integration of AI-Enabled Predictive Maintenance

Real-time diagnostics avert costly in-season breakdowns. Cloud-linked cameras flag grain-quality deviations, while vibration analytics model component fatigue to schedule parts replacement before failure. Early adopter fleets show 15–25% downtime reductions, extending engine life and stabilizing residual values. As connectivity fees expire, OEMs increasingly shift users onto annual telematics plans that enlarge aftermarket margins. These systems reduce the traditional reactive maintenance model, potentially decreasing equipment downtime during peak harvest seasons.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront capital requirement | -1.2% | Global, particularly acute in developing markets | Short term (≤ 2 years) |

| Limited aftermarket service networks | -0.8% | Asia-Pacific, Africa, and rural regions globally | Medium term (2-4 years) |

| Dependence on volatile commodity crop pricing | -1.0% | Global, cyclical impact | Short term (≤ 2 years) |

| Rapid soil-compaction regulations | -0.6% | Europe and North America, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Capital Requirement

New flagship frequently lists between USD 400,000 and USD 500,000. Elevated interest rates push annual carrying costs per unit, lengthening break-even periods even for well-capitalized farms. Although leasing and operating-rent contracts soften the blow, smaller growers still postpone purchases, slowing near-term combine harvester market growth. AGCO's strategic focus on OEM financing solutions and John Deere's expansion of financing capabilities in Brazil demonstrate manufacturers' recognition that equipment accessibility depends increasingly on innovative payment structures rather than traditional purchase models.

Limited Aftermarket Service Networks

Precision hardware demands technicians fluent in both hydraulics and machine-learning diagnostics. Coverage gaps across sub-Saharan Africa and parts of the Association of Southeast Asian Nations (ASEAN) leave owners exposed to harvest-time downtime. Digital service portals offer partial relief, yet physical parts depots and trained field engineers remain indispensable. Manufacturers are responding through digital service platforms and remote diagnostic capabilities, but the fundamental constraint of geographic service coverage remains a significant barrier to market penetration in rural regions where combine harvesters are most needed.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Self-Propelled Dominance Drives Innovation

The self-propelled segment generated a 71.35% market share in the combine harvester market in 2025, underscoring its primacy in high-acreage operations. Tractor-pulled variants alone are projected to lift the segment’s CAGR to 7.35% through 2031 as dual-flow threshing boosts grain retention. PTO-powered combine remain viable among cost-sensitive growers, but ongoing autonomy retrofits are beginning to blur the lines between legacy categories. The Tractor-pulled combine endures in cost-sensitive or fragmented landholdings, especially where capital pools are modest. Manufacturers refine hybrid drivelines that reduce fuel consumption by up to 10%, increasing the appeal for operators who must juggle diesel, AdBlue, and maintenance costs.

Fleet owners prefer self-propelled platforms due to their tight turning radius, integrated telematics, and compatibility with 12- to 18-row headers. OEMs now release over-the-air firmware that tunes concave clearance and rotor speed to crop moisture, squeezing extra throughput from existing horsepower bands. As adherence to future compaction rules tightens, articulated undercarriages and wide-track options are gaining traction within this leading segment of the combine harvester market. The segment’s innovation pipeline centers on the expansion of the combined harvesters market size through autonomous modules that enable a single driver to supervise multiple units across adjacent fields.

By Power Output: High-Horsepower Segment Captures Premium Demand

The 301 to 450 HP cohort accounted for 37.45% of the combine harvester market size in 2025 due to its cost-capacity balance. Units exceeding 450 HP, however, headline a 7.02% CAGR to 2031 as mega-farms in North and South America consolidate fields and compress harvest calendars. Elevated grain prices during cyclical upswings further justify these machines, whose 45-foot drapers and 18-row corn heads clear acreage at unrivaled speed.

Below 150 HP models cater to specialty crops and steep-slope regions where maneuverability trumps brute force. The 151 to 300 HP class addresses mid-size holdings seeking multi-crop flexibility. Across all brackets, Tier 4 and emerging Tier 5 emissions thresholds prompt engine recalibration and selective catalytic reduction upgrades, nudging buyers toward cleaner yet more complex powertrains.

Geography Analysis

North America retained 31.85% revenue in 2025, reflecting deep mechanization and entrenched replacement cycles. Capital spending nonetheless softened as growers braced for a predicted dip in large-equipment deliveries during 2025. Federal aid earmarked for climate-smart agriculture may cushion orders in the latter half of the year, especially for combines outfitted with residue-balancing kits that qualify for soil-health grants. Canada's agricultural sector benefits from strong grain export demand and government support for the adoption of precision agriculture, while Mexico's growing agricultural mechanization presents opportunities for expansion for North American manufacturers.

Asia-Pacific leads growth at an 7.85% CAGR through 2031. India’s mechanization gap has narrowed swiftly. Subsidy-backed custom-hiring centers now finance threshing sessions for smallholders who cannot yet buy machines outright. China’s 75% mechanization target propels demand for domestically assembled high-end combines that avoid import tariffs while retaining foreign sensor suites. Japan and Australia represent mature markets with a focus on precision agriculture and automation technologies, while Southeast Asian countries present emerging opportunities as agricultural productivity demands increase.

Europe’s market cools amid input-cost inflation and stricter environmental mandates. The EU Machinery Regulation 2023/1230 sets new guardrails for autonomous safety validation, raising R&D budgets for compliance. In contrast, Brazil and Argentina ride export-led cash flows that fund upgrades to 350 HP-plus combines equipped with telematics pods that simplify fleet optimization. South America benefits from a strong agricultural export performance, with Brazil's record sugarcane processing of 713 million tons in 2023 supporting equipment demand, while Argentina's agricultural biotechnology leadership creates opportunities for precision agriculture integration.

Regulatory Landscape

Across major markets, combine harvesters are shaped by on-road circulation requirements for non-road mobile machinery, functional safety and braking rules for agricultural vehicles, and harmonized safety standards for harvesters. In the European Union, Regulation (EU) 2025/14 established a harmonized type-approval framework for non-road mobile machinery circulating on public roads, and Regulation (EU) 2025/1117 updated requirements tied to agricultural and forestry vehicles, raising compliance engineering demands for OEMs selling machines that travel between fields and public roads.

Standards activity is tightening machine-level specifications and operator protection. In May 2026, EN ISO 4254-7:2017/A1:2026 updated safety requirements for agricultural harvesters, including combines, reinforcing design and documentation expectations. In China, GB/T 20790-2024 introduced updated technical requirements for head-feed harvesters, implemented in November 2024, and GB/T 46267-2025 defined large full-feed harvesters using thresholds such as a 12 kg/s rated feed rate and power above 160 kW, supporting procurement and product positioning around higher-capacity configurations. In the United States, the US EPA issued proposed amendments in July 2026 addressing certain compliance provisions for heavy-duty and nonroad engines, a rulemaking that equipment makers are tracking because it can affect in-season operability and emissions compliance strategies.

Competitive Landscape

The Combine Harvester Market concentration is moderately consolidated. Top manufacturers Deere & Company, CNH Industrial N.V., Kubota Corporation, AGCO Corporation, and Claas KGaA mbH control the lion’s share of the combine harvester market. Their combined R&D muscle funds rapid cycles of header, automation, and drivetrain upgrades. AGCO Corporation’s USD 2 billion purchase of 85% of Trimble Ag in 2023 underscores a race to secure precision-ag IP that scales across mixed-brand fleets. CNH Industrial N.V. targets 16-17% mid-cycle EBIT margins (Earnings Before Interest and Taxes) by embedding digital services and introducing the AF10 series with 775 HP and 15% lower cost of ownership.

Strategic partnerships mirror the sector’s shift from metal to microchips. New Holland’s pact with Bluewhite introduces autonomous retrofits that claim 85% labor savings in specialty crops. Deere & Company teams with satellite providers to extend machine connectivity, enabling over-the-air updates and cross-farm fleet coordination. Meanwhile, right-to-repair litigation forces OEMs to balance software protection with farmer goodwill.

Kubota Corporation dominates Asian rice machinery with sub-200 HP combines, while Rostselmash deepens presence in Eastern Europe. Component suppliers such as Linamar, fresh from acquiring Bourgault, aim to plug into OEM autonomy stacks with smart header controls. Market entrants must navigate certification barriers, tight dealer hierarchies, and high tooling costs for Tier 4 final engines.

Combine Harvester Industry Leaders

Deere & Company

Kubota Corporation

Claas KGaA GmbH

AGCO Corporation

CNH Industrial N.V.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Market opportunities are tied to demand for compliant, connected machines and the build-out of service capability. The July 2026 agreement involving John Deere, the US Federal Trade Commission, and multiple states on access to diagnostic and repair tools elevates serviceability as a differentiator in purchasing decisions, which in turn shapes how OEMs package software features and parts support across the installed base. Deere's January 2026 plan for a new parts distribution center in Hebron, Indiana, and a factory expansion in Kernersville, North Carolina, supports uptime and aftermarket logistics across North America, aligned with downstream service needs in key markets.

Asia driven mechanization programs also create opportunities. India continues to scale access through subsidized procurement and custom-hiring centers under its mechanization initiatives, while Indonesia and South Korea have published or advanced machinery and ag-bio R&D roadmaps that prioritize digital agriculture, robotics, and local strengthening of ecosystem capabilities.

Recent Industry Developments

- July 2026: John Deere finalized an agreement with the US Federal Trade Commission and five states to provide farmers with access to diagnostic and repair tools for current and future equipment. The agreement reinforces serviceability and tool access as a differentiator in connected combines, influencing how OEMs position software features and parts support across the installed base.

- June 2026: Kubota announced the upcoming release of its KC6115 and KC6130 combine harvesters (6-row models), with market availability scheduled for January 2027. The product pipeline signals continued refresh activity in mid-capacity platforms and supports competitive positioning in segments where buyers balance throughput with ownership costs.

- January 2026: John Deere outlined plans for a new parts distribution center in Hebron, Indiana, and a factory expansion in Kernersville, North Carolina, strengthening uptime and aftermarket logistics across North America. These investments expand parts availability and regional support networks, addressing downstream service needs in key markets.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as the sales value of combine harvesters used to harvest and thresh crops, counted when equipment is sold as new units into agricultural end users through OEM and dealer channels, across all major farming regions.

Scope exclusions: Used equipment resale, spare parts, attachments, and most service revenue (financing, maintenance, and operator services) are excluded unless they are bundled in the new equipment selling price.

Segmentation Overview

- By Type

- Self-propelled

- Tractor-pulled combine

- PTO-powered combine

- By Power Output (HP)

- Less than 150 HP

- 151 to 300 HP

- 301 to 450 HP

- Above 450 HP

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- France

- United Kingdom

- Spain

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

We start by mapping the demand pool and supply signals that can be checked openly. Public sources such as FAOSTAT, USDA crop and farm mechanization statistics, Eurostat machinery and agriculture datasets, UN Comtrade trade flows, and World Bank macro indicators are used to anchor harvested area, key crop mixes, and import-export movement of harvesting machinery.

After that, annual reports, investor presentations, and product catalogs are reviewed to understand typical price bands, model replacement cycles, and how shipments shift with farm income and subsidy programs. A paid subscription for company financials and news is used to cross-check revenue exposure and major capacity or distribution changes, and a paid patent database is referenced to sanity check technology adoption timing (automation, sensors, and efficiency features). These desk research sources are illustrative only, and we also used other public and paid references for data collection, validation, and research clarification.

Primary Interviews and Surveys

To fill gaps that public data does not explain well, we used expert interviews and structured surveys with OEM and dealer channel participants, large farm operators, and service and leasing stakeholders. Coverage was balanced across APAC, EMEA, and the Americas, so regional crop calendars, financing patterns, and subsidy effects could be tested before the final assumptions were locked.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 13% | APAC: 45% |

| Mid tier: 54% | Functional/Unit leaders: 38% | EMEA: 31% |

| Smaller Players: 20% | Managers: 49% | Americas: 24% |

Market-Sizing & Forecasting

Sizing starts with a top-down build that reconstructs annual demand from mechanized harvesting intensity. Harvested area by key crops, farm labor availability, and replacement timing are translated into likely unit demand, then priced using region-level average selling price ranges that reflect product mix (self-propelled versus pulled), power output, and header size.

Once the first cut was ready, we run selective bottom-up checks to keep the total realistic. For example, we roll up sampled shipment cues from dealer networks and match implied revenues to publicly visible company exposure ranges. When a country signal is missing, we apply proxy indicators (similar crop mix, similar farm size structure, and nearby import patterns), then adjust using interview inputs.

For forecasting, we use scenario analysis because combine purchases swing with farm income and policy cycles. The model tracks a small set of drivers, including grain price direction, harvested area shifts, equipment replacement age, credit availability, and emission or safety rule changes, and those inputs are stress tested with expert views before the final path is selected.

Data Validation & Update Cycle

Outputs are checked against independent signals, including trade value direction, harvested area movements, and observed pricing shifts, so unusually high or low implied volumes can be flagged early. Variance checks are run by region and by major equipment type, then assumptions are reviewed in a second analyst pass before sign-off.

The study is refreshed annually, and interim updates are triggered when material events occur, such as sharp commodity price swings, major subsidy changes, or supply disruptions. Before delivery, we run a fresh scan of key indicators and re-contact selected respondents if the newest signals conflict with the prior model view.

Mordor Intelligence's Global Combine Harvester Market Sizing Compared With Other Published Estimates

Published market sizes for combine harvesters can vary a lot, even when the topic name looks the same. The difference usually comes from how each publisher draws the boundary on what is counted in the market.

Key gap drivers include how tractor-pulled and PTO-powered configurations are treated, whether adjacent harvesting machinery types are rolled into one total, and how average selling prices are moved forward with inflation and feature upgrades. Another practical driver is refresh cadence, since late changes in farm income expectations can shift near-term purchases and change the current-year base used in the model, which is handled as a specific update step by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 12.74 B (2026) | |

| Global Consultancy A | USD 53.94 B (2024) | Uses a wider definition that appears to bundle multiple combine classes and related harvesting equipment and options, which expands the revenue pool versus a combine-only view, and it also runs on a different base year. |

| Trade Data Platform B | USD 18.20 B (2024) | Built from nominal wholesale value tied to production and trade accounting, which can understate full channel pricing and may miss domestically sold units that are not well captured in trade-based reconstruction. |

The spread in the table is mainly explained by scope and pricing basis, not by a simple math issue. When the market is kept to new combine harvester equipment sales and then validated with crop-linked demand indicators and channel price checks, the resulting number stays traceable to clear inputs and can be repeated year after year.

Key Questions Answered in the Report

How large is the combine harvester market in 2026 and what is the growth rate for it?

The combine harvester market size is USD 12.74 billion in 2026 and projected to rise at a 5.28% CAGR, reaching USD 16.48 billion by 2031.

Which region is growing fastest for combine harvesters?

Asia-Pacific leads with an 7.85% CAGR through 2031, fueled by subsidy-driven mechanization.

What segment holds the largest market share by type?

Self-propelled units captured 71.35% combine harvester market share in 2025.

Why are high-horsepower combines gaining traction?

Farms are consolidating acreage and need 450 HP-plus machines to finish harvests within shorter weather windows, driving a 7.02% CAGR for that segment.

How are OEMs addressing equipment affordability?

Manufacturers expand in-house financing and pay-per-hour rental models that lower upfront cash outlays for smallholders.

Page last updated on: