Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

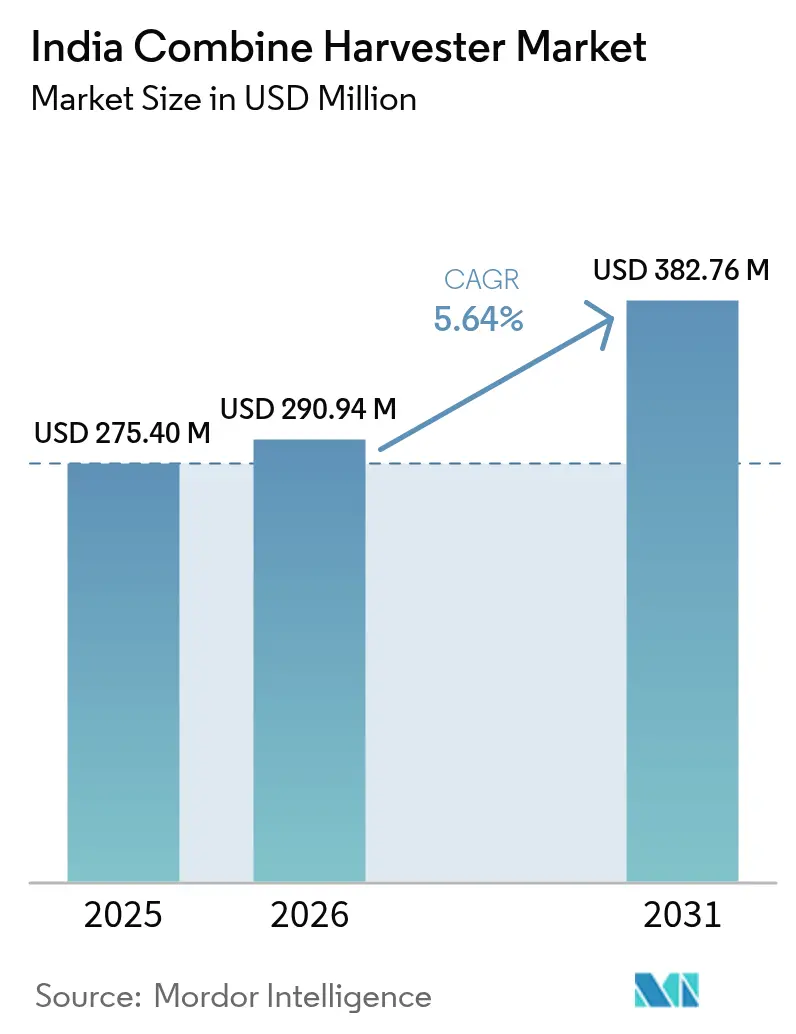

| Base Year Market Size (2025) | USD 275.4 Million |

| Market Size (2026) | USD 290.94 Million |

| Market Size (2031) | USD 382.76 Million |

| Growth Rate (2026 - 2031) | 5.64% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Combine Harvester Market Analysis by Mordor Intelligence

The India combine harvester market size was valued at USD 275.4 million in 2025 and estimated to grow from USD 290.94 million in 2026 to reach USD 382.76 million by 2031, at a CAGR of 5.64% during the forecast period (2026-2031). Rapid mechanization, supportive subsidies of 40-50% on equipment purchases, and the expansion of custom-hiring centers underpin this trajectory[1]Source: Press Information Bureau, “Digital Agriculture Mission: Tech for Transforming Farmers' Lives,” pib.gov.in. Farmers now mechanize 47% of field operations, yet the rate lags several peer nations, giving the market substantial headroom for growth[2]Source: Press Information Bureau, “Use of Advanced Machinery/Tools in Farming,” pib.gov.in. Escalating rural wages, digital agriculture initiatives, and stricter emission and safety standards are steering demand toward technologically advanced, self-propelled models. Competitive intensity remains moderate, prompting vendors to differentiate through precision-agriculture features, autonomous piloting, and service footprints that reach deep rural districts. The convergence of custom-hiring business models with harvester-as-a-service platforms is further democratizing access and enlarging the potential user base.

Key Report Takeaways

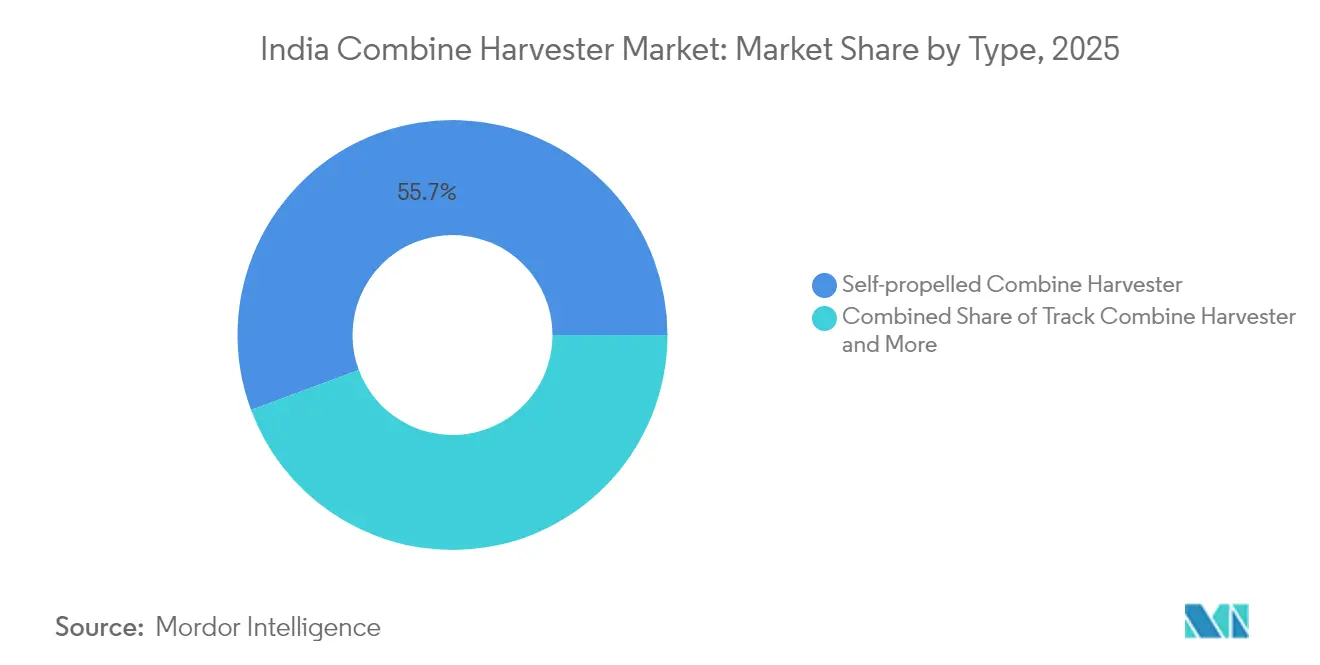

- By type, self-propelled combine harvesters led with 55.68% of the India combine harvester market share in 2025 and are positioned to expand at a 7.04% CAGR through 2031.

- By power rating, the 150-300 HP segment accounted for a 47.12% share of the India combine harvester market size in 2025, while machines above 300 HP are projected to record the fastest 7.32% CAGR through 2031.

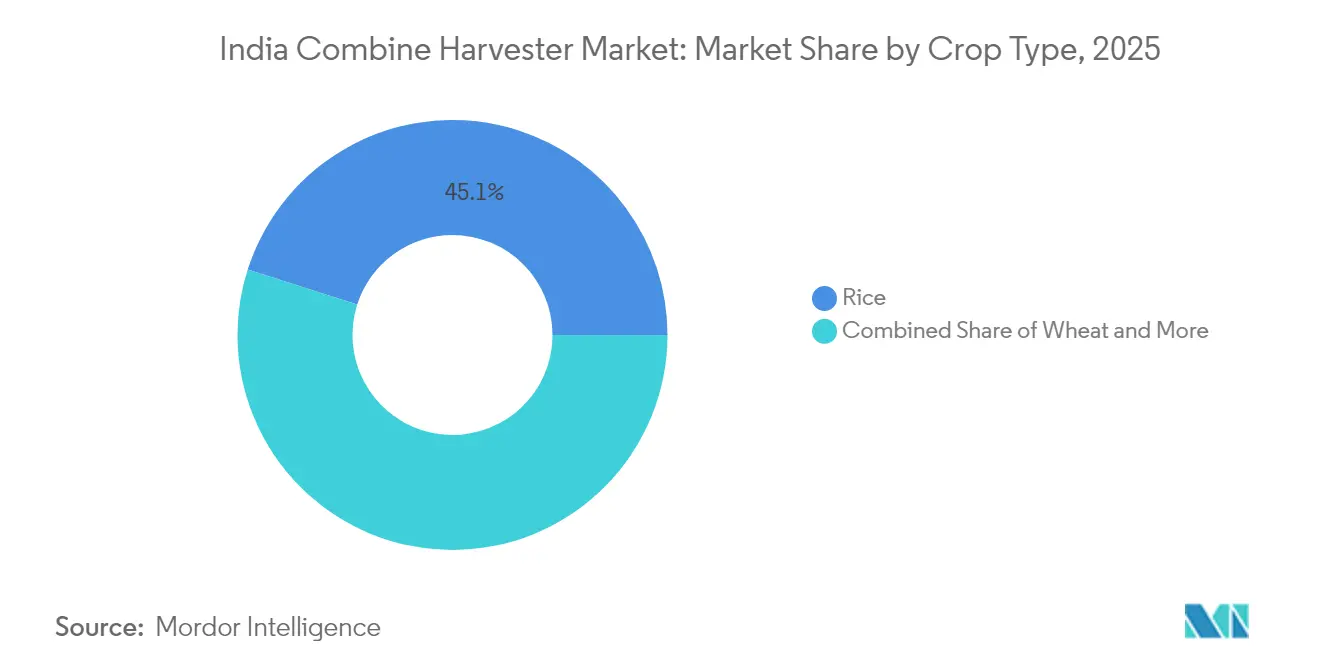

- By crop type, rice harvesting captured 45.08% revenue share in 2025, and corn harvesting is forecast to expand at a 6.72% CAGR to 2031.

- By drive mechanism, wheel-drive units held a 60.10% share in 2025, while track-drive machines are advancing at an 8.05% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Combine Harvester Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising area under grain crops | +1.2% | Uttar Pradesh, Punjab, and Haryana | Medium term (2-4 years) |

| Escalating farm labor costs | +1.5% | Punjab, Haryana, and Western Uttar Pradesh | Short term (≤ 2 years) |

| Government subsidies for mechanization | +1.0% | National | Medium term (2-4 years) |

| Rapid growth of custom-hiring centers | +0.8% | Madhya Pradesh, Karnataka, and Punjab | Short term (≤ 2 years) |

| Precision-ag retrofit kits for aging fleets | +0.5% | Punjab, Haryana, and Western Uttar Pradesh | Long term (≥ 4 years) |

| Growing availability of harvester-as-a-service models | +0.7% | Expanding to eastern and Southern states | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising area under grain crops

Area cover under foodgrains reached 1,321.04 lakh hectares during 2023-2024 from 1,301.69 lakh hectares during 2021-2022. Larger fields and tighter harvest windows motivate growers to adopt combine harvesters that can clear crops within optimal moisture thresholds, thereby minimizing post-harvest losses. Central schemes such as the National Food Security Mission promote high-yield seed varieties, indirectly boosting machine demand by raising per-acre output targets. State governments are simultaneously incentivizing mechanized residue management to combat stubble burning, making combines equipped with straw-handling attachments particularly attractive. As acreage under maize, pulses, and oilseeds widens, manufacturers are introducing multi-crop headers to serve mixed-farming zones. The resulting diversity in crop profiles reinforces sustained, geographically dispersed growth for the India combine harvester market.

Government subsidies for mechanization

Under the Sub-Mission on Agricultural Mechanization (SMAM), the federal and state governments reimburse 40-50% of the equipment purchase price. The Digital Agriculture Mission earmarks INR 2,817 crore (USD 339.4 million) to streamline subsidy delivery via an electronic farm identity stack, cutting approval time and leakage. The Kisan Credit Card program offers low-interest loans up to INR 500,000 (USD 6,024) for machinery purchases, easing capital hurdles for smallholders. Several states layer additional incentives, Karnataka co-funds public–private CHCs, while Punjab subsidizes Happy Seeder-ready combines to curb paddy-straw burning. Combined, these instruments reduce payback periods on new harvesters from five seasons to three, decisively energizing the India combine harvester market.

Precision-ag retrofit kits for aging fleets

A significant number of combines older than eight seasons remain in active service and are increasingly fitted with yield monitors, GNSS (Global Navigation Satellite System) receivers, and variable-rate controllers. Retrofit packages cost about one-third the price of a new medium-class machine, making them attractive to price-sensitive operators. Original-equipment manufacturers respond by offering factory-installed sensors and over-the-air software updates to secure aftermarket revenue. State agriculture departments reimburse up to 40% of the retrofit cost under energy-efficiency programs, incentivizing adoption. As sensor-equipped fleets generate data, platform providers monetize agronomic analytics, further embedding purchasers in connected-equipment ecosystems. These upgrades lengthen service life yet also nudge owners toward full-line replacement once digital literacy and operational gains become evident, ultimately feeding back into new-unit demand.

Growing harvester-as-a-service models

Platform start-ups partner with dealers to deploy subscription-based harvesters that bill users by machine-hours, transferring ownership risk from farmers to financiers. Early pilots in Andhra Pradesh showed operators earning additional USD 72-139 per hectare (INR 6,000-11,500) net income by bundling residue mulching and GPS (Global Positioning System) yield mapping services. Leasing companies secure preferential financing through expanded MSME (Micro, Small, and Medium Enterprises) thresholds, effective April 2025, widening asset pools without balance-sheet strain. Insurers now extend pay-per-use cover, reducing downtime liability and making the model viable in monsoon-prone states. As fleets scale, OEMs capture recurring parts revenue and build brand loyalty. These service innovations enlarge the addressable customer base and sustain multi-year growth for the India combine harvester market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost of machines | −1.8% | Nationwide, acute for small and marginal farmers | Short term (≤ 2 years) |

| Fragmented and small land holdings | −1.2% | High impact in Eastern and Northeastern states | Long term (≥ 4 years) |

| Expensive after-sales maintenance | −0.9% | Districts lacking service hubs | Medium term (2-4 years) |

| Slow rural credit disbursement to small farmers | −0.6% | Less-developed states | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High upfront cost of machines

A mid-range self-propelled harvester retails for INR 2.2 million (USD 26,506), an investment beyond the reach of most smallholders. Even with a 50% capital subsidy, the remaining payment often surpasses annual farm income, forcing reliance on rental models. Finance houses perceive higher default risk for equipment loans because collateral recovery is complex in geographically dispersed villages. Although the Kisan Credit Card offers subsidized rates, only 61% of eligible farmers held active cards in 2024, limiting immediate cash-flow relief. Limited uptake of crop insurance further compounds lenders’ risk perception. Consequently, ownership concentrates among larger farmers and CHC operators, tempering unit-sales momentum for the India combine harvester market.

Fragmented and small land holdings

In India, 85 percent of farm households cultivate less than two hectares, which limits the efficiency of machinery in the fields and lengthens the payback periods. Shallow plot sizes also hinder maneuvering and raise headland losses, diminishing the economic case for on-farm ownership. Land consolidation via leasing or Farmer-Producer Organizations (FPOs) progresses slowly because of tenancy-law complexities and social factors. Where aggregation does occur, crop calendars still vary by micro-region, complicating shared-machinery scheduling. While CHCs mitigate some challenges, logistical overlaps and transport bottlenecks persist. Until structural land reforms gain pace, fragmented holdings will remain a drag on the India combine harvester market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Self-Propelled Dominance Drives Efficiency

Self-propelled units generated 55.68% of 2025 revenue, underscoring their appeal among medium-to-large farms for all-crop versatility and standalone mobility. Buyers value integrated engines, larger grain tanks, and operator comfort during extended harvest windows, making these machines the benchmark for productivity. Tractor-powered combine harvesters remain prevalent in lower-mechanization districts, leveraging existing 50-70 HP tractor fleets to reduce capital outlay. Track combines, though niche, solve traction issues in waterlogged paddy areas and appear in government procurement lists for climate-resilient mechanization, especially in coastal Andhra Pradesh.

Looking forward, self-propelled sales are positioned to expand at a 7.04% CAGR, benefiting from Stage V emission mandates that favor new-technology adoption. OEMs integrate GNSS auto-steer, 4G telematics, and straw chopper attachments, elevating price points and average revenue per unit. Field demonstrations by Mahindra & Mahindra Ltd. and Case IH’s Axial-Flow series show 3-4% grain-loss reduction, justifying higher acquisition costs. This performance edge sustains their lead in the India combine harvester market.

By Power Rating: Mid-Range Machines Anchor Demand

Combines rated 150-300 HP accounted for 47.12% of 2025 sales, capturing the sweet spot between throughput and affordability. They handle multi-crop headers and traverse 4-6 hectare plots without extensive turnaround time, aligning well with India’s farm-size spectrum. Below-150 HP machines still interest small CHCs but face limitations in grain-tank capacity and header width, slowing field progress. Above-300 HP models, despite commanding premium prices, are registering the fastest 7.32% CAGR because large-acreage farmers and corporate growers pursue machine hours aggregation.

Stage IV TREM (Transport Related Engine Emission Norms) compliance as of January 2023 nudged OEMs to redesign engines, increasing 175 HP-plus production runs. Custom-hiring entrepreneurs in Punjab and Madhya Pradesh gravitate toward these high-output machines to maximize rental income during brief harvest peaks. Consequently, power-rating choices directly steer fleet mix and revenue profiles in the India combine harvester market.

By Crop Type: Rice Harvesting Leads Adoption

Rice harvesting generated 45.08% of 2025 revenue, reflecting combined acreage in Uttar Pradesh, West Bengal, and Tamil Nadu. Subsidy programs targeting paddy straw management accelerate the adoption of combines equipped with chaff spreaders and Happy Seeder compatibility. Wheat harvesters hold the second position, driven by near-universal mechanization in Punjab and Haryana. Corn combines are projected to grow at a 6.72% CAGR, tracking expanding maize acreage in Bihar and Karnataka for feed and ethanol demand.

Specialized headers enable rapid crop switching, allowing operators to chase back-to-back harvests across states, a critical utilization strategy in CHC fleets. OEMs now offer quick-coupler designs to minimize header change time, raising machine availability metrics. The diversification of cropping patterns, therefore, adds resilience and volume to the Indian combine harvester market.

By Drive Mechanism: Wheel Drive Retains Scale Advantage

Wheel-drive units made up 60.10% of 2025 sales, owing to simpler maintenance, lower acquisition cost, and broad dealer familiarity. Their ground-pressure profile suits the alluvial soils prevalent in the northern plains. Track-drive combines, nevertheless, post an 8.05% CAGR by excelling in wet paddy and hilly terrains, where wheel slippage risks crop damage. Government grants covering up to 50% of track-combine cost in flood-prone Assam and Odisha further accelerate uptake.

Manufacturers deploy modular undercarriages enabling conversion from wheels to tracks, protecting resale values and broadening secondary markets. Such adaptability aligns with heterogeneous agronomy, reinforcing track-drive uptake while allowing wheel-drive to retain volume leadership in the India combine harvester market.

Geography Analysis

Northern India dominates adoption. Punjab fields a high number of tractors per area and shows combine-harvest rates above a significant level, a legacy of early Green Revolution investment. Haryana follows closely, buoyed by contiguous large plots amenable to high-HP combines and dense service networks. Uttar Pradesh, though larger in arable area, reveals a patchwork mechanization index ranging from very high to nearly perfect depending on district, mirroring disparities in credit access and land holdings.

Central India, led by Madhya Pradesh, records the highest five-year growth as CHCs flourish under public–private models that deliver 20% yield gains and shorten harvest cycles. Maharashtra and Chhattisgarh are trailing yet show improving penetration through state-funded equipment banks serving tribal districts. The India combine harvester market size for this belt is set for upward revision once laggard districts hit critical mechanization thresholds.

Eastern and northeastern states represent latent demand. Despite rich paddy acreage, West Bengal and Odisha deploy fewer than five combines per 10,000 hectares due to small plot fragmentation. Government pilot schemes that aggregate holdings into 100-acre clusters and finance track-drive units could double the combine density by 2030. Southern states adopt selectively, Andhra Pradesh scales rice mechanization aggressively, while Karnataka’s millets and pulses mix requires versatile multi-crop machines. Tamil Nadu encourages sugarcane and specialized crop harvesters to handle longer maturity cycles. These regional differences diversify revenue streams and hedge market cyclicality.

Competitive Landscape

Market leadership rests with Mahindra & Mahindra Ltd., Escorts Kubota Limited, PREET Group, Kartar Agro Industries Private Limited, and Deere & Company, whose combined dealer reach spans a vast network of numerous touchpoints nationwide, positioning the India combine harvester market as moderately concentrated. Market leaders leverage economies of scale, established service networks, and government relationships to maintain competitive advantages while emerging players focus on niche segments and cost-effective solutions. Yanmar Holdings Co., Ltd. localizes component sourcing to counter currency volatility, while Deere & Company invests in remote diagnostics to slash mean-time-to-repair under 10 hours.

Strategic partnerships shape the competitive arc. DEUTZ aligns with Tractors and Farm Equipment Limited to co-develop low-emission engines adapted for tropical climates, offering OEMs ready compliance with Stage V norms. Escorts Kubota Limited pursues autonomy, unveiling robot platforms that could integrate modular harvester attachments within five years. Domestic challenger Escorts Kubota Limited pushes cost-optimized mid-HP combines to fill the value segment. Companies also vie for CHC fleet contracts, bundling financing, telematics subscriptions, and extended-warranty packages that lock operators into multi-year ecosystem plays.

Technology is the central differentiator. Precision-ag kits bundled with OEM finance give incumbents upsell leverage and generate annuity-style data service revenue. After-sales logistics now leverage predictive analytics, Mahindra & Mahindra Ltd’s mobile service vans automatically preload parts based on telematics alerts, shrinking downtime. Compliance with the Bureau of Indian Standards’ 2024 safety order favors firms with certified production facilities, raising entry barriers for smaller assemblers and sustaining the current competitive hierarchy.

India Combine Harvester Industry Leaders

Kartar Agro Industries Private Limited

PREET Group

Mahindra & Mahindra Ltd.

Deere & Company

Escorts Kubota Limited.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Escorts Kubota Limited is investing INR 4,500 crore (USD 540 million) to establish a new manufacturing facility near Jewar Airport, Uttar Pradesh, where land acquisition is in progress. The company has allocated an additional INR 400 crore (USD 48 million) for capital expenditure in FY 2025-26, with 75% designated for product development and 25% for manufacturing facility improvements.

- January 2025: Yanmar Holdings Co., Ltd. acquired CLAAS India and renamed the company to Yanmar Agricultural Machinery India Private Limited (YAMIN). The facility in Morinda, Punjab, manufactures combine harvesters and attachments for distribution in Indian and international markets.

India Combine Harvester Market Report Scope

A combine harvester is an agricultural machine used to harvest different kinds of crops by simultaneously reaping, threshing, and winnowing. The India Combine Harvester Market is segmented by type into self-propelled, track, and tractor-powered combine harvesters. The market sizing has been done in value terms (USD) for all the abovementioned segments.

By Type

| Self-propelled Combine Harvester |

| Track Combine Harvester |

| Tractor-powered Combine Harvester |

By Power Rating

| Below 150 HP |

| 150 to 300 HP |

| Above 300 HP |

By Crop Type

| Wheat |

| Rice |

| Corn |

| Other Crops |

By Drive Mechanism

| Wheel Drive |

| Track Drive |

| By Type | Self-propelled Combine Harvester |

| Track Combine Harvester | |

| Tractor-powered Combine Harvester | |

| By Power Rating | Below 150 HP |

| 150 to 300 HP | |

| Above 300 HP | |

| By Crop Type | Wheat |

| Rice | |

| Corn | |

| Other Crops | |

| By Drive Mechanism | Wheel Drive |

| Track Drive |

Key Questions Answered in the Report

What is the current value of the India combine harvester market?

The India combine harvester market size is USD 290.94 million in 2026.

How fast is demand for combine harvesters projected to grow in India?

Market value is forecast to expand at a 5.64% CAGR, reaching USD 382.76 million by 2031.

Which combine-harvester segment holds the largest revenue share by type?

Self-propelled machines command 55.68% market share, reflecting their efficiency and versatility.

How do government subsidies influence harvester adoption?

Federal and state schemes reimburse 40-50% of equipment cost and accelerate purchases through Custom Hiring Centers, significantly lowering payback periods.

Page last updated on: