Underfloor Heating Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

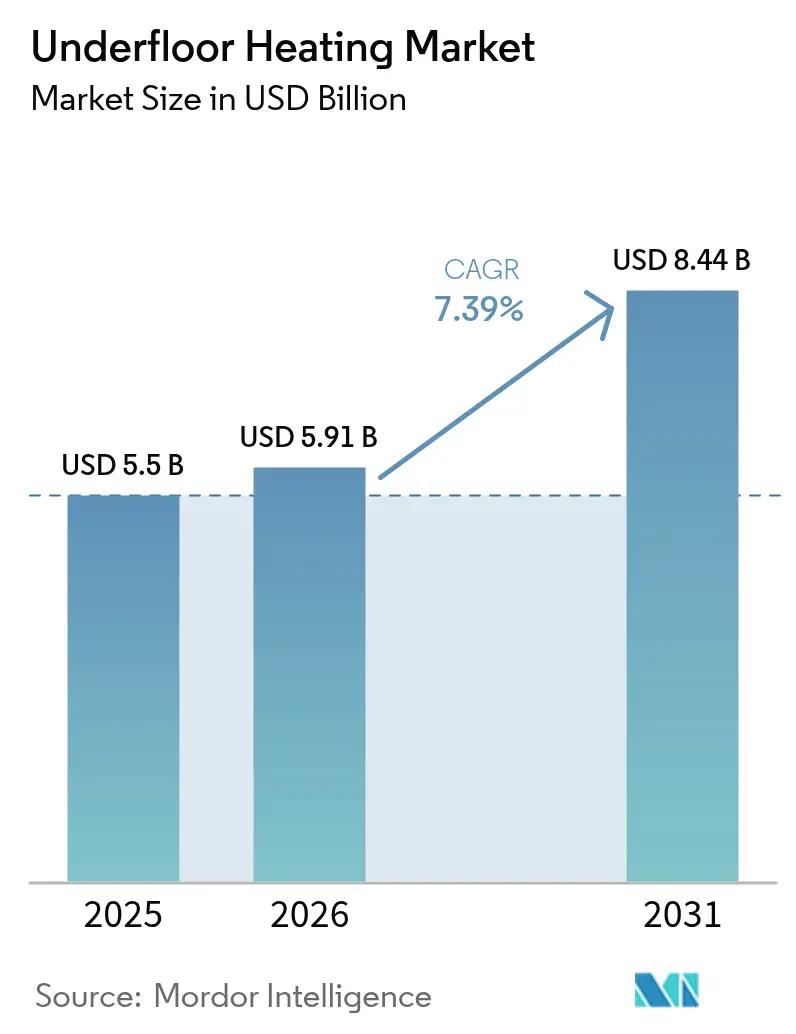

| Market Size (2026) | USD 5.91 Billion |

| Market Size (2031) | USD 8.44 Billion |

| Growth Rate (2026 - 2031) | 7.39% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Underfloor Heating Market Analysis by Mordor Intelligence

The underfloor heating market size was valued at USD 5.5 billion in 2025 and estimated to grow from USD 5.91 billion in 2026 to reach USD 8.44 billion by 2031, at a CAGR of 7.39% during the forecast period (2026-2031). Growth reflects stricter energy-efficiency mandates, rapid urbanisation, and heightened awareness of low-carbon comfort solutions. Europe’s zero-emission building agenda drives demand, while the Asia-Pacific region benefits from smart-city programs and robust heat-pump deployment. Hardware remains the revenue foundation, owing to large-scale pipe and cable demand; yet, services are evolving into a strategic revenue stream as connected controls create lifetime value opportunities. Competition is shifting from pure hardware supply toward platform-based offerings that couple hydronic or electric heat sources with data-driven optimisation services. Premium hospitality projects, digitized retrofit programs, and bio-based components collectively form the most attractive opportunity pool during the forecast period.

Key Report Takeaways

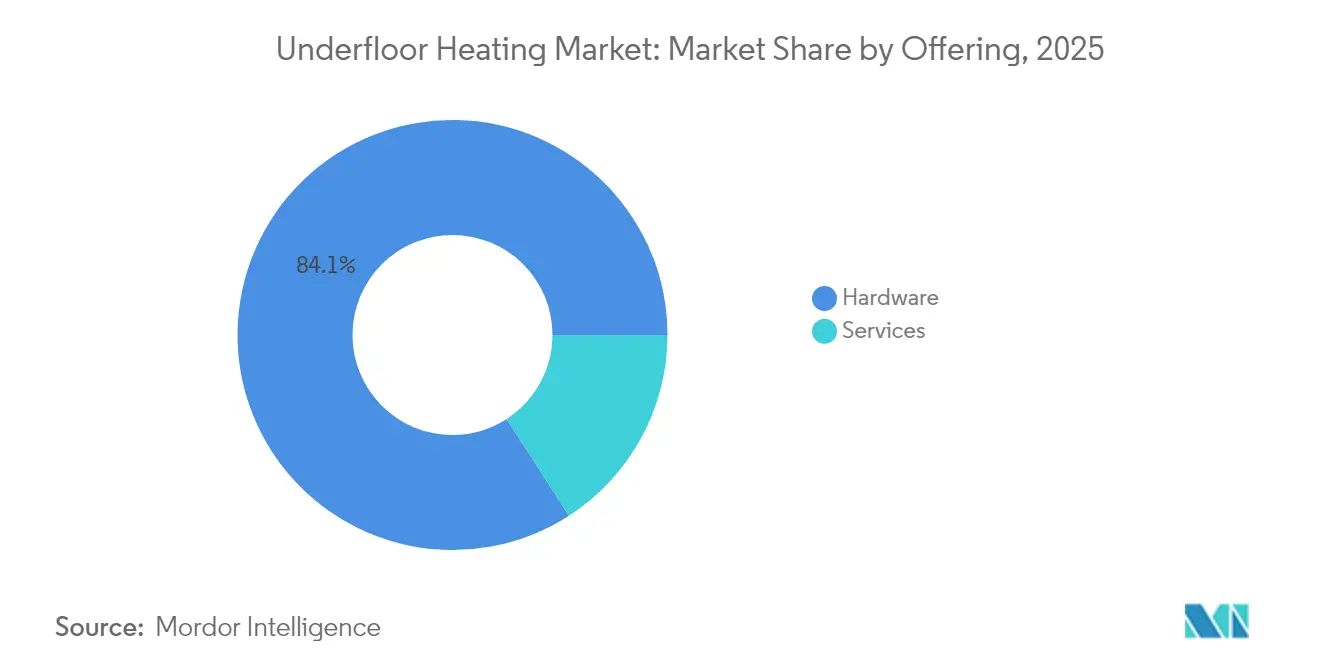

- By offering, hardware led with 84.12% revenue share of the underfloor heating market in 2025, while services are projected to grow at 8.92% CAGR to 2031.

- By system type, hydronic solutions held a 60.85% market share in the underfloor heating market in 2025, and electric alternatives are forecast to expand at an 8.34% CAGR through 2031.

- By component, heating pipes and cables accounted for a 45.62% share of the underfloor heating market size in 2025, whereas control systems are expected to advance at a 9.56% CAGR.

- By installation type, new construction accounted for a 67.95% share of the underfloor heating market in 2025; however, retrofit work is expected to accelerate at a 10.01% CAGR.

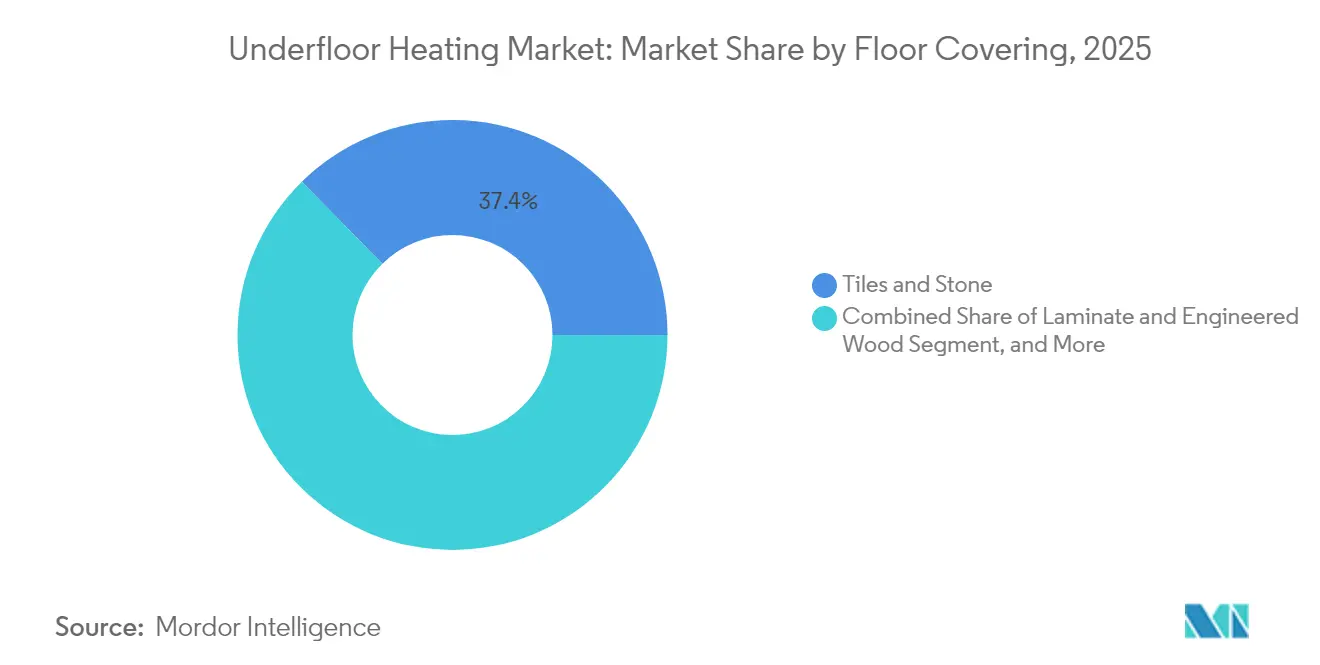

- By floor covering, tiles and stone commanded a 37.36% share of the underfloor heating market in 2025; laminate and engineered wood floors are poised to increase at an 10.86% CAGR.

- By application, residential maintained a 53.88% share of the underfloor heating market in 2025, while commercial hospitality is projected to climb at a 9.48% CAGR.

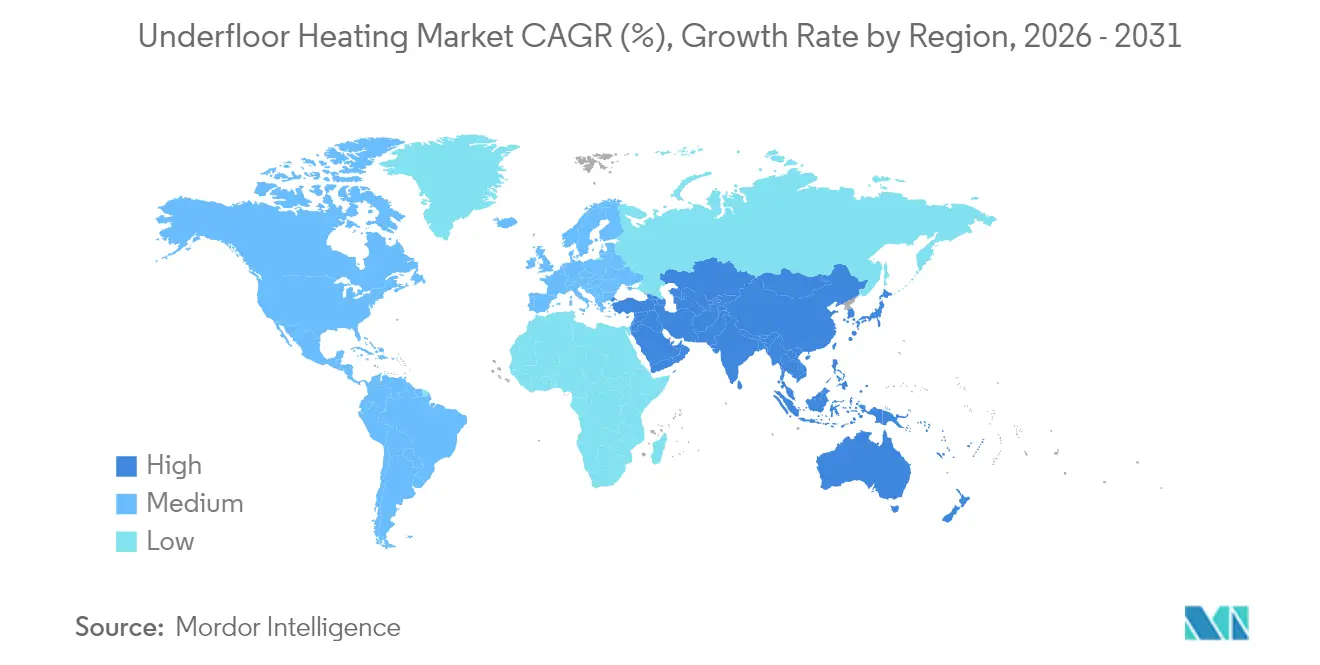

- By geography, Europe dominated with 28.15% revenue share of the underfloor heating market in 2025 and Asia-Pacific represents the fastest-growing region at 10.28% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Underfloor Heating Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Energy-efficient heating demand in cold-climate Europe | +1.8% | Europe, Nordic countries | Medium term (2–4 years) |

| Decarbonisation targets favour low-temperature radiant heating in Nordics | +1.5% | Nordic countries, Germany, UK | Long term (≥ 4 years) |

| Government subsidies for electrified retrofitting in North America | +1.2% | North America, Canada | Short term (≤ 2 years) |

| Rapid smart-home renovations boosting intelligent floor-heating controls in Asia | +1.0% | Asia-Pacific, China, Japan | Medium term (2–4 years) |

| Rising commercial floor-space in GCC integrated with underfloor systems | +0.8% | Middle East, GCC countries | Medium term (2–4 years) |

| Cost savings from solar-hydronic solutions in off-grid Oceania resorts | +0.3% | Oceania, Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Energy-Efficient Heating Demand in Cold-Climate Europe Driving Hydronic Adoption

Governments across Europe are tying renovation grants to renewable integration, pushing hydronic floor heating into mainstream building specifications. Germany’s Building Energy Act funds up to 70% of compliant systems. The UK Heat Network Technical Assurance Scheme sets performance thresholds tailored to low-temperature heat distribution.[1]UK Government, “Heat Network Technical Assurance Scheme,” gov.uk Parallel incentives in France and Italy accelerate market penetration. The resulting scale lowers component prices and encourages a shift toward integrated solar-hydronic packages that align with the EU’s zero-emission target.

Decarbonisation Targets Favour Low-Temperature Radiant Heating in Nordics

Nordic authorities promote supply temperatures of 25-27 °C that maximize heat-pump efficiency. Denmark’s Heat Pump Pool offers DKK 27,000 grants for water-source units pairing seamlessly with underfloor manifolds.[2]The Eco Experts, “Heat Pump Grants Around the World,” theecoexperts.co.uk District-heating networks in Sweden and Norway gain lower return temperatures, reducing system losses. This synergy between grid upgrades and in-building efficiency cements long-run demand across the Nordic underfloor heating market.

Government Subsidies for Electrified Retrofitting in North America

Federal programmes support HVAC electrification, funnelling grants into radiant floor retrofits that leverage low-temperature operation. Canada’s CAD 5,000 incentive lifts consumer payback prospects, while forthcoming US pump standards promise 0.55 quadrillion BTU savings over 30 years. Tighter insulation codes further expand the addressable retrofit base.

Rapid Smart-Home Renovations Boosting Intelligent Floor Heating Controls in Asia

IoT-enriched thermostats integrate occupancy sensing and weather-adaptive start functions, reducing annual bills by up to USD 500. China’s accelerating heat-pump roll-out amplifies demand for digitally coordinated floor loops. Japanese and Korean builders adopt Z-Wave control protocols that embed floor heating into broader smart-home ecosystems.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High Up-front Installation Cost in Emerging South American Markets | -0.9% | South America, Brazil, Argentina | Short term (≤ 2 years) |

| Limited Skilled Installers Restricting Retrofit Penetration in Africa | -0.6% | Africa, Sub-Saharan Africa | Medium term (2-4 years) |

| Latency in Heat-Up/Cool-Down vs. Forced-Air Systems | -0.4% | Global, particularly North America | Short term (≤ 2 years) |

| Moisture and Flooring-Material Compatibility Issues in Humid Tropics | -0.3% | Southeast Asia, Central America, Caribbean | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Up-front Installation Cost in Emerging South American Markets

Hydronic floor systems cost USD 10–20 per square foot to install, which can be challenging for affordability in price-sensitive economies. Currency volatility and reliance on imported components prolong payback periods, confining demand to upscale projects.[3]Deutsche Bank, “Infrastructure Shortfalls in Latin America,” db.com Lower-cost electric mats face high tariff-driven running expenses, underscoring the need for localised production.

Limited Skilled Installers Restricting Retrofit Penetration in Africa

Manifold balancing and pressure testing require capabilities still scarce across many African cities. Improper installation risks moisture damage and drives warranty claims, deterring potential adopters. Manufacturer-led training and certification programmes remain pivotal to unlock retrofit potential.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Hardware Dominance Drives Market Foundation

Hardware generated the majority of 2024 revenue as pipes, cables, manifolds, and actuators remain non-negotiable building-block purchases. Standardisation efforts and bio-based PEX innovation by leaders such as Uponor cut embedded emissions and lower total installed cost. Services, although smaller in value, are growing at a 8.92% CAGR as connected platforms demand professional commissioning and predictive maintenance subscriptions. Vendors now package floor loops, smart thermostats, and installation services to safeguard performance warranties and create new margin streams. The underfloor heating market is increasingly rewarding solution providers that reduce lifecycle risk and streamline building owner decision-making processes.

Technician demand escalates because smart controls must be calibrated to occupancy profiles and integrated with building-management systems. After-sales optimisation contracts help customers hit energy-target benchmarks mandated by regulators, converting once-off equipment sales into annuity revenues. These shifts enhance ecosystem stickiness and cement hardware-plus-service bundles as the default procurement path within the underfloor heating market.

By System Type: Electric Systems Challenge Hydronic Dominance

Hydronic loops retained a 60.85% share in 2025, thanks to superior operating cost economics in large footprints. Electric mats and cables, however, are registering an 8.34% CAGR by excelling in space-constrained renovations where minimal floor build-up is critical. The Schlüter DITRA-HEAT-E assembly reduces total height to 5.5 mm, enabling rapid bathroom upgrades without door-threshold changes. Hybrid layouts, where hydronic supplies principal zones and electric patches serve wet rooms, are becoming common in multifamily developments. This complementary adoption pattern expands the addressable market for underfloor heating.

Hydronic systems continue to garner green-building accolades because they complement heat pumps and solar-thermal collectors. Controls now automatically adjust flow temperature based on outside-air sensors, reducing pump energy losses. Electric solutions compete through refined thermostatic zoning and dynamic demand-response functionality that unlock utility rebates. These technology pathways ensure both system categories will coexist and flourish in distinct project archetypes within the underfloor heating market.

By Component: Control Systems Drive Technology Evolution

Heating pipes and cables comprise 45.62% of 2025 component revenue, while control systems are expanding at the fastest rate of 9.56% CAGR, as occupants seek app-centric temperature management. Weather-based early-start algorithms embedded in Warmup’s 6iE WiFi thermostat, for example, cut energy use by learning thermal lag and occupancy habits. Manifolds incorporate servo-actuators that balance zones in real-time, while insulation panels utilize recycled foam cores to increase R-values. These innovations are transforming passive heat-delivery networks into dynamic thermal ecosystems, positioning intelligent controls as the key value driver in the future underfloor heating market.

Manufacturers differentiate themselves through open-protocol gateways, enabling seamless integration with lighting, shading, and ventilation controls. Advanced diagnostics alert service teams before valve sticking or pump cavitation impacts comfort, further reinforcing service revenue streams. As a result, the underfloor heating market now values digital competency on par with mechanical reliability.

By Installation Type: Retrofit Applications Accelerate Growth

New-build projects still command 67.95% revenue share in 2025, supported by comprehensive design integration that optimises screed thickness, loop spacing, and insulation. Retrofit demand is rising at 10.01% CAGR as cities tighten minimum energy standards; the UK plans to lift rented-home ratings to Band C by 2030.

Low-profile solutions, such as Schlüter-BEKOTEC-THERM, require only 8 mm of screed, thereby mitigating floor-height constraints in heritage buildings. Fast-curing self-leveling compounds shorten downtime, allowing commercial tenants to resume operations quickly. Policy-led incentives, combined with refined retrofit kits, will reinforce this segment as a key growth engine within the broader underfloor heating market.

By Floor Covering: Laminate Innovation Drives Segment Shift

Tiles and stone accounted for 37.36% of 2025 revenue due to their optimal thermal conductivity. Engineered-wood and laminate ranges are growing at an 10.86% CAGR after manufacturers improved dimensional stability and certified products for surface temperatures of ≤ 29 °C. Junckers hardwood offerings exemplify low-emission, acoustically damped specifications that suit hospitality and premium residential projects. These design-flexible finishes appeal to architects seeking warmer aesthetics without compromising efficiency, thereby broadening material choices across the underfloor heating market.

Carpet, vinyl, and linoleum maintain niche shares and demand tailored load matching to offset higher thermal resistance. Advanced heat-diffusion plates and zoned loops mitigate the challenges, ensuring diverse floor-covering portfolios continue to coexist in the underfloor heating market.

By Application: Commercial Hospitality Emerges as Growth Leader

Residential deployments accounted for 53.88% of the 2025 value, indicating a consistent homeowner pursuit of comfort and space-saving climate control. Nonetheless, hotels, resorts, and serviced apartments are expected to post a 9.48% CAGR, driven by premium guest-experience metrics and pressure from ESG scorecards.

Pauls Stradiņš Clinical University Hospital used hydronic slabs in public zones to reduce airborne dust and maintain sanitary conditions. Similar institutional success stories reinforce procurement confidence, elevating underfloor heating as a core feature in high-traffic facilities.

Geography Analysis

Europe retained a 28.15% share in 2025 as region-wide grant schemes, low-carbon building codes, and mature installer networks underpin steady adoption. Germany’s subsidies, the UK’s network standards, and Italy’s Eco Bonus provide multi-layered financial backing. Nordic grid decarbonisation aligns perfectly with 25 °C supply loops, creating a robust local underfloor heating market. European manufacturers invest in circular-material PEX pipelines, improving life-cycle credentials and safeguarding regional technological leadership.

The Asia-Pacific region exhibits the fastest trajectory, with a 10.28% CAGR, driven by urban densification, expanding middle-class comfort expectations, and national smart-city agendas. China’s heat-pump schemes unlock synergistic low-temperature floor applications. Japanese and Korean builders utilize IoT controls for occupancy-driven energy management, integrating underfloor heating into home automation packages. India’s premium mixed-use towers specify radiant floors to meet greener-building codes, while Australia’s resort sector exploits solar-linked hydronic arrays to curb diesel reliance.

North America blends mature new-build uptake with policy-seeded retrofit momentum. Federal electrification incentives and 2028 circulator-pump standards enhance cost competitiveness. The underfloor heating market size for retrofit corridors is poised to expand as states tighten thermal envelope regulations.

The Middle East benefits from HVAC redesign in retail and hospitality, where radiant slabs counteract the effects of high ceiling stratification. South America faces affordability hurdles yet leverages infrastructure investment to integrate floor heating into flagship projects despite currency headwinds. Africa’s pipeline remains aspirational, limited by installer scarcity and financing gaps, though targeted skills programmes are underway.

Regulatory Landscape

In Europe, ecodesign policy is tightening requirements for electric underfloor local space heaters. Commission Regulation (EU) 2024/1103 entered into force on 9 May 2024 and applies from 1 July 2025, setting minimum seasonal space heating energy efficiency requirements (including a 47.5% threshold for electric underfloor local space heaters), which creates a clear compliance step-change for manufacturers selling into the EU.

Safety and lifecycle obligations are also expanding. Commission Delegated Directive (EU) 2026/74 (adopted 12 January 2026) extends repairability requirements to domestic local space heaters, including obligations around spare-parts availability for at least 10 years. This reinforces a shift toward serviceable designs and long-term parts logistics. In North America, installation and electrical safety are governed by codes and standards such as the 2024 International Residential Code (radiant-floor requirements including manifold accessibility and tubing placement rules) and the NEC/NFPA 70 (2023) requirement for GFCI protection for electric floor-heating cables in wet locations, increasing the importance of compliant controls, sensors, and installation practices.

Value Chain Analysis

The value chain begins with upstream materials, including polymers for PEX/PE-RT pipes and insulation foams, and metals such as brass and stainless steel for manifolds, valves, and fittings. These feed component manufacturers supplying heating pipes and cables, insulation panels, manifolds/mixing units, and control systems (thermostats, sensors, actuators). System assemblers and OEM/private-label producers then package these into project-ready kits tailored to new construction and retrofit constraints, after which distribution moves through HVAC wholesalers, specialist distributors, and contractor channels. Installation, commissioning, and after-sales service complete the chain, and are increasingly linked to digital configuration of controls.

Supply remains geographically uneven: Europe functions as a specialized hub for hydronic components, while China is a major export source for volume electric kits and standardized parts. Standards and compliance frameworks shape interoperability and market access, including CENELEC publication of MEST EN 50559:2024 for electric underfloor heating performance characteristics and the EU ecodesign rules under Regulation (EU) 2024/1103. Channel choices are also influenced by consolidation, such as Genuit Group plc acquiring Timoleon OEM (7 August 2024), which highlights continued investment in dry-construction panel formats used to accelerate retrofit and lightweight builds. Across the chain, logistics and inventory complexity remains high as bulky materials (pipes, panels) ship alongside high-value electronics that require tighter handling and version-controlled firmware support.

Competitive Landscape

The underfloor heating market is moderately fragmented. Uponor, Danfoss, and nVent shape core component standards, while Warmup, ThermoSoft, and Schlüter cultivate specialist niches. Technological convergence between HVAC hardware and digital platforms drives acquisitions and divestitures; nVent’s 2024 sale of Raychem, NuHeat, and Pyrotenax re-ordered competitive alignments. Leading firms seek vertical integration with control-algorithm providers to deliver end-to-end performance guarantees.

Material sustainability forms a second strategic battleground. Uponor’s bio-based PEX and circular-material pilot lines signal an industry pivot toward low-embodied-carbon products. Competitors race to certify similar offerings to satisfy procurement guidelines. Service expansion is equally vigorous; Warmup markets data-driven energy-insight dashboards, reinforcing the recurring-revenue narrative.

Partnership ecosystems broaden reach. Honeywell collaborates with proptech platforms to fit floor loops into broader smart-building suites, while Schlüter works closely with tile manufacturers to prevalidate thermal performance. Start-ups apply machine-learning optimisation that boosts 3%–5% additional savings, according to Energy Informatics research. Collective dynamics underline a sector where product performance, digital savvy, and sustainability credentials interact to shape long-term market leadership.

Underfloor Heating Industry Leaders

Uponor Corporation

nVent Electric plc

Danfoss Group

Warmup PLC

Rehau AG & Co.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Policy and program activity continues to reinforce opportunities around low-temperature, heat-pump-aligned underfloor systems and advanced controls. In the United Kingdom, the Boiler Upgrade Scheme change effective 21 July 2026 increased grants to GBP 9,000 for air-to-water or ground source heat pumps in off-gas-grid homes replacing oil or LPG, directly supporting wet (hydronic) underfloor solutions that operate efficiently at lower flow temperatures. At the same time, air-to-air heat pumps received a GBP 2,500 grant but do not support wet systems, which raises the value of clear system selection, installer education, and bundled hydronic packages.

Controls and commissioning represent a visible whitespace where vendors can reduce installation friction and address retrofit skills constraints. Connected thermostats and multi-zone platforms that integrate with broader building automation protocols are being positioned as a compliance and performance lever as standards and codes push energy efficiency and temperature-control functionality. Manufacturer moves such as REHAU's NEA SMART 2.0 factory pre-programming service, along with new connected thermostats from leading brands, point to demand for pre-configured and interoperable control stacks. This supports offerings that combine hardware, configuration, and service contracts (commissioning, diagnostics, and lifecycle support) instead of stand-alone components.

Recent Industry Developments

- July 2026: Rehau AG & Co. launched a factory pre-programming service for its NEA SMART 2.0 control system, shipping configured thermostats, control bases, and actuators to site. This shifts commissioning effort upstream, reducing on-site setup time and helping contractors standardize multi-zone installs in both new build and retrofit workflows.

- January 2026: nVent Electric plc announced the nVent NUHEAT Conductor floor heating thermostat with Wi-Fi and Bluetooth connectivity, mobile app control, and auto-adaptive scheduling. The release strengthens the role of connected controls as a differentiator in electric underfloor heating systems and supports recurring value through software-enabled optimization.

- October 2025: Warmup PLC launched the 7iE Smart Matter WiFi Thermostat, positioned as the first underfloor heating controller with Matter compatibility for major smart-home ecosystems. Matter support lowers integration friction with platforms such as Apple Home, Google Home, and Amazon Alexa, expanding addressable demand for app-centric underfloor heating controls.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the underfloor heating market includes the value of systems installed under floor surfaces that provide space heating through electric elements or hydronic piping, along with the core controls typically sold with these systems.

Scope exclusions: We exclude boilers and heat pumps sold as separate equipment, general building automation sold without underfloor heating, and flooring materials or adhesives.

Segmentation Overview

- By Offering

- Hardware

- Services

- By System Type

- Electric

- Hydronic

- By Component

- Heating Pipes and Cables

- Insulation Panels

- Manifolds and Mixing Units

- Control Systems (Thermostats, Sensors and Actuators)

- By Installation Type

- New Construction

- Retrofit

- By Floor Covering

- Tiles and Stone

- Laminate and Engineered Wood

- Carpet and Rugs

- Vinyl and Linoleum

- By Application

- Residential

- Single-Family

- Multi-Family

- Commercial

- Offices

- Retail

- Hospitality

- Institutional

- Healthcare

- Educational Facilities

- Industrial

- Residential

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Nordics

- Benelux

- Russia

- Rest of Europe

- Middle East

- GCC

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Southeast Asia

- Rest of Asia-Pacific

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with mapping where underfloor heating demand shows up in public data, and which signals reliably move with installations and system shipments. We reviewed building and construction indicators, heating policy updates, and energy efficiency programs, because these are often the first triggers for adoption at scale.

To anchor assumptions, we referred to non-paywalled sources such as International Energy Agency releases, Eurostat construction and energy statistics, U.S. Energy Information Administration heating data, U.S. Census construction spending, and standards and guidance published by bodies such as ASHRAE. We also used company filings, investor presentations, reputable trade press, and a paid subscription for company financials and news context, plus a patent database to track product direction. These examples are not exhaustive, and many other public sources and documents were reviewed to collect data, validate numbers, and clarify open questions.

Primary Interviews and Surveys

Primary conversations were used to convert broad construction and heating signals into underfloor heating specific inputs, especially for split by electric versus hydronic demand and typical price points by project type. We spoke with a mix of manufacturers, distributors, installers, and building design stakeholders across major regions, then re-contacted a subset when early model results showed large variance versus channel feedback.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 12% | APAC: 50% |

| Mid tier: 53% | Functional/Unit leaders: 28% | EMEA: 32% |

| Smaller Players: 14% | Managers: 60% | Americas: 18% |

Market-Sizing & Forecasting

Sizing was built using a top-down and bottom-up mix, where the top-down view starts from the addressable building activity and heating retrofit pool, which are then filtered by penetration rates for underfloor heating by region and building type. Once that demand pool was shaped, we corroborated results with selective bottom-up checks like sampled installer throughput, distributor channel checks, and an ASP times volume build using typical system area coverage.

Key inputs included new residential and commercial floor area additions, renovation intensity, regional electrification and efficiency incentive signals, electric versus hydronic adoption mix, and the average system selling price that changes with control features and installation complexity. Because pricing is a meaningful driver here, ASPs were trended using inflation, component cost direction, and interview based expectations for control and sensor attach rates, rather than assuming a flat price.

For forecasting, scenario analysis was used so we could reflect different paths for construction cycles and retrofit momentum, and the scenarios were tied back to what practitioners described as realistic installation capacity and permitting timelines. Where bottom-up signals were thin in smaller countries, gaps were handled by using proxy indicators (such as floor area growth and heating degree conditions) and then normalized through expert review before totals were finalized.

Data Validation & Update Cycle

Outputs were checked against independent indicators like regional construction spending trends, heating equipment demand signals, and the expected split between electric and hydronic installations. When there were outliers, we traced them back to the specific assumption driving the jump (for example, penetration rates or pricing/mix).

The model then goes through a multi-step analyst review so definitions, math, and country rollups stay consistent. Key assumptions are re-validated through follow-up calls when variance stays high.

Reports are refreshed annually, and interim updates are triggered when major policy changes, sharp currency moves, or construction slowdowns materially change near-term demand. Before delivery, a final pass is completed to reflect the latest public releases and newly validated price and mix assumptions.

Mordor Intelligence's Underfloor Heating Market Size Versus Other Published Estimates

Published market sizes for underfloor heating do not always match because teams choose different year cutoffs, price assumptions, and boundaries around what is counted as part of the system sale. Even when the same words are used, the model can move if the study leans more on construction outlooks, or if it leans more on install activity and channel feedback.

In this report, currency conversion timing and quarterly ASP refresh checks are used to keep the market value aligned with how electric mats, hydronic piping kits, and control packs are priced and bought across regions, a step that tends to reduce drift in the near years for Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 5.91 B (2026) | |

| Trade Journal A | USD 5.30 B (2024) | Uses an earlier base year and can understate current value if recent price changes and control attach rates are not refreshed frequently, and if currency translation is done using a single annual average. |

| Global Consultancy B | USD 6.19 B (2025) | Defines a broader system and component scope in parts of the value chain and applies a different pricing ladder for multi-zone controls, which can lift the reported total versus a tighter system-only definition. |

The spread is largely explained by timing and what gets priced into the system sale, especially when controls and installation related kits are treated differently. By tying value to a clear demand pool and then re-checking price and mix assumptions through field feedback, the final number stays traceable to repeatable steps rather than a single broad growth curve.

Key Questions Answered in the Report

What is the current value of the underfloor heating systems market?

The market is valued at USD 5.91 billion in 2026 and is projected to reach USD 8.44 billion by 2031.

Which system type dominates the market?

Hydronic solutions led with 60.85% share in 2025, although electric systems are growing faster at an 8.34% CAGR.

Why is Europe a leading region for underfloor heating adoption?

Europe benefits from generous subsidies, strict building-energy codes, and skilled installer networks that collectively drive demand.

What is the primary growth driver for retrofit installations?

Stricter energy-performance standards and low-profile installation technologies have pushed retrofit applications to a 10.01% CAGR forecast.

Which application segment is expanding the quickest?

Commercial hospitality is set to rise at 9.48% CAGR as hotels and resorts prioritise guest comfort and ESG compliance.

How are smart controls influencing the market?

Intelligent thermostats and IoT-enabled manifolds optimise energy consumption, making control systems the fastest-growing component segment at 9.56% CAGR.

Page last updated on: