Slovak Republic Facility Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

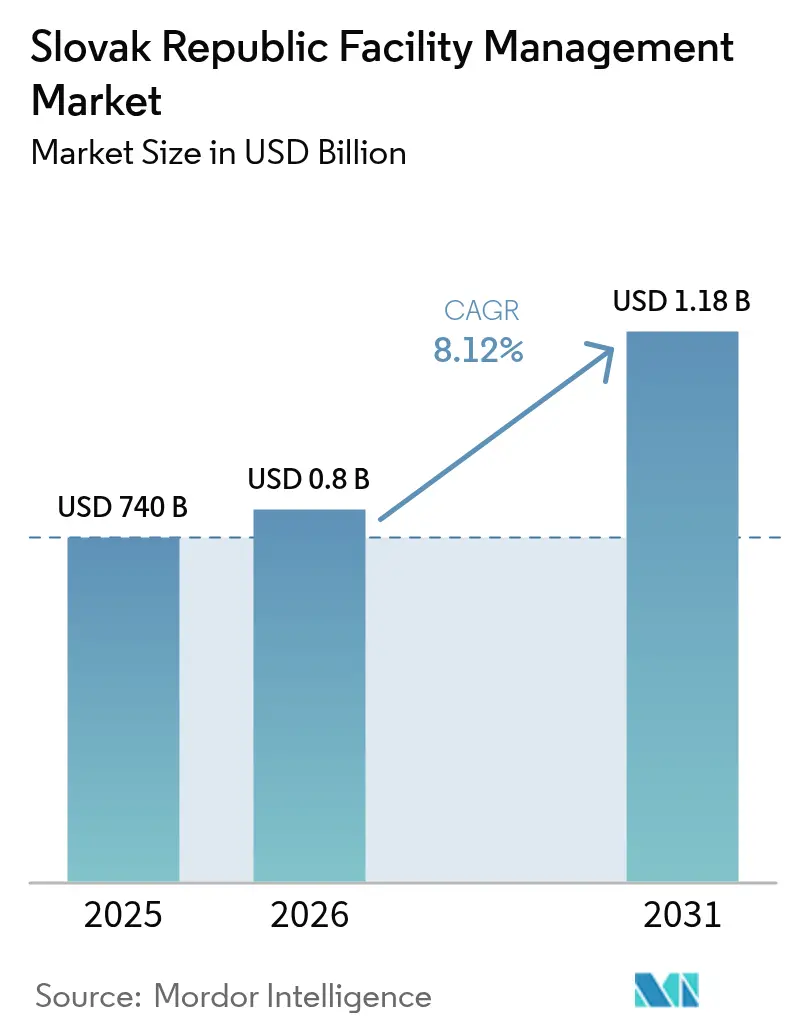

| Base Year Market Size (2025) | USD 740 Billion |

| Market Size (2026) | USD 0.8 Billion |

| Market Size (2031) | USD 1.18 Billion |

| Growth Rate (2026 - 2031) | 8.12% CAGR |

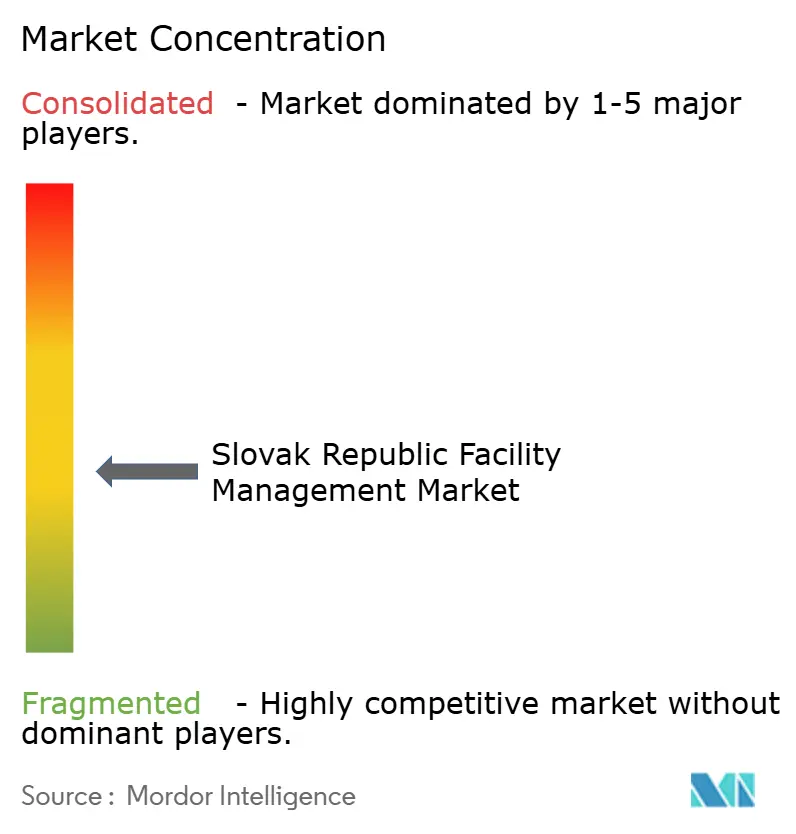

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Slovak Republic Facility Management Market Analysis by Mordor Intelligence

Slovakia facility management market size in 2026 is estimated at USD 800 million, growing from 2025 value of USD 740 million with 2031 projections showing USD 1.18 billion, growing at 8.12% CAGR over 2026-2031. Slovakia’s manufacturing-centric economy, rapid EU Recovery and Resilience Fund (RRF) deployment, and enforcement of the Energy Performance of Buildings Directive (EPBD) underpin this expansion. Battery and electronics plant construction in the western corridor, coupled with nationwide hospital, rail and education upgrades financed via roughly EUR 6 billion in RRF grants, enlarges the addressable base for technical and integrated service contracts.[1]Ministerstvo investícií SR, “Record EU-fund absorption,” mirri.gov.sk Rising ESG reporting—78% of large Slovak firms now publish sustainability data—pushes premium demand for green building bundles and AI-enabled predictive maintenance. Yet tight labour markets, concentrated in certified HVAC and electrical trades, and sustained Bratislava office vacancies temper immediate margin expansion.

Key Report Takeaways

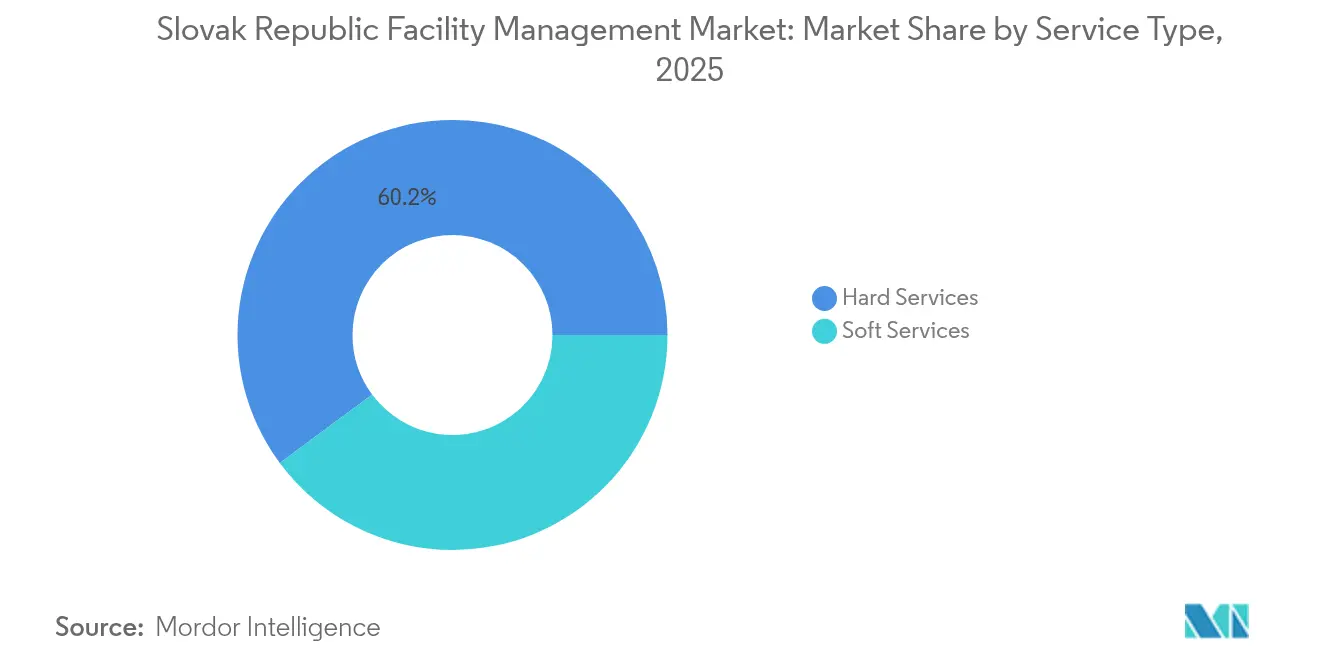

- By service type, Hard Services captured 60.15 % of the Slovakia facility management market share in 2025 while Soft Services advance at a 8.74 % CAGR through 2031.

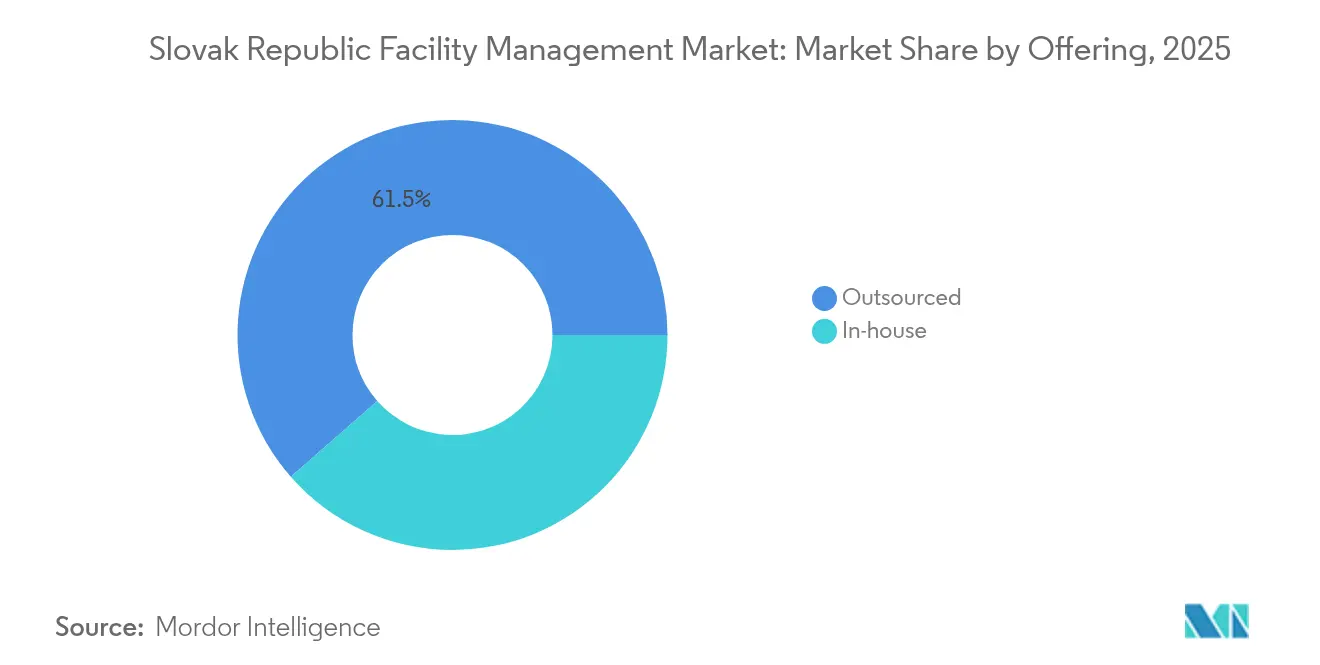

- By offering, the Outsourced model held 61.45 % of the Slovakia facility management market size in 2025 and is projected to grow at 8.35 % CAGR to 2031.

- By end-user, Commercial facilities led with 35.85 % revenue share in 2025; Institutional & Public Infrastructure is forecast to expand at an 8.42 % CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Slovak Republic Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| RRF-backed hospital, rail & education upgrades | +2.1% | National, Bratislava & regional hubs | Medium term (2-4 years) |

| Automotive, battery & electronics plant expansion | +1.8% | Western Slovakia | Short term (≤ 2 years) |

| EPBD-driven IoT/BMS & AI maintenance adoption | +1.4% | National | Long term (≥ 4 years) |

| ≥70% outsourcing penetration in Grade-A offices | +0.9% | Bratislava | Medium term (2-4 years) |

| ESG & green-certification demand | +1.2% | National | Medium term (2-4 years) |

| Retrofit of 700 k prefabricated residential blocks | +0.8% | Urban centres | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EU Recovery & Resilience Fund Infrastructure Modernization

Record-high EU fund absorption directs EUR 6 billion into Slovak hospital, rail and education projects through 2026, producing large multi-year technical FM contracts that replace fragmented commercial jobs. The Poprad-Tatry railway overhaul alone (EUR 369 million) demands logistics coordination, safety monitoring and commissioning services. [2]Korzár, “Poprad-Tatry rail modernisation,” korzar.sme.skIMF analysis confirms public-investment-led GDP support, reinforcing multi-segment demand. Providers able to bundle hard and soft disciplines with robust KPI tracking secure higher-margin, long-duration contracts.

Automotive Sector Battery Manufacturing Expansion

Hyundai Mobis (USD 257 million) and InoBat-Gotion (EUR 1 billion) anchor a battery cluster requiring cleanroom operations, hazardous-materials logistics and precision climate control. Output targets of 300 k EV power units and 240 k vehicle batteries annually necessitate 24/7 predictive maintenance, specialised fire suppression and energy-management protocols. Government incentives worth USD 28 million underline policy continuity, ensuring a stable pipeline of industrial FM opportunities.

EPBD Implementation and Smart Building Technology Integration

Slovakia adopted the EU EPBD in early 2024, mandating building system upgrades, minimum energy standards and EV-charging infrastructure. [3]Schoenherr, "The Impact of the Energy Performance of Buildings Directive on Cities and Municipalities," schoenherr.eu IoT-enabled BMS paired with AI analytics can cut office energy use by up to 37%. The government’s “Zelená domácnostiam” energy-voucher scheme exhausted EUR 47 million within months, signalling sizeable latent demand for smart-tech retrofits. FM firms offering turnkey audit-design-operate packages capture premium pricing.

ESG Compliance and Green Certification Demand

Mandatory sustainability disclosures under the Corporate Sustainability Reporting Directive elevate demand for carbon-tracking, renewable-sourcing and BREEAM/LEED compliance services. Banks in Central Europe now tie more than three-quarters of commercial real-estate lending decisions to external sustainability credentials, reshaping FM procurement norms. Integrated providers that deliver energy optimisation, waste-reduction and transparent ESG metrics enjoy higher renewal rates and fee uplifts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of certified HVAC, electrical & fire-safety technicians | -1.6% | National | Short term (≤ 2 years) |

| >14% office vacancy in Bratislava | -0.8% | Bratislava | Medium term (2-4 years) |

| Commoditised pricing trims mid-tier EBIT margins | -0.7% | National | Medium term (2-4 years) |

| Fragmented micro-vendor base | -0.5% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Technical Labour Shortage Crisis

EU-wide data list plumbers, electricians and HVAC engineers among the top shortage occupations, and Bratislava’s 2.3% unemployment masks acute skills gaps. [4]European Labour Authority, “EU Shortage Report,” ela.europa.euCedefop projects these imbalances persisting to 2035, elevating wage inflation and hindering service scalability. Providers are implementing apprenticeship pipelines and foreign-labour recruitment yet still operate below optimal capacity.

Bratislava Office Market Vacancy Pressures

Hybrid work adoption holds Bratislava office vacancy above 14%, compressing soft-FM volumes and favouring shorter, price-sensitive contracts. Investment reports note bid-ask spreads and muted transaction flows across European secondary cities, intensifying competition for a shrinking occupier base. FM firms must pivot toward logistics, life-science and mixed-use assets to offset lost cleaning and catering hours.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Technical Upgrades Sustain Hard-Service Leadership

Hard Services held a commanding 60.15 % Slovakia facility management market share in 2025, propelled by mandatory fire, HVAC and electrical system standards in industrial and public buildings. Compliance with the EPBD and stringent automotive cleanroom requirements keeps long-cycle maintenance contracts buoyant, anchoring the Slovakia facility management market size for technical disciplines to an 7.65 % CAGR through 2031. Soft Services, despite commoditisation, outpace overall growth at 8.74 % CAGR as Grade-A offices in Bratislava outsource security, reception and specialised cleaning aligned with ESG hygiene norms.

Digital convergence is blurring service silos: bundled energy management, waste optimisation and workplace-experience platforms encourage cross-sale from hard-service incumbents into soft-FM categories, smoothing revenue volatility and lifting blended margins above the sub-5 % sector average.

By Offering: Outsourcing Intensifies Across Public and Private Projects

The Outsourced model accounted for 61.45 % of the Slovakia facility management market size in 2025 and is forecast to expand at 8.35 % CAGR to 2031 as corporates and municipalities shift risk and capex to specialist partners. Integrated FM sits at the premium apex, commanding double-digit contract value growth via multi-site, multi-service bundles under unified KPIs. Single and Bundled FM remain gateways for SMEs and regional public bodies embarking on first-time outsourcing journeys.

In-house operations still cover 38.55 % of facilities, notably in energy and petrochemical plants where safety oversight is viewed as core. Yet budget-constrained ministries are piloting Public-Private Partnership FM models on new rail depots and hospitals, signalling further share gains for the outsourced cohort.

By End-User: Public Infrastructure Emerges as Fastest-Growth Node

Commercial real estate—retail, warehousing and hospitality—retained leadership with 35.85 % revenue share in 2025, reflecting Slovakia’s mid-European logistics role. Energy-efficient store retrofits and hotel pipeline recovery post-pandemic sustain demand but at a moderating pace.

Institutional & Public Infrastructure is set to grow at 8.42 % CAGR, catalysed by RRF-funded hospital overhauls, university dormitory modernisation and the EUR 369 million Poprad-Tatry rail upgrade. Industrial & Process sites gain from battery-plant capex and brownfield automotive expansions, while multi-housing and leisure complexes surface as niche, higher-margin pockets for community-oriented service providers.

Geography Analysis

Bratislava controls roughly 39.40 % of the Slovakia facility management market share in 2025, underpinned by the nation’s highest GDP per capita and dense inventory of Grade-A offices and government buildings. Premium ESG-linked contracts and multilingual workforce availability allow rate premiums relative to regional averages.

Western Slovakia records the quickest uptake—about 9.85 % CAGR—to 2031 as Novaky, Trnava and Nitra host automotive and battery megaprojects requiring continuous technical FM presence and advanced safety protocols. Central Slovakia grows steadily on the back of diversified manufacturing and logistics corridors, while Eastern regions leverage EU cohesion funding to retrofit schools, courts and regional hospitals, gradually narrowing service-quality gaps.

OECD labour data underscore disparities: Bratislava’s unemployment sits at 2.1% versus 10.7% in the East, shaping wage structures and vendor density. Providers tailoring cost-sensitive models for eastern municipalities—while deploying AI-driven monitoring centrally—can capture untapped public-sector volumes.

Competitive Landscape

The Slovakia facility management industry exhibits moderate fragmentation. Global majors ISS Facility Services, Sodexo Slovakia and ATALIAN Global Services secure multi-site industrial, finance and public-sector contracts by leveraging standardised processes and IoT platforms. Regional specialists Apleona HSG, Reiwag and ENGIE Services differentiate via deep technical certifications and local compliance fluency, especially in fire-safety and cleanroom management.

Technology is becoming the defining moat: leaders deploy digital twins, sensor-based condition monitoring and mobile workforce apps to reduce reactive callouts and enable performance-based pricing. Leadec’s circular-economy offering—encompassing waste-heat reuse and closed-loop coolant systems—illustrates ESG-led service diversification.

Margin pressure in soft-FM accelerates consolidation; smaller janitorial and security outfits unable to finance tech upgrades increasingly accept acquisition or subcontractor roles. Concurrently, rising public-sector outsourcing opens space for joint ventures that pair international capital strength with Slovak SMEs’ regional networks.

Slovak Republic Facility Management Industry Leaders

-

Apleona HSG s.r.o.

-

Reiwag Facility Services GmbH

-

OKIN FACILITY

-

BBS Facility Management s.r.o.

-

Danube Facility Services

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Gotion and InoBat broke ground on a EUR 1 billion EV battery plant, the largest single FM opportunity in Slovak industry history, requiring full-scope cleanroom and hazardous-materials management

- May 2025: The European Council ratified Slovakia’s amended RRF plan, securing EUR 6 billion for infrastructure upgrades through 2026, sustaining public-sector FM pipelines.

- March 2025: The IMF confirmed Slovakia’s GDP rebound to 2.0% in 2024, crediting high EU-fund absorption that bolsters FM demand.

- February 2025: The Finance Ministry projected 1.9% GDP growth for 2025, anchored by energy-efficient renovation projects crossing from planning to execution.

Slovak Republic Facility Management Market Report Scope

Facility management is an effective form of business management that provide relevant, cost-effective services to support the core business activities and allow them to optimize. The FM services are divided into hard facility management services and soft facility management services. Both in-house facility management and outsourced FM services are considered in the scope. The integrated facility management services (IFM) market and single and bundled services are included in the outsourced FM services segment.

The Slovak Republic facility management market is segmented by service type (hard services [asset management, MEP and HVAC services, fire systems and safety, and other hard FM services] and soft services [office support and security, cleaning services, catering services, and other soft FM services]), offering type (in-house and outsourced [single FM, bundled FM, and integrated FM]), and by end-user (commercial, hospitality, institutional & public infrastructure, healthcare, industrial & process sector, and others). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Hard Services | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard FM Services | |

| Soft Services | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft FM Services |

| In-house | |

| Outsourced | Single FM |

| Bundled FM | |

| Integrated FM |

| Commercial (IT and Telecom, Retail and Warehouses, etc.) |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) |

| Institutional and Public Infrastructure (Govt, Education, Transportation) |

| Healthcare (Public and Private Facilities) |

| Industrial and Process (Manufacturing, Energy, Mining) |

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) |

| By Service Type | Hard Services | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard FM Services | ||

| Soft Services | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft FM Services | ||

| By Offering Type | In-house | |

| Outsourced | Single FM | |

| Bundled FM | ||

| Integrated FM | ||

| By End-user Industry | Commercial (IT and Telecom, Retail and Warehouses, etc.) | |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) | ||

| Institutional and Public Infrastructure (Govt, Education, Transportation) | ||

| Healthcare (Public and Private Facilities) | ||

| Industrial and Process (Manufacturing, Energy, Mining) | ||

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) | ||

Key Questions Answered in the Report

What is the current value of the Slovak Republic facility management market?

The Slovak Republic facility management market size is USD 800 million in 2026.

How fast is the market expected to grow?

The market is forecast to expand at an 8.12% CAGR, reaching USD 1.18 billion by 2031.

Which service category dominates the market?

Hard Services lead with 60.15 % market share due to stringent technical and regulatory requirements in industrial and public buildings.

Why is outsourcing gaining traction in Slovak Republic?

Corporates and public bodies favour outsourced models to transfer risk, access specialised skills and meet EU compliance mandates, giving outsourced FM 61.45 % market share in 2025.

How does ESG regulation affect facility management providers?

Mandatory sustainability reporting and green-loan criteria incentivise integrated providers that can deliver energy optimisation, carbon tracking and certification support, unlocking premium pricing potential.

Page last updated on: