Smart Flooring Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

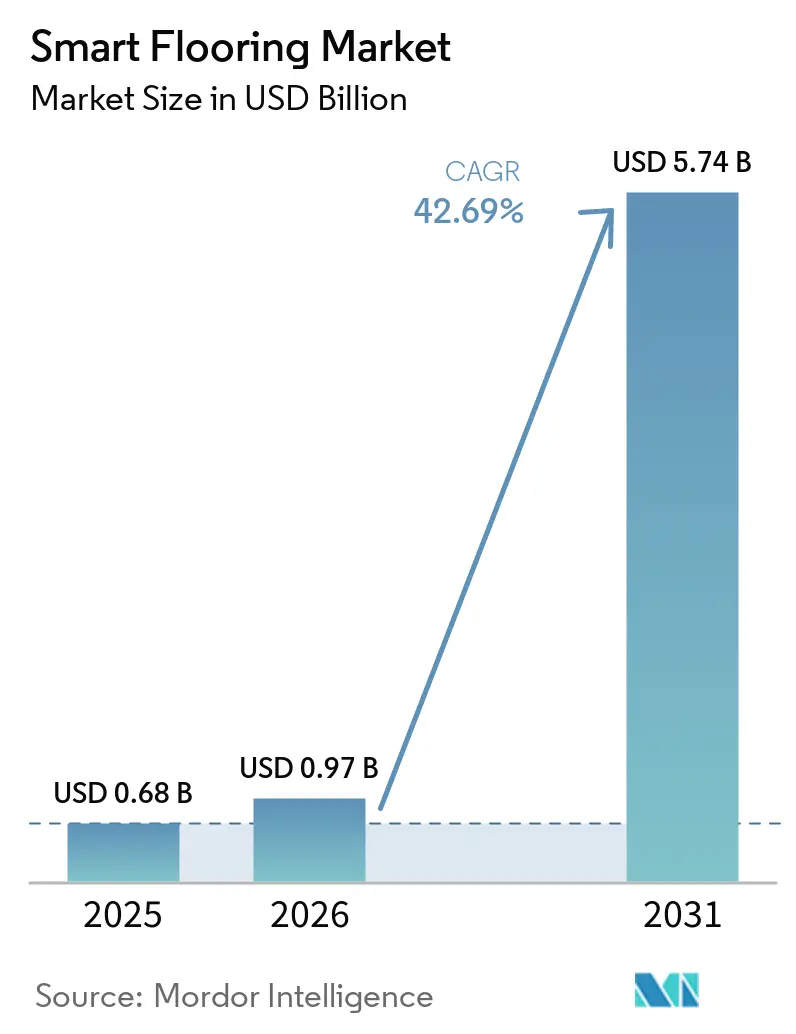

| Market Size (2026) | USD 0.97 Billion |

| Market Size (2031) | USD 5.74 Billion |

| Growth Rate (2026 - 2031) | 42.69% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Smart Flooring Market Analysis by Mordor Intelligence

The smart flooring market size was valued at USD 0.68 billion in 2025 and estimated to grow from USD 0.97 billion in 2026 to reach USD 5.74 billion by 2031, at a CAGR of 42.69% during the forecast period (2026-2031). This expansion reflects a clear shift in the smart flooring market from passive surface materials toward connected building infrastructure that can sense movement, support automation, and feed operational data into wider facility systems. Falling sensor module prices, with commercial pressure-sensor arrays declining from USD 15-20 per unit in 2020 to under USD 5, have lowered break-even thresholds and widened the addressable base from flagship smart-city projects to mid-market retrofit programs. Demand is also being reinforced by green-building compliance, hybrid workplace planning, and senior-care safety requirements, which makes the smart flooring market less dependent on discretionary spending alone. Even with interoperability issues and higher installation costs still limiting some deployments, the combination of embedded sensing, edge computing, wireless connectivity, and rising software-based recurring revenue keeps the growth outlook for the smart flooring market unusually strong.

Key Report Takeaways

- By component, hardware held 65.53% of the smart flooring market share in 2025, while software is forecast to expand at a 43.92% CAGR through 2031.

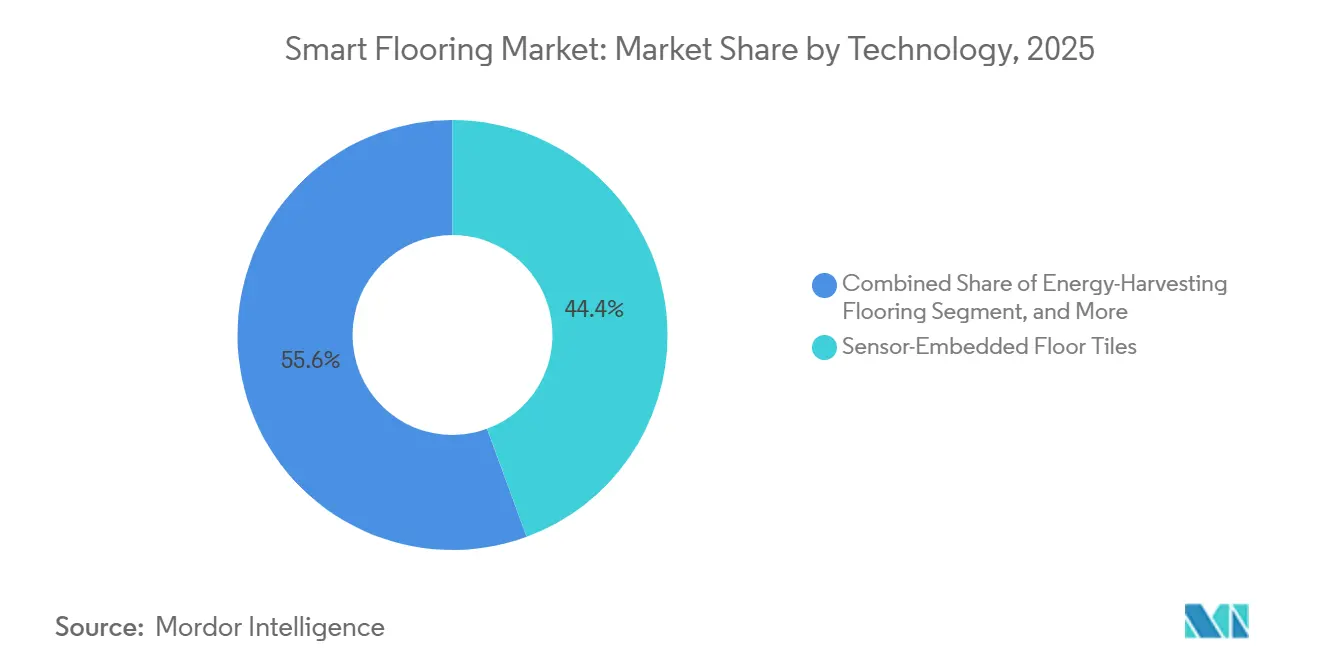

- By 2025, sensor-embedded floor tiles captured 44.38% of the market, while energy-harvesting flooring is projected to grow at a 44.57% CAGR through 2031.

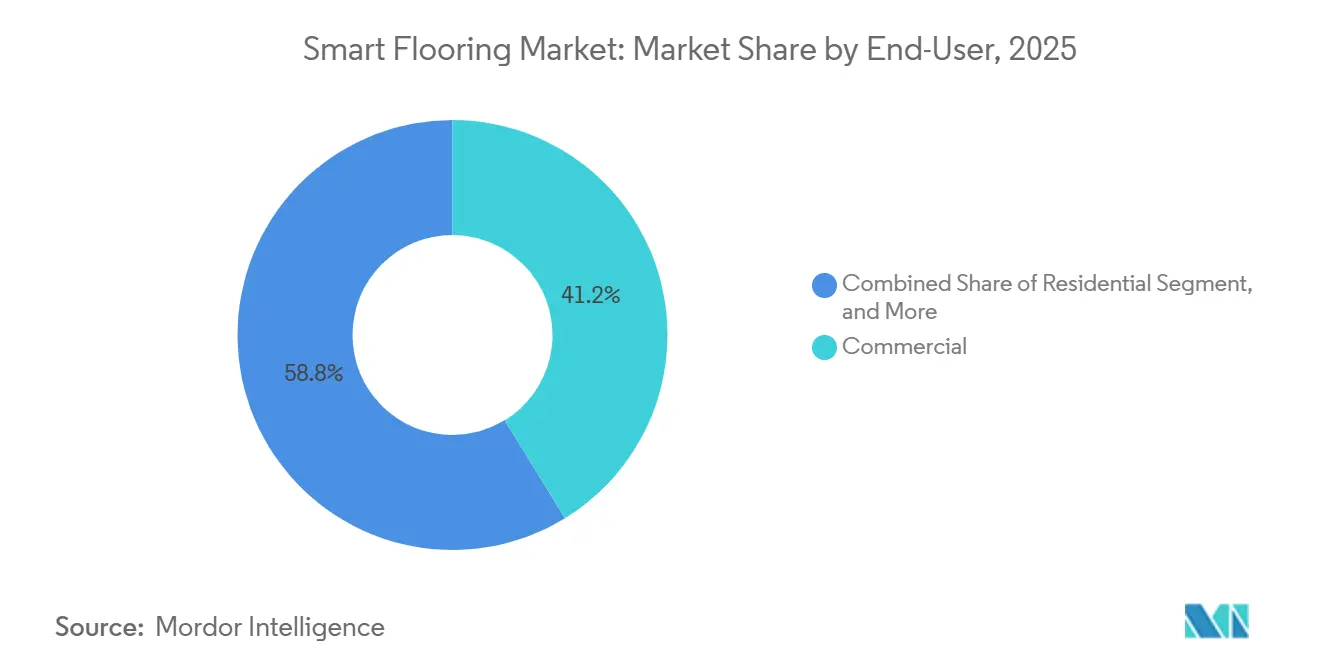

- By end-user, commercial accounted for 41.24% share in 2025, while residential is projected to advance at a 45.37% CAGR through 2031 in the smart flooring market.

- By application, occupancy and space-utilization analytics commanded 38.26% share in 2025, while gaming and interactive entertainment are forecast to grow at a 43.34% CAGR through 2031.

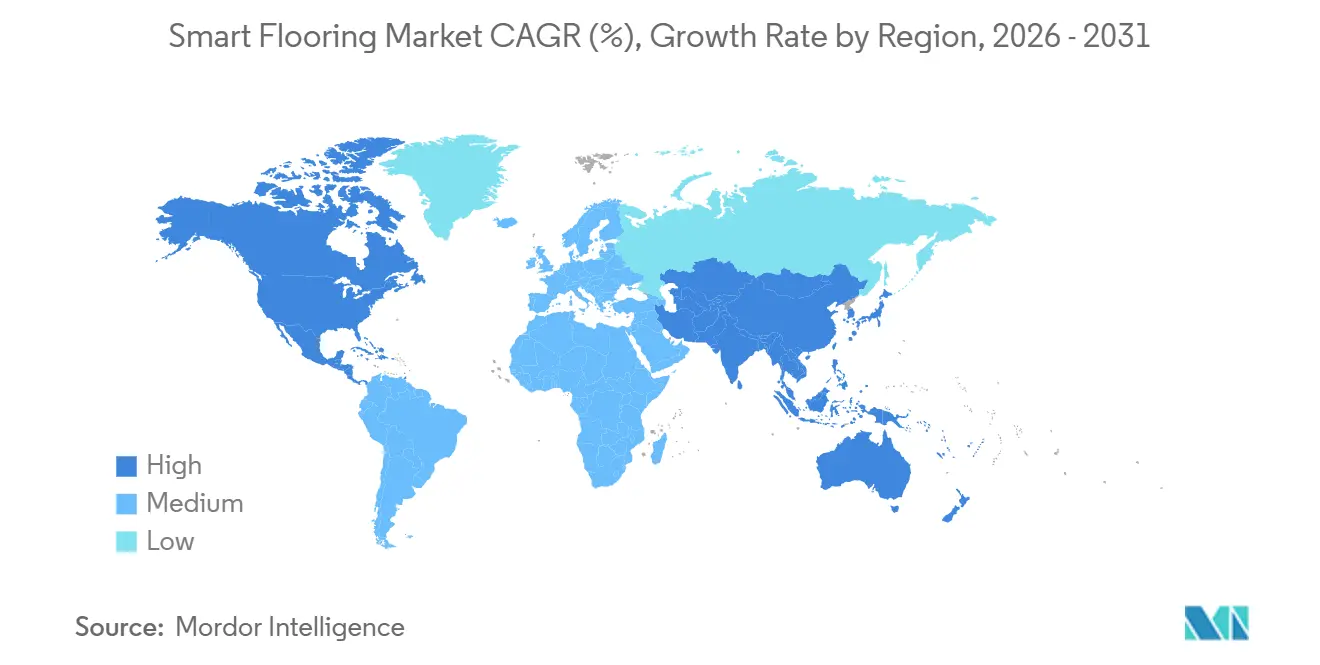

- By geography, North America held 42.73% share in 2025, while Asia-Pacific is projected to expand at a 44.54% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Smart Flooring Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Commercial Adoption For Occupancy Analytics In Office Spaces | +8.5% | Global | Short term (≤ 2 years) |

| Rising Smart-Home Renovations And Retrofit Projects | +7.2% | North America and Europe | Medium term (2-4 years) |

| Legal Mandates For Fall-Detection Systems In Senior-Care Facilities | +6.8% | Global | Short term (≤ 2 years) |

| Energy Savings From Embedded Power-Management Algorithms | +5.9% | North America and Europe enterprise markets | Medium term (2-4 years) |

| Maturing Printed Piezoelectric Materials Lowering BOM Costs | +4.3% | Global R&D centers | Long term (≥ 4 years) |

| Urban Mobility Flooring Integration In Multi-Modal Transit Hubs | +3.1% | Global transit hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Commercial Adoption for Occupancy Analytics in Office Spaces

Commercial real-estate operators are using floor-based sensing to narrow the gap between booked space and actual usage, and enterprise occupancy platforms continue to place that mismatch at 30-40% of total seat inventory. In the smart flooring market, this matters because floor sensing can deliver sub-square-meter resolution that badge systems and ceiling-mounted passive infrared devices do not. That sharper movement data helps facilities teams adjust layouts based on real usage patterns and also improves how occupancy information is fed into building management workflows.[1]Libby Owens, “Meet Area Pro, The Ultimate Occupancy Sensor for Smarter Workplaces,” XY Sense, xysense.com“Occupancy Analytics, Real-Time Occupancy Sensors and Data,” R-Zero, rzero.com Demand-controlled HVAC programs become more effective when zone-level occupancy signals are continuous rather than binary, which strengthens the operating case for the smart flooring market in office environments. A Siemens-integrated deployment cited by Capgemini UK demonstrated how anonymized floor monitoring can support building operations without identifying individuals, a design principle becoming increasingly important to enterprise buyers. This makes occupancy analytics one of the fastest ways for the smart flooring market to convert technical capability into clear commercial value.

Rising Smart-Home Renovations and Retrofit Projects

Residential demand in the smart flooring market is rising faster than older smart-home adoption curves suggested because retrofit costs are becoming less tied to full renovation cycles. Modular formats and wireless control layers have made it easier for homeowners to add smart functionality without major construction disruption, which reduces dependence on contractor-led projects. This changes the purchase decision from a large capital project into a more manageable home upgrade, especially when comfort, heating control, and occupancy awareness are packaged together. Warmup launched its 7iE Smart Matter WiFi Thermostat in October 2025, with compatibility with Apple Home, Google Home, and Amazon Alexa, strengthening the connection between underfloor heating and mainstream connected-home ecosystems. The same launch stated that SmartGeo technology reduced energy consumption by up to 25% during use testing, helping address one of the main running-cost objections in the residential smart flooring market. As a result, smart heated flooring is emerging as a practical entry point for household adoption, especially in premium homes and retrofit-led renovations.

Legal Mandates for Fall-Detection Systems in Senior-Care Facilities

The smart flooring market is also benefiting from a strong safety-driven procurement cycle in senior-care environments. The US Department of Health and Human Services Office of Inspector General reported 42,864 serious nursing-home falls among Medicare enrollees that resulted in hospitalization in one year, and related hospital costs exceeded USD 800 million.[2]Office of Inspector General, U.S. Department of Health and Human Services, “Serious Falls Resulting in Hospitalization Among Medicare-Enrolled Nursing Home Residents, July 2022–June 2023,” U.S. Department of Health and Human Services, oig.hhs.gov CMS requirements under 42 CFR § 483.25(d) and the accident-prevention review pathway hold certified facilities accountable for maintaining hazard-free conditions and adequate supervision, thereby giving fall-detection systems a compliance role rather than a purely optional one. Floor-based systems are well-suited to that setting because they can detect bed exits and falls without relying on cameras, and sensor-based prevention tools continue to gain support in the clinical literature for non-intrusive monitoring. In Japan, Magic Shields began general sales of the Koroyawa Sensor Mat III in April 2026, following a pilot deployment across 1,600 facilities, and 93% of participating hospitals said they would recommend the product.[3]“Occupancy Analytics, Real-Time Occupancy Sensors and Data,” R-Zero, rzero.comThese patterns show why elder-care monitoring remains one of the most structurally supported demand streams in the smart flooring market.

Energy Savings from Embedded Power-Management Algorithms

Energy management is another durable growth driver because building owners increasingly need operational proof of savings rather than theoretical efficiency claims. R-Zero stated that demand-controlled HVAC can achieve 20-40% HVAC energy savings when paired with high-resolution occupancy sensing, and this kind of documented performance aligns well with the value proposition of the smart flooring market.[4]Magic Shields, “Koroyawa Sensor Mat III Formal Sales Release,” Magic Shields, iza.ne.jpThe practical advantage is that floor sensors can show sub-zone movement patterns, allowing proportional HVAC responses rather than simple room-level on/off control. A study at Shoucheng International Center in China recorded a nearly 40% reduction in evening electricity consumption after smart sensing floors were connected with lighting and HVAC controls. In Europe, the Energy Performance of Buildings Directive is keeping pressure on asset owners to improve building efficiency and move toward near-zero-energy building targets by 2030.[5]European Commission, “Energy Performance of Buildings Directive (EPBD) Recast,” European Commission, europa.euThat makes the smart flooring market relevant not only for comfort and automation, but also for audit readiness, compliance, and measurable building performance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Installation and Retrofit Complexity | -12.3% | Global, with acute impact in legacy building markets | Short term (≤ 2 years) |

| Data-Privacy and Cybersecurity Concerns | -8.7% | Europe and North America regulatory markets, expanding globally | Medium term (2-4 years) |

| Lack of Open Interoperability Standards | -6.2% | Global, with particular impact on enterprise deployments | Long term (≥ 4 years) |

| Limited Installer Skill Base for Sensor-Embedded Flooring | -4.8% | Global, concentrated in emerging markets with limited technical infrastructure | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Initial Installation and Calibration Costs

High upfront cost remains the clearest near-term restraint on the smart flooring market. Full-sensor floor systems were priced at USD 75-150 per square foot, compared with USD 15-40 per square foot for conventional carpet, and retrofit work added 40% premium due to subfloor modifications and cabling complexity. That cost gap limits adoption outside larger enterprises, healthcare networks, and public-sector budgets, even though the broader addressable base includes many mid-market buyers. Calibration adds another layer of friction because sensor arrays must be tuned for site-specific vibration, airflow, and equipment signatures, or false positives will reduce trust in the analytics output. Mitsubishi Estate’s October 2025 demonstration with Aeterlink showed why wireless power matters for this category, since under-floor sensors that avoid cabling can reduce part of the installation burden in retrofit settings. Until retrofit-ready formats move closer to conventional flooring economics, cost will continue to shape which buyers can enter the smart flooring market at scale.

Lack of Global Interoperability Standards

Interoperability remains a slower but important brake on the smart flooring market because buyers want floor intelligence to plug into wider building systems without custom middleware at every site. Many vendors already transmit data through MQTT or REST APIs, but data models and schema definitions still vary enough to create integration work and vendor lock-in. This becomes a procurement problem when portfolio-scale buyers want multi-site deployment, shared dashboards, and simpler maintenance across properties. The growth of Matter in residential systems shows that cross-vendor interoperability can speed adoption when a recognized framework becomes commercially usable, and Warmup’s 7iE launch highlighted how strongly that idea resonates in connected-home controls. The smart flooring market lacks an equally recognized floor-sensing standard for commercial buildings, leaving integration risk in place. Until that standards gap closes, some buyers will keep delaying wider rollouts, even when the technical use case has already been proven.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Sensor Tiles Hold Ground As Energy-Harvesting Flooring Gains Momentum

Sensor-embedded floor tiles commanded a 44.38% share in 2025, maintaining their lead in the smart flooring market. Their position was driven by proven reliability, easier integration with existing commercial wiring infrastructure, and a better fit for the needs of office, healthcare, and retail projects. Buyers in these settings tend to prefer systems that already work with established installation practices, especially when deployment speed and maintenance simplicity affect payback. Smart heated flooring remains a distinct technology path in the smart flooring market because it addresses comfort, energy efficiency, and home automation simultaneously. Warmup’s October 2025 7iE launch demonstrated how Matter-compatible controls can connect underfloor heating to major smart-home ecosystems, strengthening the appeal of heated flooring in premium homes and retrofit projects.

Energy-harvesting flooring is the fastest-growing technology segment, with a 44.57% CAGR projected through 2031, driven by falling material costs and improved power-management circuits that are advancing self-powered sensor nodes toward commercial viability. Research published in 2024 demonstrated a prototype tile capable of harvesting up to 246 mW per tile at a material cost of USD 10.20, demonstrating how quickly the economics are improving for high-footfall use cases. Additional work on low-cost battery-free smart pavement systems also supports the idea that power-generating surfaces are becoming more practical as wireless communication loads fall. ETH Zurich’s LignoVolt project adds another dimension by embedding Rochelle salt crystals into modified wood to create recyclable piezo-parquet, bringing the smart flooring market into premium interior design and sustainability-led renovation conversations. Static-dissipative smart flooring and interactive LED flooring remain small niches, but they broaden the smart flooring market's technology base into electronics production, data centers, retail, and entertainment venues.

By Component: Software Revenue Acceleration Reshapes The Hardware-Led Market

Hardware retained 65.53% of the smart flooring market share in 2025, while software is projected to expand at a 43.92% CAGR through 2031. That starting point reflected the physical nature of early deployments, because sensor carpets, gateway hubs, and edge processors formed the non-negotiable base layer of each installation. In the first phase of the smart flooring market, buyers had to fund the full data-collection stack before they could benefit from analytics, alerts, or building-system integration. This favored vendors that could deliver hardware, local compute, and installation support as one package, especially in commercial sites where reliability mattered more than modularity. It also meant that early revenue concentration sat with physical product suppliers rather than with recurring software providers.

Software is now gaining weight because analytics subscriptions, visualization tools, and building management APIs can be layered onto installed floors without another full construction cycle. That model matters for the smart flooring industry because it creates recurring revenue and improves lifetime value per square foot. It also changes margin structure, since declining sensor costs are likely to pressure hardware pricing over time while analytics remains more defensible. As the installed base grows, vendors that control occupancy dashboards, alert logic, and workflow integration are likely to hold a stronger commercial position than those that supply only hardware shells. The next stage of the smart flooring market will therefore depend on how successfully suppliers combine open interoperability with proprietary software value that customers are willing to keep paying for.

By End-User: Commercial Scale Anchors Revenue While Residential Rewrites Growth Assumptions

Commercial end-users accounted for 41.24% share in 2025, keeping the smart flooring market centered on offices, retail sites, healthcare facilities, airports, and other high-traffic buildings. These buyers can justify deployment because occupancy intelligence, energy optimization, and safety monitoring all map to direct operational outcomes. Hybrid work patterns have made that value easier to defend, since landlords and facilities teams now need verifiable utilization data when redesigning layouts or rationalizing real estate footprints. Healthcare and senior-care settings add another layer of resilience because compliance, accident prevention, and privacy-sensitive monitoring support continued investment in floor-based sensing. This means the commercial base of the smart flooring market is supported by both efficiency goals and regulatory requirements, making it broader than a single office-only demand cycle.

Residential is smaller in revenue today but is projected to grow at a 45.37% CAGR through 2031, making it the fastest-growing end-user segment in the smart flooring market. Retrofit-friendly products, wireless control formats, and connected-home compatibility are lowering the barriers that once limited adoption to full-home renovation projects. Warmup’s Matter-compatible underfloor eating controller is a useful example because it links smart heated flooring to major home ecosystems and supports an energy-saving case that homeowners can understand in everyday terms. Industrial and logistics sites also matter because ESD-compliant, sensor-rich floors can support equipment flow, safety monitoring, and automated vehicle zones, widening the reach of the smart flooring industry beyond offices and homes. Public infrastructure and sports facilities extend that pattern further through kinetic flooring, interactive surfaces, and wayfinding-led installations in city projects and leisure venues.

By Application: Analytics Holds The Lead While Entertainment Extends The Growth Curve

Occupancy and space-utilization analytics accounted for 38.26% of the market in 2025, making it the largest application in the smart flooring market. The reason is simple, which is that enterprise buyers can connect occupancy data to immediate cost actions, such as desk planning, lease decisions, HVAC control, and cleaning schedules. That gives the application a direct link to budget decisions, making it easier to justify deployment outside experimental projects. HVAC and energy management are closely linked because floor-level data improves the precision of demand-controlled building systems, especially compared with room-level binary sensors. At the same time, fall detection and elderly-care monitoring remain among the most durable application areas in the smart flooring market because they are tied to safety compliance and non-intrusive resident monitoring.

The fastest-growing application is gaming and interactive entertainment, which is projected to expand at a 43.34% CAGR through 2031. This growth reflects how brands and venues are using interactive flooring to increase dwell time, improve engagement, and create visible experiences in physical spaces. The same logic supports customer engagement and wayfinding use cases in transit hubs and large venues, where responsive floors can guide movement while also adding value through data collection. Security and access control are still smaller use cases, but passive gait and zone-based monitoring are being considered as supportive tools in controlled facilities. As a result, the smart flooring market is no longer driven by a single application, as efficiency-led, safety-led, and experience-led uses are all contributing to demand.

Geography Analysis

North America held 42.73% of the smart flooring market share in 2025, maintaining its leading regional position. The region benefits from a large base of enterprise technology buyers, active green-building enforcement, and healthcare systems that are already familiar with compliance-driven procurement. In the United States, nursing-facility requirements under CMS 42 CFR § 483.25(d) continue to support fall-prevention investment, which strengthens one of the most regulation-linked parts of the smart flooring market. Demand-controlled HVAC programs also improve the regional case for floor sensing because building operators can tie occupancy data to measurable energy savings and operating efficiency. Europe remained another important region in the smart flooring market, supported by building-efficiency rules under the Energy Performance of Buildings Directive and by the appeal of anonymous sensing approaches in privacy-sensitive workplace environments.

Asia-Pacific is projected to grow at a 44.54% CAGR through 2031, which makes it the fastest-expanding regional segment in the smart flooring market. China has already demonstrated commercial-scale use in office properties, where smart sensing floors are linked to lighting and HVAC systems, including a nearly 40% reduction in evening electricity consumption at Shoucheng International Center. Japan is a strong elder-care demand center, and Magic Shields reported deployment of its Koroyawa Sensor Mat III across 1,600 facilities by April 2026. India adds another source of demand through industrial-park modernization and wider adoption of smart buildings, giving the regional smart flooring market exposure to both commercial and industrial settings. South Korea, Australia, and New Zealand are also helping the regional mix through smart-city and connected-building programs that support sensor-led infrastructure upgrades.

South America, the Middle East, and Africa remained smaller parts of the smart flooring market, but they are strategically important because large infrastructure projects can quickly scale demand once procurement begins. Brazil and Argentina are still centered on commercial smart-building pilots, while South Africa is the clearest early adopter in African commercial real estate. In the Gulf, city-scale development programs are creating openings for kinetic and interactive flooring, and Pavegen has highlighted growing interest in energy-autonomous public-realm surfaces that can support urban infrastructure goals. Wider adoption across Turkey, Nigeria, Egypt, and similar markets will depend on sustained urban investment, reliable integration performance, and clearer evidence of payback at scale.

Competitive Landscape

The smart flooring market remains fragmented, and no single vendor controls the category across all technologies or applications. Specialized players such as SensingTex, Future-Shape, and Pavegen compete through sensor intelligence, energy-harvesting design, and application-specific analytics, while broader flooring groups such as Tarkett, Interface, and Shaw Industries bring established distribution and existing customer access. Tarkett’s 2024 revenue reached EUR 3,331.9 million (USD 3,705.5 million), and its network of 35 production sites across 21 countries gives it a scale advantage that smaller pure-play sensor firms cannot easily match. Building-automation incumbents, including Siemens and Honeywell, are approaching the smart flooring market through broader campus, digital-twin, and BMS contracts rather than through a single flooring-only offer. This keeps the field open because strength in one layer, such as hardware manufacturing, software analytics, or automation integration, does not automatically translate into leadership across the full value chain.

Recent company actions show that competition is being shaped through adjacent capability building rather than a single product model. Warmup launched the 7iE Smart Matter WiFi Thermostat in October 2025, which tightened the link between underfloor heating and major smart-home ecosystems and strengthened the residential side of the smart flooring market. Mitsubishi Estate invested in Aeterlink and started a wireless-power demonstration at Tokiwabashi Tower in October 2025, which is directly relevant to lowering installation complexity for under-floor sensor networks. Magic Shields began general sales of the Koroyawa Sensor Mat III in April 2026 after broad piloting, strengthening the elder-care niche with a more mature commercial offering. Zurich’s LignoVolt work also points to a future pipeline of academic and material-science spinouts that could add new entrants to the smart flooring market through sustainable piezoelectric flooring formats.

The main white space remains in lower-cost commercial retrofits and in certified flooring for industrial and logistics environments, where durability, safety, and compliance matter as much as analytics depth. Over time, software platform ownership is likely to be the strongest force for concentration because recurring analytics and control layers can create switching costs even when the physical flooring itself is replaceable. Standards alignment will also shape competitive outcomes, as enterprise buyers increasingly seek easier integration and less reliance on custom middleware. For now, the smart flooring market is still defined more by deployment fit, technical specialization, and integration capability than by any one company’s scale-based dominance.

Smart Flooring Industry Leaders

Tarkett S.A.

Future-Shape GmbH

Scanalytics Inc.

Mohawk Industries, Inc.

Interface, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Tarkett expanded its Melodia vinyl flooring collection with an enlarged color palette, extending the product's role in healthcare and education environments where hygiene and design requirements converge. The expansion followed the January 2026 Interwoven Journeys carpet tile launch and consolidated Tarkett's position in high-specification commercial interiors.

- April 2026: Mohawk Group added Hero Flooring, a global high-performance resilient flooring brand using Nike Grind licensed recycled rubber, to its commercial portfolio, strengthening its offering in fitness and high-impact commercial environments and signaling an intent to serve the sports and fitness facilities end-user segment with sustainability-differentiated products.

- April 2026: Magic Shields commenced general sales of the Koroyawa Sensor Mat III in Japan, an ultra-thin (1.3 cm) sensor-integrated fall-prevention floor mat targeting hospitals and elder-care facilities. The product was already installed across over 1,600 facilities in pilot form, achieved a 93% recommendation rate among piloting institutions, and dominated its category with a 78% sales share in Japan's cushioning mat segment.

- February 2026: Interface launched Noravant, a PVC-free, resilient rubber flooring platform featuring the industry's first woodgrain design in rubber, engineered for healthcare, education, and high-traffic commercial environments. The product carries Cradle to Cradle Certified Silver status and a service lifetime of up to 35 years, advancing Interface's carbon-negative-by-2040 sustainability commitment.

Global Smart Flooring Market Report Scope

Smart Flooring refers to advanced flooring systems embedded with sensors, electronics, and connectivity that enable the floor surface to collect, process, and transmit data or perform automated functions beyond traditional structural and aesthetic roles. Unlike conventional flooring, smart flooring actively interacts with its environment and users to deliver real-time insights and controls.

The Smart Flooring Market Report is Segmented by Component (Hardware, and Software), Technology (Sensor-Embedded Floor Tiles, Smart Heated Flooring, Energy-Harvesting Flooring, Static-Dissipative/ESD Smart Flooring, and Interactive LED/Visualization Flooring), End-User (Residential, Commercial, Industrial and Logistics, Sports and Fitness Facilities, Public Infrastructure/Smart-City Installations, and Other End-Users), Application (Occupancy and Space-Utilization Analytics, Fall Detection and Elderly-Care Monitoring, HVAC and Energy Management, Security and Access Control, Customer Engagement and Wayfinding, Gaming and Interactive Entertainment, and Other Applications), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Hardware |

| Software |

| Sensor-Embedded Floor Tiles |

| Smart Heated Flooring (Electric and Hydronic) |

| Energy-Harvesting Flooring |

| Static-Dissipative / ESD Smart Flooring |

| Interactive LED / Visualization Flooring |

| Residential |

| Commercial |

| Industrial and Logistics |

| Sports and Fitness Facilities |

| Public Infrastructure / Smart-City Installations |

| Other End-Users |

| Occupancy and Space-Utilization Analytics |

| Fall Detection and Elderly-Care Monitoring |

| HVAC and Energy Management |

| Security and Access Control |

| Customer Engagement and Wayfinding |

| Gaming and Interactive Entertainment |

| Other Applications |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

| By Component | Hardware | |

| Software | ||

| By Technology | Sensor-Embedded Floor Tiles | |

| Smart Heated Flooring (Electric and Hydronic) | ||

| Energy-Harvesting Flooring | ||

| Static-Dissipative / ESD Smart Flooring | ||

| Interactive LED / Visualization Flooring | ||

| By End-User | Residential | |

| Commercial | ||

| Industrial and Logistics | ||

| Sports and Fitness Facilities | ||

| Public Infrastructure / Smart-City Installations | ||

| Other End-Users | ||

| By Application | Occupancy and Space-Utilization Analytics | |

| Fall Detection and Elderly-Care Monitoring | ||

| HVAC and Energy Management | ||

| Security and Access Control | ||

| Customer Engagement and Wayfinding | ||

| Gaming and Interactive Entertainment | ||

| Other Applications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current and forecast value of smart flooring?

The smart flooring market was valued at USD 0.68 billion in 2025, reached USD 0.97 billion in 2026, and is forecast to reach USD 5.74 billion by 2031 at a 42.69% CAGR.

Which component leads revenue in smart flooring solutions?

Hardware led revenue with a 65.53% share in 2025 because early deployments required sensor carpets, gateways, and edge processors as the physical base of each installation.

Which technology is growing the fastest in this space?

Energy-harvesting flooring is the fastest-growing technology segment, with a projected 44.57% CAGR through 2031, while sensor-embedded floor tiles remained the largest segment in 2025.

Why are commercial buildings adopting smart floors so quickly?

Offices, retail sites, healthcare facilities, and public buildings use floor sensing for occupancy analytics, HVAC control, and safety monitoring, which gives buyers clear operational value and stronger payback logic.

What is driving adoption in senior-care facilities?

Regulatory focus on accident prevention, privacy concerns around camera monitoring, and the need for real-time fall detection are pushing care providers toward sensor-based flooring systems.

Page last updated on: