Market Overview

| Study Period | 2020 - 2031 |

|---|---|

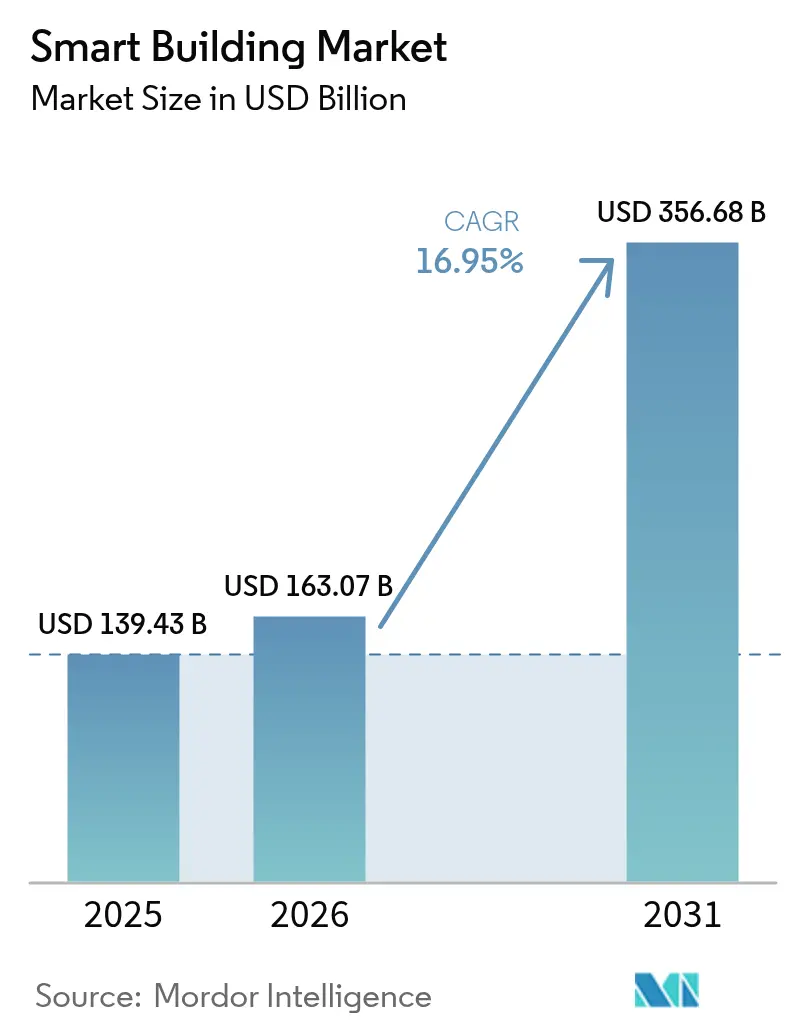

| Market Size (2026) | USD 163.07 Billion |

| Market Size (2031) | USD 356.68 Billion |

| Growth Rate (2026 - 2031) | 16.95% CAGR |

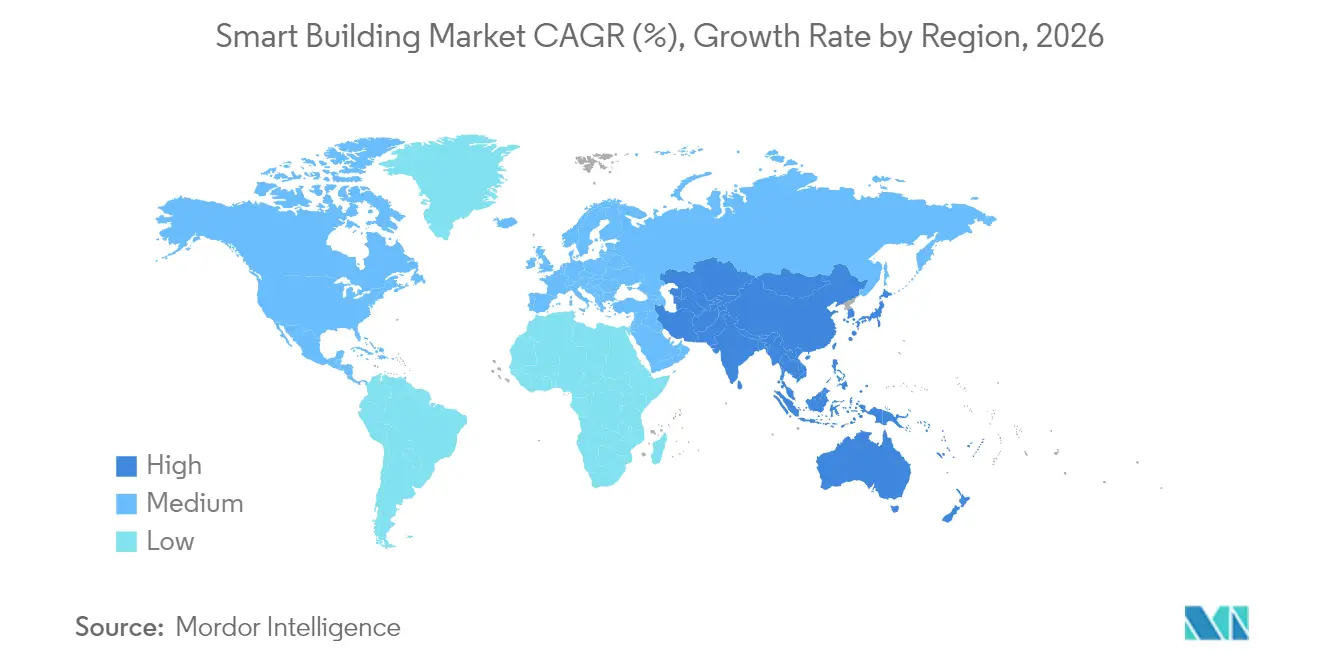

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Smart Building Market Analysis by Mordor Intelligence

The smart building market size in 2026 is estimated at USD 163.07 billion, growing from 2025 value of USD 139.43 billion with 2031 projections showing USD 356.68 billion, growing at 16.95% CAGR over 2026-2031. Enhanced integration of operational technology and information technology, combined with real-time analytics, is converting buildings from passive assets into active energy nodes. Cyber-secure, open architectures are being selected ahead of proprietary systems as owners seek to unify lighting, HVAC, security, and energy management on a single platform.[1]Stromquist & Company, “Integrated Building Automation: 2025 Outlook,” stromquist.com Retrofit demand is climbing because commercial real-estate portfolios must align with net-zero pathways, while utilities are rewarding buildings that automate demand response with new tariff structures.[2]U.S. Department of Energy, “Better Buildings Initiative Progress Update 2025,” energy.gov Asia Pacific leads adoption as China and India scale national smart-city programs that mandate connected building infrastructure.

Key Report Takeaways

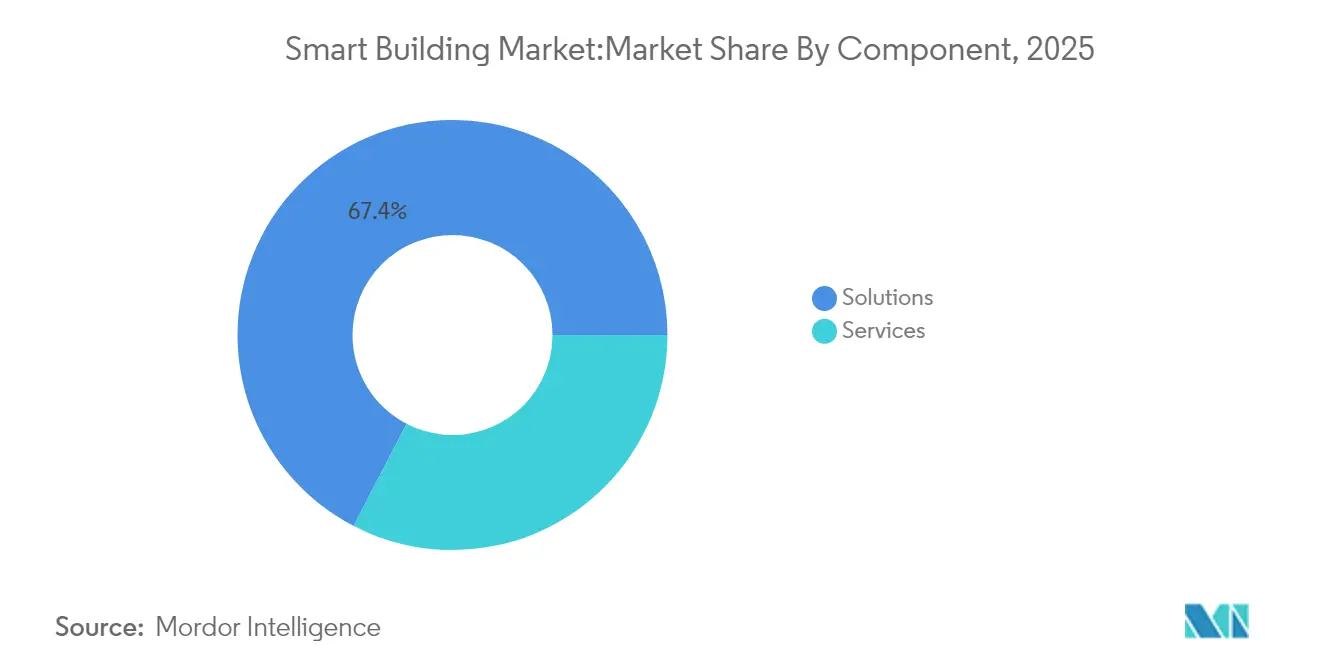

- By component, Solutions held 67.40% of revenue in 2025, while Services is forecast to record a 17.20% CAGR through 2031.

- By connectivity technology, wired infrastructure retained 54.75% market share in 2025; wireless platforms are projected to expand at an 18.35% CAGR to 2031.

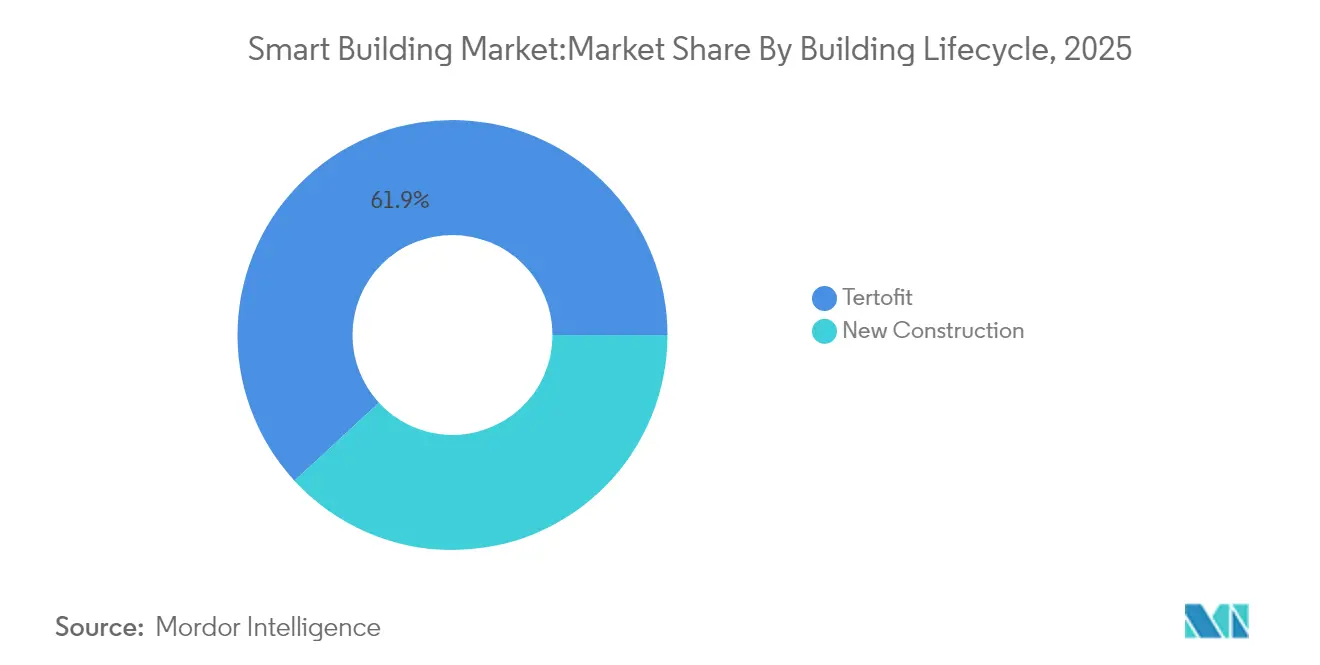

- By building lifecycle, retrofit projects captured 61.85% of the smart building market size in 2025, whereas new-construction deployments are set to grow at 17.15% CAGR between 2026 and 2031.

- By building type, commercial facilities led with 59.65% revenue share in 2025; residential buildings are anticipated to achieve the fastest 17.72% CAGR through 2031.

- By region, Asia Pacific commanded 31.55% of global revenue in 2025 and is expected to advance at a 19.85% CAGR to 2031.

- Siemens, Honeywell, Johnson Controls, and Schneider Electric collectively delivered more than 40% of multi-site smart building deployments completed in 2024.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Smart Building Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating net-zero carbon mandates | +3.2% | EU, North America, global spill-over | Medium term (2–4 years) |

| IoT sensor proliferation | +2.8% | North America, Europe, developed APAC | Short term (≤ 2 years) |

| OT-IT cybersecurity convergence | +2.1% | North America, Europe, developed APAC | Medium term (2–4 years) |

| Utility demand-response incentives | +1.7% | North America, early Europe | Short term (≤ 2 years) |

| Campus digital-twin roll-outs | +2.4% | APAC core, MEA spill-over | Medium term (2–4 years) |

| EU Taxonomy aligned finance | +1.9% | Europe, influencing global norms | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Escalating Net-Zero Carbon Mandates Driving Comprehensive Building Retrofits

Net-zero regulations require deep energy refurbishment because buildings generate 40% of global emissions. Mandates covering whole portfolios are pushing owners to install high-efficiency HVAC, electrify heat, and layer analytics that verify performance. ABB estimates the retrofit opportunity could reach USD 3.9 trillion by 2050 as decarbonization deadlines shorten.[3]ABB Group, “Global Building Retrofit Pathways,” abb.com Regional differences in definitions are accelerating local innovation, with many city codes surpassing national targets.

IoT Sensor Proliferation Enabling Real-Time Building Intelligence

An expanding sensor base is giving operators granular visibility into occupancy, equipment health, and indoor-air quality. China hosts 31 million smart buildings, while the United States has 16 million as of 2025. Platforms such as Johnson Controls’ OpenBlue have documented 10%–12% energy savings by turning raw data into prescriptive controls. Demand for low-power wireless sensors is rising as industrial sensor revenue approaches USD 29.9 billion in 2025.

OT-IT Cybersecurity Convergence Enabling Integrated Building Platforms

Secure connectivity is foundational now that buildings must exchange data with utilities and vehicle chargers. The U.S. Energy Modernization Cybersecurity Implementation Plan endorses standardized encryption for Building Energy Management Systems, facilitating grid-interactive buildings without raising cyber-risk. The International Energy Agency adds that digital controls can automate up to 10% demand flexibility in commercial stock.

Utility Demand-Response Programs Accelerating Smart Building Adoption

Dynamic tariffs reward buildings that lower load during peak periods. U.S. demand-response capacity surpassed 33 GW in 2023 and is set for double-digit growth, making automated load-shedding financially attractive. AI-driven controls allow facilities to participate without sacrificing occupant comfort, unlocking new revenue streams

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy BMS protocol fragmentation | −1.8% | Mature markets with ageing stock | Medium term (2–4 years) |

| Semiconductor device cost inflation | −1.3% | Price-sensitive emerging regions | Short term (≤ 2 years) |

| Data-privacy restrictions on cloud analytics | −0.9% | Europe + privacy-focused markets | Medium term (2–4 years) |

| Skills gap in AI-enabled facility management | −1.1% | APAC, MEA, Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Legacy BMS Protocol Fragmentation Impeding System Integration

Older Building Management Systems use proprietary protocols that complicate retrofits. A 2024 MDPI review identified this fragmentation as a top barrier, often forcing owners to deploy middleware or replace entire subsystems.[4]MDPI, “Barriers to Smart Building Deployment: A Review,” mdpi.com Integration delays raise project costs and can erode the business case for advanced analytics.

Capex Inflation for Semiconductor-Intensive Devices Post-2024 Shortage

Post-2024, rising Capex costs due to semiconductor shortages are creating structural challenges for smart building deployments, particularly in sensor-heavy systems like HVAC, access control, and energy management. Elevated wafer fab investments through 2032, combined with fluctuating foundry Capex, have kept advanced node and power/analog chip prices above pre-shortage levels, limiting OEM discounts on devices such as smart meters, controllers, and edge gateways. As a result, building owners face higher upfront costs and longer payback periods, slowing adoption in cost-sensitive commercial and mid-tier segments of the global smart building market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Solutions Dominate While Services Accelerate

Solutions generated 67.40% of 2025 revenue, reflecting their central role in lighting control, security integration, and energy management. Cloud-native Building Management Systems are replacing on-premise servers, cutting upgrade downtime and enabling faster feature deployment. Services hold a smaller share but are growing at 17.20% CAGR as owners outsource analytics, cybersecurity monitoring, and lifecycle maintenance. This shift is easing internal skill shortages while creating recurring revenue streams for vendors.Wider availability of open APIs is driving partnerships between solution providers and specialist service firms. The smart building market is seeing managed-service contracts bundled with outcome-based guarantees that commit vendors to energy-saving thresholds. As artificial-intelligence modules become embedded, demand for continuous tuning and model retraining rises, reinforcing service growth.

By Connectivity Technology: Wireless Growth Outpaces Wired Infrastructure

Wired Ethernet, BACnet MS/TP, and power-over-Ethernet still connect 54.75% of smart devices, but wireless installations are expanding at an 18.35% CAGR. Radio protocols offer install flexibility for heritage buildings where core drilling is impractical. Wi-Fi 6/6E enhances bandwidth for video analytics, while Zigbee and Thread handle low-power sensors. DECT NR+ introduces sub-GHz coverage for dense device clusters, a standard now backed by Siemens and Schneider Electric.Growing device density is shifting designs toward multi-protocol access points that coordinate Bluetooth beacons, LoRaWAN meters, and 5G gateways on a converged backbone. Cyber-hardened mesh architectures allow edge devices to negotiate credentials autonomously, cutting commissioning time.

By Building Lifecycle: Retrofit Market Dominates with Compelling ROI

Retrofits captured 61.85% of smart building market share in 2025 because energy savings deliver payback in under five years for many office portfolios. Financial penalties for exceeding carbon caps, such as Local Law 97 in New York, make upgrades unavoidable. Owners prioritize wireless sensors, variable-frequency drives, and cloud analytics because these solutions minimize tenant disruption.New construction represents 38.15% but is expanding faster at 17.15% CAGR, reflecting a design-for-digital ethos in flagship projects. Developers embed fiber, edge servers, and renewable microgrids during construction, avoiding later retrofit costs. Building Information Modeling data feeds directly into digital-twin platforms that optimize handover and operation.

By Building Type: Commercial Leads While Residential Accelerates

Commercial buildings contributed 59.65% of 2025 revenue because large floorplates amplify efficiency gains. Airports and mixed-use campuses deploy integrated command centers that blend security, HVAC, and lighting dashboards. The residential segment is smaller yet rising at 17.72% CAGR as smart thermostats and unified applications move into mid-market apartments. Bundled energy-management services are being marketed alongside broadband packages, increasing penetration.Institutional facilities such as hospitals and universities are adopting fault-detection analytics to control maintenance budgets and enhance occupant comfort. Industrial properties integrate environmental monitoring with production schedules, linking facility metrics to corporate sustainability targets.

Geography Analysis

Asia Pacific led the smart building market with a 31.55% share in 2025 and will maintain the fastest 19.85% CAGR through 2031. National smart-city programs in China, South Korea, and Singapore mandate connected building systems that feed city-wide digital twins. India’s Grade-A commercial real estate expansion is also embedding intelligent lighting, air-quality sensors, and renewable microgrids.North America follows closely, propelled by utility demand-response programs and mandatory carbon-performance disclosure. The U.S. Better Buildings Initiative has already logged USD 22 billion in savings, validating the financial case for analytics retrofits. Canada’s national building code now references smart-meter-compatible controls, nudging regional adoption.Europe shows strong policy alignment via the EU Taxonomy, Energy Performance of Buildings Directive, and Renovation Wave strategy. Data-sovereignty rules encourage edge computing, so vendors supply on-site AI inference engines coupled with cloud dashboards. Scandinavia is pioneering district heating integration, while Germany expands smart-meter gateways that communicate secure load data to grid operators.

Regulatory Landscape

Smart building deployments are increasingly shaped by building decarbonization and performance rules that embed digital controls into compliance pathways. In the European Union, Directive (EU) 2024/1275 (Energy Performance of Buildings Directive, recast) entered into effect on May 24, 2026. It establishes a framework that includes zero-emission targets for new buildings by 2030 and a phased approach to fossil-fuel heating phase-out by 2040. The EPBD also elevates smartness-related tools such as the Smart Readiness Indicator (SRI) within the broader energy performance regime, linking building upgrades to verifiable, technology-enabled outcomes.

Enforcement and federal procurement rules are also tightening requirements around cybersecurity, commissioning, and data practices. In July 2026, the European Commission moved to enforcement by launching infringement procedures against member states for missing the May 29, 2026 transposition deadline, while also publishing a first assessment of draft National Building Renovation Plans submitted between December 2025 and May 2026. In the United States, the GSA Smart Buildings program (ADM 7002.1) requires smart building components to align with OCIO standards and incorporate BIM, and DOE actions around federal building efficiency rules (including the compliance-date stay for 10 CFR part 433, subpart B until September 1, 2026) influence timing for technology refresh cycles. Internationally, ISO 24359-1:2026 further formalizes building commissioning process planning, reinforcing performance verification as part of the deployment lifecycle.

Value Chain Analysis

The smart building value chain spans semiconductor-intensive sensing and control hardware (sensors, meters, controllers, gateways), wired and wireless connectivity stacks, building management and analytics software, and integration plus lifecycle services (commissioning, cybersecurity monitoring, tuning, and maintenance). Large automation vendors (for example, Siemens, Schneider Electric, ABB, Honeywell, and Johnson Controls) increasingly bundle devices, platforms, and managed services, while specialist partners provide interoperability layers, OT-IT security tooling, and domain analytics. Deployment channels include direct enterprise sales to commercial and institutional owners, contractor and systems-integrator networks for retrofits, and OEM partnerships that embed controls into HVAC, lighting, and power equipment.

Upstream constraints and ecosystem convergence are reshaping sourcing and partner strategies. Component and logistics volatility, including tariff-driven cost pressure referenced in 2025-2026 market context, is pushing dual-sourcing and more regionalized supply nodes for controllers, power electronics, and edge gateways. At the same time, competition for cooling, power distribution equipment, and skilled labor is rising as AI data center buildouts draw on similar infrastructure inputs as smart building projects. Vendor moves in 2026 highlight convergence across adjacent energy and IoT domains, including ABBs integration work linking Samsung SmartThings Pro with ABB Ability Building Pro for enterprise IoT interoperability, and Siemens collaboration with FuelCell Energy to explore distributed energy and microgrid-aligned electrical balance-of-plant systems that connect building loads to onsite generation architectures.

Competitive Landscape

Top Companies in Smart Building Market

The smart building market features concentrated leadership yet remains open to disruptors. Honeywell, Siemens, Johnson Controls, and Schneider Electric supply end-to-end platforms that bundle sensors, controllers, and analytics. Johnson Controls has deployed OpenBlue across financial and healthcare campuses, reporting double-digit energy savings for marquee clients. Siemens’ Building X suite integrates lighting, security, and microgrid management under a common user interface.

Technology firms are entering through software layers. Cisco positions its Catalyst switches as converged building networks, while IBM pairs Maximo asset management with Watson AI for predictive maintenance. Partnerships are forming to overcome interoperability limits; Nordic Semiconductor allied with Legrand and Schneider Electric to advance DECT NR+ as a multi-vendor wireless framework.

Investment is flowing into edge-AI startups offering specialized analytics for air quality, occupancy, and equipment health. Established players respond by acquiring or partnering with these firms rather than developing niche algorithms internally, accelerating innovation while protecting installed base revenues.

Smart Building Industry Leaders

Honeywell International Inc.

Siemens AG

Schneider Electric SE

IBM Corporation

ABB Ltd

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulation-driven retrofit compliance remains a primary whitespace area because many existing portfolios still operate fragmented BMS stacks that limit measurable energy performance improvements. The EPBD recast (Directive (EU) 2024/1275), effective May 24, 2026, creates concrete triggers for upgrading non-residential automation where large HVAC or heating systems are present. National transpositions are already appearing, such as Irelands S.I. No. 168/2026 introducing an A0 building energy rating category tied to zero-emission buildings. This policy backdrop supports solutions that shorten retrofit disruption, including wireless sensing, cloud-managed BMS upgrades, and standardized commissioning aligned with ISO 24359-1:2026.

Another opportunity is the shift from point solutions to interoperable, service-led operational intelligence that reduces integration friction and sustains performance over time. Technical frameworks that standardize semantics and compliance checking (such as EN 50090-6-2:2025 for HBES IoT semantic models and CEN/TR 18276:2026 checklists for BACS compliance workflows) support multi-vendor integration, directly addressing the legacy protocol fragmentation restraint highlighted in mature building stock. Vendor actions reinforce this service-led direction: Siemens launched Asset Performance Advanced as a managed service tied to Building X in May 2026, and Schneider Electric launched EcoCare for BMS service plans in the United States in June 2026, both aligning predictive maintenance and analytics with recurring service delivery models that building owners can adopt even when internal FM skills are constrained.

Recent Industry Developments

- July 2026: Siemens signed a five-year partnership with Higher Colleges of Technology (HCT) to develop smart campus technologies aligned with UAE Net Zero 2050 goals. The collaboration centers on modernizing campus infrastructure and accelerating digital building capabilities, expanding Siemens footprint in education and public-sector deployments across the region.

- June 2026: Schneider Electric launched EcoCare service plans for Building Management Systems (BMS) in the United States, using AI-driven analytics for predictive maintenance and operational intelligence. The move strengthens Schmidts service-led model around installed BMS bases, raising competitive pressure on vendors that rely mainly on project-driven integration revenue.

- June 2024: Honeywell completed the acquisition of Carriers Global Access Solutions business. The deal expands Honeywells building security and access control portfolio, supporting more integrated smart building offerings that combine physical security data with broader building automation platforms.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the total revenue generated from smart building solutions and services that help monitor, automate, and optimize how buildings run, across commercial, residential, and industrial facilities. It includes systems that connect equipment, sensors, and software to improve energy use, safety, and operations.

Scope exclusions: We exclude standalone consumer smart-home gadgets that are not part of an integrated building system, and we also exclude general construction spending that is not directly tied to smart-enablement.

Segmentation Overview

- By Component

- Solutions

- Building Energy Management Systems

- Infrastructure Management Systems

- Intelligent Security Systems

- Lighting Control Systems

- HVAC Control Systems

- Other Solutions

- Services

- Professional Services

- Managed Services

- Solutions

- By Connectivity Technology

- Wired

- Wireless

- Wi-Fi

- ZigBee / Z-Wave

- Bluetooth Low Energy

- 6LoWPAN and Others

- By Building Lifecycle

- New Construction

- Retrofit

- By Building Type

- Residential

- Commercial

- Office

- Retail

- Hospitality

- Airports and Transportation Hubs

- Industrial and Logistics

- Institutional (Healthcare, Education, Government)

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Kenya

- Rest of Africa

- Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Rest of Asia Pacific

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping what a smart building purchase typically contains, and how that value shows up in public information. We used accessible sources such as the International Energy Agency (IEA) for buildings energy context, U.S. Energy Information Administration tables for electricity use signals, Eurostat for building and energy indicators in Europe, and United Nations trade statistics for directional checks on relevant equipment flows.

We also reviewed standards and guidance publications (for example ASHRAE and ISO documents), peer reviewed journals that discuss building automation and energy management outcomes, and company annual reports, investor decks, and reliable press coverage for adoption cues and price movement narratives. Where available, a paid subscription tool for company financials and a patent database were used only to support vendor mapping and to sanity check technology focus areas. These desk sources are not exhaustive, and many other public references were also used to collect, validate, and clarify data points during the study.

Primary Interviews and Surveys

Primary work was used to confirm what buyers count as smart building spend and how budgets split across solutions and services, especially for retrofit projects where scopes change by site. We spoke with a mix of solution providers, system integrators, building owners, and facility teams across APAC, EMEA, and the Americas, so assumptions on adoption pace, pricing, and service attach rates could be tightened where desk data was broad.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 14% | APAC: 45% |

| Mid tier: 47% | Functional/Unit leaders: 30% | EMEA: 32% |

| Smaller Players: 22% | Managers: 56% | Americas: 23% |

Market-Sizing & Forecasting

Sizing is built mainly through a top-down model where building stock, new construction versus retrofit activity, and smart system adoption rates are used to reconstruct the addressable demand pool by region. That demand pool is then converted into value using typical solution mix and service intensity, with currency handling kept consistent by year so comparisons remain clean.

To keep the numbers realistic, the totals are corroborated with selective bottom-up approximations, such as sampled vendor revenue splits, channel checks for system integration intensity, and ASP x volume logic for common building subsystems (for example energy management, security and access, and infrastructure monitoring). Inputs that materially move the model include retrofit share, commercial floor space growth, wireless versus wired preference, energy efficiency policy push, and the typical services attach rate after installation, which are then stress tested in interviews.

Forecasting is done using scenario analysis supported by a simple multivariate regression on key drivers like building activity, electricity price pressure, and smart adoption maturity, and then adjusted where experts indicate faster or slower cycles. When a region has limited public indicators, gaps are handled by using proxy metrics (such as construction output and urbanization pace) and then cross checked through primary feedback before finalization.

Data Validation & Update Cycle

Validation is done through repeated cross checks between the model output and independent signals, such as regional construction direction, building energy management uptake, and the observed balance between solutions and services. Outliers are reviewed to determine whether they come from a one-time event, a definition mismatch, or a unit conversion issue, and then the driver assumptions are revisited.

Before sign-off, the numbers go through multi-step analyst reviews, and call-backs are triggered when interview feedback shows a meaningful variance in adoption, pricing, or service attachment. Reports are refreshed annually, and interim updates are made when material events change outlook, such as major policy shifts or sharp changes in building investment. Right before delivery, we do a fresh pass on key variables so the view shared is the most current one available.

Mordor Intelligence's Smart Building Market Size Versus Other Published Estimates

Published smart building values often differ because teams do not always count the same spend, and they also pick different base years, conversion rates, and assumptions on how fast services scale after deployments. The outcome is that two reasonable looking numbers can still be far apart when you put them next to each other.

Key gap drivers are usually practical ones, such as whether retrofit programs are fully counted, whether services like integration and maintenance are included, and how solutions are grouped across energy management, security, and infrastructure monitoring. Some estimates also lean into an aggressive adoption curve for wireless upgrades, while others keep a conservative ramp and then report a smaller current-year value.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 139.43 B (2025) | |

| Global Consultancy A | USD 141.79 B (2025) | Scope packaging differs by sub-system, and service definitions can be broader, which can pull more deployment and ongoing support revenue into the counted total. |

| Industry Research Publisher B | USD 143.00 B (2025) | Uses a faster near-term uplift into 2026 and may treat certain infrastructure management items as part of the core solution bucket, which can inflate current-year value when compared to a stricter mapping. |

The table shows a tight band for 2025, and the remaining spread is mostly explained by what is treated as smart building services versus adjacent building tech spend. In Mordor Intelligence's model, integration and lifecycle services are counted only when they are tied to a defined smart building system deployment (especially in retrofit jobs), which keeps the value traceable to a repeatable demand pool rather than broad building operations spending.

Key Questions Answered in the Report

What is the current size of the smart building market?

The smart building market is valued at USD 163.07 billion in 2026 and is projected to reach USD 356.68 billion by 2031.

Which region is growing fastest for smart buildings?

Asia Pacific is forecast to register a 19.85% CAGR through 2031, driven by national smart-city programs and large-scale commercial developments.

Which is the fastest growing region in Smart Building Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Why are retrofit projects dominating the smart building market?

Existing buildings account for most floor space; retrofits deliver quick payback and help owners comply with tightening carbon regulations, giving them 61.85% market share in 2025.

How are demand-response incentives influencing adoption?

Utilities pay buildings that automatically reduce load during peak periods; U.S. programs already total more than 33 GW of flexible capacity, incentivizing investments in smart controls.

Which companies lead the competitive landscape?

Honeywell, Siemens, Johnson Controls, and Schneider Electric head the field with integrated platforms that combine hardware, software, and managed services.

Page last updated on: